Market Overview

| Study Period | 2021 - 2031 |

|---|---|

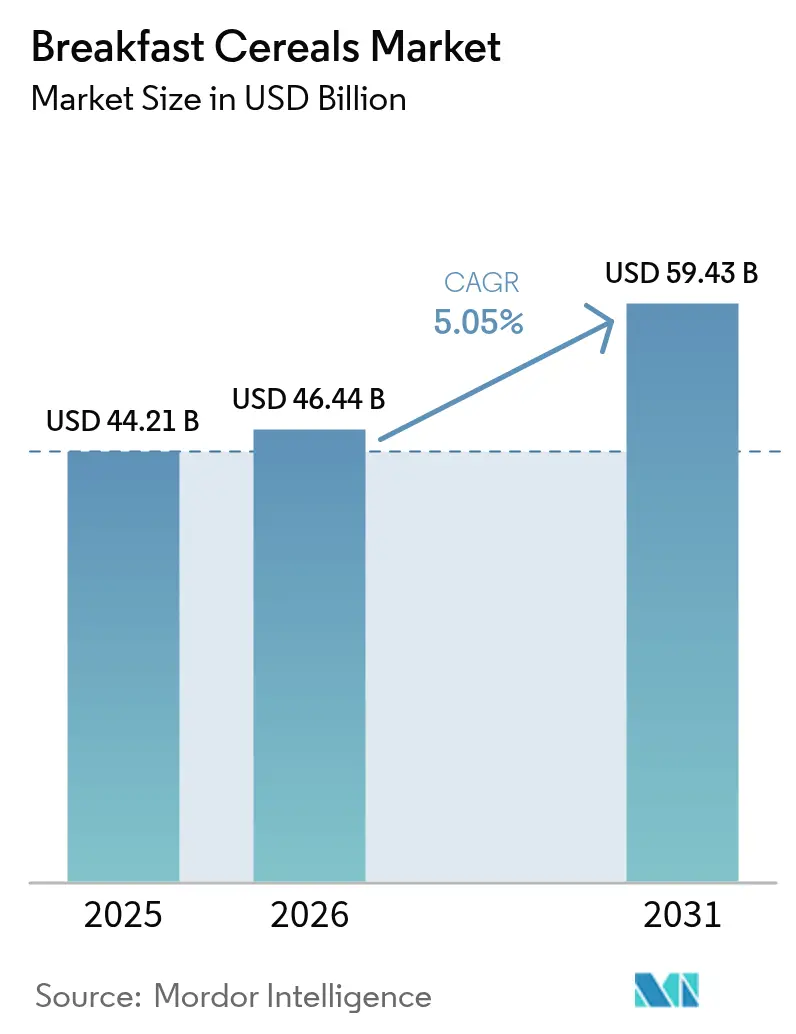

| Market Size (2026) | USD 46.44 Billion |

| Market Size (2031) | USD 59.43 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Breakfast Cereals Market Analysis by Mordor Intelligence

The global breakfast cereals market size was valued at USD 44.21 billion in 2025 and estimated to grow from USD 46.44 billion in 2026 to reach USD 59.43 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031). The market growth is driven by changing consumer preferences, increased health consciousness, and demand for convenient breakfast options. The fast-paced modern lifestyle has increased the demand for ready-to-eat and hot cereal products that offer quick meal solutions. Consumers are seeking cereals with enhanced nutritional profiles, including those fortified with fiber, protein, whole grains, and probiotics, while preferring options with reduced sugar content. The market is also experiencing growth in plant-based, organic, and gluten-free varieties to meet specific dietary requirements. In addition, the rise of e-commerce and digital grocery platforms has improved product accessibility, particularly in developing markets, contributing to the breakfast cereals market's expansion.

Key Report Takeaways

- By product type, ready-to-eat cereals led with 74.60% of breakfast cereals market share in 2025; the ready-to-cook segment is advancing fastest at a 5.75% CAGR through 2031.

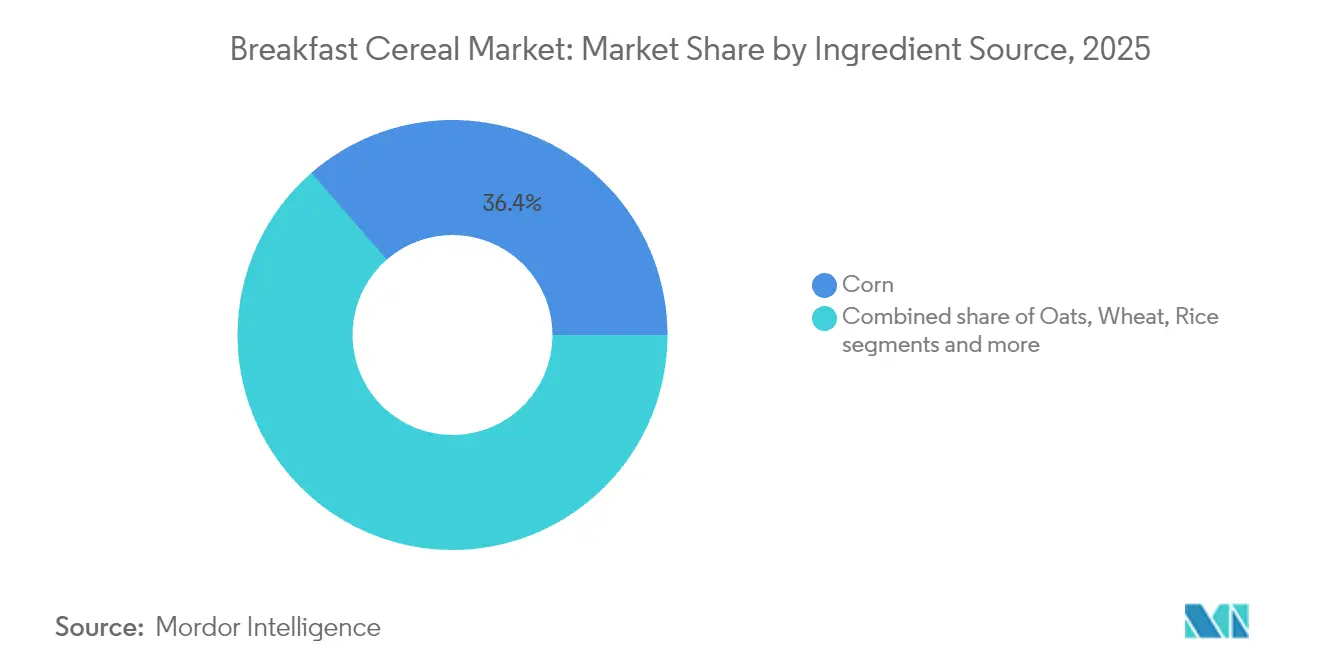

- By ingredient source, corn captured a 36.40% share of the breakfast cereals market size in 2025, whereas oat-based products are set to expand at a 6.25% CAGR to 2031.

- By packaging, traditional paperboard boxes retained 64.70% of 2025 revenue, while cups and other on-the-go formats are growing at a 9.45% CAGR, reflecting evolving packaging trends in the breakfast cereals market.

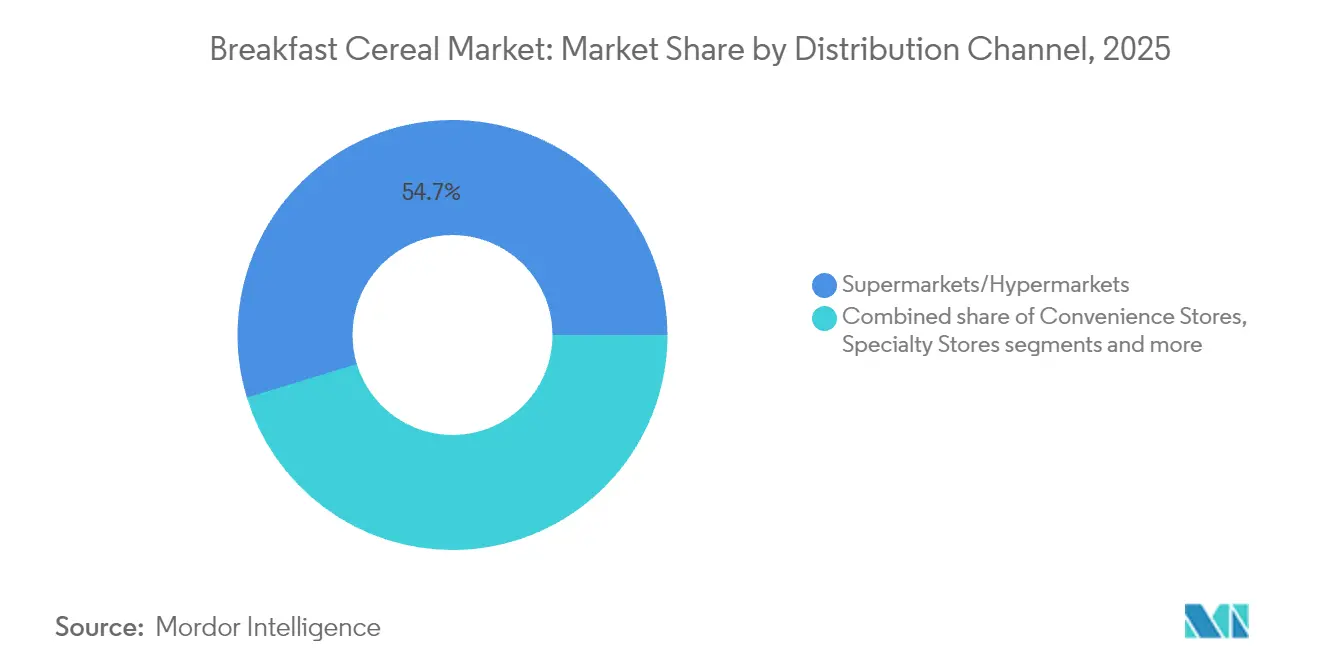

- By distribution channel, supermarkets/hypermarkets commanded 54.70% share of the breakfast cereals market size in 2025, while online retailers are advancing at an 10.85% CAGR through 2031.

- By age group, adults accounted for 47.60% of the breakfast cereals market share in 2025, while the children’s segment is projected to grow at a 5.07% CAGR through 2031.

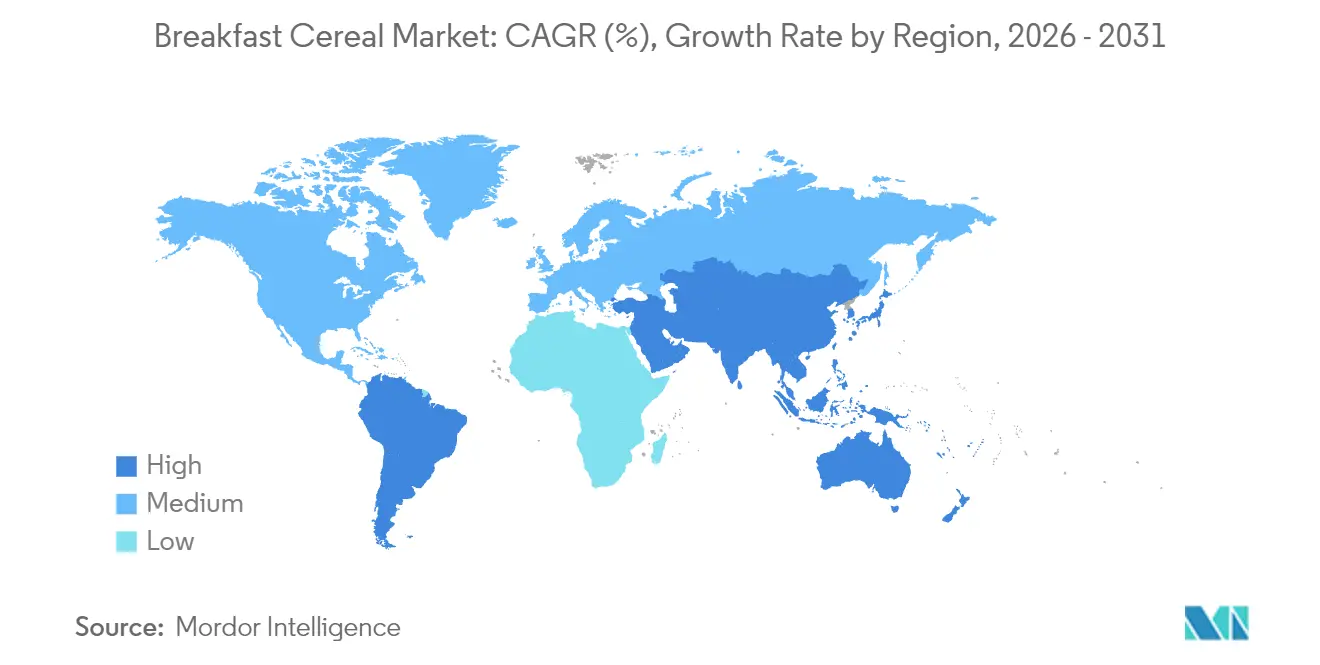

- By geography, North America maintained a 36.30% share of the breakfast cereals market in 2025; Asia-Pacific is projected to rise at a 6.10% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breakfast Cereals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-protein cereal variants among consumers | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Surge in single-serve breakfast habits fueling on-the-go cereal cups | +0.8% | Global, particularly urban centers in Asia-Pacific and North America | Short term (≤ 2 years) |

| Growing penetration of gluten-free grains expanding multi-grain cereals | +1.1% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Private-label premiumization driving value growth | +0.7% | Global, with strongest impact in Europe and North America | Long term (≥ 4 years) |

| Production technology advances enhance product quality | +0.9% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Rising children's population increases nutritional focus | +0.6% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Protein Cereal Variants Among Consumers

The breakfast cereals market is experiencing a notable transition toward protein-enriched products, driven by increased consumer focus on nutrition and health. In December 2024, General Mills Inc. expanded its Cheerios portfolio by introducing Cheerios Protein, which contains 8 grams of protein per serving. This product launch reflects market trends, supported by the 2024 Food and Health Survey from the International Food Information Council, which revealed that 71% of consumers aim to increase their protein consumption [1]Source: International Food Information Council, "2024 IFIC Food and Health Survey", ific.org. The protein cereal segment has gained particular momentum among millennial parents seeking both nutritional value and convenience, enabling manufacturers to implement premium pricing strategies. Manufacturers are also expanding their protein sources beyond dairy to include plant-based alternatives, addressing the growing flexitarian consumer base and creating new market opportunities in the breakfast cereal category. This shift continues to shape the breakfast cereals market.

Surge in Single-Serve Breakfast Habits Fueling On-the-Go Cereal Cups

The global breakfast cereals market is experiencing significant growth driven by increasing demand for single-serve and on-the-go breakfast formats, particularly cereal cups. This trend reflects the impact of urbanization and changing lifestyles among working professionals and students who have limited time for traditional breakfast meals. Single-serve cereal cups meet consumer needs by combining convenience with nutrition through portable, portion-controlled options that are easy to prepare. These formats are particularly popular in urban areas where consumers often eat breakfast during their commute or at work. Also, major cereal manufacturers are responding by diversifying their product lines with portable formats that incorporate ingredients such as granola, oats, seeds, and various milk options. The products feature improved packaging designs, including microwaveable containers, resealable lids, and recyclable materials, which enhance both functionality and environmental sustainability in the breakfast cereals market. For instance, in October 2024, Inventure launched four of its popular cereal flavors in a new 'on the go' cup format, designed for consumption at pre-school, office, or as a snack, requiring consumers to simply peel back the lid and add milk.

Growing Penetration of Gluten-Free Grains Expanding Multi-Grain Cereals

The global breakfast cereals market is experiencing growth driven by the increasing adoption of gluten-free grains and multi-grain cereals. Rising cases of gluten sensitivity, celiac disease, and consumer preference for gluten-free options have increased the demand for cereals made from alternative grains, including quinoa, amaranth, millet, sorghum, buckwheat, and brown rice. These alternatives address dietary restrictions while meeting consumer interest in wellness and gut health. Multi-grain cereals are gaining popularity due to their nutritional benefits across the breakfast cereals market, including high fiber content, essential vitamins, minerals, and complex carbohydrates that support digestive health, sustained energy, and cardiac function. For instance, in May 2024, Three Wishes, a family-owned health-focused cereal brand, launched its first grain-free granola line in three varieties: Chocolate Almond, Maple Pecan, and Original.

Private-Label Premiumization Driving Value Growth

Private label breakfast cereal brands have evolved from basic lower-cost alternatives into significant market competitors within the breakfast cereals segment. The Private Label Manufacturers Association's 2024 Annual Private Label Report indicates that store brand sales grew by 4.7% in 2023 compared to 2022. This transformation is particularly evident in health-focused breakfast cereal segments, where retailers use adaptable supply chains to introduce products that meet emerging nutritional preferences in the breakfast foods category. Retailers have enhanced their private label breakfast cereal offerings through improved packaging and merchandising while maintaining competitive pricing against national breakfast cereal brands. This increased competition has prompted national breakfast cereal manufacturers to accelerate product innovation and reevaluate their market positioning. The private label growth in breakfast cereals is strongest in North America and Europe, where consolidated retailers have developed robust consumer research capabilities and product development infrastructure for breakfast food categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile oat and corn commodity prices compressing margins | -0.9% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Intensifying anti-sugar advocacy affecting cereal sales | -0.7% | Global, with regulatory leadership in North America and Europe | Medium term (2-4 years) |

| Environmental concerns about packaging | -0.5% | Global, with regulatory pressure in Europe and North America | Medium term (2-4 years) |

| Supply chain issues and raw material cost fluctuations | -0.4% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Oat and Corn Commodity Prices Compressing Margins

Cereal manufacturers face increasing margin pressure as key ingredient costs experience significant volatility, affecting pricing strategies and production planning. The Food and Agriculture Organization (FAO) forecasts global cereal trade to decline to 478 million tonnes in 2024/25, a 6.8% decrease from 2023/24. Agricultural adaptations, including stress-tolerant hybrids and improved farming practices, have partially offset grain price volatility caused by climate change and erratic weather patterns. However, market dynamics remain unstable. The United States Department of Agriculture (USDA) projects tightening supplies for key grains in 2024-25, despite minor increases in global wheat production. This supply constraint affects manufacturers with global supply chains, as regional production disruptions impact interconnected ingredient markets. Companies are managing these challenges through long-term supplier contracts, flexible ingredient formulations, and hedging programs to stabilize input costs.

Intensifying Anti-Sugar Advocacy Affecting Cereal Sales

Growing consumer awareness of sugar's health implications presents a significant market restraint, fundamentally impacting product development and market performance across the breakfast cereals category. This constraint is particularly evident in children's cereals, where manufacturers face increasing pressure to reduce high sugar content, which traditionally served as a key taste differentiator. In 2024, the Food and Drug Administration (FDA)'s Dietary Guidelines Advisory Committee report further intensifies market challenges by recommending added sugar limitation to less than 10% of daily calories and identifying breakfast cereals as a major source of hidden sugars in the diet. In response to these market constraints, manufacturers are implementing various reformulation strategies, including alternative sweeteners, flavor-enhancing technologies that maintain sweetness perception at lower sugar levels, and gradual reduction approaches to minimize consumer rejection across the breakfast cereals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Source: Corn Leads While Oats Surge

Corn-based cereals hold a dominant 36.40% market share in 2025, benefiting from cost advantages and manufacturing efficiencies that enable competitive pricing in value segments. Oat-based products show the highest growth rate at 6.25% CAGR (2026-2031), supported by their established nutritional benefits and adaptability in both ready-to-eat (RTE) and ready-to-cook (RTC) formats. Technological advancements in oat processing have improved texture and flavor while maintaining nutritional value. The European Union leads global oats production at 33%, followed by Canada at 15% for 2024/25, according to the United States Department of Agriculture (USDA) . The regional consumption of oat-based breakfast cereals continues to increase, driven by consumer demand for nutritious, high-fiber breakfast products in the breakfast cereals market.

Wheat-based cereals continue to hold substantial market share, especially in flaked formats, while rice-based cereals gain traction in the gluten-free category. Barley remains limited to multi-grain formulations despite its nutritional benefits. Alternative grains, including quinoa and amaranth, show rapid growth in premium segments, though their overall market share remains small. This expanding range of grain sources reflects industry efforts to develop distinct products for specific dietary requirements, as demonstrated by Nestlé's commitment to using whole grains as the primary ingredient in all their ready-to-eat cereals.

By Product Type: RTE Dominates While RTC Accelerates

Ready-to-eat (RTE) cereals hold a dominant 74.60% market share in 2025, primarily due to their convenience for time-constrained households. Ready-to-cook (RTC) cereals are experiencing faster growth with a CAGR of 5.75% (2026-2031), as consumers increasingly view hot cereals as more nutritious and filling. Hot oatmeal, in particular, has gained popularity due to its health benefits and adaptability for customization with various toppings.

In the Ready-to-eat (RTE) segment, flakes remain the largest sub-segment, while granola and clusters show higher growth rates due to their wholesome ingredients and texture. Protein enrichment is driving new product development in this category. For example, in November 2024, FUEL10K introduced Multigrain Flakes in Chocolate and Red Berry flavors, featuring high-protein, high-fiber wholegrain wheat flakes. In the RTC segment, premium muesli and specialized porridge mixes are growing faster than basic oatmeal, indicating consumers' willingness to pay more for higher quality and enhanced nutritional benefits.

By Packaging Type: Boxes Dominate While Cups Innovate

Traditional boxes hold a dominant 64.70% market share in 2025, supported by established manufacturing infrastructure and consumer familiarity. Cups and bowls represent the fastest-growing segment with a projected 9.45% CAGR from 2026 to 2031, as they meet the needs of consumers seeking convenience. This format shift enables cereal consumption beyond breakfast, creating new opportunities in the snacking category.

Stand-up pouches are increasing in adoption within premium and natural cereal segments, offering product differentiation and freshness preservation. The "others" category, comprising plastic jars and bags, serves specific market segments but faces limitations in growth due to production costs and environmental concerns. Manufacturers are focusing their packaging development on both functional improvements and environmental responsibility, with substantial investment in research and development of biodegradable and recyclable materials that maintain product protection standards.

By Distribution Channel: Supermarkets Lead While E-commerce Surges

Supermarkets/hypermarkets hold a dominant 54.70% market share in breakfast cereals distribution in 2025, driven by their extensive product assortment and high consumer footfall. The e-commerce channel is experiencing significant growth at 10.85% CAGR (2026-2031), as consumers increasingly purchase breakfast cereals online. According to the Census Bureau of the Department of Commerce, U.S. retail e-commerce sales reached USD 300.2 billion in Q1 2025, adjusted for seasonal variation but not price changes. The digital transition is particularly evident among younger consumers who prefer online platforms for their convenience and ability to compare products and access nutritional information.

Convenience stores and grocery outlets maintain a strong market presence, particularly for immediate consumption needs, while specialty stores cater to premium and health-conscious consumer segments. The other distribution channels, including direct-to-consumer and food service segments, represent an emerging segment as companies explore new distribution methods. This distribution landscape evolution requires manufacturers to develop integrated channel strategies that ensure brand consistency while adapting to specific channel requirements, affecting packaging, pricing, and promotional strategies in the breakfast cereals market.

By Age Group: Adults Dominate While Children's Segment Grows

Adult-oriented cereals hold a 47.60% market share in 2025, reflecting demographic shifts and the category's expansion beyond its traditional children's focus. The children's segment maintains a higher growth trajectory at 5.07% CAGR (2026-2031), driven by manufacturers balancing nutritional value with taste appeal. This growth aligns with reformulation efforts to reduce sugar content while maintaining child-friendly flavors and formats. According to the USDA's 2024 School Breakfast Program report, 80% of weekly grains offered in school meal programs must be whole grain-rich .

The adult segment has developed distinct sub-categories focused on specific health benefits, including heart health, digestive wellness, and weight management. Manufacturers like General Mills are working to increase household penetration by targeting children who influence family purchasing decisions. This approach requires developing products that meet parents' nutritional requirements while satisfying children's taste preferences, presenting manufacturers with formulation and research challenges.

Geography Analysis

North America holds a 36.30% share of the global breakfast cereals market in 2025, supported by high per-capita consumption and extensive retail distribution networks. The region shows moderate growth as manufacturers develop value-added products to address volume challenges in mature segments. Health-oriented innovations, specifically protein-enriched varieties and reduced-sugar formulations, drive market expansion. The FDA's 2024 nutrition labeling requirements have enhanced transparency for added sugars, prompting manufacturers to adapt formulations to meet consumer preferences.

Asia-Pacific demonstrates the highest growth potential with a projected CAGR of 6.10% (2026-2031), supported by urbanization, increasing disposable incomes, and evolving dietary habits. China, India, and Southeast Asian countries show robust growth as urban consumers adopt Western-style breakfast options. International manufacturers are customizing products for local tastes while promoting nutritional benefits, establishing foundations for sustained market expansion.

Europe exhibits distinct regional consumption patterns and product preferences in a mature market environment. Consumers demonstrate high nutritional awareness, favoring organic, whole grain, and reduced-sugar products. The European Food Safety Authority's 2024 nutritional guidelines emphasize whole grain consumption and sugar reduction, affecting consumer choices and product formulations. Private label products maintain a significant market presence, with retailers developing competitive offerings across price segments. Eastern European markets present growth opportunities as rising disposable incomes support increased breakfast cereal consumption.

Competitive Landscape

The global breakfast cereals market operates under a moderately consolidated structure, with five major corporations controlling the industry: General Mills, Post Holdings, Nestlé, PepsiCo, and Marico Ltd. These organizations maintain significant operational infrastructure and distribution networks, necessitating continuous optimization of manufacturing processes while demonstrating responsiveness to evolving consumer preferences and market demands across the breakfast cereals industry.

The competitive landscape is primarily defined by strategic initiatives centered on nutritional enhancement and format diversification. According to Nestlé's 2024 Annual Report, the corporation has implemented comprehensive nutritional improvement programs across its breakfast cereal portfolio, with its Indian subsidiary achieving a 30% reduction in added sugars within the infant cereals category. Additionally, specialized manufacturers operating in high-protein and grain-free segments are demonstrating substantial growth trajectories, despite their limited market presence, thereby compelling established manufacturers to accelerate their product development cycles within the breakfast cereals industry.

The competitive environment is experiencing increased complexity due to the substantial market penetration of private label offerings. This development has intensified the necessity for established manufacturers to emphasize product differentiation and implement strategic brand positioning initiatives. Such measures are essential for maintaining premium price points and ensuring sustained consumer loyalty in an increasingly competitive market environment shaping the breakfast cereals industry.

Breakfast Cereals Industry Leaders

-

General Mills Inc.

-

Post Holdings Inc.

-

Nestlé S.A.

-

PepsiCo Inc.

-

Marico Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kellogg's launched a new cereal in collaboration with Bluey, the leading children's content brand in the United Kingdom. This partnership aligns with Bluey's ongoing expansion of licensing opportunities across markets.

- April 2025: PepsiCo introduced Mighty Life, a multigrain cereal with functional health benefits. The product comes in two varieties: Strawberry Blueberry Bliss, designed to support immune system health, and Very Vanilla, formulated to promote bone strength.

- February 2025: Seven Sundays launched a new cereal line called Little Crispies. The cereal contains sorghum, which provides a texture similar to popped rice and corn. Little Crispies are made with coconut oil and honey, contain no artificial ingredients, and are gluten-free.

- September 2024: Tata Consumer Products introduced Tata Soulfull Masala Muesli in two flavors: 'Mast Masala' and 'Teekha Twist'. This product launch represents an innovation in the breakfast cereal category.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the breakfast cereals market as the value of all ready-to-eat flakes, puffed grains, granola, muesli, and ready-to-cook hot cereals derived from processed wheat, corn, oats, rice, barley, or mixed grains that are sold to retail and food-service channels at manufacturer selling price. These products are typically consumed with milk, yogurt, or as dry snacks.

The sizing deliberately leaves out cereal bars, bakery mixes, and milk flavoring powders, which some publishers blend into 'breakfast foods.'

Segmentation Overview

-

By Product Type

-

Ready-to-Eat Cereals

- Flakes

- Puffed Cereals

- Granola and Clusters

- Others (Coated/Sugar-Frosted Cereals, Shredded and Threaded)

-

Ready-to-Cook Cereals

- Hot Oatmeal

- Muesli and Porridge Mixes

- Other Ready-to-Cook Cereals

-

Ready-to-Eat Cereals

-

By Ingredient Source

- Wheat

- Corn

- Oats

- Rice

- Barley

- Others

-

By Packaging Type

- Boxes

- Stand-Up Pouches

- Cups and Bowls

- Others (plastic jars, and bags, etc.)

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retailers

- Other Distribution Channels

-

By Age Group

- Adults

- Children

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed plant managers of cereal manufacturers, procurement leads at two regional wholesalers, and category buyers at large e-commerce grocers across North America, Europe, and Asia-Pacific. These conversations validated input cost swings, average selling prices, and emerging demand pockets (single-serve cups, protein-fortified SKUs) that raw desk data could not capture.

Desk Research

We began with trade and nutrition statistics from FAOSTAT, USDA Production, UN Comtrade shipment flows, and population diet surveys such as NHANES; these quantified grain supply, import dependence, and per-capita consumption in key regions. In parallel, we extracted company financials and brand splits from D&B Hoovers, plus annual reports and investor decks to benchmark leading players' revenue footprints. Regulatory notices (FDA sodium and sugar thresholds), retail scanner data shared through industry associations, and academic journals on whole-grain fortification trends further shaped baseline assumptions. The sources cited above are illustrative; analysts reviewed many additional open datasets for completeness.

Market-Sizing & Forecasting

A top-down demand pool model converts retail sales and household penetration into 2024 volume, which is then price-adjusted to 2025 dollars; selective bottom-up checks using sampled brand revenues and channel margins fine-tune totals. Key variables include per-capita cereal intake, urban middle-class expansion, retail ASP inflation, grain price indices, and e-commerce share of grocery. Multivariate regression links these drivers to historical growth, while scenario analysis captures sugar-tax adoption and private-label acceleration through 2030. Gaps in brand-level data are bridged with conservative interpolation anchored to publicly reported shipments.

Data Validation & Update Cycle

Outputs pass a two-step peer review, variance checks against external calorie-supply datasets, and a final sign-off by a senior analyst. Reports refresh annually, and we issue interim revisions when raw-grain price shocks or major labeling rules alter the market trajectory.

Why Mordor's Breakfast Cereal Baseline Commands Confidence

Published numbers often diverge because firms mix cereal bars, use retail mark-ups, or freeze assumptions for years. Mordor Intelligence updates inputs yearly and aligns scope with global HS codes for processed cereals, so our baseline tracks the real market that manufacturers serve.

Key gap drivers versus other publishers include differing inclusion of hot oatmeal, choice of retailer versus factory pricing, varying assumptions on online grocery share, and refresh cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 44.21 B | Mordor Intelligence | - |

| USD 42.69 B | Global Consultancy A | Excludes traditional hot cereals and relies on retail mark-ups only for Western markets |

| USD 40.01 B | Trade Journal B | Uses 2024 base year and omits e-commerce and food-service channels |

| USD 48.24 B | Research Firm C | Bundles cereal bars and fortified oats, expanding product scope |

Taken together, the comparison shows that our disciplined scope selection, timely data refresh, and blended top-down/bottom-up validation give decision-makers a balanced, transparent figure that is repeatable and easy to audit.

Key Questions Answered in the Report

What is the current size of the breakfast cereals market?

The breakfast cereals market is valued at USD 46.44 billion in 2026 and is projected to reach USD 59.43 billion by 2031.

Which product type is growing fastest within the breakfast cereals market?

Ready-to-Cook hot cereals are growing at a 5.75% CAGR, surpassing the broader market trajectory.

Why are oat-based cereals gaining momentum?

Oats offer fiber and cholesterol benefits, driving a 6.25% CAGR and helping brands satisfy gluten-free and clean-label demand.

How is online retail affecting breakfast cereals sales?

Digital channels are expanding at an 10.85% CAGR, enabling subscription models and wider SKU discovery beyond shelf limits.

Page last updated on: