Tortilla Bread Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 39.51 Billion |

| Market Size (2031) | USD 47.49 Billion |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tortilla Bread Market Analysis by Mordor Intelligence

The global tortilla market was valued at USD 38.19 billion in 2025 and is currently estimated at USD 39.51 billion in 2026. It is projected to reach USD 47.49 billion by 2031, growing at a CAGR of 3.74% during the forecast period. The market has expanded beyond its origins as a regional staple to become a global convenience food, driven by the rise of on-the-go meal culture, diversification in quick-service restaurant (QSR) menus, and ongoing reformulations catering to health-conscious consumers. A key development often overlooked is that tortillas now compete directly with sandwich bread in developed markets. This competition is not as an ethnic alternative but as a functional packaging option that better meets dietary preferences, such as calorie-conscious, allergen-free, and high-protein requirements, compared to traditional sliced bread. This cross-category competition significantly influences the growth potential of the tortilla market, alongside demographic and culinary trends.

Key Report Takeaways

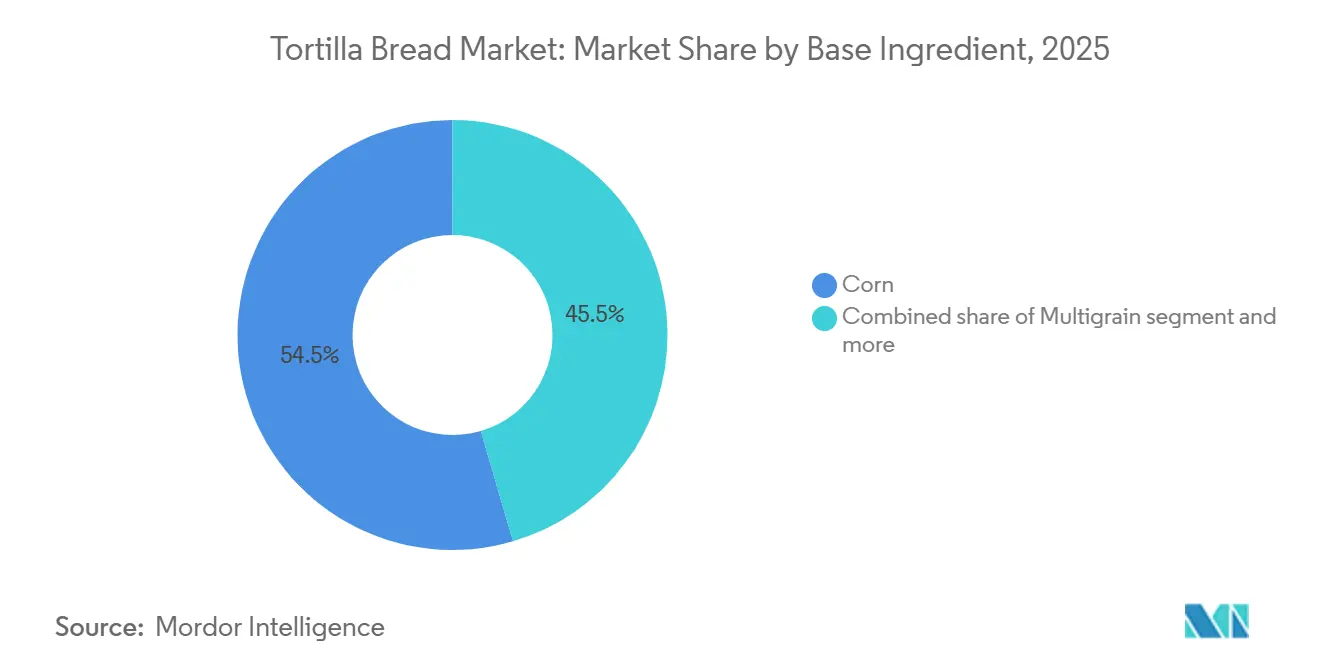

- By base ingredient, corn held 54.54% of 2025 revenue, while multigrain will post a 5.13% CAGR through 2031.

- By form, fresh led with 63.76% in 2025; frozen recorded the fastest 5.07% CAGR to 2031.

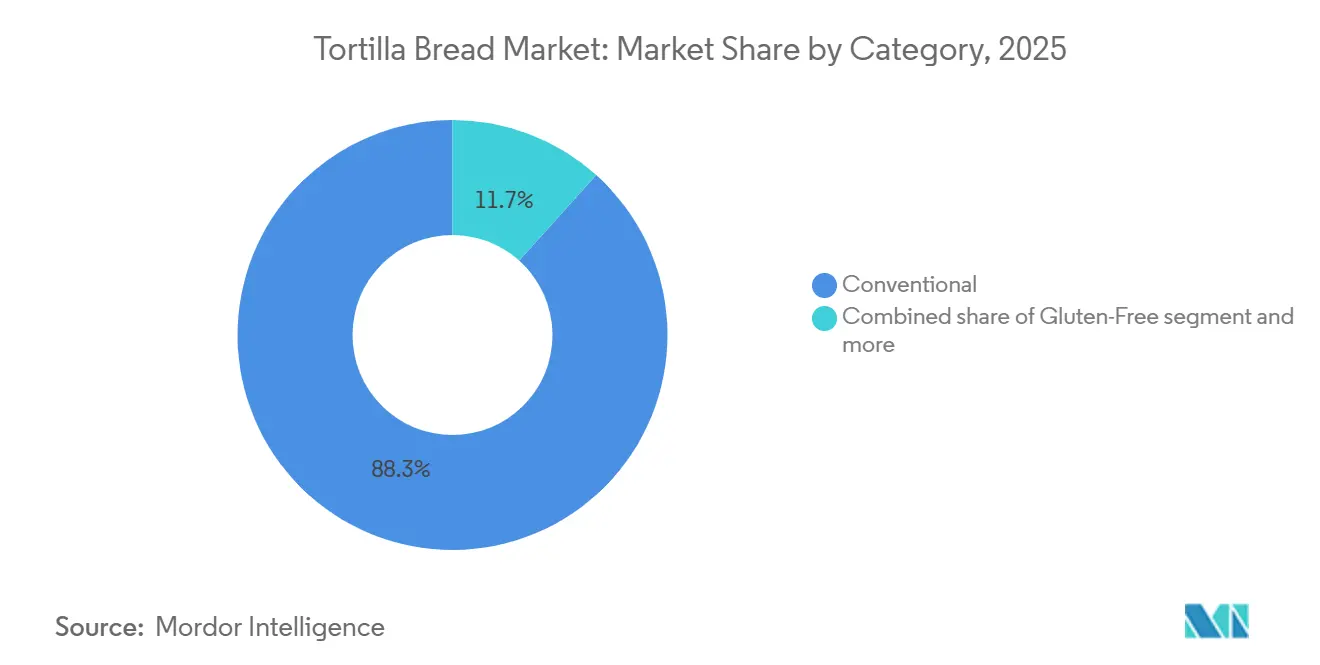

- By category, conventional accounted for 88.34% of 2025 demand, whereas gluten-free is forecast to grow at a 5.31% CAGR through 2031.

- By distribution channel, on-trade accounted for 55.11% of 2025 revenue, while off-trade is forecast to register a 4.96% CAGR through 2031.

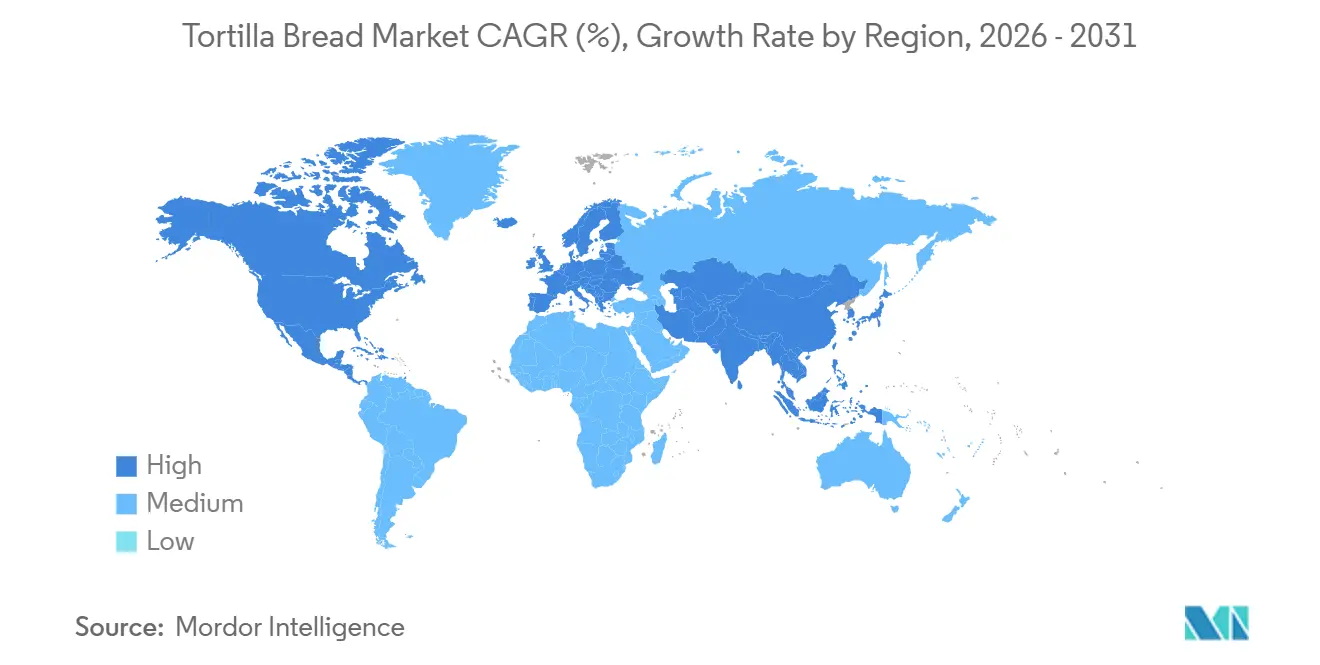

- By geography, North America accounted for 40.02% of 2025 sales, while Asia-Pacific will expand at a 4.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tortilla Bread Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for portable and on-the-go foods | +0.8% | Global; concentrated in North America, Asia-Pacific urban centers, and Western Europe | Short term (≤ 2 years) |

| Rising popularity of Mexican and Tex-Mex Cuisine | +0.7% | North America and Europe; spill-over to Asia-Pacific and Middle East and Africa | Medium term (2–4 years) |

| Product innovation in health-oriented tortillas | +0.6% | North America and European Union core; spill-over to Australia, Japan, South Korea | Long term (≥ 4 years) |

| Growth in foodservice chains | +0.9% | Global; led by North America, Asia-Pacific , and emerging Middle East | Medium term (2–4 years) |

| Extended shelf life and convenient storage support frozen variants | +0.4% | Global; Asia-Pacific import-dependent markets and foodservice hubs | Long term (≥ 4 years) |

| Expansion of private-label tortilla offerings | +0.5% | North America and Europe; early stage in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing demand for portable and on-the-go foods

The increasing demand for portable and convenient food products is a significant driver of the tortilla bread market. Consumers are increasingly preferring ready-to-eat meal options that align with fast-paced urban lifestyles and busy work schedules. Tortilla bread, known for its versatility and ease of use in wraps, rolls, and sandwiches, has become a popular alternative to traditional bread in both retail and foodservice sectors. Its adaptability to various cuisines and dietary preferences further enhances its appeal, making it suitable for a wide range of consumers. This trend is further bolstered by rising workforce participation, particularly among women. In the United States, the employment rate of women is projected to increase from 54.7% in 2023 to 54.9% in 2025, highlighting the growing demand for quick-preparation and portable meal solutions [1]Source: U.S. Bureau of Labor Statistics, "Labor Force Statistics from the Current Population Survey", hbls.gov. Additionally, the increasing focus on health-conscious eating has led to the development of whole-grain and gluten-free tortilla options, further driving market growth.

Rising popularity of Mexican and Tex-Mex Cuisine

The growing popularity of Mexican and Tex-Mex cuisine is a significant factor driving the tortilla bread market. Increased consumer exposure to Mexican flavors has bolstered demand across both foodservice and retail channels. The substantial presence of Mexican restaurants in key markets highlights this trend, with approximately 11% of all restaurants in the United States offering Mexican food[2]Source: Convenience Organization, "Roughly 1 in 10 U.S Restaurants Serve Mexican Food", convenience.org. California and Texas collectively account for nearly 40% of these establishments, reflecting high regional consumption and consistent use of tortilla bread in tacos, burritos, wraps, and other menu items. Additionally, tortilla bread's versatility as a base for various dishes has made it a staple in both traditional and fusion cuisines, further expanding its appeal among diverse consumer groups. The growing trend of convenience foods and ready-to-eat meals has also contributed to the increased adoption of tortilla bread in households and foodservice outlets.

Product innovation in health-oriented tortillas

The health-oriented tortilla segment is evolving with a focus on specific nutritional and functional attributes, setting it apart from general "better-for-you" trends. Manufacturers are emphasizing factors such as protein content, net carbohydrate count, glycemic index, and gut microbiome health rather than relying on broad wellness claims. This development aligns with data showing that 61% of the U.S. as of 2024[3]Source: Cargill, "Consumers are Seeking More Protein for Health and Taste in 2025", cargill.com. Consumers are actively seeking to increase their protein intake, driving demand for high-protein tortilla products and other functional bakery options. In response to this trend, La Tortilla Factory launched Protein and Sourdough refrigerated tortilla varieties in March 2026, addressing consumer interest in gut-healthy, high-protein, and convenient meal solutions. Furthermore, increased regulatory scrutiny from the FDA on synthetic color additives and seed oils is accelerating product reformulation. This has led manufacturers to adopt cleaner ingredient profiles, aiming to gain a competitive edge in natural and health-focused retail markets.

Growth in foodservice chains

The expansion of foodservice chains is significantly boosting the demand for tortilla bread as restaurants, quick-service restaurants (QSRs), and fast-casual outlets increasingly feature wraps, burritos, tacos, and other tortilla-based items on their menus. This trend is driven by the growing consumer inclination toward meals that are not only convenient and customizable but also reflect global culinary influences. The growth of foodservice networks has further amplified this demand, as these establishments seek to cater to diverse consumer tastes and preferences. Additionally, menu innovation, such as the introduction of fusion dishes and healthier tortilla options, along with the increasing popularity of Mexican and Tex-Mex cuisine, is reinforcing the presence of tortilla bread in both established and emerging foodservice channels. These factors collectively highlight the evolving role of tortilla bread as a versatile and essential component in modern dining experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile corn and wheat prices | -0.6% | Global; most acute in import-dependent markets (Europe, Asia-Pacific, Middle East and Africa) | Short term (≤ 2 years) |

| High competition from traditional bread products | -0.4% | Europe, North America, South America | Medium term (2–4 years) |

| Consumer perception of processed food | -0.3% | North America and Western Europe | Medium term (2–4 years) |

| Short shelf life of fresh and preservative-free variants | -0.5% | Emerging markets with limited cold-chain infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile corn and wheat prices

Volatile corn and wheat prices present a considerable challenge to the tortilla bread market, as these commodities are the primary raw materials for tortilla production. Variations in crop yields, adverse weather conditions, supply chain disruptions, geopolitical uncertainties, and fluctuating agricultural input costs contribute to unpredictable changes in ingredient prices, thereby increasing manufacturers' production costs. This price volatility can reduce profit margins, especially for smaller producers with limited purchasing power, and complicate efforts to maintain stable product pricing and secure long-term supply agreements. Additionally, the unpredictability in raw material costs can force manufacturers to frequently adjust their procurement strategies and production schedules, further straining operational efficiency. For consumers, these fluctuations may lead to inconsistent pricing, potentially affecting demand and market stability over time.

High competition from traditional bread products

High competition from traditional bread products poses a challenge to the tortilla bread market. Consumers continue to favor established bakery staples such as sliced bread, rolls, buns, and flatbreads for everyday meals. These products enjoy widespread availability, strong consumer familiarity, and a broad range of options catering to various price points and dietary preferences. Additionally, traditional bread products benefit from entrenched purchasing habits and established distribution networks, making them a convenient choice for consumers. In many regions, tortilla bread is still viewed as a niche or cuisine-specific product, which restricts its adoption among consumers who prefer conventional bread formats for sandwiches, breakfast items, and general household use. This perception is further reinforced by limited marketing efforts and a lack of integration into mainstream meal routines in some markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base Ingredient: Corn Dominates, Multigrain Accelerates

Corn tortillas accounted for 54.54% of the global market in 2025, driven by their cultural authenticity, cost-effectiveness, and naturally gluten-free characteristics. These attributes address both traditional consumer preferences and evolving dietary needs. The second-largest ingredient category, wheat/flour, caters to a different demand segment, particularly in the foodservice channel, where its pliability and suitability for large-format applications make it the preferred choice for wraps and burritos at scale.

Multigrain is the fastest-growing ingredient segment, with a 5.13% CAGR projected through 2031. This growth is fueled by investments from established manufacturers and specialty producers aiming to differentiate through enhanced nutritional profiles. Key competitive factors include fiber content, micronutrient fortification, and multi-grain blends. For example, Limagrain Ingredients introduced blue masa flour, made from traditional Mexican blue maize, to the European snack market.

By Form: Fresh Commands Scale, Frozen Closes the Gap

Fresh tortillas accounted for 63.76% of the global market in 2025, driven by consumer preference for quality and authenticity, along with the cost efficiency of ambient shelf storage at the point of sale. Within the fresh category, the refrigerated subsegment demonstrated stronger growth compared to the broader shelf-stable category. For instance, Siete Family Foods (a PepsiCo subsidiary) reported 22.2% growth in the refrigerated tortilla segment in the United States for the 52 weeks ending March 2025.

Frozen tortillas are projected to grow at a CAGR of 5.07% during 2026–2031, supported by three key factors: the need for standardized, centrally manufactured formats with extended shelf life for quick-service restaurant (QSR) operators; the expansion of export-oriented supply chains in regions with limited fresh delivery infrastructure; and increasing retail demand for freezer-aisle convenience products. According to Farm Credit Canada's 2026 Food and Beverage Report, QSRs have emerged as the largest and most resilient downstream market for baked goods and wraps post-pandemic, a trend that aligns with the supply-chain advantages of frozen formats.

By Category: Conventional Prevails, Gluten-Free Sets the Pace

Conventional tortillas accounted for 88.34% of the global market share in 2025. This dominance is attributed to the high volume of foodservice procurement and the price sensitivity of mainstream retail consumers. These factors are particularly significant in Latin America and developing markets, where tortillas are deeply ingrained in daily diets as a staple food rather than being perceived as a premium or lifestyle product. The affordability and widespread availability of conventional tortillas further reinforce their strong market position.

In the non-conventional segment, gluten-free tortillas represent the fastest-growing category, with a CAGR of 5.31% through 2031. This growth is driven by an increase in celiac disease and non-celiac gluten sensitivity diagnoses, particularly in North America and Europe, where awareness of gluten-related health issues is rising. Additionally, there is a growing consumer preference for simplified ingredient lists, reflecting a broader trend toward clean-label products. This demand extends beyond individuals with clinical dietary restrictions, as more consumers prioritize transparency and perceived health benefits in their food choices.

By Distribution Channel: On-Trade Leads as Off-Trade Gains Ground

On-trade channels accounted for 55.11% of global tortilla revenue in 2025, highlighting their significant role within quick-service restaurants (QSR), fast-casual dining, and institutional foodservice. Tortillas serve as a key ingredient for operators, driving consistent bulk-purchase demand that is both stable and relatively price-inelastic. This dominance is further supported by ongoing menu innovation. For instance, Zaxby's introduced Giant Chicken Finger Wraps in a 10-week promotional campaign across more than 1,000 locations in 2026. This initiative created a new demand for flour tortillas at a QSR chain where tortillas were not previously a core ingredient.

Off-trade channels are projected to grow at a faster rate, with a compound annual growth rate (CAGR) of 4.96% through 2031. Supermarkets and hypermarkets remain the primary distribution channels for volume, while online retail is emerging as the fastest-growing sub-channel. This growth in online retail allows specialty and premium brands to target health-conscious consumers without competing for limited shelf space in mainstream retail outlets.

Geography Analysis

North America accounted for the largest share of the tortilla bread market, representing 40.02% of revenue in 2025. This dominance is attributed to the strong popularity of Mexican and Tex-Mex cuisine, high consumption of wraps and burritos, and the widespread presence of foodservice chains offering tortilla-based menu items. The region's well-established food culture, combined with a growing preference for convenient and versatile meal options, has further fueled the demand for tortilla bread. Continuous product innovation, such as gluten-free, high-protein, and clean-label tortillas, caters to evolving consumer preferences and drives market growth in the United States, Canada, and Mexico.

The Asia-Pacific region is projected to be the fastest-growing market, with a CAGR of 4.88% during 2026–2031. Factors such as rising urbanization, increased exposure to Western and international cuisines, and growing demand for convenient meal options are driving the adoption of tortilla bread. The region's expanding middle-class population, coupled with changing dietary habits, has created a favorable environment for tortilla bread consumption. The expansion of quick-service restaurants, fast-casual dining outlets, and modern retail channels is further enhancing market penetration in countries like China, India, Japan, and Australia. Additionally, the increasing availability of tortilla bread in supermarkets and online platforms is making it more accessible to consumers.

Europe, Latin America, and the Middle East and Africa are experiencing steady growth in tortilla bread consumption. This growth is supported by increasing consumer interest in ethnic cuisines and versatile bread alternatives. In Europe, the rising popularity of Mexican cuisine and the incorporation of tortillas into fusion dishes are key drivers. In Latin America, the traditional use of tortillas as a staple food continues to sustain demand, while in the Middle East and Africa, the growing influence of Western food trends is boosting adoption. Factors such as growing retail availability, menu diversification by foodservice operators, and rising demand for convenient meal solutions contribute to market expansion in these regions.

Competitive Landscape

The tortilla bread market is moderately consolidated, comprising large multinational bakery companies and specialized tortilla manufacturers. These players compete through strategies such as product innovation, distribution expansion, and brand positioning. Established companies benefit from extensive retail and foodservice networks, while regional manufacturers capitalize on local consumer preferences and strong relationships with foodservice operators to sustain their market presence.

Competition increasingly focuses on health-oriented product development. Companies are introducing high-protein, gluten-free, sourdough, multigrain, and clean-label tortilla products to meet changing consumer preferences. Additionally, manufacturers are investing in flavor innovation, alternative ingredients, and functional formulations to diversify their portfolios and cater to health-conscious consumers seeking convenient meal options.

Beyond product innovation, companies are prioritizing expansion across foodservice and retail channels. This is achieved through strategic partnerships, broader distribution networks, and enhanced production capabilities. The rising popularity of Mexican and Tex-Mex cuisine, along with increased at-home consumption of wraps and tortilla-based meals, drives market participants to enhance brand visibility and expand product offerings to gain a competitive edge.

Tortilla Bread Industry Leaders

-

GRUMA S.A.B. de C.V.

-

Grupo Bimbo S.A.B. de C.V.

-

PepsiCo Inc.

-

Ole Mexican Foods Inc.

-

Tyson Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Hero Bread has launched a Spinach & Herb Tortilla under its Hero Tortillas line, broadening its flavor offerings beyond plain and burrito-size options. Made with real ingredients like spinach, thyme, chives, parsley, and garlic, the product is marketed as a savory, better-for-you tortilla with a natural green color derived from its ingredients rather than artificial additives.

- April 2026: PepsiCo subsidiary Siete Foods has introduced two new products to its gluten-free, heritage-inspired tortilla range: Maíz Organic Yellow Corn Tortillas and Sourdough Style Tortillas. These products aim to combine traditional Mexican-American culinary roots with modern dietary preferences.

- March 2026: La Tortilla Factory has launched two new refrigerated tortilla options: high-protein tortillas and sourdough-style tortillas. The high-protein variant addresses the growing interest in protein-rich diets and functional nutrition, while the sourdough-style tortilla aligns with trends in gut health and fermented foods, offering an artisanal alternative to conventional tortillas.

- March 2025: PACHA has unveiled Sourdough Buckwheat Tortillas, a unique product made with sprouted buckwheat and sea salt. Positioned as a clean-label, gut-friendly, and allergen-free option, these tortillas are naturally gluten-free, grain-free, and free from common allergens such as wheat, corn, soy, dairy, and nuts. The sourdough fermentation process enhances both digestibility and flavor.

Global Tortilla Bread Market Report Scope

| Corn |

| Wheat |

| Multigrain |

| Rice |

| Cassava |

| Other Alternative Grains |

| Fresh |

| Frozen |

| Conventional |

| Gluten-Free |

| Organic |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Retail Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Base Ingredient | Corn | |

| Wheat | ||

| Multigrain | ||

| Rice | ||

| Cassava | ||

| Other Alternative Grains | ||

| By Form | Fresh | |

| Frozen | ||

| By Category | Conventional | |

| Gluten-Free | ||

| Organic | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the market size of tortilla bread in 2026?

The tortilla bread market is valued at USD 39.51 billion in 2026.

Which base ingredient segment leads the market?

Corn-based tortilla bread holds the largest share at 54.54% in 2025.

Which region dominates the tortilla bread market?

North America leads the market with a 40.02% share in 2025.

Which segment is growing the fastest?

The gluten-free category is the fastest growing segment with a 5.31% CAGR (2026–2031).

Page last updated on: