Commercial Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 58.20 Billion |

| Market Size (2031) | USD 72.91 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

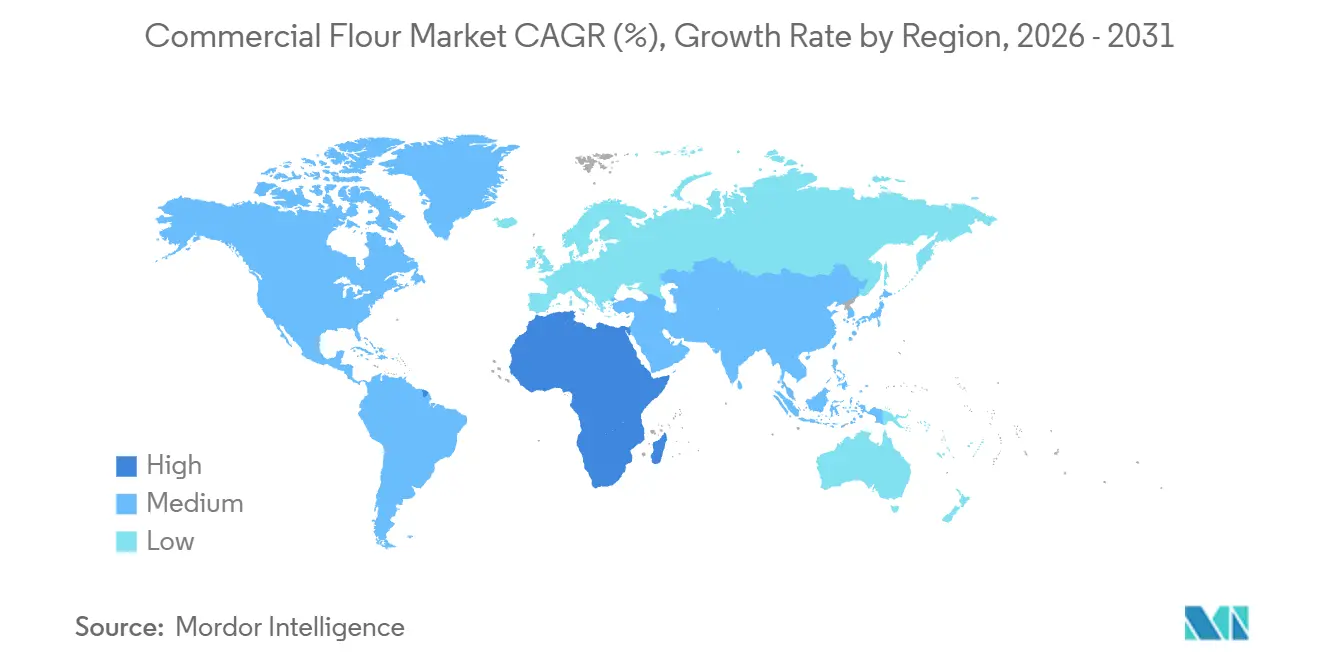

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

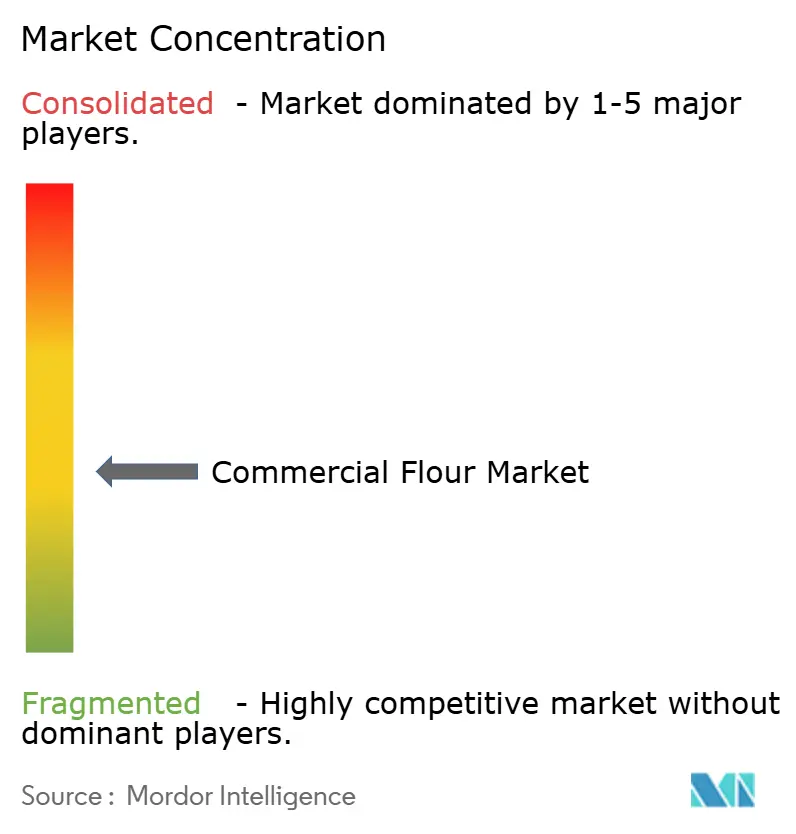

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Flour Market Analysis by Mordor Intelligence

By 2031, the commercial flour market is projected to grow from USD 55.6 billion in 2025 and USD 58.2 billion in 2026 to USD 72.9 billion, with a CAGR of 4.6% from 2026 to 2031. Demand remains steady as industrial food manufacturers, organized foodservice networks, and premium retail buyers continue to purchase large flour volumes. In 2024/25, global wheat utilization for food reached 548.3 million metric tons, highlighting the strong link between flour milling and staple food demand in major economies. Revenue growth is supported by a shift from bulk commodity flour to branded, specialty, fortified, and certified variants offering higher value per ton. Large millers are improving their position through automation, traceability, and diverse product portfolios, while smaller operators face challenges from compliance costs, technology investments, and raw material volatility. Climate stress and trade uncertainties are increasing risks to wheat supply, making scale, sourcing reach, and operational resilience critical in the commercial flour market.

Key Report Takeaways

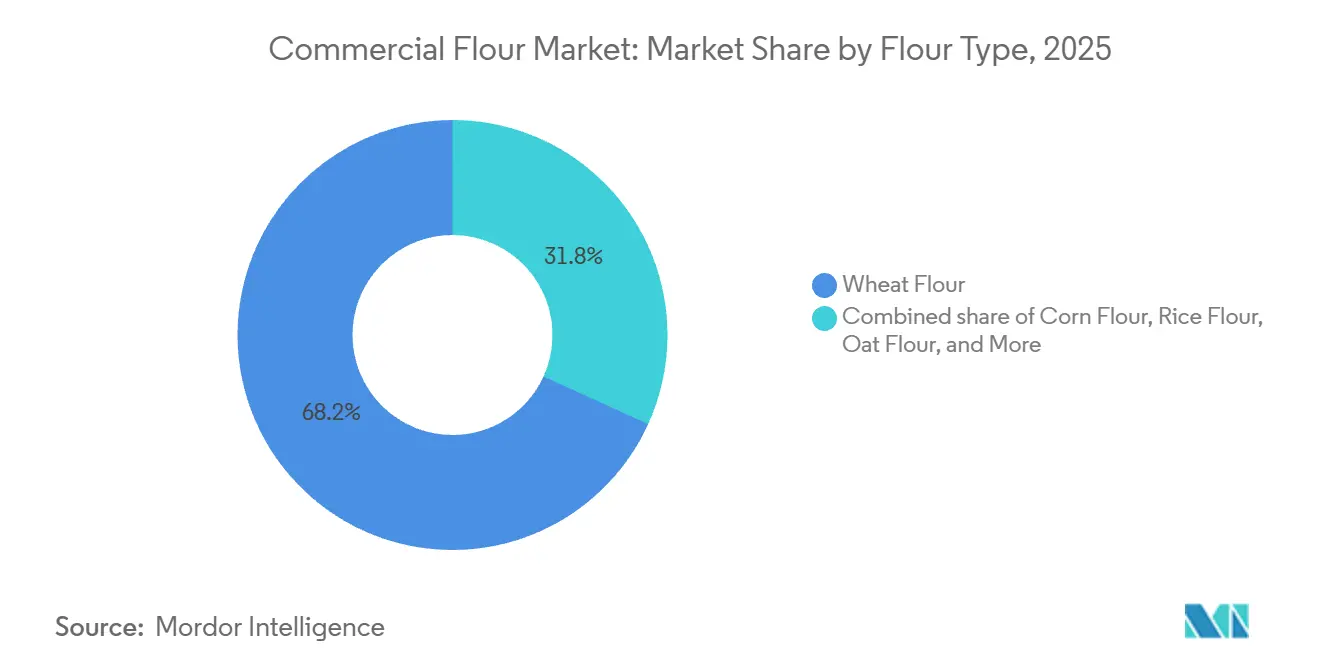

- By flour type, wheat flour held 68.2% of the commercial flour market share in 2025, while corn flour is forecast to expand at a 4.98% CAGR through 2031.

- By category, conventional flour accounted for 90.32% share of the commercial flour market size in 2025, while organic flour recorded the highest projected CAGR at 5.5% through 2031.

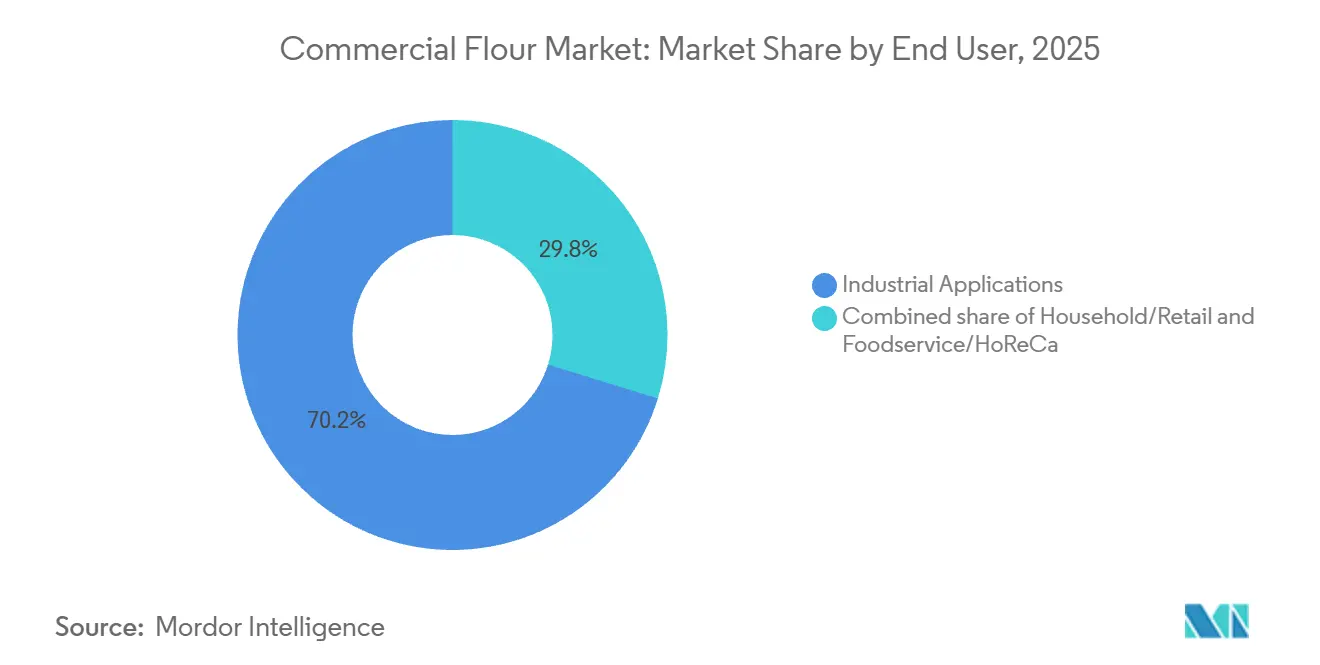

- By end user, industrial applications captured 70.23% of revenue in 2025, while the household and retail segment is advancing at a 5.9% CAGR through 2031.

- By geography, Asia-Pacific led with 43.22% revenue share in 2025, while the Middle East and Africa are forecast to grow at a 6.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Flour Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health Consciousness And Demand For Specialty Flours | +0.7% | Global, with North America and Europe dominant | Medium term (2-4 years) |

| Growth In Bakery And Processed Food Sectors | +1.1% | Global, with APAC dominant | Short term (≤ 2 years) and Medium term (2-4 years) |

| Technological Advancements In Milling And Production Processes | +0.5% | Global | Medium term (2-4 years) and Long term (≥ 4 years) |

| Increasing Demand For Gluten-Free Products | +0.6% | North America and Europe | Medium term (2-4 years) |

| Rising Preference For Organic And Non-GMO Flours | +0.4% | North America and Europe | Long term (≥ 4 years) |

| Demand For Premium And Artisanal Baked Food Products | +0.3% | North America and Europe, with emerging presence in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Bakery and Processed Food Sectors

The bakery and processed food sectors remain the largest demand drivers for commercial flour, surpassing all other end-use groups in purchase volume. In Brazil, the food processing sector processed 62% of the country’s agricultural output and generated USD 248 billion in 2025, an 8% rise from the previous year, while achieving record exports of USD 66.7 billion[1]Source: U.S. Department of Agriculture Foreign Agricultural Service, “Food Processing Ingredients Annual, Brazil”, usda.gov. Similarly, Vietnam’s food processing sector reached USD 88 billion in 2025, reflecting 11% growth, showcasing the rapid expansion of organized manufacturing in Southeast Asia. The increasing popularity of packaged foods, chain restaurants, and formal distribution networks is driving a shift in the commercial flour market from loose flour consumption to consistent industrial procurement.

Technological Advancements in Milling and Production Processes

Technology is changing the operating standard in the commercial flour market because quality, yield, and traceability now matter as much as price in many industrial contracts. AI-based optical sorting, autonomous roller mill control, and real-time digital monitoring are raising the minimum investment needed to compete at scale. These systems help mills reduce variation, improve defect detection, and limit raw material losses during production. Industrial buyers are also using tighter quality benchmarks and traceability data when selecting suppliers, which favors mills that can prove process consistency. This shift is widening the gap between modernized large operators and smaller mills that have delayed automation in the commercial flour market.

Rising Health Consciousness and Demand for Specialty Flours

Health-oriented buying is pushing the commercial flour market toward a broader mix of gluten-free, high-fiber, ancient grain, and functional products. This change is reducing the room for undifferentiated commodity flour in premium retail and premium packaged food categories. According to the data from the Organic Trade Association, total U.S. certified organic product sales reached USD 76.6 billion in 2025, up 6.8%, which points to a strong wellness backdrop that also supports certified flour demand[2]Source: Organic Trade Association, “U.S. Organic Marketplace Achieved Significant Growth in 2025”, ota.com. Food manufacturers are also writing certification requirements into procurement contracts more often, which means specialty flour demand is no longer limited to small retail niches. As a result, the commercial flour market is seeing stronger volume potential for millers that already have the sourcing, testing, and certification systems needed for differentiated products.

Increasing Demand for Gluten-Free Products

Gluten-free demand in the commercial flour market is supported by both medical need and broader diet preference. U.S. per capita wheat flour use was 126.6 pounds in 2025, continuing the decline that has been underway since 2008 as more consumers reduce conventional wheat intake. This is shifting more spending toward corn, rice, oat, and other specialty flours that can serve gluten-free positioning. The change matters because those alternative categories usually carry higher margins and less entrenched competition than bulk wheat flour. Millers that can offer a multi-grain portfolio are better placed in the commercial flour market because buyers are increasingly moving away from single-grain sourcing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Food Safety Regulations And Compliance Requirements | -0.4% | Global, especially North America and the EU | Long term (≥ 4 years) |

| Fluctuating Grain Prices And Supply Volatility | -0.7% | Global, with flour-importing nations most affected | Short term (≤ 2 years) and Medium term (2-4 years) |

| Competition From Substitute Flours And Alternative Products | -0.4% | North America and Europe | Medium term (2-4 years) |

| Climate Change Impact On Wheat Cultivation And Yields | -0.5% | APAC, Europe, and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Grain (Wheat) Prices and Supply Volatility

Wheat price swings remain one of the clearest limits on earnings stability in the commercial flour market. USDA noted in June 2025 that global wheat consumption for 2025/26 moved higher on stronger food, seed, and industrial use, while production constraints in Russia and the EU added supply uncertainty. Research published in Food Security in 2025 showed that weather extremes in Russia, together with geopolitical disruption, have been amplifying wheat price volatility in export markets. Mills that sell into fixed-price contracts cannot always pass through abrupt grain cost increases, which puts smaller operators under the most pressure. The commercial flour market therefore remains exposed not only to high wheat prices, but also to sudden price moves that disrupt planning, hedging, and buyer negotiations.

Stringent Food Safety Regulations and Compliance Requirements

Compliance has become a recurring operating burden in the commercial flour market rather than a one-time setup cost. Under FSMA, food facilities, including flour mills, must maintain written food safety plans, hazard analysis, preventive controls, and supply-chain verification programs. A 2026 GAO review found that the FDA had still not established the full traceability recordkeeping system required under FSMA Section 204, with completion now targeted for July 2028. Large mills can spread testing, audit, and documentation costs across a much bigger revenue base, while small and mid-sized mills cannot. This uneven burden is reinforcing consolidation in the commercial flour market because compliance-ready operators are more likely to gain share or acquire weaker rivals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flour Type: Wheat Dominates While Corn Flour Redefines the Alternative Segment

In 2025, wheat flour accounted for 68.2% of the commercial flour market, reflecting the strong milling, logistics, and food manufacturing systems built around wheat. In the U.S., 907 million bushels of wheat were ground into flour, producing 419 million hundredweight of flour (USDA.GOV). Wheat remains essential in bakery, pasta, noodle, and snack production due to its gluten performance and consistent handling. Rice flour holds a key role in Asia-Pacific cuisines, oat flour is gaining popularity in fiber-rich bakery products, and rye flour supports artisanal bread demand in Europe.

Corn flour is projected to grow at a 5.0% CAGR through 2031, making it the fastest-growing segment in the commercial flour market. GRUMA, in its 2025 annual report, identified itself as the largest global producer of corn flour and tortillas, with facilities in the U.S., Mexico, Central America, Europe, and Asia-Oceania. The company is expanding capacity and exploring acquisitions in Europe, indicating confidence in corn flour's potential beyond traditional markets. USDA's March 2026 forecast for 2025/26 global corn production exceeds 842 million metric tons, supporting the raw material supply for corn flour's growth.

By Category: Conventional Flour's Industrial Scale Meets Organic's Premium Momentum

In 2025, conventional flour dominated the commercial flour market, holding a 90.3% share. This dominance is largely due to the industrial food sector's reliance on cost efficiency, consistent availability, and stable formulations. Key players, including bakery chains, pasta producers, snack manufacturers, and institutional foodservice operators, find it challenging to absorb the premium costs associated with certified organic supplies, especially at high procurement volumes. Furthermore, conventional flour is deeply embedded in existing production equipment, adheres to established specifications, and meets the texture expectations of mass-market foods. These entrenched factors ensure conventional flour remains central to the commercial flour industry, even as premium categories emerge around it.

Forecasted to grow at a 5.5% CAGR through 2031, organic flour is emerging as the fastest-growing segment in the commercial flour market. In 2025, U.S. organic food sales hit USD 70.1 billion, marking a 6.9% growth, and organic products achieved a 6.1% share of the total U.S. food market. The demand surge is not just from retail shoppers; food manufacturers are increasingly turning to organic flour, leveraging it for premium shelf positioning and cleaner label claims. Given that organic flour commands a price premium of 50% to 100% over its conventional counterparts, mills with certified supply chains are motivated to ramp up capacity in this lucrative segment of the commercial flour market.

By End User: Industrial Processing Commands Volume, Household Channel Leads Growth Pace

In 2025, industrial applications accounted for 70.23% of end-user demand, underscoring the commercial flour market's deep-rooted ties to major food manufacturers and bakeries. Displacing this segment proves challenging; processors intricately design their operations, from quality checks to logistics, around specific flour standards, and any reformulation poses significant operational risks. In Vietnam, buoyed by rising international tourist arrivals and rapid chain expansions in 2025, the foodservice sector's growth underscores the robust institutional flour demand in its burgeoning food markets. Additionally, the HoReCa channel bolsters demand, particularly in regions like APAC and MEA, where organized foodservice is still on the rise.

The household and retail segment is projected to grow at a 5.9% CAGR through 2031, marking it as the fastest-growing segment in the commercial flour market. Ardent Mills highlighted a surge in premium retail innovation, noting that in the first half of 2026, new products with combined protein, fiber, and whole-grain claims outpaced all of 2025 by 92%. In March 2025, King Arthur Baking Company introduced its Buttermilk Biscuit Flour Blend, capitalizing on home baking trends to drive higher-value flour sales. This evolution has transformed the retail space within the commercial flour industry, making it more specialized, branded, and lucrative compared to its traditional commodity roots.

Geography Analysis

In 2025, the Asia-Pacific region dominated the commercial flour market, holding a significant 43.22% share. This leadership stemmed from the growing integration of wheat-based foods into daily diets and foodservice formats, particularly in urban areas of China and India. According to OECD-FAO projections for 2025, India was expected to account for 29% of the global increase in wheat production, driving world output toward 874 million metric tons by 2034. Additionally, USDA forecasts indicated that India’s food processing sector would grow from USD 355 billion in 2024 to USD 535 billion by FY2026, highlighting a strong demand channel for commercial flour.

Europe’s commercial flour market benefits from its premium bakery traditions, high demand for organic foods, and strict quality standards. Major demand centers include Germany, France, Italy, Poland, and the UK, with Poland gaining prominence due to its cost advantages and expanding consumer base. In South America, Brazil serves as the primary driver of flour consumption. In 2025, Brazil’s food processing sector utilized 62% of the country’s agricultural output. Investments totaling BRL 116 billion (USD 20.8 billion) in manufacturing and innovation further supported demand for flour in packaged foods and foodservice.

The Middle East and Africa (MEA) are projected to be the fastest-growing regions in the commercial flour market, with a CAGR of 6.01% through 2031. In June 2025, the USDA raised wheat consumption estimates for Nigeria and Sudan, while Morocco’s flour demand increased due to higher expected imports tied to food security. The region’s reliance on imported wheat creates a strong trade pipeline, favoring globally positioned millers with extensive procurement networks. Saudi Arabia, the UAE, and Egypt anchor premium and high-volume demand in the Gulf and North Africa. Meanwhile, Kenya, Nigeria, and Ghana are witnessing rapid adoption of packaged and branded flour, driven by the expansion of modern retail and quick-service restaurants. Turkey adds strategic value as both a major flour consumer and an active regional exporter. These interconnected import, consumption, and re-export activities make MEA an attractive region in the commercial flour market, despite its smaller current share.

Competitive Landscape

The commercial flour market is moderately to highly concentrated, with major players like Ardent Mills, Archer Daniels Midland, Cargill, Nisshin Seifun Group, and GoodMills Group dominating large-scale industrial supply. These companies benefit from capital access, extensive sourcing networks, commodity risk tools, and investments in automation and traceability. This cost and capability gap challenges mid-sized operators in maintaining margins, making competition heavily influenced by operational scale and pricing.

Recent strategies show how leading companies are strengthening their positions in the commercial flour market. In December 2024, Wilmar International signed an option agreement to acquire 31.06% of Adani Wilmar’s equity from Adani Commodities LLP, enhancing its presence in India’s consumer staples and flour-related sectors. In July 2025, Ardent Mills acquired Stone Mill in North Dakota to expand its certified gluten-free and identity-preserved grain offerings. In June 2025, GoodMills Group reopened its expanded Kutno mill after a EUR 25 million (USD 28 million) investment, doubling its annual capacity to 280,000 tonnes. Nisshin Seifun Group also advanced its U.S. flour milling network, aiming for a 14% increase in domestic production capacity under its medium-term plan.

Opportunities remain in large-scale certified gluten-free processing, MEA expansion, and premium consumer flour channels. Fragmented specialty supply niches offer scaling potential for well-funded firms. However, bulk millers have yet to fully adopt premium direct-to-consumer flour models, as their systems prioritize industrial volume. As buyers increasingly value grain provenance and consistency, digital traceability—linking grain origin, processing, and nutritional claims—could become a key differentiator in the market.

Commercial Flour Industry Leaders

Ardent Mills

Archer Daniels Midland Company

Cargill, Incorporated

Grain Craft

GoodMills Group GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Crown Flour Mill Ltd., a subsidiary of Olam Agri, launched two new products in Nigeria: Mama’s Choice Wheat Flour and Mama’s Pride Semolina. The launch aims to address evolving consumer preferences and strengthen Olam Agri’s portfolio of fortified grain-based products. Mama’s Choice Wheat Flour is designed for household and confectionery applications, offering finer texture, whiter finished products, and lower oil absorption for products such as cakes, doughnuts, meat pies, and local snacks.

- April 2026: Sree Sai Roller Flour Mills launched MINAR Fortified Protein Plus Multigrain Atta, a nutrient-enhanced wheat flour designed to address rising consumer demand for healthier staple foods. The product was introduced with support from nutrition experts, industry representatives, and policymakers, highlighting the growing focus on food fortification and nutrition security in India.

- March 2026: AWL Agri Business launched Fortune Atta with Multigrains, a nutritionally enhanced flour made from eight grains including wheat, soy, chana, oats, barley, maize, fenugreek, and psyllium husk, targeting health-conscious consumers. The product is rich in protein, fibre, iron, and gut-friendly beta-glucan, offering a healthier alternative to conventional wheat flour.

Global Commercial Flour Market Report Scope

| Wheat Flour |

| Rice Flour |

| Corn Flour |

| Oat Flour |

| Rye Flour |

| Other Flours |

| Organic |

| Conventional |

| Industrial Applications | Food and Beverage Processors | Bakery and Confectionery |

| Pasta and Noodles | ||

| Snacks and RTE Foods | ||

| Other Food Manufacturers | ||

| Animal Feed | ||

| Other Industrial Applications | ||

| Foodservice/HoReCa | ||

| Household |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Flour Type | Wheat Flour | ||

| Rice Flour | |||

| Corn Flour | |||

| Oat Flour | |||

| Rye Flour | |||

| Other Flours | |||

| By Category | Organic | ||

| Conventional | |||

| By End User | Industrial Applications | Food and Beverage Processors | Bakery and Confectionery |

| Pasta and Noodles | |||

| Snacks and RTE Foods | |||

| Other Food Manufacturers | |||

| Animal Feed | |||

| Other Industrial Applications | |||

| Foodservice/HoReCa | |||

| Household | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the 2031 value forecast for commercial flour?

The commercial flour market is forecast to reach USD 72.9 billion by 2031, rising from USD 58.2 billion in 2026 at a 4.6% CAGR.

Which flour type holds the largest share globally?

Wheat flour led with 68.2% share in 2025 because bakery, pasta, noodle, and snack production still rely heavily on wheat-based formulations.

Which category is growing the fastest through 2031?

Organic flour is the fastest-growing category at a 5.5% CAGR, supported by stronger health-oriented demand and wider use in premium product reformulation.

Which region leads demand and which region is growing the fastest?

Asia-Pacific held the largest share at 43.22% in 2025, while the Middle East and Africa is expected to post the fastest growth at 6.0% CAGR through 2031.

Page last updated on: