Germany Healthcare Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

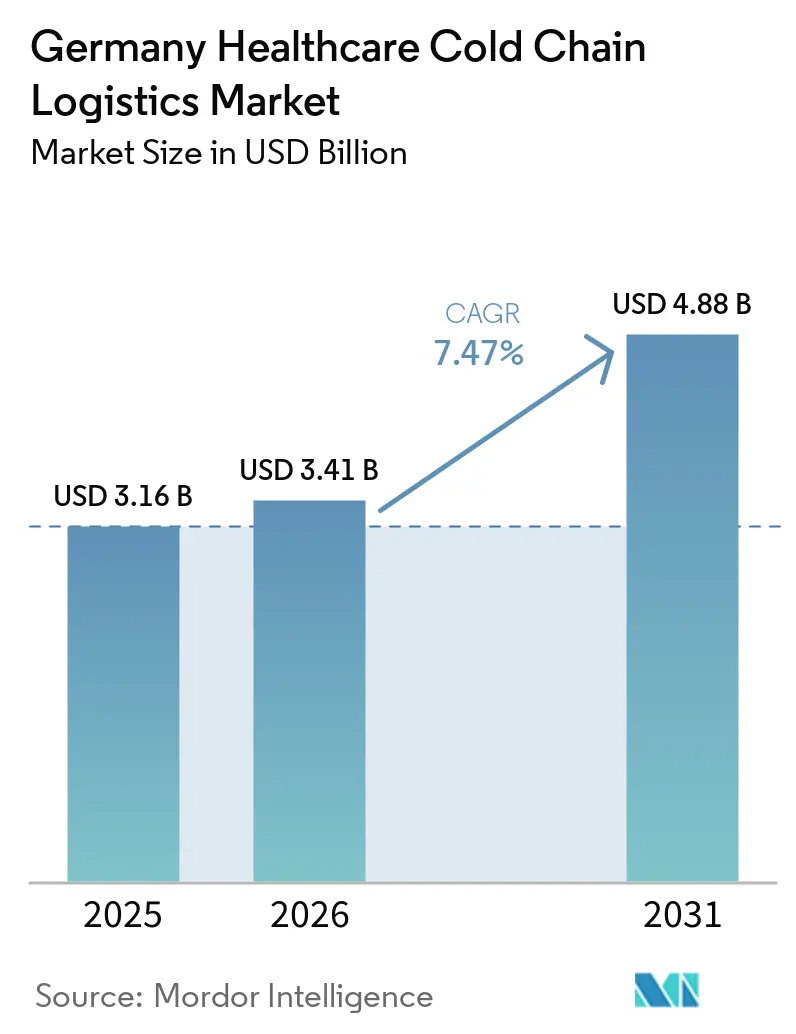

| Base Year Market Size (2025) | USD 3.16 Billion |

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.88 Billion |

| Growth Rate (2026 - 2031) | 7.47% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Healthcare Cold Chain Logistics Market Analysis by Mordor Intelligence

The Germany healthcare cold chain logistics market size is expected to increase from USD 3.16 billion in 2025 to USD 3.41 billion in 2026 and reach USD 4.88 billion by 2031, growing at a CAGR of 7.47% over 2026-2031.

Growth in the Germany healthcare cold chain logistics market is tied to the wider use of biopharmaceuticals, tighter compliance requirements under EU Good Distribution Practice rules, and the rising need for cryogenic handling for advanced therapies. The Germany healthcare cold chain logistics market continues to draw investment because healthcare-grade temperature control, documentation, and handling precision remain difficult to replace with standard cold chain assets. The ALBVVG safety stock requirement is lifting demand for GDP-compliant storage, cross-docking, and inventory management near major pharmaceutical hubs. Digital visibility has also become a core operating requirement, which gives larger operators an advantage when they can combine monitored transport, serialized documentation, and temperature tracking in one workflow. Energy costs, labor shortages, and space constraints still pressure margins, yet the Germany healthcare cold chain logistics market remains supported by regulated demand and by product categories that need specialized handling throughout the distribution chain.

Key Report Takeaways

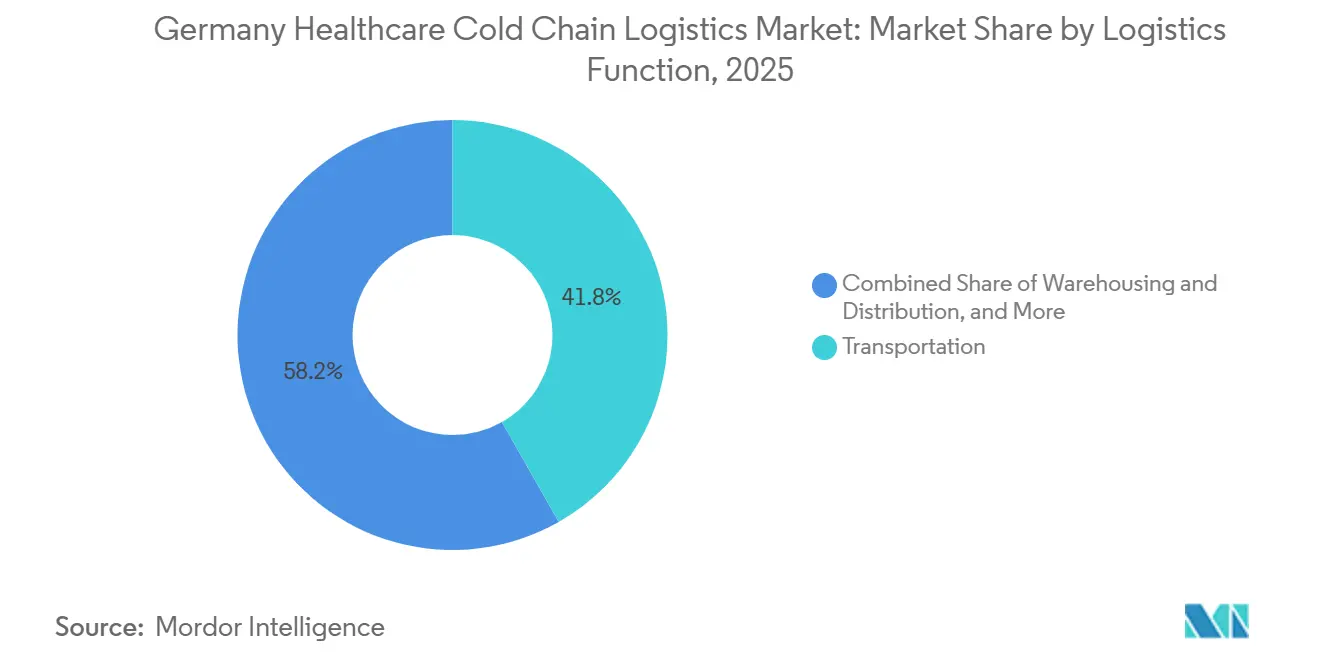

- By logistics function, transportation held 41.78% of the Germany healthcare cold chain logistics market share in 2025, while value-added services recorded the highest projected CAGR at 8.22% through 2031.

- By temperature type, chilled accounted for 48.12% of the Germany healthcare cold chain logistics market share in 2025, while frozen posted the fastest projected CAGR at 11.39% through 2031.

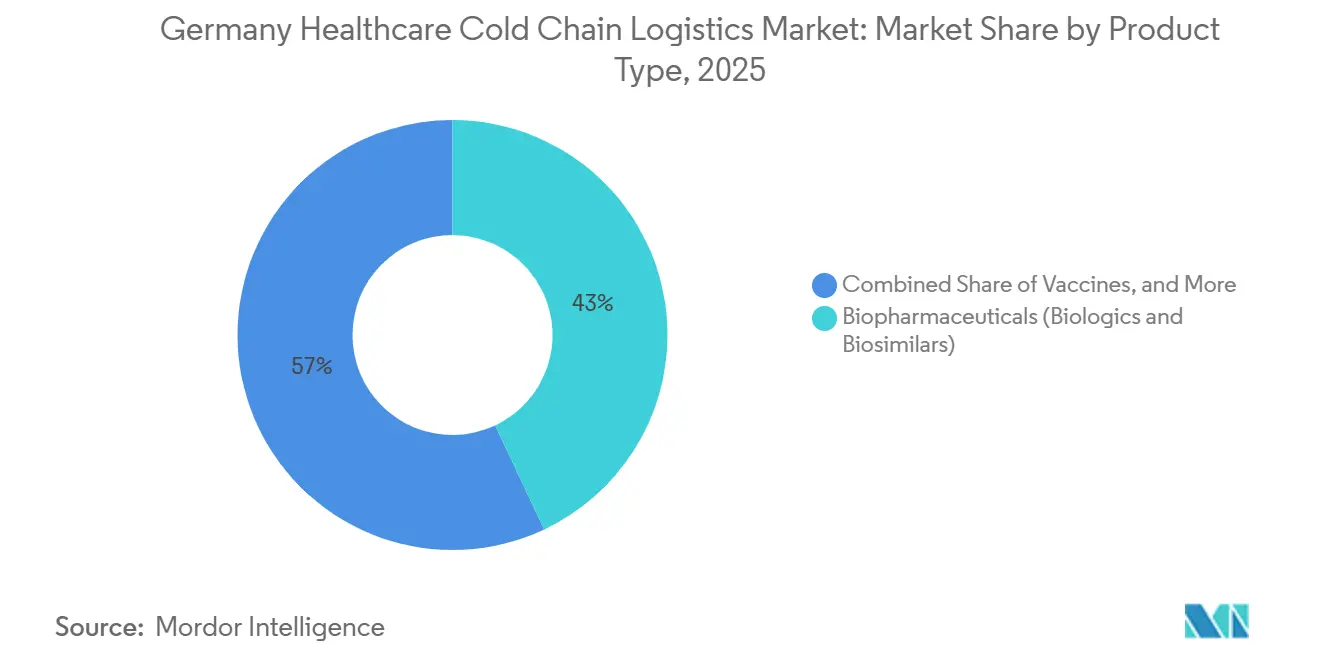

- By product type, biopharmaceuticals led with 42.98% of the Germany healthcare cold chain logistics market size in 2025, while cell and gene therapies are forecast to expand at a 13.53% CAGR through 2031.

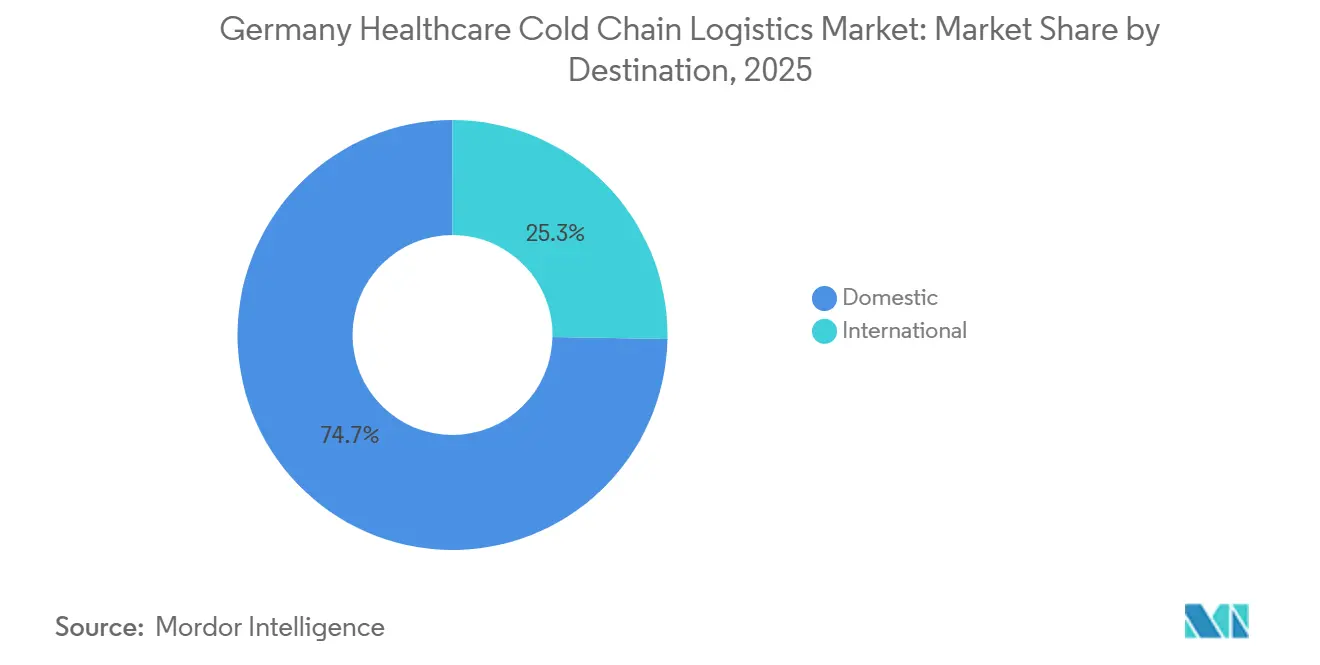

- By destination, domestic distribution held 74.70% of the Germany healthcare cold chain logistics market share in 2025, while international lanes recorded the highest projected CAGR at 8.53% through 2031.

- By end user, biopharmaceutical companies accounted for 36.35% of the Germany healthcare cold chain logistics market size in 2025, while biopharmaceutical manufacturers posted the fastest projected CAGR at 8.11% through 2031.

- By geography, North Rhine-Westphalia held 24.11% of the Germany healthcare cold chain logistics market share in 2025, while Bavaria recorded the highest projected CAGR at 8.77% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Healthcare Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologics and Biosimilars Volume Growth | +2.10% | National, with concentration in Rhine-Ruhr, Munich, Frankfurt corridors | Medium term (2-4 years) |

| Vaccine, Blood, and Specialty Therapy Cold Flows | +1.20% | National, with NRW hospital networks and Baden-Württemberg blood services as primary nodes | Medium term (2-4 years) |

| E-Prescription and Home-Delivery Expansion | +0.80% | National, urban concentration in Berlin, Munich, Hamburg, Cologne | Short term (≤ 2 years) |

| GDP-Led Digital Visibility Upgrades | +0.70% | Global with strong EMEA uplift, Germany as leading compliance adopter | Long term (≥ 4 years) |

| ALBVVG Safety-Stock Mandates Lifting Cold Inventory Nodes | +0.90% | National, hospital pharmacies and wholesale distributors across Germany | Short term (≤ 2 years) |

| CGT and Precision-Oncology Cluster Build-Out | +1.30% | Bavaria, NRW, with spillover to Baden-Württemberg | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Biologics and Biosimilars Volume Growth

Germany’s manufacturing base for biologics and biosimilars is creating demand that standard logistics systems were not built to handle. Biosimilar development costs can reach EUR 300 million (USD 324 million), and that technical complexity carries through to transport, storage, and dispensing. These products need uninterrupted 2 °C to 8 °C control from origin to point of use, and any temperature excursion can invalidate a batch and create liability exposure. Germany’s GKV-led substitution practices are also increasing the number of GDP-qualified routes needed to connect manufacturers with 19,000 pharmacies across the country. That pattern is concentrating volume with operators that already have validated infrastructure, documented temperature controls, and established GDP workflows[1]“Guidelines on Good Distribution Practice of Medicinal Products for Human Use,” Official Journal of the European Union, eur-lex.europa.eu.

ALBVVG Safety-Stock Mandates Lifting Cold Inventory Nodes

The Germany healthcare cold chain logistics market is also being lifted by the ALBVVG stockpiling framework, which is active through 2025 and 2026 and requires 6-month reserves for rebated off-patent drugs. A 2026 Scientific Reports analysis estimated the annual cost of this reserve at EUR 163 million (USD 176 million), and cold-chain products represent a meaningful part of the affected stock-keeping units because 17% to 31% of pharmaceutical shipments require temperature control. Hospital pharmacies and wholesalers have already had to expand GDP-compliant cold rooms and cross-docking capacity near major pharmaceutical clusters. The Techniker Krankenkasse Lieferklima-Report 2025 also showed that warehousing capacity remains a limiting factor even where supply reliability has improved. This requirement gives the Germany healthcare cold chain logistics market a regulatory demand floor that is less exposed to normal cyclical swings.

CGT and Precision-Oncology Cluster Build-Out

The commercial rollout of advanced therapy medicinal products is creating a cold chain niche defined by extreme temperature needs, small shipment volumes, and strict time windows. Munich’s biotech cluster is adding dedicated GDP-qualified deep-freeze and cryogenic infrastructure, with storage reaching as low as minus 196 °C in liquid nitrogen systems. Germany now acts as both an origin point and a receiving point for autologous vein-to-vein shipments, which raises the operational burden on domestic logistics providers. Their handling model depends on specialized carriers that can manage the chain of identity, patient-level traceability, and cryogenic transport without deviation[2]“E-Prescription (Elektronisches Rezept) Rollout Update,” Bundesgesundheitsministerium, bundesgesundheitsministerium.de.

GDP-Led Digital Visibility Upgrades

The EU GDP framework requires temperature excursions to be documented, investigated, and reported, which is making real-time monitoring a basic operating requirement in Germany. IoT-enabled data loggers, continuous telemetry, and cloud-based chain-of-custody records are moving from optional tools to expected controls. This shift is becoming more important as German distribution sites face closer scrutiny on how they document and respond to deviations. DHL Group’s EUR 2 billion (USD 2.16 billion) healthcare logistics investment also points to the growing role of IT systems in cold chain compliance and end-to-end visibility. The result is a service layer that combines physical transport with predictive alerts, automated reporting, and auditable documentation across each shipment leg[3]"Good distribution practice." European Medicines Agency,ema.europa.eu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Refrigeration Energy and Compliance Cost Pressure | -0.80% | National, with highest impact in Bavaria and Baden-Württemberg | Short term (≤ 2 years) |

| Qualified GDP Driver and Technician Shortages | -0.50% | National, concentrated around Frankfurt, Munich, Düsseldorf pharmaceutical hubs | Medium term (2-4 years) |

| GDP-Approved Space Scarcity Near Pharma Hubs | -0.40% | Bavaria, NRW, Frankfurt Rhine-Main | Long term (≥ 4 years) |

| Mandated Stock Buffers Raising Expiry and Returns Risk | -0.30% | National, hospital pharmacies and wholesale distributors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Refrigeration Energy and Compliance Cost Pressure

Energy use is becoming one of the clearest structural cost pressures in the Germany healthcare cold chain logistics market. LOXXESS has stated that temperature control can account for up to 65% of total electricity consumption in GDP-compliant cold chain facilities. Germany’s high industrial electricity prices make this burden harder for smaller regional operators to absorb than for global integrators with more purchasing scale. The F-Gas phase-down is also forcing fleet and facility upgrades toward low-GWP systems, which adds another capital layer before 2030. These factors are pushing the market toward consolidation because operators without retrofit capacity may struggle to keep certified cold assets competitive.

Qualified GDP Driver and Technician Shortages

The labor gap in the Germany healthcare cold chain logistics market is tighter than in general logistics because pharmaceutical transport needs GDP-trained personnel and, in some cases, ADR and therapy-specific handling credentials. That requirement narrows the available workforce even before route demand is considered. The shortage limits how many compliant lanes an operator can legally staff in high-demand corridors such as Frankfurt, Munich, and Düsseldorf. Wage pressure is rising as companies compete for trained drivers, handlers, and cold chain technicians with documented compliance backgrounds. Training programs are expanding, but the time needed to move from training to deployment means short-term relief remains limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Value-Added Services Move Faster Than Core Transport

Transportation accounted for 41.78% of the Germany healthcare cold chain logistics market size in 2025, which reflected Germany’s role as a pharmaceutical manufacturing and export gateway in Europe. Road transport remained the dominant mode because the country’s motorway network connects the main pharmaceutical clusters in NRW, Bavaria, and Baden-Württemberg with high route frequency. Air freight remained smaller by volume, yet it carried an outsized revenue contribution because time-critical biologics and cell and gene therapy shipments command premium pricing through Frankfurt. Rail and sea freight remained limited inside domestic healthcare distribution and were used more for import and export flows than for routine in-country delivery.

Value-added services are projected to grow at an 8.22% CAGR through 2031, which makes them the fastest-rising logistics function in the Germany healthcare cold chain logistics market. This expansion comes from higher regulatory complexity rather than from volume alone. Pharmaceutical customers increasingly want bundled services that include serialization support, re-labeling, documentation handling, clinical trial kitting, and chain-of-identity controls. Warehousing and distribution still hold an important position, but GDP-approved space limits near key hubs are slowing the pace at which storage capacity can scale[4] "7 GDP Requirements for Pharmaceutical Warehouses." Eupry,eupry.com/gdp/gdp-warehouses.

By Temperature Type: Chilled Volumes Lead While Frozen and Cryogenic Needs Expand Faster

The chilled segment captured 48.12% of the Germany healthcare cold chain logistics market size in 2025 because biologics, biosimilars, vaccines, blood products, and many specialty injectables still move mainly within the 2 °C to 8 °C range. Germany’s biologic prescribing growth and wider biosimilar use are sustaining that temperature band at scale. The segment also carries heavy compliance obligations because chilled-chain integrity requires close documentation and deviation management under GDP rules. That combination of volume and compliance keeps chilled handling central to the Germany healthcare cold chain logistics industry.

Frozen is the fastest-growing thermal segment, with a projected CAGR of 11.39% through 2031. Growth is being led by mRNA-derived biologics, frozen plasma products, and biosimilar formulations that need sub-zero handling throughout their shelf life. Ambient flows remain more stable, but they face margin pressure as some legacy formulations move toward broader temperature tolerance. Deep-frozen and ultra-low logistics are still niche, yet they are attracting targeted investment, including Movianto’s 2026 deep-freeze capability of minus 20 °C to minus 80 °C at its Wiesloch-Walldorf site in Baden-Württemberg.

By Product Type: Biopharmaceuticals Hold Scale While Cell and Gene Therapies Raise Technical Demands

Biopharmaceuticals held 42.98% of the Germany healthcare cold chain logistics market share in 2025, supported by Germany’s manufacturing depth in monoclonal antibodies, biosimilar insulins, plasma derivatives, and recombinant proteins. Conventional prescription and specialty pharmaceuticals remained the second-largest product group and are becoming more temperature sensitive as newer formulations move toward biologic platforms. The policy debate around exclusive rebate contracts for biosimilars has also raised concern about long-term domestic manufacturing stability, which matters because local production volumes support domestic cold chain density. This product mix keeps the Germany healthcare cold chain logistics industry tied closely to biologic scale-up rather than to standard generic flows.

Cell and gene therapies are forecast to expand at a 13.53% CAGR through 2031, making them the fastest-growing product type. Their logistics profile is very different from other healthcare products because each autologous shipment is patient-specific, time-critical, and linked to chain-of-identity requirements. Clinical trial materials, vaccines, medical devices, veterinary medicines, blood and plasma components, and diagnostic products each add separate handling rules and demand patterns. That breadth gives the product base more resilience because the Germany healthcare cold chain logistics market is not dependent on one single therapy category.

By Destination: Domestic Distribution Provides Scale While International Lanes Raise Complexity

Domestic distribution accounted for 74.70% share of the Germany healthcare cold chain logistics market size in 2025 because pharmacies, hospitals, and clinical sites across the country create a high-frequency and recurring demand base. This network remains the revenue foundation for the leading operators in the Germany healthcare cold chain logistics market. National pharmaceutical distribution rules and GDP requirements also raise entry barriers for providers that do not already have validated systems, trained staff, and wholesale distribution authorization workflows. Domestic growth remains steady, but it is being driven more by biologic volume gains and mandatory inventory build-up than by new route creation.

International lanes are projected to expand at an 8.53% CAGR through 2031, which makes them the fastest-growing destination segment. That rise is linked to Germany’s role as an export base for novel biopharmaceuticals and as a transit hub for clinical trial and advanced therapy flows across Europe. Germany exported EUR 105.8 billion (USD 114.3 billion) in pharmaceuticals in 2024, and temperature-sensitive biologics were the fastest-moving part of that trade mix. Cross-border coordination remains demanding because advanced therapies and blood products still require country-specific authority alignment, which favors operators with stronger regulatory affairs capability and better documentation discipline.

By End User: Biopharmaceutical Companies Hold the Largest Base While Manufacturers Add New Capacity

Biopharmaceutical companies accounted for 36.35% of the Germany healthcare cold chain logistics market share in 2025 because their products depend heavily on chilled, frozen, or cryogenic handling from plant to patient. These companies also prefer to outsource logistics complexity to specialist 3PL and 4PL providers instead of building full in-house temperature-controlled networks. That preference supports multi-year contracts with performance measures tied to excursion rates, on-time delivery, and documentation quality. Biopharmaceutical manufacturers are projected to record the fastest CAGR at 8.11% through 2031 as new biologic and cell therapy capacity continues to build in Munich-Martinsried and the Rhine-Ruhr corridor.

Hospitals and clinics are becoming more influential in service design because therapies such as CAR-T require close coordination between collection, transport, and infusion timing. Retail pharmacies are also becoming more relevant endpoints as e-prescription workflows support temperature-controlled home delivery. Distributors and wholesalers are absorbing more warehousing burden because safety stock rules increase the need for compliant inventory holding. That broad end-user mix means the Germany healthcare cold chain logistics industry must combine high-frequency national distribution with highly specialized therapy movements in the same operating environment.

Geography Analysis

North Rhine-Westphalia held 24.11% of the Germany healthcare cold chain logistics market share in 2025, supported by the Rhine-Ruhr pharmaceutical corridor, the country’s largest population base, and dense university hospital networks in Cologne, Düsseldorf, Essen, and Bonn. Those institutions make the region a major endpoint for high-value specialty therapies that need strict cold handling. Hospital pharmacy cooperatives in NRW have also increased procurement concentration, which favors operators that already have dedicated regional GDP infrastructure. The region benefits from Cologne-Bonn Airport and from its linkage with Frankfurt, which supports time-sensitive pharmaceutical air movements. SECURPHARM-related serialization requirements add another layer of complexity because hospital, pharmacy, and wholesaler channels frequently intersect in the same regional distribution web.

Bavaria is projected to expand at an 8.77% CAGR through 2031, making it the fastest-growing region in the Germany healthcare cold chain logistics market. Munich’s biotech and advanced therapy base is the main reason for that momentum. The Munich-Ingolstadt corridor is adding dedicated GDP-qualified sites that focus on biologic and advanced therapy distribution. Baden-Wurttemberg is also becoming more important because it combines pharmaceutical mid-market activity with medical device manufacturing across the Heidelberg-Mannheim area. Movianto’s 2026 expansion at VGP-Park Wiesloch-Walldorf adds the region’s first commercial deep-freeze pharmaceutical logistics capability and strengthens its role in sub-zero distribution.

The Rest of States, which include Hesse, Berlin-Brandenburg, Hamburg, and smaller federal states, form a diverse demand base with different operating profiles. Hesse matters because Frankfurt Airport remains Europe’s largest pharmaceutical air cargo hub and supports CEIV Pharma-certified activity from major global operators. Berlin-Brandenburg is emerging as an advanced therapy destination as treatment capacity expands at Charite - Universitätsmedizin Berlin. Hamburg is gaining relevance in pharmaceutical ocean freight after GEODIS received GDP certification there in February 2025. Together, these states broaden the geographic footprint of the Germany healthcare cold chain logistics market beyond the main manufacturing corridors.

Competitive Landscape

The Germany healthcare cold chain logistics market is moderately concentrated at the premium service tier and fragmented across the wider mid-market. DHL Group, UPS Healthcare, Kuehne+Nagel, FedEx, and GEODIS hold structural advantages because they can deploy larger capital budgets, cover international lanes, and maintain higher compliance depth across multimodal networks. DHL Group’s EUR 2 billion (USD 2.16 billion) healthcare logistics investment through 2030, along with its Florstadt expansion to 100,000 m² and the acquisition of CRYOPDP, shows the scale now shaping competitive benchmarks. At the same time, Movianto, trans-o-flex ThermoMed, Eurotranspharma, and Pharmaserv Logistics still retain strong local positions because domestic GDP-compliant routing and last-mile pharmaceutical delivery require dense local execution. Deep-freeze and cryogenic services for advanced therapies remain the clearest open niche because treatment center growth is moving faster than specialized logistics capacity.

Technology is becoming a more decisive differentiator in the Germany healthcare cold chain logistics market. Operators that combine real-time temperature telemetry, digital chain-of-custody records, and faster deviation response are winning renewals at better pricing, while passive monitoring models face stronger commoditization pressure. FedEx’s May 2025 IATA CEIV Pharma Corporate Certification across its air network, including Cologne and Frankfurt in Germany, also shows how accreditation is being used to strengthen procurement positioning. EU GDP compliance, documented quality systems, and auditable handling controls are now closer to minimum qualification standards than optional add-ons.

UPS Healthcare strengthened its position in January 2025 when it completed the acquisition of Frigo-Trans and BPL, adding a 6-temperature-zone network that extends from cryopreservation at minus 196 °C to ambient handling. Kuehne+Nagel added Frankfurt to its weekly Inspire air freight rotation in June 2026, which increased GDP-qualified air capacity on major biopharma lanes tied to Germany. GEODIS also widened modal flexibility by expanding compliant cold chain activity that includes pharmaceutical ocean freight handling in Hamburg and a broader certified network. Competition in the Germany healthcare cold chain logistics market will keep favoring operators that can combine validated infrastructure, regulatory discipline, and coverage across both domestic and cross-border healthcare flows.

Germany Healthcare Cold Chain Logistics Industry Leaders

-

United Parcel Service of America, Inc. (UPS)

-

FedEx

-

DHL Group

-

Kuehne+Nagel

-

GEODIS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Kuehne+Nagel added Frankfurt to its weekly Inspire air freight rotation, operated by a Boeing 747-8F with 140 tonnes cargo capacity, directly linking Chicago and Frankfurt, 2 major pharmaceutical production hubs, for time-sensitive healthcare shipments. The updated rotation connects Atlanta, Chicago, Frankfurt, Liege, Sharjah, and Taipei, significantly expanding GDP-qualified air freight capacity on critical biopharma lanes relevant to Germany's export corridor.

- April 2026: GEODIS opened its first dedicated healthcare cold chain cross-dock facility in the Americas, Chicago, Illinois, extending a global cold chain network that already includes certified nodes in Germany among its 170-country footprint. The 7,246.44 m² facility is bonded, exclusively dedicated to healthcare products, and operates as a critical freight forwarding node for pharmaceutical air and ocean exports.

- February 2026: DHL Group fully operationalized its dedicated transatlantic cold chain air corridor connecting Brussels and Cincinnati, with a dedicated Boeing 777 DHL Health Logistics freighter operating 6 days per week and supported by specialized ground handling technology for end-to-end GDP compliance. The Brussels hub's 45,000 m² pharma-only zone at BRUcargo provides direct connectivity to Germany's pharmaceutical manufacturing network.

- February 2026: DHL Group launched its expanded Airfreight Cold Chain Network under the new DHL Health Logistics brand, connecting more than 30 GDP-compliant aviation hubs and gateways globally. The network specifically supports biologics, vaccines, and cell and gene therapies with full end-to-end temperature visibility as part of the EUR 2 billion (USD 2.16 billion) strategic investment program.

Germany Healthcare Cold Chain Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Chilled (0-5 °C) |

| Frozen (-18-0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than -20 °C) |

| Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | |

| Biopharmaceuticals (Biologics and Biosimilars) | |

| Vaccines | |

| Clinical Trial Materials | |

| Cell and Gene Therapies | |

| Medical Devices | |

| Veterinary Medicine | |

| Blood, Plasma and Blood Components | |

| Diagnostic and Laboratory Products | |

| Organs and Human Tissues | |

| Others |

| Domestics |

| International |

| Pharmaceutical Manufacturers |

| Biopharmaceutical Manufacturers |

| Hospitals and Clinics |

| Hospitals and Retail Pharmacies |

| Healthcare Distributors and Wholesalers |

| Others |

| North Rhine-Westphalia |

| Bavaria (Bayern) |

| Baden-Wurttemberg |

| Rest of States |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Type | Chilled (0-5 °C) | |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than -20 °C) | ||

| By Product Type | Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | ||

| Biopharmaceuticals (Biologics and Biosimilars) | ||

| Vaccines | ||

| Clinical Trial Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices | ||

| Veterinary Medicine | ||

| Blood, Plasma and Blood Components | ||

| Diagnostic and Laboratory Products | ||

| Organs and Human Tissues | ||

| Others | ||

| By Destination | Domestics | |

| International | ||

| By End User | Pharmaceutical Manufacturers | |

| Biopharmaceutical Manufacturers | ||

| Hospitals and Clinics | ||

| Hospitals and Retail Pharmacies | ||

| Healthcare Distributors and Wholesalers | ||

| Others | ||

| By Region | North Rhine-Westphalia | |

| Bavaria (Bayern) | ||

| Baden-Wurttemberg | ||

| Rest of States | ||

Key Questions Answered in the Report

What is the 2031 outlook for healthcare cold chain logistics in Germany?

The value is forecast to reach USD 4.88 billion by 2031, rising from USD 3.41 billion in 2026 at a 7.47% CAGR over 2026-2031.

Which product category leads cold chain demand in Germany?

Biopharmaceuticals led with a 42.98% share in 2025 because biologics and biosimilars need controlled handling from production to dispensing.

Which temperature range is expanding the fastest?

Frozen is the fastest-growing temperature type, with an 11.39% CAGR through 2031, supported by sub-zero biologics, plasma products, and newer therapy formats.

Why is Bavaria growing faster than other regions?

Bavaria is projected to expand at an 8.77% CAGR through 2031 because Munich has a strong biotech and advanced therapy manufacturing base that needs specialized logistics.

What is driving value-added services in this space?

Value-added services are growing at an 8.22% CAGR because drug makers increasingly need bundled support for serialization, documentation, re-labeling, and chain-of-identity controls.

How important is domestic distribution for Germany?

Domestic movements accounted for 74.70% of demand in 2025 because pharmacies, hospitals, and clinical sites across the country create steady and recurring cold chain volumes.

Page last updated on: