Digital Twin GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.99 Billion |

| Market Size (2031) | USD 50.26 Billion |

| Growth Rate (2026 - 2031) | 48.37% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Twin GPU Market Analysis by Mordor Intelligence

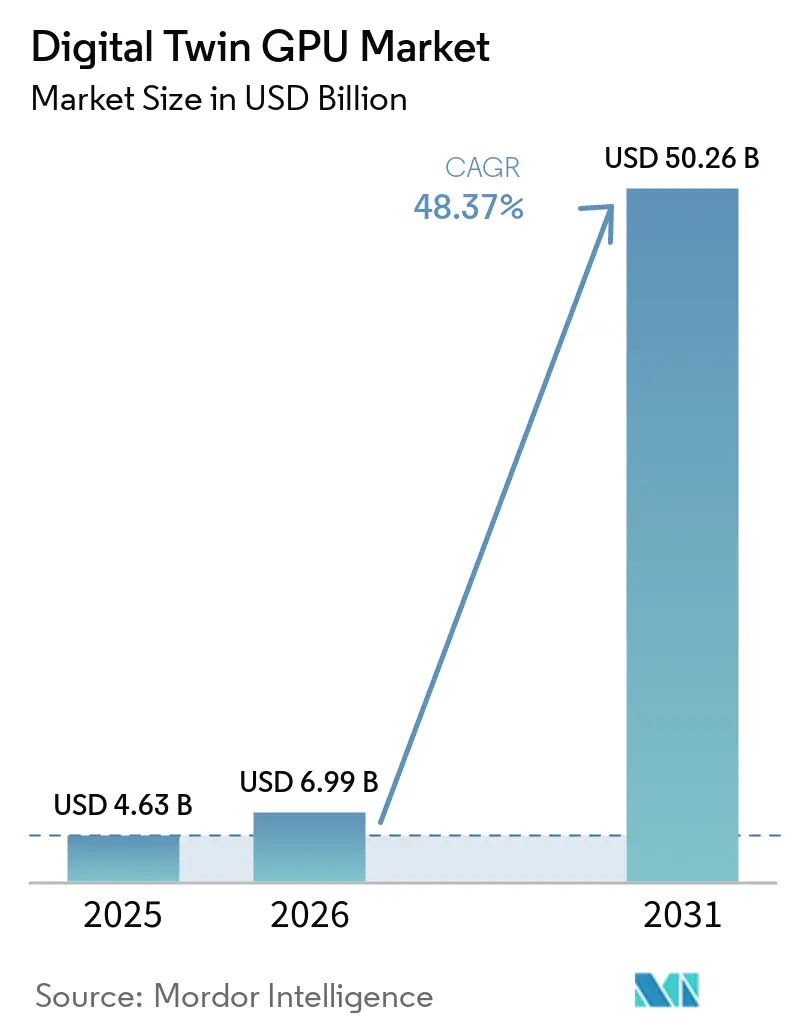

The digital twin GPU market size is projected to be USD 4.63 billion in 2025, USD 6.99 billion in 2026, and reach USD 50.26 billion by 2031, growing at a CAGR of 48.37% from 2026 to 2031. The pace of expansion reflects the way physics-based simulation, live operational data, and AI model development are moving into the same computing stack across large industrial environments. The digital twin GPU market is no longer being shaped by a single use case, because enterprises now use the same GPU foundation for design validation, synthetic data generation, robotics training, and operational monitoring. Large capital programs in AI factories, smart manufacturing, and connected assets are pushing GPU-backed twin environments from optional engineering tools into core digital infrastructure. The digital twin GPU market is also benefiting from parallel deployment strategies, with enterprises keeping latency-sensitive workloads on local systems while shifting burst simulation and training runs to cloud GPU pools. Competitive behavior shows a mix of concentration and fragmentation, with the digital twin GPU market centered around a small set of GPU platform leaders while simulation software, integration services, and domain applications remain spread across a broader vendor base.

Key Report Takeaways

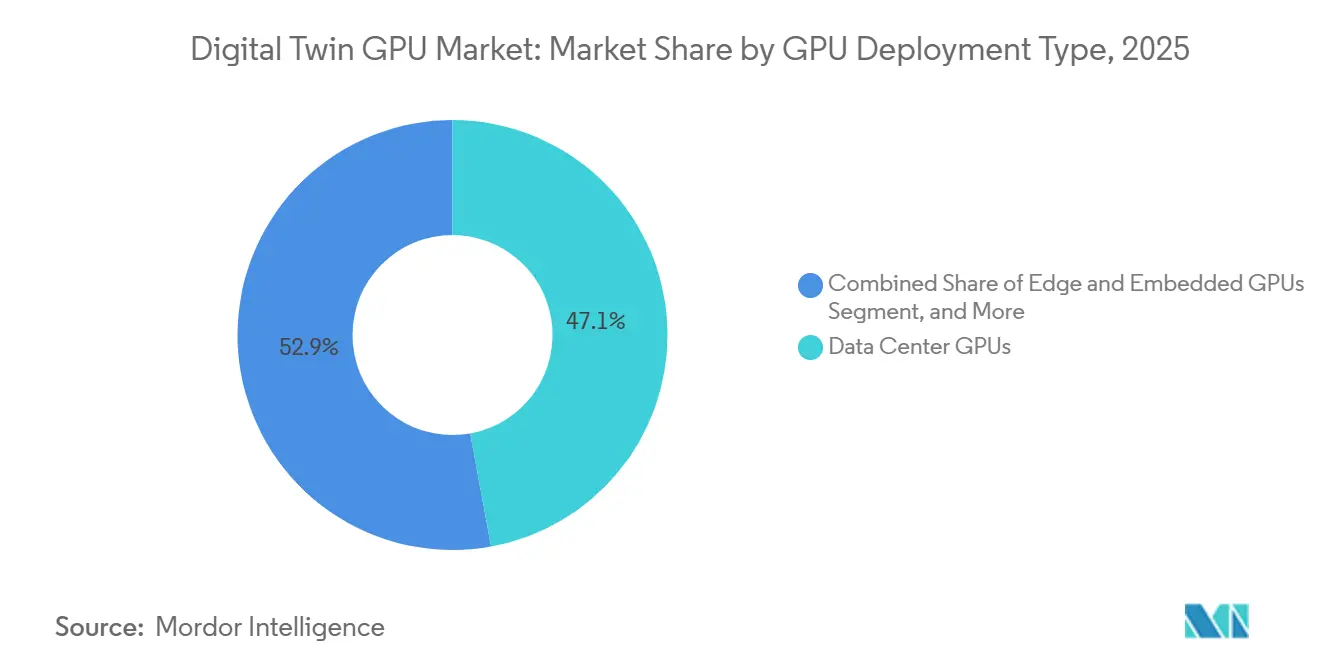

- By GPU deployment type, data center GPUs held 47.14% share of the digital twin GPU market in 2025, while edge and embedded GPUs are projected to expand at a 48.99% CAGR through 2031.

- By GPU integration type, discrete GPUs accounted for 75.33% of the digital twin GPU market size in 2025, while integrated and embedded GPUs are expected to grow at a 49.04% CAGR through 2031.

- By deployment model, on-premises captured 48.78% of the segment in 2025, while cloud deployment is projected to advance at a 49.16% CAGR through 2031.

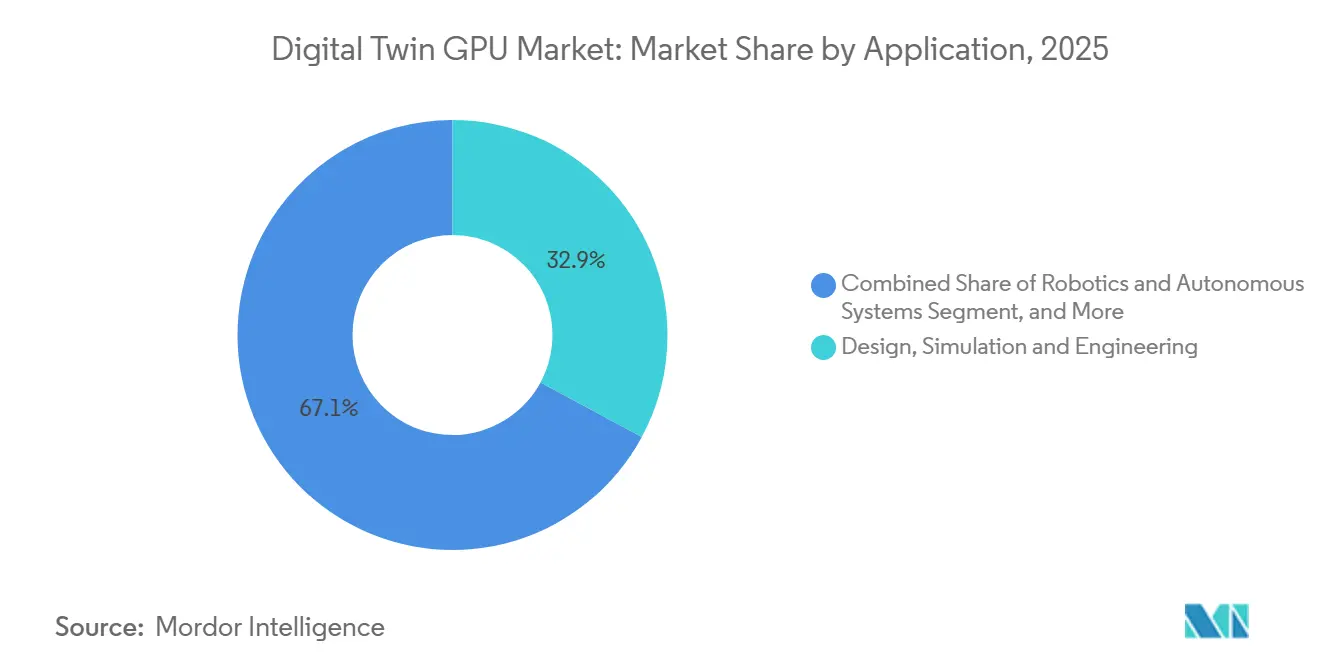

- By application, design, simulation, and engineering represented 32.86% share in 2025, while robotics and autonomous systems is forecast to expand at a 49.24% CAGR through 2031.

- By end user, manufacturing held 33.66% of the digital twin GPU market share in 2025, while healthcare and life sciences is projected to record a 49.22% CAGR through 2031.

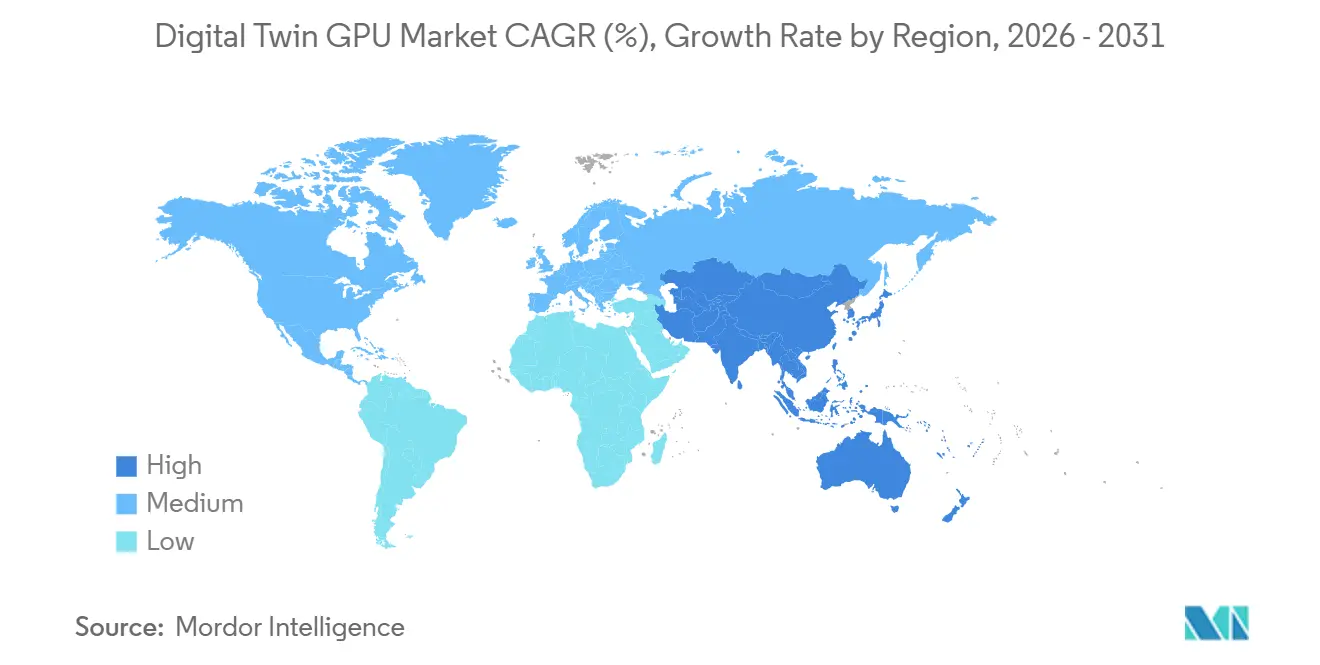

- By geography, North America held 36.16% of the digital twin GPU market share in 2025, while Asia-Pacific is expected to grow at a 49.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Twin GPU Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Industrial AI and Simulation-Heavy Workloads | +11.8% | Global, with core concentration in North America, Germany, Japan, and South Korea | Short term (≤ 2 years) |

| Rising Adoption of GPU-Accelerated Digital Twin Workflows in Manufacturing | +10.2% | North America, Germany, Japan, South Korea, and China | Short term (≤ 2 years) |

| Need for Faster Virtual Commissioning and Design Iteration Cycles | +8.5% | North America and EU, automotive, aerospace, and heavy machinery sectors | Medium term (2-4 years) |

| Growing Use of Real-Time Physics-Based Rendering and 3D Visualization | +6.8% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Shift Toward Cloud and Hybrid GPU Infrastructure for Twin Execution | +4.5% | Global, with North America leading cloud adoption, APAC core accelerating | Medium term (2-4 years) |

| Rising Demand for Edge AI Inference in Connected Asset Environments | +3.0% | APAC core, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion Of Industrial AI And Simulation-Heavy Workloads

Industrial AI deployments have changed the compute profile of digital twin platforms because workloads now run as continuous, physics-aware pipelines instead of occasional batch simulations. NVIDIA introduced the Omniverse DSX Blueprint in October 2025 to support the design and operation of gigawatt-scale AI factories, which showed that digital twin environments are moving into far larger compute footprints than many industrial teams planned for earlier in the cycle.[1]NVIDIA, “NVIDIA Launches Omniverse DSX Blueprint, Enabling Global AI Infrastructure Ecosystem to Build Gigawatt-Scale AI Factories,” NVIDIA Blog, blogs.nvidia.com The June 2025 launch of an industrial AI cloud in Germany, built around 10,000 GPUs for European manufacturing use cases, reinforced the same point, with simulation, robotics, and factory digital twins all tied to high-throughput GPU infrastructure. In the digital twin GPU market, that matters because each additional simulation pass improves synthetic data quality, and better synthetic data supports stronger model performance in the next cycle. The result is a self-reinforcing investment pattern in which simulation demand, AI model refinement, and twin fidelity continue to pull GPU demand higher. This is one of the clearest reasons the digital twin GPU market is expanding faster than a simple hardware replacement cycle would suggest.

Rising Adoption Of GPU-Accelerated Digital Twin Workflows In Manufacturing

Manufacturing operators are embedding GPU-backed simulation into day-to-day production planning, which shifts digital twins from engineering support tools into operating systems for factory decisions. Siemens introduced Digital Twin Composer in January 2026 with NVIDIA Omniverse libraries, and the launch highlighted plant-scale twins with physics-level accuracy for production planning and facility change validation. Siemens and NVIDIA also expanded their partnership in January 2026 around an industrial AI operating system, with a commitment to complete GPU acceleration across Siemens' simulation portfolio and with early customer interest already visible across large industrial groups. In the digital twin GPU market, manufacturing does more than contribute the largest end-user share, because it also acts as the earliest large-scale proving ground for GPU-native simulation workflows that later spread into other sectors. This shift is visible in the way software portfolios are being rebuilt around GPU-native paths rather than adapted from CPU-first environments. It also explains why the digital twin GPU market continues to deepen inside factory planning, throughput optimization, and line redesign programs.

Need For Faster Virtual Commissioning And Design Iteration Cycles

Virtual commissioning has compressed development timelines by moving system validation into simulated environments before equipment is physically installed. Rockwell Automation showcased Emulate3D Factory Test at NVIDIA GTC 2025, using NVIDIA Omniverse APIs and OpenUSD so engineers could run factory acceptance testing in a virtual setting before deployment.[2]Rockwell Automation, “Rockwell Automation Showcases Emulate3D Factory Test for the First Time at NVIDIA GTC 2025,” Rockwell Automation, rockwellautomation.com Rockwell also demonstrated AI-orchestrated factory engineering with Microsoft at Hannover Messe 2026, which showed how emulation, orchestration logic, and cloud workflows are being linked more tightly than before.[3]Rockwell Automation, “Rockwell Automation Demonstrates AI-Orchestrated Factory Engineering with Microsoft at Hannover Messe 2026,” Rockwell Automation, rockwellautomation.com In the digital twin GPU market, the important shift is that validation work is moving upstream into the design and procurement stage, which makes GPU infrastructure part of planned plant spending rather than an afterthought. Engineering teams using simulation-first commissioning can test far more design variants within the same project window than CPU-based workflows usually allow. That makes faster iteration one of the most direct demand drivers in the digital twin GPU market.

Growing Use Of Real-Time Physics-Based Rendering And 3D Visualization

Real-time physics-based rendering is becoming a standard operating layer for digital twins, not a premium feature reserved for visual presentation. Synopsys released Ansys 2026 R1 with a GPU-accelerated multispectral light propagation engine in Ansys AVxcelerate Sensors and with broader NVIDIA Omniverse integration for a more unified 3D digital twin workflow. Siemens and NVIDIA also expanded their work in June 2025 around Teamcenter Digital Reality Viewer, which brought real-time ray tracing and physics-based digital twin visualization deeper into PLM environments. In the digital twin GPU market, this changes the role of visualization because photorealistic rendering is increasingly being used inside engineering review and decision loops rather than after those decisions are already complete. That shift raises both compute intensity and session frequency across product development, layout review, and immersive collaboration use cases. It also supports wider adoption of the digital twin GPU market in sectors where design fidelity and operational realism directly affect approval, safety, and deployment speed.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of High-Memory GPU Infrastructure and Cooling | -3.5% | Global, most acute in emerging APAC markets, South America, and Middle East and Africa | Short term (≤ 2 years) |

| Interoperability Gaps Across PLM, CAE, IoT, and Twin Platforms | -2.2% | Global, most pronounced in APAC and Rest of World | Medium term (2-4 years) |

| Cybersecurity and Data Sovereignty Concerns in Connected Twin Environments | -1.2% | Global, heightened regulatory influence in EU and North America | Medium term (2-4 years) |

| Shortage of Domain Talent for Physics-Based Model Calibration | -0.8% | Global, most acute in emerging markets and specialized aerospace and defense applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost Of High-Memory GPU Infrastructure And Cooling

High-memory GPUs designed for simulation-heavy workloads remain expensive for many operators, especially when those deployments must support rendering, AI inference, and live sensor fusion at the same time. The cost burden extends well beyond the chip, because sustained twin execution also requires specialized cooling, high-bandwidth interconnects, and power infrastructure that many facilities were not designed to carry. AWS made Amazon EC2 G7 instances generally available in June 2026 with NVIDIA RTX PRO 4500 Blackwell Server Edition GPUs, and the offering showed strong performance gains, but it also underlined that high-end GPU access still requires scale and clear workload economics. In the digital twin GPU market, thermal management is a particularly serious barrier because continuous simulation creates a cooling profile that differs from narrower burst inference patterns. Smaller manufacturers and asset operators therefore face a harder adoption path than large enterprises with existing data center capacity or flexible cloud budgets. Until leasing, shared pools, and as-a-service options align better with this workload pattern, cost will remain a meaningful brake on the digital twin GPU market.

Interoperability Gaps Across PLM, CAE, IoT, And Twin Platforms

Digital twin deployments often run across separate software estates, which means product data, simulation models, sensor streams, and visualization layers do not always connect cleanly. PTC showed one route toward tighter integration through its work linking Windchill PLM with NVIDIA Omniverse libraries, which support workflows that connect managed product data with GPU-powered simulation environments. The broader challenge is that many engineering processes were built for file exchange across standalone tools, while live operational twins require streaming data and two-way synchronization across systems. In the digital twin GPU market, this gap slows deployment timelines, raises implementation cost, and keeps some twin programs limited to isolated engineering use cases rather than broad operational rollouts. OpenUSD is helping design and visualization tools move toward a shared structure, but the same standardization is still incomplete at the operational technology layer. Until that gap narrows, the digital twin GPU market will continue to face adoption friction in environments that depend on deep integration across PLM, CAE, IoT, control systems, and historian platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Deployment Type: Data Centers Lead While Edge Architectures Gain Ground

Data center GPUs held 47.14% of this segment in 2025, which kept them at the center of the digital twin GPU market size because the largest simulation workloads still require centralized, high-memory, high-bandwidth infrastructure. Those environments remain the preferred location for aerodynamic modeling, large model training, generative twin design, and synthetic data generation at production scale. Workstation GPUs continue to serve engineers and simulation teams that need local compute for interactive exploration, validation, and visual review before a model is moved into broader production environments. Edge and embedded GPUs are projected to expand at a 48.99% CAGR through 2031, which reflects the way real-time asset monitoring and operational inference are moving closer to machines, vehicles, and plant-floor systems. The digital twin GPU market is therefore developing as a layered architecture rather than a winner-take-all deployment pattern.

The same segment is also showing a budget shift from centralized infrastructure spending toward distributed operational technology spending, especially in factories and asset-heavy facilities where local decision speed matters. In the digital twin GPU industry, that shift is most visible in automotive, semiconductor, and smart infrastructure programs that evaluate compute return at the machine or asset level instead of only at the enterprise platform level. SK Telecom applied NVIDIA Omniverse libraries to build digital twins of SK Hynix semiconductor fabs in June 2026, which illustrated how centralized fab simulation and distributed data streams are increasingly being handled in the same architecture. Data center GPUs still anchor the largest production environments, but edge deployments are expanding because many operating teams now want inference and monitoring at the point where conditions change in real time. This balance is likely to keep both centralized and distributed GPU demand active across the digital twin GPU market through the forecast period.

By GPU Integration Type: Discrete GPUs Anchor Performance While Embedded Options Accelerate

Discrete GPUs accounted for 75.33% of the segment in 2025, which gave them the leading position in the digital twin GPU market size because high-fidelity simulation and live 3D rendering still depend on memory capacity and parallel compute density. Those workloads include physics-heavy simulation, low-latency visualization, and operational models that must run without wide tolerance for delay. Integrated and embedded GPUs are projected to grow at a 49.04% CAGR through 2031, which reflects stronger adoption of GPU capability inside industrial edge devices, ruggedized modules, and purpose-built automation hardware. The digital twin GPU market is seeing this shift most clearly in jurisdictions that are prioritizing local data handling and on-premises inferencing for regulated or sensitive industrial environments. That keeps discrete GPUs dominant today while giving embedded options a stronger growth path through the forecast period.

The competitive logic in this segment also rests on software maturity, because many simulation libraries have been optimized first for discrete GPU architectures. NVIDIA's CUDA-X, PhysicsNeMo, and Omniverse libraries continue to reinforce that installed base, which supports the leading role of discrete GPUs in high-end twin execution. At the same time, ABB Robotics built RobotStudio HyperReality on NVIDIA Omniverse with availability planned for the second half of 2026, and the platform points to stronger embedded simulation fidelity with reported 99% correlation between virtual and physical behavior. In the digital twin GPU industry, that matters because edge-resident systems are no longer limited to low-fidelity visualization or narrow inferencing tasks. As embedded software stacks improve, more monitoring and localized optimization workloads can move away from centralized compute without losing too much realism. This leaves the digital twin GPU market with a dual path in which discrete GPUs retain the performance center while embedded GPUs extend the addressable footprint.

By Deployment Model: On-Premises Retains Scale While Cloud Expands Fastest

On-premises deployment held 48.78% of the segment in 2025, which reflected the fact that many operators still need local infrastructure for latency-sensitive twin execution and regulated operational data flows. Manufacturing and process sectors continue to prefer local deployments where PLC, SCADA, and proprietary system integration are tightly linked to day-to-day operations. Cloud deployment is projected to rise at a 49.16% CAGR through 2031, and that growth shows how enterprises are using external GPU pools for burst simulation, synthetic data generation, and temporary scaling that would be inefficient to provision permanently. In the digital twin GPU market, this keeps cloud attractive for variable workloads while preserving local infrastructure for control-critical functions. The hybrid model sits between these two choices and is increasingly becoming the practical operating pattern for larger industrial groups.

AWS and NVIDIA announced in 2026 that more than 1 million NVIDIA GPUs would be deployed across AWS regions, which materially expanded cloud-side GPU availability for enterprises that need elastic simulation capacity. Microsoft also deepened integration between Microsoft Fabric and NVIDIA Omniverse libraries in March 2026, which creates a cleaner route for enterprise data to feed physically accurate twin environments on cloud infrastructure. Oracle added ready-to-deploy digital twin solutions that combine NVIDIA L40S GPUs with operational optimization services, which showed how cloud providers are packaging these environments for actual industrial use rather than generic compute access. In the digital twin GPU market, hybrid adoption is growing because it lets companies keep control systems and sensitive telemetry close to operations while shifting compute-heavy exploration to external GPU capacity. That operating split is now one of the clearest structural patterns across the digital twin GPU market.

By Application: Design And Simulation Lead While Robotics Advances Rapidly

Design, simulation, and engineering accounted for 32.86% of the application segment in 2025, which kept this use case at the core of the digital twin GPU market size because it remains the original and broadest reason enterprises deploy high-performance twin environments. Engineers continue to rely on these workflows to evaluate geometry, materials, and system behavior before physical prototypes or facility changes are approved. Robotics and autonomous systems is forecast to grow at a 49.24% CAGR through 2031, which reflects the need for large volumes of physics-accurate simulation to train policies, test robot behavior, and validate edge cases before live deployment. Virtual commissioning and factory planning are also expanding, particularly where operators want to validate layout, sequencing, and automation logic before capital is committed. This mix keeps design-led demand large while pushing robotics toward a stronger growth role in the digital twin GPU market.

Rockwell Automation launched FactoryTalk Orchestration in June 2026 and tied it to Emulate3D digital twin software, which showed how simulation-validated orchestration is being pushed into real operating workflows rather than left inside engineering teams alone. Siemens Digital Twin Composer also illustrates how photorealistic and physics-accurate scenes are being used in collaborative reviews, which makes visualization itself a recurring source of GPU demand rather than a one-time design step. Predictive maintenance and asset optimization are becoming more GPU intensive as physics-informed models replace simpler threshold-based alerts and require continuous synchronization with live sensor data. Real-time monitoring, operations control, and immersive collaboration therefore remain relevant application areas even when they do not lead by share or CAGR. The digital twin GPU market is expanding across applications because each step from design to deployment now depends more directly on simulation fidelity and rendering speed.

By End User: Manufacturing Anchors Demand While Healthcare Broadens Adoption

Manufacturing held 33.66% of the end-user segment in 2025, which made it the leading source of digital twin GPU market share because automotive, electronics, and semiconductor operations combine high simulation complexity with strong pressure on cycle time. These environments use GPU-backed twins for plant layout planning, throughput tuning, robotic workflow testing, and process change validation before physical execution begins. Healthcare and life sciences are forecast to grow at a 49.22% CAGR through 2031, which reflects rising use of surgical robotics, patient-specific simulation, and AI-assisted diagnostic workflows. In the digital twin GPU market, this is an important shift because growth is moving beyond factory optimization into safety-critical and patient-centered use cases. The result is a wider adoption base for the digital twin GPU market, even though manufacturing remains the main volume anchor.

L&T Technology Services launched an AI-powered lung digital twin platform in March 2026 on NVIDIA AI infrastructure, which turned static CT scans into dynamic simulation-ready lung models for planning and navigation use cases. NVIDIA, Foxconn, and Taiwan medical centers also used Omniverse-powered hospital digital twins in June 2026 to test and validate robotic systems before physical deployment, with reported gains in deployment time and navigation accuracy. Outside these areas, automotive and transportation, aerospace and defense, energy and utilities, oil and gas, IT and telecom, and smart infrastructure each bring different simulation intensity and regulatory requirements. BMW's use of NVIDIA Omniverse libraries for full-scale plant twin development also shows how product development and operational planning can converge inside the same GPU-enabled environment. That breadth keeps manufacturing in the lead while steadily widening the end-user reach of the digital twin GPU market.

Geography Analysis

North America held 36.16% of the digital twin GPU market size in 2025, which kept it in the lead because the region combines GPU platform development, hyperscaler infrastructure, and a deep base of industrial software vendors. The United States anchors this position through adoption across automotive, aerospace, semiconductor, and defense environments where simulation intensity is high and compute budgets are established. Canada and Mexico support regional depth through automotive manufacturing networks and supply chains that are steadily integrating digital twin workflows at the tier-1 level. AWS expanded this position further through its plan to deploy more than 1 million NVIDIA GPUs across AWS regions, with early concentration in major U.S. regions that industrial users can access for burst workloads. Microsoft also open-sourced its Azure Physical AI Toolchain in March 2026, which gave North American operators a more standardized route to physically accurate cloud-connected twins.

Europe remains a major part of the digital twin GPU market because its industrial base is strong and its regulatory environment is pushing many operators toward controlled deployment models. Germany accounts for a disproportionate share of activity, supported by the industrial AI cloud announced in June 2025 and by Siemens' use of Erlangen as a blueprint for AI-driven adaptive manufacturing. The United Kingdom and France remain secondary growth pockets, with demand linked to engineering services, aerospace, and defense simulation. Across the region, cybersecurity and data residency requirements are shaping the timing and structure of deployments as much as raw demand is shaping them.

Asia-Pacific is projected to advance at a 49.07% CAGR through 2031, which makes it the fastest-growing regional block in the digital twin GPU market. Semiconductor fab digitalization in South Korea and Taiwan, smart manufacturing programs in China, Japan, and India, and a broader wave of AI infrastructure spending are all pushing demand higher. SK Telecom and SK Hynix demonstrated fab-focused digital twins with NVIDIA Omniverse libraries in June 2026, which showed how semiconductor operations are becoming one of the most compute-intensive adopters in the region. Micron and MetAI also advanced simulation-ready fab twins on NVIDIA Omniverse in June 2026, adding more evidence that high-value manufacturing environments are shaping regional momentum. China is scaling through domestic AI infrastructure and industrial automation, Japan is driven by robotics and precision manufacturing, and South Korea is anchored by semiconductor and battery production. India is emerging through IT-led integration capability, while South America and Middle East and Africa are expanding from a smaller base with early demand centered on energy and utilities.

Competitive Landscape

The digital twin GPU market is moderately concentrated at the GPU platform tier, because a limited number of compute and software stack providers shape the core runtime environment for simulation-heavy twin execution. NVIDIA holds a central role through CUDA-X, PhysicsNeMo, and Omniverse libraries, while the broader field remains fragmented across simulation software, PLM integration, cloud delivery, and sector-specific applications. This means the digital twin GPU market has clear platform leaders, but it does not operate as a closed market because many value layers are still open to specialists, integrators, and software partners. Cross-vendor collaboration is therefore one of the main competitive tools, especially where interoperability and enterprise adoption still depend on partner ecosystems. OpenUSD continues to matter in that setting because it supports a common structure for exchange across visualization and design workflows, which helps vendors build around shared frameworks instead of isolated stacks.

Several strategic moves in 2025 and 2026 show how companies are trying to widen their position inside the digital twin GPU market. Siemens and NVIDIA expanded their partnership in January 2026 to accelerate GPU support across Siemens' simulation portfolio and to move toward an industrial AI operating system for manufacturing workflows. Rockwell Automation launched FactoryTalk Orchestration in June 2026 and tied it to Emulate3D to strengthen simulation-validated deployment and factory orchestration. Microsoft deepened Azure and Omniverse integration in March 2026, which supports a cleaner route from enterprise data systems into physically accurate digital twin environments. AWS expanded available GPU capacity through new instances and a broader NVIDIA deployment plan, which helps cloud providers compete not just on raw compute but also on access speed and scalability.

White space remains strongest in midmarket-accessible toolchains and in vertical-specific models where general factory platforms do not yet address sector detail well enough. Healthcare robotics, smart building management, and energy asset optimization remain notable areas where domain-specific modeling depth can still differentiate new entrants. NVIDIA's Factory Operations Blueprint release at Computex 2026 also showed that agentic AI is becoming a new competitive layer, because vendors now want twins that can optimize and extend workflows instead of only visualizing them. That direction raises the importance of ecosystem control, software libraries, and integration depth, not only hardware performance alone. The digital twin GPU market therefore combines concentrated control in the platform layer with open competition across implementation, domain logic, and application packaging.

Digital Twin GPU Industry Leaders

NVIDIA Corporation

Siemens AG

Dassault Systèmes SE

Ansys, Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Rockwell Automation launched FactoryTalk Orchestration software at the Automate show in Chicago on June 22, 2026. The platform coordinates material flow and production processes end-to-end, integrating with Emulate3D digital twin software to provide simulation-validated orchestration before physical deployment, directly addressing the commissioning validation gap for GPU digital twin adopters.

- June 2026: AWS announced general availability of Amazon EC2 G7 instances on June 18, 2026, powered by NVIDIA RTX PRO 4500 Blackwell Server Edition GPUs with 32 GB of GPU memory per unit and up to 700 Gbps of Elastic Fabric Adapter networking bandwidth. G7 instances deliver 4.6x AI inference performance improvement over the preceding G6 generation, expanding cloud GPU availability for digital twin simulation and AI inference workloads.

- June 2026: SK Telecom applied NVIDIA Omniverse libraries to build digital twins of SK Hynix semiconductor fabs, using NVIDIA Agent Toolkit-based "Agentic Digital Twin Modeling" technology to automate data conversion, scene optimization, and performance improvement for large-scale manufacturing environments with complex GPU memory demands.

- June 2026: Micron and MetAI developed simulation-ready fab twins on NVIDIA Omniverse libraries using the OpenUSD framework and MetAI's MetGen platform, creating a scalable foundation for digital twin simulation and future AI-driven automation across Micron's semiconductor manufacturing environments.

Global Digital Twin GPU Market Report Scope

The Digital Twin GPU Market refers to the market for GPU-based hardware and software used to power digital twin workloads, including real-time simulation, visualization, and physics-based modeling. It supports virtual replicas of products, processes, factories, and infrastructure that continuously update with live data.

The Digital Twin GPU Market Report is Segmented by GPU Deployment Type (Workstation GPUs, Data Center GPUs, Edge and Embedded GPUs), GPU Integration Type (Discrete GPUs, and Integrated / Embedded GPUs), Deployment Model (On-Premises, Cloud, and Hybrid), Application (Design, Simulation and Engineering, Virtual Commissioning and Factory Planning, Predictive Maintenance and Asset Optimization, Real-Time Monitoring and Operations Control, Robotics and Autonomous Systems, 3D Visualization, and Rendering and Immersive Collaboration), End User (Manufacturing, Automotive and Transportation, Aerospace and Defense, Energy and Utilities, Oil and Gas, Healthcare and Life Sciences, IT and Telecom, and Smart Infrastructure and Buildings), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| Workstation GPUs |

| Data Center GPUs |

| Edge and Embedded GPUs |

| Discrete GPUs |

| Integrated / Embedded GPUs |

| On-Premises |

| Cloud |

| Hybrid |

| Design, Simulation and Engineering |

| Virtual Commissioning and Factory Planning |

| Predictive Maintenance and Asset Optimization |

| Real-Time Monitoring and Operations Control |

| Robotics and Autonomous Systems |

| 3D Visualization, Rendering and Immersive Collaboration |

| Manufacturing |

| Automotive and Transportation |

| Aerospace and Defense |

| Energy and Utilities |

| Oil and Gas |

| Healthcare and Life Sciences |

| IT and Telecom |

| Smart Infrastructure and Buildings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By GPU Deployment Type | Workstation GPUs | |

| Data Center GPUs | ||

| Edge and Embedded GPUs | ||

| By GPU Integration Type | Discrete GPUs | |

| Integrated / Embedded GPUs | ||

| By Deployment Model | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Application | Design, Simulation and Engineering | |

| Virtual Commissioning and Factory Planning | ||

| Predictive Maintenance and Asset Optimization | ||

| Real-Time Monitoring and Operations Control | ||

| Robotics and Autonomous Systems | ||

| 3D Visualization, Rendering and Immersive Collaboration | ||

| By End User | Manufacturing | |

| Automotive and Transportation | ||

| Aerospace and Defense | ||

| Energy and Utilities | ||

| Oil and Gas | ||

| Healthcare and Life Sciences | ||

| IT and Telecom | ||

| Smart Infrastructure and Buildings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the current and forecast value of the digital twin GPU market?

The digital twin GPU market size stands at USD 6.99 billion in 2026 and is forecast to reach USD 50.26 billion by 2031, up from USD 4.63 billion in 2025, at a 48.37% CAGR over 2026-2031.

Which region leads digital twin GPU adoption today?

North America led with 36.16% share in 2025, supported by hyperscaler GPU infrastructure, industrial software depth, and strong adoption across automotive, aerospace, semiconductor, and defense use cases.

Which region is growing the fastest for digital twin GPU deployments?

Asia-Pacific is the fastest-growing region with a 49.07% CAGR through 2031, driven by semiconductor fab digitalization, smart manufacturing programs, and expanding AI compute investment.

Which end-user sector contributes the most demand?

Manufacturing held the largest end-user share at 33.66% in 2025 because factories use GPU-backed twins for layout planning, simulation, robotics validation, and process optimization.

Which application is expanding the fastest in this space?

Robotics and autonomous systems is projected to grow at a 49.24% CAGR through 2031 as operators need physics-accurate simulation for robot policy training, fleet testing, and synthetic data generation.

What is slowing wider adoption of GPU-backed digital twins?

The main barriers are the high cost of high-memory GPU infrastructure and cooling, along with interoperability gaps across PLM, CAE, IoT, and live twin platforms that raise deployment complexity and cost.

Page last updated on: