Market Overview

| Study Period | 2021 - 2031 |

|---|---|

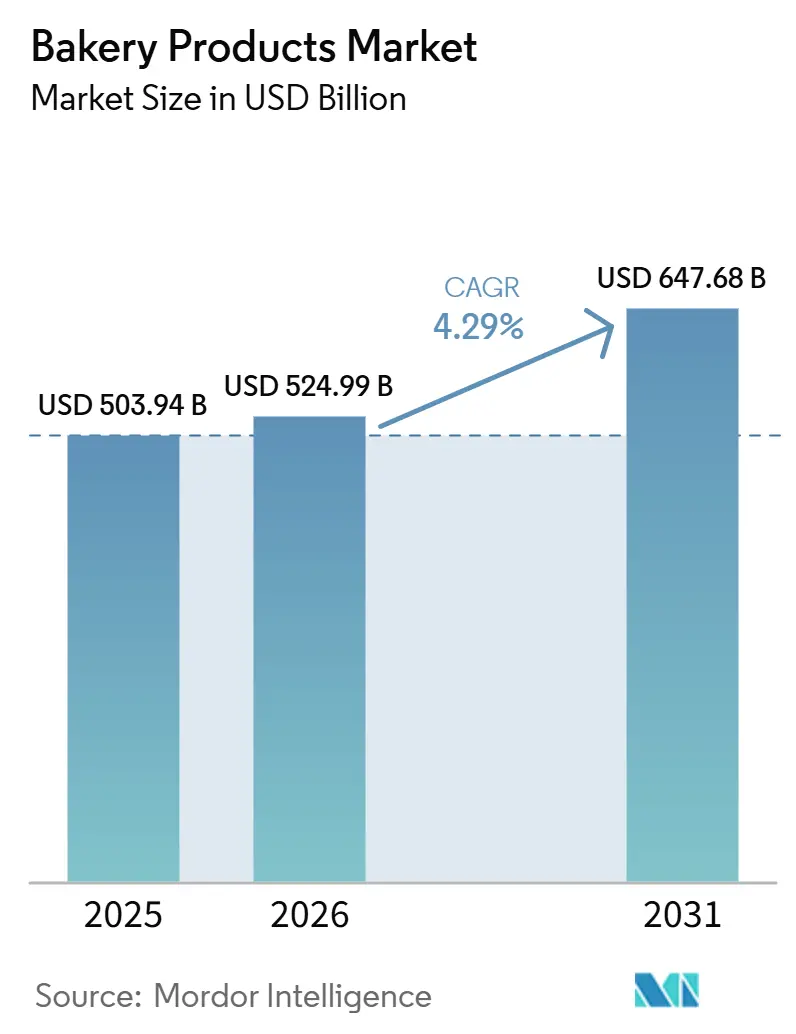

| Market Size (2026) | USD 524.99 Billion |

| Market Size (2031) | USD 647.68 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bakery Products Market Analysis by Mordor Intelligence

The global bakery products market size in 2026 is estimated at USD 524.99 billion, growing from the 2025 value of USD 503.94 billion, with 2031 projections showing USD 647.68 billion, growing at 4.29% CAGR over 2026-2031. Sustained growth in the bakery products market stems from steady demand for staple bread and a fast-rising appetite for health-forward snacks. Wider access to convenient retail channels also aligns with modern lifestyles. Upcycled ingredients certified by the Upcycled Food Association have moved from experimental trials to mainstream lines, signaling a shift toward circular-economy sourcing that resonates with eco-conscious shoppers [1]Source: Upcycled Food Association. "Savoring Sustainability: A 2024 Round-Up of Upcycled Food Trends." upcycledfood.org. Automation in the bakery products market is also reshaping production: robotic micro-bakeries embedded in stores deliver artisan-style freshness while easing chronic labor shortages, a pain point flagged by the majority of commercial bakers in 2024 workforce surveys.

Key Report Takeaways

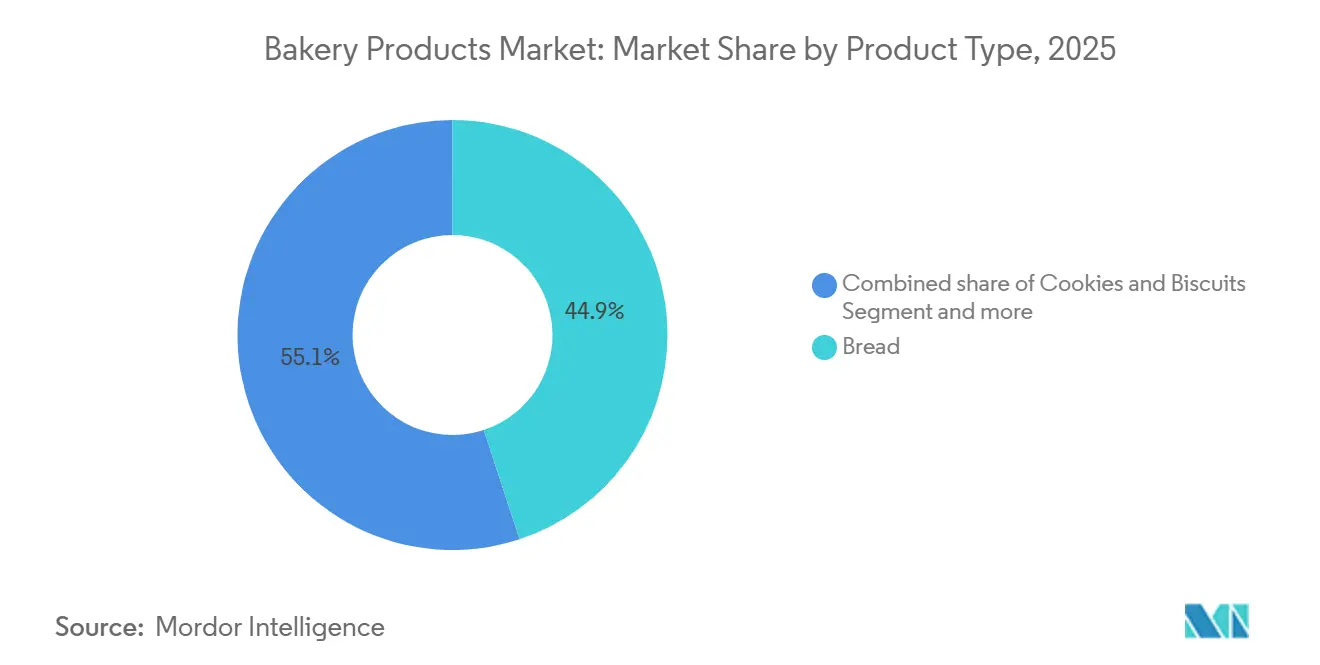

- By product type, bread led with 44.98% of the bakery products market share in 2025, while morning goods recorded the fastest rise at 5.52% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 46.85% share of the bakery products market in 2025; online retail is expanding at a 6.05% CAGR to 2031.

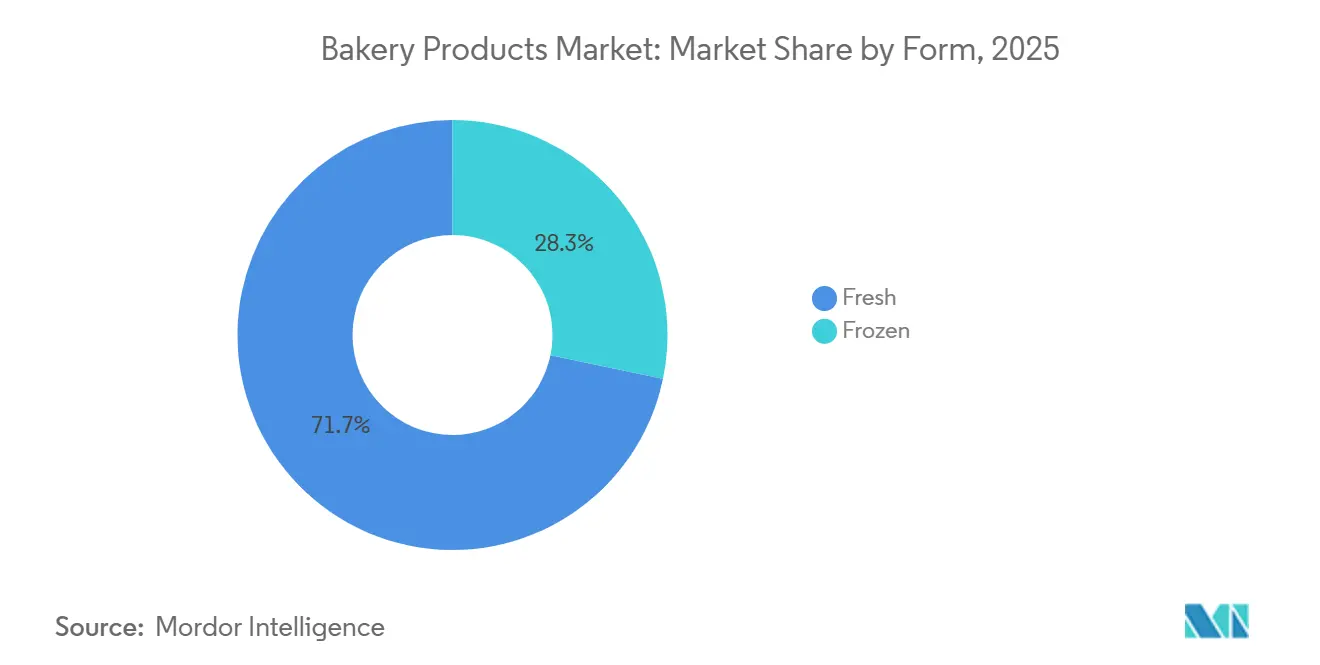

- By form, fresh items commanded 71.74% share of the bakery products market size in 2025, and frozen goods are advancing at a 6.49% CAGR through 2031.

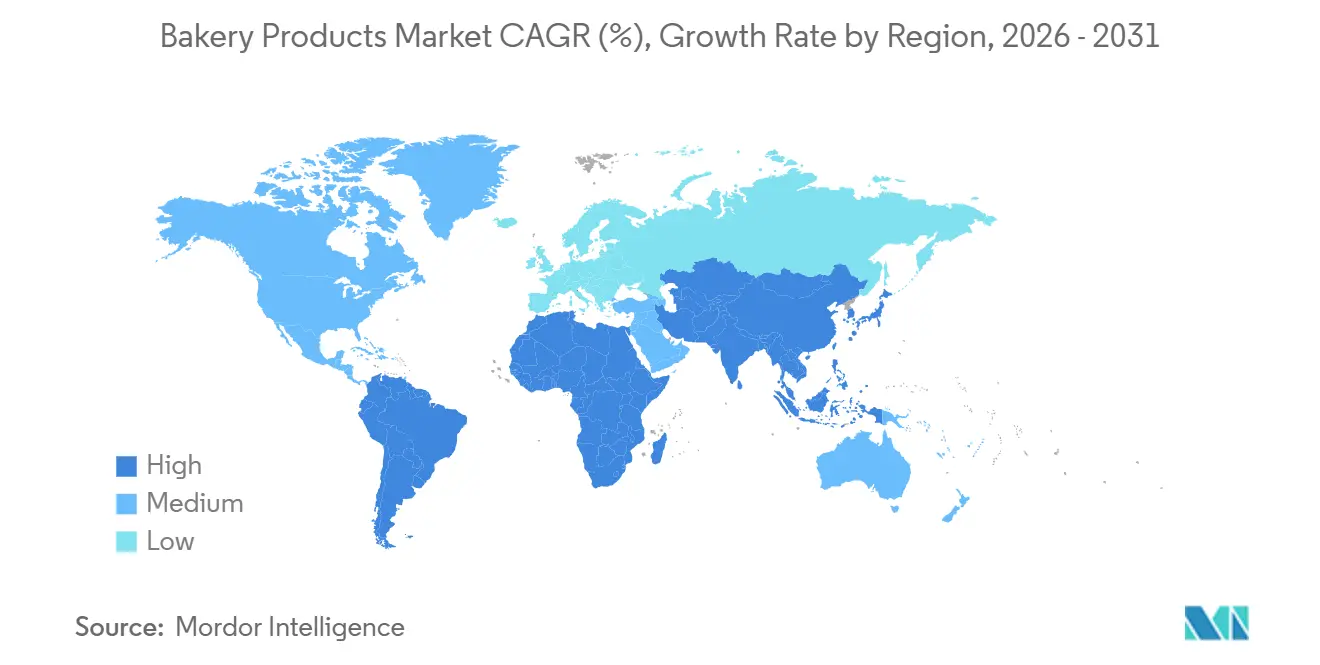

- By geography, Europe captured 32.84% of the bakery products market share in 2025, whereas Asia-Pacific shows the strongest upside with a 5.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gluten-free and allergen-free formulations | +0.8% | Global, early adoption in North America & Europe | Medium term (2-4 years) |

| On-the-go, portion-controlled bakery snacks | +0.6% | Global, especially Asia-Pacific metros | Short term (≤ 2 years) |

| Rising disposable incomes in emerging economies | +0.9% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Direct-to-consumer subscription bakeries | +0.4% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| Upcycled ingredients for cost and sustainability | +0.5% | Global, led by North America & Europe | Medium term (2-4 years) |

| In-store automated micro-bakeries lift freshness perception | +0.7% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Gluten-free and Allergen-free Formulations

In the bakery products market, regulators tightening label rules and consumers demanding inclusive diets are propelling gluten-free and allergen-free items from niche shelves into core bakery aisles. The 2024 FDA recall of mislabeled gluten-free loaves spotlighted the cost of compliance lapses and accelerated investment in dedicated production lines. Commercial Bakeries’ 2024 buyout of Imagine Baking added specialized R&D and separate allergen-controlled facilities, giving the acquirer a faster path into premium free-from segments. In the European Union, mandatory allergen statements became more conspicuous under updated regulations, nudging retailers to expand shelf space for certified products that simplify consumer choice [2]Source: FDA Agency News. "New Grains Gluten Free Bakery Issues Allergy Alert on Undeclared Eggs, Tree Nuts, Soy, and Milk in Bakery Products." forceforhealth. As ingredient suppliers unlock volume pricing for rice-, oat-, and sorghum-based flours, unit costs are declining, allowing mainstream brands to offer free-from variants with minimal price uplift. Retailers in North America and Europe now dedicate full bays to these lines, a practice mirrored by leading chains in Japan and Australia, signaling a lasting shift toward inclusive bakery offerings.

On-the-Go, Portion-Controlled Bakery Snacks

Urban commuters juggling tight schedules gravitate to single-serve muffins, filled croissants, and protein-enriched cookies that can be eaten in transit. The American Bakers Association’s 2024 roadmap placed special emphasis on merchandising smaller pack sizes to curb food waste and resonate with calorie-conscious buyers. Pack-tech innovators have responded with high-barrier films that retain softness for seven days without preservatives, supporting wider distribution windows [3]Source: American Bakers Association. "Charting the Course: ABA's Strategic Roadmap for 2024 and Beyond." americanbakers.org. Asia-Pacific convenience stores report double-digit sales growth for heat-and-eat buns targeting office workers, while social-media campaigns pairing portion guidance with QR-code nutrition panels reinforce healthy indulgence cues. Premium pricing on multipacks offsets higher material costs, boosting margins even as volume per pack shrinks.

Rising Disposable Incomes in Emerging Economies

World Bank projections show low-income nations expanding at 5.8% in 2025, unlocking discretionary spend for packaged foods. Latin American households likewise stretch grocery baskets to include value-added pastries, supported by wider cold-chain coverage. IMF (International Monetary Fund) analysis confirms that income elasticity dwarfs price sensitivity for bakery staples once per-capita GDP surpasses USD 4,000, underscoring the importance of macroeconomic tailwinds. Manufacturers that localize flavors, matcha in Vietnam, dulce de leche in Peru, garner higher basket penetration without abandoning global recipes, illustrating how economic lift and cultural cues converge to drive bakery premiumization.

In-Store Automated Micro-Bakeries Lift Freshness Perception

In-store automated micro-bakeries significantly drive demand by strengthening the perception of freshness, which is a key purchase trigger in bakery products. Consumers associate freshly baked, in-store items with better taste and quality, with over half of shoppers believing in-store bakery products are fresher than packaged alternatives. This enhanced freshness perception increases impulse buying, as the bakery is a highly impulsive category where more than 50–60% of purchases are unplanned. The live baking experience, through aroma, visibility, and real-time production, creates a strong sensory appeal, encouraging consumers to buy immediately. Additionally, micro-bakeries improve store image and attract higher footfall, as shoppers often choose stores based on bakery quality and freshness. Overall, by combining convenience with “just-baked” appeal, automated micro-bakeries convert perception into higher sales and repeat purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar, fat and additive health concerns | -1.2% | Global, especially developed markets | Short term (≤ 2 years) |

| Wheat and other cereal price volatility | -0.8% | Global, higher impact in price-sensitive economies | Short term (≤ 2 years) |

| Carbon-footprint scrutiny of supply chains | -0.4% | Europe, North America, developed Asia-Pacific | Medium term (2-4 years) |

| Skilled artisan-baker labor shortages | -0.6% | Global, acute in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sugar, Fat and Additive Health Concerns

Sugar, fat, and additive health concerns act as a key restraint in the bakery market by shifting consumer preferences toward healthier alternatives. High intake of added sugar, commonly found in bakery items like cakes, cookies, and pastries, is strongly linked to obesity, diabetes, and heart disease, making consumers increasingly cautious about frequent consumption. Similarly, concerns over saturated fats and artificial additives (preservatives, flavor enhancers) are raising awareness about long-term health risks, reducing demand for highly processed baked goods. As a result, many consumers are actively reducing indulgent bakery intake or switching to low-sugar, low-fat, and clean-label products. This trend is further reinforced by regulatory guidelines recommending limits on added sugar consumption, pushing brands to reformulate products. Consequently, traditional bakery segments, especially indulgent categories, face demand pressure, particularly among health-conscious and younger consumers.

Wheat and Other Cereal Price Volatility

Wheat and Other Cereal Price Volatility acts as a restraint on the bakery products market by increasing production costs and squeezing margins. Global supply disruptions, such as Black Sea export uncertainties, have led to sharp fluctuations in wheat prices, affecting both large and small-scale bakeries. Manufacturers unable to pass these cost increases to consumers may face reduced profitability, while recipe diversification or sourcing alternatives can add complexity and operational challenges. Additionally, frequent price swings make long-term planning and inventory management challenging for bakeries, particularly in price-sensitive markets. This volatility can also slow innovation, as companies may hesitate to launch new products when raw material costs are unpredictable. Overall, price volatility in key cereals limits growth and puts pressure on the affordability of bakery products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bread Dominance Meets Morning Goods Innovation

Bread generated the largest slice of the bakery products market size, accounting for 44.98% revenue in 2025. Population-wide familiarity, affordable pricing, and mealtime versatility anchor its lead, while continuous recipe tweaks, whole-grain, low-GI, or protein-fortified, align with evolving dietary ideals without alienating core consumers. Regulators allow tartaric acid derivatives up to 15,000 mg/kg, helping bakers manage texture during shelf life. Major players also explore sourdough fermentation to lend natural preservatives and artisan flavor cues.

Morning goods, though smaller, are the bakery products market’s fastest-moving niche with a 5.52% CAGR outlook. Grab-and-go culture underpins mini-croissants and muffins, while better-for-you twists, chia, flax, or reduced sugar, let brands capture indulgence and wellness in one pack. Suppliers such as Farinart launched customizable clean-label mixes to cut R&D time for smaller factories, fostering product diversity. The interplay of premiumization and convenience makes morning goods a magnet for both local craft bakers and global snack giants chasing incremental growth.

By Distribution Channel: Traditional Retail Strength Versus Digital Disruption

Supermarkets and hypermarkets contributed 46.85% of 2025 revenue, reaffirming their status as the primary touchpoint for everyday bread and pastry purchases. Their broad assortments support cross-category promotions, encouraging shoppers to pair bread with spreads or deli items. Private-label loaves now rival national brands on taste scores, letting retailers defend margins even under consumer watchdog scrutiny of grocery pricing.

Online retail, expanding at a 6.05% CAGR, brings the bakery products industry into living rooms through next-day delivery, insulated shippers, and subscription boxes promising rotating flavors. D2C bakers analyze order data to adjust weekly offerings, reducing waste and enhancing loyalty. E-commerce also democratizes access to niche gluten-free or vegan pastries that may lack shelf presence in brick-and-mortar stores. Pandemic-era habit shifts, particularly among millennials, have proven sticky, suggesting that digital channels will keep chipping away at supermarket dominance.

By Form: Fresh Preference Drives Frozen Innovation

Fresh items in the bakery products market controlled 71.74% of 2025 sales, supported by sensory appeal and the theater of in-store baking. Retailers market “bake-time stamps” to assure shoppers of recency, and loyalty-app push alerts notify when baguettes leave the oven. While freshness underwrites premium pricing, it also causes higher shrinkage; therefore, AI-driven forecasting tools optimize batch sizes daily. This blend of technology and tradition not only enhances customer satisfaction but also boosts the bottom line.

Frozen lines, projected to clock a 6.49% CAGR, address out-of-stocks and food-service demand for consistent quality across geographies. Isochoric freezing prevents ice crystals, preserving cell integrity and flavor better than conventional blast methods. The planned Vandemoortele–Délifrance merger to form a USD 2.5 billion frozen powerhouse underscores scale economics critical in this sub-segment. Longer shelf life enables regional distribution hubs, reducing transport emissions per loaf and aligning with Scope 3 reduction pledges. This strategic move not only solidifies their market position but also champions sustainability in the industry.

Geography Analysis

In 2025, Europe held the largest market share at 32.84% in the bakery products market, driven by its strong bakery culture, advanced retail systems, and regulations that encourage innovation despite being stringent. The introduction of new EU additive limits and the 2025 deforestation-free sourcing rule is pushing suppliers toward verifiable supply chains, increasing compliance costs but enhancing consumer trust. Merger and acquisition discussions, such as Kingsmill–Hovis talks, indicate market rationalization to address cost inflation and sustainability investments.

Additionally, nonprofit WRAP's goal of cutting greenhouse gas emissions is steering the industry toward eco-friendly packaging and renewable energy adoption in production facilities. Asia-Pacific, with a 5.62% CAGR, is the fastest-growing region, supported by a rising urban middle class and trade facilitation under the APEC Food Safety Modernisation Framework. Governments are revising nutrition policies, such as Singapore's 2025 expansion of Nutri-Grade to bakery beverages, which is driving reduced-sugar reformulations. Halal certification rollouts in Indonesia and Malaysia, while adding paperwork, are unlocking access to broader Muslim consumer markets. The region is also blending local and Western flavors, as seen in innovations like pandan-flavored swiss rolls and kimchi-stuffed buns.

North America in the bakery products market remains influential due to strong brand presence and advanced automation, though growth is modest due to market saturation. The American Bakers Association's “destination workplace” initiative aims to address skilled labor shortages, while state government grants help offset capital expenditures on energy-efficient ovens. South America, the Middle East, and Africa, though smaller in market share, are experiencing mid-single-digit growth driven by urban population increases and improved cold chain logistics. In Oman, the planned merger of Salalah Mills and Atyab Food highlights regional ambitions to scale up and establish a diversified bakery hub. These developments across regions reflect a dynamic global bakery market adapting to regulatory, sustainability, and consumer trends.

Competitive Landscape

With a low concentration score, the bakery products market showcases a fragmented landscape. This fragmentation, driven by diverse product categories, distribution channels, and regional preferences, allows both established multinational corporations and emerging regional players to carve out their niches through differentiated positioning strategies. Major players like Grupo Bimbo, Yamazaki Baking, and Mondelez International are not only consolidating to harness economies of scale but are also investing in automation technologies. These investments are crucial, especially given that industry workforce studies highlight a skilled labor shortage impacting the majority of commercial bakers. Navigating the maze of food safety and labeling regulations has become a competitive edge, granting companies enhanced market access and bolstered consumer trust.

Across the industry, strategic maneuvers are evident: vertical integration, a pivot towards direct-to-consumer channels, and innovations centered on sustainability. These efforts not only address carbon footprint concerns but also prioritize product quality and affordability. The Transition Pathway Initiative, in its scrutiny of the 26 largest publicly listed food producers, underscores the imperative for clearer disclosures on Scope 3 emissions and agricultural inputs. This presents a golden opportunity for companies to stand out by showcasing their environmental responsibility through transparent reporting and sustainable sourcing.

While there's a burgeoning demand for health-conscious product formulations and automated production technologies, the market also sees potential in expanding to emerging regions. However, challenges loom in the form of plant-based alternatives, subscription-based distribution models, and innovations in upcycled ingredients, all of which are reshaping traditional manufacturing and marketing paradigms. To navigate these waters, companies are turning to advanced technologies, from isochoric freezing preservation methods to automated micro-bakery systems, not just to capture market share but also to tackle challenges in labor availability and the push for sustainable supply chains.

Bakery Products Industry Leaders

-

Associated British Foods plc

-

Grupo Bimbo, S.A.B. de C.V.

-

Mondelēz International, Inc.

-

Yamazaki Baking Co. Ltd

-

Aryzta AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ITC Sunfeast Farmlite, known for its healthier biscuit offerings, expanded its portfolio by introducing a new range of sugar-free cookies. This move was in line with ITC's broader vision of 'Help India Eat Better'.

- April 2025: Vandemoortele and Délifrance announced their intention to merge, creating a new global leader in the frozen bakery market with an estimated combined turnover of EUR 2.4 billion, enhancing product offerings and accelerating sustainability initiatives across Europe and Asia.

- May 2024: Commercial Bakeries Corp completed the strategic acquisition of Hollandia Bakeries Ltd. and the Good Food Company Inc., expanding its capabilities in the North American private label cookie segment and enhancing its bakery network.

Global Bakery Products Market Report Scope

Bakery products are prepared from flour or meal derived from grains and are available in a wide range. The global bakery products market is segmented based on product type, distribution channel, form, and geography. The market has been segmented based on product type into cakes and pastries, biscuits, bread, morning goods, and other product types. Based on the distribution channel, the market has been segmented into hypermarkets/supermarkets, convenience/grocery stores, specialty stores, online retail stores, and other distribution channels. Based on form, it's divided into fresh and frozen. Finally, based on geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD).

By Product Type

| Bread |

| Cakes and Pastries |

| Biscuits/Cookies |

| Morning Goods |

| Other Product Types |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience and Grocery Stores |

| Specialty Bakery Stores |

| Online Retail Stores |

| Other Channels |

Form

| Fresh |

| Frozen |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bread | |

| Cakes and Pastries | ||

| Biscuits/Cookies | ||

| Morning Goods | ||

| Other Product Types | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience and Grocery Stores | ||

| Specialty Bakery Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| Form | Fresh | |

| Frozen | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the global bakery products market in 2026 and what growth is expected by 2031?

The market stands at USD 524.99 billion in 2026 and is projected to reach USD 647.68 billion by 2031, growing at a 4.29% CAGR.

Which product category holds the largest revenue share in bakery?

Bread dominates with 44.98% of 2025 sales, supported by universal consumption and continuous recipe innovation.

Which region shows the fastest growth momentum?

Asia-Pacific leads with a 5.62% CAGR through 2031, thanks to rising incomes, urbanization, and evolving dietary habits.

What retail channel is expanding the quickest?

Online retail, fueled by direct-to-consumer subscriptions and improved cold-chain logistics, is advancing at a 6.05% CAGR.

How are companies addressing labor shortages in baking?

Leading firms deploy automated micro-bakeries and robotic slicers that reduce manual workload while ensuring consistent product quality.

Page last updated on: