United States Rice Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

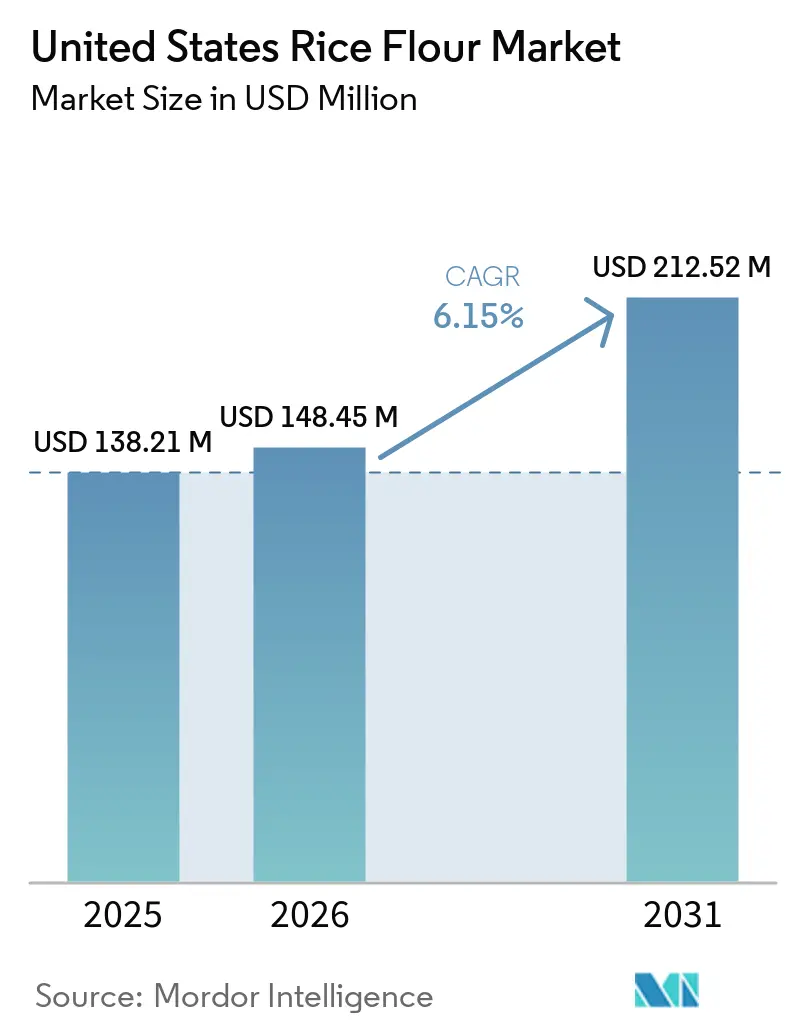

| Base Year Market Size (2025) | USD 138.21 Million |

| Market Size (2026) | USD 148.45 Million |

| Market Size (2031) | USD 212.52 Million |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

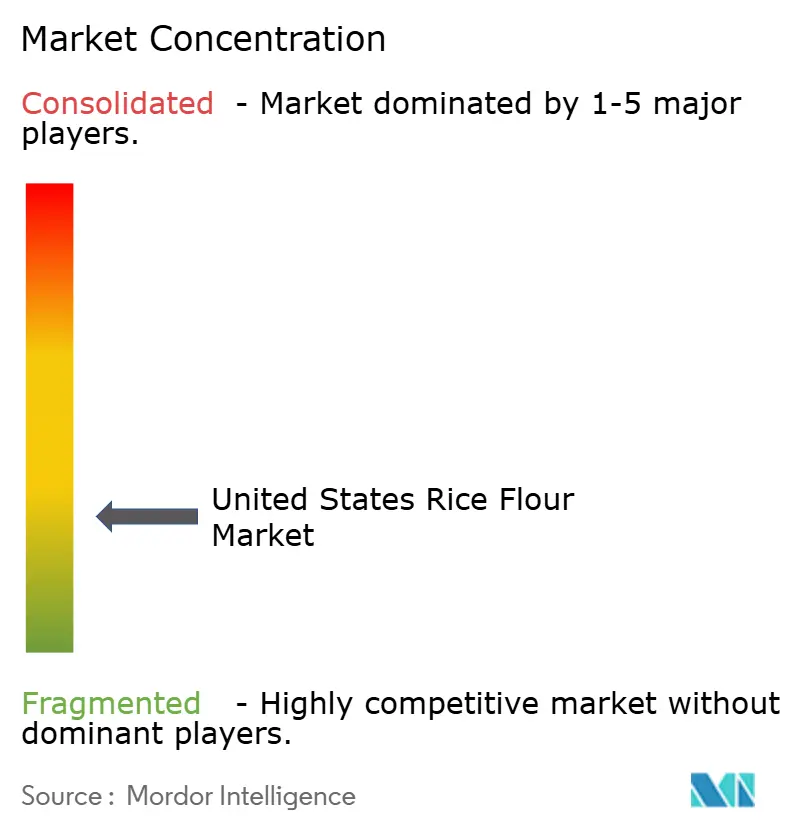

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Rice Flour Market Analysis by Mordor Intelligence

The United States rice flour market size was valued at USD 138.2 million in 2025 and is estimated to grow from USD 148.5 million in 2026 to reach USD 212.5 million by 2031, at a CAGR of 6.2% during the forecast period 2026 to 2031. The United States rice flour market is moving beyond a narrow health-food niche because large food manufacturers now use rice flour in mainstream bakery, snack, sauce, and infant nutrition products, which gives demand a broader and more stable base. The United States rice flour market is also benefiting from stronger gluten-free demand, as a large pool of consumers either manage diagnosed celiac disease or avoid gluten for other dietary reasons, which is pushing rice flour into regular procurement cycles rather than occasional specialty buying. Supply conditions remain shaped by domestic production geography, with Southern long-grain milling clusters supporting large industrial volumes and California supporting specialty and organic grades, which gives some suppliers a clear advantage in freight, traceability, and contract responsiveness. The United States rice flour market remains moderately concentrated because a small group of large ingredient companies controls a large share of industrial relationships, yet smaller specialty millers still hold room to grow in ultra-fine, pre-gelatinized, and certified low-arsenic grades that larger incumbents do not fully cover. Near-term growth still faces pressure from tighter Arkansas acreage and stricter buyer attention to inorganic arsenic in rice-based foods, especially in infant nutrition, where testing, sourcing, and documentation increasingly influence supplier selection

Key Report Takeaways

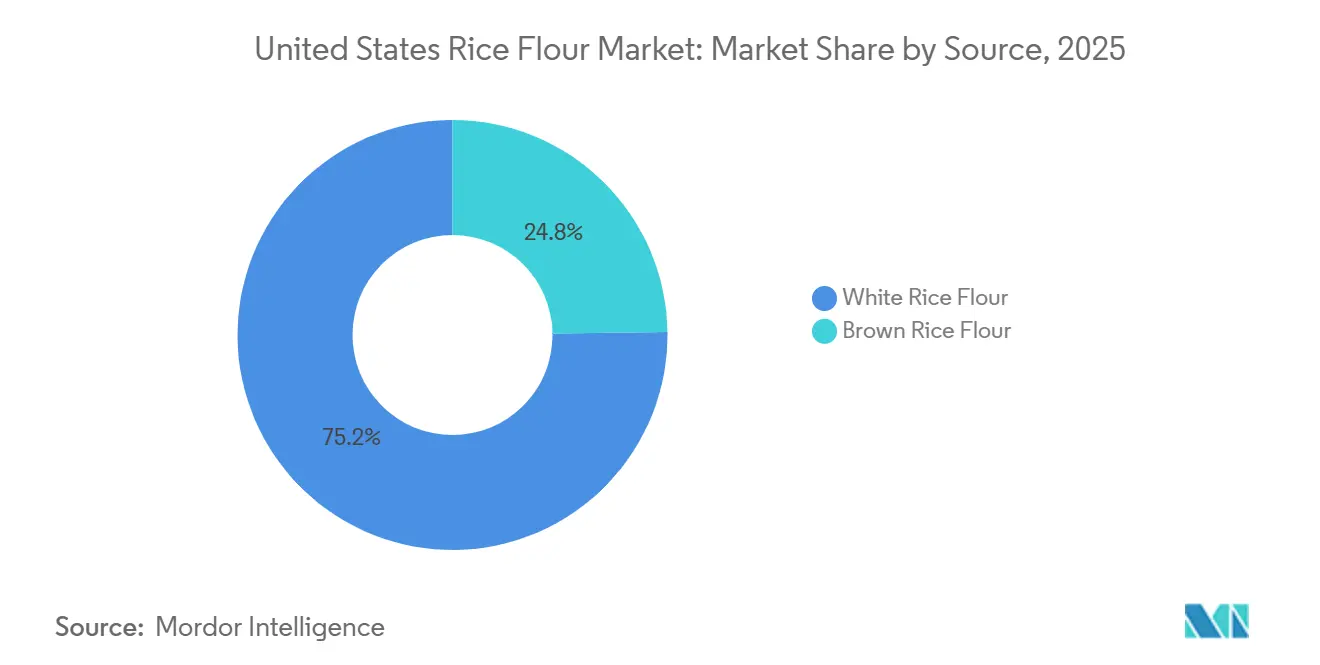

By source, white rice flour held 75.2% of the United States rice flour market size in 2025, while brown rice flour is projected to expand at a 7.2% CAGR through 2031.

By nature, conventional rice flour accounted for 68.3% of the United States rice flour market size in 2025, while organic rice flour is forecast to grow at an 8.2% CAGR through 2031.

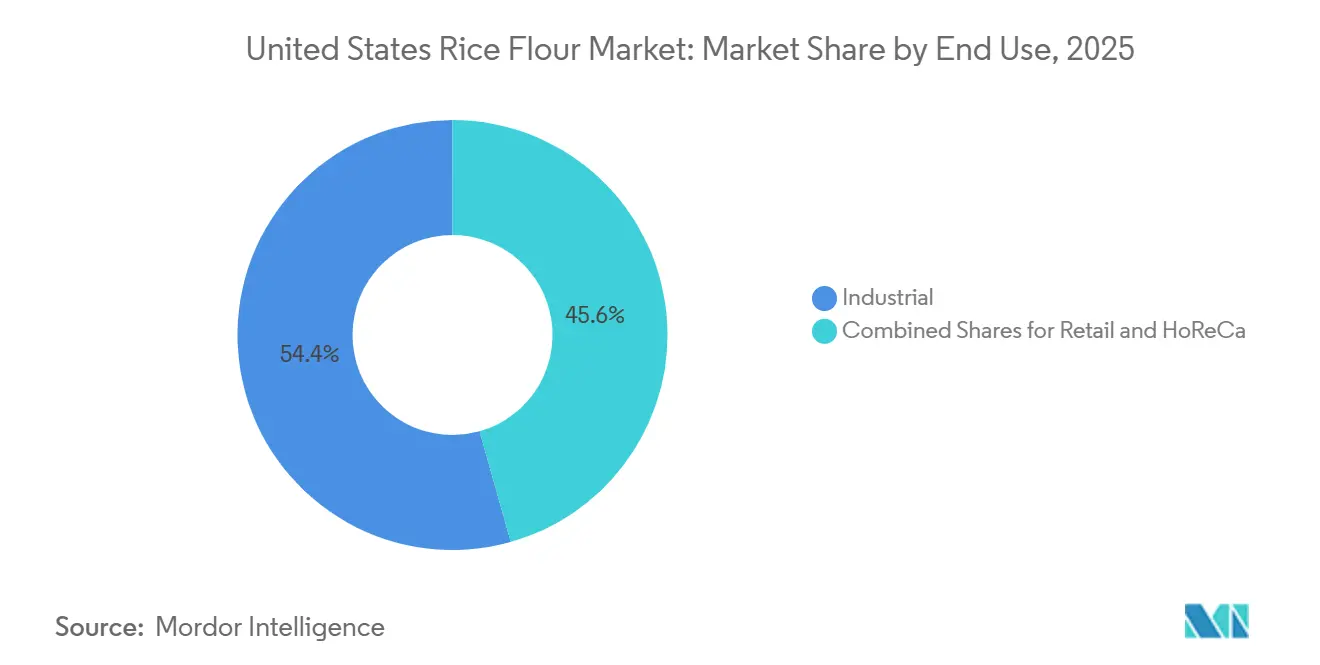

By end use, industrial applications captured 54.4% of the United States rice flour market share in 2025, while the retail channel recorded the highest projected CAGR at 8.2% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Rice Flour Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Gluten-Free Products | +2.2% | National, with concentrated retail gains in California, New York, and Pacific Northwest | Short term (≤ 2 years) |

| Increasing Consumer Inclination Towards Clean-Label Formulations | +1.3% | National, strongest pull from Midwest and Northeast food manufacturers | Medium term (2-4 years) |

| Growth of Rice Flour in Infant and Specialty Diet Products | +0.8% | National, with early procurement gains in Southeast milling clusters | Short term (≤ 2 years) |

| Expansion of Rice Flour in Snack and Convenience Foods | +0.6% | National, led by California, Texas, and Illinois processing hubs | Medium term (2-4 years) |

| Premiumization of Organic and Non-GMO Pantry Staples | +0.5% | Pacific Coast and Northeast premium retail corridors | Medium term (2-4 years) |

| Functional Milling Advances for Finer Texture and Better Binding | +0.4% | National, with spillover into foodservice and industrial baking | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Gluten-Free Products

The single most powerful tailwind behind the United States rice flour market is the structural growth of medically motivated and lifestyle-driven gluten-free consumption. Approximately 1% of the United States population carries a celiac diagnosis, but the functionally relevant consumer cohort, those who actively avoid gluten regardless of formal diagnosis, is estimated at up to 6% of Americans, according to research published in Seed World in January 2026. A critical second-order dynamic is that this driver is increasingly originating not from specialty retailers but from mainstream mass-market brands, as large CPG companies like General Mills reformulate core SKUs such as Cheerios and Betty Crocker baking mixes to include or qualify as rice-flour-based gluten-free alternatives. General Mills. This mainstreaming effect shifts rice flour from a specialty ingredient into a commodity procurement category, which fundamentally changes volume expectations and contract structures for millers. The FDA's allergen-labeling guidance (2025 revised edition) reinforces manufacturer incentives to verify and label gluten-free status, accelerating reformulation timelines and locking in rice flour as a preferred base[1]Source: U.S. Food and Drug Administration, “Arsenic in Food,” U.S. Food and Drug Administration, fda.gov.

Increasing Consumer Inclination towards Clean-Label Formulations

Clean-label demand is reshaping ingredient procurement in a way that disproportionately benefits rice flour over synthetic thickeners and modified starches. The non-obvious dimension of this driver is an industrial shift: Ingredion's R&D expenditure reached USD 71 million in FY2025, with clean-label starches and functional ingredient systems as a primary investment pillar, while the company's Indianapolis-based texture and healthful solutions facility is receiving a USD 100 million capital infusion, a signal that large ingredient companies see clean-label reformulation as a multi-year volume shift, not a trend. When food manufacturers swap out synthetic binders for rice flour in commercial baking and snack production, the resulting demand is sticky because re-reformulating back carries labeling and consumer-perception costs. The USDA NOP's compliance requirements for organic claims create an additional layer of traceability that positions certified domestic rice flour suppliers advantageously against imported alternatives.

Growth of Rice Flour in Infant and Specialty Diet Products

Infant nutrition remains one of the more defensible pockets of demand in the United States rice flour market because buyers in this area value digestibility, consistency, and strict sourcing controls. According to the UNICEF data from 2025, 3.66 million babies were born in the United States[2]UNICEF, "How many babies are born each year in the US?" data.unicef.org. Rice flour fits well in specialty diet products because it is widely used in formulations that aim to reduce allergen complexity and maintain gentle texture in finished foods. FDA activity under the Closer to Zero program has increased attention on contaminants in foods for babies and young children, which pushes suppliers to invest in testing and verified low-arsenic sourcing rather than compete on price alone. That same pressure creates an advantage for suppliers that can prove compliance, because infant food brands are more likely to reward documented quality with longer contracts and tighter supplier lists. California’s 2025 baby food disclosure rules further raised the reporting burden for heavy metals, which increased the value of suppliers that already had strong analytical systems in place. This means the United States rice flour market can still grow in infant and specialty diet products even while safety scrutiny becomes stricter, because compliance itself is turning into a barrier that favors prepared suppliers

Expansion of Rice Flour in Snack and Convenience Foods

Snack and convenience food manufacturing is becoming a more important outlet for the US rice flour market because product developers need base ingredients that support binding, coating, crispness, and texture control across multiple formats. Rice flour works well in this setting because fine particle size, neutral taste, and predictable gelatinization help manufacturers manage sensory consistency without adding strong off-notes. The demand is especially attractive for suppliers because snack applications often require tighter mesh size, viscosity control, and formulation precision than standard household cooking uses. Those tighter specifications reduce direct commoditization and let capable millers compete on performance rather than only on price. Product launches elsewhere in the rice ingredient chain also point to broader innovation momentum, including Riviana Foods’ April 2026 launch of Success Boil-in-Bag Sticky Rice for Eastern United States retailers. As convenience formats expand, the United States rice flour market stands to benefit most, where suppliers can deliver repeatable functional performance at commercial production scale

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from other gluten-free flours | -1.2% | National; most intense in premium retail and specialty food channels | Short term (≤ 2 years) |

| Price volatility in US rice inputs and contract sourcing pressure | -0.8% | Concentrated in Arkansas, Louisiana, and California producing regions | Medium term (2–4 years) |

| Low consumer awareness beyond niche gluten-free buyers | -0.5% | Midwest and South, where wheat-flour culture remains dominant | Long term (≥ 4 years) |

| Labeling, certification, and traceability burden for organic and non-GMO claims | -0.4% | Pacific Coast and Northeast; high compliance cost at smaller mills | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Competition from Other Gluten-Free Flours

The United States rice flour market faces stronger competition from almond, oat, cassava, coconut, and chickpea flours, especially in premium retail channels where brand stories and nutrition positioning strongly shape shelf appeal. Chickpea and almond flour have built added traction among buyers who prioritize protein or keto positioning, which makes them a visible alternative for consumers who do not select products mainly for texture or neutral taste. This weakens rice flour’s exclusivity in clean-label and gluten-free positioning because several substitutes can now make similar front-of-pack claims. Even so, rice flour still holds a technical edge in coatings, sauces, and extruded snacks where neutral flavor and predictable behavior matter more than high-protein branding. Rice also benefits from a food safety and formulation advantage because it is not among the FDA’s major allergens, unlike tree nuts and some legume-based alternatives that can complicate labeling and plant handling. The restraint is real, but it is stronger in consumer-facing premium formats than in industrial uses, where performance still carries more weight than diet fashion

Price Volatility in United States Rice Inputs and Contract Sourcing Pressure

Input volatility remains a structural risk for the United States rice flour market because domestic milling economics are closely tied to rice acreage, harvest conditions, and farm-level pricing in a few key states. Arkansas harvested 1.3 million acres in 2025, down from 1.4 million acres in 2024, after severe Delta flooding and stronger competition from soybeans pressured planted area and grower returns. USDA’s April 2026 Rice Outlook projects Arkansas long-grain acreage falling further to 900,000 acres in 2026, which would mark the lowest level since 1987 and tighten the raw material base for millers that depend on Southern supply. USDA ERS also reported a 2025 to 2026 season-average farm price of USD 12.1 per hundredweight for all rice, which keeps cost pressure elevated across sourcing contracts[3]Source: U.S. Department of Agriculture Economic Research Service, “Rice, Market Outlook,” U.S. Department of Agriculture, ers.usda.gov. As domestic availability tightens, buyers may need more import blending and more complex origin management, which creates landed-cost volatility and makes domestic source verification harder for brands that market strict provenance claims. This restraint matters because the United States rice flour market depends on steady throughput, yet milling margins can narrow quickly when raw material certainty falls, and contract terms reset more often.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: White Rice Dominates; Brown Rice Closes the Gap

White rice flour held 75.23% of the United States rice flour market in 2025, a position rooted in decades of established use across commercial baking, industrial coatings, and foodservice thickening applications. Its fine, neutral-flavored profile integrates seamlessly into a wide range of processed food formulations without altering the sensory characteristics of the host product, a property that makes it the default specification for contract manufacturers supplying major CPG brands. Pillsbury's Gluten Free All-Purpose Flour Blend, which uses rice flour as its primary base, is among the best-known retail expressions of white rice flour's mainstream penetration, illustrating how consumer product reformulation at scale sustains bulk demand for millers.

Brown rice flour, the fastest-growing segment at a projected CAGR of 7.24% through 2031, benefits from a structural advantage that white rice flour does not share: its whole-grain positioning aligns with fiber and nutrient-density claims increasingly demanded by formulators targeting the health and wellness consumer. The global rise in whole-grain label claims, reinforced by General Mills' FY2026 commitment to delivering at least 8 g of whole grain per serving across its Big G cereals portfolio, signals that ingredient procurement is shifting toward whole-grain-compatible inputs at scale. Lundberg Family Farms' proprietary breeding investments, which delivered the Regenerative Organic Certified Black Pearl and Red Jasmine varieties in 2025, strengthen the specialty brown rice supply base and underpin premium brown rice flour positioning in natural retail channels.

By Nature: Conventional Maintains Scale; Organic Commands Growth Trajectory

Conventional rice flour retained 68.25% of the market in 2025, sustained by its price competitiveness and availability through established milling infrastructure serving large industrial buyers. The United States rice milling industry encompasses 78 plants, according to Kentley Insights' 2025 Rice Milling Market Report, the overwhelming majority of which operate on conventional (non-certified) supply chains that serve the nation's bakery and food manufacturing base. At this scale, price per hundredweight and supply consistency remain the primary purchasing criteria, where conventional flour retains a structural cost advantage.

Organic rice flour is forecast to advance at the highest CAGR in the market, 8.24% through 2031, driven by USDA organic-certified demand pulling purchasing from premium food retailers, baby food manufacturers, and health-focused foodservice operators. This growth rate is not solely a function of consumer preference; it also reflects supply-side investment. Lundberg Family Farms has transitioned more than 99% of its organically grown rice to Regenerative Organic Certified® status, while USDA AMS's November 2025 call for public comment on revisions to United States Standards for Rice may update grading definitions relevant to how organic and specialty grades are formally procured across the supply chain. The certification and traceability infrastructure required to serve the organic channel acts as a practical barrier that concentrates value in the hands of established certified millers, and organic-certified operators command significantly higher margin profiles, a dynamic that is attracting both incremental investment from large players and selective new entry from specialty operators.

By End Use: Industrial Scale Anchors Revenue; Retail Leads Growth

The industrial segment held 54.36% of market revenue in 2025, a position underpinned by rice flour's role as a functional workhorse across bakery manufacturing, snack extrusion, sauce thickening, and pet food coating operations. Industrial buyers operate at volumes where even modest per-unit price advantages translate into significant procurement savings, locking in supply contracts that favor large-scale millers with consistent production quality, supply chain transparency, and food safety assurance. Riceland Foods' April 2025 launch of a 64,000 sq ft FDA-compliant warehouse in Memphis, Tennessee, strategically positioned for rail-connected distribution across Arkansas and Missouri processing plants, directly addresses the logistics needs of industrial customers requiring reliable, high-volume supply.

The retail segment is forecast to grow at 8.23% CAGR through 2031, the fastest pace of any end-use channel. The underlying dynamic is not merely rising gluten-free awareness but the consolidation of alternative baking into mainstream supermarket assortments: Mintel's 2026 data shows United States consumers eating rice more than once a week jumped from 37% in 2023 to 45% in 2025, reflecting a normalization of rice-based products in everyday home cooking. Bob's Red Mill's selection to Fast Company's 2025 Most Innovative Companies list, alongside its November 2025 launch of Super-Fine Cake Flour, Self-Rising Flour, and High Fiber Flour, illustrates how specialty millers are creating retail pull by moving beyond commodity-flour positioning into functional baking solutions. The foodservice/HoReCa segment occupies the middle ground, serving gluten-free menu certification needs and Asian cuisine applications, with demand increasingly driven by chain restaurant procurement requirements that favor consistent ingredient grading.

Geography Analysis

The United States rice flour market is organized around a few production centers rather than a broad national manufacturing spread, and the South-Central region remains the core supply base because it holds the majority of United States long-grain rice milling capacity. Arkansas and nearby states matter most in this system because their mills support large industrial contracts for bakery, snack, and ingredient customers across the country. Riceland Foods processes more than 2.8 million tons of grain annually from 5,500 member farms concentrated in Arkansas and Missouri, which shows how much throughput is tied to this corridor. The same concentration also creates risk, and the Arkansas acreage decline in 2025 exposed how weather disruption in one region can tighten raw material availability for a large share of the United States rice flour market. USDA’s 2026 outlook for even lower Arkansas acreage suggests that mills and industrial buyers in this corridor may need more import blending or wider domestic sourcing to protect throughput.

California forms the second key production geography in the United States rice flour market because the Sacramento Valley is the country’s main medium- and short-grain base and a central node for specialty and organic flour supply. The state produces 24% of United States rice output, and although medium- and short-grain area fell by 15,000 acres in 2026, California still looks more stable than it did during the drought-disrupted 2022 period. This matters because certified organic and premium clean-label buyers depend on origin verification and documentation that California-based suppliers are often better positioned to provide. Lundberg Family Farms’ 2025 commercialization of Black Pearl rice, with 25% higher per-acre yield than prior cultivars, further strengthened the region’s long-term specialty supply base.

Demand in the United States rice flour market is strongest in high-value urban corridors along the Pacific Coast and in the Northeast, where packaged organic, gluten-free, and specialty baking products move through premium retail and foodservice channels. Minneapolis-St. Paul remains an important industrial procurement hub because large grain handlers and ingredient suppliers use the area to serve national bread and baking brands. Texas is also becoming more relevant as rice flour usage spreads in Asian-inspired quick-service formats and broader foodservice menus, which takes demand beyond its earlier gluten-free niche. The Southeast still functions mainly as a supply region, but local consumption is also rising as rice-based staples and snacks gain more everyday acceptance across diverse household groups

Competitive Landscape

The United States rice flour market is moderately concentrated because a limited number of large ingredient suppliers control major industrial relationships, while a second layer of specialty millers and natural food brands competes in premium retail and organic channels. Ingredion, Ardent Mills, Riceland Foods, and ADM remain the most visible names in large-scale supply, while Bob’s Red Mill, Lundberg Family Farms, Koda Farms, and Eden Foods carry a stronger presence in specialty and consumer-facing formats. This split shapes competition because industrial suppliers focus on price certainty, logistics, specification control, and compliance, while specialty players depend more on sourcing narratives, organic status, and retail brand trust. The result is a market where the top tier is meaningful, yet no single player appears to own every attractive niche inside the United States rice flour market. That gap is most visible in functional specialty grades such as pre-gelatinized, ultra-fine, and micronized rice flour for instant foods, beverage systems, and texture-sensitive applications.

Ingredion’s USD 100 million investment in its Indianapolis texture and healthful solutions facility shows how large players are trying to strengthen their position in higher-value functional ingredient categories around rice and starch systems. At the same time, improved precision milling and extrusion systems are helping smaller regional processors meet tighter particle-size and texture specifications, which makes mid-market competition more credible than it was before. Compliance also matters because USDA organic rules and FDA food safety expectations raise the cost of entry for new premium suppliers that lack documentation systems and audit readiness FDA. This keeps value concentrated among operators that can combine processing capability with certification discipline and customer support.

Strategic activity in 2025 and 2026 shows how companies are trying to widen capability rather than simply add volume in the United States rice flour market. Ardent Mills agreed to acquire Stone Mill in July 2025, which added gluten-free and identity-preserved grain processing strength to its emerging nutrition portfolio. Ingredion announced a recommended all-cash acquisition of Tate & Lyle in June 2026 at an implied enterprise value of GBP 3.7 billion, or USD 5.0 billion, which points to faster consolidation in global functional ingredients and could reshape formulation partnerships in the United States. Bob’s Red Mill also expanded its specialty baking range in late 2025, reinforcing the view that consumer-facing differentiation remains important even as larger suppliers chase industrial functionality and scale.

United States Rice Flour Industry Leaders

-

Archer Daniels Midland Company

-

Ingredion Incorporated

-

Ardent Mills LLC

-

Ebro Foods S.A.

-

General Mills, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Riceland Foods partnered with ODW Logistics to launch a new 64,000 sq ft FDA-compliant warehouse in Memphis, Tennessee, accessible by rail. The facility is designed to improve inventory redistribution, expand production capacity from Riceland's Arkansas and Missouri plants, and serve rising industrial customer demand for US-origin rice ingredients.

- February 2025: Ingredion announced a USD 100 million capital investment in its Indianapolis texture and healthful solutions manufacturing facility, targeting clean-label starches, rice-based ingredients, and specialty hydrocolloids as core growth areas. The company reported R&D spending of USD 71 million in FY2025, reinforcing its commitment to functional specialty ingredient development.

- July 2024: Cargill expanded its clean-label ingredient portfolio with the introduction of SimPure™ 92260, a highly soluble rice flour designed as a label-friendly alternative to maltodextrin. The ingredient delivers comparable viscosity, bulking functionality, and sensory performance while enabling a one-to-one replacement in a wide range of food applications, including bakery products, snacks, cereals, bars, dairy products, sauces, dressings, and convenience foods.

United States Rice Flour Market Report Scope

| White Rice Flour |

| Brown Rice Flour |

| Conventional |

| Organic |

| Retail |

| Foodservice/HoReCa |

| Industrial |

| By Source | White Rice Flour |

| Brown Rice Flour | |

| By Nature | Conventional |

| Organic | |

| By End Use | Retail |

| Foodservice/HoReCa | |

| Industrial |

Key Questions Answered in the Report

What is the 2026 value of the United States rice flour market?

The United States rice flour market stands at USD 148.45 million in 2026 and is forecast to reach USD 212.52 million by 2031 at a 6.15% CAGR

Which source segment leads United States rice flour demand?

White rice flour led with 75.23% share in 2025 because it offers neutral taste and consistent starch performance across bakery, coatings, and thickening uses.

Why is organic rice flour growing faster in the United States?

Organic rice flour is projected to grow at 8.24% through 2031 because premium retail, infant nutrition, and traceability-focused buyers are pulling more certified supply into the channel

Which end-use channel is expanding the fastest?

Retail is the fastest-growing end-use channel at an 8.23% CAGR through 2031, supported by stronger home baking demand and wider specialty flour offerings at mainstream stores

Page last updated on: