Market Overview

| Study Period | 2021 - 2031 |

|---|---|

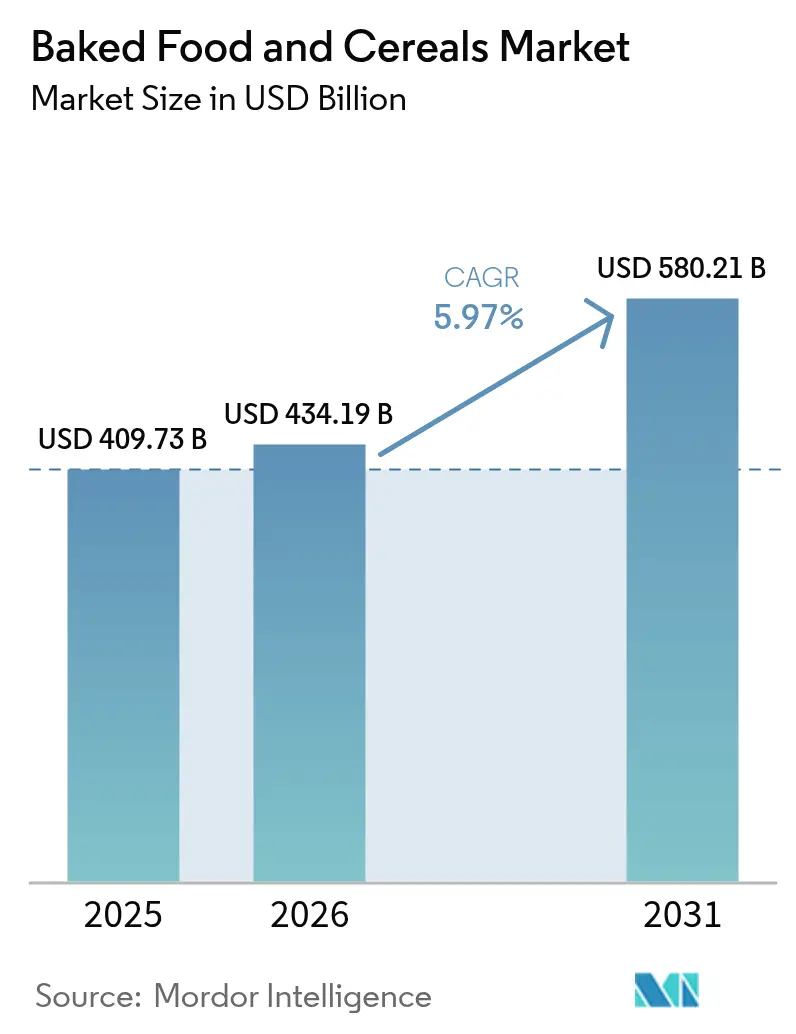

| Market Size (2026) | USD 434.19 Billion |

| Market Size (2031) | USD 580.21 Billion |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

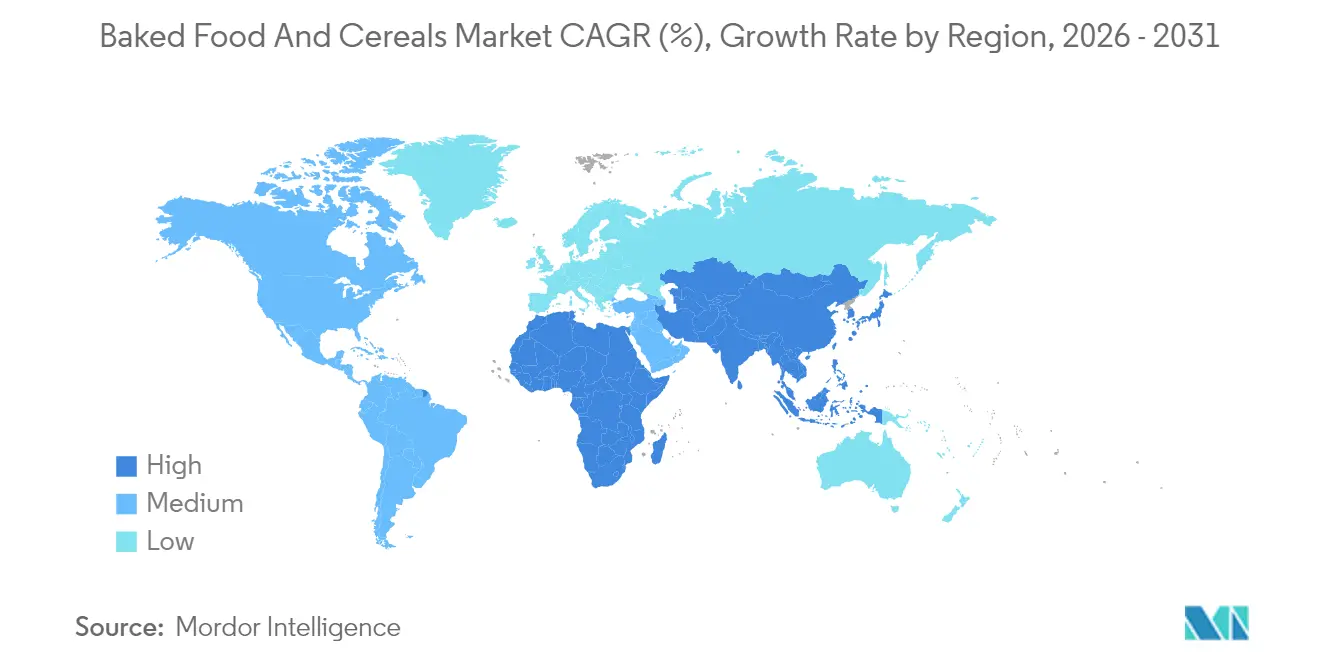

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Baked Food And Cereals Market Analysis by Mordor Intelligence

In 2025, the baked foods and cereals market size was valued at USD 409.73 billion. baked foods and cereals market size in 2026 is estimated at USD 434.19 billion, growing from 2025 value of USD 409.73 billion with 2031 projections showing USD 580.21 billion, growing at 5.97% CAGR over 2026-2031. This growth is largely driven by an increasing appetite for convenient breakfast and snack options, a regulatory push towards organic certifications, and a notable shift in grocery spending towards digital platforms. Major manufacturers are expanding their offerings, introducing protein-fortified breads, gluten-free crackers, and fiber-rich cereals, all aimed at health-conscious consumers. They're also navigating raw material price fluctuations through strategies like forward contracting and utilizing frozen formats. While budget-conscious shoppers are leaning towards private-label products, premium artisanal items are carving out a niche, boosting margins through a focus on authenticity, local sourcing, and techniques like sourdough fermentation. In today's competitive landscape, success hinges on strategies like omnichannel merchandising, packaging tailored for last-mile delivery, and rolling out innovations that blend indulgence with health-conscious cues.

Key Report Takeaways

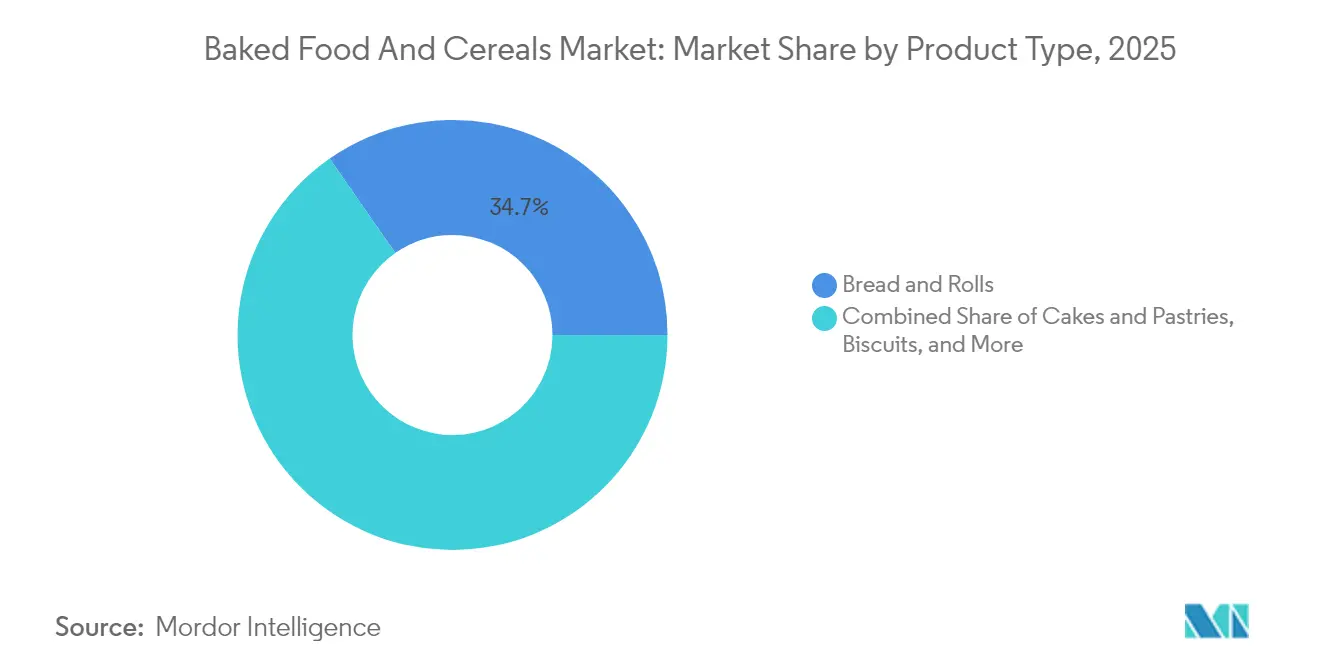

- By product type, bread and rolls commanded 34.68% of the baked food and cereals market share in 2025, while crackers and savory biscuits are poised to expand at a 6.98% CAGR through 2031.

- By category, conventional lines held 61.75% revenue share in 2025; organic offerings are forecast to grow at an 7.79% CAGR between 2026 and 2031.

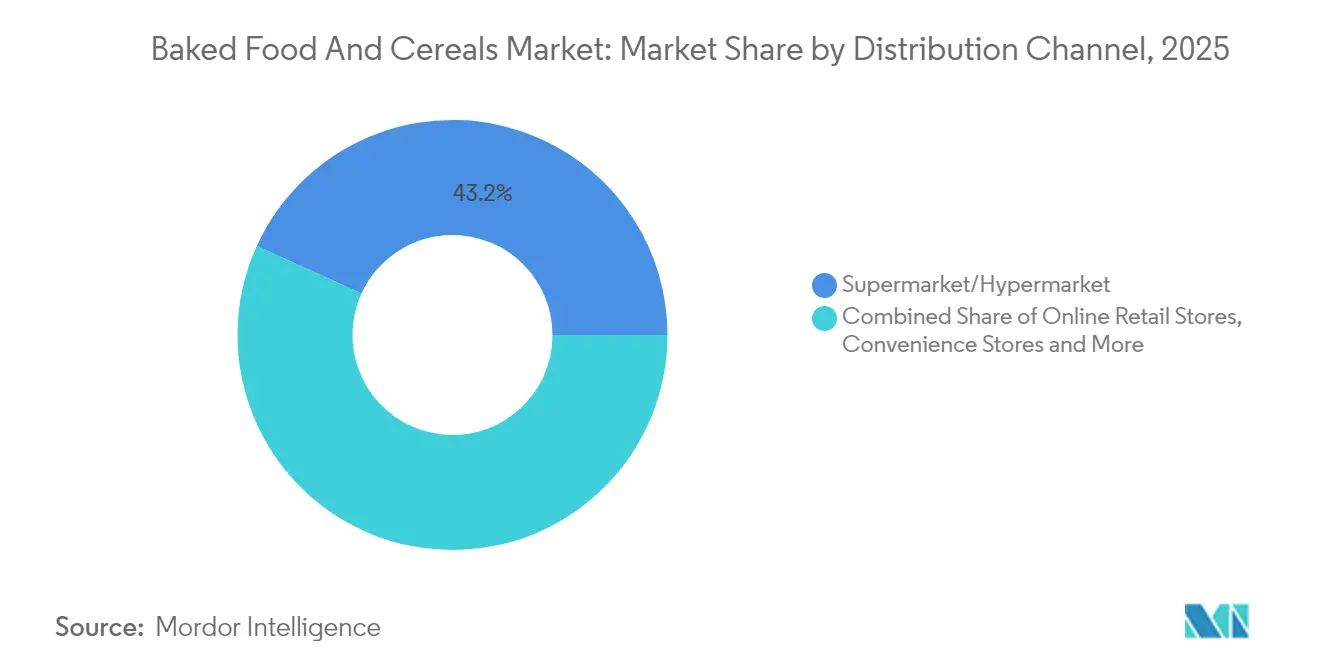

- By distribution channel, supermarkets and hypermarkets led with 43.21% of the baked food and cereals market size in 2025, whereas convenience stores are projected to post a 7.55% CAGR.

- By geography, North America accounted for 36.18% revenue share in 2025; Asia-Pacific is expected to rise at an 8.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Baked Food And Cereals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer demand for convenient and on-the-go breakfast and snack options | +1.2% | Global, with concentration in North America and urban Asia-Pacific | Medium term (2-4 years) |

| Rising interest in organic and clean-label baked foods and cereals | +1.1% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of e-commerce and digital retail channels | +0.9% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Innovation in product formulations | +0.8% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Rising consumer shift towards snacking culture | +1.0% | Global, particularly strong in North America and Europe | Medium term (2-4 years) |

| Growing popularity of artisanal and specialty bakery products | +0.7% | Europe and North America, emerging in Asia-Pacific urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand for Convenient and On-the-Go Breakfast and Snack Options

Urbanization and busy daily routines have made portable, shelf-stable food formats a common choice rather than a niche option. The United States Department of Agriculture reports that 83% of children and adults eat breakfast daily, often during their commute or at work[1].The U.S. Department of Agriculture (USDA), "Breakfast Consumption by U.S. Children and Adolescents", ars.usda.gov This shift has encouraged manufacturers to create single-serve products that are both filling and nutritious, catering to changing eating habits that move away from traditional meal patterns. Retailers have adapted by increasing grab-and-go sections and chilled bakery areas to serve consumers looking for fresh, ready-to-eat options. The demand for convenience and nutrition has also led to innovations like protein-fortified biscuits and fiber-enriched breakfast bars, as brands strive to combine health benefits with good taste and texture. For example, Warburtons launched Protein Flatbreads in August 2024, targeting fitness-conscious consumers who value macronutrient-rich, portable food options.

Rising Interest in Organic and Clean-Label Baked Foods and Cereals

Regulatory standardization and increasing consumer concerns about synthetic additives are driving a shift toward organic and clean-label products. The organic food market in the European Union is growing at 6% annually, supported by unified certification frameworks across member states and more shelf space allocated by retailers. The United States Department of Agriculture's Organic Integrity Database lists over 41,000 certified operations worldwide, showing the significant supply chain changes needed to meet the demand for traceable and pesticide-free ingredients. A report by Puratos reveals that 73% of consumers prefer familiar ingredients in their food, highlighting a demand for simple and recognizable ingredient lists instead of complex chemical names. This preference also influences production methods, with sourdough fermentation becoming more popular for its ability to lower the glycemic index and improve mineral absorption without using synthetic additives.

Expansion of E-Commerce and Digital Retail Channels

Digital commerce has shifted from being an additional option to a critical part of business strategy, as shopping habits formed during the pandemic have become permanent. Vietnam's food e-commerce market grew at a positive compound annual growth rate between 2020 and 2024, showing how emerging markets are skipping traditional retail systems and moving directly to mobile-first shopping. This change has led manufacturers to redesign packaging for direct-to-consumer deliveries, ensuring it is durable for shipping while still appealing for unboxing. Subscription services and customized product assortments have made online shopping more attractive, helping brands secure repeat customers and collect data to improve products. In 2024, the Supplemental Nutrition Assistance Program expanded online acceptance to more retailers, making digital shopping accessible to lower-income households and increasing the customer base for e-commerce bakery and cereal products.

Innovation in Product Formulations

Reformulation has become crucial as health-conscious consumers pay closer attention to sodium, sugar, and saturated fat levels in products. DIOSNA has highlighted significant efforts to reduce salt and sugar content while maintaining taste, using enzyme technologies and fermentation processes to improve flavor. Sourdough fermentation naturally increases shelf life, reducing the need for preservatives and meeting clean-label requirements without affecting product stability. Functional ingredients like plant-based proteins, omega-3 fatty acids, and prebiotic fibers are being added to crackers and breakfast cereals, turning them into products that offer specific health benefits. In February 2024, Britannia Industries introduced Nutrichoice Essentials high-protein digestive biscuits to cater to the growing demand for functional snacks that support active lifestyles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly fragmented market with intense competition | -0.5% | Global, particularly acute in mature markets like North America and Europe | Short term (≤ 2 years) |

| Supply chain disruptions and raw material price volatility | -0.8% | Global, with acute pressure in import-dependent regions | Medium term (2-4 years) |

| Perishability and short shelf life | -0.4% | Global, more pronounced in regions with underdeveloped cold chain infrastructure | Medium term (2-4 years) |

| Health concerns over gluten and allergen content | -0.6% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions and Raw Material Price Volatility

Wheat supply issues and trade restrictions have caused significant instability in ingredient procurement. According to the Organisation for Economic Co-operation and Development and the Food and Agriculture Organization, global wheat stocks have fallen to 257.6 million metric tons, the lowest level in nine years[2]Organisation for Economic Co-operation and Development and Food and Agriculture Organization, "OECD-FAO Agricultural Outlook 2024-2033.", oecd.org.. This drop has reduced supply reserves, making prices more vulnerable to weather changes and policy decisions. Following the Ukraine conflict, 63 food-related export restrictions were imposed, disrupting global trade and forcing importers to find alternative sources at higher costs. In the United States, the wheat season-average farm price for 2024/25 is projected to be between USD 5.55 and USD 5.60 per bushel. While relatively stable, this price remains higher than pre-pandemic levels, keeping costs elevated for millers and bakers. From October to December 2024, flour milling activity totaled 231 million bushels, a 2% increase from the previous year, reflecting strong demand that continues to strain supply and limit price relief.

Perishability and Short Shelf Life

Fresh bakery products face significant shelf-life limitations, complicating inventory management, distribution logistics, and waste reduction efforts. Suppliers to major retailers operate under weekly tender systems and risk rejection for quality deviations, posing challenges for producers without scale or cold-chain infrastructure. Sourdough fermentation provides a natural solution by extending shelf life through organic acid production, reducing the need for chemical preservatives while supporting clean-label positioning. Frozen bakery formats have also emerged as a strategic approach, allowing centralized production, extended distribution timelines, and reduced spoilage risks. Grupo Bimbo's acquisition of Pagnifique in Uruguay in September 2024 expanded its frozen bread and pastry offerings, utilizing freezing technology to serve geographically dispersed markets without compromising product quality. However, the balance between freshness perception and logistical efficiency remains a strategic challenge, as consumers often associate shorter shelf life with artisanal quality, while retailers prioritize products that minimize markdown losses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bread Anchors Volume, Crackers Drive Growth

Bread and rolls held a 34.68% market share in 2025, remaining a key category due to their widespread use in daily meals and affordability, which appeals to consumers across all income levels. Sourdough bread has seen growing demand because of its lower glycemic index and better mineral absorption, making it a popular choice for health-conscious consumers looking for nutritious options without compromising on taste or tradition. Premium products, featuring artisanal preparation and whole-grain ingredients, enable brands to stand out and maintain profitability despite competition from private-label alternatives.

Crackers and savory biscuits are expected to grow at a 6.98% CAGR from 2026 to 2031, driven by their increasing popularity as snacks and their versatility as meal accompaniments or standalone options. The demand for GMO-free crackers has grown at a positive rate, highlighting a strong consumer preference for clean-label products with simple and transparent ingredients, even at premium prices. Cheese crackers experience a seasonal surge in demand during December, while ongoing innovations in plant-based proteins and functional ingredients continue to drive steady growth throughout the year.

By Category: Conventional Dominates, Organic Accelerates

Conventional products held a 61.75% market share in 2025, driven by their affordability and widespread availability, which appeal to cost-conscious consumers dealing with inflation. During periods of economic uncertainty, consumers often opt for more affordable options, maintaining steady demand for conventional products. In 2023, Aldi opened 109 new stores across the United States, strengthening its position as a discount retailer. This expansion helped Aldi capture market share from traditional supermarkets and increased the presence of private-label products in bakery and cereal categories. Conventional products also benefit from efficient supply chains and manufacturing processes, which allow competitive pricing while ensuring consistent availability and product variety.

Organic alternatives are expected to grow at a compound annual growth rate (CAGR) of 7.79% from 2026 to 2031, supported by clearer regulations and growing consumer preference for certified pesticide-free ingredients. According to the United States Department of Agriculture's Organic Integrity Database, there are over 41,000 certified organic operations worldwide, reflecting the significant changes in supply chains to meet the demand for traceable organic products. In February 2024, Nature's Path launched Organic Sprouted Grain Toaster Pastries, which use sprouted grains to improve nutrient content while adhering to clean-label standards. Organic certification also builds consumer trust in markets where there is skepticism about synthetic additives and genetically modified organisms. This trust justifies the higher prices of organic products, ensuring profitability despite increased production costs.

By Distribution Channel: Supermarkets Lead, Convenience Stores Surge

Supermarkets and hypermarkets accounted for 43.21% of the market share in 2025, leveraging their scale, broad product assortment, and promotional strategies to dominate bakery and cereal distribution. The expansion of private-label products within this channel has intensified competition, as retailers utilize bakery and cereal categories to drive traffic and contribute to profit margins. Discount formats, such as Aldi and Lidl, have disrupted traditional supermarket economics, with Poland's discount channel capturing the majority of value share. This has compelled established players to streamline assortments and adopt competitive pricing strategies.

Convenience stores are projected to grow at a 7.55% CAGR from 2026 to 2031, driven by urbanization and the increasing demand for on-the-go consumption. These stores prioritize proximity and speed over extensive product assortments. Convenience stores focus on grab-and-go packaging and single-serve formats, aligning with the growing snacking culture and shorter meal occasions. Vietnam's retail landscape highlights the potential of this channel, as supermarkets and convenience stores gain market share while traditional wet markets decline. Urban consumers in Vietnam increasingly prioritize hygiene and convenience. In January 2025, Fuel10K expanded into protein cake mixes, targeting the convenience channel, where functional snacking options command premium pricing and cater to impulse purchasing behavior.

Geography Analysis

In 2025, North America held a 36.18% market share, driven by high per-capita consumption of packaged bakery goods and efficient supply chains enabling broad distribution and strong promotions. The Supplemental Nutrition Assistance Program expanded online acceptance to more retailers, increasing digital access for low-income households and diversifying the e-commerce customer base for bakery and cereal products. U.S. digital grocery sales grew 18.4% year-over-year, with projections exceeding USD 330 billion by 2027, highlighting e-commerce's growing role in distribution and margins. W.K. Kellogg invested USD 500 million in supply chain upgrades across three plants to meet demand in both retail and direct-to-consumer channels. Canada and Mexico added volume, with Mexico benefiting from proximity to U.S. manufacturing hubs, enhancing cross-border supply chain efficiency.

Asia-Pacific is projected to grow at an 8.36% CAGR from 2026 to 2031, driven by rising incomes, urbanization, and the adoption of Western breakfast habits. China and India offer significant opportunities as middle-class consumers seek convenience and branded packaged foods. Japan's mature market supports demand for premium bakery products, while Australia's grocery sector, led by Coles and Woolworths, ensures stable distribution for local and imported brands. In 2024, Nissin Foods acquired ABC Pastry in Australia for AUD 33.7 million (USD 22.5 million) and Gaemi Food in South Korea for USD 35 million, reflecting Japanese manufacturers' focus on regional growth through local acquisitions. Urbanization and modern retail formats in Indonesia, Thailand, and Singapore further drive incremental growth.

Europe sustained its position through premiumization and organic product expansion. The U.K. saw growth in specialty bakery formats, with consumers willing to pay more for quality and craftsmanship. Warburtons launched Belgian Waffles in September 2024 and Protein Flatbreads in August 2024, catering to demand for indulgent and functional products at premium prices. Germany, Italy, France, Spain, and the Netherlands remain key markets, while Poland and Belgium show growth potential as incomes rise. In Brazil, wheat products account for 5% of food processing output, with clean-label and plant-based trends gaining traction among urban consumers. Argentina, Colombia, Chile, and Peru contribute volume but face challenges from economic instability and currency fluctuations. In the Middle East and Africa, Saudi Arabia, the UAE, and Turkey lead demand for packaged bakery goods, supported by expatriates and tourism. Egypt's flour milling capacity and Nigeria's large population offer long-term potential, though infrastructure and import reliance limit short-term growth.

Competitive Landscape

The baked food and cereals market is fragmented, with many local, domestic, and global players competing in the segment. The strong presence of local players intensifies competition among market participants. Major companies in this industry include Grupo Bimbo SAB de CV, Kellanova, General Mills, Mondelez International Inc., and Nestlé S.A.

New entrants are using direct-to-consumer channels and niche strategies to avoid traditional retail barriers. In response, established companies are focusing on innovation and expanding their capacities. For example, W.K. Kellogg's investment of around USD 500 million in supply chain improvements across three plants demonstrates the scale needed to efficiently serve both retail and e-commerce markets while maintaining competitive delivery times and cost efficiency.

Technological advancements in production, such as enzyme formulations for product reformulation, sourdough fermentation to extend shelf life, and automation to reduce labor costs, are becoming critical for success. As labor costs increase and consumers demand consistent quality, these innovations help companies stay competitive. Furthermore, compliance with regulations like the United States Food and Drug Administration's Food Safety Modernization Act and the European Union Regulation 1169/2011 on allergen labeling requires strict operational standards. These regulations benefit larger players with dedicated quality assurance teams while creating challenges for smaller, underfunded competitors[3]European Union. "Regulation (EU) No 1169/2011 on Food Information to Consumers.", eur-lex.europa.eu..

Baked Food And Cereals Industry Leaders

-

Grupo Bimbo SAB de CV

-

General Mills Inc.

-

Mondelez International Inc.

-

Nestlé S.A.

-

Kellanova

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hill Biscuits, a sweet biscuit manufacturer, launched its first savoury cracker to its portfolio, Simply Savoury. According to the brand, it is available in a 300g pack and a snack pack containing two crackers.

- February 2025: Britannia, in partnership with Warner Bros. Discovery, launched a limited-edition Harry Potter biscuit. According to the brand, the new product, Pure Magic Choco Frames, features open choco biscuits. Each pack contains five specially embossed biscuits, representing the four Hogwarts houses—Gryffindor, Slytherin, Ravenclaw, and Hufflepuff.

- February 2025: Bonn has expanded its product line with the launch of TRUE ZERO MAIDA Wholewheat Brown Bread. According to the brand, the product is free from palm oil and preservatives, it is high in fiber, trans-fat free, and cholesterol-free, making it the ideal choice for individuals who are health-focused and looking for nutritious food options.

- February 2025: Nestlé India has launched its latest product in the breakfast cereals category: Munch Choco Fills, now available throughout India. According to the brand, this cereal breakfast features a delightful combination of a crunchy outer shell and a chocolatey filling.

Global Baked Food And Cereals Market Report Scope

Bakery products are commonly classified as bread, cakes, cookies, rolls, and pastries, an everyday staple in various regions that provide nutrients in the human diet. On the other hand, cereals consumed as breakfast are made from processed grains or multiple grains, such as corn, oats, wheat, and others.

The global baked food and cereals market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into bread, breakfast cereals, biscuits and cookies, morning goods, cakes and pastries, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialist stores, convenience stores/grocery stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa.

The report offers the market size in value terms in USD for all the above-mentioned segments.

Product Type

| Bread and Rolls |

| Cakes and Pastries |

| Biscuits and Cookies |

| Breakfast Cereals |

| Crackers and Savory Biscuits |

| Others |

Category

| Conventional |

| Organic |

Distribution Channel

| Supermarket/Hypermarket |

| Specialist Store |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Bread and Rolls | |

| Cakes and Pastries | ||

| Biscuits and Cookies | ||

| Breakfast Cereals | ||

| Crackers and Savory Biscuits | ||

| Others | ||

| Category | Conventional | |

| Organic | ||

| Distribution Channel | Supermarket/Hypermarket | |

| Specialist Store | ||

| Online Retail Store | ||

| Convenience Store | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the baked food and cereals market?

The baked food and cereals market size reached USD 434.19 billion in 2026 and is forecast to climb to USD 580.21 billion by 2031.

Which product segment is growing the fastest within baked goods and cereals?

Crackers and savory biscuits are projected to register the quickest growth, advancing at a 6.98% CAGR through 2031.

How quickly is organic bakery gaining ground?

Organic baked foods are expanding at an 7.79% CAGR as certification processes mature and consumers prioritize clean-label assurances.

Which sales channel offers the highest growth potential?

Convenience stores are set to post a 7.55% CAGR, propelled by urbanization and demand for grab-and-go formats.

Page last updated on: