GPU Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 73.5 Billion |

| Market Size (2031) | USD 227.30 Billion |

| Growth Rate (2026 - 2031) | 25.33% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Networking Market Analysis by Mordor Intelligence

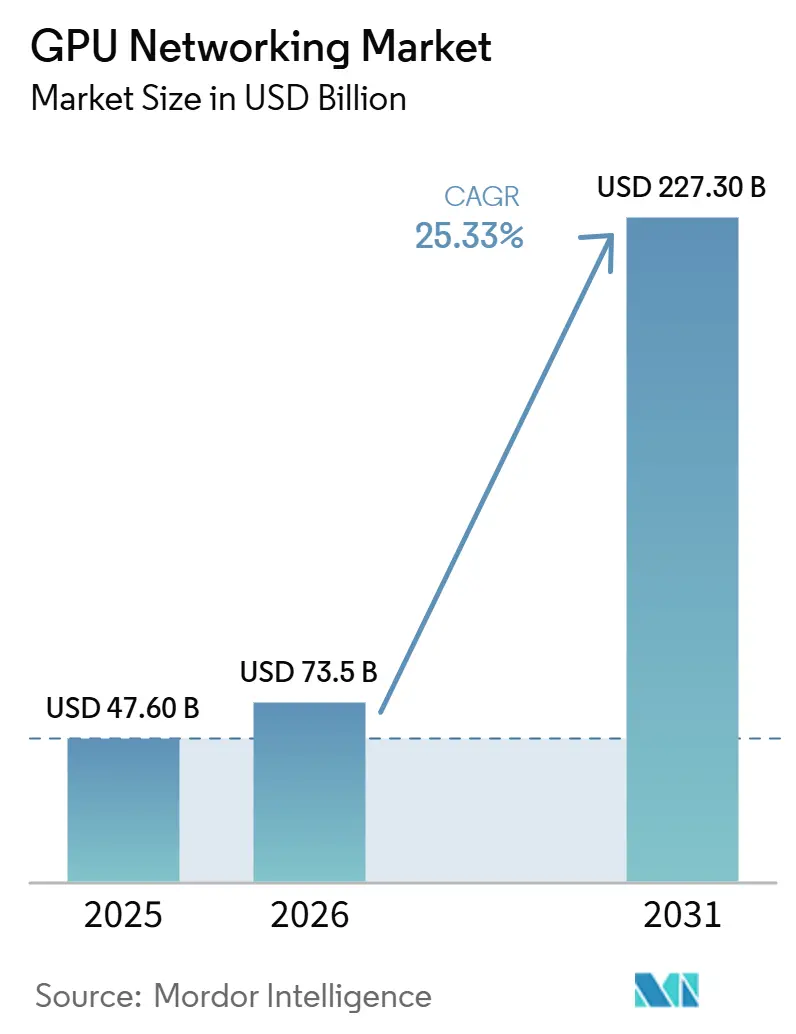

The GPU networking market size is expected to increase from USD 47.6 billion in 2025 to USD 73.5 billion in 2026 and reach USD 227.3 billion by 2031, growing at a CAGR of 25.33% over 2026-2031. The GPU networking market is being reshaped by a change in data center design, where the network now affects AI training speed instead of only supporting compute. As GPU clusters move from thousands to hundreds of thousands of accelerators, inter-GPU bandwidth has become a core engineering limit, which is pushing spending toward high-speed switching, optics, and interconnect silicon. The GPU networking market is also seeing faster vendor competition because buyers now prefer integrated platforms that combine switching, DPUs, optics, and software in validated AI factory designs. Supply remains tight in high-speed switch silicon and optical components, so order timing and procurement scale still affect deployment speed. At the same time, power ceilings, cooling limits, and fabric interoperability choices are creating room for orchestration software, managed integration, and deployment services across the GPU networking market.

Key Report Takeaways

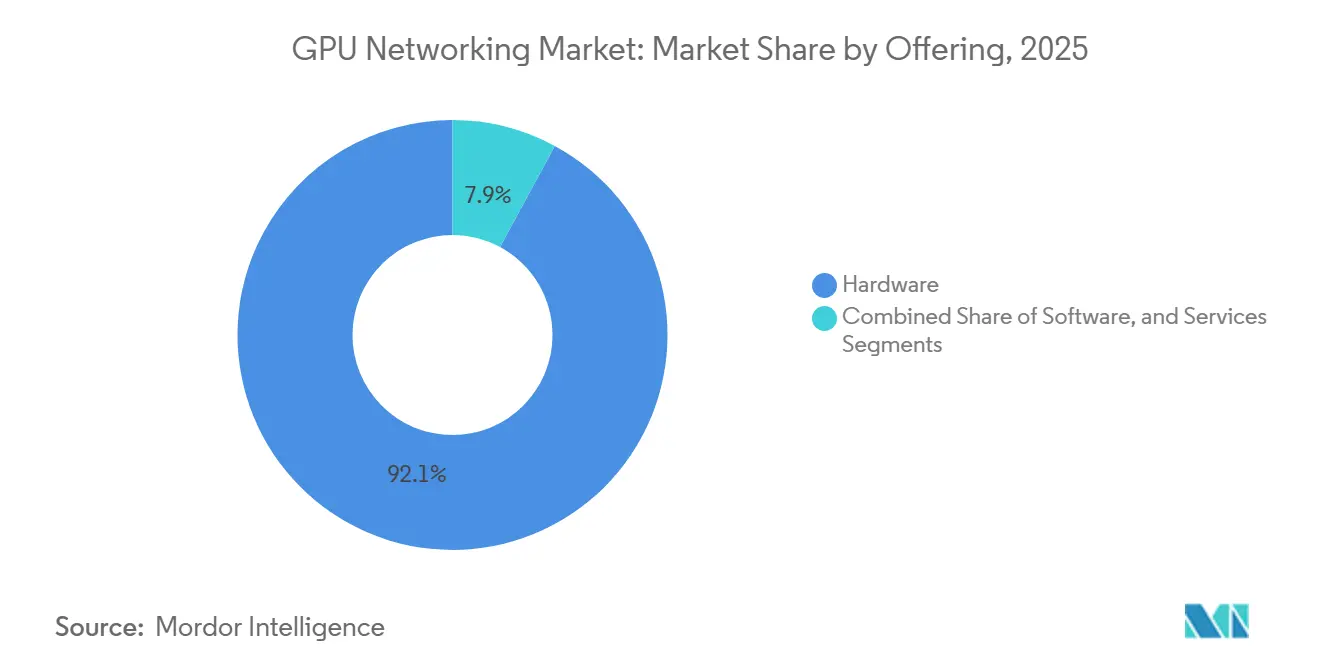

- By offering, hardware held 92.11% of the GPU networking market share in 2025, while software is projected to expand at a 26.21% CAGR through 2031.

- By network type, Ethernet accounted for 47.33% of 2025 revenue, while the GPU networking market size for Scale-Up GPU Interconnects is projected to expand at a 26.62% CAGR through 2031.

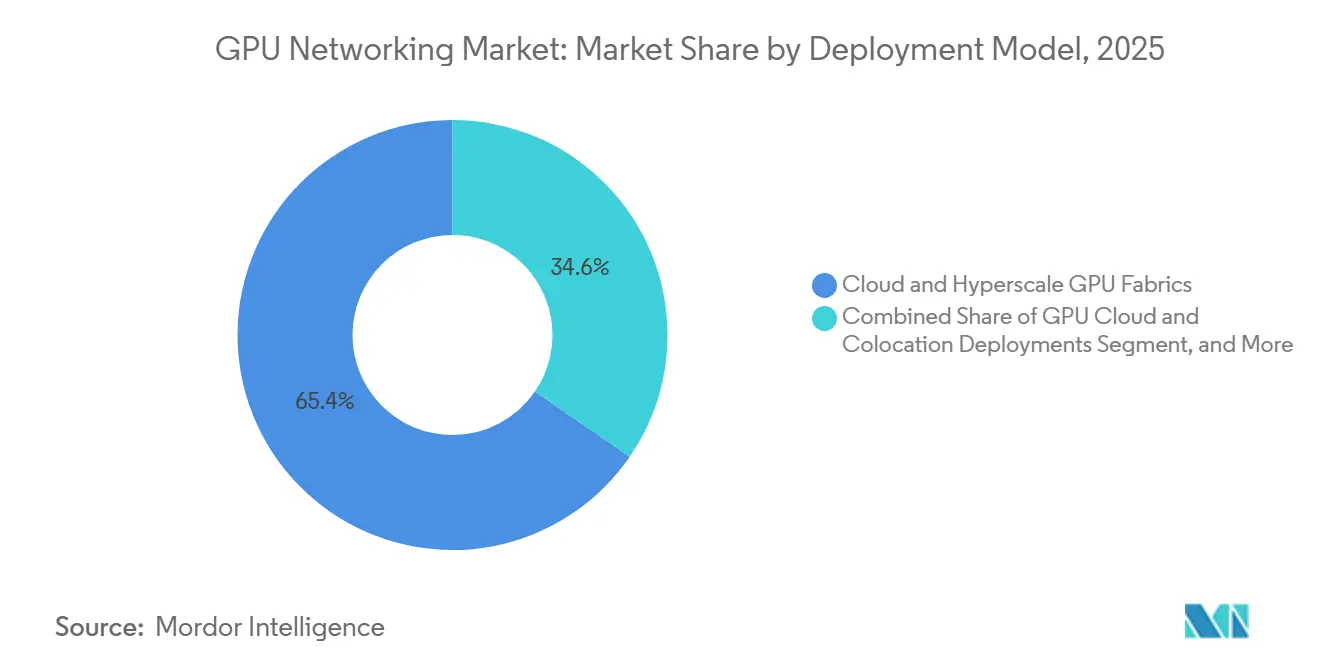

- By deployment model, Cloud and Hyperscale GPU Fabrics held 65.42% of 2025 revenue, while GPU Cloud and Colocation Deployments are projected to grow at a 26.53% CAGR through 2031.

- By end user, cloud service providers accounted for 58.12% of 2025 revenue, while enterprises are projected to record the fastest growth at a 26.32% CAGR through 2031.

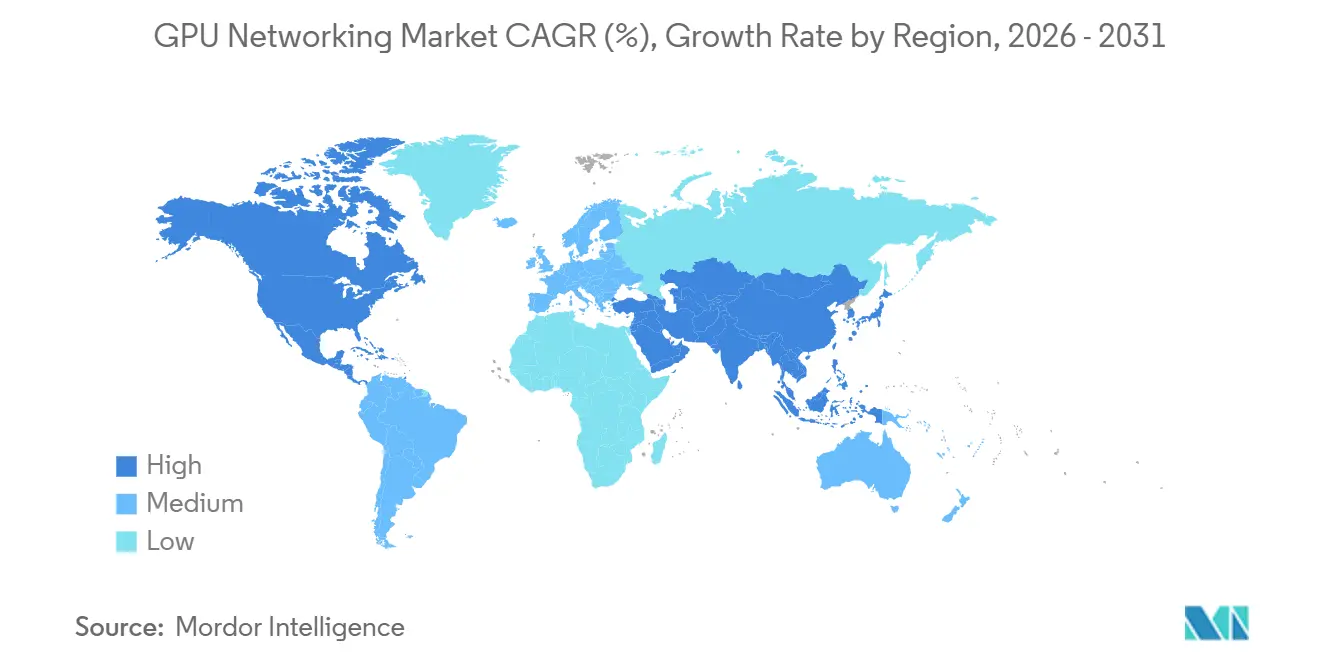

- By geography, North America held 38.44% of the GPU networking market share in 2025, while the GPU networking market size for Asia-Pacific is projected to expand at a 26.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Cluster Density in Hyperscale Data Centers | +8.2% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rapid Shift to 400G and 800G Network Upgrades | +6.1% | Global, with early-mover advantage in North America and China | Short term (≤ 2 years) |

| Growing Adoption of Lossless Ethernet for GPU Fabrics | +4.5% | North America and Europe, Asia-Pacific spill-over | Medium term (2-4 years) |

| Accelerating Use of InfiniBand for Large Model Training | +2.8% | North America, Japan, and South Korea | Short term (≤ 2 years) |

| Co-Packaged Optics Adoption in High-Speed GPU Fabrics | +2.1% | North America, early adoption in Japan and South Korea | Medium term (2-4 years) |

| Increased Demand for White-Box and ODM-Based AI Network Builds | +1.2% | North America and Asia-Pacific core, with spill-over to Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising AI Cluster Density Pushes Back-End Network to Center Stage

The GPU networking market is drawing more capital from hyperscale data centers because AI cluster density is rising faster than earlier web infrastructure cycles. AI accelerator rack power moved from below 20 kW in the web-services era to above 150 kW, and public roadmaps now point to pod-scale systems nearing 1 MW. That density forces operators to place more GPUs into tighter footprints, which raises east-west bandwidth demand across the back-end fabric. As a result, the GPU networking market now sits closer to the center of AI infrastructure planning, because underbuilt fabrics can leave expensive compute capacity waiting on data movement. Procurement priorities have shifted toward high-speed switching, optics, and dense interconnect designs that can keep large training clusters balanced. This also explains why the GPU networking market is attracting sustained spending even when buyers are already committing very large budgets to accelerators and storage.

Rapid Shift to 400G and 800G Fuels Ethernet Switch Revenue

The GPU networking market is benefiting from a faster Ethernet speed transition than most enterprise infrastructure categories have seen. 400G became mainstream in 2024, 800G entered production in 2025, and 1.6 Tbps platforms began reaching the market in 2026 through new product launches. Arista introduced the 7060XE7 Series in June 2026 with 100 Tbps aggregate switching capacity per platform using 224G SerDes and Broadcom Tomahawk 6 silicon.[1]Arista Networks, “Arista Introduces Next-Generation 1.6Terabit Portfolio for AI Fabrics,” Arista Newsroom, arista.com Celestica then made its DS6000-series 1.6 TbE switches available to order in April 2026, which brought the same speed class into the ODM channel. Each speed generation is shortening the upgrade cycle, so buyers that are deploying 800G today are already planning migration paths to 1.6T. Standards alignment is also shaping purchase decisions, since support for OCP ESUN and UEC specifications is becoming more important in the GPU networking market.

Lossless Ethernet for GPU Fabrics Displaces InfiniBand as the Scale-Out Default

The GPU networking market is seeing a clear shift toward Ethernet in scale-out AI fabrics, especially where buyers want open ecosystems and broader sourcing options. The Ultra Ethernet Consortium released UEC 1.0 in June 2025, which rebuilt parts of the Ethernet stack with packet spray, multi-path RDMA, and out-of-order delivery to improve behavior in AI clusters.[2]Ultra Ethernet Consortium, “UEC 1.0 Specification,” Ultra Ethernet Consortium, ultraethernet.org RoCEv2 with congestion controls such as Priority Flow Control, Explicit Congestion Notification, and DCQCN is now being treated as practical for many training workloads at production scale. Large cloud operators have leaned toward RoCEv2 because it fits established Ethernet tools and supports multi-vendor supply strategies. NVIDIA reinforced this transition in May 2026 by publishing the Multipath Reliable Connection specification through the Open Compute Project with support from OpenAI, Microsoft, AMD, Broadcom, and Intel. This is widening the addressable share of the GPU networking market for Ethernet-based platforms without removing the role of specialized fabrics in the largest clusters.

InfiniBand Maintains Dominance for Frontier-Scale Model Training

The GPU networking market still depends on InfiniBand for frontier-scale model training where deterministic lossless behavior and very low latency remain essential. NVIDIA’s Quantum-X InfiniBand CPO switch began shipping to early adopters in 2026 with 144 ports of 800G InfiniBand and silicon photonics co-packaged optics.[3]NVIDIA Corporation, “Silicon Photonics Networking for Agentic AI,” NVIDIA Networking, nvidia.com NVIDIA also outlined rack-scale system designs around the Vera Rubin platform, which highlights how scale-up and scale-out fabric choices are being reconsidered together. In the largest training environments, network power efficiency now matters almost as much as speed because the fabric can consume a large share of the cluster networking power budget. This keeps InfiniBand relevant in the GPU networking market even as Ethernet expands into more scale-out deployments. It also supports continued investment in next-generation InfiniBand roadmaps as model complexity keeps increasing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity of GPU Networking Infrastructure | -3.2% | Global, most acute for enterprises and emerging-market operators | Medium term (2-4 years) |

| Interoperability and Vendor Lock-In Risk Across Fabric Stacks | -2.5% | Global, particularly in multi-vendor enterprise and sovereign AI deployments | Long term (≥ 4 years) |

| Power, Cooling, and Rack Density Constraints in AI Facilities | -2.0% | North America, Europe, Asia-Pacific secondary | Medium term (2-4 years) |

| Limited Supply of High-Speed Switch Silicon and Optical Components | -1.8% | Global, concentrated in North America, Japan, and Taiwan supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity Concentrates Market Access Among Hyperscale Operators

The GPU networking market still carries a large upfront cost burden, and that burden shapes who can deploy production-grade fabrics at scale. A full AI networking build requires switches, NICs, DPUs, transceivers, cabling, software, and integration work, so the spending threshold is far higher than in conventional data center upgrades. This favors hyperscale buyers that can negotiate at volume and spread fixed engineering costs across very large deployments. Enterprise buyers and smaller cloud operators often face a much steeper per-GPU networking cost because their procurement scale is lower and their integration teams are smaller. The result is slower adoption in parts of the GPU networking market that depend on private builds or regional infrastructure programs. This cost barrier is also increasing interest in validated architectures and service-led deployment models that reduce execution risk for smaller buyers.

Interoperability Fragmentation Introduces Strategic Risk Across Fabric Stacks

The GPU networking market is divided across proprietary and open fabric approaches, which creates a long-term interoperability problem for buyers that need flexibility. NVLink and NVSwitch, InfiniBand, Ethernet, and UALink each carry different software expectations, performance profiles, and supplier ecosystems. The UALink Consortium published version 1.0 of its open specification in July 2025, which created a formal alternative to proprietary scale-up interconnects, but deployment remains early. Mixing these paradigms inside one cluster can make congestion management harder because the control behavior of one fabric does not cleanly map onto another. Buyers that choose one tightly integrated vendor stack gain speed of deployment, but they also reduce negotiating leverage and make future refresh cycles more binary. This tension remains a meaningful brake on the GPU networking market, especially in sovereign and enterprise deployments that need long-term supplier flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware's Grip Persists While Software Scales Faster

Hardware accounted for 92.11% of 2025 revenue and remained the largest component of the GPU networking market. That concentration reflects the high cost of physical infrastructure, especially switches, NICs, DPUs, cables, and optical transceivers. Switching platforms formed the largest hardware block because 800G Ethernet and InfiniBand systems are central to AI cluster design. NICs and DPUs also gained weight as buyers moved network offload, telemetry, and traffic management onto dedicated silicon inside the server stack. This bundling trend is making compute and networking procurement more interdependent across the GPU networking market.

Cables and transceivers remained the third major hardware pillar, and their availability still affected deployment schedules in the GPU networking market. Buyers could secure accelerators and switch platforms, but cluster turn-up still depended on optical readiness and qualified interconnect inventory. Software is projected to expand at a 26.21% CAGR through 2031, which makes it the fastest-growing offering in the GPU networking market. Network orchestration, adaptive routing, telemetry, and congestion control are moving from optional tools to operating requirements as cluster sizes increase. Services are also becoming more important because enterprise and sovereign operators often need deployment support, integration help, and ongoing operations expertise to run GPU fabrics at scale.

By Network Type: Scale-Up Interconnects Reshape the Fabric Hierarchy

Ethernet held 47.33% of 2025 revenue and led the GPU networking market by network type. That lead reflects Ethernet’s role in scale-out AI back-end networks, front-end management layers, and storage traffic. RoCE-enabled Ethernet has become the practical default for many AI training environments where buyers want open standards and broader sourcing. The Ultra Ethernet Consortium’s UEC 1.0 release in June 2025 strengthened that position by extending Ethernet behavior for AI cluster requirements. Standard Ethernet still mattered for support traffic, while higher-performance RoCE deployments carried more of the training workload inside the GPU networking market.

InfiniBand remained critical where deterministic performance and very low latency outweighed the benefits of broader interoperability. At the same time, Scale-Up GPU Interconnects are forecast to grow at a 26.62% CAGR through 2031, making them the fastest-growing network type in the GPU networking market. The main reason is architectural, because AI systems are now pushing more traffic inside the compute pod rather than only between nodes. NVIDIA’s Vera Rubin NVL144 direction and AMD’s Infinity Fabric reflect the rising importance of terabit-class intra-cluster bandwidth. UALink 1.0 also widened the design path for open scale-up fabrics, which keeps this part of the GPU networking market strategically important.

By Deployment Model: Hyperscale Dominates, Colocation Accelerates

Cloud and Hyperscale GPU Fabrics held 65.42% of 2025 revenue and set the pace for the GPU networking market by deployment model. These operators control procurement at a scale that lets them influence switch design, optics qualification, and network operating system choices. Their buying power lowers per-bit cost and gives them earlier access to constrained components than most other customer groups. This also means many technology choices in the GPU networking market are effectively set by a small number of hyperscale teams before the broader market follows. The concentration creates a winner-take-most effect for vendors that achieve qualification inside these large cloud environments.

GPU Cloud and Colocation Deployments are projected to grow at a 26.53% CAGR through 2031, making them the fastest-growing deployment model in the GPU networking market. These platforms appeal to enterprise buyers that need dedicated performance but do not want to build a full private AI factory. The European Commission’s AI Gigafactory initiative, which targets 5 facilities with up to EUR 20 billion (USD 21.80 billion) in public funding, points to an extended demand pipeline for colocation-scale networking from 2027 onward. On-premises AI clusters are also gaining ground in regulated sectors where data governance limits public cloud use. This leaves the GPU networking market with a more layered deployment profile, where hyperscale remains dominant, but colocation and regulated on-premises demand are expanding more quickly.

By End User: CSP Concentration Eases As Enterprise Adoption Scales

Cloud service providers held 58.12% of 2025 revenue and remained the largest end-user group in the GPU networking market. Their leadership came from early capital deployment in AI training and inference infrastructure across global cloud platforms. These buyers also function as reference accounts for major launches, which means product validation often starts with their technical requirements. Government and defense users continued to build air-gapped GPU fabrics for sovereign and classified workloads. Research and academia remained smaller in total spend, but they still played an early role in testing emerging interconnect designs inside the GPU networking market.

Enterprises are projected to grow at a 26.32% CAGR through 2031, which makes them the fastest-growing buyer group in the GPU networking market. This shift reflects the move from cloud API experimentation toward on-premises and dedicated inference clusters in production settings. Cisco expanded its Secure AI Factory with NVIDIA in March 2026 to shorten enterprise deployment timelines with validated reference architectures and integrated security. Enterprise spending still leans toward integrated hardware and software stacks because multi-vendor interoperability is difficult for smaller IT teams to manage. As-as-service models from neocloud and colocation providers are helping narrow that gap, which should widen the enterprise base of the GPU networking market over the forecast period.

Geography Analysis

North America held 38.44% of 2025 revenue and remained the largest regional block in the GPU networking market. The region is anchored by the capital programs of major U.S. hyperscalers, which continue to shape global demand for switches, transceivers, and interconnect silicon. NVIDIA’s move into Ethernet switching leadership through Spectrum-X showed how tightly compute and networking decisions are now linked in this region. Cloud providers such as Google, Amazon, Microsoft, and Meta announced multiyear AI infrastructure expansions in 2025 and 2026, which kept pressure on 800G and 1.6T supply chains. The United States also remains the main design and procurement center for many white-box and ODM programs, so decisions made there flow quickly through Asian manufacturing ecosystems. Canada and Mexico added supporting capacity where power availability and proximity to U.S. cloud infrastructure made regional deployments practical.

Europe remained the second-largest region in the GPU networking market and continued to advance on the back of sovereign AI policy, hyperscaler expansion, and digital infrastructure programs. Deutsche Telekom and NVIDIA opened Germany’s Industrial AI Cloud in Munich in February 2026 with 10,000 NVIDIA Blackwell GPUs and EUR 1 billion (USD 1.09 billion) in investment. The UK also attracted commitments from NVIDIA, Microsoft, and Google that exceeded GBP 40 billion (USD 50 billion) in early 2026, including NVIDIA’s plan to install 120,000 Blackwell GPUs in British data centers by end-2026. The European Commission’s AI Gigafactory program is expected to add 5 facilities with up to EUR 20 billion in public funding, which extends the future project pipeline for rack-scale networking.

Asia-Pacific is projected to grow at a 26.42% CAGR through 2031, making it the fastest-growing region in the GPU networking market. China, Japan, South Korea, and India are driving different demand patterns across public cloud, sovereign AI, telecom, and industrial deployments. China’s large internet companies continue to invest heavily in data center capacity, and domestic procurement priorities are supporting local GPU networking build-outs. Japan is also showing early momentum in distributed photonic networking. NTT East completed a proof of concept between Tokyo and Fukuoka in March 2026 using the IOWN All-Photonics Network and recorded average round-trip latency of 13.26 ms over 1,000 km. NTT said in April 2026 that it plans to increase data center IT power capacity from 300 MW to 1 GW by 2033, with AI networking as a central theme. Southeast Asia, South America, and the Middle East and Africa are emerging demand pools in the GPU networking market as sovereign funds and digital economy programs back regional GPU cloud and colocation builds.

Competitive Landscape

The GPU networking market has a split structure with a concentrated top tier and a broader set of ODM and component specialists underneath it. NVIDIA, Broadcom, Arista Networks, and Cisco account for much of the branded revenue and shape many of the performance standards used in new AI clusters. NVIDIA moved quickly in Ethernet switching by tying Spectrum-X to GPUs, BlueField DPUs, LinkX optics, and CUDA software in one validated architecture. That combination gave buyers a shorter path to deployment and made integrated design a stronger competitive weapon in the GPU networking market. Arista responded in June 2026 with the 7060XE7 Series, which used Broadcom Tomahawk 6 silicon to offer an open-standards alternative for AI fabrics.

Cisco also expanded its relationship with NVIDIA in February 2025 and March 2026 to stay relevant in enterprise, neocloud, and telecom AI deployments. The partnership produced the Cisco N9100, which brought Spectrum-X silicon into a partner-developed switch while preserving Cisco’s Silicon One path for other designs. Broadcom remained foundational because its switch ASIC franchise underpins both branded and ODM platforms across the GPU networking market. This is why competition is not only about complete switches, but also about who controls the silicon roadmap, the optics path, and the reference architecture around the cluster.

The optical tier is becoming more strategic inside the GPU networking market because high-speed photonics now affects both supply security and system efficiency. NVIDIA committed USD 4 billion to Lumentum Holdings and Coherent Corporation in March 2026 to secure indium phosphide EML production capacity for Quantum-X and Spectrum-X co-packaged optics systems. That move showed how leading vendors are trying to secure component access before broader shortages slow customer rollouts. It also raised the importance of vertical integration, because companies that control silicon, optics, and system design can defend margins and lead times more effectively. Huawei continued to hold a strong domestic position in China through its HiSilicon ASIC portfolio and Atlas AI cluster architecture, which leaves the GPU networking market with a parallel ecosystem that is partly separated from Western supply chains.

GPU Networking Industry Leaders

NVIDIA Corporation

Broadcom Inc.

Arista Networks, Inc.

Cisco Systems, Inc.

Celestica Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Arista Networks announced the 7060XE7 Series, a portfolio of 1.6 Tbps networking platforms built on Broadcom Tomahawk 6 silicon, delivering 100 Tbps aggregate switching capacity with 224G SerDes technology; the platform supports air-cooled, liquid-cooled, and hybrid-cooled configurations for AI clusters from thousands to hundreds of thousands of GPUs. Ecosystem validation from Microsoft Azure, Oracle Cloud Infrastructure, and Meta underpins early adoption confidence. Air-cooled models (64×1.6T) are scheduled for Q4 2026 availability.

- May 2026: NVIDIA committed USD 4 billion to Lumentum Holdings and Coherent Corporation to secure priority indium phosphide EML production capacity for its Quantum-X and Spectrum-X co-packaged optics switches. The commitment, disclosed in March 2026, extends NVIDIA's effective EML supply access through at least 2027, raising lead times for all other buyers.

- April 2026: Celestica made its DS6000-series 1.6 TbE switches available for order on April 29, 2026, the first commercially orderable 1.6T GPU networking platform from an ODM vendor. Powered by Broadcom Tomahawk 6 with up to 102.4 Tbps non-blocking switching capacity, the DS6000 supports SONiC and complies with UEC and OCP ESUN specifications.

- March 2026: Cisco expanded its Secure AI Factory with NVIDIA on March 16, 2026, introducing the Cisco N9100 switch powered by NVIDIA Spectrum-6 Ethernet silicon at 102.4 Tbps, compressing enterprise AI deployment timelines from months to weeks. The expansion added edge AI capabilities via NVIDIA RTX PRO Blackwell GPUs and integrated Cisco AI Defense security across multi-agent environments.

Global GPU Networking Market Report Scope

The Global GPU Networking Market refers to the rapidly evolving industry segment that integrates Graphics Processing Units (GPUs) with advanced networking technologies to accelerate data-intensive workloads, high-performance computing (HPC), artificial intelligence (AI), machine learning (ML), and cloud-based applications across distributed systems.

The GPU Networking Market Report is Segmented by Offering (Hardware [Switches, Network Interface Cards and DPUs, and Cables and Transceivers], Software [Network Orchestration and Management Software and Monitoring and Telemetry Software], and Services [Integration and Deployment Services and Support and Maintenance Services]), Network Type (Ethernet [Standard Ethernet and RoCE-enabled Ethernet], InfiniBand, Scale-Up GPU Interconnects [NVLink/NVSwitch, Infinity Fabric, and UALink and Other Emerging Interconnects]), Deployment Model (On-Premises AI Clusters, Cloud and Hyperscale GPU Fabrics, and GPU Cloud and Colocation Deployments), End User (Cloud Service Providers, Enterprises, Government and Defense, Research and Academia, and Telecommunications Service Providers), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Switches |

| Network Interface Cards and DPUs | |

| Cables and Transceivers | |

| Software | Network Orchestration and Management Software |

| Monitoring and Telemetry Software | |

| Services | Integration and Deployment Services |

| Support and Maintenance Services |

| Ethernet | Standard Ethernet |

| RoCE-enabled Ethernet | |

| InfiniBand | |

| Scale-Up GPU Interconnects | NVLink/NVSwitch |

| Infinity Fabric | |

| UALink and Other Emerging Interconnects |

| On-Premises AI Clusters |

| Cloud and Hyperscale GPU Fabrics |

| GPU Cloud and Colocation Deployments |

| Cloud Service Providers |

| Enterprises |

| Government and Defense |

| Research and Academia |

| Telecommunications Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Offering | Hardware | Switches |

| Network Interface Cards and DPUs | ||

| Cables and Transceivers | ||

| Software | Network Orchestration and Management Software | |

| Monitoring and Telemetry Software | ||

| Services | Integration and Deployment Services | |

| Support and Maintenance Services | ||

| By Network Type | Ethernet | Standard Ethernet |

| RoCE-enabled Ethernet | ||

| InfiniBand | ||

| Scale-Up GPU Interconnects | NVLink/NVSwitch | |

| Infinity Fabric | ||

| UALink and Other Emerging Interconnects | ||

| By Deployment Model | On-Premises AI Clusters | |

| Cloud and Hyperscale GPU Fabrics | ||

| GPU Cloud and Colocation Deployments | ||

| By End User | Cloud Service Providers | |

| Enterprises | ||

| Government and Defense | ||

| Research and Academia | ||

| Telecommunications Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the GPU networking market?

The GPU networking market stood at USD 47.6 billion in 2025, reached USD 73.5 billion in 2026, and is forecast to reach USD 227.3 billion by 2031 at a 25.33% CAGR.

Why is network architecture becoming so important for AI clusters?

Larger GPU clusters need far more east-west bandwidth, so interconnect speed, congestion control, and power efficiency now directly affect training throughput and infrastructure utilization.

Which part of the stack holds the largest share today?

Hardware led with 92.11% of 2025 revenue because switches, NICs, DPUs, transceivers, and cables still absorb most spending in production GPU fabric deployments.

Which network type is growing the fastest in GPU cluster deployments?

Scale-Up GPU Interconnects are projected to expand at a 26.62% CAGR through 2031 as buyers place more bandwidth inside compute pods and rack-scale systems.

Who are the biggest buyers of GPU networking systems?

Cloud service providers held 58.12% of 2025 revenue, but enterprise adoption is rising faster and is projected to grow at a 26.32% CAGR through 2031.

Which region is expanding the fastest for GPU networking demand?

Asia-Pacific is the fastest-growing region with a projected 26.42% CAGR through 2031, while North America remained the largest regional market in 2025 with a 38.44% share.

Page last updated on: