Europe Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

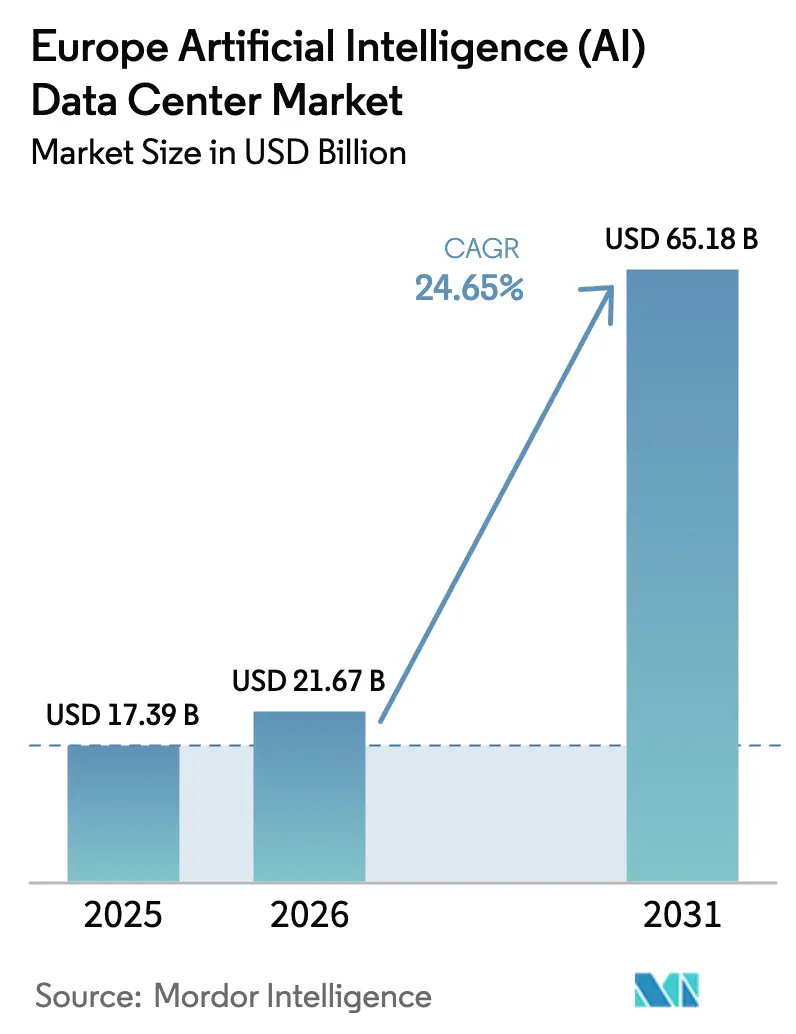

| Base Year Market Size (2025) | USD 17.39 Billion |

| Market Size (2026) | USD 21.67 Billion |

| Market Size (2031) | USD 65.18 Billion |

| Growth Rate (2026 - 2031) | 24.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The European artificial intelligence data center market size was valued at USD 17.39 billion in 2025 and estimated to grow from USD 21.67 billion in 2026 to reach USD 65.18 billion by 2031, at a CAGR of 24.65% during the forecast period (2026-2031). Growing public-sector mandates for digital sovereignty, moratoria in legacy hubs that reduce available capacity, and the rapid adoption of liquid cooling collectively accelerate capital investment, despite near-term power-grid constraints. Enterprises view dedicated sovereign AI clusters as the most reliable method for protecting intellectual property while meeting forthcoming EU AI Act requirements, so demand shifts from general-purpose cloud to purpose-built, high-density facilities. Operators with renewable power purchase agreements enjoy materially lower operating costs because AI training workloads consume three to five times more electricity per compute unit than historical enterprise software. Long-term supply–demand imbalances thereby create durable pricing power for incumbents, especially in Northern Europe, where abundant wind resources align with strict EU taxonomy rules.[1]European Commission, “EuroHPC Joint Undertaking Selects Hosting Entities for AI Factories,” digital-strategy.ec.europa.eu

Key Report Takeaways

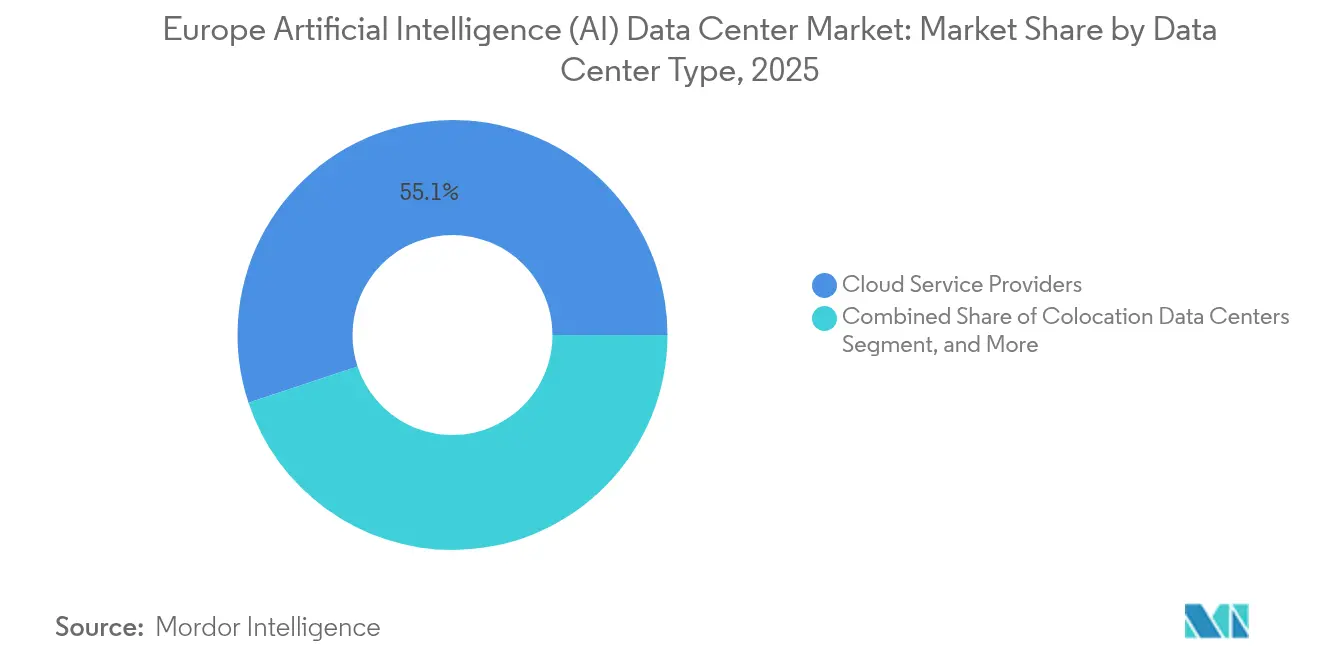

- By data center type, Cloud Service Providers led the European artificial intelligence data center market with 55.10% of the market share in 2025; Colocation facilities are expected to rise fastest at a 26.35% CAGR through 2031.

- By component, Software accounted for 45.10% of Europe's artificial intelligence data center market size in 2025; Hardware is poised to expand at a 25.9% CAGR to 2031.

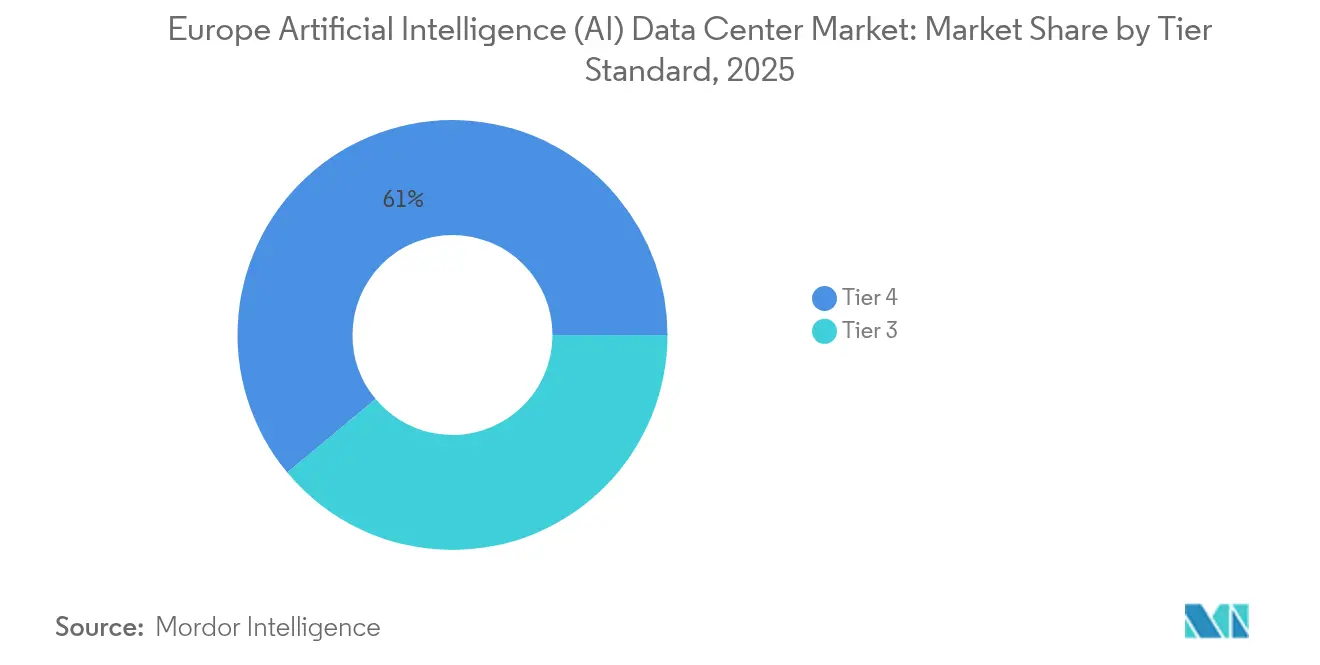

- By tier standard, Tier 4 facilities captured a 61.05% revenue share of Europe's artificial intelligence data center market in 2025, while Tier 3 deployments recorded the highest projected CAGR at 26.9% from 2025 to 2031.

- By end-user industry, IT and ITES held a 33.20% share of Europe's artificial intelligence data center market in 2025; the Internet and Digital Media sector is projected to advance at a 25.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe represents one dimension of a structure that spans multiple continents and economic zones. Our artificial intelligence (ai) data center market report covers details on that full global structure.

Europe Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Sovereign-AI Compute Clusters across EU Member-States | +4.8% | EU-wide, concentrated in FLAP-D markets | Medium term (2-4 years) |

| Accelerated Build-out of 400V Liquid-Ready White-Space in FLAP-D Markets | +3.2% | Frankfurt, London, Amsterdam, Paris, Dublin | Short term (≤ 2 years) |

| EU Green Deal and Carbon Border Adjustment Mechanism Driving Low-Carbon AI Power Sourcing | +2.1% | EU-wide with Nordic leadership | Long term (≥ 4 years) |

| Expansion of Offshore-Wind and Nuclear SMR Pipelines Enabling Carbon-Free AI Compute | +1.7% | Northern Europe, France, UK | Long term (≥ 4 years) |

| Availability of Horizon-Europe and IPCEI Grants for Exascale GPU Infrastructure | +1.4% | EU member states with research institutions | Medium term (2-4 years) |

| Rapid Uptake of AI-Driven Energy-Optimisation Platforms among European Colo and Cloud Operators | +1.2% | Major data center markets across Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Sovereign-AI Compute Clusters across Member States

European governments are funding indigenous computing to reduce their reliance on U.S. hyperscalers, deploying EuroHPC AI Factories that ensure national data residency and isolate classified workloads.[2]EuroHPC Joint Undertaking, “EuroHPC JU Selects Hosting Entities for AI Factories,” eurohpc-ju.europa.eu France earmarks EUR 500 million for sovereign clusters, and Germany’s IPCEI-CIS scheme adds direct capital grants for exascale facilities. Predictable multi-year offtake contracts emerging from these programs de-risk operator revenue and entice secondary-market entrants. The strategic narrative links compute capacity to economic competitiveness, so policy momentum is unlikely to reverse during the forecast window. Resulting procurement preferences accelerate bookings for operators that hold both security clearances and ISO 27001 certifications, which compress sales cycles for high-density halls.

Accelerated Build-out of 400V Liquid-Ready White Space in FLAP-D

Operators retrofit legacy halls with 400V power distribution and manifold systems that accept direct-to-chip and immersion cooling, eliminating protracted shutdowns required for later upgrades.[3]Equinix, “Equinix Completes 400V Infrastructure Upgrades Across Europe,” equinix.com Ready-made capacity enables enterprises to install NVIDIA H100 or AMD MI300X clusters within 45 days, significantly below the 120-day industry standard. Competitive barriers thus shift from location to electrical design as operators without 400V infrastructure face lost deals when procurement cycles tighten. Financing markets now quantify “liquid-ready” premiums in underwriting models, encouraging rapid regional rollouts. Early movers capitalize on ‘first-available’ advantages that translate into higher rack-density rents and extended contract durations.

EU Green Deal and Carbon Border Adjustment Mechanism

The carbon border levy creates a tangible price on Scope 2 emissions, so operators lock 10- to 15-year renewable PPAs to shield margins from future penalties. Microsoft’s 10.5 GW renewable portfolio in Europe demonstrates the scale at which larger buyers now hedge power exposure. Facilities in coal-intensive grids suffer a competitive disadvantage because AI training costs amplify even single-digit power-price differentials. Procurement teams now rank carbon-adjusted electricity rates above latency in site-selection matrices, steering new capacity toward Nordic and Iberian regions that feature abundant wind, hydro, and solar resources.

Expansion of Offshore Wind and Nuclear SMR Pipelines

WindEurope projects 111 GW of European offshore installations by 2030, and nascent SMR programs promise steady baseload creditable under the EU taxonomy. Data-center operators sign sleeved PPAs at source nodes, reducing transmission losses that erode renewable attributes. Long-term contracts provide revenue certainty to generation developers and lock competitive power pricing for AI workloads. Mixed portfolios combining intermittent wind and 24/7 nuclear output deliver both carbon-free and high-availability profiles required for large language model training.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Connection Moratoria in Amsterdam, Dublin and Frankfurt Hubs | -2.1% | Amsterdam, Dublin, Frankfurt metropolitan areas | Short term (≤ 2 years) |

| Severe Skills Gap in High-Density Liquid-Cooling Operations across CEE and Mediterranean Regions | -1.8% | Central and Eastern Europe, Southern Europe | Medium term (2-4 years) |

| Stringent EU Taxonomy and BREF Requirements Increasing Time-to-Permit for New Campuses | -1.3% | EU-wide, particularly new market entrants | Medium term (2-4 years) |

| High CAPEX of Two-Phase Immersion Retrofits in Legacy Tier III Sites | -0.9% | Established data center markets with aging infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Moratoria in Core Hubs

Amsterdam, Dublin, and Frankfurt municipalities have frozen new data-center power hookups until grid upgrades are completed, sidelining 2.5 GW of queued projects in Amsterdam alone. The policy inflates the asset values of existing high-density spaces and redirects new builds to secondary metropolitan areas, such as Madrid, Milan, and Warsaw, where grid headroom is still available. Hyperscalers grudgingly accept longer fiber backhauls or edge nodes to mitigate added latency. Short-run supply constraints temper the expansion of Europe's artificial intelligence data center market, yet they also raise unit pricing for commissioned megawatts, partially offsetting the lost volume.

Severe Skills Gap in High-Density Liquid-Cooling Operations

Two-phase immersion systems proliferate, but only a minority of technicians hold certifications in coolant chemistry or leak detection. Central and Eastern European sites rely on talent imports from Nordic countries, which elevates operating expenses and elongates commissioning timelines. The EC Digital Skills platform lists liquid cooling among its top workforce shortages; however, training capacity remains sparse outside of Germany and Sweden. Skills scarcity pushes operators toward turnkey solutions from specialized vendors, but this dependency narrows supplier choice and heightens integration risk, an implicit cost that restrains Europe's artificial intelligence data center market growth during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Momentum Narrows Cloud Lead

Europe's artificial intelligence data center market size for Cloud Service Providers totaled USD 9.58 billion in 2025, capturing the lion’s share because hyperscalers placed clusters close to financial exchanges and academic networks. Still, colocation facilities added leasing revenue at a 26.35% CAGR, shrinking the cloud premium as enterprises value physical control under GDPR mandates. Many European banks now deploy training nodes within leased suites that feature dedicated cages, encryption at rest, and customer-owned keys, keeping sovereign data onsite while benefiting from shared chilled-water loops.

Colocation’s economics benefit from 400V retrofits, which enable 60 kW racks without structural overhauls, allowing operators to monetize stranded white space faster than hyperscale builds that require greenfield land, new substations, and multi-year permitting cycles. Edge and enterprise segments remain niche, yet micro-data center rollouts inside 5G base stations drive inference workloads supporting autonomous transportation, industrial robotics, and smart city services. Secondary markets, such as Warsaw, see municipalities waive property taxes for edge enclosures that recycle waste heat into district grids, providing operators with incremental revenue through power-purchase credits.

By Component: Hardware Spending Surges as GPU Cycles Shrink

Software retained 45.10% of the European artificial intelligence data center market share in 2025, as firms initially invested in model orchestration layers and ML workflows. Hardware, though, will dominate incremental spending as GPU generations compress into twelve-month cycles, forcing continuous refresh to capture per-watt performance gains. Boards built around NVIDIA H100 and AMD MI300X require copper busbars, blind-mate liquid connectors, and reinforced floors, so capex intensity rises.

Rack-scale designs featuring compute-interconnect fabrics, such as NVLink switchless topologies, reduce latency and training time; however, they also require symmetrical power feeds and active rear-door heat exchangers. Uninterruptible-power-supply makers offer lithium-ion cabinets rated for 15-year lifespans, aligning with sustainability reporting requirements under EU taxonomy. Services revenue grows as system integrators bundle firmware tuning, cluster partitioning, and carbon-accounting dashboards that big banks and telcos now mandate.

By Tier Standard: Cost-Aware Workload Segmentation Gains Traction

Tier 4 halls generated 61.05% of the revenue in 2025, as model-training outages can jeopardize multimillion-dollar runs that can last for weeks. Operators integrate redundant pumps and looped manifolds to reach 99.995% availability, satisfying financial services regulators that equate downtime with systemic risk.

Tier 3 facilities, which post a 26.9% CAGR, rely on modular power-train blocks, enabling incremental expansion at sub-40 MW scales. Some providers market “Tier 3-plus” offerings with N+2 cooling but single utility feeds, striking a balance between expenditure and reliability. The approach lifts average revenue per kilowatt because customers pay tier-based surcharges according to workload criticality rather than flat rates.

By End-user Industry: Media Overtakes as Generative Content Scales

IT and ITES firms leveraged proprietary data to refine developer tools, securing a 33.20% revenue share in 2025. Yet Internet and Digital Media clients deliver the fastest 25.8% CAGR as text-to-video models and real-time personalization permeate streaming, retail, and social platforms. GPU cluster reservations doubled after 2024’s viral generative-music releases that demanded millisecond inference latency for consumer soundtracks.

Banks deploy transformer models for anti-money laundering alerts that reduce false-positive rates and lower compliance costs, but their unit densities remain moderate compared to media workloads. Healthcare pilots invest in image-segmentation algorithms for radiology reads, though regulation stretches production timelines. Manufacturing outfits are increasingly deploying edge AI nodes for defect detection, which feed centralized retraining loops in regional colocation hubs, thereby exploiting reduced data gravity. Government and defense bodies sign multi-year sovereign cloud agreements that stipulate EU citizenship for on-site personnel, locking incumbents into long-term contracts with stable power.

Geography Analysis

Frankfurt, London, Amsterdam, Paris, and Dublin collectively contribute about 64.20% of installed AI-ready megawatts, benefiting from carrier-dense campuses and subsea cable landings that lower latency to North America and Asia. Frankfurt leads due to Germany’s exporting industries and central location, but new sub-station approvals lag demand, so booked-but-unbuilt capacity lengthens delivery timelines. London retains gravitational pull from financial trading houses despite post-Brexit data-transfer regulations that complicate cross-border workloads.

Amsterdam and Dublin moratoria reroute pipeline projects toward Madrid, Milan, and Warsaw, which advertise available grid headroom and employer tax credits. Warsaw alone earmarks EUR 2.1 billion of National Recovery Plan funds for digital infrastructure grants, payable upon energization, to accelerate campus start-ups. Nordic markets harness free-air cooling and abundant hydropower; operators there quote power prices 40% below continental averages, enticing AI training clusters that prioritize opex over network latency. France surges on policy support that includes a EUR 4 billion Microsoft investment and two EuroHPC AI Factory awards, signaling the government's intent to anchor sovereign computing domestically. The United Kingdom pursues independent AI governance but remains intertwined with EU supply chains, so operators hedge by retaining dual compliance audits. Energy considerations increasingly outweigh metro preferences; projects adjacent to North Sea wind farm landing stations and French SMR sites receive expedited approvals because they contribute to national carbon targets. Consequently, Europe's artificial intelligence data center market experiences geographically diversified growth, which mitigates moratorium risk and stabilizes the overall CAGR.

Mordor Intelligence tracks the artificial intelligence (ai) data center market across other major regions such as Asia, Middle East and Africa, and North America, with additional country-level coverage spanning Spain, Netherlands, Germany, France, United Kingdom, and United Arab Emirates, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Europe's artificial intelligence data center market hosts a layered competitive field where silicon vendors, infrastructure suppliers, and facility operators converge. NVIDIA dominates high-end GPUs, but AMD’s MI300X series secures sovereign deployments by offering per-rack security modules favored by public-sector buyers. European challenger SiPearl collaborates with Arm to launch Rhea processors optimized for EuroHPC exascale nodes, injecting regional supply-chain resiliency.[4]SiPearl, “SiPearl Unveils Rhea Processor for European Exascale Computing,” sipearl.com

Power and cooling integrators Schneider Electric, Vertiv, and ABB differentiate through modular liquid-loop skids that shorten installation cycles. Niche players Submer Technologies and Iceotope specialize in immersion systems that lower PUE to near 1.05, capturing deals where carbon budgets supersede capex. Facility operators Equinix and Digital Realty scale via acquisitions; Equinix’s purchase of 150 MW in Frankfurt and Amsterdam instantly supplies 400V liquid-ready halls to latency-sensitive tenants.

Competition intensifies at the edge, where OVHcloud and Scaleway leverage sovereign credentials for public-sector workloads, undercutting U.S. hyperscalers on data-residency guarantees. Patent filings for liquid cooling have increased by 340% since 2022, illustrating technology arms races that raise barriers for entrants lacking significant R&D capabilities. Moratoria in Amsterdam and Dublin strengthen incumbent positioning by restricting new entrants to secondary metropolitan areas that lack equivalent connectivity. Overall, incumbents with integrated silicon-to-facility stacks hold the upper hand; however, white space exists in specialized edge and immersion-cooling niches where agile disruptors can thrive.

Europe Artificial Intelligence (AI) Data Center Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Arm Ltd.

Graphcore Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft announced a EUR 4 billion expansion of AI and cloud infrastructure across France, adding dedicated AI clusters to the Marseille and Lyon regions.

- January 2025: Submer Technologies has raised EUR 15 million in Series B funding to scale immersion-cooling systems for European AI data centers.

- December 2024: NVIDIA began rolling out the Blackwell architecture at EuroHPC sites in Barcelona and Jülich, quoting a 5× model-training performance gain compared to the H100.

- November 2024: Equinix closed a USD 500 million acquisition of three hyperscale centers in Frankfurt and Amsterdam, adding 150 MW of AI-ready capacity.

- November 2024: Iceotope partnered with Hewlett Packard Enterprise to integrate precision liquid cooling into HPE AI servers destined for European clients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Europe Artificial Intelligence-optimised Data Center market as all revenue earned inside purpose-built or retrofit facilities, hyperscale, colocation, enterprise, and edge, where racks, power and cooling are designed for GPU/AI accelerators, high-density networking, and AI-specific orchestration software. Values represent annual revenue realized by hardware, software, and service suppliers, expressed in constant 2024 USD.

Scope exclusion: Stand-alone on-premise HPC clusters housed outside commercial or colocation facilities are excluded.

Segmentation Overview

- By Data Center Type

- Cloud Service Providers

- Colocation Data Centres

- Enterprise / On-Premises / Edge

- By Component

- Hardware

- Power Infrastructure

- Cooling Infrastructure

- IT Equipment

- Racks and Other Hardware

- Software Technology

- Machine Learning

- Deep Learning

- Natural Language Processing

- Computer Vision

- Services

- Managed Services

- Professional Services

- Hardware

- By Tier Standard

- Tier 3

- Tier 4

- By End-user Industry

- IT and ITES

- Internet and Digital Media

- Telecom Operators

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Manufacturing and Industrial IoT

- Government and Defense

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Interviews with facility engineers, hyperscale procurement leads, and colocation sales heads across the U.K., Germany, France, the Nordics, and Iberia validated rack-density norms, average selling price (ASP) ranges, and grid-queue lead times, while an online survey of European CTOs provided adoption rates for AI inference versus training workloads.

Desk Research

We first mapped the installed AI-ready white-space using open-source build permits, Eurostat trade codes for GPUs/AI servers, and ENTSO-E grid-connection data, complemented by policy papers from the EU DG-ENER, Climate Neutral Data Centre Pact briefs, and national ICT associations such as Bitkom and techUK. Company 10-Ks, investor decks, and press releases revealed landed cost trends for liquid-cooling skids and 400 V busways. Consulted paid datasets such as D&B Hoovers (financials) and Dow Jones Factiva (deal flow) filled revenue splits for private operators. This list is illustrative; dozens of additional sources were screened to cross-check figures.

Market-Sizing & Forecasting

A top-down "AI load pool" model estimates 2024 baseline spend by reconciling trafficked GPU server imports with installed MW and typical USD/MW revenue conversion. It then corroborates totals through selective supplier roll-ups and channel ASPx volume checks. Key variables include:

Average rack density (kW) shift toward >75 kW liquid-cooled racks, GPU server import growth under CN 84715005, EU ETS carbon price trajectory influencing opex pass-through, grid-connection lead times in FLAP-D hubs versus emerging markets, and vacancy compression rates from CBRE/JLL quarterly trackers.

Five-year forecasts apply multivariate regression on these drivers, blended with scenario analysis for power-capex constraints, and gap-filled where operator-level data were sparse.

Data Validation & Update Cycle

Outputs pass variance screens against independent capacity tallies, followed by peer review and a senior analyst sign-off. Mordor refreshes the model annually; interim updates trigger when utility tariffs, major build announcements, or regulation (e.g. EU Energy Efficiency Directive) move the baseline materially.

Why Mordor's Europe Artificial Intelligence (AI) Optimised Data Center Baseline Commands Reliability

Published numbers often diverge because firms bundle different facility types, count capex instead of revenue, or freeze exchange rates at report launch dates.

Key gap drivers include broader "all data center" scopes, inclusion of non-AI racks, or one-off investment values. Mordor focuses only on revenue tied to AI-ready capacity, normalizes FX quarterly, and revisits grid-power constraints with each update.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.97 B (2024) | Mordor Intelligence | - |

| USD 47.23 B (2024) | Regional Consultancy A | Measures entire data center spend, mixes capex & opex |

| USD 53.8 B (2024) | Trade Journal B | Aggregates full facility revenue, lacks AI-specific filter, biennial refresh |

In sum, by isolating AI-driven demand signals, triangulating desk and field evidence, and refreshing every year, Mordor Intelligence delivers a balanced, decision-ready baseline that executives can track and replicate.

Key Questions Answered in the Report

What is the projected value of the Europe artificial intelligence data center market by 2031?

The market is forecast to reach USD 65.18 billion by 2031, driven by a 24.65% CAGR over 2026-2031.

Which data center type is growing fastest in this space?

Colocation facilities are expanding at a 26.35% CAGR because enterprises want hybrid models that combine physical control with hyperscale-like scalability.

How do grid-connection moratoria affect facility deployment?

Moratoria in Amsterdam, Dublin, and Frankfurt delay new power hookups, pushing new builds to secondary metros such as Madrid, Milan, and Warsaw and tightening supply in core hubs.

Why is liquid cooling critical for AI workloads?

GPUs like NVIDIA H100 generate heat loads beyond air-cooling limits; liquid cooling supports rack densities above 50 kW while lowering PUE near 1.05.

Which region offers the lowest power costs for AI training clusters?

Nordic countries deliver power prices about 40% below continental averages thanks to abundant hydro and wind resources, making them attractive for energy-intensive training.

What competitive advantage do sovereign cloud providers hold?

Providers such as OVHcloud comply with strict data-residency requirements, giving them an edge for government and regulated-industry AI workloads that cannot be hosted on U.S. hyperscalers.

Page last updated on: