Doughnut Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

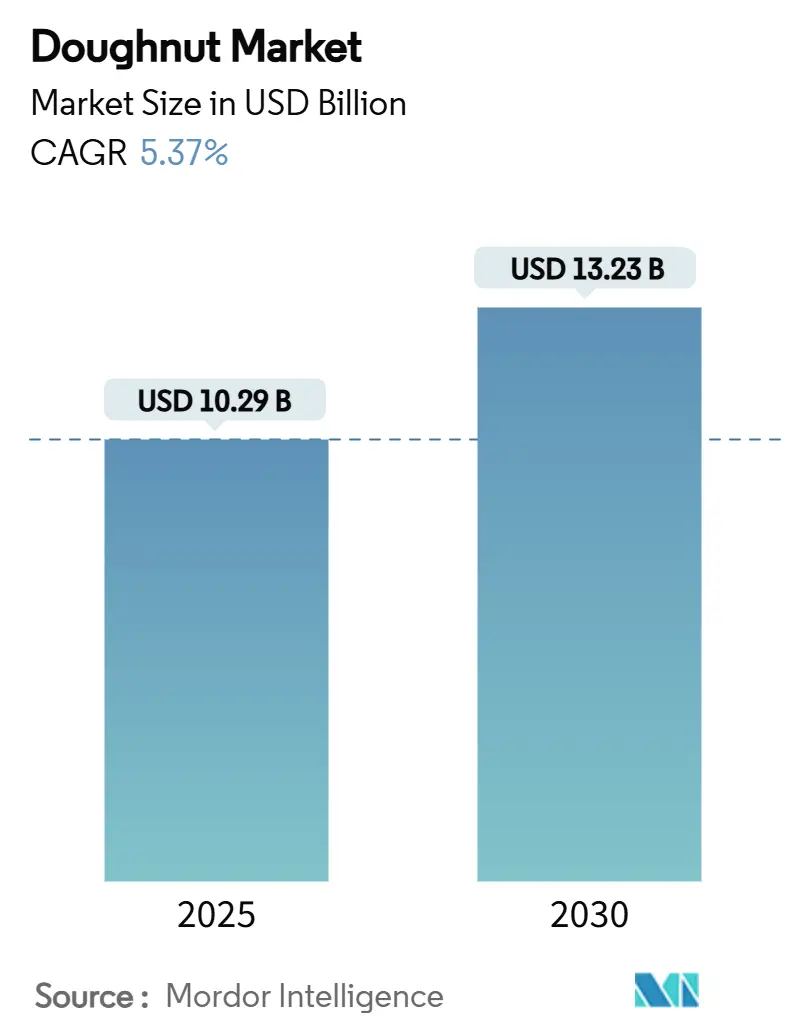

| Market Size (2025) | USD 10.29 Billion |

| Market Size (2030) | USD 13.23 Billion |

| Growth Rate (2025 - 2030) | 5.37% CAGR |

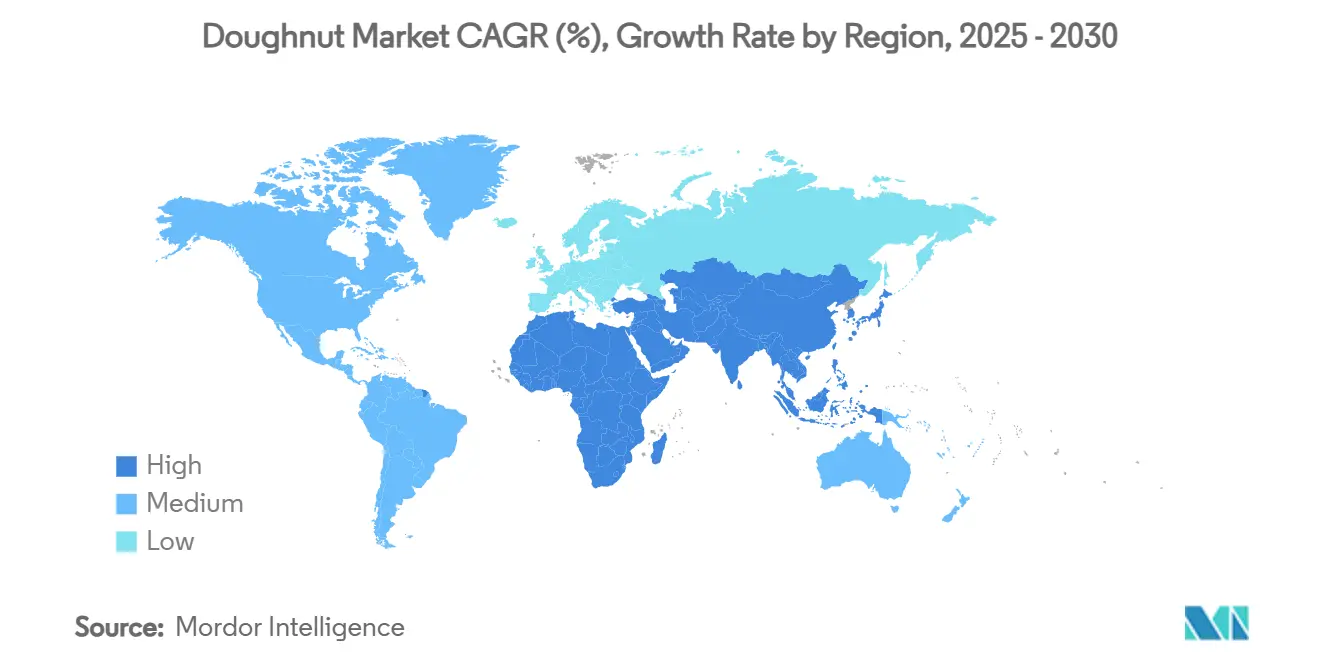

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

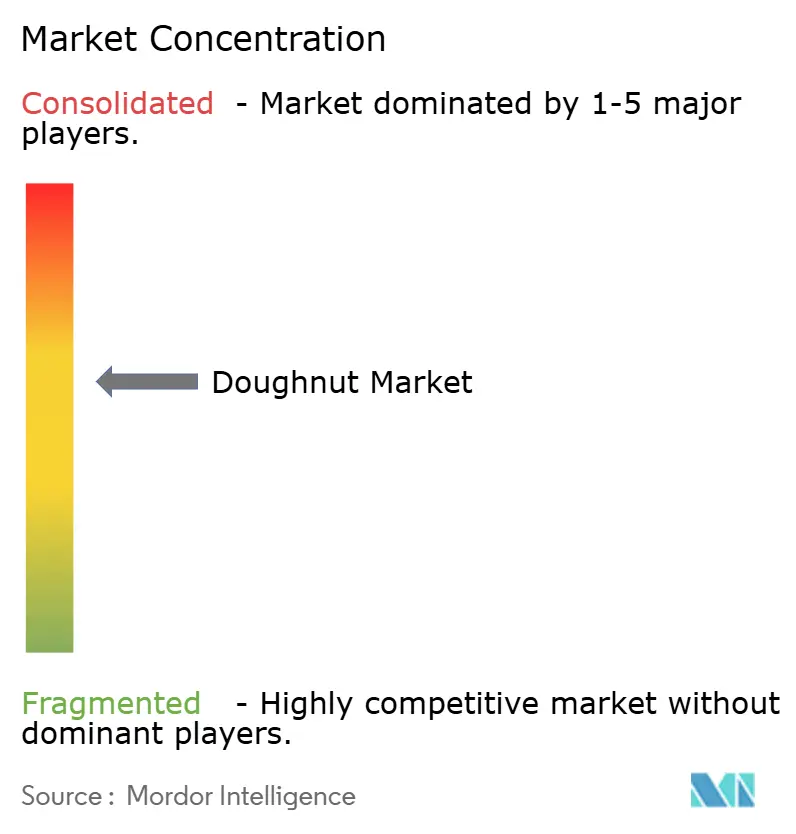

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Doughnut Market Analysis by Mordor Intelligence

The doughnut market size reached USD 10.29 billion in 2025 and is forecast to advance to USD 13.23 billion by 2030, translating into a 5.37% CAGR. Strong demand for indulgent yet portable snacks, expanding premium ranges priced above the mainstream tier, and improvements in shelf-life technologies keep the growth path steady. The rise of unique flavors, fillings, and toppings, including salted caramel, matcha, and cookies and cream, is attracting consumers. Supermarkets and hypermarkets remain the largest distribution avenue, yet digital channels and quick-commerce applications are expanding reach, especially in dense urban cores. Manufacturers that invest in traceability systems to comply with the FDA’s FSMA Rule 204, coming into force in January 2026, are positioned to defend shelf space and win retailer confidence. Meanwhile, emerging formats such as doughnut holes, mini-rings, and exotic flavor lines widen usage occasions, helping brands hedge against health-driven category pressure.

Key Report Takeaways

- By product category, conventional offerings held 87.92% of the doughnut market share in 2024, while free-from lines are projected to post a 7.58% CAGR through 2030.

- By packaging format, multi-packs commanded 49.24% revenue share in 2024; single-serve packs are expected to expand at a 7.19% CAGR over 2025–2030.

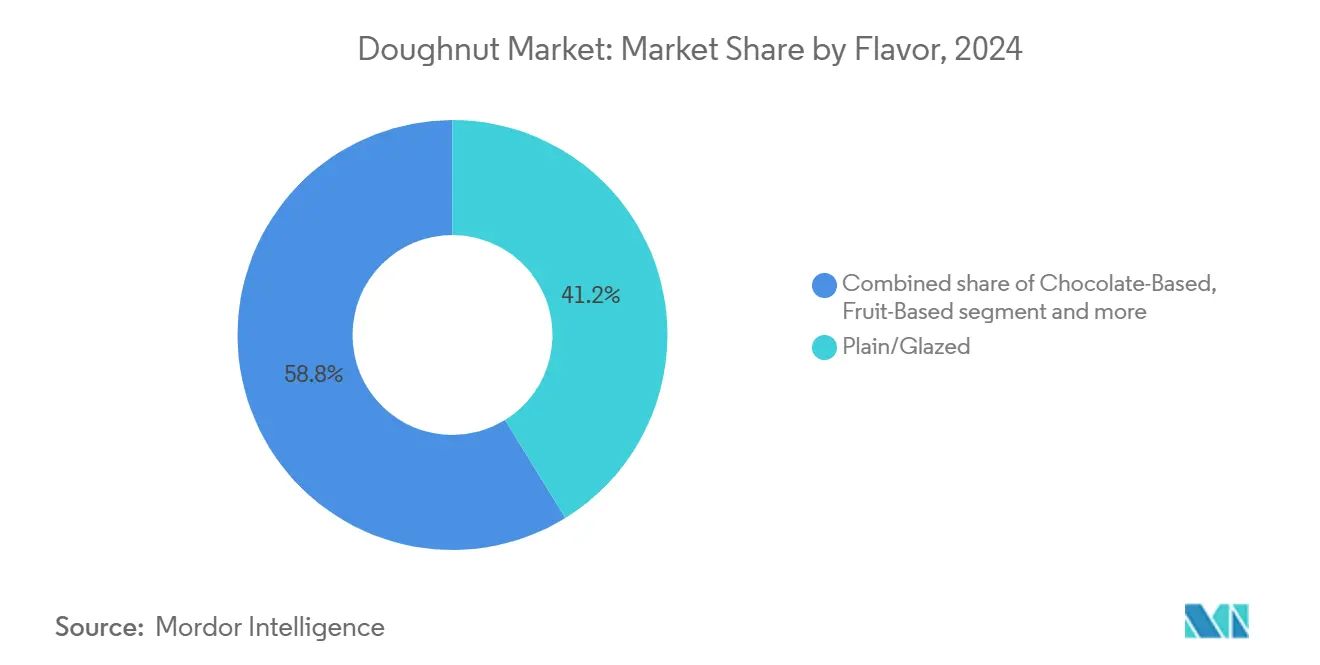

- By flavor profile, plain/glazed products secured 41.20% share of the doughnut market size in 2024; savory and exotic variants are slated to grow at an 8.35% CAGR to 2030.

- By distribution channel, supermarkets and hypermarkets led with 47.01% revenue share in 2024, whereas online and quick-commerce platforms are projected to rise at a 10.76% CAGR during the forecast window.

- By geography, North America commanded 37.97% of 2024 revenue, and the Middle East and Africa are expected to post an 8.03% CAGR, outpacing every other region.

Global Doughnut Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing appetite for customization and personalization | +0.8% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Innovation in flavors and product offerings | +1.2% | Global, led by North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Demand for premium, artisanal, and limited-edition varieties | +0.9% | North America and Europe core, spill-over to urban Asia-Pacific | Medium term (2-4 years) |

| Technological advancements in doughnut packaging | +0.7% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Rising popularity of doughnut holes and snackable formats | +0.6% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| On-the-go convenience and snacking trend | +1.1% | Global, strongest in urban centers worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing appetite for customization and personalization

Diners now view sweet bakery choices as an expression of identity, and brands are responding with flexible lines that allow seasonal toppings, mix-and-match assortments, and label personalization. Personalization in the doughnuts can range from custom flavors and toppings to branded packaging and unique designs. Customers are increasingly seeking unique and memorable experiences, making personalization a key differentiator for donut businesses. Digital listening tools mine social feeds for flavor cues, enabling short production runs that minimize inventory risk. Urban millennials and Gen Z are the early adopters, yet demand is filtering into suburban chains that offer click-and-collect for tailored boxes. Mobile ordering interfaces further reinforce the habit by letting consumers build baskets in real time, driving both average selling price and order frequency. The result is a resilient revenue stream anchored in experience rather than price promotion.

Innovation in flavors and product offerings

Limited-time varieties built around global desserts, savory spices, or alcohol infusions remain the most visible tactic for traffic generation. Alcohol-inspired profiles such as Irish-cream glaze entice novelty seekers, while umami-leaning notes like chili-lime capture cross-category snackers. In addition, since 2024, rapid-fit lines using natural colorants and encapsulated fillings have kept shelf stability intact while shortening reformulation cycles. Chains replicate the cadence of fashion drops, launching new flavors every four to six weeks to preserve relevance. Premium positioning lets operators hold margins even amid rising input costs, underscoring flavor agility as a hedge against commodity swings. Moreover, in April 2025, Krispy Kreme introduced the "Craving Cheesecake" collection in New York, offering three new cheesecake-inspired doughnut flavors: strawberry dream cheesecake, cookies and kreme cheesecake, and caramel delight cheesecake. These flavors are made available for a limited time at participating locations.

Demand for premium, artisanal, and limited-edition varieties

The premiumization wave elevates doughnuts from an everyday treat to “affordable luxury,” enabling mark-ups of 20–40%. The demand for premium donuts is strong and growing, with consumers increasingly seeking out unique flavors, high-quality ingredients, and visually appealing options. The desire for indulgent treats, social media buzz around creative donuts, and the popularity of gourmet and artisanal foods fuel this trend. Small-batch narratives that highlight heritage grains or region-specific fruit purees feed social outreach and earn menu placement in high-footfall cafés. Artificial scarcity via numbered boxes and tie-ins with pop-culture franchises triggers impulse buys. Younger cohorts regard such purchases as shareable experiences, amplifying organic reach on platforms such as TikTok. The willingness to pay more for hallmarks of craft, hand glazing, single-origin cocoa, and gluten-free flours offsets lower per-capita consumption in health-conscious demographics.

Technological advancements in doughnut packaging

Technological advancements are impacting doughnut packaging in several key areas, including automation, sustainability, and enhanced presentation. Automated packaging systems are increasing efficiency and reducing labor costs, while eco-friendly materials and innovative designs are appealing to environmentally conscious consumers. Modified-atmosphere pouches, high-barrier films, and plant-based trays are extending freshness windows to 25–30 days without freezing. Sensor-equipped labels that monitor temperature deviations reassure retailers handling longer supply distances. QR codes route consumers to videos detailing ingredient provenance, bolstering trust ahead of FSMA-mandated traceability. Lightweight bio-resins trim freight weight, cutting logistics emissions and aligning with corporate sustainability goals. Collectively, these innovations enlarge the geographic radius of daily fresh deliveries, giving makers headroom to negotiate new retail listings and cross-border export trials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to high sugar and fat content | -1.4% | Global, most pronounced in developed markets | Medium term (2-4 years) |

| Competition from healthier snack alternatives | -0.9% | North America and Europe core, expanding globally | Short term (≤ 2 years) |

| Short shelf life and freshness issues | -0.8% | Global, particularly challenging in emerging markets | Short term (≤ 2 years) |

| Stringent food safety and labeling regulations | -0.6% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns related to high sugar and fat content

In a bid to combat rising health concerns, legislators across various regions are contemplating taxes on sugary foods. Concurrently, initiatives like mandatory front-of-pack labeling are being introduced to guide consumers towards healthier choices. Public health campaigns frequently spotlight doughnuts in their obesity narratives, leading retailers to reduce their shelf space. In response, major food producers are launching product lines with 20-25% less sugar and incorporating fiber to mitigate glycemic spikes. Grupo Bimbo's achievement of 95% positive nutrition in its product portfolio demonstrates how major players are responding to these pressures through reformulation and portfolio optimization [1]Source: Grupo Bimbo, “Annual Integrated Report 2024,” grupobimbo.com. However, reformulating products isn't straightforward; for instance, it demands investments in alternative sweeteners that replicate sucrose's bulking properties without sacrificing taste. Those producers who can't adapt swiftly may face dwindling sales as households tighten their budgets on discretionary calories. As health concerns mount, the food industry finds itself at a crossroads. With consumers becoming increasingly aware of the implications of high sugar and fat content, the pressure on producers intensifies.

Competition from Healthier Snack Alternatives

As consumers increasingly prioritize nutritious foods and beverages, donuts are grappling with heightened competition from healthier snack alternatives. This trend stems from a growing awareness of the health risks tied to high sugar and fat consumption, coupled with a preference for sustainable and ethically sourced foods. Once the domain of baked sweets, prime aisle endcaps now showcase protein bars, nut clusters, and dried fruit chips. Startups, backed by venture capital, emphasize clean formulations, transparent sourcing, and functional benefits like added collagen or adaptogens. Workplace vending partners are leaning towards calorie-controlled items, pushing traditional donut SKUs out of the lineup. As consumer preferences shift, so does merchandising space. Brands that remain entrenched in indulgent marketing risk losing their snack-time relevance. In response, major bakers are experimenting with hybrid SKUs that combine protein isolates and reduced sugar, though taste remains a challenge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Conventional Dominance Faces Free-From Disruption

The conventional segment's commanding 87.92% market share in 2024 reflects entrenched consumer preferences for traditional doughnut formulations and established brand loyalty built over decades. The segment enjoys streamlined procurement flows for staples such as enriched wheat flour, consolidating margins even when commodity prices fluctuate. Price points remain within reach for value-oriented shoppers who buy in multipacks for household consumption. Yet regulatory pressure and consumer self-monitoring of sugars invite reformulation or diversification into better-for-you variants. To hedge, leading producers have introduced reduced-sugar glazes and baked, not fried, rings within their mainstream portfolios.

The current 7.58% CAGR implies free-from could approach a low-double-digit share before 2030, narrowing the conventional lead in the doughnut market. Free-from offerings, though smaller in absolute terms, outpace the category in growth. Gluten-free and sugar-free recipes leverage advances in rice-, cassava-, and pulse-based flours to replicate crumb structure. Premium selling prices compensate for smaller batch sizes, and messaging around digestive wellness widens the consumer set beyond celiac or diabetic shoppers. Retailers grant incremental shelf space because the products add shopper basket value. Brands that marry free-from attributes with indulgent flavor, think salted-caramel gluten-free, achieve velocities comparable to conventional bestsellers. Grupo Bimbo's acquisition of Amaritta Food to enhance gluten-free offerings exemplifies how major players are investing in free-from capabilities to capture this emerging demand.

By Packaging Format: Multi-Pack Leadership Challenged by Single-Serve Convenience

In 2024, multi-pack formats command a substantial 49.24% market share, capitalizing on a value perception and household consumption trends that lean towards bulk buying. Yet, it's the single-serve packaging that's making waves, boasting a robust 7.19% CAGR. This surge is largely attributed to the rising trend of on-the-go consumption and a growing preference for portion control. Shoppers with families are still gravitating towards value-priced multi-packs, particularly in club stores where buying in bulk translates to reduced unit costs. Beyond just savings, these multi-packs optimize shelf space and streamline replenishment cycles for retailers. They also sync seamlessly with weekly shopping trips, offering manufacturers a consistent throughput. However, with shrinking household sizes and an uptick in individual snacking moments, single-serve packs are witnessing a meteoric rise in popularity. These compact portions not only address portion-control concerns but also conveniently fit into lunch boxes, catering perfectly to commuters seeking a mess-free snack.

Single-serve units are not just about convenience; they also promise higher margins per piece. They open the door to flavor experimentation, especially with assorted packs. Quick-commerce platforms have a soft spot for this SKU, as it aligns perfectly with their promise of delivery in under 30 minutes, all without the need for refrigeration. In a nod to sustainability, mono-material wrappers, now recyclable in numerous curbside programs, are helping producers counteract previous environmental criticisms. Furthermore, producers with interlocking production lines enjoy the flexibility of switching between unit counts with minimal downtime, ensuring optimal plant utilization. As the market evolves, the dynamics between multi-pack and single-serve formats will be intriguing to watch. With the growing emphasis on sustainability and convenience, brands that can adeptly navigate these waters stand to gain the most. The future seems bright for both formats, but the trajectory will largely depend on shifting consumer preferences and market trends.

By Flavor Profile: Traditional Glazed Dominance Meets Exotic Innovation

In 2024, plain and glazed varieties dominate the market, holding a 41.20% share, underscoring their foundational role and widespread appeal. Meanwhile, savory and exotic flavors are surging ahead, boasting an impressive 8.35% CAGR, fueled by consumers' adventurous palates. Chocolate flavors enjoy consistent demand, thanks to their familiar allure and seasonal spikes, while fruit-based options ride the wave of health trends and a preference for natural ingredients. This flavor segmentation paints a picture of a market where time-honored tastes meet bold experimentation. Manufacturers are not just sticking to their guns; they're also dabbling in limited-time and seasonal offerings to gauge market reactions.

The rise of exotic flavors mirrors a larger culinary shift towards global fusions and unique combinations, often leading to buzzworthy moments on social media. Combinations like maple-bacon and chili-lime are winning over consumers who prioritize experience and are ready to pay a premium for it. While traditional flavors enjoy steady demand and operational efficiency, it's the innovative varieties that are carving out brand differentiation and boosting profit margins. The pace of flavor innovation is quickening, with manufacturers harnessing consumer insights and social media trends to swiftly craft and trial new offerings. As the market evolves, the interplay between tradition and innovation becomes ever more pronounced. While established flavors continue to anchor the market, the appetite for the unconventional is reshaping its contours. The future promises a tantalizing blend of the familiar and the avant-garde, ensuring that consumers remain at the heart of flavor evolution.

By Distribution Channel: Supermarket Dominance Disrupted by Digital Commerce

In 2024, supermarkets and hypermarkets command a dominant 47.01% market share, capitalizing on their established infrastructure and ingrained consumer shopping habits for packaged goods. Meanwhile, online retail and quick-commerce platforms are on the rise, boasting a robust 10.76% CAGR, fueled by a surge in digital adoption and enhancements in last-mile delivery. Cafes and bakery outlets carve out a niche, positioning themselves as key players for premium and artisanal products. In contrast, other distribution avenues, such as vending machines and convenience stores, cater to accessibility and spur-of-the-moment purchases. This evolution in distribution channels mirrors a broader transformation in retail, where the emphasis increasingly leans towards convenience and accessibility in shaping purchase decisions.

Online retail is witnessing a pronounced uptick, especially among younger demographics and urban dwellers, who prioritize convenience and are adept at digital transactions. Quick-commerce platforms, with their promise of same-day delivery, are emerging as formidable competitors to the convenience offered by traditional retail. This digital surge not only reshapes consumer habits but also paves the way for direct-to-consumer brands and subscription models, allowing them to sidestep conventional retail markups. A case in point is Greggs, whose digital channel expansion is evident with app transactions jumping from 12.5% to 20.1%, underscoring the shift of traditional retailers towards a digital-first approach [2]Source: Snack and Bakery, “Single-Serve Packaging Trends 2024,” snackandbakery.com. While traditional channels still hold sway in impulse buying and instant gratification, they face the pressing challenge of evolving to meet the omnichannel expectations of today's consumers. The retail landscape is undergoing a seismic shift, with digital channels gaining prominence and traditional avenues adapting to stay relevant. As consumer preferences evolve, driven by convenience and digital comfort, retailers must navigate this changing terrain, balancing between established practices and the demands of a digital-first future. The interplay between online and traditional channels will shape the future of retail, making it imperative for all players to stay agile and responsive.

Geography Analysis

North America retained 37.97% of global revenue in 2024. Deep-rooted breakfast habits, densely distributed retail networks, and the presence of multinational bakery groups anchor sales. The McDonald’s–Krispy Kreme test rollout, scaling toward 6,000 restaurants by 2026, exemplifies how strategic distribution alliances can unlock incremental reach without heavy capital spend [3]Source: McDonald’s USA, “McDonald’s and Krispy Kreme Expand Testing to Hundreds of Restaurants,” mcdonalds.com. Health concerns are tempering per-capita intake, yet reformulation and premium limited-edition drops keep interest alive. Canada mirrors these patterns, albeit with stronger free-from traction due to higher diagnosed celiac rates.

Asia-Pacific remains the highest-potential growth engine. Urbanization and rising disposable incomes push packaged snacks into mainstream baskets. India’s packaged food sector is forecast to reach INR 4,883 billion by FY26, creating ample headroom for sweet bakery adoption as per its BDO India [4]Source: BDO India, “India Packaged Food Report 2025,” bdo.in. Japanese consumers value premium texture and flavor authenticity, supporting higher price points in convenience store chains that restock multiple times a day. Australia’s food channel normalization post-pandemic sees private labels pressing price points, yet branded doughnut lines maintain loyalty through promotional tie-ups with entertainment franchises.

The Middle East and Africa, turned out to be the fastest-growing cluster at 8.03% CAGR through 2030. Young demographics, large shopping-mall footprints, and a surge in Western-style café culture spur demand. Krispy Kreme’s Morocco entry in 2024, with localized flavors and gluten-free SKUs, shows the strategy of fusing global brand equity with regional taste cues. Supply chain challenges, including cold-chain gaps, drive interest in high-barrier packaging that secures product integrity under extreme temperatures, supporting broader penetration in the doughnut market.

Competitive Landscape

This evolving landscape showcases a moderate market concentration, highlighting a significant share held by a select few, yet leaving ample space for innovation-driven challengers to carve their niche in the doughnut arena. In the competitive landscape of the doughnut market, major players like Hostess Brands, Grupo Bimbo, Krispy Kreme, J.M. Smucker (bolstered by its acquisition of Hostess), and McKee Foods command national prominence. However, they share the spotlight with regional artisan makers and private labels.

The scale of these industry giants not only provides them with leverage in ingredient sourcing but also affords them substantial advertising budgets. This financial muscle translates into national TV campaigns, a luxury that smaller players find hard to match. The trend of consolidation is evident: In 2024, Grupo Bimbo expanded its footprint by acquiring brands in Eastern Europe and South America, enhancing its dominance in the sweet baked goods segment. Meanwhile, J.M. Smucker is steering Hostess Brands with a five-point strategy, emphasizing heightened marketing efforts to resonate with Gen Z audiences.

Equally crucial is the innovation in route-to-market strategies. Krispy Kreme has adopted a hub-and-spoke model, ensuring fresh doughnuts reach grocery and gas station "spokes" daily. This strategy not only amplifies visibility but also curtails capital intensity. Furthermore, retail media collaborations facilitate targeted coupon distributions, enhancing scan data metrics. Concurrently, loyalty applications gather consumer insights, fine-tuning flavor offerings. Automation is also making waves, with initiatives like optical glazing systems and AI-driven packaging inspections boosting throughput and minimizing waste, granting early adopters a competitive edge. Opportunities abound in health-centric segments, regional flavor adaptations, and digitally-driven direct-to-consumer approaches, especially those promising warm doughnut deliveries within an hour in major metropolitan areas.

Doughnut Industry Leaders

Grupo Bimbo, S.A.B. de C.V.

Krispy Kreme, Inc.

McKee Foods Corporation

Yamazaki Baking Co., Ltd

The J.M. Smucker Company (Hostess Brands, LLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Krispy Kreme launched expansion into Brazil through a joint venture with Ipiranga's AmPm convenience store chain, leveraging AmPm's 1,500-location network for efficient scaling. This capital-light franchise strategy demonstrates how global brands are penetrating emerging markets through strategic partnerships with established retail infrastructure.

- October 2024: Grupo Bimbo announced acquisitions in Eastern Europe and South America, including Don Don in Serbia, Slovenia, Croatia, and Montenegro, plus Wickbold in Brazil, expanding its global footprint in packaged bread and sweet baked goods markets. These transactions reflect active merger and acquisition strategies focused on geographic expansion and market consolidation.

- August 2024: Krispy Kreme opened its first shop in Morocco in partnership with franchisee Americana, featuring local flavors and gluten-free options alongside the Hot Light Theatre Shop concept. This expansion demonstrates how global brands are adapting to regional preferences while maintaining core brand identity.

- January 2024: Krispy Kreme announced expansion into Spain through a joint venture with Glaseadas Originales, planning 500 fresh points of access in major cities over five years. This strategic move reflects continued international expansion in European markets with strong growth potential.

Global Doughnut Market Report Scope

| Free-From |

| Conventional |

| Single-Serve (≤2 pieces) |

| Multi-Pack (3–12 pieces) |

| Family/Bulk Pack (more than 12 pieces) |

| Plain/Glazed |

| Chocolate-Based |

| Fruit-Based |

| Savory/Exotic |

| Supermarkets/Hypermarkets |

| Cafes/Bakery Outlet |

| Online Retail |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | India |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Category | Free-From | |

| Conventional | ||

| By Packaging Format | Single-Serve (≤2 pieces) | |

| Multi-Pack (3–12 pieces) | ||

| Family/Bulk Pack (more than 12 pieces) | ||

| By Flavor | Plain/Glazed | |

| Chocolate-Based | ||

| Fruit-Based | ||

| Savory/Exotic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Cafes/Bakery Outlet | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the doughnut market?

The doughnut market was valued at USD 10.29 billion in 2025 and is projected to reach USD 13.23 billion by 2030

Which product category is growing fastest?

Free-from doughnuts, including gluten-free and sugar-free lines, are advancing at a 7.58% CAGR through 2030.

How are distribution channels shifting?

Supermarkets remain the largest channel, yet online retail and quick-commerce platforms are expanding fastest at a 10.76% CAGR.

What regions present the strongest growth potential?

Asia-Pacific and the Middle East and Africa show the highest growth, driven by urbanization, rising incomes, and expanding modern retail.

Page last updated on: