United States Healthcare Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

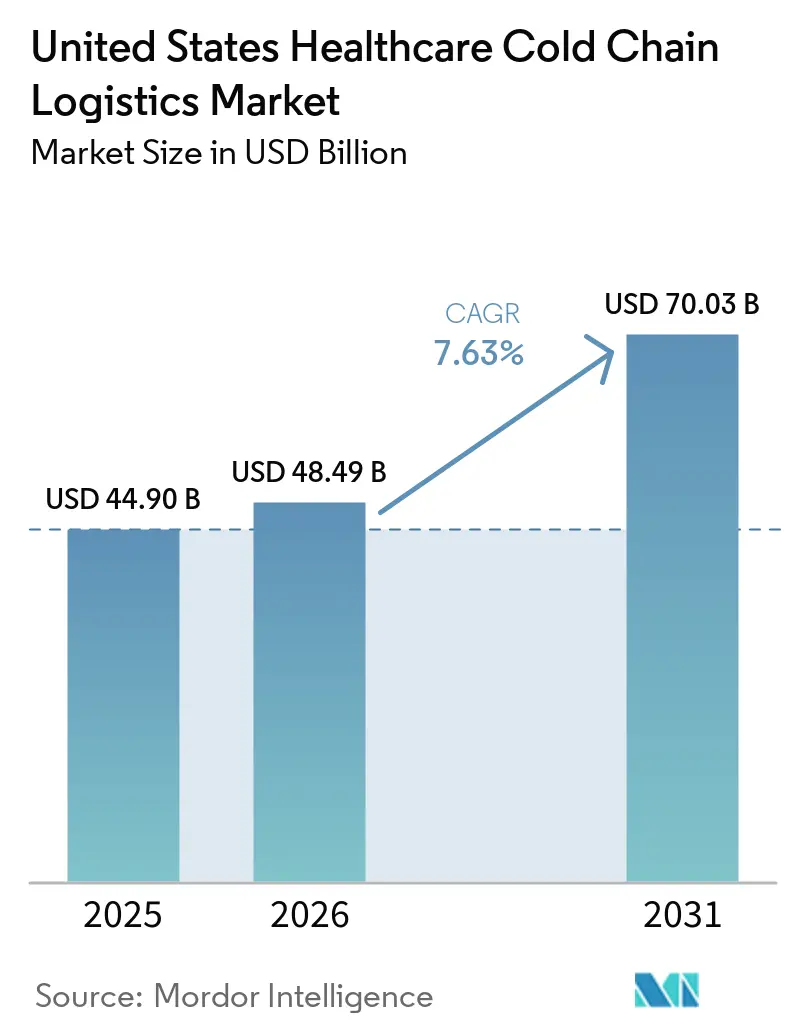

| Base Year Market Size (2025) | USD 44.90 Billion |

| Market Size (2026) | USD 48.49 Billion |

| Market Size (2031) | USD 70.03 Billion |

| Growth Rate (2026 - 2031) | 7.63% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Healthcare Cold Chain Logistics Market Analysis by Mordor Intelligence

The United States healthcare cold chain logistics market size was valued at USD 44.9 billion in 2025 and is estimated to grow from USD 48.49 billion in 2026 to reach USD 70.03 billion by 2031, at a CAGR of 7.63% during the forecast period (2026-2031).

The United States healthcare cold chain logistics market is supported by a broader biologics launch base, faster commercialization of cell and gene therapies, and a replenishment cycle for GLP-1 injectables that has increased the frequency of chilled deliveries across pharmacy and specialty networks. Demand is being shaped by structural changes rather than short-term swings, because domestic biologics manufacturing is expanding under supply resilience priorities, and newer therapies continue to favor temperature-sensitive large molecules over older small-molecule generics. Updated compliance expectations are also making cold-chain infrastructure harder to treat as an optional cost line, especially as route qualification, excursion review, and electronic traceability move deeper into daily operations across the distribution chain. The United States healthcare cold chain logistics market is also seeing a closer link between domestic production growth and route validation needs, which is lifting demand for monitoring platforms, specialist 3PL networks, and audit-ready data systems at the same time. Competition is separating into 2 layers, with UPS Healthcare, FedEx, and DHL adding scale through acquisitions and network investment, while specialist operators such as Cryoport Systems and Marken retain advantages in ultra-specialized lanes that broad generalists still struggle to serve efficiently.

Key Report Takeaways

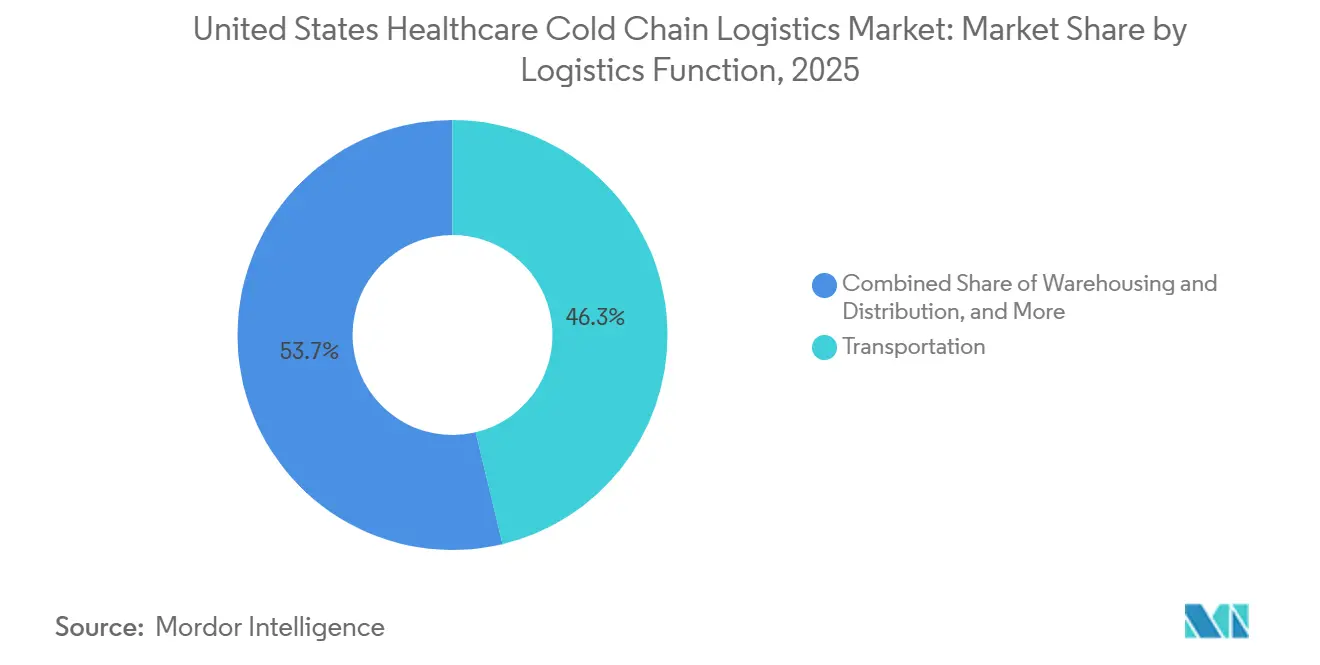

- By logistics function, transportation led with 46.25% share of the United States healthcare cold chain logistics market size 2025, while value-added services are projected to expand at an 8.38% CAGR through 2031.

- By temperature type, ambient handling accounted for 46.62% of the United States healthcare cold chain logistics market share in 2025, while deep-frozen and ultra-low temperature bands are forecast to grow at an 11.55% CAGR through 2031.

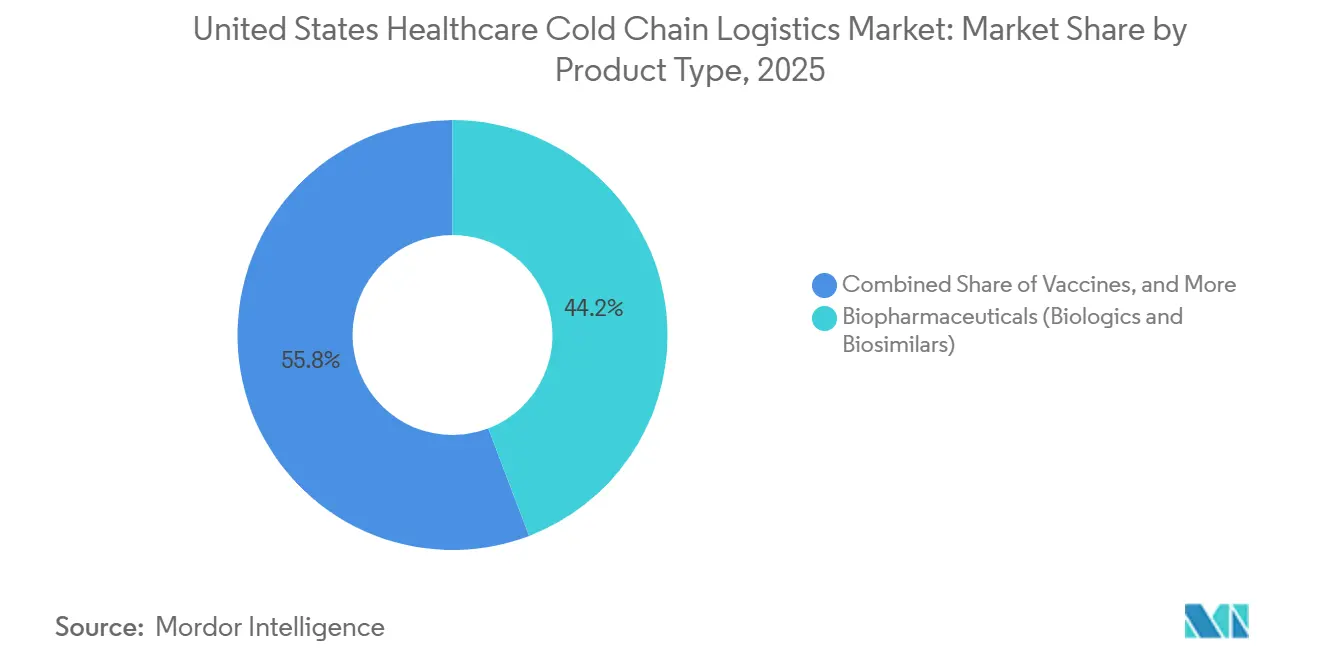

- By product type, biopharmaceuticals held 44.2% of the United States healthcare cold chain logistics market share in 2025, while cell and gene therapies are projected to record the fastest CAGR at 13.69% through 2031.

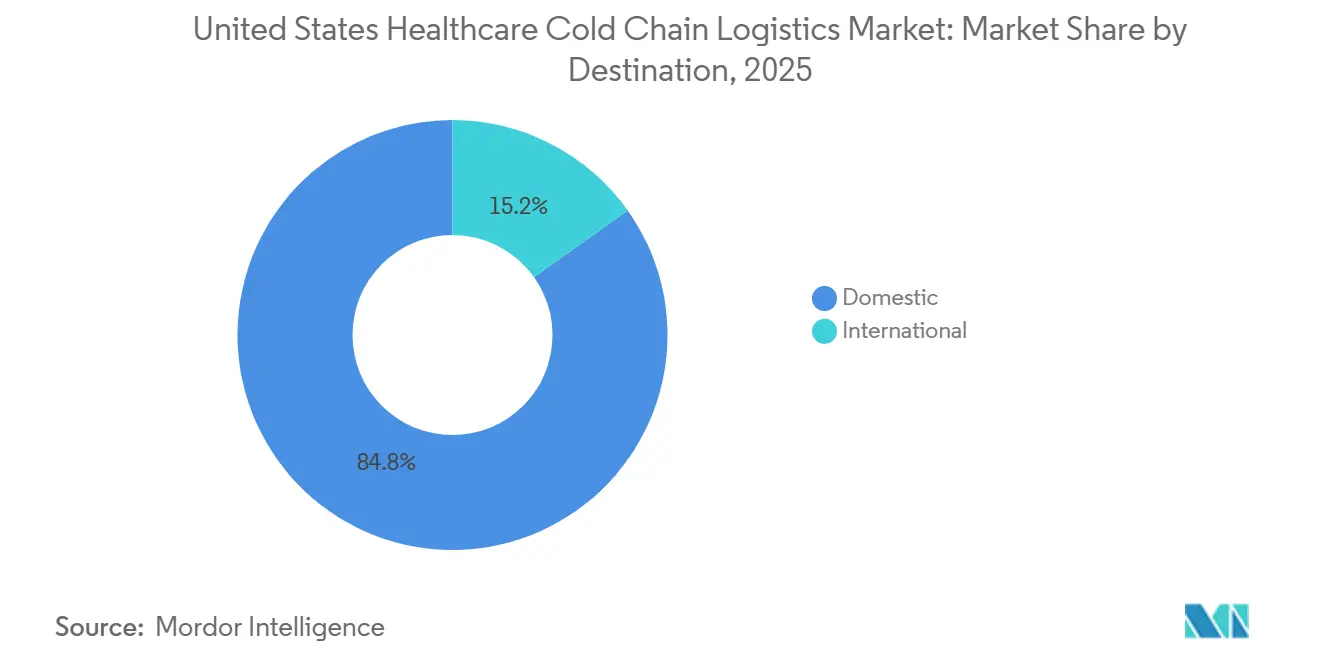

- By destination, domestic flows represented 84.84% of the United States healthcare cold chain logistics market size in 2025, while international lanes are forecast to advance at an 8.69% CAGR through 2031.

- By end user, pharmaceutical manufacturers held 56.2% of the United States healthcare cold chain logistics market share in 2025, while biopharmaceutical manufacturers are forecast to grow at an 8.27% CAGR through 2031.

- By geography, the Northeast captured 26.84% of the United States healthcare cold chain logistics market size in 2025, while the Southwest is projected to expand at an 8.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Healthcare Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Biologics and Specialty-Pharma Cold-Chain Demand | +1.8% | National, concentrated in Northeast and Midwest pharma corridors | Long term (≥ 4 years) |

| Cell and Gene Therapy Commercialization | +1.5% | National, with early concentration in Boston-Philadelphia biotech corridors | Long term (≥ 4 years) |

| Outsourcing to Specialist 3PLs and Digital Visibility Stacks | +1.0% | National | Medium term (2-4 years) |

| Vaccine, Plasma, and Other High-Integrity Temperature-Sensitive Flows | +0.7% | National, high intensity in Southeast and Midwest distribution hubs | Medium term (2-4 years) |

| Home Infusion and Specialty-Pharmacy Direct-To-Patient Fulfillment | +0.8% | National, highest density in suburban Northeast and Southeast | Medium term (2-4 years) |

| GLP-1 Injectable Replenishment Intensity and Tighter Cold-Chain Turns | +1.2% | National, highest velocity in Southwest and West Coast pharmacy networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Biologics and Specialty-Pharma Cold-Chain Demand

The United States healthcare cold chain logistics market is absorbing a biologics pipeline that is larger and more temperature sensitive than the system built for traditional drug distribution. Cencora said in November 2025 that half of all products launched globally through 2027 would require cold-chain storage, up from 37% during 2013 to 2017, and paired that view with a USD 1 billion plan to expand its United States distribution network. That shift matters because oncology injectables, immunologics, and similar specialty products depend on validated 2 °C to 8 °C lanes with continuous monitoring, which raises the value of premium operators over general freight providers. Biosimilar approvals are also adding more handling intensity than many buyers first expected, because new parallel SKUs often need the same refrigerated treatment as the originator products they compete against. FDA storage and distribution expectations under 21 CFR Part 211 tie temperature control to product quality throughout the journey rather than only at the factory gate[1]“Temperature Monitoring Regulatory Update — June 2026,” Temperature Indicators Ltd, temperature-indicators.co.uk. In practice, that makes compliance-grade cold-chain capability a core service line in the United States healthcare cold-chain logistics market rather than a back-end support function.

Cell and Gene Therapy Commercialization

The United States healthcare cold chain logistics market is being pushed into a very different operating model by cell and gene therapies, because many of these shipments are patient-specific and time-critical. Unlike conventional batch drugs, many autologous therapies are one-of-one products that move between collection centers, manufacturers, and treatment sites, so a failed delivery can erase both clinical and commercial value. Required temperature conditions often fall between -70 °C and -150 °C, which exceed the limits of standard pharmaceutical buildings and increase demand for modular medical cryogenic setups where permanent capacity is not yet available. DHL recognized this shift in 2025 when it acquired CryoPDP, a specialist in clinical-trial and cell and gene therapy logistics, and SDS Rx, which added a large United States final-mile footprint with more than 200 locations. As treatment access spreads beyond a small set of elite academic centers, the United States healthcare cold chain logistics market must extend ultra-cold reach to hospitals that have limited cryogenic experience. That expansion remains one of the clearest operating gaps across secondary United States markets.

Outsourcing to Specialist 3PLs and Digital Visibility Stacks

The United States healthcare cold chain logistics market is seeing more manufacturers hand logistics complexity to specialist 3PLs because portfolio requirements now move faster than internal distribution teams can adapt. EVERSANA expanded that specialist model in April 2025 with a 358,000 square feet cGDP-certified distribution center in Memphis, Tennessee, more than doubling cold-chain storage capacity and adding AI-enabled robotic fulfillment. The outsourcing decision is not only about labor or building costs, because manufacturers increasingly want one platform that combines IoT temperature sensing, exception management, serialization support, and an audit-ready record. DSCSA interoperability requirements have reinforced this shift by raising the minimum standard for data integrity across the wholesale and dispensing chain[2]“Drug Supply Chain Security Act (DSCSA),” U.S. Food and Drug Administration, fda.gov. Providers that can integrate channel management, temperature control, and digital traceability into a single system are winning a larger share of new product launches. That pattern is making digital visibility a direct commercial differentiator in the United States healthcare cold chain logistics market.

Vaccine, Plasma, and Other High-Integrity Temperature-Sensitive Flows

The United States healthcare cold chain logistics market still relies on vaccine and plasma logistics as a base load that keeps network utilization steady, even before higher-value specialty volumes are added. CDC guidance requires continuous vaccine cold-chain control from manufacturing storage through transport to the provider site, and any out-of-range reading can trigger investigation and possible write-off. McKesson’s role as the CDC vaccine distribution contractor shows how government-linked cold-chain contracts create recurring revenue streams that are difficult for smaller rivals to access. Blood and plasma flows add another layer of operating rigor because they require tight temperature control and compatibility tracking across multiple handoff points. Together, these flows give operators a refrigerated utilization floor that helps recover fixed costs before premium biologics or trial shipments enter the network. That base is one reason scale still matters in the United States healthcare cold chain logistics market, even as newer specialty segments grow faster.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex, Energy, and Validation Costs | -1.4% | National | Long term (≥ 4 years) |

| Skilled-Labor Shortages and Temperature-Excursion Risk | -0.9% | National, acute in Southwest and Southeast expansion markets | Medium term (2-4 years) |

| USP Route Qualification and Data-Integrity Burden | -0.7% | National | Long term (≥ 4 years) |

| Site-of-Care Cryogenic Readiness Gaps for Advanced Therapies | -0.8% | National, highest gap outside Northeast and Mid-Atlantic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex, Energy, and Validation Costs

The United States healthcare cold chain logistics market remains constrained by the high cost of building compliant ultra-cold capacity. Cryogenic storage that operates at -80 °C to -150 °C requires specialized mechanical systems, backup power, and continuous monitoring, and the estimates indicate that facility construction costs can run 30% to 50% above standard cold storage costs. Operating costs are also higher because deep-freezing and ultra-low zones can cost 3 to 5 times as much per pallet as refrigerated storage. Qualification expectations under FDA good manufacturing practice rules and USP General Chapter 1079.4 add another layer, since each site must complete temperature mapping and performance qualification before commercial handling begins[3]“General Chapter <1079.4> Temperature Mapping for the Qualification of Storage Areas,” United States Pharmacopeia, usp.org. That often creates a 12- to 24-month gap between capital commitment and revenue generation, narrowing the field to operators with stronger balance sheets. This cost barrier keeps supply tight in the United States healthcare cold chain logistics market, even while it protects pricing power for established providers.

Skilled-Labor Shortages and Temperature-Excursion Risk

The United States healthcare cold chain logistics market also faces a workforce challenge, because regulated cold-chain operations require people who understand validation, quality systems, and excursion review. Needed roles include validation engineers, regulatory staff, chain-of-custody specialists, and temperature-excursion investigators, and supply has not kept up with the pace of network expansion. The revised USP General Chapter 1079.2, effective August 1, 2025, tightened excursion evaluation rules, clarified documentation expectations, and warned against the misuse of mean kinetic temperature in excursion management. That means every deviation now demands a more formal review process, which can slow throughput when staffing depth is weak. The labor gap and excursion risk reinforce each other because weaker training raises the chance of handling mistakes, and every deviation consumes scarce technical time. Providers that pair structured training with AI-led exception management are turning that gap into a commercial premium inside the United States healthcare cold chain logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Transportation Anchors Volume While Value-Added Services Lead Growth

Transportation accounted for 46.25% of the United States healthcare cold chain logistics market size by logistics function in 2025, making it the largest functional pool in the category. Road freight held the leading position within transportation because daily pharmaceutical replenishment still depends on dense truck networks and temperature-controlled lanes serving wholesalers, pharmacies, and specialty distributors. Air freight generated the highest revenue per shipment within transportation because time-sensitive biologics and cell and gene therapy movements still require premium speed and handling discipline. Sea and inland waterway transport remained a small part of healthcare cold-chain value, mostly tied to bulk plasma proteins and bulk drug substance flows moving between coastal manufacturing sites and distribution hubs. Rail also began to show practical relevance on selected corridors, especially after J.B. Hunt launched an intermodal refrigerated service in 2025 between Monterrey, Mexico, and Pennsylvania for non-inspection-required temperature-sensitive commodities.

Value-added services are forecast to expand at an 8.38% CAGR through 2031, which makes them the fastest-growing functional segment in the United States healthcare cold chain logistics market. Growth is coming from secondary packaging, kitting, serialization support, clinical hold management, and returns processing, all of which are becoming billable services rather than bundled support tasks. Warehousing and distribution remains the second-largest function because specialty drug portfolios now require refrigerated, frozen, and controlled room-temperature zones inside the same building. The more important change is qualitative, because operators are no longer selling only square footage and cooling capacity. In the United States healthcare cold chain logistics industry, warehousing is shifting toward an information-rich service where real-time inventory visibility, audit-ready records, and predictive stock management help decide pricing and customer retention.

By Temperature Type: Ambient Dominates Volumes but Ultra-Cold Is the New Growth Engine

Ambient handling held 46.62% of the United States healthcare cold chain logistics market share by temperature type in 2025, which shows that the healthcare cold chain in the United States still spans more than refrigerated biologics alone. A large share of volume includes OTC products, controlled room-temperature therapies, and oral formulations that move in tightly managed ambient settings instead of chilled environments. Chilled 0 °C to 5 °C and frozen -18 °C to 0 °C bands formed the next tier, supported by vaccines, plasma proteins, and traditional specialty-drug traffic. This mix explains why the United States healthcare cold chain logistics market continues to depend on flexible multi-temperature infrastructure rather than a single cold profile. It also shows why network design must support both high-volume replenishment and high-integrity specialty movements at the same time.

Deep-frozen and ultra-low bands below -20 °C are projected to grow at an 11.55% CAGR through 2031, the fastest pace among temperature types in the United States healthcare cold chain logistics market. That growth reflects the commercialization wave in cell and gene therapy, where product integrity often depends on conditions far below the range used for traditional biologics. Part of the acceleration comes from a low historical base, but the underlying direction is still structural because more approved advanced therapies are entering commercial distribution. Cryoport’s first quarter 2026 results and its planned fourth quarter 2026 opening of a Global Supply Chain Center in Santa Ana, California, show that infrastructure providers are scaling ultra-cold capacity before demand fully lands. The United States healthcare cold chain logistics market size for ultra-low lanes remains smaller than ambient and chilled categories today, but it is becoming one of the most strategically important pockets of future expansion.

By Product Type: Biopharmaceuticals Command Share as CGTs Define the Frontier

Biopharmaceuticals held 44.2% of the United States healthcare cold chain logistics market size by product type in 2025, making them the largest product segment in the market. That position reflects the commercial scale of monoclonal antibodies, fusion proteins, recombinant hormones, and biosimilars that now anchor specialty formularies across major payer and provider channels. Pharmaceuticals, as a broader category, remained the second-largest segment, but their cold-chain intensity per unit stayed lower than that of biopharmaceuticals. Vaccines, clinical trial materials, medical devices, veterinary medicine, blood and plasma, diagnostic products, and related categories together showed how broad the service mix has become. The result is that the United States healthcare cold chain logistics market is no longer defined by a narrow biologics niche, even though biopharmaceuticals set the baseline demand profile.

Cell and gene therapies are forecast to expand at a 13.69% CAGR through 2031, which makes them the fastest-growing product category by a wide margin. Thermo Fisher Scientific strengthened this advanced-therapy ecosystem in April 2026 by opening a 290,000 square feet bioprocess design center in Plainville, Massachusetts, with 4,000 square feet of biologics laboratory and training space. That move points to a closer physical link between upstream bioproduction and downstream cold-chain execution, especially where time-to-patient matters[4]“Thermo Fisher Scientific Opens U.S. Flagship Bioprocess Design Center to Accelerate the Delivery of Life-changing Therapies,” BusinessWire, businesswire.com. Organs and human tissues remain small by volume, but they still command the highest urgency per shipment because any logistics failure is irreversible. In the United States healthcare cold chain logistics industry, those premium urgency lanes continue to favor operators with dedicated medical courier systems and strict chain-of-custody controls.

By Destination: Domestic Flows Dominate but International Corridors Accelerate

Domestic flows accounted for 84.84% of the United States healthcare cold chain logistics market share by destination in 2025, confirming that the market is still primarily built around internal production and consumption. The United States remains both the largest pharmaceutical consumer and a major domestic manufacturer, which naturally creates a broad national distribution system. Domestic dominance is also reinforced by the practical benefits of DSCSA visibility, because internal lanes are easier to monitor and standardize than more complex international chains. The Midwest and Northeast remain key hub-and-spoke anchors, with Chicago, Indianapolis, and the Philadelphia-New Jersey corridor supporting next-day pharmaceutical reach across much of the continental United States. This network density gives the United States healthcare cold chain logistics market a strong home-based structure even as cross-border demand rises.

International flows are projected to grow at an 8.69% CAGR through 2031, which places them above the overall growth rate. Export growth from United States-based contract manufacturing and a busier pharmaceutical trade lane with Mexico are the main reasons this segment is advancing faster. Port Laredo in Texas handles around 8,000 trailers daily in cross-border cold-chain trade and serves as the main land gateway for temperature-sensitive flows between Mexico and the United States. DHL added more transatlantic support in February 2026 when it activated a dedicated Boeing 777 freighter operating 6 days per week between Brussels and Cincinnati. That kind of dedicated capacity suggests the United States healthcare cold chain logistics market size tied to international lanes will keep gaining strategic importance even if domestic flows remain dominant.

By End User: Pharma Manufacturers Lead Revenue Base as Biopharma Outpaces the Field

Pharmaceutical manufacturers held 56.2% of the United States healthcare cold chain logistics market share by end user in 2025, which gave them the largest revenue base across the market. Their lead reflects the fact that most temperature-sensitive product volume still originates with manufacturers that rely on wholesale and distribution partners to move it across national networks. This structure is visible in large embedded service relationships where companies such as McKesson and Cardinal Health combine distribution activity with cold-chain handling. Cardinal Health reinforced that large-volume manufacturer model in September 2025 by announcing a new flagship forward distribution center in Indianapolis with a robotic storage and retrieval system designed to keep employees outside refrigerated zones.

Biopharmaceutical manufacturers are forecast to grow at an 8.27% CAGR through 2031, the fastest pace among end-user cohorts in the United States healthcare cold chain logistics market. Their growth reflects a shift toward more proprietary distribution programs that can deliver deeper temperature visibility and tighter control than bundled wholesale models often provide. Hospitals and clinics, hospitals and retail pharmacies, and healthcare distributors and wholesalers remain important demand pools, but each group is shaped by a different balance between patient proximity and logistics complexity. Competitive tension is rising between specialty pharmacy chains and hospital outpatient dispensing programs because reliable cold-chain execution is now influencing formulary access and manufacturer relationships. That dynamic keeps the United States healthcare cold chain logistics market closely tied to changes in care setting, channel control, and product complexity rather than simple shipment volume alone.

Geography Analysis

The Northeast accounted for 26.84% of the United States healthcare cold chain logistics market share in 2025, making it the largest regional cluster. Its lead stems from the high concentration of pharmaceutical manufacturing, R&D activity, academic medical centers, and specialty pharmacies across New Jersey, Pennsylvania, and Massachusetts. This regional density creates a self-reinforcing system where manufacturing sites, treatment centers, and high-value distribution routes remain physically close to one another. Newark Liberty International Airport and Philadelphia International Airport also strengthen the region by serving as air gateways for imported active ingredients and exported finished products. That makes the Northeast more than a domestic demand center, because it also connects the United States healthcare cold chain logistics market to global pharmaceutical traffic.

The Southeast benefits from major distribution investments that continue to improve network depth and route flexibility. EVERSANA’s Memphis site, opened in 2025, added 358,000 square feet of cGDP-certified capacity and more than doubled the company’s cold-chain storage footprint. The Midwest remains a strategic crossroads, and GEODIS reinforced that role in April 2026 by opening a 78,000 square feet healthcare cold-chain cross-dock at Chicago O’Hare with 5,200 square feet of temperature-controlled zones. Kuehne+Nagel extended that Midwest role further in June 2026 through a weekly Chicago-to-Frankfurt routing on its own-controlled air freight network. On the West Coast, California’s Bay Area and San Diego continue to support dense specialty-drug dispensing and clinical-trial activity that keeps premium air capacity well utilized.

The Southwest is forecast to grow at an 8.93% CAGR through 2031, the fastest pace among the United States regions in the market. Growth is being supported by near-shore pharmaceutical flows through the Texas-Mexico border corridor, stronger GLP-1 dispensing intensity in large population centers, and greenfield investment in Arizona and Texas. Port Laredo remains central to that story because it functions as the main land-based cold-chain node for North American pharmaceutical commerce. Cryoport’s planned fourth quarter 2026 opening of a Global Supply Chain Center in Santa Ana will also give the West a stronger advanced-therapy anchor as California clinical programs continue to scale.

Competitive Landscape

The United States healthcare cold chain logistics market is moderately concentrated at the top, but it remains fragmented across mid-market and specialty niches where more than 20 identified operators still compete. UPS Healthcare, FedEx, and DHL continue to hold the strongest positions in large-scale air freight and national ground coverage because they can fund networks that smaller rivals cannot match. UPS strengthened that scale model in 2025 through its USD 1.6 billion acquisition of Andlauer Healthcare Group, which added specialized cold-chain transportation and 3PL capabilities across North America. DHL used a similar expansion path by acquiring CryoPDP and SDS Rx in 2025, adding specialist cell and gene therapy capabilities and a final-mile healthcare footprint with more than 200 United States locations. FedEx took a different route, reporting USD 400 million in new annualized healthcare logistics revenue in 2025 and securing IATA CEIV Pharma corporate certification across its global hubs and ramps.

Integrated distributors such as Cencora, McKesson, and Cardinal Health occupy another important tier in the United States healthcare cold chain logistics market because they sit close to originating shippers and embedded wholesale contracts. That position gives them strong end-user access, but pure-play specialists still pressure them in complex biologics and advanced-therapy lanes where visibility and excursion performance matter more than scale alone. Cryoport Systems and Marken remain relevant examples of this specialist edge because ultra-specialized transport and clinical logistics are difficult for broad generalists to standardize at the same service level. The next white space appears to sit where cryogenic site support meets data services, because no single operator clearly dominates cryogenic installation, site readiness assessment, staff training, and real-time cell and gene therapy chain-of-custody on one managed platform. Providers that can combine those pieces may gain an outsized position as treatment centers expand beyond a few leading biotech hubs.

Technology-led visibility specialists are also shaping competition by pairing physical logistics with IoT monitoring, predictive exception management, and blockchain-style chain-of-custody tools. These tools are especially relevant for mid-sized operators that cannot fund a fully proprietary digital stack but still need audit-grade performance. Certification has become another practical filter in air freight access, because IATA’s CEIV Pharma framework is now held by UPS Healthcare, FedEx, and Kuehne+Nagel at a scale that matters for major pharmaceutical tenders. Smaller providers without that compliance credential are more likely to be left out of regulated tenders even when they can compete on lane price. This keeps the United States healthcare cold chain logistics market open to specialists, but it also raises the entry bar for anyone trying to move from niche coverage into national regulated scale.

United States Healthcare Cold Chain Logistics Industry Leaders

-

United Parcel Service of America, Inc. (UPS)

-

FedEx

-

DHL Group

-

Cencora

-

McKesson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Kuehne+Nagel activated a weekly Chicago-to-Frankfurt routing as part of its Inspire own-controlled aircraft network, effective June 2026, directly linking 2 major pharmaceutical distribution hubs across the Atlantic and supporting time-sensitive healthcare shipments with controlled capacity and frequency.

- April 2026: Thermo Fisher Scientific opened its United States Flagship Bioprocess Design Center in Plainville, Massachusetts, a 290,000 square feet integrated facility, adding 4,000 square feet of biologics laboratory and training space designed to support end-to-end bioproduction of vaccines and CGTs, accelerating the co-location of manufacturing and cold-chain logistics for advanced therapies.

- April 2026: GEODIS unveiled the Americas' first dedicated healthcare cold-chain cross-dock facility in Chicago, Illinois, a 78,000 square feet Container Freight Station with 5,200 square feet of temperature-controlled zones at O'Hare International Airport, exclusively serving pharmaceutical air and ocean imports and exports across GEODIS's 170-country network.

- February 2026: DHL Group activated a dedicated Boeing 777 freighter operating 6 days per week between Brussels, BRU, and Cincinnati, CVG, as part of its EUR 2 billion (USD 2.2 billion) DHL Health Logistics investment, providing a GDP-compliant end-to-end cold chain between Europe's leading pharma gateway and a growing United States life sciences hub.

United States Healthcare Cold Chain Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Chilled (0-5 °C) |

| Frozen (-18-0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | |

| Biopharmaceuticals (Biologics and Biosimilars) | |

| Vaccines | |

| Clinical Trial Materials | |

| Cell and Gene Therapies | |

| Medical Devices | |

| Veterinary Medicine | |

| Blood, Plasma and Blood Components | |

| Diagnostic and Laboratory Products | |

| Organs and Human Tissues | |

| Others |

| Domestics |

| International |

| Pharmaceutical Manufacturers |

| Biopharmaceutical Manufacturers |

| Hospitals and Clinics |

| Hospitals and Retail Pharmacies |

| Healthcare Distributors and Wholesalers |

| Others |

| Northeast |

| Southeast |

| Midwest |

| Southwest |

| West |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Type | Chilled (0-5 °C) | |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Product Type | Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | ||

| Biopharmaceuticals (Biologics and Biosimilars) | ||

| Vaccines | ||

| Clinical Trial Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices | ||

| Veterinary Medicine | ||

| Blood, Plasma and Blood Components | ||

| Diagnostic and Laboratory Products | ||

| Organs and Human Tissues | ||

| Others | ||

| By Destination | Domestics | |

| International | ||

| By End User | Pharmaceutical Manufacturers | |

| Biopharmaceutical Manufacturers | ||

| Hospitals and Clinics | ||

| Hospitals and Retail Pharmacies | ||

| Healthcare Distributors and Wholesalers | ||

| Others | ||

| By Region | Northeast | |

| Southeast | ||

| Midwest | ||

| Southwest | ||

| West | ||

Key Questions Answered in the Report

What is driving growth in the United States healthcare cold chain logistics through 2031?

Growth is being supported by biologics expansion, cell and gene therapy commercialization, GLP-1 injectable replenishment, domestic manufacturing re-onshoring, and tighter compliance requirements. The sector is projected to rise from USD 48.49 billion in 2026 to USD 70.03 billion by 2031 at a 7.63% CAGR.

Which logistics function is the largest today?

Transportation is the largest function, holding 46.25% of total revenue in 2025. Its lead is supported by daily road-based replenishment and premium air freight for time-sensitive biologics and advanced therapies.

Which temperature band is growing the fastest in the United States healthcare cold chain logistics space?

Deep-frozen and ultra-low segments below -20 °C are expected to post the fastest growth, with an 11.55% CAGR through 2031. That pace is closely tied to the commercial scaling of cell and gene therapies.

Why are domestic flows still much larger than international lanes?

Domestic flows held 84.84% of total activity in 2025 because the United States is both a large pharmaceutical producer and the largest end market. International corridors are still growing faster at 8.69% CAGR, led by export growth and cross-border trade with Mexico.

Which end users matter most for service providers?

Pharmaceutical manufacturers remained the largest end-user group with 56.20% share in 2025, while biopharmaceutical manufacturers are the fastest-growing cohort at an 8.27% CAGR. This mix reflects the increasing weight of specialty and large-molecule therapies in distribution demand.

What is the biggest operational challenge for advanced therapy logistics providers?

The key challenge is not only transport capacity, but also site-of-care readiness. Many hospitals outside major biotech clusters still need cryogenic equipment, trained staff, and formal receiving protocols before they can handle advanced therapies at scale.

Page last updated on: