Bio-Pharma Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

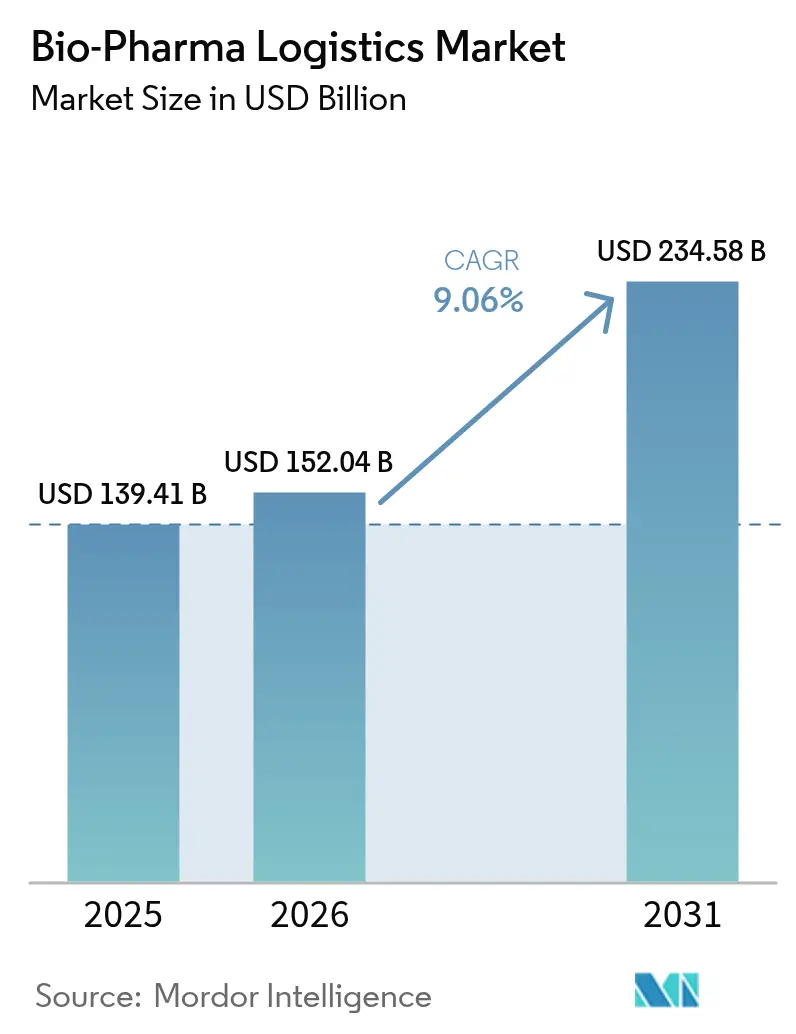

| Market Size (2026) | USD 152.04 Billion |

| Market Size (2031) | USD 234.58 Billion |

| Growth Rate (2026 - 2031) | 9.06% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio-Pharma Logistics Market Analysis by Mordor Intelligence

The Bio-Pharma Logistics Market size was valued at USD 139.41 billion in 2025 and estimated to grow from USD 152.04 billion in 2026 to reach USD 234.58 billion by 2031, at a CAGR of 9.06% during the forecast period (2026-2031). The growth reflects an industry pivot from conventional bulk drug distribution toward highly specialized, temperature-controlled networks engineered for advanced biologics, mRNA vaccines, and personalized cell & gene therapies. Scaling requirements for ultra-low-temperature shipping (down to −150 °C) are reshaping service portfolios, pushing providers to expand liquid-nitrogen capacity and real-time monitoring. Heightened regulatory scrutiny—exemplified by the European Medicines Agency’s decision to discontinue blanket GDP certificate extensions—also amplifies demand for certified third-party logistics partners. Parallel sustainability pressures spur investments in reusable packaging, route optimization, and electrified fleets as shippers aim to curb supply-chain emissions that account for more than 80% of industry carbon output.

Key Report Takeaways

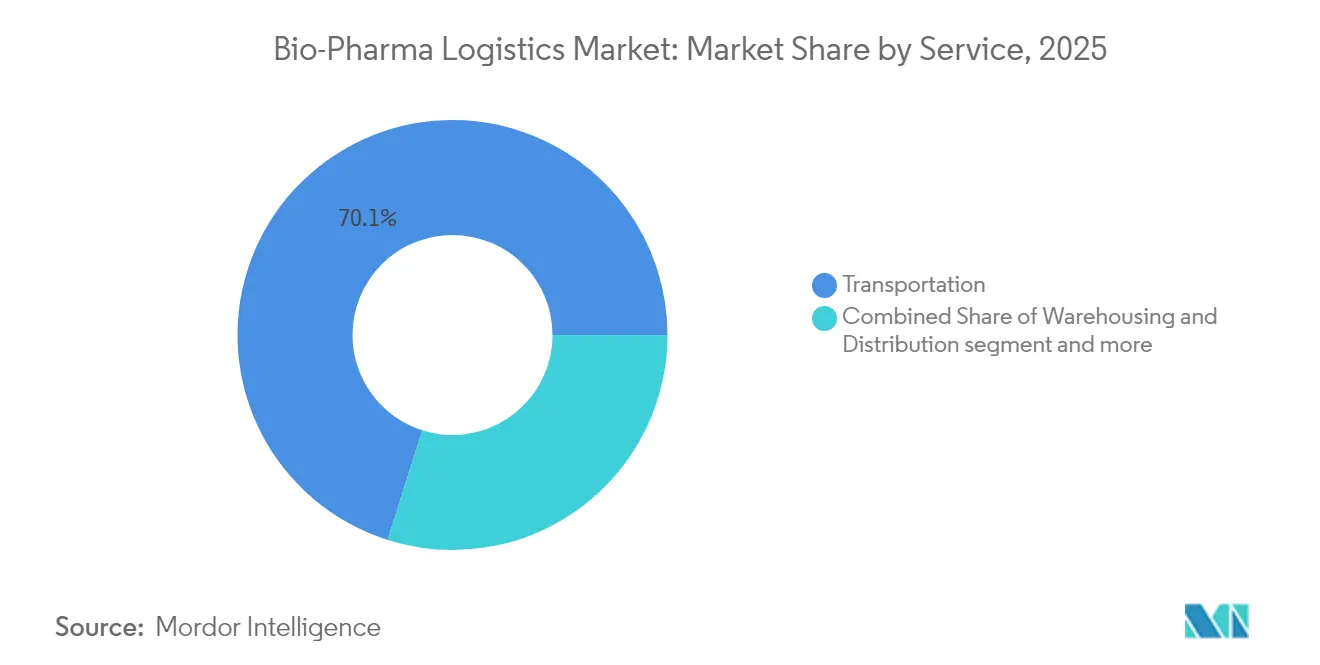

- By service, transportation held 70.12% of the biopharma logistics market share in 2025. The bio-pharma logistics market for value-added services is forecast to outpace the market with a 10.77% CAGR between 2026 and 2031.

- By temperature range, cold chain commanded 68.40% of the biopharma logistics market size in 2025. The bio-pharma logistics market for cold chain is advancing at a 10.49% CAGR between 2026 and 2031.

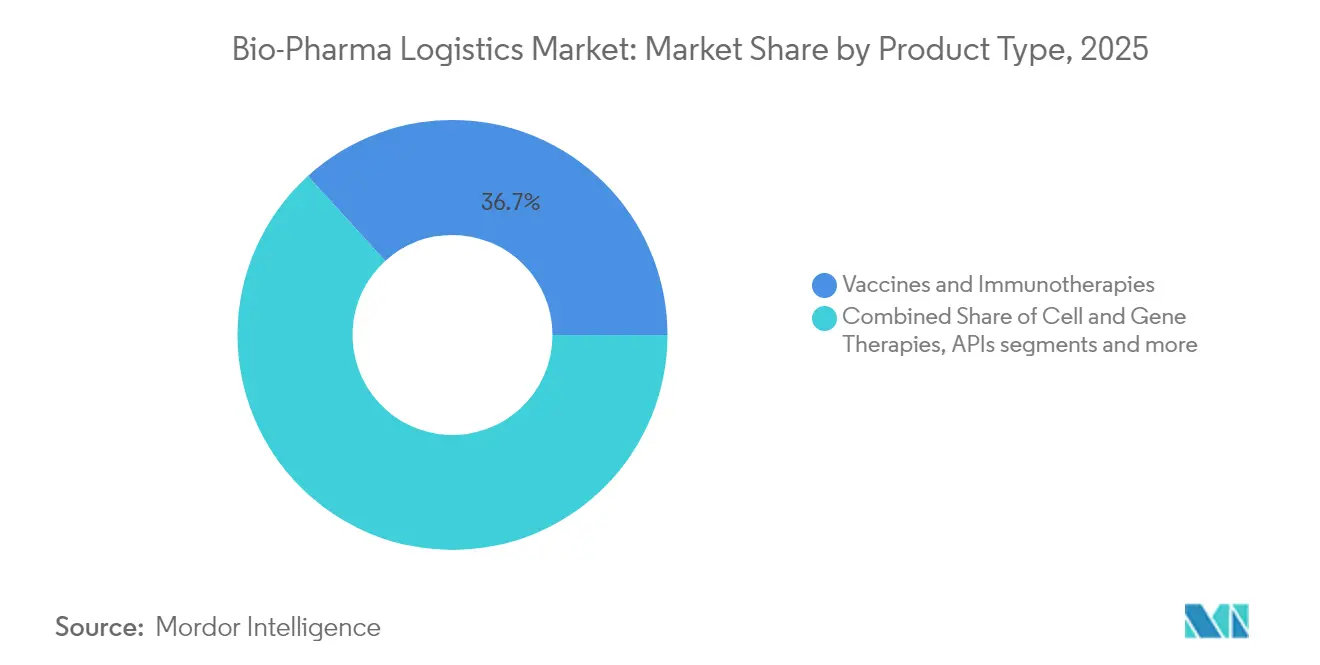

- By product type, vaccines and immunotherapies led with 36.74% of the biopharma logistics market revenue share in 2025. The bio-pharma logistics market for cell & gene therapies exhibits the fastest trajectory at 13.05% CAGR between 2026 and 2031.

- By end-user, bio-pharma manufacturers captured 58.10% of the bio-pharma logistics market share in 2025. The bio-pharma logistics market for CROs/CMOs records the highest projected CAGR at 12.02% between 2026 and 2031.

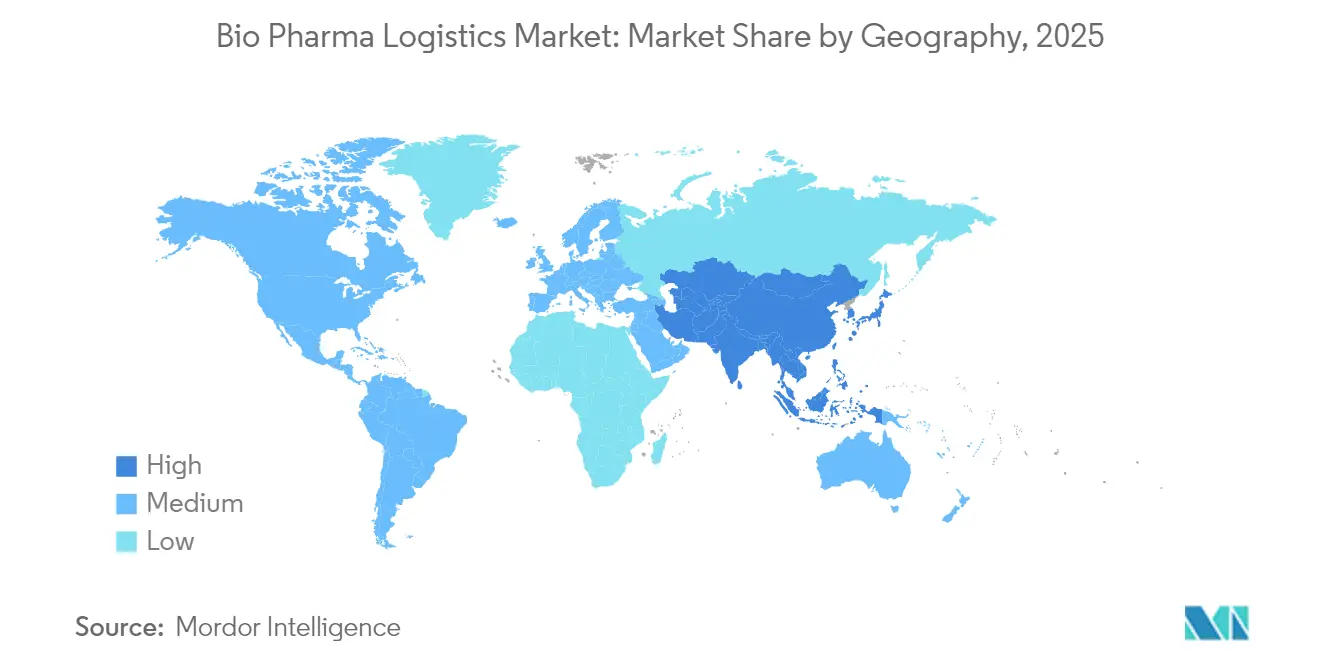

- By geography, North America retained leadership with 41.20% of the biopharma logistics market share in 2025. The bio-pharma logistics market for Asia-Pacific is set to expand at 11.06% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bio-Pharma Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in High-Value Biologicals & Specialty Pharma Share Elevating Cold-Chain Demand | +2.1% | Global, with a concentration in North America & Europe | Medium term (2-4 years) |

| Advanced Therapies Growth (mRNA, Cell & Gene) Necessitating Ultra-Low-Temperature Logistics | +1.8% | North America & Europe leading, Asia-Pacific emerging | Long term (≥ 4 years) |

| Globalization & Decentralization of Clinical Trials Accelerating Direct-to-Patient Shipments | +1.4% | Global, with early adoption in North America & Europe | Short term (≤ 2 years) |

| Stringent Worldwide GDP/GxP Compliance Mandating Outsourcing to Certified 3PLs | +1.6% | Global, with emerging markets catching up | Medium term (2-4 years) |

| E-commerce & D2C Distribution of Specialty Medicines Boosting Last-Mile Temperature-Controlled Delivery | +1.2% | Developed markets leading, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Emerging-Market Biologics Manufacturing Expansion Increasing Cross-Border Cold-Chain Flows | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in High-Value Biologicals & Specialty Pharma Elevating Cold-Chain Demand

Cold-chain failures cost the sector USD 35 billion annually, underscoring the financial imperative for resilient temperature management. Logistics providers deploy AI-driven predictive analytics to foresee excursion risks, while security upgrades counter rising counterfeit threats. Frontier Scientific Solutions invested USD 1.5 billion in Foreign Trade Zone infrastructure around Wilmington and Shannon airports to cut transit times and safeguard high-value biologics [1]Frontier Scientific Solutions, “FTZ Investments Enhance Biologics Cold-Chain Corridor,” biopharminternational.com.

Advanced Therapies Growth (mRNA, Cell & Gene) Necessitating Ultra-Low-Temperature Logistics

mRNA and viral-vector products require storage as low as −150 °C. Cryoport and SK Pharmteco launched an integrated platform spanning manufacturing and distribution tailored to such therapies[2]Cryoport Systems, “Cryoport and SK pharmteco Announce Integrated Advanced-Therapies Supply-Chain Platform,” cryoport.com. Research into thermostable lipids that preserve mRNA at standard refrigeration may ease dependence on deep-freeze networks, yet current pipelines still rely heavily on cryogenic infrastructure. DHL’s acquisition of CRYOPDP, handling more than 600,000 ultra-cold consignments annually, illustrates consolidation around specialized capacity.

Globalization & Decentralization of Clinical Trials Accelerating Direct-to-Patient Shipments

Decentralized trials lift recruitment and retention, but shift logistics from depot-to-site to home delivery. Sponsors now demand flexible, demand-led inventory models plus tele-health coordination. FedEx expanded Life Science Centers across Asia and rolled out sensor-based tracking to manage residential temperature control [3]FedEx Expands Life Science Centres Across Asia with Sensor-Based Tracking,” BioSpectrum Asia, biospectrumasia.com.

Stringent Worldwide GDP/GxP Compliance Mandating Outsourcing to Certified 3PLs

The EMA’s 2025 return to strict GDP certification and India’s revised Schedule M enforce global best practices, prompting drug makers to outsource to networks like Kuehne+Nagel’s 270 GxP-certified sites. In the United States, the Drug Supply Chain Security Act’s serialization regime further elevates compliance complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capacity Constraints in Temperature-Controlled Airfreight & LN₂/Dry-Ice Supply Driving Cost Volatility | -1.3% | Global, with acute pressure in North America & Europe | Short term (≤ 2 years) |

| Divergent Global Regulatory & Customs Requirements Causing Delays and Excursion Risk | -0.9% | Global, particularly affecting cross-border shipments | Medium term (2-4 years) |

| High Carbon Footprint of Cold-Chain Operations Prompting Costly Sustainability Investments | -0.7% | Global, with stricter requirements in Europe & North America | Medium term (2-4 years) |

| Scarcity of Skilled Workforce & GDP-Certified Infrastructure in Emerging Regions Limiting Reliability | -0.6% | Emerging markets in Asia-Pacific, Middle East and Africa, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capacity Constraints in Temperature-Controlled Airfreight & LN₂/Dry-Ice Supply Driving Cost Volatility

Dry-ice shortages during the COVID-19 vaccine rollout revealed a fragile supply base. Air separation units wrestle with high energy prices, while airfreight belly-hold capacity competes with e-commerce. Vienna Airport’s Pharma Handling Center doubled cold-chain space, yet forward bookings still exceed slot availability, causing rate spikes and forcing mode shifts.

Divergent Global Regulatory & Customs Requirements Causing Delays and Excursion Risk

Only 14% of U.S. dispensers were DSCSA-ready before the FDA’s enforcement grace period, and error rates of 30% in EPCIS data risk shipment quarantines. China’s Anti-Espionage Law has delayed Western inspections, while the EU Medical Device Regulation backlog slows combination-product clearances, collectively prolonging border dwell times and heightening excursion risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Services Outpace Traditional Transportation

Transportation accounted for 70.12% of bio pharma logistics market revenue in 2025, anchored by road networks for last-mile and air corridors for time-critical biologics. Nonetheless, value-added services are forecast to grow 10.77% annually to 2031 as clients demand labeling, kitting, and qualified-person release alongside core transport. Providers leverage AI in warehouses to anticipate capacity peaks and prevent temperature deviations. Catalent’s FastChain platform illustrates the shift toward demand-led fulfilment, pairing real-time inventory with regional depots. The bio pharma logistics market size for value-added services is projected to widen steadily, reflecting regulatory complexity and patient-centric packaging needs. Transportation will retain scale but face pricing pressure as supply tightens in temperature-controlled trucking and airfreight.

Within transport, road logistics remains dominant for sub-zero deliveries across continental networks, while air plays a critical role in ultra-cold gene-therapy consignments despite ongoing capacity constraints. Sea freight gains modest share as sustainability targets drive modal shifts for stable biologics. Warehousing growth tracks with clients’ off-site storage preferences, particularly in Europe where new GMP-compliant cold rooms unlock cross-border distribution.

By Temperature Range: Cold Chain Dominance Amid Ultra-Cold Growth

Cold chain services captured 68.40% of the bio pharma logistics market in 2025 and will expand fastest at 10.49% CAGR. Refrigerated (2-8 °C) lanes underpin vaccines and insulin flows, yet ultra-cold (−20 °C to −150 °C) emerges as the star sub-segment for mRNA and cell & gene therapies. The bio pharma logistics market size tied to ultra-cold shipments is forecast to nearly double by 2031. Providers invest in vacuum-insulated panels, phase-change materials, and nitrogen-based dry shippers with IoT beacons for live temperature feeds.

Ambient (15-25 °C) networks continue to serve traditional oral solids but grow slower as formularies tilt toward biologics. Frozen (0 °C to −20 °C) remains niche for specific APIs and long-term stockpiles. Sustainability imperatives accelerate a pivot to reusable shippers and electrified reefers, creating hybrid models pairing green power with dense thermal mass. Blockchain pilots track chain-of-custody events to assure compliance.

By Product Type: Cell & Gene Therapies Lead Innovation-Driven Growth

Vaccines and immunotherapies led 2025 revenue with a 36.74% share, buoyed by ongoing public-health programs. Yet, cell & gene therapies headline growth at 13.05% CAGR through 2031, pushing demand for bespoke, monitored containers. Cold-chain qualified packaging for viral vectors incorporates vibration-damping and slow-release dry ice. The bio-pharma logistics market share for vaccines will moderate as prophylactic programs stabilize, while APIs and bulk biologics maintain steady volume into large-scale plants.

Advanced analytical testing, such as ion-pair reversed-phase chromatography for mRNA impurity profiling, lengthens pre-release lead times, making secure interim storage vital. Finished-dose biologics benefit from efficiencies in fill-finish plants but still depend on end-to-end cold visibility.

By End-User: CROs and CMOs Drive Outsourcing Acceleration

Bio-pharma manufacturers held 58.10% revenue share in 2025; however, CROs/CMOs grow fastest at 12.02% CAGR as firms outsource complexity. That shift multiplies shipment lanes because each CMO services multiple sponsors. Hospitals and trial sites require direct-to-patient options and flexible resupply. The bio pharma logistics market size allocated to CRO/CMO workstreams will therefore rise disproportionately, attracting specialist carriers with clinical-trial licensure and remote-visit expertise.

Manufacturers still command bulk volume, leveraging long-term contracts with integrators to secure capacity. Specialty pharmacies and emerging direct-therapist delivery models form a diversifying tail, each demanding granular tracking for chain-of-identity.

Geography Analysis

North America retained 41.20% share of the bio pharma logistics market in 2025 on the back of entrenched pharmaceutical manufacturing, dense GDP-certified networks, and the early adoption of IoT-enabled monitoring. Major capex programs, such as UPS’s USD 1.6 billion acquisition of Andlauer Healthcare Group, deepen regional infrastructure and reinforce standards leadership.

Asia-Pacific is projected to grow at 11.06% CAGR and will account for the majority of the incremental market value through 2031. Chinese innovators are relocating vector production to Singapore and Thailand to diversify risk, while India expands injectables output under revised GMP rules. Singapore’s new multi-tenant pharma hub embodies the region’s push for high-grade cold storage and cross-border rapid clearance. As a result, the bio-pharma logistics market size related to intra-Asia trade lanes is set to accelerate.

Europe remains a powerhouse, leveraging tight regulatory compliance and extensive road-rail cold corridors. DHL’s 30,000 m² climate-neutral expansion near Frankfurt supports sub-zero warehousing down to −70 °C, reinforcing the continent’s capability to manage cell & gene therapy pipelines. Ongoing consolidation raises service quality, though capacity constraints persist at key cargo gateways like Schiphol and Brussels.

South America and the Middle East & Africa exhibit emerging opportunity profiles. Government vaccine campaigns and growing chronic-disease treatment uptake catalyze the need for certified cold rooms and road-to-air interfaces. However, patchy power grids and limited GDP oversight pose service-quality challenges, slowing the pace of infrastructure upgrades.

Competitive Landscape

The bio-pharma logistics market is moderately consolidated, with the top five integrators controlling an estimated majority of global certified capacity. DHL, UPS, FedEx, Kuehne+Nagel, and DB Schenker leverage capital strength to scale multi-temperature campuses and AI-enabled control towers. DHL earmarked EUR 2 billion (USD 2.29 billion) for health logistics through 2030, including new deep-freeze chambers to reinforce cell-therapy lanes. UPS followed with targeted European and Canadian acquisitions, adding six-zone warehouses and passive packaging know-how.

Specialists such as Cryoport Systems and World Courier differentiate via end-to-end solutions for personalized medicines. Cryoport’s strategic alliance with SK pharmteco merges vector manufacturing and cryogenic transport services to capture value along the advanced-therapy chain. Meanwhile, regional players invest in vertical integration; Asia’s YCH Group and Kerry Logistics deploy virtual temperature dashboards to compete against global integrators in local last-mile execution.

Technology adoption forms the new battleground. Providers integrate blockchain-verified electronic documentation to streamline customs releases and employ predictive analytics to forecast dry-ice replenishment cycles. Sustainability initiatives—including electric-truck fleets and reusable phase-change shippers—serve both cost and brand equity goals as clients seek carbon-neutral supply chains.

White-space remains in underserved emerging markets where GDP facilities are scarce. Firms offering socially accepted temperature-controlled drone delivery and solar-powered cold rooms stand to capture growth, provided they secure local regulatory approvals.

Bio-Pharma Logistics Industry Leaders

Deutsche Post DHL Group

Kuehne + Nagel

UPS (Marken)

FedEx

DSV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DHL Express opened a USD 140 million cargo hub at Lyon-Saint Exupéry Airport capable of 17,500 parcels per hour, including vaccine flows, and equipped with 78 EV chargers

- May 2025: DHL Group expanded its Florstadt Life Sciences & Healthcare Campus with 30,000 m² of climate-neutral storage down to −70 °C.

- April 2025: UPS announced a CAD 2.2 billion (USD 1.6 billion) deal for Andlauer Healthcare Group to bolster Canadian cold-chain capacity.

- January 2025: UPS completed acquisitions of Frigo-Trans and BPL, adding six multi-temperature warehouses and broad European road coverage

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global biopharma logistics market as paid transportation, warehousing, distribution, and selected value-added services that keep vaccines, cell and gene therapies, bulk biologic APIs, and finished biologic doses within required temperatures or ambient ranges from factory gate to clinical or commercial end points worldwide. We count specialist 3PLs and integrators whenever shipments comply with GDP or GxP standards.

Scope Exclusion: Moves of small-molecule generics, diagnostic reagents, medical devices, and captive in-house fleets are outside this scope.

Segmentation Overview

- By Service

- Transportation

- Road

- Rail

- Sea/Ocean

- Air

- Warehousing & Distribution

- Value-Added Services (Labelling, Kitting, QP Release)

- Transportation

- By Temperature Range

- Cold Chain

- Ambient (15-25 °C)

- Refrigerated (2–8 °C)

- Frozen (0 °C to -20 °C)

- Ultra-Cold / Cryogenic (-20 °C to -150 °C)

- Non Cold Chain

- Cold Chain

- By Product Type

- Vaccines & Immunotherapies

- Cell & Gene Therapies

- APIs & Bulk Biologics

- Finished Dose Biologics

- Others

- By End-user

- Bio-Pharma Manufacturers

- CROs (Contract Research Organizations) & CMOs (Contract Manufacturing Organizations)

- Hospitals & Clinical-Trial Sites

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed supply-chain heads at biotech firms, planners at cold-chain 3PLs, and procurement managers at hospitals in North America, Europe, Asia-Pacific, and the Middle East. These conversations clarified lane costs, service-mix shifts, and emerging bottlenecks, closing gaps flagged during desk work.

Desk Research

We began by mining public datasets such as UN Comtrade HS-3002/3006 trade flows, WHO vaccine volume reports, Eurostat road freight tables, IATA special-cargo statistics, and US FDA DSCSA filings to anchor historic demand curves. Mordor analysts then enriched the base with carrier yield trends, airport throughput, and GDP warehouse capacity released by transport ministries, Air Cargo World, and STAT Trade Times. Paid repositories, namely D&B Hoovers and Dow Jones Factiva, verified company splits and facility investments. The sources named illustrate breadth; many additional references informed cross-checks.

A second pass aligned currency year, fuel surcharge evolution, and regional GDP rule changes so numbers sit on comparable cost footing across continents.

Market-Sizing & Forecasting

A top-down rebuild of biologic export and domestic consumption spend sets the 2024 baseline. Then, selective bottom-up roll-ups of lane volumes multiplied by blended tariffs validate totals. Key variables like pipeline share of biologics, ultra-cold shipment incidence, GDP warehouse footprint, air-freight yields, fuel surcharges, and active cell and gene trials feed a multivariate regression that projects demand to 2030. Scarce lane data are imputed through regional penetration ratios confirmed in interviews.

Data Validation & Update Cycle

Mordor analysts compare outputs with customs tallies, airline special-cargo revenue, and quarterly disclosures; deviations beyond five percent trigger fresh calls and model tweaks. Reports refresh annually, with interim updates whenever material events shift flows.

Why Our Bio Pharma Logistics Baseline Commands Reliability

Published estimates often diverge because firms pick different product baskets, cost definitions, and refresh cadences. We surface these drivers so users understand why totals vary.

Key gap factors include counting or excluding clinical-trial moves, monetizing kitting revenue, base-year FX choices, and the speed at which new CGT lanes enter models. According to Mordor Intelligence, our live tariff tracking and yearly rebuilds curb drift that arises when others extend legacy curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 139.41 Bn | Mordor Intelligence | - |

| USD 156.90 Bn | Global Consultancy A | Includes small-molecule and device freight, single-year FX |

| USD 110.98 Bn | Industry Journal B | Omits value-added services and clinical-trial lanes |

| USD 152.00 Bn | Regional Consultancy C | Holds tariffs constant at 2023 levels, ignores fuel surcharges |

These contrasts show how our disciplined scope selection, variable tracking, and yearly refresh give decision-makers a balanced, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current size of the bio pharma logistics market?

The bio pharma logistics market reached USD 152.04 billion in 2026 and is on track to hit USD 234.58 billion by 2031.

Which segment in the bio pharma logistics market is growing the fastest?

Value-added services—such as labeling, kitting, and qualified-person release—are expanding at 10.77% CAGR, outpacing traditional transportation.

Why is ultra-cold logistics crucial for future growth?

Advanced mRNA and cell & gene therapies require temperatures down to −150 °C, driving investment in cryogenic infrastructure and specialized packaging.

Which region will contribute the most incremental growth through 2031?

Asia-Pacific holds the highest forecast CAGR at 11.06%, supported by rising biomanufacturing and clinical-trial activity.

How are sustainability goals influencing the industry?

Shippers and carriers are adopting reusable packaging, electrified fleets, and route-optimization algorithms to cut emissions that comprise over 80% of pharma supply-chain carbon output.

Page last updated on: