Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 102.36 Billion |

| Market Size (2031) | USD 125.38 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

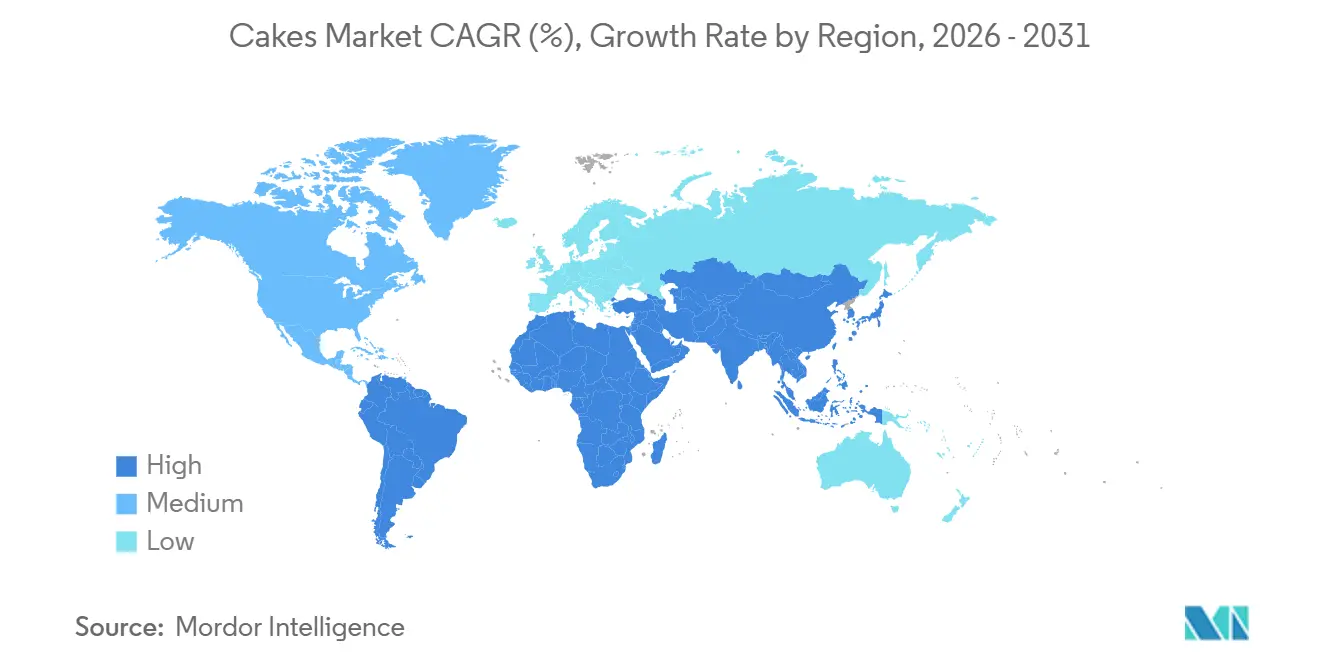

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

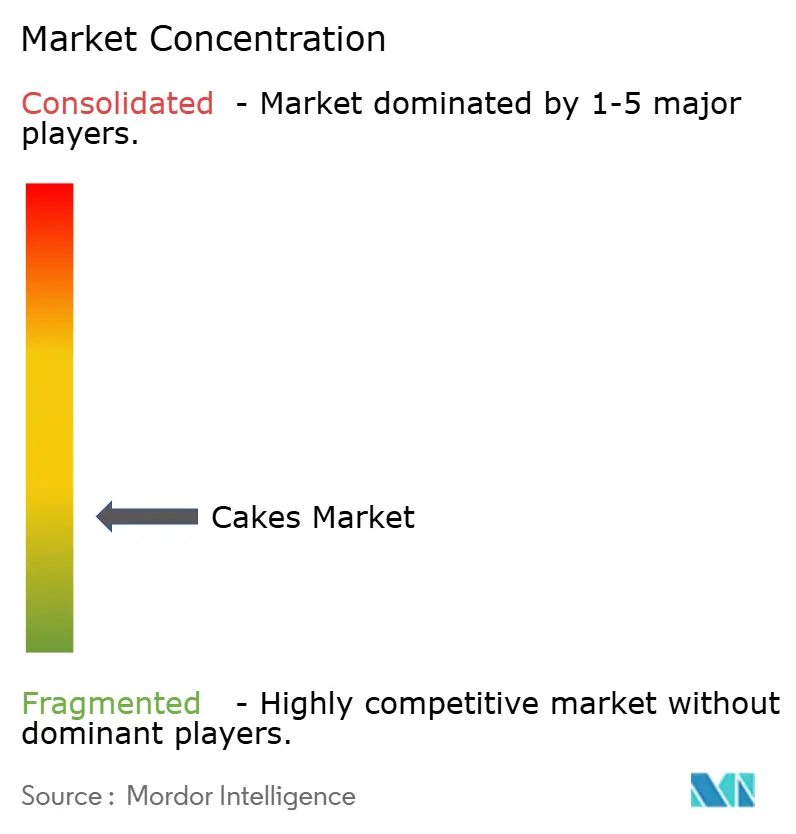

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cakes Market Analysis by Mordor Intelligence

The cakes market was valued at USD 98.31 billion in 2025 and is projected to grow from USD 102.36 billion in 2026 to USD 125.38 billion by 2031, registering a CAGR of 4.14% during the forecast period (2026-2031). This growth reflects a steady and structurally supported trajectory. The market's expansion is driven by the dual role of cakes as everyday indulgences and essential celebratory items, alongside shifting consumption patterns that emphasize convenience, portion-controlled formats, and premium experiences. Cakes maintain strong emotional and cultural significance, with demand rooted in celebrations, gifting occasions, and social gatherings, while also gaining traction in routine snacking and dessert consumption. Additionally, growth is supported by increasing consumer preferences for customization, visual appeal, and experiential eating, where cakes are appreciated not only for their taste but also for their presentation and personalization.

Key Report Takeways

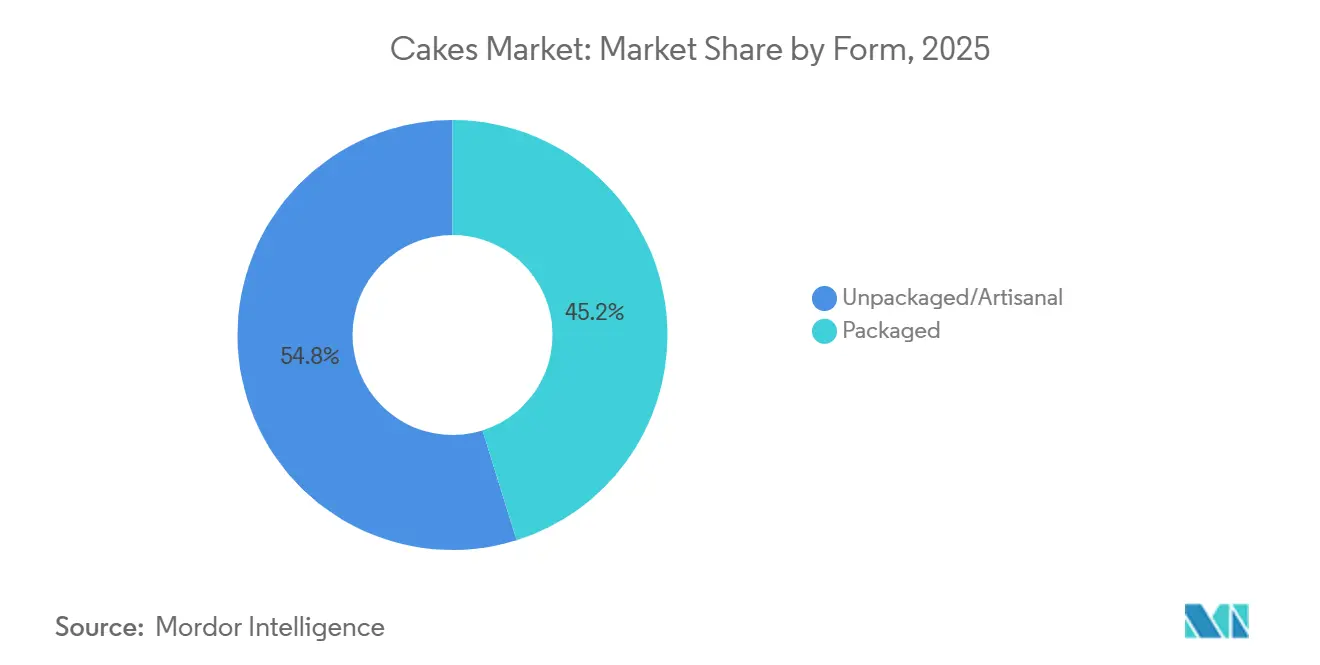

- By form, unpackaged/artisanal formats captured 54.83% revenue share of the cakes market in 2025, while packaged variants are on track for a 4.82% CAGR to 2031.

- By product type, celebration cakes led with 36.11% of cakes market share in 2025; cupcakes are forecast to accelerate at a 4.63% CAGR through 2031.

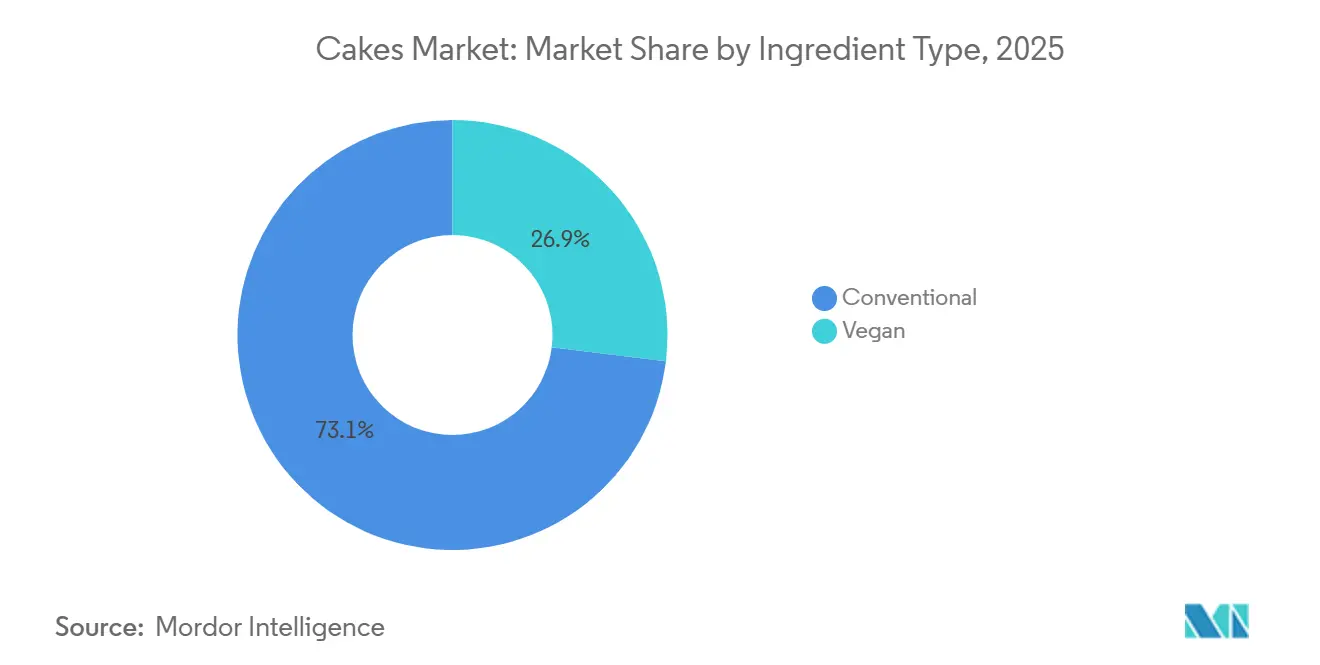

- By ingredient type, conventional recipes commanded a 73.06% share of the cake market size in 2025, but vegan formulations are advancing at a 5.45% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 42.76% distribution share in 2025; online retail is expanding at a 6.58% CAGR on the strength of cold-chain e-commerce investments.

- By geography, Asia-Pacific accounted for 33.87% of global revenue in 2025, while South America is projected to log the fastest 5.91% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cakes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for free-from cakes | +0.7% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Innovation in product flavors and varieties | +0.6% | Global, with early adoption in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Impact of celebrations and festive demand | +0.9% | Global, with peaks in South America, Middle East, and India | Long term (≥ 4 years) |

| Influence of social media and visual food culture | +0.8% | Global, with highest intensity in North America, Europe, and urban Asia | Short term (≤ 2 years) |

| Advancements in baking technology and ingredients | +0.5% | North America, Europe, and large-scale producers in Asia-Pacific | Medium term (2-4 years) |

| Expansion of artisanal and premium cake offerings | +0.6% | North America, Europe, Middle East, and affluent urban centers globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer preference for free-from cakes

The increasing consumer preference for free-from cakes, such as gluten-free, dairy-free, egg-free, nut-free, and allergen-reduced options, is becoming a key driver of growth in the global cakes market. This trend is largely influenced by greater awareness of food allergies, intolerances, and digestive sensitivities, as well as a broader shift toward mindful and inclusive eating habits. Consumers are seeking desserts that enable participation in celebrations and everyday indulgence without compromising dietary requirements, positioning free-from cakes as a mainstream alternative rather than a niche offering. Retailers and bakeries are responding by expanding their dedicated free-from product ranges, focusing on cross-contamination control and clear labeling to build consumer trust and encourage repeat purchases. Additionally, the appeal of free-from products now extends beyond individuals with medical dietary needs to include flexitarians and health-conscious consumers who perceive these products as cleaner and easier to digest.

Innovation in product flavors and varieties

Innovation in product flavors and varieties continues to be a critical growth driver in the global cakes market, as consumers increasingly demand unique, indulgent, and differentiated dessert experiences that go beyond traditional offerings. Persistent experimentation with flavors, textures, fillings, and hybrid concepts not only sustains consumer interest but also fosters repeat purchases and drives premiumization across both artisanal and packaged segments. Brands are actively merging categories by integrating cakes with ice cream, cookies, and other desserts to develop multi-sensory products that align with evolving indulgence trends and the culture of social sharing. This emphasis on innovation was exemplified in August 2025, when Baskin-Robbins launched Cake in a Box, a new range of indulgent, layered ice cream cakes featuring flavors such as cookie dough and cookie crave. The launch highlights how creative flavor development and format reinvention can rejuvenate demand, appeal to younger consumers, and expand consumption occasions beyond traditional celebrations.

Impact of celebrations and festive demand

The demand for cakes during celebrations and festive occasions remains a key driver of the global cakes market. Cakes continue to hold significance as symbolic centerpieces for emotional, social, and cultural events. Occasions such as birthdays, weddings, anniversaries, seasonal festivals, and themed celebrations consistently drive the demand for premium, visually appealing, and limited-edition cake products. Consumers are increasingly open to experimenting with themed flavors, decorative designs, and indulgent recipes during festive periods, leading to higher purchase frequency and premium pricing. This trend is further supported by brands utilizing seasonal storytelling and exclusivity to create urgency and differentiation. For example, in January 2025, Nothing Bundt Cakes introduced three limited-time cakes for Valentine’s season, such as Biscoff Cookie Butter Cake, Marble Cake with Chocolate Frosting, and Chocolate Raspberry Heart made with Dove. Such time-sensitive launches demonstrate how brands effectively align flavors and formats with celebration-driven consumption and emotional gifting moments.

Influence of social media and visual food culture

The increasing influence of social media and visual food culture is a significant driver of the global cakes market. Visually appealing desserts are shaping consumer discovery, preferences, and purchasing behavior. Image-focused and short-form video platforms are boosting demand for aesthetically striking cakes, such as themed celebration cakes, drip cakes, custom designs, and limited-edition offerings, by transforming them into shareable social experiences rather than just food items. Social media exposure accelerates trend cycles, allowing flavors, decorations, and formats to gain rapid popularity while encouraging impulse purchases driven by visual appeal and peer influence. This trend is particularly pronounced in digitally active markets. For example, according to World Population Review, as of October 2025, India had the largest Facebook audience globally, with over 581.6 million users [1]Source: World Population Review, "Facebook Users by Country 2025", worldpopulationreview.com. Such extensive social media penetration significantly increases the visibility of cake trends, bakery brands, and customized creations, effectively converting online engagement into both offline and online sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulatory scrutiny on sugar and additives | -0.4% | Global, with strictest enforcement in Europe, North America, and select Latin American countries | Medium term (2-4 years) |

| Allergen-related constraints | -0.3% | Global, with highest impact in North America and Europe due to stringent labeling laws | Short term (≤ 2 years) |

| Strong competition from alternative desserts | -0.5% | North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Short shelf life and high spoilage risk | -0.4% | Emerging markets in Asia-Pacific, Africa, and Latin America with less developed cold chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing regulatory scrutiny on sugar and additives

Increasing regulatory scrutiny on sugar content and food additives serves as a significant restraint on the global cakes market. Cakes are often classified as indulgent products with high sugar and refined ingredient profiles. Governments and food safety authorities in various regions are implementing stricter regulations concerning sugar reduction targets, front-of-pack labeling, and the allowable use of artificial colors, flavors, and preservatives. These regulations require manufacturers and bakeries to reformulate traditional cake recipes, which poses technical challenges due to sugar's essential role in providing sweetness, texture, browning, moisture retention, and shelf life. Reducing or replacing sugar and synthetic additives often necessitates the use of alternative sweeteners, functional fibers, or natural stabilizers, increasing formulation complexity and potentially affecting taste consistency. Furthermore, stricter labeling and compliance requirements impose additional operational challenges, particularly for smaller bakeries and artisanal producers with limited regulatory expertise.

Allergen-related constraints

Allergen-related constraints are a major challenge for the global cakes market, as traditional cake recipes frequently include common allergens such as gluten (wheat), eggs, dairy, and nuts. With rising awareness of food allergies and intolerances, there has been a significant increase in stricter labeling requirements, enhanced cross-contamination controls, and heightened consumer scrutiny. These developments have introduced substantial operational complexities for both large manufacturers and small bakeries. To effectively manage allergen segregation, businesses are often required to set up dedicated production lines, maintain specialized storage facilities, and implement rigorous cleaning protocols. These necessary measures not only lead to higher operational costs but also limit scalability, particularly for artisanal and in-store bakery operations, making it challenging to meet growing consumer demand while ensuring compliance with safety standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Packaged Variants Gain Ground

Unpackaged and artisanal cakes accounted for 54.83% of the global cakes market share in 2025, highlighting their strong position driven by shifting consumer preferences toward freshness, authenticity, and experiential consumption. This segment benefits from the growing demand for freshly prepared, bakery-made cakes that prioritize taste, texture, and visual appeal over extended shelf life. Consumers increasingly associate these cakes with superior quality, natural ingredients, and minimal use of preservatives, aligning with clean-label expectations and transparency in food preparation. Additionally, artisanal bakeries' ability to provide high levels of customization, including personalized designs, unique flavor combinations, dietary adaptations, and occasion-specific themes, further drives demand and encourages repeat purchases. The growing popularity of local and regional bakeries, which often emphasize traditional recipes and handcrafted techniques, also contributes to the segment's appeal.

Packaged cakes are expected to grow at a compound annual growth rate (CAGR) of 4.82% through 2031, reflecting their rising importance in convenience-oriented consumption patterns. This segment is fueled by increasing demand for ready-to-eat, portable, and portion-controlled dessert options that cater to busy lifestyles and on-the-go eating occasions. Packaged cakes offer consistent quality, extended shelf life, and ease of storage, making them suitable for everyday consumption beyond special occasions. Innovations in packaging technologies, such as moisture-retention materials and modified-atmosphere solutions, are enhancing freshness perception while enabling broader distribution reach. Additionally, the introduction of healthier packaged cake options, including low-sugar, gluten-free, and fortified variants, is expanding the consumer base and addressing evolving dietary preferences.

By Product Type: Celebration Cakes Lead, Cupcakes Accelerate

Celebration cakes accounted for 36.11% of the global cakes market share in 2025, highlighting their importance in social, cultural, and emotional consumption occasions. This segment is primarily driven by the enduring role of cakes in life events and celebrations, where they serve as a symbolic centerpiece. Consumer demand is further bolstered by a growing preference for premium, visually appealing, and highly customized cakes, including themed designs, personalized messages, photo cakes, and multi-tier creations, which enhance the experiential value of celebrations. Additionally, innovation in flavors, fillings, textures, and decorative techniques allows bakeries to continually update their offerings and cater to diverse taste preferences. The increasing popularity of artisanal craftsmanship, handcrafted decorations, and premium ingredients further enhances the perceived value of celebration cakes, encouraging higher spending per occasion.

Cupcakes are projected to grow at a compound annual growth rate (CAGR) of 4.63% through 2031, driven by shifting eating behaviors and a rising preference for snacking and smaller, portion-controlled indulgences. This growth aligns with evolving consumption patterns, where traditional meal structures are increasingly being replaced by flexible eating occasions. For example, according to the International Food Information Council (IFIC) in 2024, 56% of Americans reported replacing traditional meals with snacking or smaller meals, indicating a structural shift toward convenient, bite-sized food formats [2]. Cupcakes align well with this trend due to their single-serve nature, ease of consumption, and lower commitment compared to full-sized cakes, making them suitable for everyday indulgence rather than being limited to celebratory occasions.

By Ingredient Type: Vegan Surge Reshapes Formulations

Conventional ingredient formulations accounted for a 73.06% share of the global cakes market in 2025, underscoring their continued dominance due to established consumer familiarity, sensory reliability, and manufacturing consistency. This segment is primarily driven by the widespread use of traditional ingredients such as refined wheat flour, sugar, eggs, dairy, and conventional fats. These ingredients collectively deliver the classic taste, texture, volume, and mouthfeel that consumers widely associate with cakes. Both artisanal bakers and large-scale manufacturers favor conventional formulations for their predictable performance during mixing, baking, and decoration, ensuring uniform quality across batches. Furthermore, these formulations offer greater flexibility in flavor innovation, structural stability for layered and decorated cakes, and compatibility with a wide range of fillings, frostings, and toppings.

Vegan ingredient alternatives are growing at a compound annual growth rate (CAGR) of 5.45% through 2031, reflecting a significant shift toward plant-based, dairy-free, and egg-free cake formulations in both artisanal and packaged formats. This growth is driven by increasing consumer interest in plant-forward diets, ethical and environmental considerations, and heightened awareness of food intolerances related to eggs and dairy. The segment also benefits from its alignment with other fast-growing claims, including lactose-free, cholesterol-free, and allergen-conscious positioning, which broadens its appeal beyond strictly vegan consumers. Additionally, bakeries and manufacturers are actively expanding their vegan product portfolios to attract younger, urban, and health-conscious demographics while maintaining indulgent flavor profiles. For example, in September 2024, vegan brand OGGS launched its Cruelty-Free Lemon Loaf Cake in Tesco stores and on Ocado in the United Kingdom.

By Distribution Channel: Online Retail Outpaces Traditional Formats

Supermarkets and hypermarkets accounted for 42.76% of global cake distribution in 2025, maintaining their position as the leading sales channel in the market. This dominance is attributed to their ability to provide high product visibility, a wide assortment, and the convenience of one-stop shopping. These retailers offer packaged cakes, fresh in-store bakery products, and premium celebration cakes under one roof. Large-format stores benefit from dedicated bakery sections, in-store baking facilities, and customized cake counters, effectively combining artisanal freshness with large-scale accessibility. Additionally, the availability of strong private-label offerings alongside established branded products enhances consumer choice across various price points, flavors, and dietary preferences. Supermarkets and hypermarkets also drive impulse purchases by strategically positioning cakes in high-traffic areas such as bakery aisles, end caps, and festive displays.

Online retail stores are projected to grow at a compound annual growth rate (CAGR) of 6.58% through 2031, making them the fastest-growing distribution channel in the global cakes market. This growth is fueled by increasing consumer demand for convenience, time efficiency, and seamless ordering, particularly for both everyday indulgences and occasion-based cake purchases. Online platforms allow consumers to explore extensive product assortments, compare flavors, designs, and dietary attributes, and place orders for customized or pre-designed cakes with ease. The expansion of same-day and next-day delivery services, supported by advancements in cold-chain and last-mile logistics, has significantly improved the feasibility of delivering fresh and premium cakes without compromising quality. Furthermore, digital channels enable large-scale personalization, allowing customers to add custom messages, select portion sizes, and choose options such as vegan, eggless, or reduced-sugar cakes directly through user-friendly interfaces.

Geography Analysis

In 2025, Asia-Pacific accounted for 33.87% of cakes market revenue, establishing itself as the leading regional market. This dominance is attributed to rapid urbanization, changing lifestyles, and the increasing popularity of Western-style bakery products in countries such as China, India, Japan, and Southeast Asia. Urbanization has significantly influenced food consumption patterns, driving demand for convenient, premium, and celebration-oriented baked goods. For example, the National Bureau of Statistics of China reported that approximately 67% of China’s population resided in urban areas in 2024, enhancing access to modern retail formats, in-store bakeries, and online food delivery platforms [3]Source: National Bureau of Statistics of China, "Degree of urbanization in China", stats.gov.cn. Additionally, the cultural integration of cakes into birthdays, festivals, and social gatherings, coupled with exposure to global flavors, artisanal formats, and customized celebration cakes, supports sustained growth in both volume and value.

South America is projected to grow at a CAGR of 5.91% through 2031, making it the fastest-growing regional market globally. This growth is driven by the cultural significance of cakes in festive occasions, family celebrations, and social events, where cakes play a central role. The increasing availability of packaged cakes for everyday snacking, along with the rising demand for premium and decorated cakes for celebrations, is broadening consumption beyond traditional bakery channels. Innovations in flavors tailored to regional preferences, smaller portion sizes, and enhanced retail and distribution infrastructure are further accelerating market growth across key South American countries.

North America and Europe represent mature cake markets, supported by well-established bakery traditions, the widespread availability of both packaged and artisanal products, and ongoing innovation in premium, clean-label, and indulgent offerings. These regions maintain consistent demand for cakes, driven by both everyday consumption and celebration-related purchases. In contrast, the Middle East and Africa, while holding smaller market shares, demonstrate significant growth potential. Key factors driving growth in these regions include urban expansion, a young consumer demographic, increased exposure to Western bakery formats, and rising demand for premium and customized cakes in urban areas. These regional trends highlight a global market characterized by stability and scale in mature regions, alongside long-term growth opportunities in emerging markets.

Competitive Landscape

The cakes market is moderately fragmented, featuring a mix of large multinational manufacturers, regional bakery chains, and numerous local and artisanal players. Prominent multinational companies like Grupo Bimbo, Flowers Foods, and Mondelēz International compete based on brand strength, extensive distribution networks, standardized quality, and diverse product portfolios that range from everyday packaged cakes to premium snack options. These companies benefit from economies of scale, strong retail partnerships, and the ability to sustain high-volume production across multiple regions.

White-space opportunities are increasingly evident in vegan, allergen-free, and clean-label cake segments. Incumbent manufacturers often face challenges in reformulating products to maintain taste consistency, texture, and shelf stability at scale. In contrast, smaller, specialized brands are well-positioned to address these gaps by offering differentiated, premium-priced products that cater to evolving dietary preferences and ethical considerations. Additionally, online-first and cloud bakery models are gaining momentum by bypassing traditional retail costs, enabling direct-to-consumer engagement, faster product development cycles, and data-driven personalization. These digitally native players utilize consumer insights to customize flavors, portion sizes, and other options, thereby intensifying competition for both packaged cake manufacturers and brick-and-mortar bakeries.

Technology adoption is transforming competitive dynamics within the cakes market. Large-scale manufacturers are investing significantly in automation, advanced baking equipment, and packaging innovations to enhance operational efficiency, product consistency, and shelf life. Automation facilitates higher production throughput and cost control, while advancements in moisture retention, modified-atmosphere packaging, and ingredient functionality improve the quality of packaged cakes. Additionally, digital tools such as demand forecasting, inventory optimization, and e-commerce integration are becoming critical for maintaining a competitive edge in the market.

Cakes Industry Leaders

-

Grupo Bimbo S.A.B. de C.V.

-

Flowers Foods Inc.

-

McKee Foods Corporation

-

Mondelēz International, Inc

-

Monginis Foods Pvt Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Cumbrian bakery Bells of Lazonby introduced the free-from We Love Cake range, which included the new Carrot Cake Slices. These slices were free from gluten, wheat, and milk, featuring a softly spiced carrot sponge layered with smooth, dairy-free frosting.

- November 2025: IGP launched its Global Cake Collection, a chef-curated assortment of eight cakes inspired by global flavors. The collection included options such as French salted caramel, Italian mocha espresso, and Indian rasmalai, highlighting diverse dessert craftsmanship and expanding its premium gifting portfolio.

- July 2025: FFG and Nadiya Hussain launched the Rainbow Celebration Cake, featuring bold flavor combinations and a vibrant design. The product is intended to elevate both everyday moments and special occasions.

- March 2025: Wonder Brand introduced a new snack cake lineup, including Crème-Filled Chocolate Cupcakes, Iced Honey Buns, Pecan Cinnamon Twists, and Peanut Butter Wafers, among other products.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cakes market as all value generated from freshly baked or industrially produced cakes, celebration, sponge, cupcakes, cheesecakes, and other variants sold through retail and food-service channels worldwide, whether packaged or artisanal. We consider sales in constant 2024 USD.

Scope exclusion: meat, dairy or plant-based meal substitutes, pastries, pies, and cake mixes are not counted.

Segmentation Overview

-

By Form

- Packaged

- Unpackaged/Artisanal

-

By Product Type

- Celebration Cakes

-

Cupcakes

- Center-filled

- Plain

-

Sponge Cakes

- Plain

- Center-filled

- Others

- Other Cakes

-

By Ingredient Type

- Conventional

- Vegan

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed artisanal bakers, packaged cake brand managers, ingredient suppliers, and leading grocery buyers across Asia-Pacific, Europe, the Americas, and the Gulf. Discussions clarified average selling prices, shrinkage rates, vegan uptake, and online fulfillment costs, letting us validate desk findings and fine-tune regional assumptions.

Desk Research

We began by mapping supply and demand signals from freely available tier-1 bodies such as the United States Department of Agriculture, Eurostat, UN Comtrade, and the China Bakery Association, complemented by trade journals like Baking Business and Food Navigator. Company 10-Ks, retailer scanner data extracts, and media archives on Dow Jones Factiva enriched price and channel intel. Our team accessed D&B Hoovers for private bakery financials and Questel for patent cues on shelf-life enhancers. These sources illustrate trends, yet are not exhaustive; many additional references guided data cleaning and cross-checks.

Market-Sizing & Forecasting

A blended top-down build, starting with per-capita bakery spend, retail outlet density, and household dessert frequency, creates the 2025 demand pool, which we reconcile with sampled bottom-up roll-ups of manufacturer shipments and supermarket category sales. Variables such as urbanization rates, premium cake share, average retail price per kilogram, online grocery penetration, and consumer price inflation feed a multivariate regression that projects figures to 2030. Where supplier roll-ups undershoot implied demand, we adjust using channel leakage factors gathered from interviews.

Data Validation & Update Cycle

Outputs pass three filters: automated variance checks against historic elasticities, peer review by a senior analyst, and a reconciliation against independent trade indicators. We refresh each model annually and issue interim tweaks when material events, raw-material shocks, new taxes, and major recalls shift the outlook. Before publication, an analyst performs a fresh sense-check so clients receive the latest view.

Why Mordor Intelligence's Cakes Market Baseline Earns Trust

Published estimates diverge because data collectors choose different product scopes, price anchors, and refresh cadences. Our disciplined scope and annual updates minimize that spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 100.87 B (2025) | Mordor Intelligence | |

| USD 97.69 B (2025) | Global Consultancy A | Bundles pastries and sweet pies, inflating addressable value |

| USD 67.34 B (2024) | Market Data Firm B | Counts only packaged retail sales; artisanal and food-service volumes omitted; older base year |

| USD 56.75 B (2024) | Analytical Boutique C | Narrow category definition and limited regional coverage, relying on assumed ASPs |

The comparison shows that when scope widens indiscriminately, totals rise; yet when channels or geographies are sliced out, values fall. By selecting a consistent cake-only lens, triangulating prices, and refreshing yearly, Mordor delivers a balanced, transparent baseline clients can repeat and trust.

Key Questions Answered in the Report

What is the current value of the global cakes market?

The cakes market size stands at USD 102.36 billion in 2026 and is forecast to reach USD 125.38 billion by 2031.

Which cake segment shows the fastest growth through 2031?

Cupcakes are projected to grow at a 4.63% CAGR as portion-control and grab-and-go formats gain popularity.

How large is the vegan cakes opportunity?

Vegan cakes are the quickest-growing ingredient segment, advancing at a 5.45% CAGR and commanding 20-30% price premiums.

Which sales channel is expanding the most?

Online retail is set to rise at a 6.58% CAGR, driven by cold-chain e-commerce and cloud-bakery models.

Page last updated on: