Corn Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

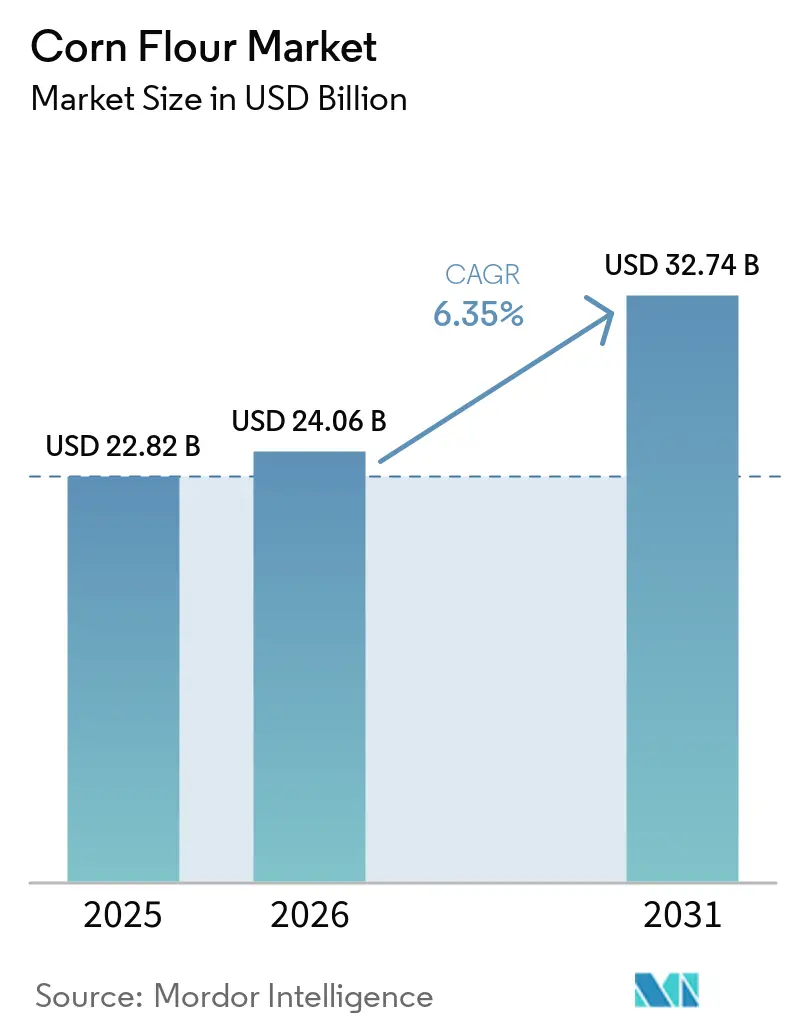

| Market Size (2026) | USD 24.06 Billion |

| Market Size (2031) | USD 32.74 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corn Flour Market Analysis by Mordor Intelligence

The corn flour market size is projected to be USD 22.8 billion in 2025, USD 24.1 billion in 2026, and reach USD 32.7 billion by 2031, growing at a CAGR of 6.4% from 2026 to 2031. The surge in the corn flour market is largely attributed to escalating diagnoses of celiac disease and non-celiac gluten sensitivity, driving a heightened demand for gluten-free staples across both retail and industrial sectors. Additionally, the market is reaping benefits from the burgeoning processed and convenience food manufacturing in the Asia-Pacific and Latin America. Here, the appetite for packaged snacks, bakery items, and ready-to-eat meals is broadening the base of industrial buyers. Demand for corn flour is gaining resilience, bolstered by fortification programs in over 143 countries. These programs, which encompass at least one grain or oil vehicle, maize flour included, are ensuring procurement extends beyond typical consumer spending cycles. The landscape is becoming increasingly competitive, with large ingredient companies reshaping the corn flour market through acquisitions, capacity transfers, and formulation-driven expansions. Concurrently, a tightening global corn supply and recurring mycotoxin concerns are amplifying the importance of traceability, testing, and quality assurance. This emphasis is proving advantageous for millers equipped to navigate these challenges.

Key Report Takeaways

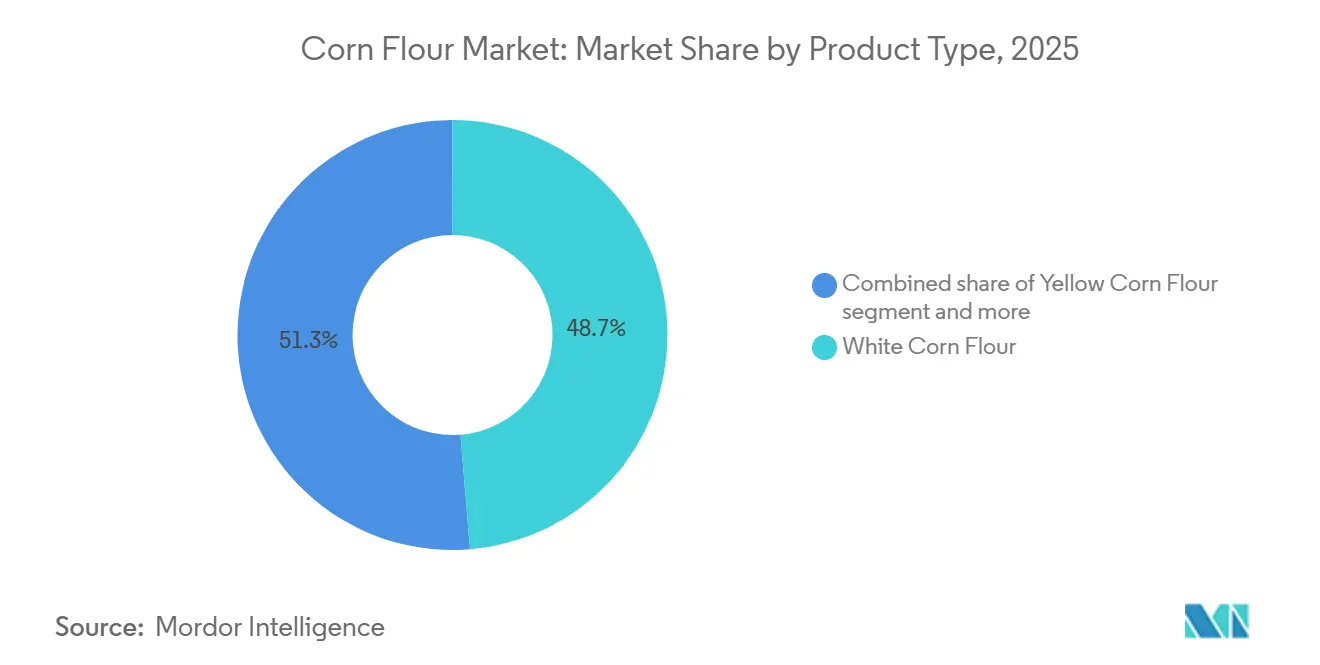

- By product type, white corn flour accounted for the largest share of the corn flour market, at 48.7% in 2025, while yellow corn flour is projected to grow at the fastest CAGR of 7.0% during 2026-2031.

- By nature, conventional corn flour retained 89.6% share of the corn flour market in 2025, whereas organic corn flour is forecast to expand at a 7.6% CAGR through 2031.

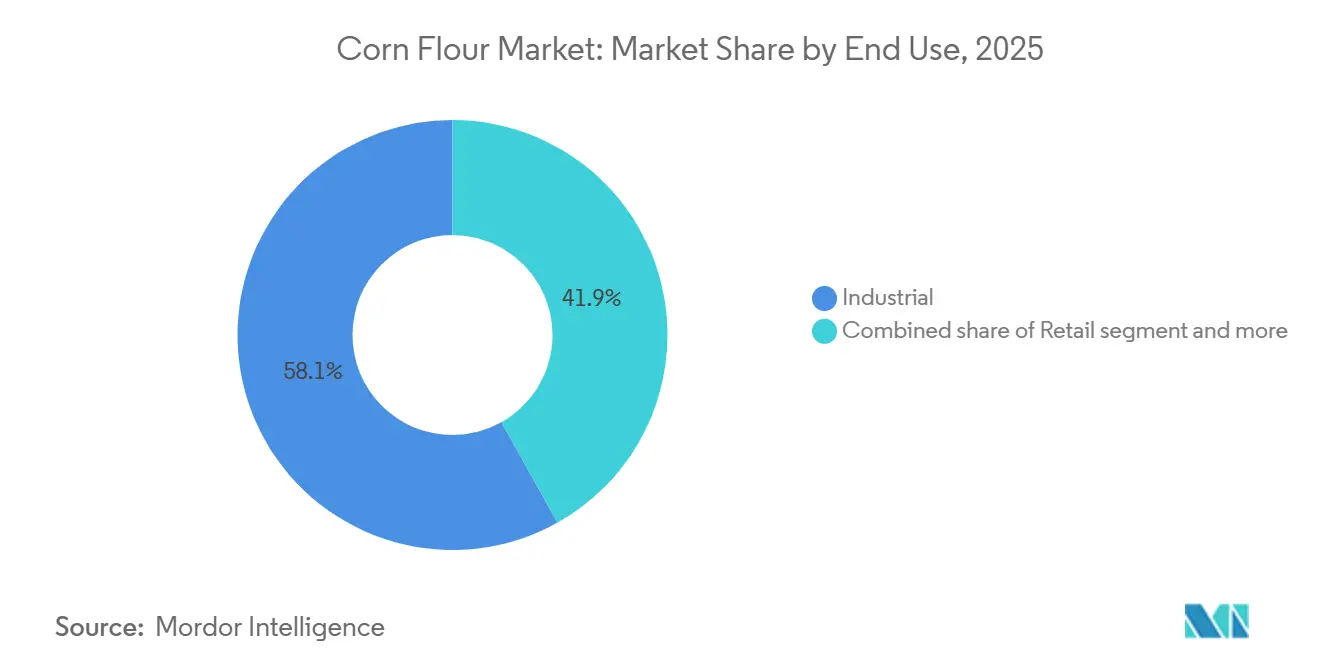

- By end use, industrial applications accounted for the largest share of the corn flour market, at 58.1% in 2025, while retail is projected to grow at the fastest CAGR of 7.5% during 2026-2031.

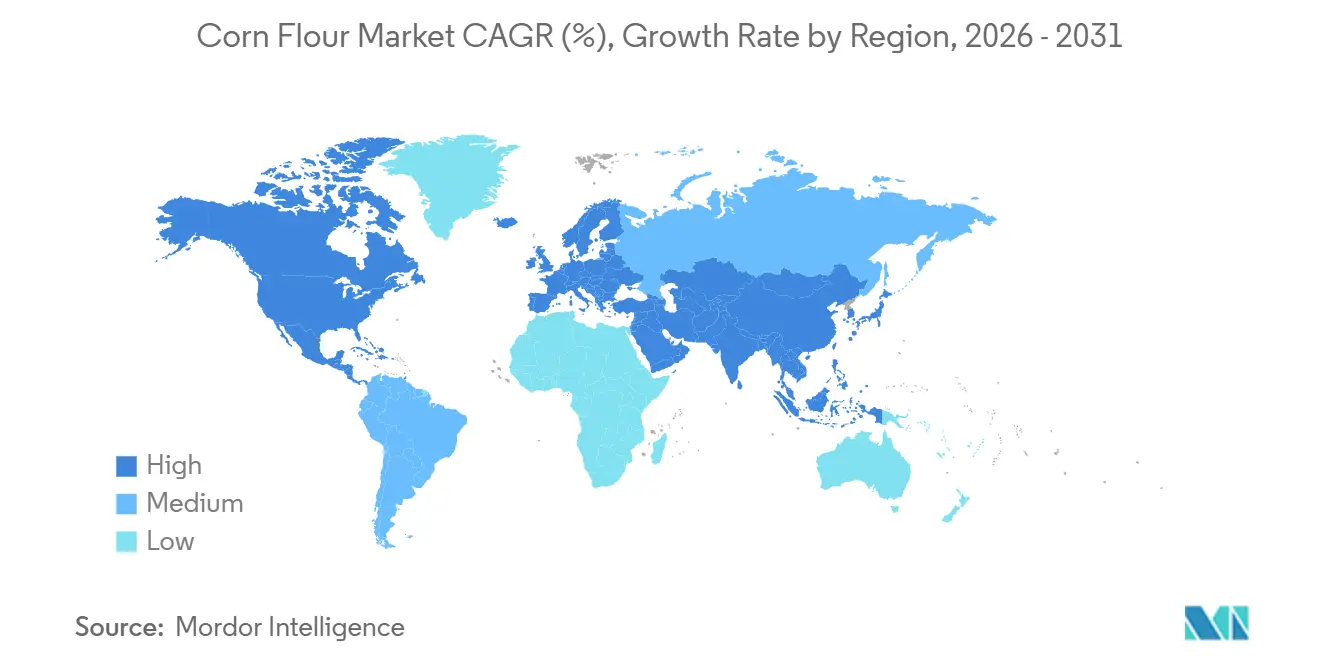

- By geography, North America accounted for the largest share of the corn flour market, at 36.4% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 8.0% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Corn Flour Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Gluten-Free and Allergen-Free Staples | +1.8% | Global; highest impact in North America and Europe | Short term (≤ 2 years) |

| Expansion of Processed and Convenience Food Manufacturing | +1.2% | Asia-Pacific core, spill-over to Latin America and MEA | Medium term (2–4 years) |

| Expansion of Clean-Label and Simple-Ingredient Reformulations | +0.9% | North America and the EU | Short term (≤ 2 years) |

| Menu Diversification in Tortillas, Snacks, and Bakery Formats | +0.8% | Global; concentrated in North America and Latin America | Medium term (2–4 years) |

| Fortification-Ready Corn Flour Blends for Nutrient-Dense Foods | +0.6% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Technological Advancements in Milling and Processing | +0.5% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising demand for gluten-free and allergen-free staples

Corn flour, celebrated for its natural gluten-free attributes, finds itself at the forefront of a rapidly evolving trend in the food industry. The US FDA, under the Food Allergen Labeling and Consumer Protection Act, has set a benchmark: defining "gluten-free" as containing less than 20 ppm of gluten. This ruling, while voluntary, wields significant commercial influence, establishing a certification standard that aligns with consumer expectations. This raises the stakes for corn flour suppliers vying for prominence in health-focused retail spaces. Celiac disease, as highlighted by Beyond Celiac, affects around 3 million Americans. However, this figure only scratches the surface. A much larger demographic, including those with non-celiac gluten sensitivity and individuals opting for wheat-free diets, fuels a market growth that extends beyond mere medical needs. Furthermore, it's noteworthy that about 83% of celiac cases in the U.S. are believed to be undiagnosed. This suggests that improvements in diagnosis rates, thanks to enhanced gastroenterological screenings, could act as a latent demand booster for gluten-free corn flour, rather than signaling a market that's already saturated [Future Market Insights]. Compliance measures, like the FDA's gluten-free labeling and similar EU directives (Regulation EC No. 41/2009), are reshaping the landscape[1]Source: U.S. Food and Drug Administration, “Gluten-Free Labeling of Foods,” U.S. Food and Drug Administration, fda.gov . They compel corn flour suppliers to invest in specialized, allergen-free milling infrastructures, consequently elevating the capital costs for legitimate market entry.

Expansion of processed and convenience food manufacturing

Urbanization in Asia-Pacific and Latin America is transforming corn flour from a mere commodity into a vital formulation ingredient. In India, China, and Indonesia, food manufacturers are ramping up the production of packaged snacks, bakery goods, and ready-to-eat items. They increasingly favor corn flour, thanks to its neutral flavor, binding properties, and cost-effectiveness compared to wheat flour. According to World Grain, the global market for pre-cooked maize flours, mainly used for instant dough and arepas, is on the rise. This category is projected to grow at over 10% annually, largely fueled by swift urbanization in regions where maize is a staple[2]Source: World Grain, “World Grain,” World Grain, world-grain.com . A significant outcome of this growth is the heightened influence of foodservice manufacturers in determining specification standards. As major QSR and institutional food chains globalize their operations, they are insisting on uniform particle size, moisture content, and microbiological profiles from corn flour suppliers. This demand is steering them towards millers who can showcase consistent process control on a large scale.

Expansion of clean-label and simple-ingredient reformulations

Processed food brands are increasingly prioritizing clean-label ingredients, with corn flour emerging as a key beneficiary. Across the industry, functional native corn starches, marketed as "corn flour" or “corn starch,” are being embraced. These non-GMO, naturally gluten-free alternatives are now supplanting synthetic thickeners and modified starches in dairy, confectionery, and ready-meal applications. This shift is driven by buyers' preference for shorter, more recognizable ingredient lists. In February 2024, Ingredion launched NOVATION Indulge 2940, a non-GMO functional native corn starch aimed at dairy and dessert gelling. This move underscores how clean-label positioning is not just a trend but a catalyst for premium product development, elevating corn flour derivatives in the market. Geographically, the clean-label movement's concentration is pivotal for forecasting. North American natural food channels and European premium retailers show the highest willingness to pay for certified non-GMO and organic corn flour. Meanwhile, in the Asia-Pacific, there's a notable acceleration of this trend, driven by middle-income consumers becoming more discerning about ingredient lists in packaged foods.

Fortification-ready corn flour blends for nutrient-dense foods

The WHO's endorsement of iron and folic acid fortification in maize flour and corn meal, now a staple in national nutrition programs across Sub-Saharan Africa and South Asia, has birthed a robust industrial procurement channel. This channel operates largely independent of the typical consumer spending cycles. In practice, several nations in the Americas and Africa have adopted the industrial fortification of maize flour with these essential nutrients. The Food and Agriculture Organization has lauded this approach, deeming it an efficient, straightforward, and cost-effective solution to tackle widespread micronutrient deficiencies. A crucial yet often overlooked aspect of this initiative lies in its supply chain implications. Fortification mandates compel millers to invest in certified blending and quality assurance infrastructures. This not only elevates entry barriers but also skews advantages towards large-scale industrial processors, sidelining smaller regional mills. As a result, millers who have committed to fortification-compatible facilities enjoy a consistent volume premium, insulated from the fluctuations of commodity price cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Competition from Alternative Flours | -1.2% | Global | Short term (≤ 2 years) |

| Volatility in Corn Raw Material Quality and Supply | -0.9% | North America, Latin America | Short term (≤ 2 years) |

| Limited Functional Performance Compared to Wheat Flour | -0.8% | Europe, North America | Medium term (2–4 years) |

| Susceptibility to Mycotoxin Contamination | -0.7% | Asia-Pacific, Sub-Saharan Africa, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in corn raw material quality and supply

In 2026, millers grapple with corn price fluctuations and availability challenges, especially those lacking long-term hedging or direct agreements with farmers. The USDA's May 2026 Feed Outlook anticipates the US corn season-average farm price for 2026/27 to rise to USD 4.40 per bushel, up from the USD 4.15 forecasted for 2025/26. This uptick is attributed to an expected 4% dip in harvested acreage and dwindling stocks-to-use ratios[3]Source: U.S. Department of Agriculture Economic Research Service, “Feed Outlook,” USDA ERS, ers.usda.gov . While global coarse grain supplies for 2026/27 are set at 2,156 million metric tonnes, 15 million metric tonnes shy of the 2025/26 figures, declines are primarily seen in the U.S., EU, and Argentina. These drops, however, are somewhat balanced by production surges in China and Brazil. In Mexico, the corn flour industry, with a white corn demand exceeding 20 million tonnes annually, witnessed a staggering 120% year-on-year surge in white corn purchases during the first two months of 2026. This spike underscores tight domestic production and a growing reliance on imports. Millers without contracted sourcing not only face price volatility but also grapple with quality inconsistencies. Weather events and fragmented supply chains lead to variations in moisture, protein, and starch profiles.

Susceptibility to mycotoxin contamination

Mycotoxin contamination has evolved from a sporadic seasonal concern to a persistent threat, necessitating continuous monitoring and investment in mitigation. A global survey, conducted between September 2025 and February 2026, examined corn harvested in 2025 across 18 countries. The findings revealed widespread co-contamination in nearly every market, with aflatoxins often surpassing regulatory thresholds in the Philippines and Serbia. Meanwhile, Algeria, Brazil, China, Colombia, Mexico, and Thailand saw a predominance of fumonisins. Data from Q1 2026 confirmed the trend: analyses of global corn samples detected DON in 40%, fumonisins in 32%, and ZEN in 35%. Notably, corn gluten meal showed 100% presence of fumonisins in analyzed samples, highlighting the heightened contamination risk in milling co-products throughout the value chain. DSM-Firmenich's PROcheck survey on the 2025 US corn crop noted a 10 percentage point rise in fumonisin occurrence compared to the 2024 crop, emphasizing a multi-year upward trajectory influenced by climate variability in key corn-growing regions. For corn flour producers, this means that practices like frequent grain testing, near-infrared mycotoxin screening, and segregated storage are transitioning from mere best practices to essential competitive advantages. This shift is largely driven by major food brands incorporating supplier-level contamination monitoring into their procurement contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milling Innovation Reshapes Yellow Flour's Value Case

Yellow corn flour is rapidly becoming the preferred choice for innovation-driven demand, with a projected CAGR of 6.96% through 2031, the fastest among product types. Specialty snack makers, breakfast cereal brands, and functional food developers are increasingly adopting yellow corn flour for its unique flavor and carotenoid benefits. Bühler's online NIR measurement technology, used at LifeLine Foods LLC, is transforming corn grit processing by enabling real-time fat and moisture monitoring. This helps millers meet the stringent standards of specialty yellow corn flour buyers, while reducing quality control costs and increasing yields by an estimated 0.3%. In 2025, white corn flour led the market with a 48.71% share, driven by strong demand from nixtamalized tortilla producers in Mexico and the U.S., where corn-flour-based masa is integral to industrial food processing and foodservice supply chains. Other corn flour variants, such as blue corn, high-fiber types, and stone-ground specialties, though smaller in scale, are gaining traction in North America's natural food retail as artisanal baking expands beyond traditional wheat and white corn.

The corn flour market also reflects distinct supply-chain investment trends. Gruma, the global leader in nixtamalized corn flour, operates 18 milling plants in Mexico, a footprint that secured its market dominance but drew scrutiny from COFECE's antitrust authority in 2024. Gruma is addressing these concerns through supply chain transparency commitments rather than asset divestitures. Meanwhile, smaller producers are leveraging non-GMO and organic certifications to command premium prices in export markets. For example, Bob's Red Mill offers Organic Whole Grain Corn Flour, Gluten Free Corn Flour, and Organic Masa Harina as distinct SKUs, catering to consumers' preference for certified products. As trace-and-test technologies become more accessible, the gap between high-volume commodity nixtamalized corn flour and premium-certified specialty grades is expected to grow.

By Nature: Organic Segment Accelerates on Retailer-Led Reformulation

Forecasts indicate that the organic corn flour segment will experience a CAGR of 7.61% through 2031, making it the fastest-growing segment in the nature category. This momentum is more significantly driven by pressures from retailers to reformulate than by direct consumer demand. Major grocery chains across North America are increasingly mandating non-GMO and organic standards for their private-label baking and snack ingredients. This shift has transformed what was once considered a premium niche into a standard requirement for volume relevance. While conventional corn flour dominated the nature segment with an 89.62% share in 2025 and is poised to maintain its lead due to cost advantages and the economies of scale in industrial milling, it will nonetheless see a gradual decline in its market share. This erosion is attributed to the rising organic category, bolstered by significant investments from large processors in certified supply chains. Notably, organic corn flour, despite commanding a premium price over its conventional counterparts, is witnessing a growth in its volume share. This trend is particularly advantageous for millers who can ensure and trace their organic supply from farm to mill.

In July 2025, Ardent Mills inked a deal to acquire Stone Mill, a specialty grain cleaning facility located in Richardton, North Dakota. This move underscores how top millers are establishing dedicated infrastructures for certified specialty ingredients. Such investments align with their broader strategy to diversify from traditional commodity wheat flour into burgeoning nutrition categories. Concurrently, General Mills has broadened its Cascadian Farm organic cereal lineup to include Kernza grain. This move highlights the food industry's commitment to sourcing differentiation, which has implications for expectations within the corn flour supply chain. In Europe, there's a growing trend where sustainable and regenerative sourcing certifications are gaining traction. Retailers are increasingly valuing these certifications, driven by a heightened preference for traceable ingredient origins that align with commitments to carbon and land-use considerations.

By End Use: Retail's Digital Channels Outpace Traditional Industrial Growth

In 2025, the industrial segment commanded 58.13% of the market, with food & beverage manufacturing leading the charge. This dominance was particularly evident in bakery products, snacks, and beverages, as well as in animal feed applications, where corn flour is prized for its cost-effectiveness as an energy and starch source. Retail, however, is on a rapid ascent, projected to grow at a 7.51% CAGR through 2031. This surge is largely fueled by the rise of e-commerce platforms and the expanding reach of health-food retailers. These platforms are making premium and specialty corn flour easily accessible to home bakers and health-conscious consumers. Foodservice occupies a pivotal middle ground: major QSR chains and institutional kitchens are turning to corn flour for tortilla chips, coatings, and batters. Their substantial volumes strike a balance between the scale needs of industrial suppliers and the quality demands of branded retail. Ingredion's March 2026 collaboration with Shiru, an AI-driven ingredient discovery firm, underscores a significant trend. Their focus on pioneering functional proteins for food and beverage uses hints at a future where specialty ingredients, like corn-flour-based blends, are crafted through data analytics rather than traditional trial-and-error methods.

Within the industrial realm, the food & beverage sector is reaping rewards from diversifying menus in both Western and emerging markets. General Mills' 2026 product lineup, featuring Old El Paso Birria Taco Kits and Tabasco co-branded taco shells, underscores the direct link between global QSR menu innovations and corn flour's pivotal role in tortillas and snacks. While animal feed applications, a major player in industrial demand, are sensitive to fluctuations in corn prices, they also face heightened risks from mycotoxin contamination. The online retail segment is revolutionizing the corn flour landscape. By facilitating direct-to-consumer sales of specialty, certified, and single-origin products, it's achieving margins that traditional grocery shelves have long struggled to maintain.

Geography Analysis

In 2025, North America commanded a dominant 36.4% share of the corn flour market. Meanwhile, the Asia-Pacific region is poised to experience the swiftest growth, projected at an 8% CAGR through 2031. Bolstering North America's position, the U.S. achieved a record corn harvest of 16.7 billion bushels for the 2025/26 season, ensuring ample raw materials for extensive milling. Conversely, Mexico grappled with a constrained supply of white corn in 2025 and early 2026, intensifying sourcing pressures for millers and underscoring the need for reliable sourcing. While Canada played a minor role, urban retail channels witnessed a surge in demand for premium clean-label and organic products, driven by a growing health-conscious consumer base.

Urbanization across major economies in the Asia-Pacific is fueling a surge in demand for packaged foods, positioning the region as the primary growth driver in the corn flour market. In a testament to this bullish sentiment, General Mills inaugurated its second manufacturing unit in Nashik, Maharashtra, with a substantial investment of INR 100 crore (approximately USD 11 million). China's industrial appetite is also on the rise, spurred by the proliferation of Western-style food outlets and quick-service restaurants in its cities. However, a 2025 peer-reviewed study spotlighted quality control hurdles, identifying DON, ZEN, and fumonisins as predominant contaminants in maize across three of China's growing regions. Meanwhile, Thailand, Indonesia, and Vietnam are emerging as secondary growth hubs. Notably, Riddhi Siddhi Gluco Biols' acquisition of Cargill's wet milling facility in Karnataka in May 2026 underscores the increasing local processing ambitions of South Asian buyers.

Demand dynamics for corn flour vary across Europe, South America, the Middle East, and Africa. In 2025, France's flour milling sector imported 420,000 tonnes of corn flour, predominantly sourced from Germany and Belgium, which supplied over 80% of the imports. This trend underscores heightened regional trade pressures on specialty flour pricing. Concurrently, a dip in EU corn production from 59.6 million tonnes in 2024 to 56.8 million tonnes in 2025 exerted upward pressure on raw material costs. South America, spearheaded by Brazil, Argentina, and Colombia, continues to be a pivotal supply hub. At the same time, nations like Egypt, Morocco, and Nigeria in the Middle East and Africa are unveiling fresh opportunities, buoyed by their expanding food manufacturing sectors.

Competitive Landscape

Globally, the corn flour market exhibits moderate consolidation, but national sub-segments, particularly nixtamalized ones, see a pronounced concentration. Major players like Gruma, Ardent Mills, ADM, Cargill, and Ingredion leverage their scale, integrated supply chains, and established customer relationships for structural advantages. A pivotal shift occurred in July 2025 when Grain Craft acquired Bunge’s North American corn milling facilities, bolstering its position as a mid-tier rival in dry corn milling and dry masa. Yet, opportunities abound in the corn flour market, especially in organic, non-GMO, fortification-ready, and certified gluten-free blends, where margins are fatter and differentiation is paramount.

Companies in the corn flour market are split in their strategies: some focus on expanding processing throughput, while others prioritize traceability, certification, and application-specific performance. For instance, ADM enhanced its Clinton, Iowa facility with two high-speed receiving pits, each capable of handling 25,000 bushels per hour, to boost grain handling and origination efficiency. Bühler’s digital measurement system at LifeLine Foods slashed response time from two hours to mere minutes and upped yield by 0.3%, underscoring the edge process analytics can provide. Ardent Mills deepened its specialty focus with the July 2025 Stone Mill acquisition, pushing beyond conventional flour lines. Meanwhile, Ingredion's June 2026 bid for Tate & Lyle, if finalized, promises to amplify its scale in specialty ingredients, setting a higher competitive benchmark for standalone millers.

The corn flour market presents a dichotomy: global moderation contrasts with local concentration. In 2024, COFECE determined that Gruma commanded a dominant share, between 50% and 90%, of Mexico’s nixtamalized corn flour segment. While the authority mandated remedies, it refrained from imposing obligatory plant divestitures. This underscores a growing emphasis on compliance, supply transparency, and buyer trust, rivaling the significance of installed capacity in staple food markets. Expect fierce competition in functional, certified, and premium blends, with volume leadership hinging on procurement prowess, scale, and consistent quality.

Corn Flour Industry Leaders

Archer Daniels Midland Company

Cargill, Incorporated

General Mills, Inc.

Ardent Mills LLC

Gruma, S.A.B. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ADM announced a multimillion-dollar investment in its Clinton, Iowa, corn processing facility, adding two new high-speed receiving pits, each capable of processing 25,000 bushels per hour, along with expanded grain storage and infrastructure. The project is designed to reduce farmer wait times during peak harvest periods, with receiving pit completion expected by end-2026 and storage enhancements by summer 2027.

- May 2026: Ingredion announced a strategic joint venture with Sanstar Limited and a 9% equity investment in the company, India's leading manufacturer of corn-based specialty products. The partnership will commission a greenfield facility to manufacture diversified specialty pharmaceutical and food ingredient products, combining Sanstar's local manufacturing expertise with Ingredion's global formulation and go-to-market capabilities in a high-growth APAC market.

- May 2026: Riddhi Siddhi Gluco Biols Ltd. completed the acquisition of Cargill's corn wet milling facility in Davangere, Karnataka, India. The integrated plant, with 300,000 metric tonnes of annual processing capacity, strengthens RSGBL's production footprint and capacity to serve food, pharmaceutical, and industrial customers in South India.

Global Corn Flour Market Report Scope

Corn flour is a fine powder made from grinding dried whole corn kernels. The corn flour market is segmented by product type, nature, end use, and geography. By product type, the market is segmented into white corn flour, yellow corn flour, and other corn flour types. By nature, the market is segmented into conventional and organic. By end use, the market is segmented into industrial, foodservice, and retail. The industrial segment is further sub-segmented into food and beverages, animal feed, and other industrial applications. The food and beverages include segments like bakery products, snacks, beverages, and other food and beverage applications. Similarly, the retail segment is further sub-segmented into supermarkets/hypermarkets, convenience stores, online retail, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| White Corn Flour |

| Yellow Corn Flour |

| Other Corn Flour Types |

| Conventional |

| Organic |

| Industrial | Food and Beverages | Bakery Products |

| Snacks | ||

| Beverages | ||

| Other Food and Beverage Applications | ||

| Animal Feed | ||

| Other Industrial Applications | ||

| Foodservice | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | White Corn Flour | ||

| Yellow Corn Flour | |||

| Other Corn Flour Types | |||

| Nature | Conventional | ||

| Organic | |||

| End Use | Industrial | Food and Beverages | Bakery Products |

| Snacks | |||

| Beverages | |||

| Other Food and Beverage Applications | |||

| Animal Feed | |||

| Other Industrial Applications | |||

| Foodservice | |||

| Retail | Supermarkets/Hypermarkets | ||

| Convenience Stores | |||

| Online Retail | |||

| Other Distribution Channels | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Sweden | |||

| Belgium | |||

| Poland | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Thailand | |||

| Singapore | |||

| Indonesia | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Peru | |||

| Chile | |||

| Rest of South America | |||

| Middle East and Africa | United Arab Emirates | ||

| South Africa | |||

| Saudi Arabia | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current outlook for the corn flour market through 2031?

The corn flour market is projected to move from USD 24.1 billion in 2026 to USD 32.7 billion by 2031 at a 6.4% CAGR, supported by gluten-free demand, processed food expansion, and fortified staple programs.

Which product segment is leading demand in corn flour?

White corn flour led with 48.7% share in 2025 because tortilla and masa applications remain deeply embedded in North American food demand.

Which segment is growing the fastest in corn flour byproduct and nature?

Yellow corn flour is the fastest-growing product type at 7% CAGR, while organic corn flour is the fastest-growing nature segment at 7.6% CAGR through 2031.

Why is the Asia-Pacific important for future corn flour growth?

Asia-Pacific is expected to post the fastest regional growth at 8% CAGR through 2031 as urbanization, packaged food demand, and local processing investments continue to expand.

Page last updated on: