Bread Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

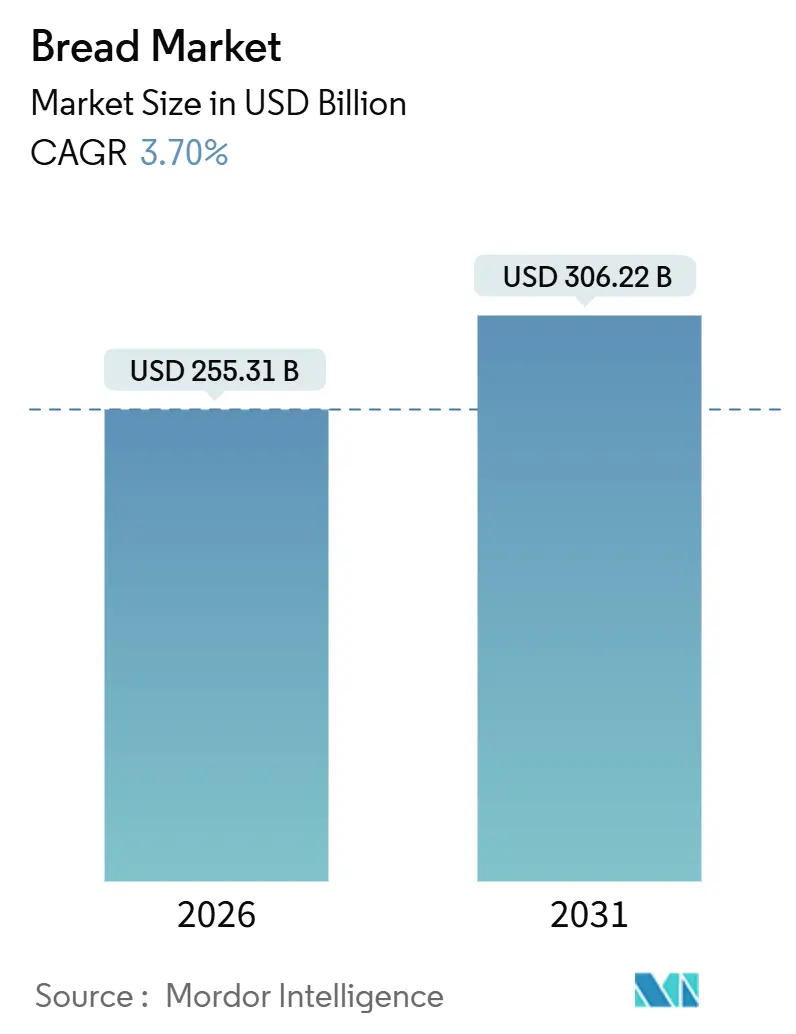

| Market Size (2026) | USD 255.31 Billion |

| Market Size (2031) | USD 306.22 Billion |

| Growth Rate (2026 - 2031) | 3.70% CAGR |

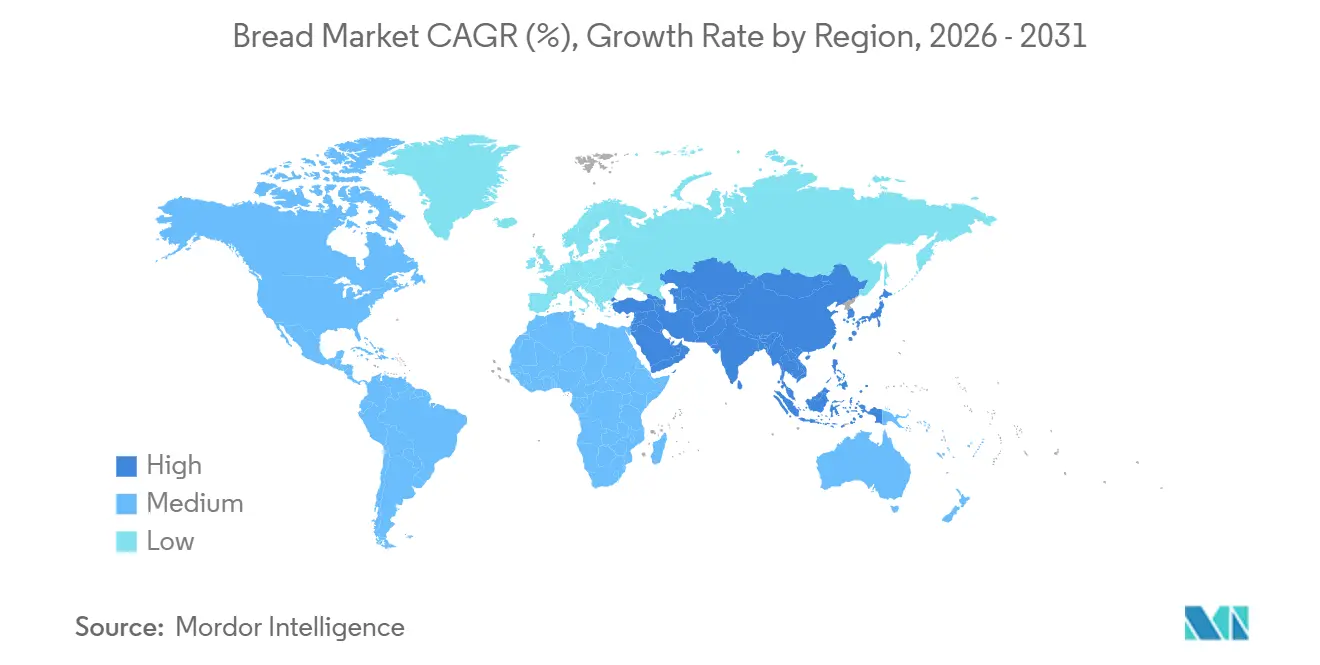

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bread Market Analysis by Mordor Intelligence

The bread market is valued at USD 255.31 billion in 2026 and is projected to reach USD 306.22 billion by 2031, advancing at a 3.70% CAGR. This growth is driven by urban migration, the rising focus on functional nutrition, and increasing digital commerce penetration, all contributing to the category's acceleration beyond traditional bakery trends. The growing popularity of multigrain and 'free-from' recipes highlights a significant shift in consumer perception, transforming bread from a basic staple to a wellness-oriented product. At the same time, producers are adopting technologies such as robotic handling and continuous mixing to maintain margins amid rising wheat costs. This growth is particularly evident in Asia-Pacific's mid-tier urban centers, where packaged loaves are replacing traditional flatbreads, and in Europe, where retailers are leveraging in-store bakeries to offer high-margin artisan products. Competitive strategies are focusing on vertical integration to manage costs and mergers and acquisitions to expand healthier product portfolios, supporting both volume stability and premium pricing in the bread market.

Key Report Takeaways

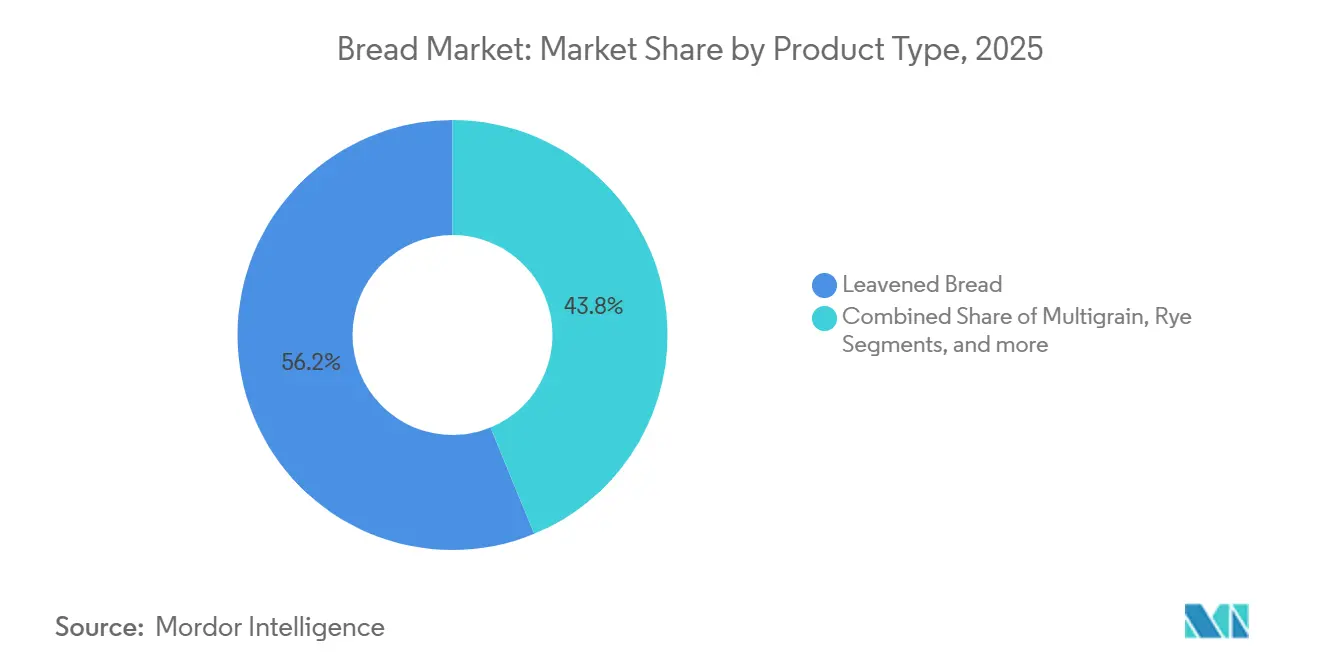

- By product type, leavened bread led with 56.21% of bread market share in 2025; unleavened and flatbreads are forecast to expand at a 3.92% CAGR through 2031.

- By ingredient type, wheat commanded 56.84% of the bread market size in 2025, whereas multigrain variants are projected to grow at a 4.11% CAGR between 2026-2031.

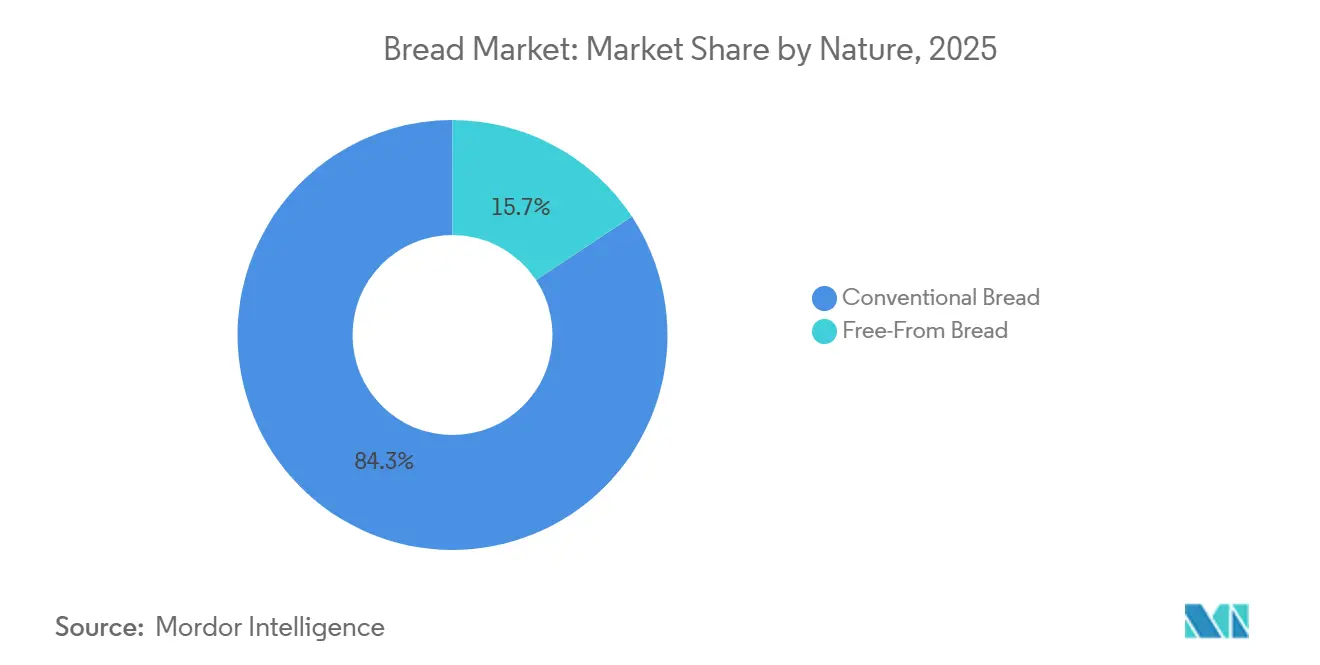

- By nature, conventional lines accounted for 84.29% of the bread market size in 2025, while free-from alternatives are advancing at a 5.32% CAGR during the same outlook period.

- By distribution channel, off-trade secured 64.11% of bread market sales in 2025, yet on-trade volumes are anticipated to climb at a 4.85% CAGR to 2031.

- By geography, Europe retained 29.55% revenue leadership in 2025; Asia-Pacific is set to deliver the fastest regional CAGR of 5.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bread Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for functional and fortified breads boosts demand | +0.8% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rapid urbanization driving packaged bread adoption | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥4 years) |

| Expansion of artisanal in-store bakeries | +0.5% | North America and Europe, emerging in urban South America | Short term (≤2 years) |

| Advancements in baking technology improve production efficiency | +0.6% | Global, led by North America and Europe | Medium term (2-4 years) |

| E-commerce penetration increasing direct-to-consumer frozen bread sales | +0.4% | North America, Europe, and tier-1 cities in Asia-Pacific | Short term (≤2 years) |

| Government wheat subsidy programs increasing affordability | +0.5% | India, United States, select Middle East markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising demand for functional and fortified breads

Functional bread has shifted from being a niche health food to becoming a common presence on mainstream shelves. This change is primarily driven by clearer regulations and consumers' willingness to pay more for proven health benefits. In December 2024, the United States Food and Drug Administration updated its "healthy" nutrient-content claim. The new guidelines require products to include substantial amounts of specific food-group components while restricting added sugars, saturated fats, and sodium. These updates have triggered extensive reformulations in the bread category. Over 80 countries now enforce fortification mandates, requiring wheat flour to be enriched with folic acid, iron, and B vitamins. This has established a baseline expectation, which many manufacturers are exceeding by incorporating omega-3s, prebiotics, and plant sterols. In 2024, India expanded its wheat flour fortification program nationwide, leading to an estimated 40% increase in folic acid intake among women of reproductive age. This highlights the critical role of policy in driving the adoption of functional ingredients. Leveraging this regulatory momentum, brands are launching breads designed to address specific health needs, such as cardiovascular health, gut microbiome support, and glycemic control. This transformation is redefining bread from a basic dietary staple to a proactive wellness product. However, the key challenge remains: integrating these bioactive ingredients without compromising the bread's flavor, texture, or overall sensory appeal.

Rapid urbanization driving packaged bread adoption

Urban migration in Asia-Pacific and Africa is reducing meal-preparation times and popularizing Western-style breakfast habits. This change is driving structural demand for shelf-stable, portion-controlled bread. The growing urban population supports this market trend. For instance, the Population Reference Bureau reported that 83% of North America's population lived in urban areas in 2025[1]Source: Population Reference Bureau, "World Population Data Sheet", prb.org. Urban households dedicate 25% to 30% less time to cooking compared to rural households, leading to a preference for pre-sliced loaves and burger buns over traditional flatbreads, which require skilled preparation. However, this shift varies by region; tier-2 and tier-3 cities are adopting packaged bread more rapidly than tier-1 metros, where the market is fragmented by a preference for artisanal and premium options. For manufacturers, this indicates that volume growth will increasingly come from mid-tier urban centers rather than established coastal hubs. Consequently, distribution networks must be optimized for smaller order sizes and longer last-mile routes.

Expansion of artisanal in-store bakeries

Supermarkets and hypermarkets are increasingly repurposing underutilized areas within their stores to establish in-store bakeries. These bakeries leverage the sensory appeal of freshly baked bread, particularly its aroma, to attract more customers and encourage larger purchases. This shift gained significant traction after the pandemic, as retailers aimed to differentiate themselves from the growing competition posed by e-commerce platforms and discount store formats. In North America, Whole Foods and Wegmans have notably expanded their in-store bakery operations by 15% to 20% since 2023. These expansions include the installation of stone-deck ovens and the recruitment of certified bakers to produce high-quality, European-style artisan loaves. The strategic intent behind this move is clear: in-store bakeries not only deliver higher gross margins compared to center-store packaged bread but also create a positive perception of the retailer as a premium-quality destination. However, this strategy is not without its challenges. Labor costs and waste rates remain significant concerns, as artisanal bread has a much shorter shelf life of 24 to 48 hours, compared to the 7 to 10 days typical for packaged loaves.

Advancements in baking technology improve production efficiency

Bakeries are increasingly adopting automation and digitalization to address ongoing challenges such as thin profit margins and skilled labor shortages. These technologies help reduce labor dependency, enhance product consistency, and expedite product changes. FANUC, in collaboration with the Danish Technological Institute, developed a robotic bread production system. This solution, integrated with vision technology, identifies defects in real-time, cutting waste by 15% and ensuring compliance with retailer quality standards. Reading Bakery Systems launched its continuous mixing technology in several European plants in 2025. This system enables bakers to quickly adjust dough hydration and fermentation parameters, allowing them to respond promptly to fluctuations in ingredient costs or changes in consumer preferences. However, these innovations are capital-intensive, with the high cost of robotic lines favoring larger, established players and creating a competitive barrier for smaller regional bakeries. This trend points to a future industry structure divided into two segments: large, automated bakeries serving the mass market and small, artisanal bakeries targeting premium niches, leaving mid-sized producers at a disadvantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in global wheat prices compressing margins | -0.6% | Global, acute in import-dependent Middle East and North Africa | Short term (≤2 years) |

| Safety concerns and product recalls | -0.3% | North America and Europe, emerging awareness in Asia-Pacific | Short term (≤2 years) |

| Cold-chain gaps limiting frozen bread distribution | -0.4% | Sub-Saharan Africa, Southeast Asia, rural South America | Medium term (2-4 years) |

| Growing popularity of low-carb diets negatively impacts bread consumption | -0.7% | North America, Europe, urban Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in global wheat prices compressing margins

Geopolitical tensions, weather anomalies, and export restrictions are driving fluctuations in wheat prices, which are negatively impacting bakery profitability. This is particularly evident in regions dependent on imports and lacking effective hedging mechanisms. The United States Congressional Budget Office predicts that wheat prices will average USD 6.80 per bushel in 2026, reflecting a 9.7% rise from 2024[2]Source: United States Department of Agriculture, "USDA Agricultural Projections to 2033", usda.gov. This price volatility is further exacerbated by Russia's export quotas and drought conditions in Australia's wheat-producing regions. Bread manufacturers, who typically operate with gross margins of 25% to 35%, are under pressure: a 10% increase in wheat prices can reduce net margins by 3 to 5 percentage points unless retail prices are adjusted. In Egypt and Morocco, where wheat imports are a significant part of the supply chain, governments have imposed bread price caps to maintain social stability. This policy forces private bakeries to either absorb the higher costs or exit the market. Smaller producers, however, often lack the financial resources to manage these challenges, leaving them particularly susceptible to margin compression and potential market consolidation.

Growing popularity of low-carb diets negatively impacts bread consumption

In high-income markets, where increasing obesity and diabetes rates drive health-conscious eating, diets such as ketogenic, paleo, and low-carb have redefined bread from a dietary staple to a discretionary indulgence. This change is not confined to North America; urban consumers in China and India are also shifting away from traditional staples like rice and bread, favoring protein-rich alternatives such as eggs, Greek yogurt, and legume-based snacks. Manufacturers are addressing this trend by launching protein-enriched breads. For example, Flowers Foods introduced Nature's Own Keto buns in April 2024, featuring just 1 gram of net carbs. However, these products primarily target a niche audience and have not reversed the overall decline in bread consumption. This indicates that bread producers must either adapt to slower volume growth by focusing on premium offerings or diversify into related categories like tortillas, wraps, and flatbreads that align with low-carb dietary preferences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flatbreads Gain as Ethnic Cuisines Mainstream

Between 2026 and 2031, the market for unleavened and flatbreads is expected to grow at a rate of 3.92%, exceeding the 3.55% growth anticipated for leavened bread. This trend is driven by the increasing adoption of tortillas, pitas, and chapatis, which are transitioning from ethnic specialties to everyday staples in multicultural markets. In 2025, leavened bread accounted for 56.21% of the market, supported by the popularity of sliced loaves, burger buns, and baguettes in North American and European breakfast and sandwich occasions. However, unleavened formats are gaining traction, particularly in quick-service restaurants, where tortilla wraps and pita pockets offer hand-held convenience and portion control that traditional sandwiches often lack. Ciabatta and specialty leavened breads are growing faster than standard white loaves, reflecting a shift toward premiumization within the leavened segment. Baguettes remain culturally significant in France, where protected geographic indications ensure traditional production methods. At the same time, frozen par-baked baguettes are capturing market share in export regions that prioritize convenience over authenticity.

Producers with flexible production lines capable of alternating between leavened and unleavened formats are better positioned in the competitive landscape. This flexibility is increasingly important as retailers demand a wider variety of SKUs to meet the needs of diverse consumer groups. While leavened bread remains versatile across meal occasions, such as breakfast toast, lunch sandwiches, and dinner sides, its growth is limited by market saturation in mature regions and competition from low-carb alternatives. The expansion of quick-service restaurants continues to drive demand for burger buns and sandwich slices. Meanwhile, unleavened breads face fewer regulatory challenges, as they typically do not require the preservatives and dough conditioners needed for leavened bread's shelf stability, appealing to consumers seeking clean-label products. The growth outlook for this segment indicates that producers heavily reliant on traditional loaves risk losing market share unless they diversify into flatbread formats or invest in premium leavened options that justify higher price points.

By Ingredient Type: Multigrain Breads Capture Health-Conscious Spend

Between 2026 and 2031, multigrain bread is expected to achieve the highest growth rate among ingredient types, with a projected CAGR of 4.11%. This growth is fueled by increasing consumer demand for fiber, protein, and micronutrients that refined wheat lacks. In 2025, wheat bread accounted for 56.84% of the revenue, supported by well-established supply chains, a neutral flavor profile, and cost advantages compared to specialty grains. However, multigrain options featuring ingredients like oats, barley, flax, quinoa, and ancient grains are gaining popularity in North America and Europe. These regions emphasize dietary guidelines recommending 25 to 30 grams of daily fiber, with whole-grain consumption linked to reduced cardiovascular risks. Rye bread, on the other hand, retains its niche appeal in Scandinavia and Germany, where dense, sourdough-leavened loaves are cultural staples.

The dominance of wheat bread is largely due to its scalability in agriculture and efficient processing. However, this cost advantage is gradually shrinking as ingredient suppliers achieve economies of scale in ancient-grain milling and retailers accept higher prices for health-oriented products. Rye bread's limited growth outside Northern Europe highlights the challenges of scaling niche grains, as rye requires longer fermentation times and specialized baking techniques, increasing production complexity. Multigrain formulations enable manufacturers to market products as "whole grain" or "high fiber" without the sensory drawbacks of 100% whole-wheat bread, which many consumers find too dense or bitter. The growth trajectory of the multigrain segment suggests that innovation in blending functional grains with sensory modifiers will be a key driver for capturing market share.

By Nature: Free-From Breads Command Premium Pricing

Between 2026 and 2031, the free-from bread market is projected to grow at a CAGR of 5.32%, nearly twice the overall category's growth rate. This increase is fueled by a rise in celiac diagnoses, greater allergen awareness, and a shift toward clean-label preferences, driving demand for gluten-free, low-sodium, and additive-free products. In 2025, conventional bread accounted for 84.29% of the market volume due to its affordability and wide availability. However, free-from variants are capturing a larger share of market value, supported by their price premiums. The United States Food and Drug Administration requires gluten-free products to contain less than 20 parts per million of gluten, creating a regulatory advantage for specialized manufacturers with dedicated production facilities. Low-sodium breads are gaining popularity as hypertension rates climb. The American Heart Association recommends a daily sodium intake of no more than 1,500 milligrams, but a single serving of conventional bread can contain 150 to 250 milligrams. This has prompted reformulations that reduce sodium content by 25% to 40% without compromising flavor.

Conventional bread continues to dominate the market due to its accessibility and lower cost. However, as suppliers scale up production, the prices of gluten-free flours, such as rice, tapioca, and potato, are decreasing. This trend is narrowing the price gap, making free-from options more accessible to mainstream consumers. Certifications from organizations like the Gluten Intolerance Group's Gluten-Free Certification Organization provide third-party validation, enhancing consumer trust and supporting premium pricing. Despite this, free-from breads face challenges in replicating the texture and shelf life of gluten-containing products. Gluten's elasticity and structural properties are difficult to replicate with alternative binders like xanthan gum or psyllium husk. To address these issues, manufacturers are investing in enzyme technologies and fermentation methods. Some brands have achieved near-equivalence with conventional bread in blind taste tests. The rapid growth of this segment reflects a lasting change in consumer expectations, where "free-from" has evolved from a niche health claim to a mainstream attribute influencing purchasing decisions across various demographics.

By Distribution Channel: On-Trade Rebounds as Foodservice Recovers

Between 2026 and 2031, on-trade channels are expected to grow by 4.85%, surpassing the off-trade's growth rate of 3.45%. This growth is driven by restaurants, hotels, and catering services recovering from pandemic-related declines and focusing on premium bread to enhance their menu offerings. In 2025, off-trade channels, including supermarkets, hypermarkets, convenience stores, and online retail, accounted for 64.11% of total sales. These channels benefit from frequent purchases and impulse buying. However, the on-trade recovery is primarily supported by quick-service restaurants incorporating artisanal bread into value meals. Full-service restaurants are upgrading their bread offerings, replacing standard rolls with house-made sourdough and focaccia. This strategy not only differentiates their menus but also increases the perceived value of meals. Additionally, hotel breakfast buffets, a key on-trade segment, are expanding their bread options to include gluten-free, multigrain, and ethnic varieties, catering to international guests and dietary preferences.

Off-trade's stronghold is maintained by supermarkets and hypermarkets, which drive significant bread sales through private-label programs that offer competitive pricing while maintaining acceptable quality. Convenience and grocery stores also play a crucial role by meeting top-up shopping needs, supported by extended hours and proximity to residential areas. Online retail is the fastest-growing segment, with e-commerce platforms effectively managing cold-chain logistics to deliver frozen dough and ambient-stable loaves. Rising internet penetration further boosts online bread sales. For example, in 2024, 5.5 billion people, or 68% of the global population, were internet users, up from 65% in the previous year, according to the International Telecommunication Union[3]Source: International Telecommunication Union, "Facts and Figures 2024 - Internet use", itu.int. Specialist retailers, such as health-food stores and ethnic grocers, address niche demands for organic, gluten-free, and culturally specific breads, which are often underrepresented in mainstream channels. The faster growth of the on-trade reflects shifts in the foodservice industry. Labor shortages are prompting operators to adopt pre-sliced, portion-controlled bread to reduce preparation time, while premiumization trends favor suppliers offering customization and co-branding options. These trends suggest that manufacturers should implement a dual strategy: produce high-volume, cost-effective products for the off-trade and develop differentiated, service-oriented offerings for the on-trade to achieve comprehensive market coverage.

Geography Analysis

In 2025, Europe accounted for 29.55% of global bread revenue, with Germany, France, and the United Kingdom leading the charge. In these nations, bread isn't just food; it's a cultural staple, with per-capita consumption surpassing 50 kilograms annually. While Germany leans towards dense, whole-grain varieties, France cherishes its protected-origin baguettes. This creates a stable demand, but both markets face challenges: population stagnation and a shift in dietary preferences limit volume growth. Meanwhile, Italy and Spain are outpacing their northern counterparts, fueled by a surge in foodservice demand from tourism and an uptick in breakfast bread consumption, due to a Mediterranean diet embracing more baked goods. In Russia, where state-subsidized rye loaves once reigned supreme, there's a notable shift towards packaged wheat bread. This change is propelled by urbanization and the encroachment of Western retail formats. However, geopolitical sanctions have thrown a wrench in ingredient imports and stifled innovation. Looking ahead, even as volumes stabilize, the region's trajectory hints at value gains driven by premiumization and organic positioning.

Asia-Pacific is set to outpace all regions, with a projected growth rate of 5.25% from 2026 to 2031. As incomes rise in China, India, and Southeast Asia, there's a noticeable shift from rice-centric diets to an embrace of packaged bread. In India, Britannia Industries' expansion, coupled with government wheat-procurement programs stabilizing flour prices, has spurred a surge in packaged bread consumption. Southeast Asia, particularly Thailand, Indonesia, and Vietnam, holds immense growth potential. However, cold-chain deficiencies hinder frozen-dough distribution, compelling manufacturers to invest heavily in ambient-stable alternatives. Growth patterns in the region are uneven: while coastal urban centers swiftly adopt packaged bread, rural locales remain steadfast to rice and traditional flatbreads. This creates a divided market, necessitating customized distribution and product strategies.

North America is witnessing a decline in per-capita consumption. This downturn is largely attributed to the rising popularity of low-carb and gluten-free diets, which are reshaping traditional bread consumption habits. The United States bread market is becoming increasingly consolidated. Major players like Flowers Foods, Grupo Bimbo, and Associated British Foods now command a significant share of packaged bread sales, leaving scant opportunity for newcomers. In Canada, bread consumption is on a modest rise, buoyed by a growing immigrant population and a heightened demand for ethnic breads such as naan and pita. Mexico stands out as a burgeoning market within North America, with tortilla consumption surging by 8% annually. This growth is driven by the expansion of quick-service restaurants and the rising popularity of home meal replacement kits. In South America, Brazil and Argentina lead the bread market, with offerings like French-style baguettes and Italian-inspired loaves echoing their colonial culinary histories. The Middle East and Africa present a patchwork of opportunities. In the United Arab Emirates and Saudi Arabia, wheat imports and bread price subsidies aim to keep bread affordable. In contrast, Sub-Saharan Africa grapples with challenges: low purchasing power and a lack of cold-chain infrastructure hinder the penetration of frozen doughs in the bread market.

Mordor Intelligence provides coverage of the bread market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The bread market is highly fragmented, with multinational corporations, regional leaders, and local specialists actively competing across different price ranges and product categories. Grupo Bimbo SAB de CV, Flowers Foods, Inc., and Associated British Foods Plc dominate the market by utilizing their extensive distribution networks and diverse brand portfolios. However, smaller specialists focusing on premium offerings are challenging these leaders by providing unique, high-quality bread options that cater to niche consumer preferences.

To mitigate wheat-price volatility, industry players are adopting vertical integration strategies. For example, Associated British Foods acquired Hovis Group in August 2025, gaining milling assets that secure flour costs and enable proprietary blends. Technology adoption is a key competitive differentiator, with leading companies implementing robotic depanning, AI-driven quality vision, and continuous mixing systems to reduce labor costs by 30% to 40% while improving product consistency. In the free-from and multigrain segments, smaller brands like Canyon Bakehouse and Dave's Killer Bread are thriving, achieving premium pricing and strong sales despite limited distribution. Emerging disruptors are also leveraging direct-to-consumer models, such as frozen bread subscriptions and meal-kit partnerships, to bypass traditional retail channels and capture higher margins, though scaling these operations remains a challenge.

Strategic trends in the industry highlight a divide: mass-market producers prioritize cost leadership through automation and product line optimization, while premium brands focus on clean labels, organic certifications, and co-branding with foodservice operators. Patent activity is concentrated on enzyme technologies and fermentation processes that naturally extend shelf life without preservatives. For instance, a 2024 patent by Lesaffre introduces a yeast strain that produces natural antimicrobials, reducing the need for additives like calcium propionate and sorbates, which consumers increasingly avoid. The competitive landscape indicates that mid-sized producers lacking scale or differentiation may face margin pressures, while agile specialists and vertically integrated giants are positioned to capture significant market value.

Bread Industry Leaders

-

Grupo Bimbo S.A.B. de C.V.

-

Yamazaki Baking Co., Ltd.

-

Flowers Foods, Inc.

-

Campbell Soup Company

-

Associated British Foods Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bonn introduced True Zero Maida wholewheat brown bread, A health-focused option. Bonn's True Zero Maida wholewheat brown bread sets a new benchmark in the healthy bread category.

- January 2025: Flowers Foods acquired Simple Mills for USD 795 million, significantly expanding its presence in the better-for-you baked goods segment with a brand known for clean ingredients and nutritional focus.

- January 2025: Schmidt Baking, part of the H and S Family of Bakeries, has rolled out a new bread line under its Old Thyme brand, named Artisan’s Choice. The lineup features three distinct varieties: Italian Rustico, crafted with olive oil, sea salt, garlic, and onion; and Rustic Brioche, a sweet, indulgent loaf that's both dairy and egg-free.

- September 2024: Grupo Bimbo expanded its South American presence by acquiring Brazil-based Wickbold brands, enhancing its product portfolio and distribution capabilities in the region's largest bread market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global bread market as all leavened and unleavened loaves, rolls, buns, baguettes, and flatbreads baked from grain-based dough and sold fresh or frozen through retail, foodservice, and institutional channels across every major geography. Bread from both artisanal bakeries and industrial lines is counted at wholesale value in USD.

Products such as bread mixes, improvers, crumbs, pizza-crust blanks, and non-grain substitutes are outside this scope.

Segmentation Overview

-

By Product Type

-

Leavened Bread

- Loaves

- Baguettes

- Burger Buns

- Sandwich Slices

- Ciabatta

- Other Product Types

-

Unleavened/Flat Bread

- Tortilla

- Pita

- Chapati/Roti/Paratha

- Others

-

Leavened Bread

-

By Ingredient Type

- Wheat Bread

- Rye Bread

- Multigrain Bread

- Other Ingredients

-

By Nature

- Conventional Bread

- Free-From Bread

-

By Distribution Channel

-

Off-Trade

- Convenience/Grocery Stores

- Specialist Retailers

- Supermarkets/Hypermarkets

- Online Retail

- Other Channels

- On-Trade

-

Off-Trade

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed commercial bakers, grain millers, ingredient blenders, and grocery buyers across North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. These conversations confirmed average selling prices, premiumization trends, gluten-free penetration, and plant-capacity utilizations that secondary data only hinted at.

Desk Research

We began with factual datasets from sources such as FAO crop balances, USDA ERS grain outlooks, Eurostat retail indices, and the Federation of Bakers consumption panels to frame supply, demand, and price corridors. Company filings and investor decks strengthened channel-split assumptions, while news archives from Dow Jones Factiva and financials within D&B Hoovers informed competitive concentration.

Trade-association releases, UN Comtrade shipment ledgers, and peer-reviewed nutrition journals provided signals on health-driven product shifts. The list above is illustrative, and many other publications were consulted for data collection, validation, and clarification.

Market-Sizing and Forecasting

We apply a top-down reconstruction that starts with country-level flour usage and bread-production statistics, then adjusts for trade flows and wastage to derive apparent bread output. Results are cross-checked with selective bottom-up roll-ups of sampled baker revenues and retailer scan volumes. Key variables include global wheat output, per-capita bread intake, packaged-bread share in urban retail, average loaf ASP progression, and health-claim penetration. A multivariate regression model projects each driver through 2030, and scenario stress tests refine growth in volatile grain-price years before final sign-off by our lead analyst team.

Data Validation and Update Cycle

Outputs pass three-layer variance checks, peer review, and senior sign-off. Reports refresh annually, with interim updates triggered when a material shock, such as a harvest shortfall or new labeling law, alters the base equation. A final pass is run just before delivery so clients receive the latest view.

Why Mordor's Bread Baseline Commands Reliability

Published estimates often diverge because firms choose dissimilar product lists, pricing nodes, and refresh cadences. Key gap drivers include packaged-only scopes, aggressive ASP escalators, or reliance on historical consumption elasticities that new operator feedback no longer supports.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 245.13 B (2025) | Mordor Intelligence | |

| USD 342.4 B (2024) | Global Consultancy A | Excludes unpackaged artisanal bread yet inflates value by applying retail markups across all units |

| USD 196.95 B (2024) | Trade Journal B | Limited country coverage and flat ASPs that ignore premium health segments |

This comparison shows that Mordor's disciplined scope selection, variable tracking, and annual refresh deliver a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the bread market and its expected size by 2031?

The bread market stands at USD 255.31 billion in 2026 and is projected to reach USD 306.22 billion by 2031.

How fast is the bread market growing?

It is expanding at a 3.70% CAGR over the 2026-2031 forecast period.

Which product segment is growing the fastest?

Unleavened and flatbreads are forecast to post the highest growth at a 3.92% CAGR through 2031.

Why are multigrain breads gaining popularity?

Consumers seek higher fiber and micronutrient density, pushing multigrain variants to a 4.11% CAGR.

Page last updated on: