AI Accelerators Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 174.69 Billion |

| Market Size (2031) | USD 518.12 Billion |

| Growth Rate (2026 - 2031) | 24.30% CAGR |

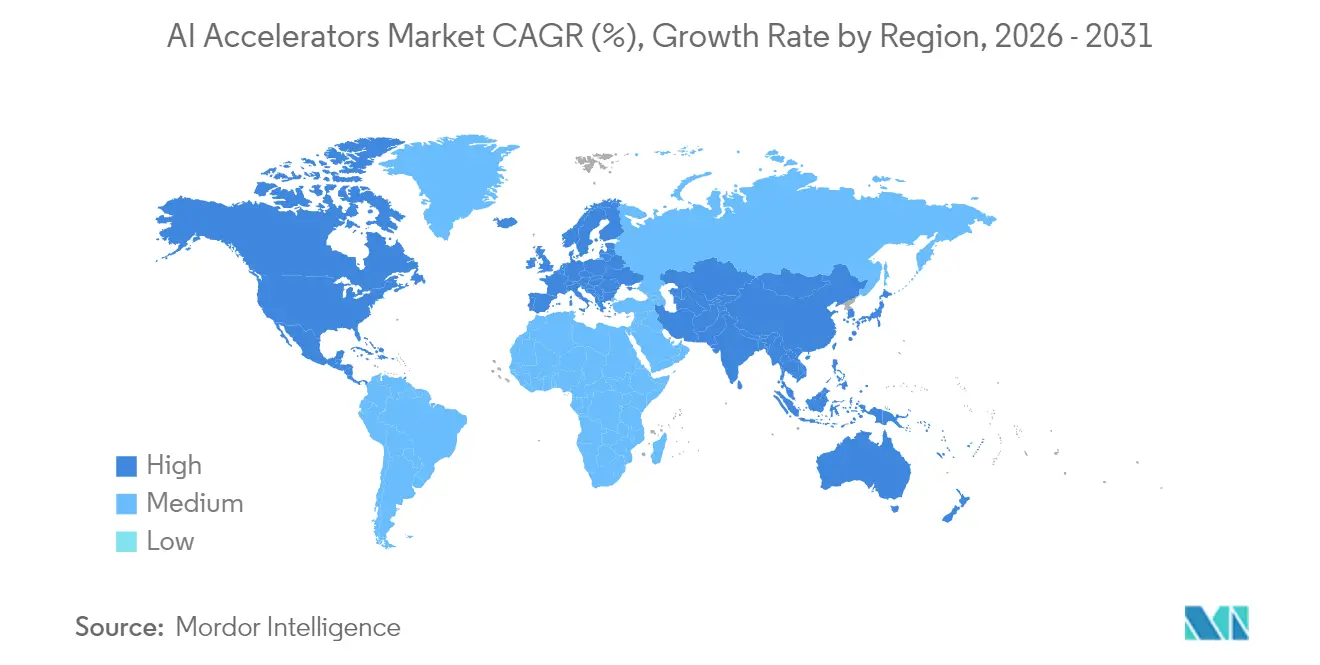

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Accelerators Market Analysis by Mordor Intelligence

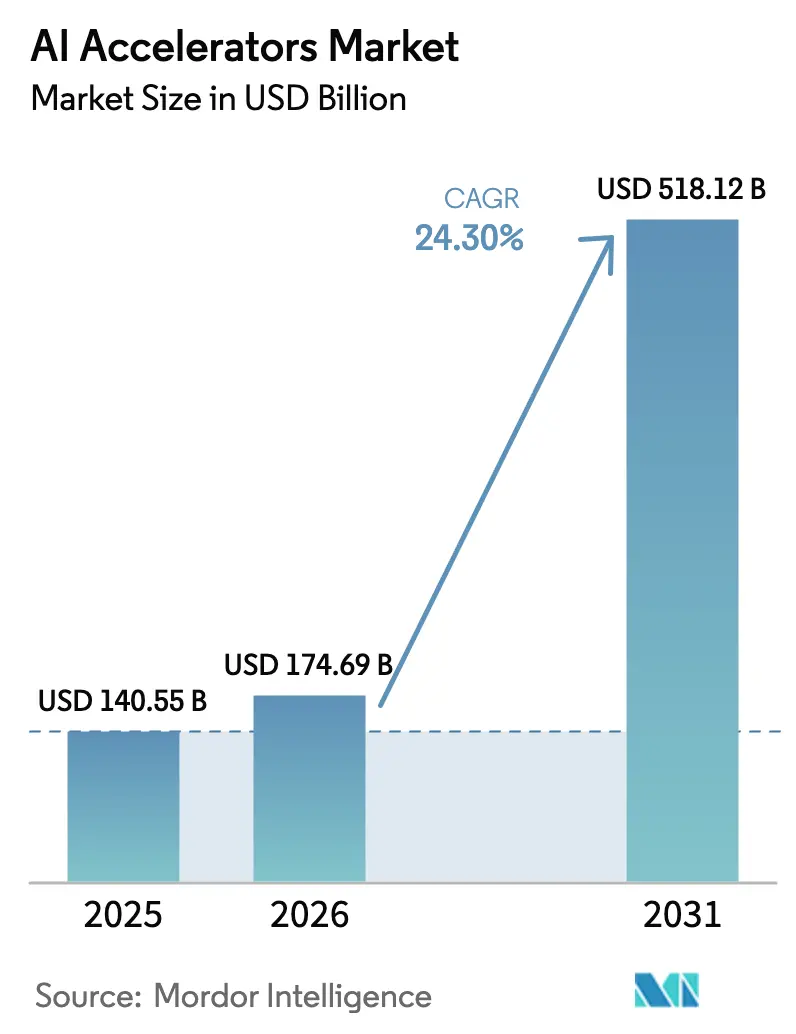

The AI accelerators market size is expected to grow from USD 140.55 billion in 2025 to USD 174.69 billion in 2026 and is forecast to reach USD 518.12 billion by 2031 at 24.30% CAGR over 2026-2031. This exceptional growth reflects hyperscale demand for generative-AI compute, aggressive semiconductor capital spending, and rapid architectural shifts favoring high-bandwidth memory and advanced packaging. North America retained leadership through concentrated cloud deployments, while Asia-Pacific delivered the fastest unit growth as Chinese electric-vehicle (EV) makers and South Korean chip firms pushed proprietary silicon. Custom application-specific integrated circuits (ASICs) are gaining ground as operators seek lower total cost of ownership, yet graphics processing units (GPUs) continue to dominate early-stage training because of their versatile software ecosystem [1]Center for Strategic and International Studies, “The AI Power Surge: Growth Scenarios for GenAI Datacenters Through 2030,” csis.org . Supply-chain constraints in advanced packaging and high-bandwidth memory, together with rising data-center power densities, are reshaping facility design and regional investment priorities.

Key Report Takeaways

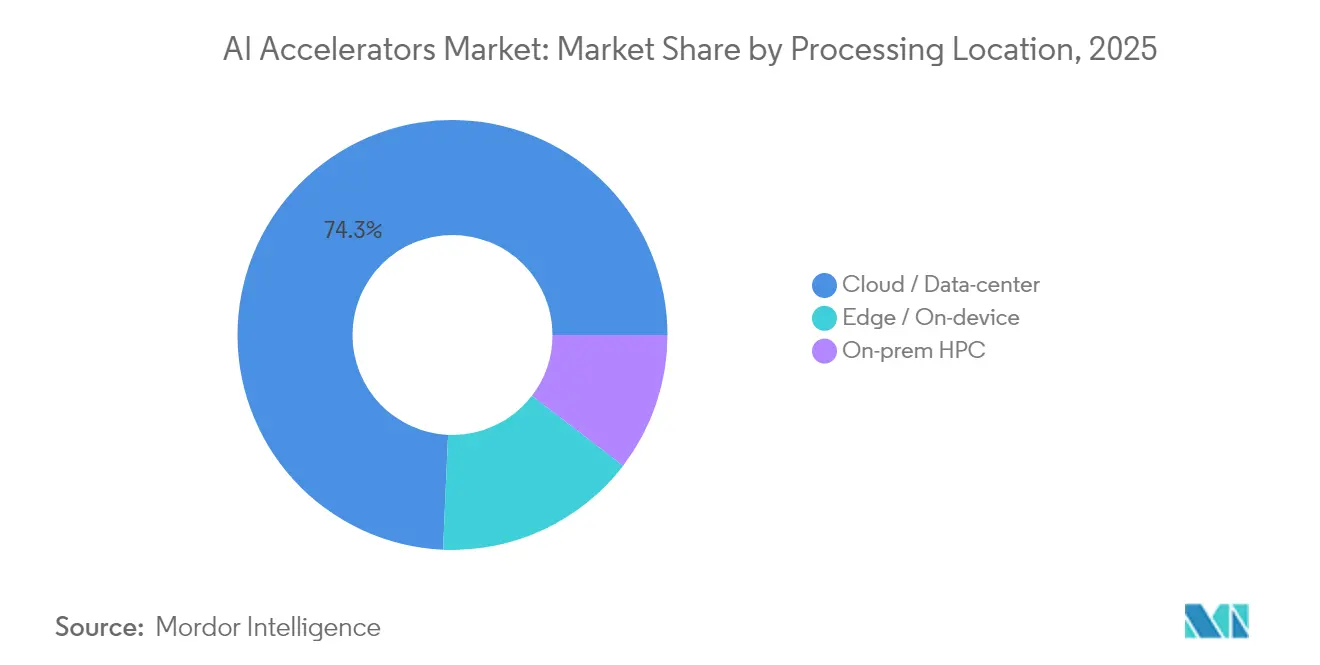

- By processing location, cloud/data-center deployments captured 75% of the AI accelerators market share in 2024, whereas edge/on-device solutions are advancing at a 27% CAGR to 2030.

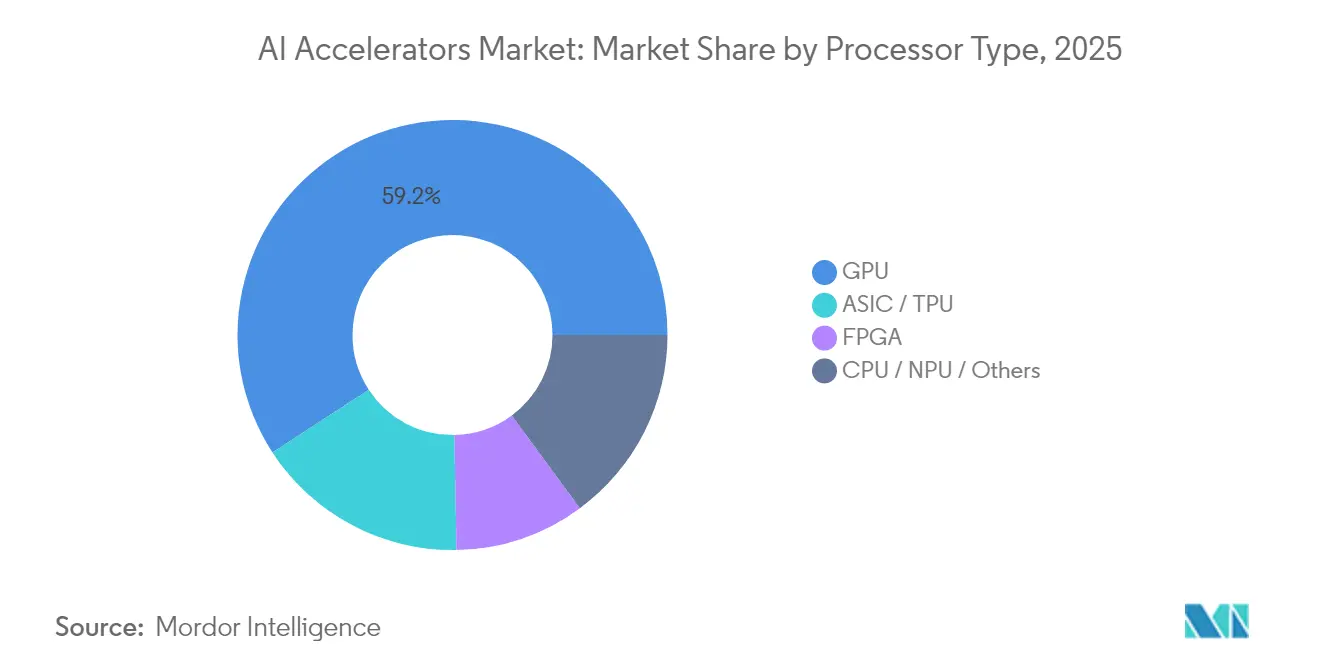

- By processor type, GPUs led with 60% revenue share in 2024; ASICs are projected to grow at a 28% CAGR through 2030.

- By function, training applications accounted for 58% of the AI accelerators market size in 2024, while inference is rising at a 27% CAGR during the same horizon.

- By end-user industry, hyperscale cloud service providers held 53% share of the AI accelerators market size in 2024, whereas automotive OEMs and Tier-1 suppliers are expanding at a 26% CAGR to 2030.

- By geography, North America commanded a 44% share in 2024, and Asia-Pacific is exhibiting the highest growth at a 28% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI Accelerators Market Trends and Insights

Drivers Impact Analysis Table*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI compute demand in hyperscale data centers | +8.5% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Chiplet and advanced-packaging breakthroughs | +4.8% | Taiwan, South Korea, United States | Medium term (2-4 years) |

| Growth of low-power edge accelerators for automotive and health | +6.2% | Global, strongest in automotive clusters | Long term (≥ 4 years) |

| Government incentives for domestic AI-silicon fabrication | +3.7% | United States, Europe, Japan, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Demand for Generative-AI Compute in Hyperscale Data Centers

Hyperscale operators are scaling to hundreds of thousands of high-end GPUs per campus to support both model training and 24-7 inference. Industry forecasts indicate the installed base may reach 6.5–7 million units annually by 2025, lifting power requirements toward 84 GW, or roughly one additional U.S. state’s present-day grid load [CSIS.ORG]. Sustained demand has driven NVIDIA’s data-center revenue from USD 110 billion in 2024 to an expected USD 173 billion in 2025, reinforcing the importance of supply security and driving unprecedented investment in advanced packaging capacity.

Proliferation of Edge AI Devices Needing Low-Power Accelerators

Automotive and healthcare platforms require sub-20 millisecond latency and stringent data-sovereignty compliance, prompting a shift toward on-device inference. The automotive AI chipset market is projected to reach USD 14.68 billion by 2034, growing at 20% annually, while the U.S. Food and Drug Administration has cleared 950 AI-enabled medical devices since tracking began, up 15% in the first half of 2024. New solutions such as Telechips’ A2X deliver 200 TOPS within integrated system-on-chip packages, signaling a clear path toward cost-efficient, localized intelligence.

Chiplet & Advanced-Packaging Breakthroughs Boosting Memory Bandwidth

Heterogeneous chiplet architectures are overcoming the memory wall that limits AI throughput. Universal Chiplet Interconnect Express (UCIe) enables multi-vendor die-to-die links, and 3.5D assemblies from industry leaders integrate more than 6,000 mm² of silicon in one package.[2]Nature Electronics, “High-Performance, Power-Efficient Three-Dimensional System-in-Package Designs with UCIe,” nature.com When combined with high-bandwidth memory, these designs lift bandwidth density well beyond the trajectory of conventional monolithic scaling.[3]IBM Research, “Meeting the Explosive Demands of AI with Chiplet Architectures,” ibm.com

Government CHIPS-Style Incentives for Domestic AI-Silicon Fabs

The U.S. CHIPS and Science Act earmarked USD 52.7 billion in direct support, triggering more than USD 540 billion in announced private-sector projects and establishing a 25% investment tax credit for advanced manufacturing. Comparable programs in Japan, Europe, and India are accelerating regional capacity build-outs while introducing “guardrails” that limit expansion in sensitive jurisdictions, permanently altering foundry decision making.

Restraints Impact Analysis Table*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-5 nm wafer shortages | −4.2% | Taiwan, South Korea, United States | Short term (≤ 2 years) |

| Escalating total cost of ownership for liquid-cooled clusters | −3.1% | Global hyperscale markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

<5 nm Wafer Shortages Throttling Shipment Volumes

Even after process ramp-ups, leading-edge wafer demand exceeds supply. TSMC’s monthly 3 nm output is expected to reach 125,000 wafers in the second half of 2025, yet competing orders from consumer electronics and data-center firms sustain a sellers’ market that keeps wafer prices near USD 21,000[6]Taiwan Semiconductor Manufacturing Company, “Advanced Node Capacity Update,” tsmc.com . Limited alternative capacity prolongs delivery lead-times and raises the capital intensity of new AI designs.

Escalating TCO of Liquid-Cooled GPU Clusters

Next-generation accelerators exceed 1,000 W per device, pushing rack densities beyond 140 kW and making liquid cooling indispensable. Adoption reached 10% of hyperscale racks by late 2024 and continues to rise as existing mechanical-electrical infrastructure struggles to dissipate heat efficiently[5]TrendForce, “Liquid Cooling Penetration Expected to Reach 10% by Late 2024,” trendforce.com . Operators face additional costs for coolant distribution, leak detection, and specialized maintenance, which together slow the pace of datacenter rollout in power-constrained regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processor Type: GPUs Retain Leadership while ASICs Accelerate

GPUs held 59.20% revenue share of the AI accelerators market in 2025. Their broad software ecosystem, epitomized by CUDA, keeps them indispensable for research and early-stage development. The AI accelerators market size for ASICs is projected to expand at a 27.15% CAGR, reflecting bespoke designs by hyperscalers seeking energy and cost efficiency during steady-state inference. Vendor roadmaps show cloud operators increasing internal tape-outs and committing foundry volume to proprietary silicon. Field-programmable gate arrays (FPGAs) remain attractive where reconfigurability offsets lower peak throughput, notably for evolving edge workloads. CPU/NPU hybrids address cost-sensitive consumer devices through tight integration of host processing, security engines, and neural cores, broadening merchant supplier opportunities.

Momentum toward ASICs is reshaping capital allocation. Broadcom anticipates a USD 60–90 billion ASIC opportunity by 2027, and internal TPUs, Tranium, or Inferentia devices increasingly enter production clusters. Continued GPU primacy is therefore expected in training-intensive research, yet a structurally higher share of inference spend will migrate to ASICs as compiler maturity, open-source toolchains, and software abstractions progress. The resulting mixed-architecture environment favors suppliers capable of delivering unified toolchains across heterogeneous hardware targets.

By Processing Location: Clouds Dominate yet Edge Gains Speed

Cloud and colocation facilities accounted for 74.30% of 2025 spending, underpinned by economies of scale and better access to sub-5 nm wafers. Nevertheless, edge delivery is surging at a 26.20% CAGR as automotive autonomy, point-of-care health diagnostics, and privacy regulation require local inference. The AI accelerators market now supports a two-tier model in which centralized training is complemented by distributed inference, enabling application developers to minimize latency while relieving bandwidth stress. On-premises high-performance computing (HPC) clusters retain importance for financial-services firms and national laboratories that must control data and ensure deterministic latency.

Automotive OEMs illustrate the edge inflection. NVIDIA’s Orin and Thor product timelines prompted Chinese brands to bolster internal silicon programs, and Korean vendors are aligning packaging roadmaps with vehicle-grade temperature and safety standards. Healthcare follows a similar arc as diagnostic imaging vendors embed AI pipelines directly into scanners, avoiding cloud round-trips that would compromise workflow efficiency or patient privacy.

By Function: Training Leads, Inference Surges

Training consumed 57.30% of 2025 revenue, mirroring the heavy computational cost of frontier model creation. As those models commercialize, inference dollars will climb faster, achieving a 26.10% CAGR through 2031. The AI accelerators market size devoted to inference benefits from ASIC designs that trade numerical precision for power efficiency. In practice, inference workloads require sustained but lower-latency compute, which aligns with accelerator architectures emphasizing memory bandwidth over raw floating-point density. Emerging devices claim an order-of-magnitude watt-per-token improvement over flagship GPUs, underscoring the economic logic behind the shift.

The transition alters buying patterns. Enterprises once focused on maximum training throughput now emphasize cluster utilization rates, compiler support, and inference orchestration middleware. Benchmarks therefore extend beyond TOPS or FLOPS to include time-to-first-token and total cost per generated output. Suppliers responding with vertically integrated hardware-software stacks are winning pilots that convert rapidly into multiyear commitments, solidifying revenue visibility.

By End-User Industry: Hyperscalers Anchor Demand, Autos Accelerate

Hyperscale cloud providers controlled 52.40% of spending in 2025, a consequence of their massive public-cloud fleets and internal product pipelines. Each new generative-AI feature release—from search to office productivity—pulls additional accelerator capacity into service level agreements that target single-digit millisecond response times. Cloud vendors are simultaneously investing billions in proprietary chips to reduce dependence on merchant devices and compress operating costs.

Automotive manufacturers represent the fastest-growing buyer group, expanding at a 25.30% CAGR. The sector’s Valley-style product refresh cycles drive continuous hardware demand, from level-2+ advanced driver assistance to full self-driving ambitions. NVIDIA commanded roughly 30% of the global ADAS compute market in 2024, but Chinese suppliers such as Horizon Robotics, Huawei, and new Korean entrants are eroding that share through cost-optimized, ASIL-compliant products. Healthcare follows closely as the surge in AI-enabled imaging catapults clinical-grade inference into routine practice. Financial-services and telecom segments round out demand through low-latency trading strategies and AI-RAN rollouts, each requiring domain-specific accelerator tuning.

Geography Analysis

North America captured a 43.50% share of the AI accelerators market in 2025. Concentration of hyperscale cloud headquarters, venture funding depth, and CHIPS Act stimulants continue to channel both demand and fabrication capacity into the region. Ongoing investments in on-shore foundries, advanced packaging, and high-bandwidth-memory assembly are expected to diversify supply chains and mitigate geopolitical exposure.

Asia-Pacific posted the fastest growth, advancing at a 27.00% CAGR between 2025 and 2031. Chinese EV firms rapidly iterate proprietary automotive silicon, while South Korean consolidation—exemplified by the Rebellions-Sapeon merger—creates national champions able to negotiate lithography and packaging capacity. Taiwan’s dominance in sub-5 nm wafer output remains critical, though geopolitical risk elevates incentives for Japanese, Indian, and Singaporean facilities specializing in advanced memory test and assembly.

Europe holds a smaller but influential position, guided by stringent regulatory regimes and a robust automotive manufacturing base. The forthcoming AI Act, together with sustainability mandates, is nudging accelerator design toward transparency, energy efficiency, and lifecycle accountability. Meanwhile, Middle East and African countries are commissioning green-field data centers anchored by renewable-energy availability, laying groundwork for future regional growth once policy, skills, and connectivity mature.

Competitive Landscape

The AI accelerators market exhibits high concentration. NVIDIA retained about 80% of global training revenue in 2024 owing to CUDA lock-in, integrated software libraries, and a mature partner ecosystem. AMD widened its footprint through acquisitions of ZT Systems and Silo AI, which together add system-integration expertise and model-optimization talent that help close the gap with NVIDIA’s end-to-end stack[8]Advanced Micro Devices, “AMD Completes Acquisition of Silo AI,” amd.com . Google, Amazon, and Microsoft each deploy home-grown devices—TPU, Trainium, and Maia respectively—to internal workloads and to public-cloud tenants, subtly eroding merchant GPU dominance.

Specialists such as Groq, Cerebras, and Graphcore focus on niche architectures tailored to transformer inference, wafer-scale training, or sparse-tensor workloads. Their success hinges on compiler maturity and developer adoption. Edge-focused entrants—including Hailo, DeepX, and Axelera—pursue ultra-low-power designs priced well below USD 1 per TOPS, addressing the long-tail of embedded devices.

Competitive pressure is shifting toward holistic solutions that bundle hardware, orchestration software, and service layers. NVIDIA’s acquisition of Run:ai illustrates this pivot, embedding scheduling intelligence deep into the silicon value proposition and complicating competitors’ efforts to win share on price or performance alone. Regulatory scrutiny and open-source interoperability layers like ROCm and ZLUDA are broadening options for developers, though real switching remains inhibited by code-migration costs and ecosystem familiarity.

AI Accelerators Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc. (AMD) (Xilinx, Inc.)

Intel Corporation (Habana Labs Ltd.)

Google LLC

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: AMD acquired ZT Systems for USD 4.9 billion, broadening its data-center systems portfolio and accelerating delivery of integrated AI servers.

- August 2024: AMD completed the USD 665 million takeover of Silo AI, adding multilingual model-development capabilities.

- August 2024: Rebellions and Sapeon merged under government sponsorship to form a larger South Korean AI-semiconductor entity.

- May 2025: Telechips introduced the A2X automotive accelerator with 200 TOPS NPU performance, targeting global OEM programs.

- February 2025: Meta entered talks to acquire FuriosaAI as part of a USD 65 billion multiyear hardware investment plan.

- May 2025: Axelera AI raised USD 68 million to scale its RISC-V–based Metis edge-inference platform.

Global AI Accelerators Market Report Scope

| GPU |

| ASIC / TPU |

| FPGA |

| CPU / NPU / Others |

| Cloud / Data-center |

| Edge / On-device |

| On-prem HPC |

| Training |

| Inference |

| Hyperscale Cloud Service Providers |

| Enterprise & Colocation Data-centers |

| Automotive OEMs & Tier-1s |

| Healthcare & Life-sciences |

| Financial Services |

| Telecom & 5G Infrastructure |

| Other End user (Government, Cyber security, Manufacturing among others) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Australia & New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Processor Type | GPU | ||

| ASIC / TPU | |||

| FPGA | |||

| CPU / NPU / Others | |||

| By Processing Location | Cloud / Data-center | ||

| Edge / On-device | |||

| On-prem HPC | |||

| By Function | Training | ||

| Inference | |||

| By End-User Industry | Hyperscale Cloud Service Providers | ||

| Enterprise & Colocation Data-centers | |||

| Automotive OEMs & Tier-1s | |||

| Healthcare & Life-sciences | |||

| Financial Services | |||

| Telecom & 5G Infrastructure | |||

| Other End user (Government, Cyber security, Manufacturing among others) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Australia & New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the AI accelerators market in 2026?

The AI accelerators market size reached USD 174.69 billion in 2026 and is forecast to climb to USD 518.12 billion by 2031.

What is the projected growth rate for AI accelerator spending?

Aggregate spending is expected to advance at a 24.30% CAGR between 2026 and 2031.

Which processor type dominates current deployments?

GPUs command 59.20% of 2025 revenue thanks to their mature software ecosystem and versatility across workloads.

Why are ASIC-based accelerators gaining popularity?

Custom ASICs improve total cost of ownership for inference by offering higher power efficiency and lower unit cost than general-purpose GPUs.

Which region is expanding the fastest?

Asia-Pacific is growing at a 27.00% CAGR as Chinese EV makers and South Korean fabless firms scale proprietary AI silicon.

What is the biggest operational challenge facing data-center operators?

Rising power density above 140 kW per rack is driving mandatory adoption of liquid-cooling systems, adding cost and complexity to facility design.

Page last updated on: