AI PC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.51 Billion |

| Market Size (2031) | USD 26.48 Billion |

| Growth Rate (2026 - 2031) | 12.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI PC Market Analysis by Mordor Intelligence

The AI PC market size is expected to grow from USD 12.87 billion in 2025 to USD 14.51 billion in 2026 and is forecast to reach USD 26.48 billion by 2031 at 12.78% CAGR over 2026-2031. Faster on-device generative AI, cheaper neural processing units, and data-sovereignty rules are prompting enterprises to refresh fleets rather than rely on cloud inference. Microsoft’s internal rollout of Copilot-ready notebooks to 200,000 employees proved that AI-native hardware boosts measurable productivity, spurring Fortune 500 buyers to shorten refresh cycles. Parallel cost reductions, Qualcomm’s Snapdragon X2 Elite cut NPU silicon costs 18% year-over-year, making Arm-based designs price-competitive for mid-tier enterprises. Mini PCs are emerging at industrial and retail edges where space, dust, and thermals disfavor tower PCs, while direct-to-business channels that bundle Microsoft 365 Copilot subscriptions erode traditional reseller margins.

Key Report Takeaways

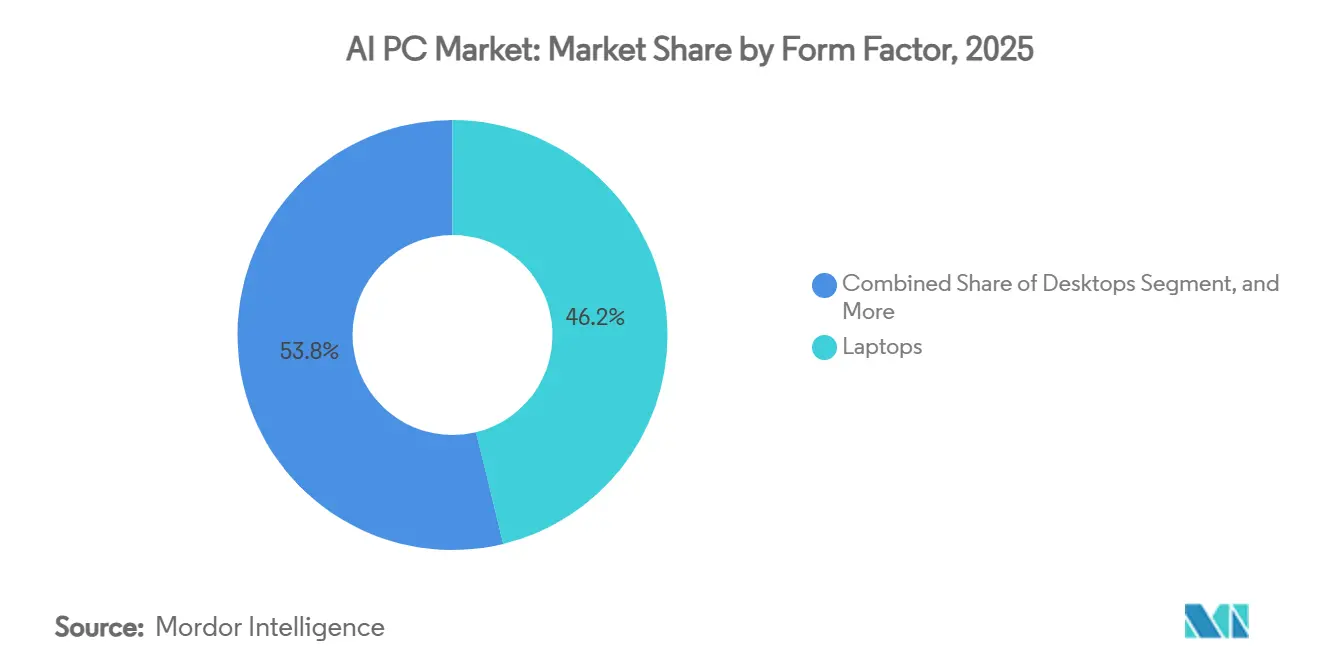

- By form factor, laptops led with 46.21% revenue share in 2025, while mini PCs are projected to expand at a 13.58% CAGR through 2031.

- By processor architecture, x86 devices held 71.14% of the AI PC market share in 2025, whereas Arm is forecast to grow at a 13.38% CAGR through 2031.

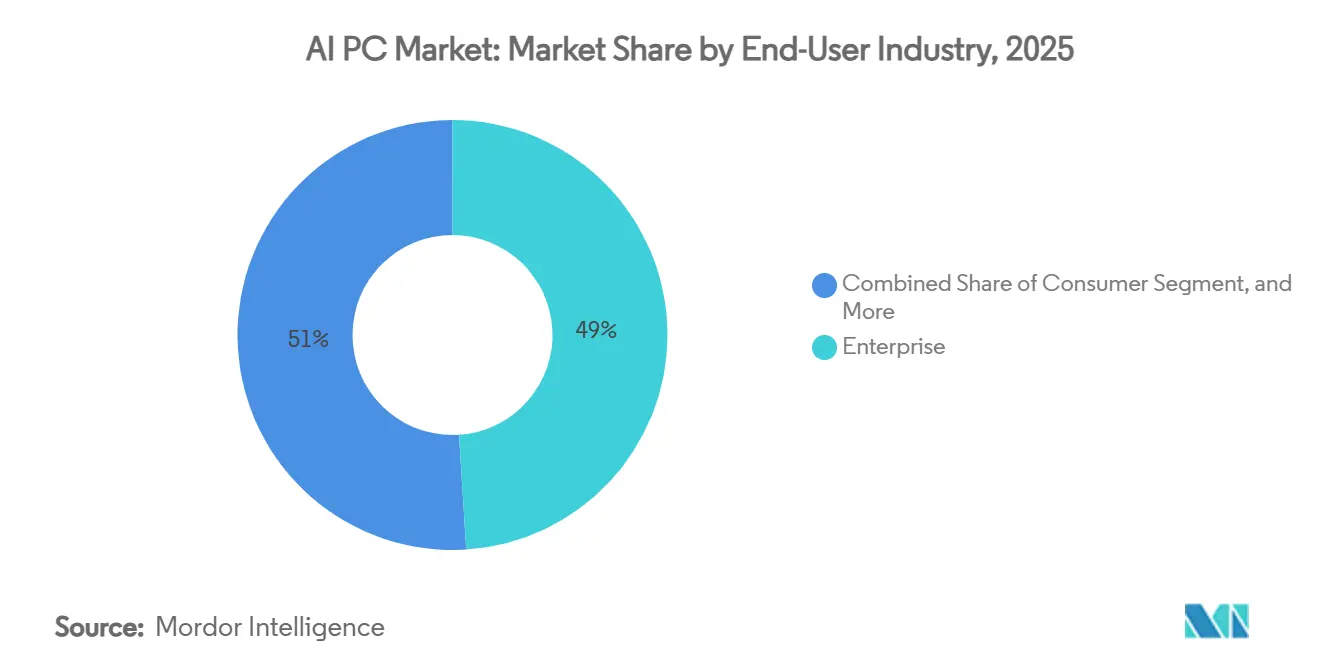

- By end-user industry, enterprise deployments accounted for 48.98% of shipments in 2025, while government and public-sector demand is advancing at a 13.49% CAGR to 2031.

- By sales channel, online retail captured 63.81% of 2025 revenue, and direct B2B sales are advancing at a 13.49% CAGR through 2031.

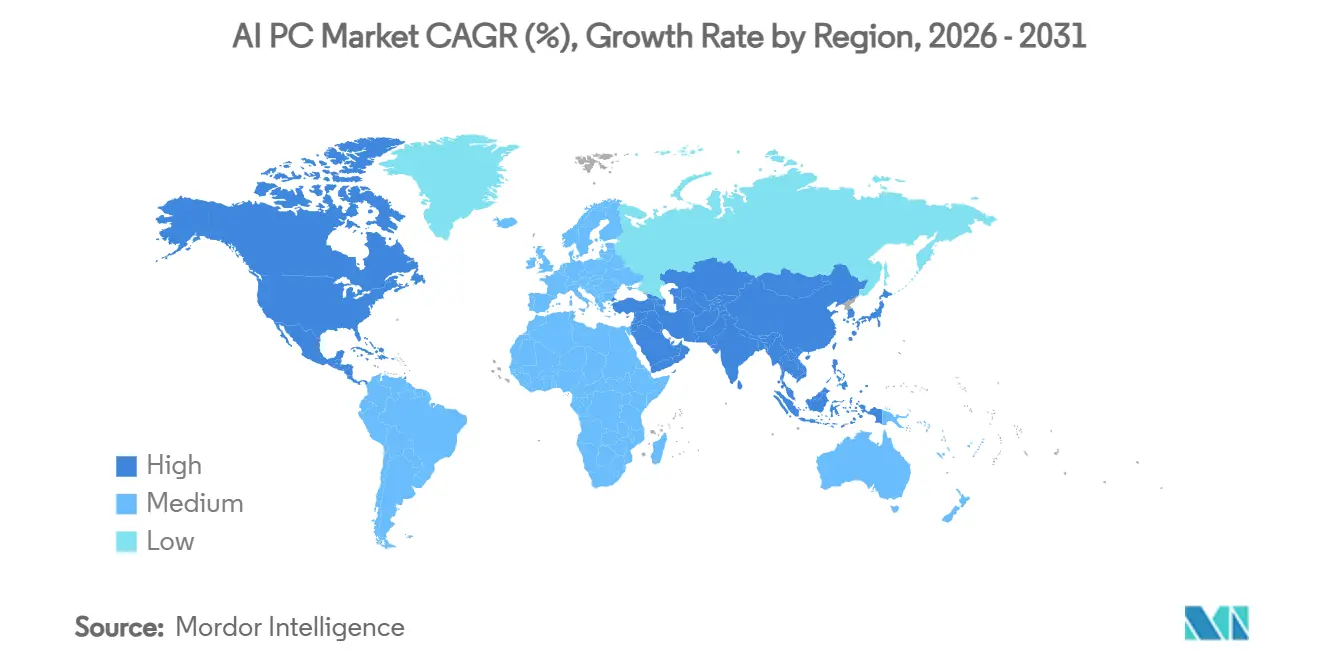

- By geography, North America commanded 43.29% of the AI PC market in 2025, and Asia-Pacific is expanding at a 13.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI PC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Integration of On-Device Generative AI | +3.2% | Global, early focus in North America and Europe | Short term (≤ 2 years) |

| Falling Cost Curve for NPUs | +2.8% | Global, especially Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Microsoft Copilot and Similar OS Upgrades | +2.1% | North America, Europe, Australia | Short term (≤ 2 years) |

| Data-Local Compliance Mandates | +1.9% | Europe, China, North America | Medium term (2-4 years) |

| Corporate Sustainability Targets | +1.4% | Europe, North America, Japan | Long term (≥ 4 years) |

| Venture Funding for AI-Optimized PCs | +1.0% | North America with spillover to Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Integration of On-Device Generative AI Capabilities

Real-time translation, code generation, and image synthesis are now executed locally, converting the PC into a self-contained inference engine. Dell disclosed that enterprise customers running local AI saw cloud egress bills fall by 22% and task completion speeds rise by 15% in 2025.[1]Investor Relations Team, “Q1 2026 Results,” Dell Technologies, delltechnologies.com Regulated sectors value this shift because proprietary data never traverses external APIs. Apple’s M4 MacBook Pro, shipping since November 2025, integrates a 38-core neural engine that handles 13-billion-parameter models on the device. Law firms now complete contract review internally, avoiding liability associated with third-party cloud services.

Falling Cost Curve for NPUs in x86 and Arm-Based PCs

Advanced packaging, chiplets, and through-silicon via technologies have significantly reduced die area and improved yields, enabling more efficient production processes. Qualcomm reported an 18% reduction in cost per TOPS for the Snapdragon X2 Elite, which began shipping in January 2026. Intel’s Lunar Lake, launched in September 2025, introduced a discrete AI tile that helps distribute costs across high-volume SKUs, making advanced AI capabilities more accessible. AMD followed suit with the Ryzen AI 300, priced below USD 700, which delivers 40 TOPS performance in mainstream laptops.[2]Investor Relations, “Ryzen AI 300 Launch,” AMD, amd.com This reduction in the bill of materials has expanded the availability of AI features beyond premium ultrabooks, extending their reach into commercial desktops and education-focused device fleets.

Microsoft Copilot and Similar AI-Native OS Upgrades

Windows 11 mandates 40 TOPS NPUs for Copilot Plus PCs, embedding AI into core workflows to enhance productivity and streamline operations. Microsoft reported a 19% increase in meeting efficiency and a 12% improvement in email response times after deploying 200,000 units internally by December 2025. These results highlight the significant impact of AI integration on workplace efficiency. Lenovo’s Copilot-certified ThinkPad X1 Carbon emerged as its fastest-selling commercial laptop in North America in 2025, driven by the growing demand for AI-enabled devices. Once employees become accustomed to features like Recall indexing and live captions, reverting to legacy hardware becomes impractical due to the associated retraining costs, which deter hardware churn.

Data-Local Compliance Mandates Boosting Edge Processing

The EU Data Act and China’s Personal Information Protection Law impose strict regulations requiring enterprises to store personal data within their respective borders, thereby making cloud-based inference less viable. This shift in regulatory requirements has driven companies to explore alternative solutions that ensure compliance while maintaining operational efficiency. HP reported a significant increase in demand for AI PCs with on-device inference capabilities, with European orders rising by 41% quarter over quarter in Q1 2026. This trend highlights a growing preference for localized data processing to mitigate the risks of non-compliance. Multinational corporations are now evaluating the potential GDPR penalties against the additional costs of deploying AI PCs. Many have concluded that investing in local inference systems is more cost-effective than undergoing extensive cross-border compliance audits, which can be both time-consuming and expensive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Standardized AI Benchmarking for PCs | -1.6% | Global | Short term (≤ 2 years) |

| Limited Battery Life Under AI Workloads | -1.3% | Global, especially mobile-first Asia-Pacific | Medium term (2-4 years) |

| Enterprise Security Concerns Around Local Tuning | -0.9% | North America, Europe | Short term (≤ 2 years) |

| Slow Replacement Cycles in Education Sector | -0.7% | Global, acute in budget-constrained regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardized AI Benchmarking for PCs

MLPerf omits client-device inference, leaving buyers to decode vendor-specific metrics, which makes it difficult to evaluate performance across different devices. A survey conducted in February 2026 revealed that 37% of IT managers delayed AI PC purchases due to the lack of third-party validation. This lack of standardized benchmarks, such as apples-to-apples scores for tasks like background transcription or multimodal queries, makes it difficult for finance teams to accurately assess and model the potential productivity gains from these investments. As a result, organizations face uncertainty about justifying the adoption of AI-enabled PCs, further slowing decision-making in this segment.

Limited Battery Life Under AI Workloads

AnandTech measured a 28% drop in battery life when Windows 11 Recall and live captions ran concurrently on a Snapdragon X Elite notebook in January 2026. This significant reduction highlights the challenges of balancing advanced features with energy efficiency. While NPUs (Neural Processing Units) are highly efficient per operation, the continuous inference workload prevents the device from entering deep sleep states, which are crucial for power conservation. The impact is particularly pronounced for Asia-Pacific field workers, who depend heavily on devices with all-day battery life to maintain productivity in remote or demanding environments. Unfortunately, advancements in battery chemistry have not kept pace with the rapid improvements in silicon technology, further exacerbating the issue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form Factor: Mini PCs Gain Industrial Traction

Mini PCs are projected to grow at 13.58% CAGR through 2031, outpacing laptops, desktops, and workstations. Laptops retained 46.21% of the AI PC market share in 2025, but demand for palm--size systems at the edge signals diversification of the AI PC market. ASUS won design wins in January 2026 with its NUC 14 Pro AI across three European retail chains for real-time customer analytics. Lenovo’s 0.7-liter ThinkCentre Neo 50q Gen 5 deploys a Snapdragon X2 Elite processor in a design with limited airflow, underscoring the AI PC industry's shift toward fanless designs.[3]Press Release, “ThinkCentre Neo 50q Gen 5,” Lenovo, lenovo.com

Verticals such as digital signage, point-of-sale, and factory inspection value rugged enclosures and low acoustics. Desktops still address cost-sensitive contact centers, while workstations blend NPUs with discrete GPUs for Adobe and AutoCAD workloads. Dell’s Precision 5490 routes preprocessing to the NPU and rendering to the GPU, cutting export time 18% in Premiere Pro. The AI PC market now benchmarks form-factor choices on thermals, latency, and upgradability rather than raw CPU clock speeds.

By Processor Architecture: Arm Challenges x86 Incumbency

x86 commanded a 71.14% share in 2025, yet Arm is scaling at a 13.38% CAGR in battery efficiency and Windows 11 Arm64 optimizations, highlighting another battleground in the AI PC market. Qualcomm shipped more than 4 million Snapdragon X-series processors in 2025, most of which were used in commercial laptops from HP, Lenovo, and Dell. Apple’s M4 sustains 18-hour battery life with 38 TOPS on the device, showcasing its ability to balance high performance with extended usage times, making it a preferred choice for professionals requiring reliable and efficient devices.

Intel’s Lunar Lake counters with a 48-TOPS NPU tile, designed to enhance AI processing, while AMD’s Ryzen AI 300 delivers 50 TOPS in sub-USD 700 laptops, making advanced AI features more accessible to budget-conscious consumers. Emerging RISC-V vendors are targeting embedded niches where licensing costs pinch margins, offering a cost-effective alternative for specific applications. Procurement scorecards now track NPU throughput and on-device model capacity alongside traditional CPU-GPU specs, reflecting the growing importance of energy efficiency and AI processing power in determining the overall value of devices in the AI PC market.

By End-User Industry: Government Sector Accelerates Adoption

Enterprise deployments accounted for 48.98% of 2025 shipments, underscoring the growing adoption of AI PCs in business environments, driven by their proven ability to enhance productivity. These deployments have been supported by documented use cases that highlight measurable gains in efficiency and performance. Government and public-sector demand is also on the rise, growing at a CAGR of 13.49%, driven by significant investments in digital transformation initiatives across key regions, including the United States, the United Kingdom, and India. For instance, London’s Government Digital Service implemented a mandate in April 2025 requiring AI-capable endpoints, while India allocated INR 12 billion (USD 144 million) to support state-level rollouts of AI-enabled systems.

On the other hand, consumer adoption of AI PCs has been slower, as buyers carefully evaluate the additional USD 200-400 cost against the perceived benefits. In the education sector, refresh cycles typically span five years, which limits the immediate demand for AI PCs. Furthermore, only 14% of U.S. K-12 school districts have prioritized AI PCs for their 2026 procurement plans. However, consultancy case studies have demonstrated that AI-enabled PCs, such as those equipped with Copilot features, can accelerate document review processes by 27%. These findings are gradually convincing corporate decision-makers that the higher upfront investment in AI PCs can be recouped within a short period through improved operational efficiency.

By Sales Channel: Direct B2B Models Reshape Distribution

Online retail accounted for 63.81% of market share in 2025, driven by its convenience and accessibility for customers. However, direct B2B channels are emerging as the fastest-growing distribution path, advancing at a CAGR of 13.49%. This growth is attributed to vendors increasingly bundling hardware and AI software into multi-year contracts, thereby redefining value capture in the AI PC industry. For instance, Dell reported that 72% of its Q1 2026 AI PC orders included Microsoft 365 Copilot subscriptions, highlighting the growing demand for integrated solutions. Similarly, HP introduced its Workforce Experience Platform in June 2025, which provides IT managers with remote NPU telemetry and firmware control capabilities. This platform has been instrumental in reducing the total cost of ownership by 15%, further enhancing its appeal to enterprise customers.

Offline retail continues to maintain a presence, particularly in regions with low credit-card penetration, where traditional purchasing methods remain prevalent. However, advancements in virtual configurators and augmented reality (AR) try-outs are gradually reducing foot traffic in physical stores. Manufacturers are leveraging direct usage data to refine firmware updates, which enhance on-device model accuracy. This iterative process creates a positive feedback loop, further accelerating the shift toward online and direct B2B channels.

Geography Analysis

North America accounted for 43.29% of 2025 revenue, buoyed by early adoption of Copilot Plus PC in financial services and healthcare. A U.S. federal memorandum issued in March 2025 instructed civilian agencies to standardize on AI-capable endpoints, accelerating refreshes. At Veterans Affairs and at Social Security.[4]Government Services Administration, “Federal Endpoint Memorandum,” gsa.gov Canada's Treasury Board set aside CAD 450 million (USD 333 million) for AI PCs in fiscal 2026. Mexico’s demand is clustered in maquiladora plants that deploy edge analytics to cut defect rates.

Asia-Pacific is the fastest-growing region, expanding at a 13.81% CAGR through 2031. Lenovo and Huawei released laptops with indigenous NPUs in Q2 2025, aligning with Beijing’s semiconductor self-reliance goals. India’s 60 million-strong SME base chooses AI PCs to sidestep cloud bandwidth costs, aided by Wipro bundles that localize models to regional languages. Mature Japanese and Korean enterprises match adoption to corporate carbon-neutrality mandates set by Tokyo and Seoul authorities.

Europe’s trajectory revolves around the EU Cloud Sovereignty Framework. Germany’s cybersecurity agency urgedcritical infrastructuree operators to keep their infrastructure on-premises in February 2026. France and the United Kingdom promote sovereign data paths that favor AI PCs over hyperscale services. Southern Europe lags because tighter public budgets delay refresh cycles, yet logistics firms in Italy and Spain now trial mini PCs for predictive maintenance, nudging volume upward. In the Middle East and Africa, the United Arab Emirates and Saudi Arabia spearhead demand through smart-city initiatives, whereas South African miners deploy AI PCs underground for vibration analysis, where bandwidth is scarce.

Competitive Landscape

The five largest vendors, Lenovo, HP, Dell, Apple, and ASUS, controlled about 60% of 2025 shipments, indicating a moderately concentrated AI PC market. Apple leverages full-stack control, funneling its neural engine across macOS and first-party apps for seamless power management. Windows OEMs counter with deep alliances, such as Dell and HP bundle Copilot seats and remote NPU management portals that lock IT administrators in. Patent filings for sub-15-watt inference jumped 34% year-over-year, led by Qualcomm, Intel, and AMD with more than 200 submissions covering chiplet layouts and sparse-matrix engines.

White-space competition emerges in education, where Framework and Chuwi sell modular boards under USD 600. Framework raised USD 18 million in March 2025 to ramp up user--swappable NPU modules, aligning with sustainability goals in public tenders. Mini PC niches remain fragmented, allowing boutique brands to differentiate on passive cooling and DIN-rail mounting. Vendors now race to curate pre-trained model libraries, finance and health assistants, and code assistants, so hardware plus subscription beats commoditized silicon alone.

Strategic moves illustrate the pivot from raw CPU battles to AI ecosystems. Qualcomm unveiled Snapdragon X3 Elite with 60 TOPS and partnerships spanning 12 OEMs in March 2026. Dell shipped the Precision 5490 in February 2026, featuring CPU-GPU-NPU hand-offs that slash video rendering time. Lenovo’s Neo 50q Mini PC shipped in January 2026 into retail analytics installs. Such roll-outs show how the AI PC market links silicon innovation directly to vertical use-case monetization.

AI PC Industry Leaders

Lenovo Group Limited

HP Inc.

Dell Technologies, Inc.

Apple Inc.

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Qualcomm revealed Snapdragon X3 Elite, a 60-TOPS NPU part, with 12 OEM design wins targeting on-device large-language-model tuning.

- February 2026: Dell introduced the Precision 5490, a mobile workstation powered by Intel Core Ultra with hybrid CPU-GPU-NPU orchestration that cuts Adobe export times by 18%.

- January 2026: Lenovo launched ThinkCentre Neo 50q Gen 5, a 0.7-liter Snapdragon X2 Elite mini PC for retail and healthcare kiosks.

- December 2025: Microsoft completed the internal deployment of 200,000 Copilot Plus PCs, reporting 19% faster meetings and 12% quicker email replies.

Global AI PC Market Report Scope

The AI PC Market encompasses the development, production, and commercialization of personal computing devices integrated with dedicated artificial intelligence (AI) capabilities, enabling on-device processing of machine learning and generative AI workloads. These systems are equipped with specialized hardware components, such as neural processing units (NPUs), AI-optimized CPUs and GPUs, and software frameworks that enable the efficient execution of AI applications locally, reducing reliance on cloud-based processing.

The AI PC Market Report is Segmented by Form Factor (Laptops, Desktops, Workstations, and Mini PCs), Processor Architecture (x86, Arm, RISC-V and and Other Architectures), End-User Industry (Consumer, Enterprise, Education, and Government and Public Sector), Sales Channel (Online Retail, Offline Retail, and Direct B2B Sales), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Laptops |

| Desktops |

| Workstations |

| Mini PCs |

| x86 |

| Arm |

| RISC-V and Other Architectures |

| Consumer |

| Enterprise |

| Education |

| Government and Public Sector |

| Online Retail |

| Offline Retail |

| Direct B2B Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Form Factor | Laptops | ||

| Desktops | |||

| Workstations | |||

| Mini PCs | |||

| By Processor Architecture | x86 | ||

| Arm | |||

| RISC-V and Other Architectures | |||

| By End-User Industry | Consumer | ||

| Enterprise | |||

| Education | |||

| Government and Public Sector | |||

| By Sales Channel | Online Retail | ||

| Offline Retail | |||

| Direct B2B Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the AI PC market by 2031?

The AI PC market is forecast to reach USD 26.48 billion by 2031.

Which form factor is expected to grow the fastest through 2031?

Mini PCs are projected to register the highest growth at a 13.58% CAGR.

How fast is Arm architecture expanding inside commercial AI PCs?

Arm-based systems are advancing at a 13.38% CAGR between 2026 and 2031.

Why are government agencies prioritizing AI PCs over cloud inference?

Data-local regulations and national digital-sovereignty programs favor on-device processing for compliance and security.

Which sales channel is gaining momentum for enterprise AI PC purchasing?

Direct B2B portals that bundle hardware and AI software are growing the fastest, expanding at a 13.49% CAGR.

What battery-life penalty do AI workloads impose on mobile PCs today?

Independent tests show continuous AI features can reduce battery endurance by around 28%.

Page last updated on: