Frozen Dough Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

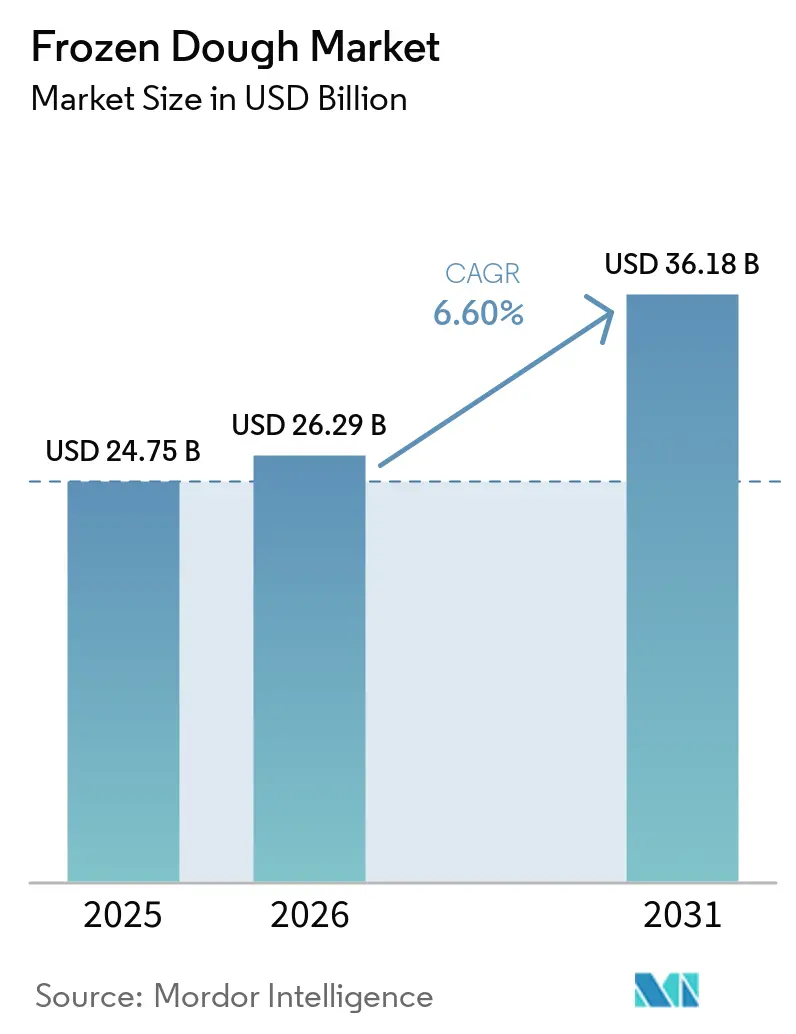

| Market Size (2026) | USD 26.29 Billion |

| Market Size (2031) | USD 36.18 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

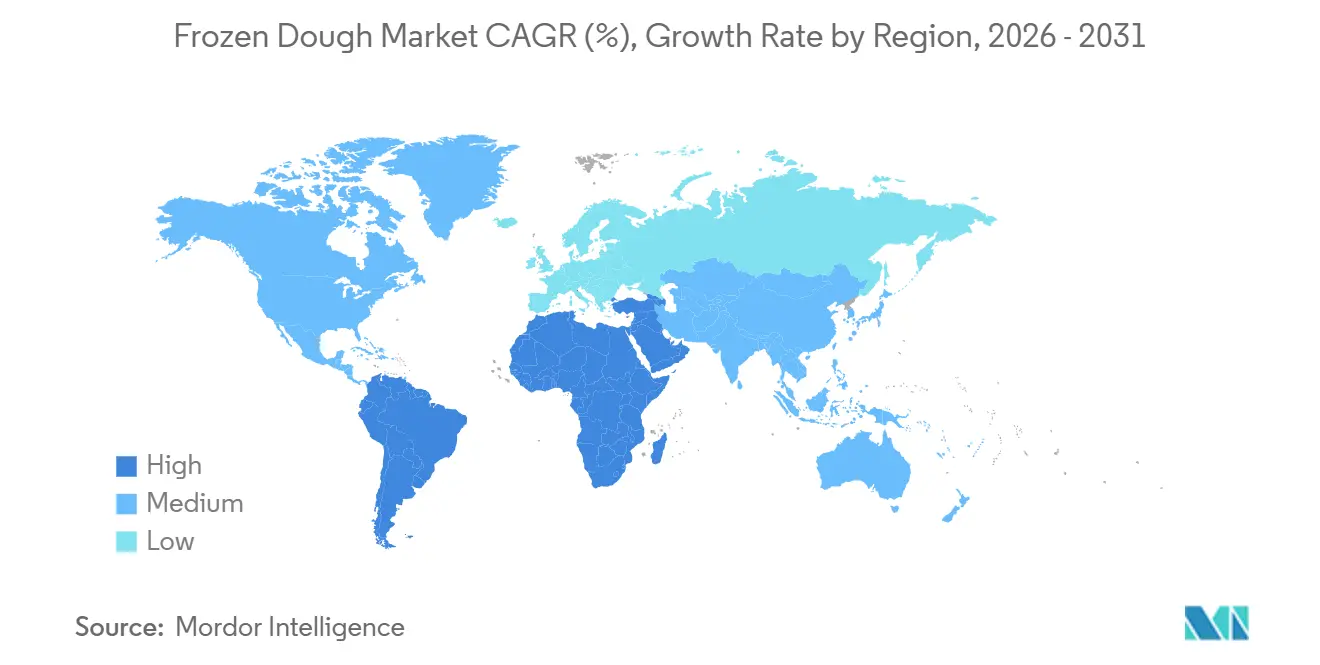

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frozen Dough Market Analysis by Mordor Intelligence

The frozen dough market size is expected to grow from USD 24.75 billion in 2025 to USD 26.29 billion in 2026 and is forecast to reach USD 36.18 billion by 2031 at 6.60% CAGR over 2026-2031. This upward trajectory is driven by a rising appetite for convenient bakery products, an increasing embrace of frozen prebaked ingredients by quick-service restaurants, and technological advancements that extend shelf life without sacrificing taste or texture. Innovations like energy-efficient freezing tunnels, enzyme-based dough conditioners, and adaptable cold-chain systems are enhancing efficiency and reducing waste, charting a robust growth path for the frozen dough market. Regulatory changes, notably the U.S. FDA's ban on partially hydrogenated oils, have led to cleaner product reformulations, aligning the market with health-conscious consumers. Additionally, significant investments in bakery automation are reducing labor costs and meeting the demands of major global foodservice brands. While the market grapples with fluctuating commodity prices and energy-intensive storage challenges, strategic hedging and stringent energy regulations offer a buffer, ensuring margin stability and continued growth potential.

Key Report Takeaways

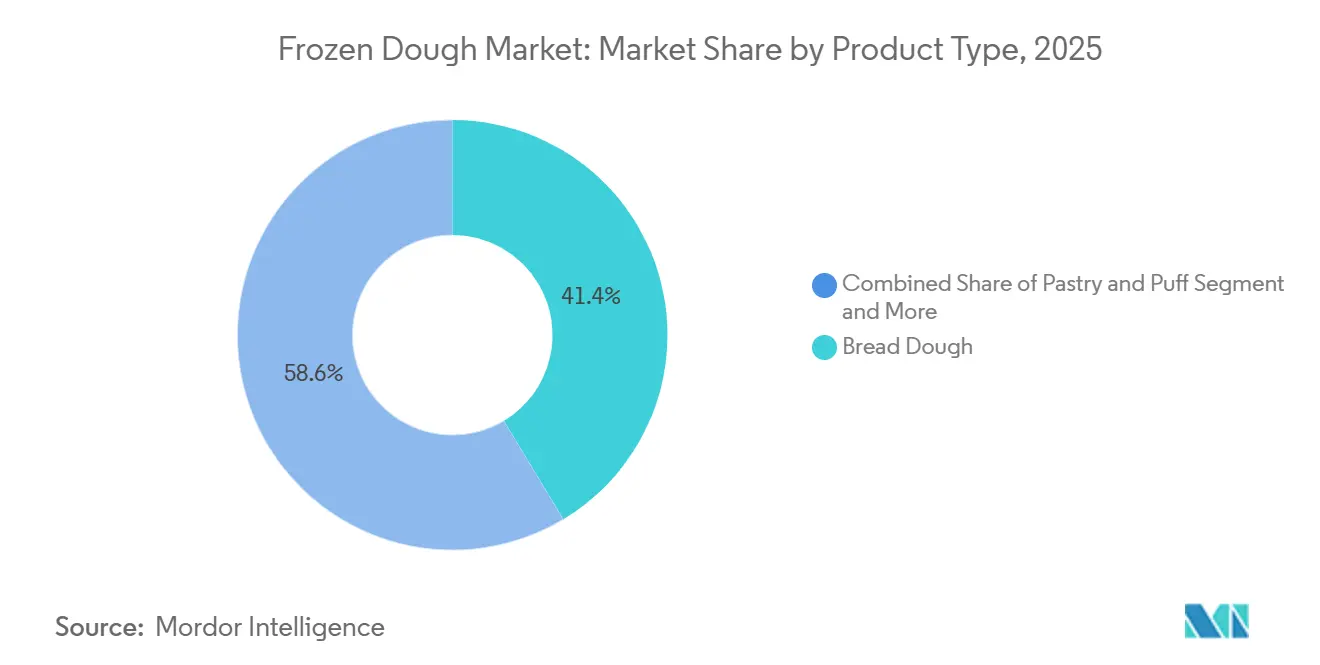

- By product type, bread dough held 41.37% of the frozen dough market share in 2025, and Pastry and Puff dough are projected to expand at a 5.84% CAGR through 2031.

- By dough form, dough balls captured a 36.96% frozen dough market share in 2025, and Pre-shaped dough is forecast to grow at a 6.64% CAGR to 2031.

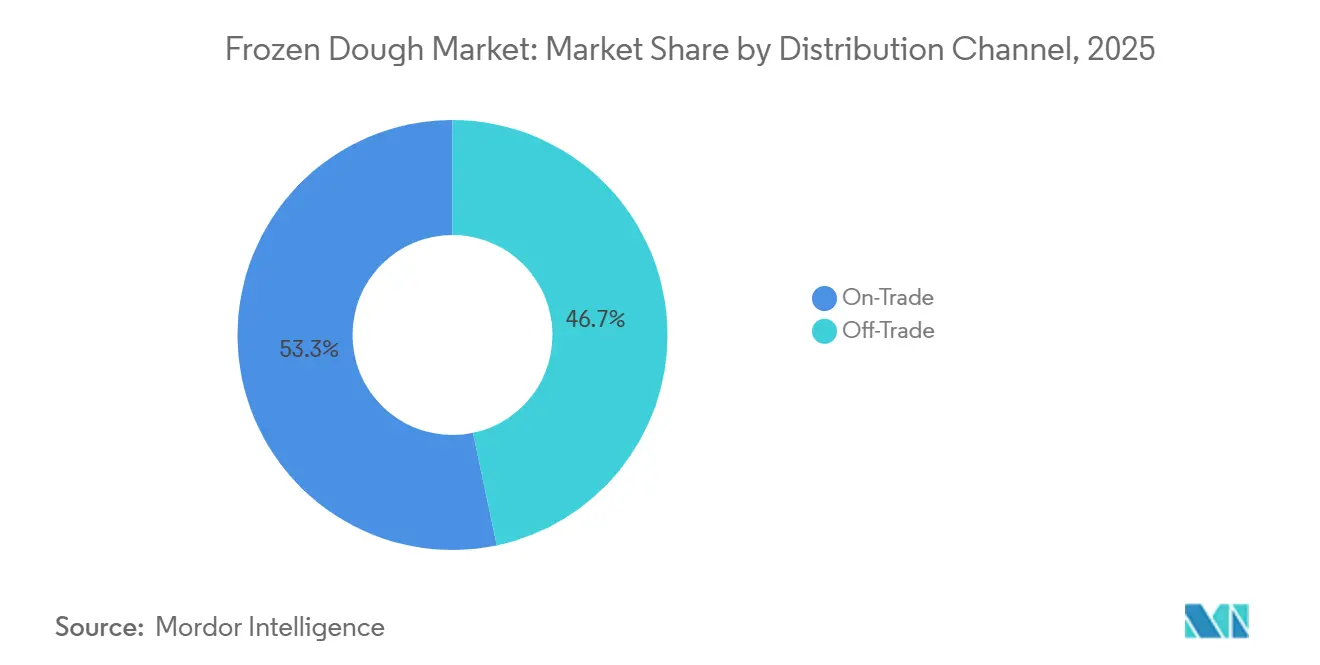

- By distribution channel, on-trade accounted for 53.27% of the frozen dough market size in 2025, and Off-trade is advancing at 9.25% CAGR through 2031.

- By geography, Europe led with a 43.26% share of the frozen dough market in 2025, and Asia-Pacific remains the fastest region, rising at an 8.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Frozen Dough Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label demand in frozen bakery | +1.2% | Global, with stronger emphasis in North America & Europe | Medium term (2-4 years) |

| Mill-level enzyme innovations enabling longer freezer shelf-life | +0.8% | Global, led by developed markets | Long term (≥ 4 years) |

| Expansion of quick-service restaurant chains in emerging economies | +1.1% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Growth of cold-chain logistics infrastructure | +0.9% | Global, with accelerated growth in Asia-Pacific | Long term (≥ 4 years) |

| Bakery automation lowering unit costs | +0.7% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth in Home-baking | +0.6% | Global, with peaks in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Clean-label Demand in Frozen Bakery

Growing consumer insistence on recognizable ingredients is remolding formulations across the frozen dough market. Brands now swap synthetic preservatives for plant-derived antimicrobials such as Kemin Industries Shield V, a clean-label mold inhibitor that preserves freshness without sensory trade-offs [1]Source: Snack Food & Wholesale Bakery, “Kemin Industries Introduces Shield V,” snackandwholesalebakery.com. Regulatory backing in North America and Europe reinforces the trend, incentivizing broader applications of enzyme toolkits that permit the removal of emulsifiers yet keep volume and softness intact. Novozymes Valena and Optiva solutions illustrate how tailored biosystems raise fiber content, curb carbon intensity, and deliver dough stability during protracted frozen storage. As the global clean-label ingredients sector increases, bakers view transparency as a premium lever that commands higher shelf prices and deepens retailer partnerships. The shift supports the long-run competitiveness of the frozen dough market by differentiating products in crowded freezers and sustaining consumer trust.

Mill-level Enzyme Innovations Enabling Longer Freezer Shelf-life

Advanced maltogenic amylases and bacterial enzymes address starch retrogradation, the principal quality loss mechanism during freezing and thawing. RIBUS Nu-BAKE enhancer, harvested from rice bran, offers organic-compliant conditioning that lifts loaf volume and maintains crumb elasticity. The technology taps higher water absorption indices that allow leaner formulas while sustaining machinability, a gain that translates into faster production benches and lower energy draw for mixers. Bakeries leveraging such enzyme classes report extended distribution radii because product freshness benchmarks persist well past typical freezer holding periods. These innovations also mitigate food waste, a rising retailer concern, thereby reinforcing sustainable procurement mandates. Persistent investment in enzyme R&D, therefore, underpins both cost control and environmental targets within the frozen dough market

Expansion of Quick-service Restaurant Chains in Emerging Economies

The rapid growth of multinational QSR franchises in Asia-Pacific is a pivotal force lifting the frozen dough market. Operators such as Krispy Kreme have partnered with McDonald’s USA to supply frozen doughnuts nationwide by 2026, a model now mirrored in high-density urban centers across India, Indonesia, and the Gulf states [2]Source: Krispy Kreme, “McDonald’s USA Partnership Expansion,” krispykreme.com. The standardized nature of frozen inputs ensures menu uniformity, reduces on-site baking skills, and accelerates rollouts, critical in markets where trained bakers remain scarce. Heightened QSR footprint correlates with cold-chain gains, supporting broader frozen bakery penetration. With the majority of foodservice players in the United States already relying on more frozen foods, the template for volume growth appears transferable to developing regions, feeding a virtuous cycle for the frozen dough market.

Growth of Cold-chain Logistics Infrastructure

Temperature-controlled warehousing grew by an extra 2.5 million ft² in 2024, as given by real estate firm CBRE, reflecting record investment inflows as retailers, e-grocers, and foodservice buyers widen frozen assortments. Collaborations such as Canadian Pacific, Kansas City, and Americold enhance Mexico-US corridors, shaving transit times and supporting just-in-time restocking. IoT sensors priced USD 500-2,000 are now common fixtures, pushing real-time quality checks and enabling dynamic routing during traffic or weather disruptions. Research proving that elevating set points from -18 °C to -15 °C cuts energy by over 10% without sensory damage underscores how system optimization can offset electricity inflation while shrinking CO₂ emissions by up to 17.7 million tons annually [3]Source: Food Digital, “Optimizing Cold Storage Temperatures,” fooddigital.com. These logistics strides unlock new towns and smaller formats for the frozen dough market, narrowing fresh-baked parity gaps and fueling incremental volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile wheat & butter prices | -0.8% | Global, with higher sensitivity in cost-conscious markets | Short term (≤ 2 years) |

| Energy-intensive frozen storage costs | -0.6% | Global, with higher impact in regions with expensive energy | Long term (≥ 4 years) |

| High initial investment for production and freezing technology | -0.5% | Emerging markets and small-to-medium enterprises globally | Medium term (2-4 years) |

| Tightening trans-fat regulations for laminated doughs | -0.4% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Wheat and Butter Prices

Average wheat quotes reached USD 6.69 per bushel in 2024, moving above the USD 5.85 multi-year mean and magnifying cost exposure for dough lines where raw commodities form up to half the bill of materials, as given by the United States Department of Agriculture (USDA). Butter tracks similar peaks due to tight milk supplies, further squeezing producers that lack robust hedging programs. Despite a 2% lift in winter wheat acreage for the 2025 harvest, as given by the United States Department of Agriculture (USDA), weather variability and geopolitical trade shifts render forward curves unstable, complicating procurement budgets. Retail pass-through remains limited as competitive freezer aisles restrain price elasticity. The Bureau of Labor Statistics notes bakery shelf prices jumped 10.5% between May 2022 and December 2023, illustrating how layered cost elements stretch consumer tolerance even when grain futures soften. Elevated ingredient volatility thus curbs margin recovery and tempers near-term output from the frozen dough market.

Energy-intensive Frozen Storage Costs

Refrigeration systems consume 20-30% of end-to-end operating outlays inside the frozen dough industry, challenging profitability in regions with rising power tariffs. Upcoming United States efficiency rules for walk-in coolers and freezers take effect in December 2027 and will require capital retrofits but promise a leaner kilowatt draw once installed. Maintenance accounts for another 10-15% of cold-store budgets, while insurance premiums cost annually per facility, additionally reflecting higher risk profiles relative to dry storage. Operators are trialing automated racking and AI dispatch to smooth peak loads; early adopters report double-digit reductions in kilowatt-hour consumption. However, the payback window can extend beyond five years, deterring smaller players from immediate upgrades. These realities keep cost pressure on the frozen dough market, especially in export-oriented plants that hold inventory for extended periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bread Dough Dominance Faces Specialty Challenge

In 2025, bread dough commands a dominant 41.37% share of the market, underscoring its pivotal role from QSR sandwich buns to artisanal loaves. Its supremacy is attributed to its versatility and the standardization benefits it offers, allowing foodservice operators to achieve consistency while minimizing labor and skill dependencies. Traditional applications of bread dough are transforming to enzyme technologies and clean-label reformulations. The segment's stability is bolstered by the expansion of QSRs in emerging markets, where standardized bread products uphold brand consistency across varied environments. In response to competitive pressures, manufacturers are channeling investments into automation and enzyme innovations, aiming to extend shelf life while retaining the operational benefits that make bread dough a favorite for high-volume applications.

The pastry and puff dough segment is the fastest growing within the frozen dough market, driven by surging demand for convenience foods and premium baked products. From 2026 to 2031, this segment is expected to achieve a robust CAGR of 5.84%. Its rapid expansion is attributed to several trends: more consumers are seeking easy-to-prepare solutions for both home and foodservice use, a burgeoning interest in specialty and gourmet baked goods, and cultural influences fueling experimentation with diverse pastries. The popularity of products like croissants, Danish pastries, and tarts, together with increased offerings from retailers and QSRs, are accelerating the adoption and growth of pastry & puff dough worldwide.

By Dough Form: Dough Balls Lead While Pre-Shaped Innovation Accelerates

Dough balls retained 36.96% of the frozen dough market in 2025 as their blank-canvas character suits diverse shaping, stretching, and topping routines. Operators gain portion accuracy and menu flexibility, essential when SKU counts expand to meet localized taste trends. It offers significant convenience and versatility to commercial bakeries, foodservice outlets, and even home bakers, enabling easy handling, reduced preparation time, and consistent product output. Their portion-controlled size appeals to foodservice operators for quick preparation and standardized serving, making them an essential product of the frozen dough market.

Pre-shaped dough, although smaller in share, is on a 6.64% CAGR ascent through 2031 as automated lines like FRITSCH MULTIFLEX M 700 cut and position up to 20 strokes per minute with minimal manual oversight. This capability reduces training hours and mitigates skilled labor shortages, a chronic issue in busy commissaries. Continuous mixers, smooth rheology, shrinking batch variability, and enabling longer production windows. Enhanced freezing curves preserve yeast vitality in complex shapes that historically suffered from blow-outs or crust deficits. With these gains, pre-shaped croissants, bagels, and braided loaves unlock new profit pools, particularly in high-volume breakfast chains. Laminated variants, part of the wider “others” group, command premium margins but face formula scrutiny as regulators restrict partially hydrogenated oils. Bakeries integrating enzyme emulsification and specialty fats aim to replicate traditional flake without banned lipids, an R&D race poised to add upwards to the frozen dough market.

By Distribution Channel: On-Trade Strength Meets Off-Trade Digital Transformation

On-trade buyers, including QSRs, cafés, and institutional caterers, controlled 53.27% of the frozen dough market in 2025, favoring volume contracts, vendor-managed inventory, and exacting consistency guidelines. Foodservice operators are drawn to frozen dough for its consistent quality, convenience, and labor-saving benefits. These products allow outlets to quickly prepare a range of fresh, high-quality baked goods. Chain expansion in emerging economies keeps this channel dominant, with dough prepared at central plants and shipped frozen to satellite outlets, thereby ensuring uniformity and simplifying training. Institutional dining, spanning hospitals and universities, supplements baseline demand due to standardized menus and outsourced service models.

Yet the 9.25% CAGR surge in off-trade through 2031 signals a structural pivot toward retail and direct-to-consumer. Supermarkets elevate freezer planograms, employing vertical glass doors that improve product visibility and cut energy loss. Convenience stores widen ready-to-eat offerings, banking on commuter snacking. E-commerce lifts the frozen dough market by pairing insulated shippers with dense last-mile networks that shorten transit and uphold temperature integrity. Consumers, acquainted with grocery apps since pandemic lockdowns, display rising willingness to order frozen staples online when savings or limited-edition flavors appear. Hybrid models blur channel lines: restaurant brands retail frozen versions of in-store hits, capturing incremental revenue while protecting brand equity. This duality ensures balanced growth across trade verticals, shielding the frozen dough market from channel-specific downturns.

Geography Analysis

Europe sustained a 43.26% share of the frozen dough market in 2025, an outcome of entrenched bread culture, pervasive cold-store grids, and regulations that favor artisanal authenticity alongside industrial efficiency. Germany and France feature dense bakery footprints, while the United Kingdom registers high per-capita spending on convenience bakery. Capacity additions such as Freiberger’s new UK pizza facility echo steady retail appetite and export prospects across the continent. Clean-label fervor, organic certification, and lower-salt mandates further characterize European policy frameworks, compelling manufacturers to invest in reformulations that maintain shelf life without controversial additives. These conditions support premium pricing and create defensible niches within the frozen dough market.

Asia-Pacific, the fastest region with an 8.31% CAGR to 2031, rides on urbanization, expanding middle classes, and QSR diffusion. China anchors volume with sprawling city clusters that prize convenience and Western-style snacks, while India’s bakery spending rises as dual-income households seek ready-to-bake breads. Deployment of new cold depots across Indonesia, Vietnam, and the Philippines shortens delivery loops, curbing thaw spoilage and supporting broader SKU offerings. Nissin Foods’ AUD 33.7 million purchase of ABC Pastry in Australia signals commitment to capture migrant-led demand for Asian dough formats.

North America remains a mature but technologically advanced arena where automation, AI scheduling, and predictive maintenance hold sway. United States bakeries plan AI rollouts within 12 months, targeting waste cuts and tighter process control. Canadian operations benefit from bilateral trade and shared food safety codes, easing cross-border flows. Mexico gains stature as a near-shore production hub, aided by the Canadian Pacific Kansas City and Americold alliance that augments refrigerated infrastructure along the corridor. Though growth rates trail emerging territories, the region’s high per-capita volume and innovation leadership render it indispensable to suppliers refining formulation science and efficiency benchmarks for global export. The Middle East and Africa market also benefits from economic development, infrastructure advances, and a trend toward clean-label, organic, and premium frozen dough offerings, particularly in urban centers such as the UAE and South Africa. Government initiatives like Dubai’s 2040 Urban Master Plan are further shaping market demand toward healthier, more sustainable products.

Competitive Landscape

The frozen dough market exhibits moderate fragmentation, and a cluster of multinational and regional competitors is locked in process innovation and niche flavor battles. Industrial leaders pursue vertical integration, securing wheat mill inputs, enzyme labs, and dedicated cold fleets to insulate cost structures and command service premiums. Automation sits at the core of strategic differentiation: Reading Bakery Systems' DoughBot processes up to 4,000 lb per hour, letting bakeries offset wage inflation that can account for 25% of cold-chain payrolls.

Enzyme partnerships with biotech firms accelerate clean-label transitions, giving first movers a marketing edge in regulated markets that penalize synthetic emulsifiers. Consolidation under private-equity stewardship accelerates scale ambitions. The September 2024 acquisition of Rise Baking Company by Platinum Equity and Butterfly underscores investor appetite for roll-up plays in high cash-conversion cycles. Vandemoortele’s majority stake in Banneton Bakery supplies a first U.S. production foothold for the European group, aligning continental logistics and recipe R&D.

Specialty newcomers focus on gluten-free and organic corridors, selling direct online to skirt slotting fees, yet the capital intensity of frozen distribution tempers rapid share gains. FDA Food Safety Modernization Act updates tighten hazard analysis, elevating compliance hurdles that favor well-capitalized incumbents. Altogether, technological muscle, portfolio breadth, and regulatory readiness define the competitive chessboard, with room for targeted acquisitions to consolidate fragmented segments and lift the overall frozen dough market value.

Frozen Dough Industry Leaders

Aryzta AG

Lantmännen Unibake

Europastry

Cérélia Group

General Mills, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Doughlicious®, the British-born cult-favorite cookie dough brand, renowned for its artisanal frozen gelato bites and its penchant for pushing the boundaries of novelty snacks, has made a bold move with the launch of its latest offering: Cookies & Cream.

- October 2024: General Mills Foodservice has unveiled its Pillsbury frozen bread dough line, aiming to simplify high-quality bread baking for bakeries. This new Pillsbury range enables in-store bakeries to efficiently produce fresh bread, even with limited time and resources, and without the need for specialized labor. Designed for versatility, these easy-prep products can seamlessly fit into various back-of-house operations, eliminating the necessity of a proof box. Notably, some items come pre-scored or pre-stamped for added convenience.

- August 2023: Entenmann's, the iconic baked goods brand, has launched its latest offering: Refrigerated Ready-To-Bake Cookie Dough. Gracing the shelves of Albertson's stores nationwide, it is curated with the same beloved flavors.

Global Frozen Dough Market Report Scope

The Frozen Dough Market Report is Segmented by Product Type (Bread Dough, Pizza Crust Dough, Pastry and Puff Dough, Cookie and Sweet Dough, Others), Dough Form (Dough Balls, Sheeted Dough, Pre-Shaped Dough, Others), Distribution Channel (On-Trade, Off-Trade), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Bread Dough |

| Pizza Crust Dough |

| Pastry and Puff Dough |

| Cookie and Sweet Dough |

| Others |

| Dough balls |

| Sheeted Dough |

| Pre-Shaped Dough |

| Others |

| On-trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retailer | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Russia | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Columbia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Iran | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bread Dough | |

| Pizza Crust Dough | ||

| Pastry and Puff Dough | ||

| Cookie and Sweet Dough | ||

| Others | ||

| By Dough Form | Dough balls | |

| Sheeted Dough | ||

| Pre-Shaped Dough | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retailer | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Columbia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Iran | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current frozen dough market size and projected growth?

The frozen dough market size is USD 24.75 billion in 2025 and is projected to reach USD 36.18 billion by 2031, representing a 6.60% CAGR

Which product type leads the frozen dough market?

Bread dough leads with 41.37% share in 2025, supported by its versatility across QSR and retail bakery channels.

Which region shows the fastest growth in the frozen dough market?

Asia-Pacific registers the fastest growth, advancing at an 8.31% CAGR through 2031 due to rapid QSR expansion and upgrading cold-chain logistics.

What role does automation play in the frozen dough industry?

Systems like Reading Bakery DoughBot and Fritsch Multiplex lower labor costs, boost throughput, and ensure consistent quality, giving automated plants a competitive edge.

Page last updated on: