AI Accelerator Cluster Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

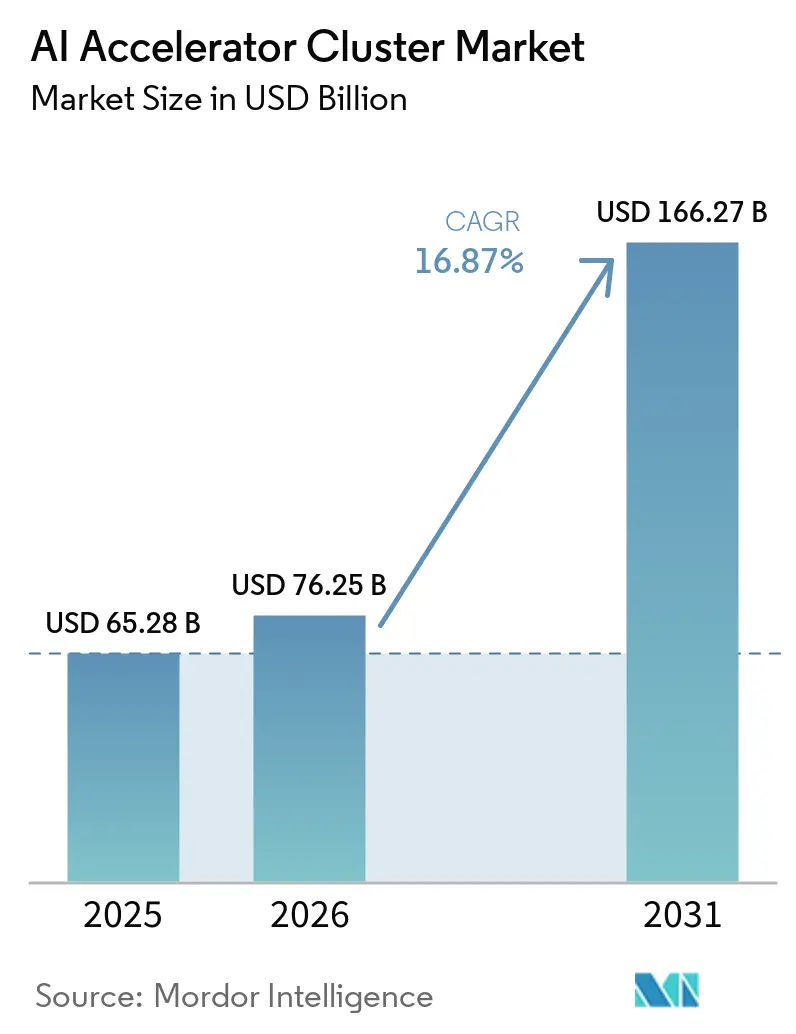

| Market Size (2026) | USD 76.25 Billion |

| Market Size (2031) | USD 166.27 Billion |

| Growth Rate (2026 - 2031) | 16.87% CAGR |

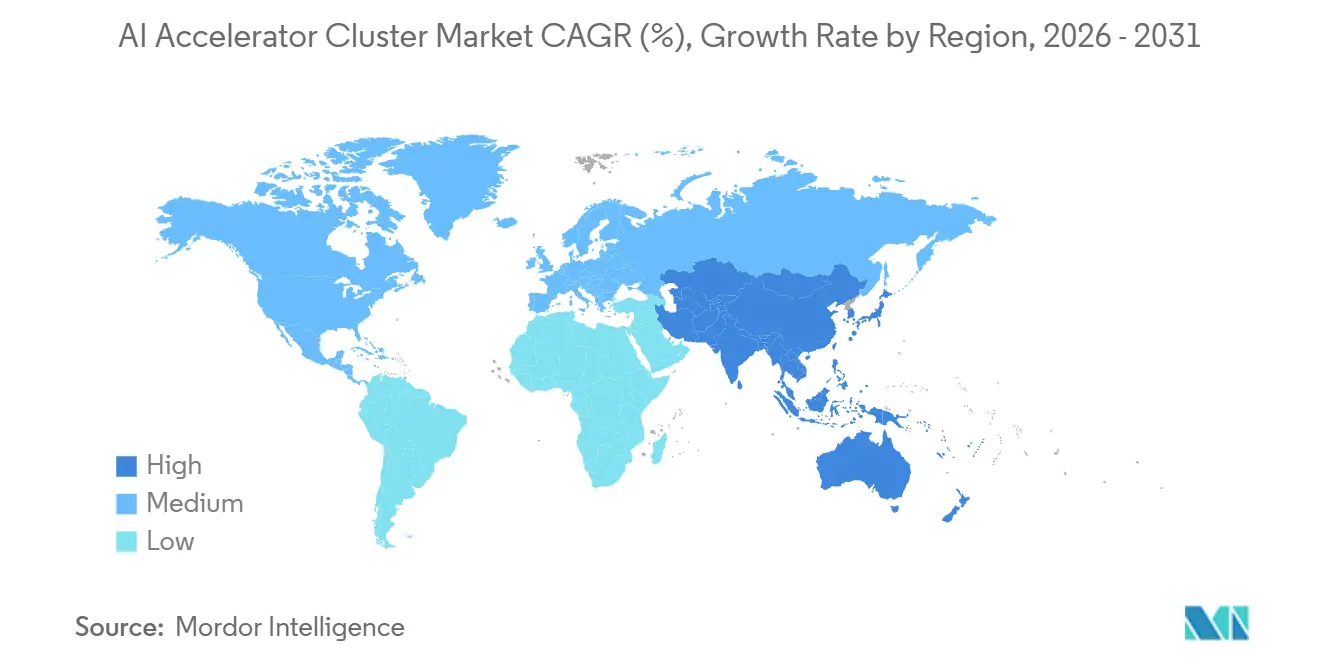

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

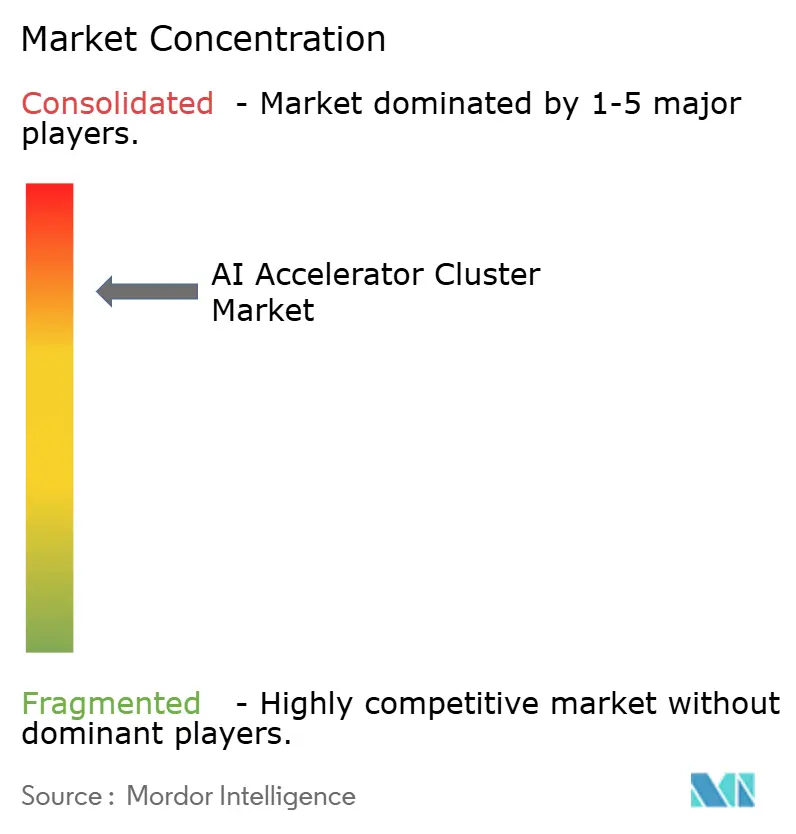

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Accelerator Cluster Market Analysis by Mordor Intelligence

The AI accelerator cluster market size is expected to grow from USD 65.28 billion in 2025 to USD 76.25 billion in 2026 and is forecast to reach USD 166.27 billion by 2031 at 16.87% CAGR over 2026-2031. The AI accelerator cluster market is expanding because model training keeps moving to larger systems, while enterprise inference is shifting from shared capacity to dedicated deployments. The demand pattern also reflects a broader change in procurement, because software control, power design, and networking choices now shape cluster value as much as accelerator purchases do. Regional policy is also influencing the AI accelerator cluster market, with export controls and sovereign compute programs pushing buyers to build capacity inside preferred technology blocs. Competition remains intense, but the strongest positions sit with vendors that can support full rack-scale systems, memory access, networking, and cooling at the same time. This is creating new openings in orchestration software, hybrid deployment design, and region-specific supply partnerships across the AI accelerator cluster market.

Key Report Takeaways

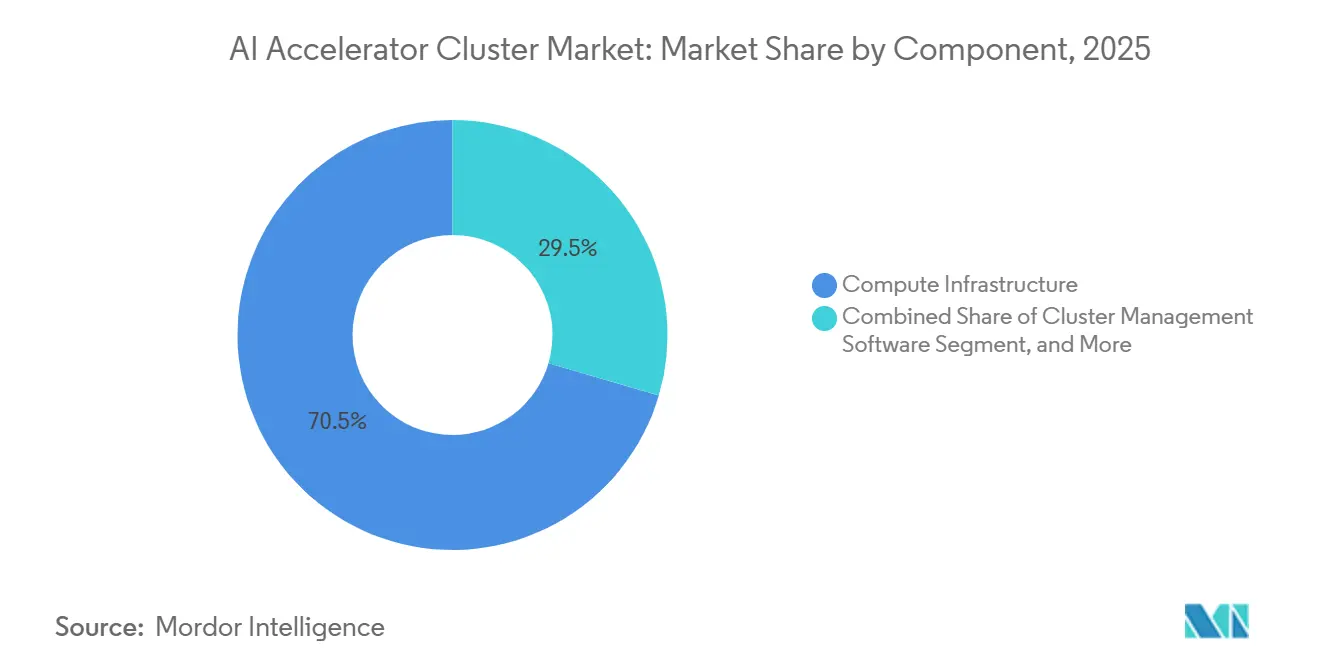

- By component, compute infrastructure commanded 70.46% of the AI Accelerator Cluster market revenue in 2025, while cluster management software is projected to expand at a 17.04% CAGR through 2031.

- By accelerator architecture, GPU-based clusters held 80.27% of the AI Accelerator Cluster market revenue share in 2025, while custom AI ASIC-based clusters are expected to record the highest CAGR at 17.21% through 2031.

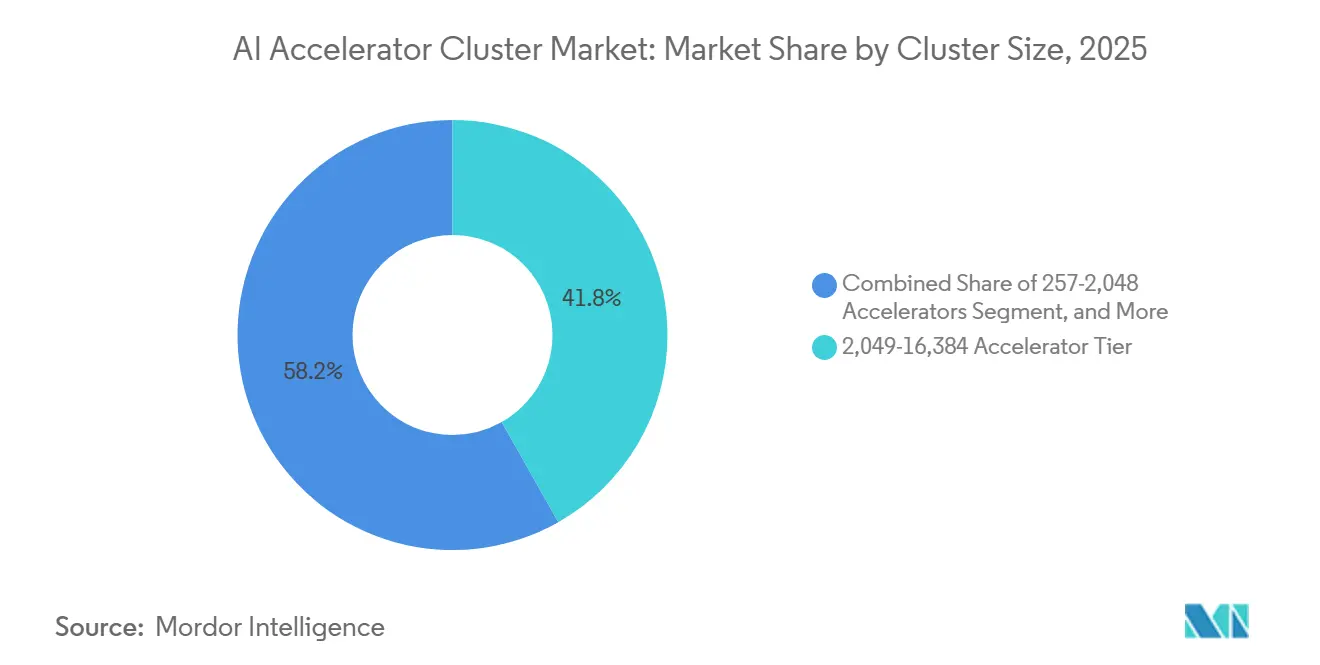

- By cluster size, the 2,049-16,384 accelerator tier accounted for 41.81% of revenue in 2025, while clusters above 16,384 accelerators are projected to grow at a 17.42% CAGR through 2031.

- By function, training clusters held 60.54% share in 2025, while inference is expected to expand at a 17.26% CAGR through 2031.

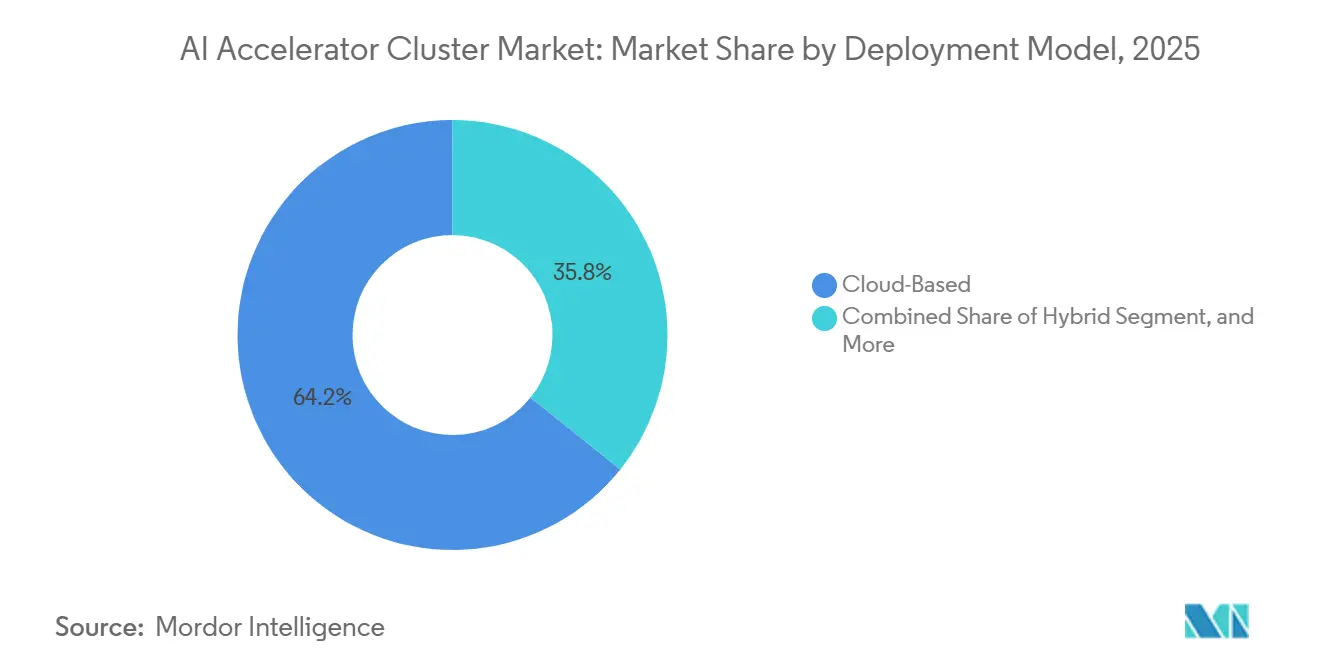

- By deployment model, cloud-based deployments captured 64.24% share in 2025, while hybrid deployments are projected to advance at a 17.56% CAGR through 2031.

- By end user, hyperscale cloud service providers accounted for 63.48% of revenue in 2025, while government and research institutions are expected to grow at a 17.37% CAGR through 2031.

- By geography, North America held 52.64% of the AI accelerator cluster market in 2025, while Asia-Pacific is projected to post the fastest regional CAGR at 17.22% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Accelerator Cluster Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Generative AI Training Workloads | +4.5% | Global | Short term (≤ 2 years) |

| Hyperscale Cloud Capital Expenditure on AI Infrastructure | +3.8% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Rising Cluster-Scale Demand for Low-Latency Interconnects | +2.5% | Global | Medium term (2-4 years) |

| Shift Toward Dedicated Inference Clusters in Enterprise Data Centers | +2.1% | North America and Europe | Medium term (2-4 years) |

| Export-Control Driven Regional Buildout of Domestic AI Compute Capacity | +1.8% | Asia-Pacific, Middle East | Medium term (2-4 years) |

| Power-Dense Rack Design Improvements Enabling Larger Cluster Deployments | +1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion Of Generative AI Training Workloads

The AI accelerator cluster market is being pushed higher by the rapid increase in training scale for frontier models, because buyers now plan for much larger compute blocks than they did a few years ago. Rack-level and factory-level infrastructure have moved into production to support this shift, which shows that vendors now expect sustained demand rather than short project spikes.[1]NVIDIA Corporation, “NVIDIA Vera Rubin Ramps Into Full Production to Power Agentic AI Factories Worldwide,” NVIDIA Investor Relations, nvidia.com The training cycle matters beyond the first purchase, because once a model family is built on a certain compute and networking stack, later deployment often stays aligned with the same architecture. That makes hardware demand more durable across the AI accelerator cluster market, especially when customers want smoother software compatibility and easier fleet expansion. It also raises the cost of delay for operators, because every postponed build can affect later inference readiness, vendor qualification, and software tuning work. The result is a procurement pattern in the AI accelerator cluster market where large training systems influence several later spending decisions across compute, memory, software, and facility design.

Hyperscale Cloud Capital Expenditure On AI Infrastructure

Large cloud operators continue to shape the AI accelerator cluster market because their infrastructure programs set the pace for system orders, supplier commitments, and deployment calendars. The scale of current factory-style rollouts is visible in the production ramp of NVIDIA's Vera Rubin platform, which entered full production in May 2026 through 150 supply-chain partners, 350+ factories, and 30 countries. The same pattern appears in system design, where liquid-cooled rack platforms are now being shipped as complete infrastructure blocks rather than as isolated server upgrades.[2]Dell Technologies, “Dell PowerRack Transforms AI Infrastructure With Scalable Compute, Networking and Storage,” Dell Technologies, dell.com This matters for the AI accelerator cluster market because long planning cycles in memory, advanced packaging, networking, and cooling now start much earlier in the buying process. It also makes supply access more uneven, since vendors with long-term design wins and partner alignment can secure build capacity ahead of smaller buyers. As a result, hyperscale spending is not only adding capacity in the AI accelerator cluster market, it is also shaping who can obtain key components on time.

Rising Cluster-Scale Demand For Low-Latency Interconnects

The AI accelerator cluster market is also being driven by stronger demand for low-latency interconnects, because model performance at scale depends on how efficiently accelerators exchange data across the fabric. The industry push behind open Ethernet for AI is now more formalized, with the Ultra Ethernet Consortium highlighting congestion control, load balancing, and security as key requirements for modern AI networking. This changes buying priorities across the AI accelerator cluster market, because networking is no longer treated as a support layer that can be added after compute decisions are made. Operators need higher throughput and more predictable communication behavior as clusters move toward larger footprints and more demanding training runs. That makes open, multi-vendor networking models more attractive when buyers want to reduce dependence on a single protocol or vendor path. It also increases the value of vendors that can deliver validated fabric behavior at rack scale, since performance losses from poor interconnect design can cancel out gains from adding more accelerators.

Shift Toward Dedicated Inference Clusters In Enterprise Data Centers

Dedicated inference systems are becoming a stronger demand source for the AI accelerator cluster market, especially where enterprises want better cost control, lower latency, and tighter data handling. Dell Technologies reported that more than 4,000 AI Factory customers had purchased 8-GPU to 32-GPU systems across healthcare, finance, and legal sectors by 2025. That supports a clear shift in the AI accelerator cluster market, where inference is moving from shared environments into dedicated infrastructure for repeated production use. Buyers in regulated fields are especially important here, because they often need local control over model weights, sensitive data, and service reliability. The spending pattern is also more repeatable, since inference systems tend to be refreshed in line with model upgrade cycles rather than only when a new training project begins. This gives the AI accelerator cluster market a steadier replacement base that is less tied to a single headline model launch.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Power and Cooling | -2.0% | Global | Short term (≤ 2 years) |

| Supply Constraints in Advanced Packaging and High-Bandwidth Memory | -1.5% | Global | Short term (≤ 2 years) |

| Software Portability and Vendor Lock-In Risk | -0.8% | North America and Europe | Medium term (2-4 years) |

| Data Center Grid Interconnection Delays for Mega-Clusters | -0.7% | North America, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost Of Ownership For Power And Cooling

Power and cooling remain a major restraint on the AI accelerator cluster market because facility readiness is now a deciding factor in whether systems can be deployed on schedule. NVIDIA stated that Vera Rubin NVL72 runs at around 132 kW under sustained training loads, which makes direct liquid cooling a requirement rather than an option. The same source noted that liquid cooling is becoming central to AI factory design, which means the hardware sales often depend on whether the site can handle thermal and power density at the rack level. The International Energy Agency also reported that data center electricity demand could double between 2022 and 2026, and it flagged power grid limits as a growing source of project delay.[3]International Energy Agency, “Energy and AI, Executive Summary,” International Energy Agency, iea.org This creates a layered cost issue in the AI accelerator cluster market, because buyers must fund accelerators, cooling systems, facility upgrades, and, in some cases, grid-related waiting periods. It also slows broader enterprise adoption, since many mid-sized operators cannot absorb the retrofit burden as easily as hyperscalers or state-backed programs.

Supply Constraints In Advanced Packaging And High-Bandwidth Memory

Supply constraints in high-bandwidth memory and advanced packaging continue to limit the AI accelerator cluster market, even when end demand stays strong. IEEE Spectrum reported that HBM demand surged in 2025 and remained under pressure in 2026, while industry supply remained concentrated among a very small group of manufacturers. The same report cited Micron's view that demand would outstrip supply substantially for the foreseeable future, which shows that the constraint is not expected to ease quickly. This matters for the AI accelerator cluster market because memory shortages affect finished system shipments, cloud pricing, and the timing of cluster expansion plans. Buyers can still want more compute, but actual delivery depends on whether memory, packaging, and qualification steps move in sync. The result is a market where strong order books do not always translate into immediate revenue recognition or immediate physical deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Compute Infrastructure Leads Revenue While Management Software Gains Importance

Compute infrastructure held 70.46% of revenue in 2025, which made it the largest component in the AI accelerator cluster market. That lead reflected the central role of accelerator silicon, rack-scale server systems, and power distribution hardware in every deployment. Networking infrastructure remained the next most important spending layer, because high-bandwidth fabrics determine whether larger clusters can operate efficiently under training and inference loads. Storage infrastructure and services also remained important, especially where parallel file systems and nearby object storage were needed to reduce data movement delays. The AI accelerator cluster market still shows a clear hardware bias at the component level, because most early spending goes first to systems that can be installed, energized, and brought into production.

Cluster management software is projected to grow at 17.04% CAGR from 2026 to 2031, which makes it the fastest-moving component in the AI accelerator cluster market. This reflects a practical shift, because scheduling, fault recovery, and power-aware orchestration become harder as systems move toward very large accelerator counts. Software also gains value when operators manage mixed hardware environments and want higher utilization across different node types. In that sense, the AI accelerator cluster industry is not moving away from hardware demand, but it is assigning more value to the layer that keeps large systems stable and productive. Over time, software orchestration is likely to capture a larger share of wallet inside the AI accelerator cluster market because cluster complexity keeps rising with scale.

By Accelerator Architecture: GPUs Hold The Base While Custom ASICs Advance

GPU-based clusters held 80.27% of revenue in 2025, which kept them at the center of the AI accelerator cluster market. Their lead came from broad support across training, research, and flexible enterprise use cases where software compatibility remains a priority. This installed base also gave buyers confidence in support tools, system integration, and developer familiarity. TPU-based clusters remained concentrated in internal deployments, while FPGA-based clusters stayed limited to narrower use cases such as low-latency inference or telecom workloads. Heterogeneous accelerator formats remained relevant in selected environments, but they did not alter the main structure of the AI accelerator cluster market.

Custom AI ASIC-based clusters are projected to grow at 17.21% CAGR from 2026 to 2031, which makes them the fastest-growing architecture in the AI accelerator cluster market. Their growth reflects a clear buyer motive, because purpose-built silicon can deliver better cost efficiency in stable, high-volume inference environments. The shift is most visible among large operators that can spread design costs across very large deployments and repeated workloads. This keeps GPUs in a strong position for general-purpose flexibility, but it also gives custom silicon a stronger foothold where throughput-per-dollar matters more than broad programmability. As this mix evolves, the AI accelerator cluster market is likely to stay GPU-led in revenue while becoming more architecturally varied at the high-volume inference edge.

By Cluster Size: Mid-Range Systems Hold Share While Larger Installations Expand Faster

The 2,049-16,384 accelerator tier accounted for 41.81% of revenue in 2025, which made it the largest cluster size band in the AI accelerator cluster market. This range fits more easily within current data center footprints, utility timelines, and operational processes than the largest build formats. It also matches the needs of hyperscaler training blocks and large enterprise inference deployments that want meaningful scale without the longest facility lead times. Smaller tiers remained relevant for departmental AI work, research use, and buyers with stricter data residency requirements. That kept the AI accelerator cluster market broad at the lower end even while the largest systems drew the most attention.

Clusters above 16,384 accelerators are projected to grow at 17.42% CAGR from 2026 to 2031, which marks the fastest expansion among size bands in the AI accelerator cluster market. This growth reflects demand from frontier labs, sovereign compute programs, and hyperscalers that continue to push larger model development. At that scale, interconnect topology, communication efficiency, and fault isolation become central engineering issues rather than secondary tuning matters. AMD's expanded work with Meta on the Helios rack-scale platform shows how vendors are redesigning system architecture to support very large deployments more effectively. The pattern suggests that the AI accelerator cluster market will keep a large installed base in mid-range deployments while directing a growing share of new investment toward much larger cluster formats.

By Function: Training Holds The Revenue Base While Inference Moves Faster

Training clusters held 60.54% share in 2025, which kept them as the largest functional category in the AI accelerator cluster market. Their lead came from the high capital intensity of frontier model development and the large system footprints required to support it. Training also tends to lock in broader hardware, software, and networking choices for later phases of deployment. That is why training continues to anchor the revenue base even as inference volumes grow faster. In revenue terms, the AI accelerator cluster market still relies heavily on the scale and cost of training environments.

Inference is projected to grow at 17.26% CAGR from 2026 to 2031, and that makes it the fastest-growing function in the AI accelerator cluster market size. This reflects the spread of production AI use cases where ongoing query volumes, agent-based workflows, and enterprise automation require dedicated serving infrastructure. Dell's record of more than 4,000 AI Factory customers by 2025 supports the view that enterprise inference build-outs are no longer limited to early adopters. Inference also changes hardware economics, because buyers care more about throughput-per-watt and throughput-per-dollar than they do about peak training performance. That shift gives the AI accelerator cluster market a wider set of future architecture paths, especially for specialized serving workloads.

By Deployment Model: Cloud Keeps The Largest Position While Hybrid Gains Momentum

Cloud-based deployments captured 64.24% share in 2025, which kept them as the largest deployment model in the AI accelerator cluster market size. Their advantage came from access to pooled accelerator capacity, managed orchestration, geographic redundancy, and easier burst support for variable workloads. Large cloud operators also continue to benefit from earlier procurement, better supply access, and broader integration capabilities across system layers. This makes the cloud especially attractive for training workloads and for enterprises that do not want to build full facility support in-house. The AI accelerator cluster market, therefore, still relies on cloud scale as its main deployment base.

Hybrid deployments are projected to grow at 17.56% CAGR from 2026 to 2031, which makes them the fastest-growing model in the AI accelerator cluster market. This reflects a practical operating pattern, where enterprises keep sensitive inference tasks on dedicated local systems while sending training or short-term overflow work to the cloud. That approach helps buyers balance cost, compliance, and utilization without locking every workload into a single environment. On-premises deployments remain important in defense, financial services, and life sciences, but hybrid is gaining ground because it matches the real split between controlled data and elastic compute demand. As the AI accelerator cluster market matures, hybrid design is likely to become a standard structure for buyers that need both local control and scalable external capacity.

By End User: Hyperscalers Dominate Spending While Public Programs Add New Demand

Hyperscale cloud service providers accounted for 63.48% of revenue in 2025, which made them the leading end-user group in the AI accelerator cluster market. Their role extends beyond direct purchases, because their buying decisions shape memory allocation, packaging schedules, and network equipment planning across the supply chain. This also gives them stronger leverage in vendor selection and road map alignment than most other customer groups. Enterprises remained the second-largest group, and their position improved as dedicated inference economics became more attractive. As a result, the AI accelerator cluster market still takes its baseline direction from hyperscaler procurement behavior.

Government and research institutions are projected to grow at 17.37% CAGR from 2026 to 2031, which makes them the fastest-growing end-user group in the AI accelerator cluster market. EuroHPC selected 19 AI Factory consortia across more than 20 member states between December 2024 and October 2025, which shows how public programs are building a more independent demand pipeline. This matters because sovereign compute programs are often guided by control, access, and national capability rather than short-term cloud pricing. Telecommunications providers and colocation companies are also starting to play a more visible role by offering managed GPU infrastructure to mid-market buyers. Together, these shifts show that the AI accelerator cluster industry is broadening its end-user mix even while hyperscalers remain the largest buyers.

Geography Analysis

North America held 52.64% of the AI accelerator cluster market share in 2025, which kept it as the largest regional market. The region benefits from the concentration of hyperscaler headquarters, mature data center corridors, and a deep pool of frontier AI development activity. It also has a strong base of value-chain companies across accelerators, servers, networking, and systems integration. At the same time, grid readiness has become a real constraint for new large-scale deployments, and policy attention around data centers and power access has increased. Texas Senate Bill 6, enacted in June 2025, was designed to streamline parts of the ERCOT large-load interconnection process and clarify how utility upgrade costs are handled for new demand.

Asia-Pacific is projected to expand at 17.22% CAGR from 2026 to 2031, which makes it the fastest-growing regional part of the AI accelerator cluster market. Growth in the region reflects a mix of domestic Chinese capacity buildout, public support for compute infrastructure, and stronger interest in power-rich deployment corridors. Huawei stated that its Ascend 950PR entered commercial deployment in 2026, and it also highlighted the Shenzhen Ascend cluster as a fully indigenous 14,000-card installation that went live in March 2026. That development shows how export-control pressure is pushing regional ecosystems to deepen domestic capability rather than step back from expansion. The region is therefore becoming more important to the AI accelerator cluster market not only because it is growing quickly, but also because it is forming more distinct local supply and deployment paths.

Europe held a meaningful position in the AI accelerator cluster market in 2025, with demand shaped more by sovereignty goals than by stand-alone hyperscaler expansion. The Franco-German joint paper on digital sovereignty in June 2026 called for a stronger European technology package and targeted a 30-50% sovereign compute share for public-sector workloads by 2027 and 2028. EuroHPC's AI Factory selections are reinforcing that direction by creating a coordinated public infrastructure base across the region. South America and the Middle East and Africa remained smaller markets, but sovereign investment and infrastructure diversification efforts are gradually making them more relevant to the wider AI accelerator cluster market.

Competitive Landscape

The AI accelerator cluster market remains concentrated at key control points, even though the broader stack includes many system, software, and networking participants. NVIDIA kept a strong position through its rack-scale platform strategy, which moved beyond chip supply and into validated factory infrastructure, ecosystem coordination, and production depth. That approach matters because buyers in the AI accelerator cluster market increasingly prefer integrated solutions that reduce qualification time across compute, cooling, and interconnect layers. Memory supply also remains highly concentrated, which reinforces the advantage of vendors that can secure long-term component access. As a result, competition in the AI accelerator cluster market is strong, but the ability to execute at scale is still concentrated among a limited group of firms.

A second strategic pattern in the AI accelerator cluster market is the split between integrated platform vendors and open ecosystem participants. Dell, HPE, and Supermicro continue to compete by offering pre-validated system architectures that combine compute, networking, storage, and liquid cooling into deployable rack-scale designs. NVIDIA reinforced this model in May 2026 when Vera Rubin entered full production through a broad manufacturing network. AMD and Meta also expanded their strategic partnership for 6 GW of AMD GPUs, using a custom MI450-based platform and the Helios rack-scale architecture. Dell then confirmed production shipments of liquid-cooled PowerEdge XE9812 rack systems with NVIDIA Vera Rubin NVL72 to CoreWeave in March 2026. These moves show that strategic advantage in the AI accelerator cluster market now depends as much on delivery form and integration depth as on component performance.

Regulation is also shaping competition in the AI accelerator cluster market. The U.S. Bureau of Industry and Security issued guidance in May 2026 that reinforced license requirements for advanced computing items tied to restricted entities, regardless of end destination in certain cases. That raises compliance risk for vendors with globally distributed sales and support models, and it supports the emergence of more region-specific compute ecosystems. At the same time, partnerships such as NVIDIA and SK hynix on next-generation memory show that supply-chain coordination is becoming a competitive tool in its own right. The AI accelerator cluster market is therefore consolidating around firms that can combine hardware scale, supply assurance, system integration, and regulatory adaptability.

AI Accelerator Cluster Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Alphabet Inc.

Amazon.com, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: AMD and Rackspace Technology signed a definitive agreement for the phased deployment of an initial 30 MW of AMD-based AI compute across Rackspace's global data centers, beginning in late 2026 through 2028, establishing AMD as Rackspace's strategic silicon partner at the infrastructure layer.

- May 2026: NVIDIA's Vera Rubin platform ramped into full production, with 150 supply-chain partners across 350+ factories and 30 countries shipping rack-scale systems, including Dell Technologies, HPE, Lenovo, and Supermicro, marking the transition from Blackwell to the third-generation MGX rack-scale AI factory architecture.

- May 2026: AMD announced over USD 10 billion in investments across the Taiwan ecosystem to expand advanced packaging capacity and accelerate deployment of the AMD Helios rack-scale platform, with leading ODM partners including Wiwynn, Wistron, and Inventec ramping AMD Instinct MI450X-based systems for the second half of 2026.

- May 2026: AMD and Meta Platforms announced an expanded strategic partnership to deploy 6 GW of AMD GPUs, the first deployment using a custom AMD Instinct MI450-based GPU optimized for Meta's workloads, with initial shipments scheduled for the second half of 2026 using the AMD Helios rack-scale architecture co-developed through the Open Compute Project.

Global AI Accelerator Cluster Market Report Scope

The AI Accelerator Cluster Market refers to the market for interconnected groups of AI accelerators deployed together to train and run large AI models at high speed and scale. It includes GPU, NPU, and ASIC-based clusters used in data centers, cloud platforms, and enterprise AI infrastructure to handle demanding workloads such as generative AI, deep learning, and large-scale inference.

The AI Accelerator Cluster Market Report is Segmented by Component (Compute Infrastructure, Networking Infrastructure, Storage Infrastructure, Cluster Management Software, and Services), Accelerator Architecture (GPU-Based Clusters, TPU-Based Clusters, FPGA-Based Clusters, Custom AI ASIC-Based Clusters, Heterogeneous Accelerator Clusters), Cluster Size (Up to 256 Accelerators, 257–2,048 Accelerators, 2,049–16,384 Accelerators, and Above 16,384 Accelerators), Function (Training, and Inference), Deployment (Cloud, On-Premises, and Hybrid), End User (Hyperscale Cloud Service Providers, Enterprises, Government and Research, Institutions, Telecommunications Providers, Colocation Service Providers), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Compute Infrastructure |

| Networking Infrastructure |

| Storage Infrastructure |

| Cluster Management Software |

| Services |

| GPU-Based Clusters |

| TPU-Based Clusters |

| FPGA-Based Clusters |

| Custom AI ASIC-Based Clusters |

| Heterogeneous Accelerator Clusters |

| Up to 256 Accelerators |

| 257-2,048 Accelerators |

| 2,049-16,384 Accelerators |

| Above 16,384 Accelerators |

| Training |

| Inference |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Hyperscale Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| Telecommunications Providers |

| Colocation Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | Compute Infrastructure | |

| Networking Infrastructure | ||

| Storage Infrastructure | ||

| Cluster Management Software | ||

| Services | ||

| By Accelerator Architecture | GPU-Based Clusters | |

| TPU-Based Clusters | ||

| FPGA-Based Clusters | ||

| Custom AI ASIC-Based Clusters | ||

| Heterogeneous Accelerator Clusters | ||

| By Cluster Size | Up to 256 Accelerators | |

| 257-2,048 Accelerators | ||

| 2,049-16,384 Accelerators | ||

| Above 16,384 Accelerators | ||

| By Function | Training | |

| Inference | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End User | Hyperscale Cloud Service Providers | |

| Enterprises | ||

| Government and Research Institutions | ||

| Telecommunications Providers | ||

| Colocation Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the AI accelerator cluster market in 2026?

The AI accelerator cluster market was valued at USD 76.25 billion in 2026 and is forecast to reach USD 166.27 billion by 2031 at a 16.87% CAGR.

Which component generates the most revenue in AI accelerator clusters?

Compute infrastructure led the revenue mix with a 70.46% share in 2025, showing that hardware systems still absorb the largest portion of spending.

Why are inference deployments becoming more important for cluster vendors?

Inference is projected to grow at 17.26% through 2031, and enterprise buyers are increasingly adopting dedicated systems for production use, cost control, and data handling.

Which deployment model is growing the fastest?

Hybrid deployments are expected to record the fastest growth at 17.56% through 2031 as enterprises balance local control with cloud scalability.

Which region leads current demand and which one is growing fastest?

North America held 52.64% share in 2025, while Asia-Pacific is projected to grow the fastest at 17.22% through 2031.

What is the biggest operational challenge for new AI cluster deployments?

Power and cooling remain the main operational constraint, because high rack densities and liquid cooling needs raise facility costs and can delay deployment schedules.

Page last updated on: