Edge AI Accelerators Market Size and Share

Market Overview

| Study Period | 2025 - 2030 |

|---|---|

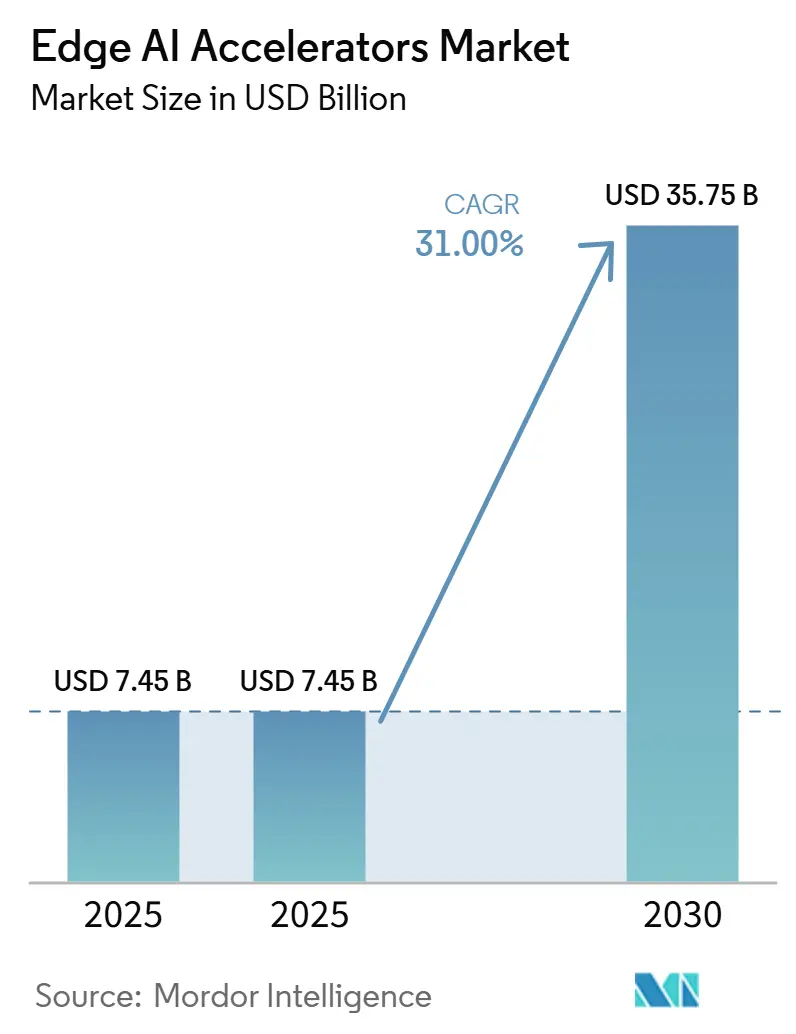

| Market Size (2025) | USD 7.45 Billion |

| Market Size (2030) | USD 35.75 Billion |

| Growth Rate (2025 - 2030) | 31.00% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edge AI Accelerators Market Analysis by Mordor Intelligence

The Edge AI Accelerators market size stood at USD 7.45 billion in 2024 and is projected to register a 31% CAGR, lifting the value to USD 35.75 billion by 2030. Sovereign AI regulations, falling $/TOPS, and widening 5G rollouts are pushing enterprises toward on-device inference that meets data-privacy mandates, trims cloud egress fees, and supports real-time decision loops. Hardware differentiation is shifting from general-purpose GPUs to application-specific architectures, while a tightening 5-10 W power envelope is becoming the design sweet spot for fanless industrial systems. Form-factor innovation ranges from system-on-chip (SoC) packages in high‐volume consumer devices to USB sticks that democratize inference for developers. Competitive intensity is sharpening as established fabs advance to 3 nm nodes to satisfy performance-per-watt targets that smaller foundries cannot match, opening consolidation opportunities among niche ASIC suppliers. Meanwhile, quantum-enhanced sensing and neuromorphic learning are creating fresh white-space for vendors able to certify deterministic sub-millisecond latency in safety-critical workflows.[1]Intel Corporation, “What Is Neuromorphic Computing?,” intel.com

Key Report Takeaways

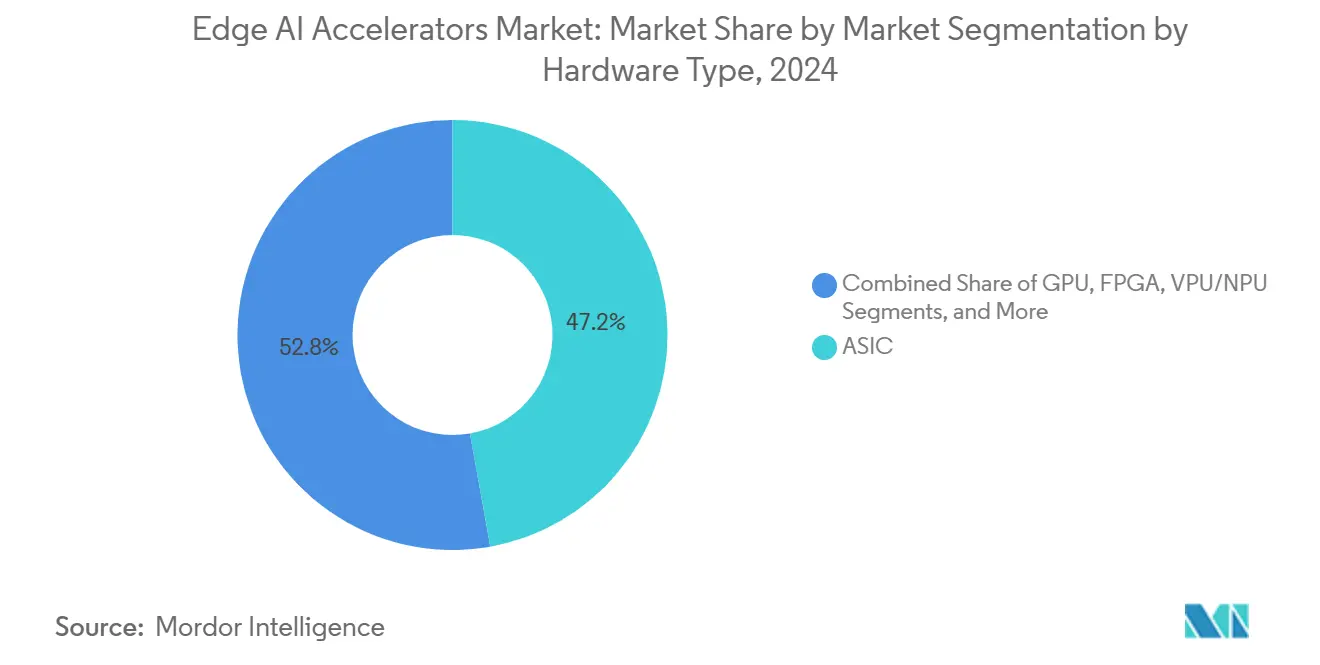

- By hardware type, ASICs led with 47.2% Edge AI Accelerators market share in 2024, while USB stick accelerators posted the fastest 29.23% CAGR through 2030.

- By power consumption envelope, the 5-10 W band accounted for 38.1% of the Edge AI Accelerators market size in 2024; sub-1 W devices are forecast to expand at a 28.7% CAGR.

- By form factor, SoCs captured 42% revenue share in 2024, yet USB sticks remain the fastest-growing at 29.23% CAGR.

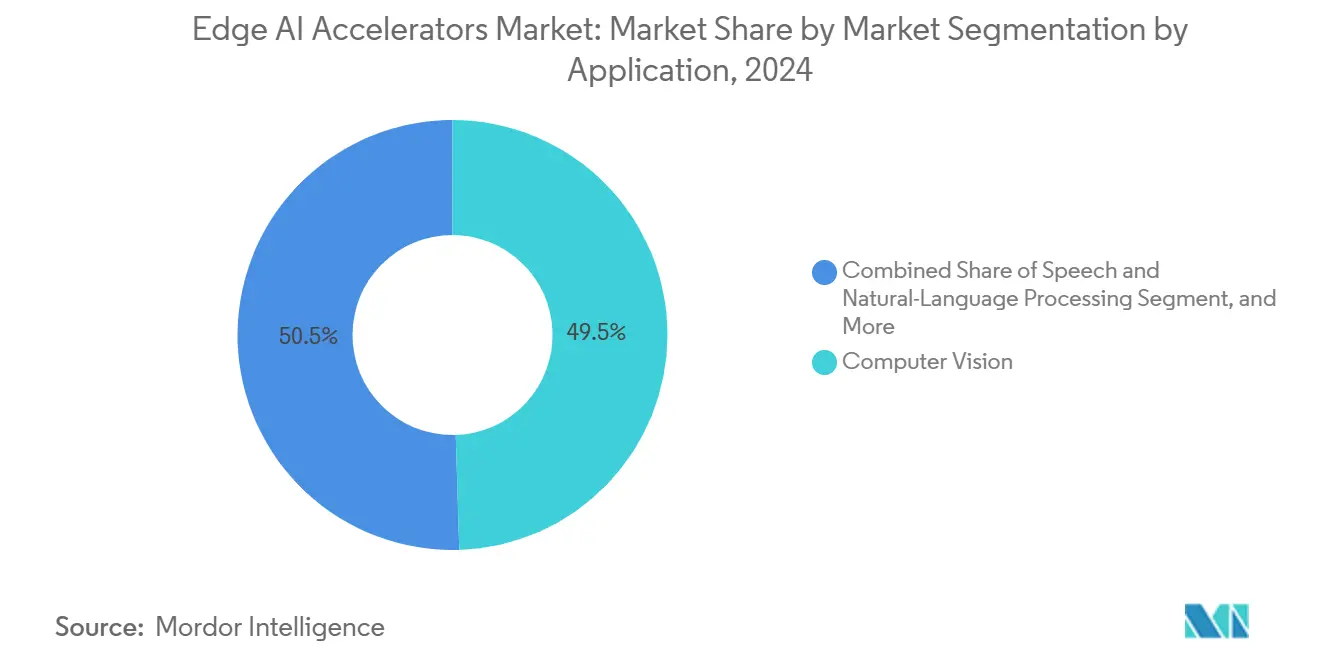

- By application, computer vision dominated with 49.5% revenue share in 2024; autonomous navigation is advancing at a 28.9% CAGR.

- By end-user industry, automotive held 31% share of the Edge AI Accelerators market size in 2024, while healthcare is set to post a 27.9% CAGR to 2030 following FDA clearance of 950 AI/ML devices in 2024.

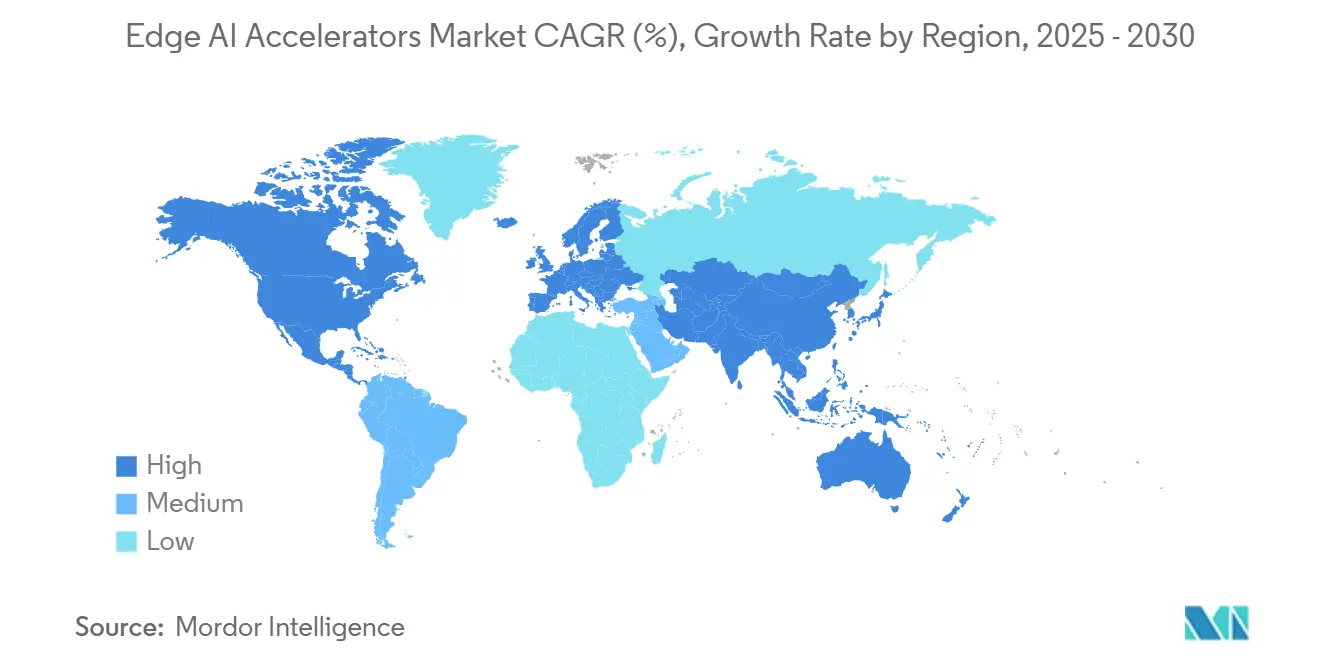

- By geography, North America commanded 40% revenue in 2024; Asia-Pacific is poised for a 29.88% CAGR that could overtake the region’s leadership by 2030 as it targets 62% of global semiconductor output.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Edge AI Accelerators Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of smart cameras and IoT devices | +8.5% | Global with APAC leadership | Short term (≤ 2 years) |

| Data-privacy regulations driving on-device inference | +7.2% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Falling USD/TOPS and improved performance-per-watt of edge ASICs | +6.8% | Global, concentrated in semiconductor hubs | Medium term (2-4 years) |

| Bandwidth and latency constraints in autonomous systems | +5.9% | North America, EU, with China expansion | Long term (≥ 4 years) |

| Emergence of TinyML frameworks on micro-controllers | +4.7% | Global with industrial focus | Short term (≤ 2 years) |

| Edge-native foundation models for multimodal AI | +3.9% | North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Smart Cameras and IoT Devices

Mass deployment of intelligent cameras in factories, traffic systems, and retail spaces is pushing inference to the edge. Sony’s IMX500 embeds a DSP inside the image sensor so frames are interpreted locally, slashing network traffic by up to 90% and shrinking decision latency below 10 ms.[2]Sony Semiconductor Solutions, “IMX500 Intelligent Vision Sensor,” sony-semicon.co.jp Multimodal references are rising as microphones and mm-wave radars piggyback on the same edge board, forcing accelerators to juggle vision, audio, and time-series workloads without exceeding 5-10 W.

Data-Privacy Regulations Driving On-Device Inference

The EU AI Act joins HIPAA and GDPR in demanding that patient, financial, and defense data stay on-premise. Edge-optimized silicon lets hospital imaging suites, bank branches, and municipal surveillance networks comply without sacrificing algorithmic sophistication. EdgeRunner AI ships air-gapped assistants that fine-tune large language models locally, eliminating cloud exposure and meeting zero-trust mandates for classified workloads.[3]EdgeRunner AI, “Company Overview,” edgerunnerai.com

Falling USD/TOPS and Improved Performance-Per-Watt of Edge ASICs

Selode’s 15 W Mother Box hits 308 INT8 TOPS, making each TOPS cost one-quarter of NVIDIA Jetson Orin prices on launch, while EdgeCortix taps TSMC 3 nm to pack extra SRAM close to compute for a 2.2× jump in energy efficiency.[4]EdgeCortix Inc., “SAKURA-II Product Brief,” edge-cortix.com As capital-intensive EUV lines amortize, price drops ripple into smart retail shelves and agricultural drones that once failed cost-benefit checks.

Edge-Native Foundation Models for Multimodal AI

Edge-tuned large language models prune parameter counts while retaining contextual grounding. Qualcomm’s AI Hub is shipping 4-billion-parameter multimodal models that execute at 15 W on the Snapdragon 8 Elite, enabling on-device captioning, translation, and anomaly detection despite no backhaul connectivity.[6]Qualcomm Technologies Inc., “Snapdragon 8 Elite Platform,” qualcomm.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented h/w-s/w ecosystem lengthens integration cycles | -4.20% | Global, acute for SMEs | Medium term (2-4 years) |

| Thermal management limits in fan-less designs | -3.80% | Global with high impact in industrial settings | Short term (≤ 2 years) |

| Higher unit economics vs. cloud GPU at scale | -3.30% | Global, most acute for high-volume AI deployments | Medium term (2-4 years) |

| Lack of standardized on-device AI benchmarks | -2.80% | Global, especially across heterogeneous edge AI ecosystems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Hardware-Software Ecosystem Lengthens Integration Cycles

The Edge AI Accelerators market wrestles with APIs split across CUDA, OpenVINO, TVM, and vendor-specific SDKs. Enterprises spinning up proofs of concept on a USB stick often face multi-month rewrites when migrating to a mezzanine card. Absence of uniform benchmarking complicates ROI sign-off, delaying volume orders, especially for mid-market OEMs with lean engineering staffs. Cross-vendor ONNX compliance is improving, yet device-level power-gating tactics still require hand-tuned kernels that lock customers into single-supplier roadmaps.[8]PIMIC, “Listen VL130 Product Datasheet,” pimic.ai

Thermal Management Limits in Fan-Less Designs

Edge inference nodes wedged into kiosks, camera poles, or AGVs must meet -40 °C to +85 °C ranges without fans that ingest dust or buzzy maintenance calls. Heat-flux spikes during transformer attention layers push hotspot temperatures past 100 °C in less than 200 ms, throttling performance unless exotic phase-change materials or Frore’s solid-state AirJet tiles are applied.[7]Frore Systems, “AirJet Solid-State Cooling Technology,” frore-systems.com Thermal budgets therefore cap model complexity, making quantization and sparsity essential for field-deployed resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hardware Type: ASICs Lead Performance Optimization

ASIC devices captured 47.2% Edge AI Accelerators market share in 2024, confirming a pivot from general-purpose compute toward domain-tuned logic that drives 4–7× gains in TOPS-per-watt. The segment promises a 25.4% CAGR to 2030 as design starts migrate to 3 nm where SRAM proximity slashes DRAM fetch penalties. GPUs remain vital in software-first prototyping venues, yet they cede volume deployments to inference-only cores that deliver deterministic latency. FPGAs keep a niche in aerospace where reconfigurability outweighs unit cost. Neuromorphic chips such as Intel Loihi 2 run constraint-satisfaction workloads at 37× lower energy than CPUs.[9]Ambarella Inc., “CV3-AD SoC Family,” ambarella.com

Performance-densities favor ASICs for surveillance NVRs, smart-factory PLCs, and in-cab driver monitoring. Meanwhile, the Edge AI Accelerators market size attached to brain-inspired silicon forecasts a 34% CAGR because event-driven spiking networks fire only when a signal arrives, trimming idle current to microwatts.[10]Google Coral, “USB Accelerator Technical Overview,” coral.ai ASIC roadmaps increasingly bundle secure elements and LPDDR-in-package to simplify system validation. As automotive Tier 1s lock multi-year supply agreements, volume guarantees give fabs the incentive to fast-track functional-safety certification at the mask level.[11]Nanowear Inc., “SimpleSense-BP FDA Clearance,” nanowear.com

By Power Consumption Envelope: Ultra-Low Power Drives Innovation

The 5-10 W bracket held 38.1% of Edge AI Accelerators market size in 2024, serving fanless DIN-rail controllers and city-pole computer-vision nodes. Shipments within the <1 W category are projected to expand 28.7% CAGR through 2030, reaching nearly one-quarter of unit volume as coin-cell wearables, tire-pressure sensors, and smart locks add always-on intelligence.

Neuromorphic and processing-in-memory chips headline this ultra-low-power wave, using event-based logic and analog compute to shed refresh cycles. PIMIC’s Listen VL130 reduces DSP workloads by routing MAC operations inside SRAM, cutting power 10× over discrete MPU-DSP combos. Edge-optimized BMS algorithms running on 1-3 W NPUs now prolong e-scooter battery range by 12%. Higher envelopes above 10 W persist in rack-mount telco edge clusters where full-precision generative models need >100 TOPS and AC feed lines are available.

By Form Factor: System Integration Drives Adoption

SoCs delivered 42% revenue in 2024, underpinned by phone and TV chipsets that ship in the tens of millions. USB sticks, posting a 29.23% CAGR, democratize the Edge AI Accelerators market by letting developers add 4-20 TOPS to laptops without new motherboards; Google’s Coral USB remains the flagship at 4 TOPS INT8 within a 2.5 W budget.

Module and board-level products slot into legacy PLC backplanes or robotic arms, giving system integrators more I/O and thermal headroom. PCIe edge cards pack multiple NPUs and high-bandwidth GDDR6 for smart-factory servers that need real-time video analytics. Innovation now couples five TPUs into a single M.2 board, yielding 20 TOPS under 15 W for kiosk OEMs who cannot retool chassis molds. As BOM convergence accelerates, SoC vendors bundle NPUs with radios and ISPs, slicing SKU count and shrinking MTBF risk.

By Application: Computer Vision Dominance Faces Multimodal Challenge

Computer vision retained 49.5% Edge AI Accelerators market share in 2024 on the back of mature CNN pipelines in retail loss-prevention, ADAS, and industrial QA. Autonomous navigation workloads are poised for a 28.9% CAGR as drone corridors and warehouse AMRs multiply. Vision-centric SoCs like Sony’s IMX500 perform pixel-level inference at the sensor, cutting PCIe bandwidth by 80%.

NLP and speech deployments are shifting to edge endpoints such as voice remotes and in-cabin assistants to avoid cloud round-trips that leak personal data and degrade QoS during outages. Predictive-maintenance algorithms ingest vibration spectra and temperature curves locally, flagging anomalies before catastrophic downtime. Sensor-fusion stacks now merge LiDAR, mm-wave radar, and camera feeds on the same accelerator, demanding mixed-precision arithmetic and temporally aware transformers. TinyML frameworks squeeze keyword-spotting nets into sub-256 kB flash, helping microcontrollers join the Edge AI Accelerators market without bill-of-materials bloat.

By End-User Industry: Healthcare Acceleration Challenges Automotive Leadership

Automotive applications contributed 31% of Edge AI Accelerators market size in 2024 as L2+ ADAS functions proliferated across mid-priced vehicles. ISO 26262 ASIL B/C designs now embed redundant NPUs to maintain lane-keeping when one path fails. Tier 1s such as Continental deployed Ambarella CV3-AD chips to achieve 500 TOPS at <55 W for level-3 systems.

Healthcare’s 27.9% CAGR reflects FDA clearance of 950 AI/ML devices in 2024, legitimizing bedside and ambulatory diagnostics that must keep patient data on-premise. Wearables such as Nanowear’s SimpleSense-BP harness sub-1 W NPUs to crunch photoplethysmography streams and deliver clinical-grade blood-pressure readings without cuffs. Industrial, consumer, and smart-city verticals follow closely, each layering in AI to extend asset life, personalize experiences, or decongest traffic, all contributing incremental demand for low-latency silicon.

Geography Analysis

North America generated 40% of 2024 revenue thanks to early adopter ecosystems in Silicon Valley automotive labs and hyperscaler R&D centers. Defense directives on zero-trust and on-shore silicon sourcing further lock government contracts into domestic suppliers.

Asia-Pacific’s 29.88% CAGR is propelled by state grants and vertically integrated ODMs that migrate smartphones, scooters, and CCTV cameras into AI-enabled variants nearly in lock-step with node shrinks. TSMC already controls 62% global foundry share, underwriting a stable supply of 3 nm wafers for edge ASIC startups while Japanese fabless vendors like Socionext leverage local automotive OEM demand to seed regional clusters.[12]Taiwan Semiconductor Manufacturing Company, “2024 Annual Report,” tsmc.com

Europe emphasizes compliance over volume, with GDPR and the AI Act mandating on-device inference for sensitive data. Automakers in Germany, France, and Sweden are frontloading ASIC design to guarantee traceability and functional-safety proofs. Emerging deployments in the Middle East use edge AI traffic cameras to conserve scarce water by routing vehicles away from flooded roads. South America pilots smart-agriculture drones that infer crop stress offline to accommodate patchy rural networks, gradually widening the Edge AI Accelerators market footprint.

Competitive Landscape

The Edge AI Accelerators market is moderately fragmented; the top five vendors together hold roughly 45% revenue, well below the threshold for oligopoly. NVIDIA leverages CUDA lock-in and 1,500 Jetson ecosystem partners while investing in 49 edge-AI startups during 2024 to seed future software demand. Intel promotes neuromorphic Loihi boards to carve a power-efficiency niche unaddressed by GPUs.[13]NVIDIA Corporation, “Jetson Partner Ecosystem,” nvidia.com

Startups chase domain-specific slices: BrainChip’s Akida focuses on on-device learning for industrial IoT; DEEPX targets cost-sensitive home appliances with sub-5 W NPUs; Hailo scales TOPS density for autonomous taxi fleets with credit-card-sized modules that slide into existing ECUs. VC appetite endured a capital drought in other tech categories; 30 edge-AI chip firms still closed rounds in 2024-2025 as hardware differentiation offers tangible barriers to entry.

Strategic moves include the 2025 MediaTek-NVIDIA pact to co-develop AI PC silicon that merges Arm CPU clusters with discrete GPU-class tensor cores, and Intel’s 2025 unveil of a 1-billion-neuron Loihi-2-based research system that demonstrated 37× lower power on combinatorial optimization tasks versus x86 servers. Consolidation looms as smaller fabless players confront rising tape-out costs; alliances with OSATs and IP houses aim to share risk while maintaining time-to-market.

Edge AI Accelerators Industry Leaders

NVIDIA Corporation

Intel Corporation

Qualcomm Technologies Inc.

Google LLC

MediaTek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EdgeRunner AI closed a USD 12 million Series A for air-gapped generative assistants tailored to defense and healthcare.

- June 2025: Embedl raised EUR 5.5 million (USD 6 million) to optimize models for embedded defense and robotics use cases.

- April 2025: NVIDIA and MediaTek partnered on AI PC chips slated for H1 2025 release.

- March 2025: Intel unveiled its largest Loihi 2 neuromorphic computer, hitting 37× CPU energy savings on CSP benchmarks.

- February 2025: Qualcomm launched Snapdragon 8 Elite on 3 nm to provide 45% CPU uplift and 2-times NPU efficiency in flagship mobiles.

Global Edge AI Accelerators Market Report Scope

The Edge AI Accelerators Market Report is Segmented by Hardware Type (ASIC, GPU, FPGA, and More), Power Consumption Envelope (Less Than 1W, 1-3W, and More), Form Factor (System-On-Chip, Module/Board, PCIe/Edge Card, USB/Stick Accelerator), Application (Computer Vision, Speech and NLP, and More), End-User Industry (Consumer Electronics, Automotive, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| ASIC |

| GPU |

| FPGA |

| VPU / NPU |

| Heterogeneous SoC |

| Less Than 1 W |

| 1-3 W |

| 3-5 W |

| 5-10 W |

| 10-20 W |

| More Than 20 W |

| System-on-Chip |

| Module / Board |

| PCIe / Edge Card |

| USB / Stick Accelerator |

| Computer Vision |

| Speech and Natural-Language Processing |

| Predictive Maintenance / Anomaly Detection |

| Autonomous Navigation and Control |

| Sensor Fusion and Data Aggregation |

| Consumer Electronics and Wearables |

| Automotive and Transportation |

| Industrial and Manufacturing |

| Smart Cities and Public Safety |

| Healthcare and Life Sciences |

| Aerospace and Defense |

| Agriculture |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Hardware Type | ASIC | ||

| GPU | |||

| FPGA | |||

| VPU / NPU | |||

| Heterogeneous SoC | |||

| By Power Consumption Envelope | Less Than 1 W | ||

| 1-3 W | |||

| 3-5 W | |||

| 5-10 W | |||

| 10-20 W | |||

| More Than 20 W | |||

| By Form Factor | System-on-Chip | ||

| Module / Board | |||

| PCIe / Edge Card | |||

| USB / Stick Accelerator | |||

| By Application | Computer Vision | ||

| Speech and Natural-Language Processing | |||

| Predictive Maintenance / Anomaly Detection | |||

| Autonomous Navigation and Control | |||

| Sensor Fusion and Data Aggregation | |||

| By End-User Industry | Consumer Electronics and Wearables | ||

| Automotive and Transportation | |||

| Industrial and Manufacturing | |||

| Smart Cities and Public Safety | |||

| Healthcare and Life Sciences | |||

| Aerospace and Defense | |||

| Agriculture | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the value of the Edge AI Accelerators market in 2024?

The Edge AI Accelerators market was valued at USD 7.45 billion in 2024.

How fast is the Edge AI Accelerators market expected to grow?

The market is forecast to post a 31% CAGR from 2025 to 2030.

Which hardware category leads the space?

ASIC devices dominated with 47.2% share in 2024, reflecting demand for application-specific performance.

Why is healthcare the fastest-growing vertical for edge AI chips?

FDA clearance of 950 AI/ML devices is driving hospitals to adopt on-device inference for privacy-compliant diagnostics.

Which region will see the highest growth through 2030?

Asia-Pacific is projected to grow at a 29.88% CAGR as it scales semiconductor production capacity.

What power envelope is most common in industrial edge deployments?

The 5-10 W bracket balances compute density with fanless thermal limits and led with 38.1% share in 2024.

Page last updated on: