China Pharmaceutical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

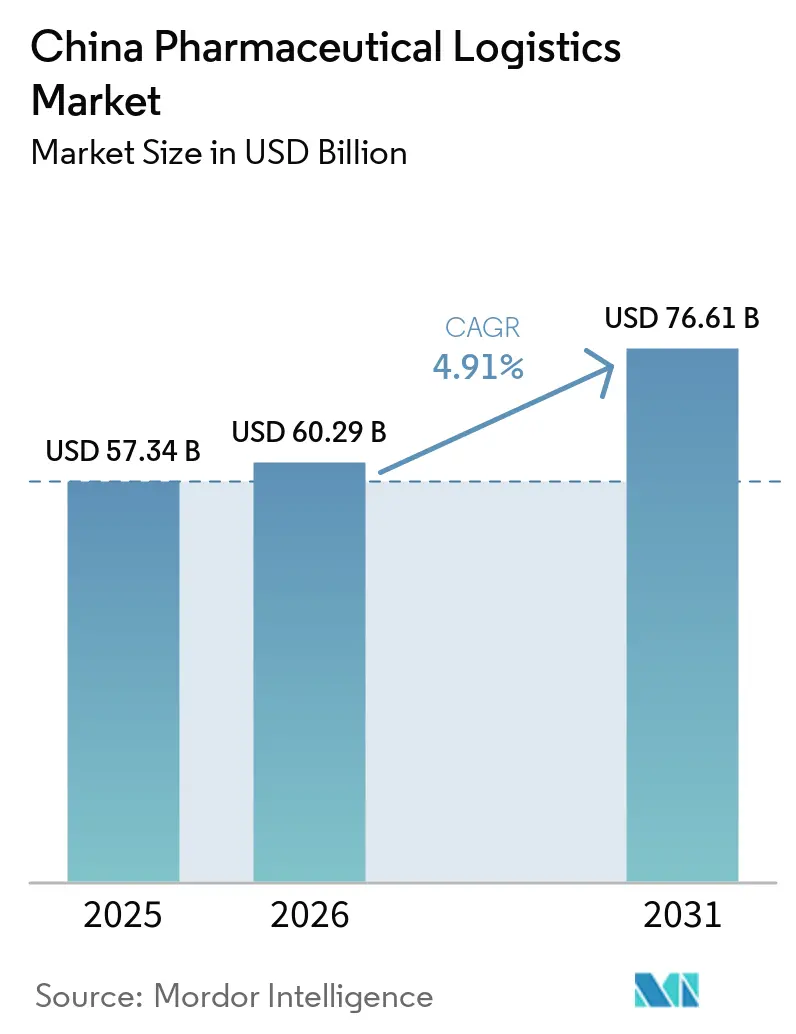

| Base Year Market Size (2025) | USD 57.34 Billion |

| Market Size (2026) | USD 60.29 Billion |

| Market Size (2031) | USD 76.61 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

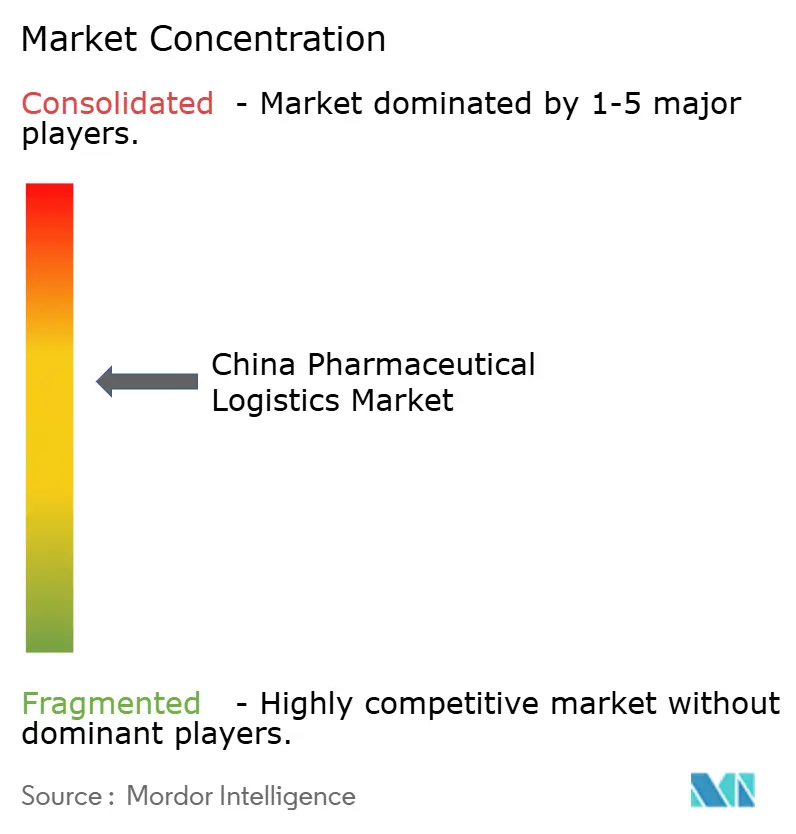

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Pharmaceutical Logistics Market Analysis by Mordor Intelligence

The China pharmaceutical logistics market size is valued at USD 57.34 billion in 2025, projected to reach USD 60.29 billion in 2026, and USD 76.61 billion by 2031, growing at a CAGR of 4.91% from 2026 to 2031.

The market is supported by steady demand for medicines from an aging population, a large domestic pharmaceutical production base, and a policy system that links distribution quality more directly to drug safety and service consistency. The China pharmaceutical logistics market is also moving away from a narrow transport model toward broader supply-chain execution that includes warehousing, monitoring, traceability, and specialized fulfillment for sensitive therapies. The NMPA guidance issued in March 2026 establishes a more uniform national baseline and reduces the earlier gap between provincial operating standards, thereby pushing capital toward qualified end-to-end infrastructure and more integrated operating models. The China pharmaceutical logistics market is also seeing a sharper competitive split, as state-backed distributors still hold strong hospital-channel positions while technology-led operators are gaining ground in cold-chain, fast delivery, and pharmacy e-commerce fulfillment. Premium-margin cold-chain services and outsourced value-added functions are therefore growing faster than the broad logistics cost base, which keeps the market’s value creation stronger than headline cost growth alone suggests.

Key Report Takeaways

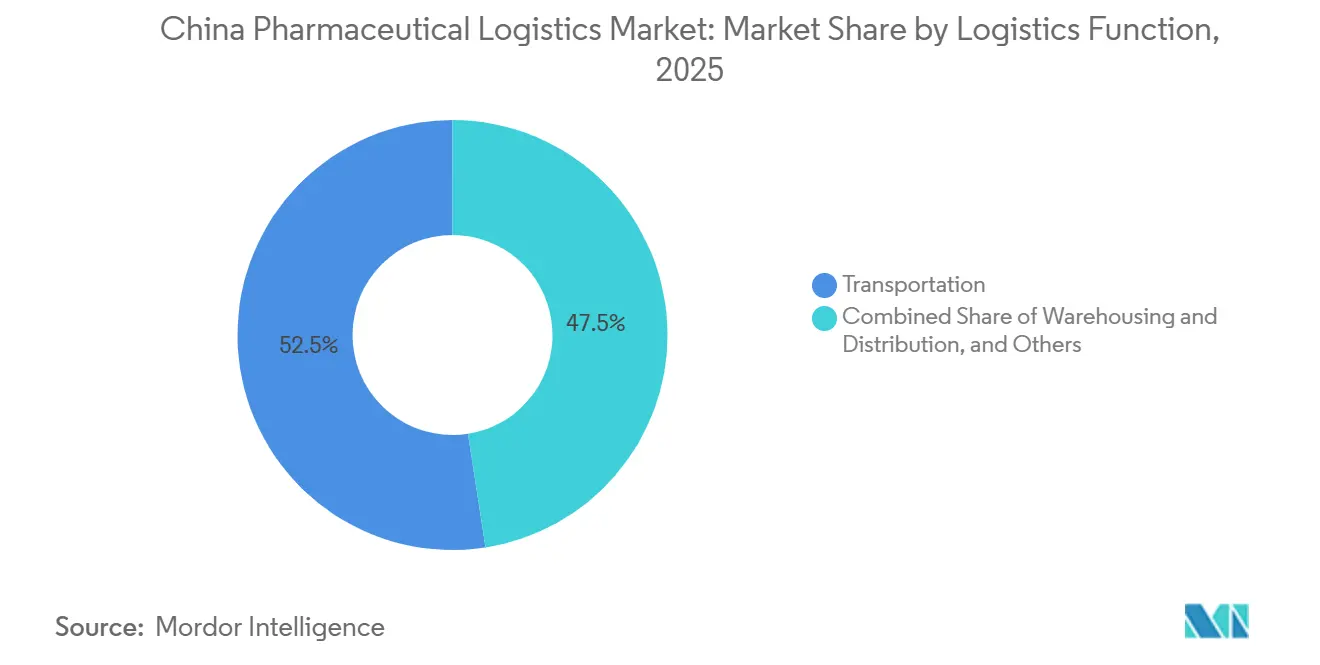

- By logistics function, transportation held 52.46% of the China pharmaceutical logistics market share in 2025, while value-added services are forecast to expand at a 7.74% CAGR through 2031.

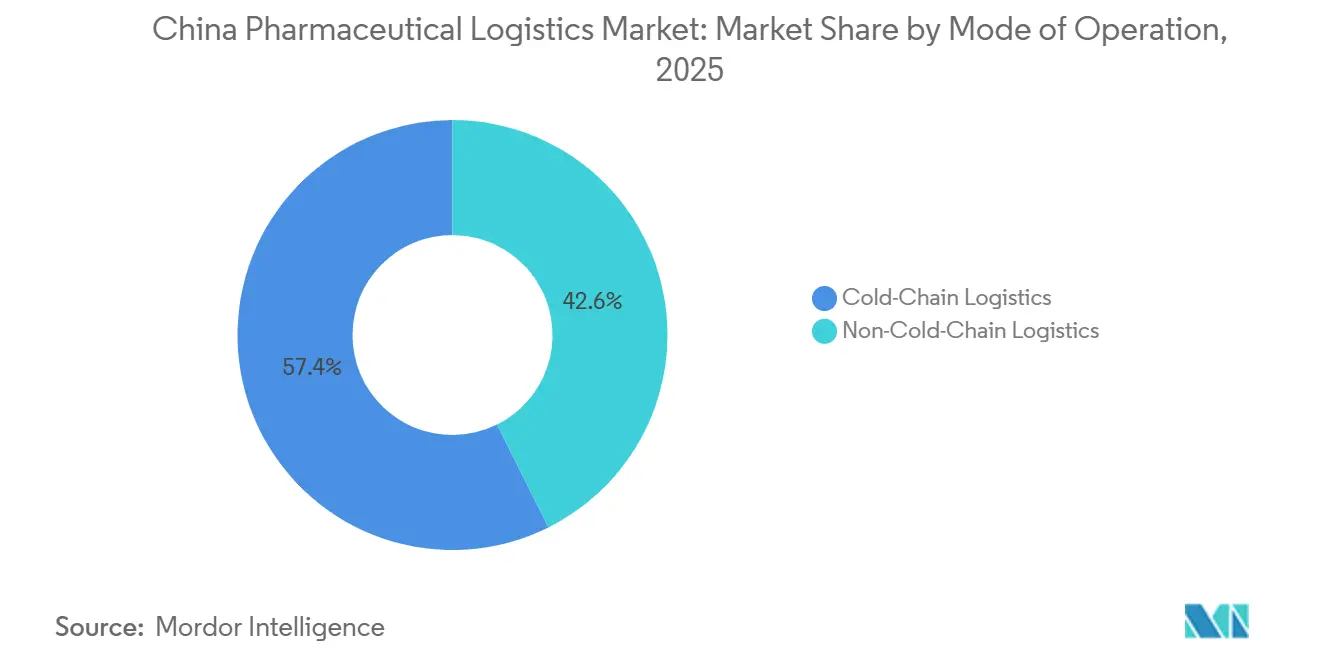

- By mode of operation, the cold chain accounted for 57.36% of the China pharmaceutical logistics market size in 2025 and is also the fastest-growing segment, with a 6.91% CAGR through 2031.

- By product type, prescription drugs led with a 40.92% of the China pharmaceutical logistics market share in 2025, while cell and gene therapies are projected to grow at an 8.05% CAGR through 2031.

- By geography, the East region accounted for 29.20% of the China pharmaceutical logistics market in 2025, while the Southwest region is forecast to grow at a 6.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Essential-Drug distribution network | +1.1% | National, concentrated gains in Central and Northwest provinces | Medium term (2-4 years) |

| Growth in biologics and temperature-controlled demand | +1.2% | East primary, South and Southwest secondary | Long term (≥ 4 years) |

| Rise of e-commerce pharmacies and 24-Hour delivery expectations | +0.8% | North, East, South in tier-1 and tier-2 cities, with spillover to Central | Medium term (2-4 years) |

| Stricter GDP Audit and Licensing Enforcement | +0.6% | National, with earlier compliance gains in East and South | Short term (≤ 2 years) |

| Centralized-procurement hubs drive regional consolidation | +0.5% | National, with primary hubs in North, East, and Central | Medium term (2-4 years) |

| Drone and autonomous vehicle pilots for Western Mid-Mile Routes | +0.3% | Southwest and Northwest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of the National Essential-Drug Distribution Network

The updated 2025 National Basic Medical Insurance Drug Directory widened the reimbursed product base and, for the first time, added a commercial health insurance category for innovative drugs, which directly increases the flow of covered medicines through licensed distribution channels[1]“Circular on Issuing the National Basic Medical Insurance, Work-Related Injury Insurance and Maternity Insurance Drug Directory (2025),” NHSA, nhsa.gov.cn. . That change matters for the China pharmaceutical logistics market because reimbursed access expands throughput at both the hospital and retail ends of the chain. It underscores the need for additional ambient capacity, but also for qualified cold-chain infrastructure as innovative therapies enter broader circulation. The policy direction under the 15th Five-Year Plan also supports larger national distributors, which strengthens scale advantages in compliance, route density, and procurement execution. For the China pharmaceutical logistics market, the result is a larger national flow base paired with a higher minimum service standard. Smaller operators that cannot fund traceability, serialization, and temperature-controlled assets are therefore under more pressure as the distribution network broadens.

Rapid Growth in Biologics and Temperature-Controlled Demand

Biologics and other temperature-sensitive products are shifting the operating center of the China pharmaceutical logistics market, as they require tighter controls, stronger validation, and more robust exception management than ambient generics. Pharmaceutical cold-chain logistics costs in China reached CNY 26.78 billion (USD 3.79 billion) in 2025, while cold storage capacity rose 5.43% to 4.525 million cubic meters, a faster rate than growth in ambient warehousing. The technical shift is even greater in the cell and gene therapy lanes, where transport can shift from the established 2 °C to 8 °C range toward cryogenic conditions of -150 °C to -196 °C for certain products. That requirement narrows the field to operators with specialized equipment, validated handling protocols, and staff training that general freight firms do not usually maintain. It also allows qualified providers to defend higher pricing than they can in ambient, procurement-led flows. In the China pharmaceutical logistics market, this pushes capital toward premium cold-chain corridors even when broader price pressure affects standard medicine distribution.

Rise of E-Commerce Pharmacies and 24-Hr Delivery Expectations

The China pharmaceutical logistics market is also being reshaped by faster retail delivery expectations and by the broader integration of online healthcare purchasing into everyday drug access. Meituan’s healthcare delivery network already connects around 250,000 pharmacies nationwide and reports an average delivery time of 22 minutes, which shows how quickly consumer expectations have shifted in urban markets. In April 2026, Taobao Shangou and Jointown Pharmaceutical Group launched an integrated warehouse system for instant healthcare retail in 12 cities, including cold-chain delivery for insulin and diagnostic reagents. This changes the service model from periodic replenishment toward rapid, distributed fulfillment supported by smaller validated nodes close to demand centers. Traditional hub-and-spoke operators are less well-positioned for that model because their networks were built around batch movement into hospitals and conventional pharmacy channels. The China pharmaceutical logistics market, therefore, has a growing opening for operators that combine pharmacy connectivity, real-time inventory visibility, and compliant last-mile cold delivery.

Stricter GDP Audit and Licensing Enforcement

Stricter GDP enforcement is raising the compliance bar across the China pharmaceutical logistics market and is accelerating the removal of operators that relied on uneven provincial licensing standards[2]“Trends and Disparity in the Provision and Consumption of Essential Medicines in China,” Frontiers in Public Health, frontiersin.org. FRONTIERSIN.ORG. The March 2026 NMPA guidance sets a harmonized national direction, which matters because certification and system integration now play a bigger role in market access and contract eligibility. Multinational operators are responding with targeted investment, as Nippon Express China secured GDP certification for its Shanghai and Lianyungang facilities in early 2025. FedEx also received IATA CEIV Pharma Corporate Certification for its Guangzhou Baiyun International Airport hub in June 2025, which strengthens its standing in biopharma handling and regulated cross-border movement. In practical terms, certification is no longer just a technical requirement, because it supports pricing power on sensitive lanes and narrows the pool of logistics partners that pharmaceutical companies can approve. That is concentrating more contract volume with verified providers across the China pharmaceutical logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented rural last-mile infrastructure | -0.4% | Northwest, Southwest, Northeast, and rural Central | Long term (≥ 4 years) |

| Escalating cold-chain energy costs under carbon caps | -0.3% | National, with the strongest pressure in East and South | Medium term (2-4 years) |

| Dry-ice supply rules for MRNA Vaccines | -0.2% | East and South manufacturing clusters | Short term (≤ 2 years) |

| Urban hospital traffic-control delivery curfews | -0.2% | North, East, and South tier-1 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Rural Last-Mile Infrastructure

Rural last-mile weakness remains one of the clearest operating limits in the China pharmaceutical logistics market. China’s pharmaceutical vehicle fleet reached 46,416 units in 2025, but investment still clustered around stronger urban corridors, which left lower-tier markets with thinner certified capacity and less route redundancy. That imbalance matters more in western and mountainous provinces, where road-only delivery can conflict with temperature stability windows and time-sensitive replenishment needs. A 2025 Frontiers in Public Health study also showed that access to essential medicines still varies across regions, with socio-economic conditions continuing to shape actual availability despite broad policy efforts. Providers serving centralized procurement contracts in rural areas often face underpriced last-mile costs, which reduces the funds available for asset upgrades and service expansion. Drone pilots in Hainan, Yunnan, Xinjiang, and Chongqing show that the constraint can be reduced, but the China pharmaceutical logistics market still lacks broad commercial coverage in many difficult inland routes.

Escalating Cold-Chain Energy Costs Under Carbon Caps

Energy cost pressure is a second structural restraint for the China pharmaceutical logistics market because compliant refrigeration is both electricity-intensive and difficult to scale cheaply in weaker margin environments. The broader policy backdrop is becoming firmer, as the OECD reported that China’s expanding carbon pricing framework would raise the share of emissions covered by pricing mechanisms to 34%[3]“Effective Carbon Rates 2025,” OECD Publications, oecd.org. OECD.ORG. That direction matters because cold storage and refrigerated transport cannot easily reduce energy use without capital spending on more efficient systems and controls. Operators with stronger balance sheets can invest in greener equipment and absorb the payback period, but mid-tier firms are less able to do so while procurement pressure continues to limit pricing on conventional flows. This favors larger players and adds to consolidation pressure over time. In the China pharmaceutical logistics market, the issue is not only cost inflation; it also affects where new cold-chain capacity is built and how quickly inland networks can be upgraded.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Transportation Commands Scale While Value-Added Services Lead Growth

Transportation held 52.46% of the China pharmaceutical logistics market share in 2025, making it the largest functional segment across the operating chain. The segment’s scale reflects the central role of road movement in intercity transfers, urban replenishment, hospital delivery, and pharmacy restocking. Air freight remains relevant for urgent biologics, high-value samples, and selected clinical shipments where speed and temperature control matter more than cost. Inland waterway and sea transport still support bulk ambient flows in selected corridors where delivery windows are less strict, and unit economics favor larger-volume movement. Total warehousing capacity reached 93.816 million cubic meters in 2025, which shows that the transport layer continues to work in close coordination with a large national storage base.

The second half of this segment tells a different story, because value-added services are forecast to grow at a 7.74% CAGR through 2031 and are now becoming central to differentiation. Pharmaceutical manufacturers increasingly want third parties to handle serialization, GDP-compliant temperature monitoring, DTP pharmacy fulfillment, and cold-chain-as-a-service instead of building those capabilities alone. That shift changes the economics of the China pharmaceutical logistics industry, because margins move away from pure transport yield and toward compliance-heavy service overlays. SF Holding’s formal creation of a supply chain business group for life sciences and pharmaceuticals in late 2025 reflects that repositioning and helped drive more than 20% revenue growth in the vertical. Warehousing and distribution therefore remain important as a stable middle layer, but growth is increasingly tied to digital integration, validated handling, and outsourced service depth rather than storage space alone.

By Mode of Operation: Cold-Chain Holds the Premium Position

Cold-chain logistics accounted for 57.36% of the China pharmaceutical logistics market size in 2025 and is projected to grow at a 6.91% CAGR through 2031, making it both the largest and fastest-growing operating mode. This dual position shows how the China pharmaceutical logistics market is separating into a premium compliance-led tier and a larger but lower-yield ambient tier. Cold storage capacity expanded to 4.525 million cubic meters in 2025, while the cold-chain vehicle fleet reached 16,175 units, which still left specialized transport capacity well below the level implied by demand for sensitive products. The gap matters because biologics, vaccines, and advanced therapies need validated equipment, traceability, and response systems that general fleet operators cannot easily provide. It also supports stronger pricing for operators that already meet those requirements.

Non-cold-chain logistics still carry a large volume base, especially in centralized procurement flows for ambient generics and routine prescription distribution. That part of the China pharmaceutical logistics industry benefits from steady throughput and route density, but it faces weaker yield because volume-based procurement compresses distributor economics. A 2026 Frontiers in Pharmacology study showed that national centralized drug procurement creates broad availability mandates across provinces with different levels of development, which keeps ambient distribution relevant nationwide. Even so, operators in non-cold-chain lanes increasingly need to add monitoring, visibility, and compliance services if they want to defend margins. The resulting split is clear, because ambient scale remains necessary, but capital and strategic attention in the China pharmaceutical logistics market are moving more decisively toward cold-chain capability.

By Product Type: Prescription Drugs Provide Base Volume While Cell and Gene Therapies Expand Fastest

Prescription drugs accounted for 40.92% of the China pharmaceutical logistics market size in 2025, supported by hospital-centered dispensing patterns and the continued dominance of institutional channels in medicine distribution. This segment provides a large, recurring base load for the China pharmaceutical logistics market, helping established distributors maintain route density and warehouse utilization. The flow is especially important for operators with longstanding hospital relationships and broad geographic coverage. OTC medicines also matter, particularly as e-commerce pharmacies and same-city delivery are enabling faster replenishment cycles for household health products. Biologics and biosimilars add another important layer, because their handling needs are closely tied to the expansion of validated cold-chain infrastructure across the country.

Cell and gene therapies are forecast to grow at a 8.05% CAGR through 2031, making them the fastest-growing product category in the report. Their importance exceeds their current volume because they affect custody rules, packaging standards, identity controls, and temperature requirements across the entire supply chain. The China pharmaceutical logistics market therefore needs more than additional refrigerated capacity, because these therapies depend on chain-of-identity handling and continuous monitoring across collection, manufacturing return, and patient delivery. Clinical trial materials are also expanding in parallel as China deepens its role in regulated multinational research flows. Medical devices and diagnostics benefit from the same GDP-compliant storage and hospital supply processing trends, while veterinary medicines continue to grow on the back of more conventional ambient distribution networks.

Geography Analysis

The East region accounted for 29.20% of the China pharmaceutical logistics market size in 2025, and that leadership rests on the Yangtze River Delta’s combined strength in pharmaceutical manufacturing, hospital demand, air cargo access, and GDP-compliant cold storage. Shanghai, Jiangsu, and Zhejiang continue to host some of the country’s most advanced bonded and temperature-controlled logistics assets. Novo Nordisk’s hub in Shanghai’s Pudong Airport Comprehensive Bonded Zone became fully operational in 2025, featuring multi-temperature storage, humidity control, and automation, which reflects the region’s role as a benchmark for high-standard pharmaceutical logistics[4]“Novo Nordisk Unveils Logistics Hub in Shanghai,” CIIE 2025, english.shanghai.gov.cn. ENGLISH.SHANGHAI.GOV.CN. The South region, led by Guangdong, complements the East by serving as a major international corridor for biologics and other regulated healthcare flows. FedEx’s CEIV Pharma-certified Guangzhou hub and KLN’s exclusive 4PL arrangement for Teva in the Greater Bay Area both show how the southern corridor is becoming more specialized and more outsourced.

The North region remains important because Beijing, Tianjin, and Hebei combine hospital density, policy visibility, and institutional procurement volume. Beijing’s 2026 traffic governance measures around 22 major hospitals are reshaping delivery schedules and vehicle planning, which is pushing distributors toward smaller loads, more precise appointment systems, and greater use of night delivery windows. The Central region is gaining strategic importance as a link between stronger coastal clusters and inland demand zones. The Northeast still serves meaningful hospital demand, but the region faces a harder path in building logistics momentum because demographic outflow and weaker manufacturing weight reduce the pace of new investment.

The Southwest and Northwest represent the most consequential long-term frontier for the China pharmaceutical logistics market. The Southwest is forecast to grow at 6.29% CAGR through 2031, supported by public infrastructure spending, rising inland pharmaceutical production, and more active drone-based route testing. Chongqing’s emergency medicine drone route, launched in March 2025, reduced a 45-minute road journey to 26 minutes, while Yunnan’s commercial drone flight in March 2026 cut a much longer mountain route to 27 minutes. The Northwest still faces the steepest last-mile challenge, yet Xinjiang’s Tianyi Low-Altitude Logistics Operation Center and Xi’an’s drone delivery route show how the region is testing new operating models for medical distribution. These moves do not remove the structural gap immediately, but they improve the operating case for more reliable pharmaceutical service in difficult terrain. Over time, this means geographic growth in the China pharmaceutical logistics market will depend not only on demand density, but also on how well new transport formats are integrated into compliant regional networks.

Competitive Landscape

The China pharmaceutical logistics market remains semi-consolidated at the top, with state-backed distributors still holding the strongest positions in hospital and institutional channels through long-established distribution and warehousing systems. Their advantage comes from route density, procurement relationships, broad inventory reach, and established compliance processes rather than from speed alone. This top-tier structure still matters because the hospital channel remains central to the flow of prescription medicines in China. At the same time, the China pharmaceutical logistics market is becoming more competitive in the faster-growing lanes for biologics, same-day fulfillment, and value-added services. That shift is weakening the old assumption that scale in conventional hospital distribution is enough to protect margins across all logistics functions.

Technology-native operators are using a different playbook. SF Holding has been building a more focused life sciences and pharmaceutical offering, and its 2025 annual results highlighted more than 20% revenue growth in that vertical after the formal setup of a dedicated supply chain business group. JD Logistics is also part of this competitive shift through healthcare fulfillment and fast delivery infrastructure, even though the strongest publicly cited operating examples in the supplied material center more on channel expansion than on certified pharmaceutical asset ownership. In the China pharmaceutical logistics market, these companies compete by using digital forecasting, distributed fulfillment, and tighter customer interface rather than by relying only on the legacy distributor model. The result is a two-track landscape where incumbents defend broad institutional flows and newer platforms capture share where convenience, visibility, and cold-chain responsiveness matter more.

Multinational operators remain important in cross-border pharmaceutical corridors, clinical trial logistics, and certified handling for sensitive products. FedEx strengthened its position in China with CEIV Pharma certification for Guangzhou in 2025, while Nippon Express China secured GDP certification for facilities in Shanghai and Lianyungang, both of which signal deeper commitment to regulated pharmaceutical logistics. Another strategic move came from KLN Logistics Network, which was selected by Teva as its exclusive 4PL provider in the Greater Bay Area in March 2025, reinforcing the trend toward integrated outsourcing in high-value healthcare corridors. The April 2026 Taobao Shangou and Jointown integrated warehouse rollout is another example, because it links e-commerce pharmacy demand with compliant same-day logistics infrastructure in 12 cities. Taken together, these moves show that the China pharmaceutical logistics market is still led by scale players at the top, but its future share shifts will be decided more by compliance depth, cold-chain capability, and digital fulfillment quality than by network size alone.

China Pharmaceutical Logistics Industry Leaders

Sinopharm Logistics

China Resources Pharmaceutical Commercial

Shanghai Pharma Logistics

Jointown Pharmaceutical Group

SF Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Taobao Shangou and Jointown Pharmaceutical Group launched China's first integrated warehouse system for instant healthcare retail, incorporating cold-chain delivery for temperature-sensitive products, including insulin and diagnostic reagents, across 12 cities; this positions Jointown at the intersection of pharmaceutical e-commerce and same-day cold-chain logistics, directly competing with Meituan's O2O healthcare delivery model.

- December 2025: Sinotrans established a joint venture with China Railway International Multimodal Transport Co. (a China State Railway Group subsidiary) to form Sinotrans Railway Container (Xi'an) International Logistics Co., expanding multimodal pharmaceutical and cargo connectivity from the Northwest into Central and Eastern China.

- October 2025: Novo Nordisk's warehousing and logistics center in Shanghai's Pudong Airport Comprehensive Bonded Zone became fully operational, integrating multi-temperature storage, advanced humidity monitoring, and automation for bonded and non-bonded pharmaceutical distribution, setting a new benchmark for international pharmaceutical company logistics hubs in China.

- August 2025: Northwest China's first urban drone pharmaceutical delivery route was launched in Xi'an's Baqiao District by Shaanxi Provincial Logistics Group, using a high-payload rotor drone that covers 13.5 km and reduces delivery time by over 3 times compared to ground transport, contributing to the "15-minute pharmaceutical emergency logistics circle" initiative.

China Pharmaceutical Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

| Prescription Drugs |

| OTC Drugs |

| Biologics and Biosimilars |

| Vaccines and Blood Products |

| Clinical Trail Materials |

| Cell and Gene Therapies |

| Medical Devices and Diagnostics |

| Veterinary Medicine |

| Others |

| North |

| Northeast |

| East |

| Central |

| South |

| Southwest |

| Northwest |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics and Biosimilars | ||

| Vaccines and Blood Products | ||

| Clinical Trail Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices and Diagnostics | ||

| Veterinary Medicine | ||

| Others | ||

| By Region | North | |

| Northeast | ||

| East | ||

| Central | ||

| South | ||

| Southwest | ||

| Northwest |

Key Questions Answered in the Report

What is the 2026 value of China pharmaceutical logistics?

The market value stands at USD 60.29 billion in 2026.

Which logistics function leads in China?

Transportation remained the largest function with 52.46% share in 2025, supported by its role in trunk routes, hospital supply, and urban replenishment.

Why is cold-chain so important in China’s drug supply chain?

Cold-chain held 57.36% share in 2025 and is projected to grow at 6.91% CAGR, driven by biologics, vaccines, and more demanding temperature-controlled therapies.

Which product group is growing the fastest?

Cell and gene therapies are the fastest-growing product type with an 8.05% CAGR through 2031 because they require specialized handling and cryogenic transport.

Which Chinese region is the largest and which is growing the fastest?

The East led with 29.20% share in 2025, while the Southwest is expected to post the fastest growth at 6.29% CAGR through 2031.

What is changing competition in this space?

Competition is shifting as state-backed distributors defend hospital channels while technology-led operators and certified international firms gain in cold-chain, e-commerce fulfillment, and high-compliance lanes.

Page last updated on: