AI Search Optimization Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

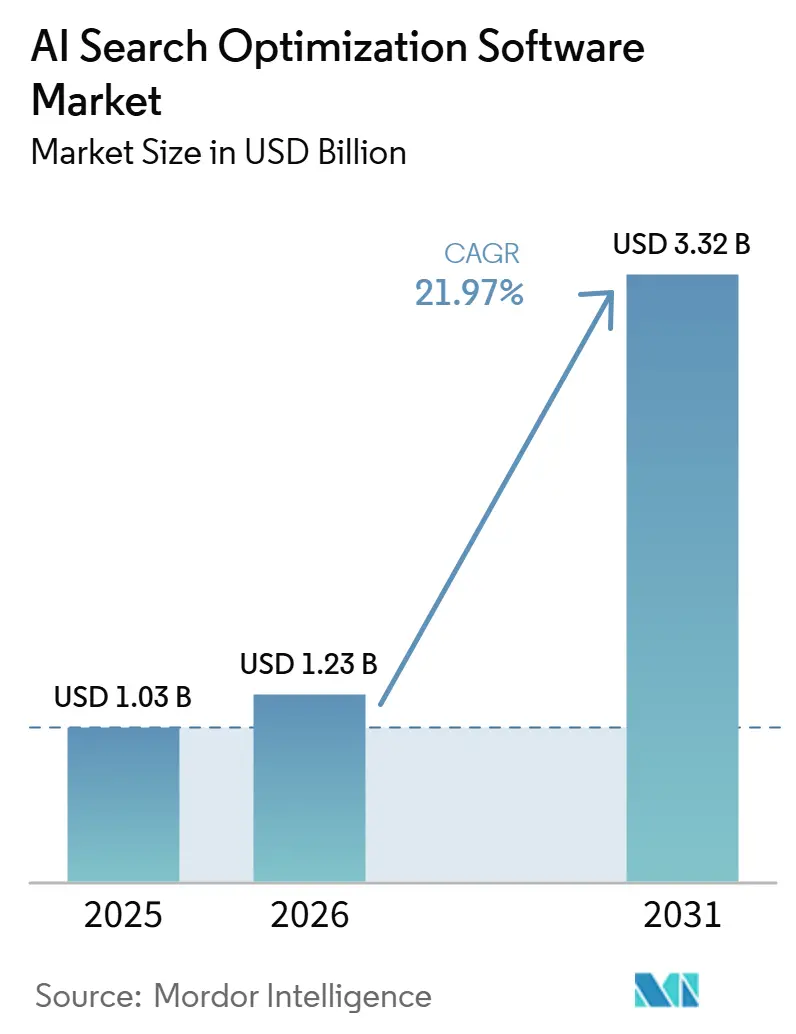

| Market Size (2026) | USD 1.23 Billion |

| Market Size (2031) | USD 3.32 Billion |

| Growth Rate (2026 - 2031) | 21.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Search Optimization Software Market Analysis by Mordor Intelligence

The AI search optimization software market size is expected to grow from USD 1.03 billion in 2025 to USD 1.23 billion in 2026 and is forecast to reach USD 3.32 billion by 2031 at 21.97% CAGR over 2026-2031. Growth is tied to a broad change in digital discovery, as answer engines now handle more of the user journey before a visit reaches a traditional search results page. Enterprise buyers are responding because AI visibility is becoming a direct business measure, especially where discovery quality matters more than traffic volume. Demand is also rising because brands need tools that can track citations, monitor shifting answer formats, and manage visibility across closed systems that lack clear measurement paths. Vendor competition is centered on faster feature releases, better citation intelligence, and wider multi-engine coverage, which is pushing the AI search optimization software market toward platform depth rather than basic ranking dashboards. The main opportunity for the AI search optimization software market lies in attribution, localization, and governance, where buyers need software that connects AI discovery to business outcomes without relying on manual monitoring.

Key Report Takeaways

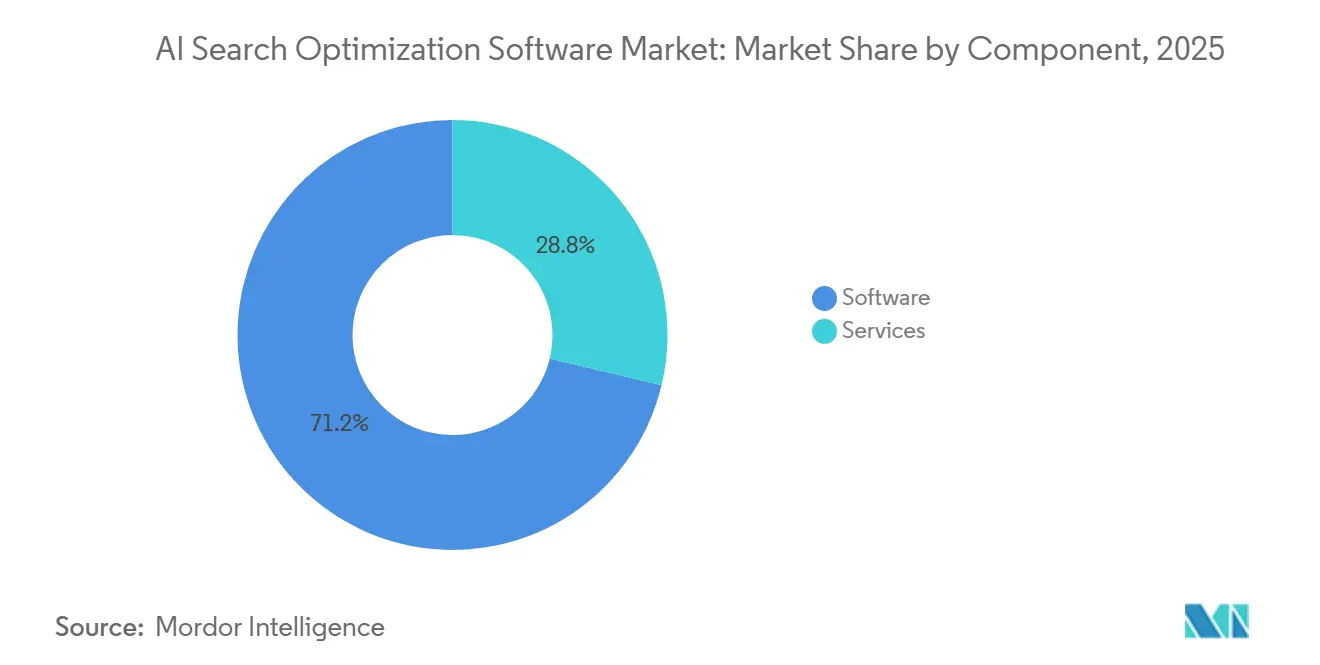

- By component, software accounted for 71.24% of revenue in 2025, and services are projected to expand at a 24.83% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 68.41% of the AI search optimization software market size in 2025, and hybrid deployment is expected to grow at 23.19% CAGR through 2031.

- By optimization type, content optimization led with 26.73% share in 2025, and AI search visibility optimization is projected to grow at 26.42% CAGR through 2031.

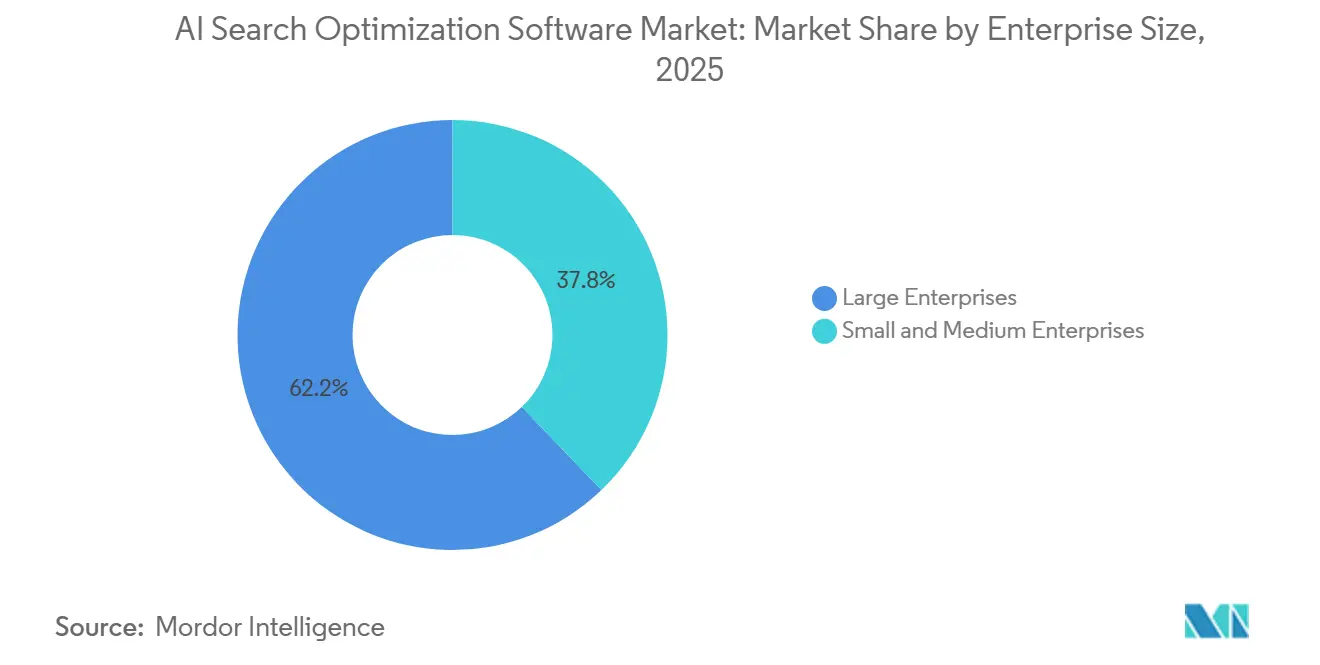

- By enterprise size, large enterprises held 62.18% share in 2025, and small and medium enterprises are expected to expand at 25.36% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 24.86% of the market share in 2025, and healthcare and life sciences are projected to grow at a 24.71% CAGR through 2031.

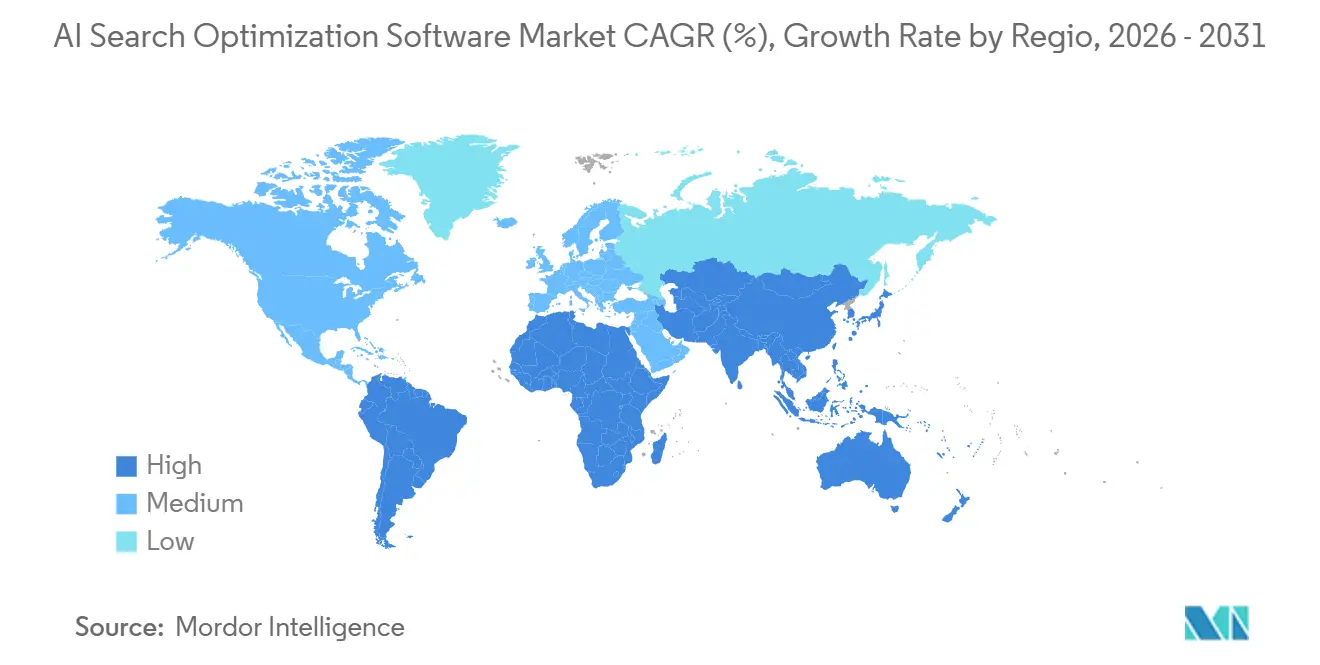

- By geography, North America held 34.62% of the AI search optimization software market share in 2025, and Asia-Pacific is projected to expand at 27.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Search Optimization Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Enterprise Demand for AI Search Visibility | +4.8% | Global, with early concentration in North America and Western Europe | Short term (≤ 2 years) |

| Shift From Keyword Ranking to Answer Engine Optimization | +4.2% | Global, strongest in North America and Asia-Pacific core | Short term (≤ 2 years) |

| Need to Reduce Organic Traffic Volatility from AI Overviews | +3.6% | North America and Europe, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Content Scale Requirements Across Multi-Property Brands | +2.9% | Global, concentrated in enterprise-heavy markets | Medium term (2-4 years) |

| Budget Reallocation Toward Measurable Organic Efficiency | +2.3% | North America, Europe, Japan, Australia | Medium term (2-4 years) |

| Early-Mover Advantage In Proprietary Citation Tracking | +1.7% | North America, with early gains in the United Kingdom, Germany, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Demand for AI Search Visibility

Enterprise adoption has moved quickly because AI citation gaps are harder to detect than standard ranking gaps, and that makes the need for dedicated monitoring more urgent. The AI search optimization software market is benefiting from this shift because large marketing teams now treat a lack of AI visibility as an operating risk rather than just a growth issue. Semrush stated in June 2026 that its expanded AI Visibility Index analyzed 126 million U.S. AI search prompts and found wide variation in brand mention rates across competing brands in the same category.[1]Semrush, “Semrush Releases Expanded 2026 AI Visibility Index, Analyzing 126 Million AI Search Prompts,” Semrush, semrush.com That kind of uneven citation exposure makes manual review a weak control process, especially in large organizations with many brands, products, and content teams. The result is a retention advantage for vendors that can provide repeatable visibility benchmarks, because buyers cannot clearly see these gaps with conventional analytics tools. This pattern supports recurring demand across the AI search optimization software market as enterprises move from testing to structured platform adoption.

Shift from Keyword Ranking to Answer Engine Optimization

The move from keyword ranking to answer engine optimization is changing what buyers expect from search software. The AI search optimization software market is gaining from this transition because citation presence matters more in answer environments than a single blue-link position. Enterprise contracts have also expanded as buyers pay for monitoring, competitive benchmarking, and response-surface intelligence rather than for simple keyword dashboards. Conductor reinforced this direction in April 2026, when it launched its next-generation AI Search Performance offer as a unified system of record for answer engine optimization.[2]Conductor, “Conductor Delivers Next-Generation AI Search Performance, Introducing the Industry's Only System of Record for AEO,” Business Wire, businesswire.com That move shows how incumbent platforms are recasting core product value around answer visibility, workflow execution, and performance management. As this shift continues, the AI search optimization software market is likely to reward vendors that can integrate search, content, technical signals, and citation control into a single operating layer.

Need to Reduce Organic Traffic Volatility from AI Overviews

Traffic volatility has become a direct buying trigger, as brands can lose visits even when their content ranks well in traditional search results. Ahrefs reported in 2025 that the top-ranking page saw a 58% drop in clicks when an AI Overview was present.[3]Ahrefs, “Update, AI Overviews Reduce Clicks by 58%,” Ahrefs, ahrefs.com This pressure is pushing the AI search optimization software market toward tools that can detect when AI Overviews appear, show who gets cited, and help teams improve placement inside those answer surfaces. BrightEdge addressed that gap in 2025 with its AI Early Detection System, which tracked AI search traffic patterns and competitor presence inside AI results. The commercial appeal is clear because these tools are no longer framed only as growth software; they are also framed as protection against search interface changes that can disrupt existing traffic flows. That risk-based framing has made the AI search optimization software market more relevant to finance and executive teams, not only to SEO specialists.

Content Scale Requirements Across Multi-Property Brands

Large brands are dealing with a scale problem that manual workflows cannot manage well across regions, products, and languages. The AI search optimization software market is benefiting because buyers need a way to keep facts, structure, and brand language aligned across thousands of pages and answer surfaces. SEOClarity advanced this use case in April 2026 with ArcAI 3.0, which added agentic content briefing, narrative control, and prompt research capabilities for enterprise teams.[4]seoClarity, “seoClarity Launches ArcAI 3.0 to Reclaim Brand Narrative in AI Search,” seoClarity, seoclarity.net This matters because content work in large organizations is shifting from isolated page optimization to governed production and scalable monitoring. The change also supports software budgets at the expense of service-only models, since the research, briefing, and monitoring layers can be standardized inside a platform. In regulated sectors, that same need is even stronger because governance, traceability, and accuracy checks are now part of the buying decision.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unclear Attribution Between AI Visibility and Revenue | -2.6% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Fast-Changing Search Interfaces and Ranking Signals | -2.0% | Global | Short term (≤ 2 years) |

| Limited Access to Closed or Restricted AI Search Systems | -1.4% | Global, compounded in Asia-Pacific due to local AI ecosystem fragmentation | Medium term (2-4 years) |

| Buyer Skepticism Around New Category ROI | -0.9% | North America and Europe, especially in finance-led procurement cycles | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Unclear Attribution Between AI Visibility And Revenue

The largest buying barrier is still attribution. Many finance teams want a direct line between an AI citation event and a later revenue event, and that link is often not visible at the prompt level. BrightEdge stated in 2025 that AI search was functioning as a research channel with near-zero direct conversions tracked at that stage of adoption. That makes it harder for vendors in the AI search optimization software market to justify budgets through last-click logic, even when marketing teams can see the strategic value. The problem is sharper in large enterprises because they have strict buying processes and stronger demands for audited performance evidence. Until vendors build better assisted-conversion and pipeline-influence models, attribution opacity will remain a meaningful restraint on faster category conversion.

Fast-Changing Search Interfaces and Ranking Signals

Product planning is difficult because AI search interfaces change much faster than traditional search systems did. The AI search optimization software market is exposed to this pace because features tied too closely to one answer engine can lose relevance when that engine changes its behavior. Semrush responded in January 2026 by releasing Query Fan-Out Analysis, which exposed background queries generated by AI models before they produced a response. The release showed that vendors must now build around new signal types that were not part of product roadmaps a year earlier. For buyers, this creates selection risk because software quality depends not only on current features, but also on how quickly the vendor can adapt. That uncertainty slows some purchases at the top of the funnel, especially when procurement teams prefer tools with broader cross-engine coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads Revenue While Services Gain On Execution Needs

Software accounted for 71.24% of the market in 2025, indicating that platform subscriptions formed the primary revenue base early in the category's development. The AI search optimization software market favored software-first because buyers needed dashboards, citation monitoring, technical diagnostics, and reporting systems before they could scale large service programs. This pattern also reflects the SaaS structure of the category, where platforms can roll out updates across many accounts as answer engines change. Enterprise teams adopted these tools faster than services-led models because visibility monitoring requires repeat use, not one-time project work. The software segment, therefore, anchored the commercial base of the AI search optimization software market in 2025.

Services are projected to grow at a 24.83% CAGR through 2031, making them the fastest-growing component over the forecast period. Growth in services comes from implementation complexity, since many teams still need help with strategy, integration, workflow setup, and managed execution. This is not a sign of software weakness; it shows that the category is moving from tool purchase to operational use. BrightEdge illustrated this combined approach in March 2026 when it launched AI Hyper Cube and also expanded related capabilities around AI agent monitoring and visibility analysis. Over time, service growth is likely to further support platform adoption, as buyers often start with guided delivery before shifting more activity into software-led workflows.

By Deployment Mode: Cloud Holds The Core Position While Hybrid Builds In Regulated Settings

Cloud-based deployment accounted for 68.41% of the AI search optimization software market in 2025, leaving it well ahead of other deployment models. The cloud model fits the category because vendors need to update prompt libraries, integrations, and tracking logic frequently as answer engines change. It also supports shared benchmarking, faster onboarding, and lower deployment friction across distributed teams. These benefits made the cloud the default choice for enterprises that wanted speed and broad feature access. As a result, cloud remained the main delivery layer for the AI search optimization software market in 2025.

Hybrid deployment is expected to grow at a 23.19% CAGR through 2031, reflecting demand from sectors with stricter data and governance requirements. Healthcare, financial services, and public sector buyers often need tighter control over proprietary data, customer records, and internal testing environments. Hybrid models give these buyers a way to keep sensitive processes within their own infrastructure while still using cloud-based benchmarking or interface layers where needed. Botify supported the enterprise cloud security case in June 2025 by expanding its AI agents and MCP Server integration, and by joining the AWS ISV Accelerate Program. On-premise remains the smallest mode, but it still serves a narrow group of buyers that operate under strict sovereignty and security frameworks. The broader direction suggests that flexibility, not a single architecture, will shape deployment choices across the AI search optimization software market.

By Optimization Type: Content Still Leads While Visibility Monitoring Becomes The Fastest Growth Area

Content optimization accounted for 26.73% of the market in 2025, making it the largest optimization type by revenue. That lead came from the fact that content tools were already familiar to SEO teams before answer engine optimization gained speed. Buyers could extend existing content review, briefing, and scoring workflows into AI-oriented use cases faster than they could build new systems from scratch. The AI search optimization software market, therefore, began with a strong content base, especially for enterprises seeking to improve answer-readiness across large site libraries. Content remained the largest area because it connected directly to publishable work and existing budget lines.

AI search visibility optimization is projected to grow at a 26.42% CAGR through 2031, making it the fastest-rising optimization type. This shift shows that buyers are moving from creation support toward monitoring where and how a brand appears across answer engines. Technical SEO automation still matters because crawlability, site structure, and machine-readable signals remain basic conditions for citation inclusion. Analytics and performance monitoring are also rising because attribution remains a major buying barrier. SEOClarity addressed the narrative-control and accuracy side of this issue in April 2026 with ArcAI 3.0 and its monitoring modules. Reputation and brand presence optimization remains smaller, but it carries high strategic weight because outdated or incorrect AI responses can affect trust faster than low rankings did in earlier search models.

By Enterprise Size: Large Enterprises Generate Most Revenue While Smaller Buyers Lift Growth

Large enterprises held a 62.18% share in 2025, making them the main revenue anchor for the category. Their lead reflects larger digital budgets, broader brand portfolios, and a stronger need for governance across teams and markets. These organizations also face greater exposure when AI answer engines omit or misstate their content, which makes structured monitoring easier to justify. The AI search optimization software market, therefore, scaled first through enterprise-grade contracts, where buyers viewed these platforms as operating infrastructure rather than optional tools. This concentration in large accounts also helped vendors refine their products for multi-property use cases and formal reporting requirements.

Small and medium enterprises are projected to expand at a 25.36% CAGR through 2031, making them the fastest-growing buyer group. Lower-priced tools, simpler workflows, and the growing risk of exclusion from AI-generated shortlists support their growth. The J.P. Morgan Chase Institute reported in April 2026 that small-business AI adoption had reached 10% within 6 months for the 2025 access cohort. That pattern matters because it shows rising willingness among smaller firms to test AI tools when the use case is clear. In the AI search optimization software industry, this buyer group is likely to widen the customer base faster than it lifts the average contract value. Vendors that can combine usability, affordability, and clear reporting should gain the most as this part of the AI search optimization software market develops.

By End-User Industry: Retail And E-Commerce Lead Spending While Healthcare And Life Sciences Expand Faster

Retail and e-commerce accounted for a 24.86% share in 2025, making them the largest end-user group. Their lead came from the direct link between product discovery and revenue, since answer engines can now surface recommendations without requiring a full visit to a brand site. This made citation management and the presence of answers especially important for sellers competing on visibility during shortlist creation. The AI search optimization software market, therefore, saw early strength in retail use cases where commercial returns are easier to understand. The segment also benefited from the speed at which digital commerce teams test discovery channels.

Healthcare and life sciences are projected to grow at a 24.71% CAGR through 2031, making them the fastest-growing end-user group. Growth here is tied to the higher need for accuracy, structured information, and monitored responses in medical and health-related content environments. Buyers in this group are less focused on content volume alone and more on correctness, traceability, and quality of visibility. BFSI also remains an important adopter because prospective clients increasingly use AI tools when comparing providers and products. IT and telecom organizations use these tools to protect technical authority and brand presence in AI-generated summaries. Across the wider AI search optimization software market, vertical demand is likely to deepen most in sectors where a misleading or missing answer has a clear cost.

Geography Analysis

North America held 34.62% of the AI search optimization software market share in 2025, making it the largest regional segment. The region led because major enterprise buyers, mature digital marketing budgets, and several core platform operators are concentrated in the United States. This made North America the earliest large-scale testing ground for answer engine optimization tools and operating workflows. Canada and Mexico were smaller contributors, but both supported regional demand through enterprise digital adoption and cross-border brand activity.

Europe remained a structurally important region for the AI search optimization software market, as Germany, the United Kingdom, and France accounted for the core of enterprise demand. The region also carries added importance because accuracy, transparency, and governance concerns are especially relevant in its business and policy environment. Buyers in Europe are more likely to value controlled workflows and documented response quality, which supports demand for software with monitoring and governance layers. Asia-Pacific is projected to grow at a 27.84% CAGR through 2031, making it the fastest-growing regional segment in the AI search optimization software market. This growth reflects a more fragmented answer-engine environment, which increases the need for multi-engine visibility tools rather than single-platform optimization approaches.

India is expanding with its digital enterprise base, while Japan and South Korea remain attractive markets for enterprise-grade software and managed execution. Semrush supported the case for broader regional demand in May 2026, when it expanded its AI Visibility Database to 32 countries and added 17 new regional markets, bringing the prompt base to more than 261 million LLM prompts. South America is still earlier in adoption, but Brazil and Argentina are building relevance as digital marketing maturity improves. The Middle East and Africa remain the smallest region, though Saudi Arabia and the United Arab Emirates stand out because of digital transformation spending. Nigeria and South Africa offer longer-term potential where cost-efficient tools can match less mature enterprise infrastructure. The OECD stated in December 2025 that AI adoption among small and medium-sized enterprises still lagged that of larger firms globally, indicating underpenetrated demand across South America, the Middle East, and Africa.

Competitive Landscape

The AI search optimization software market remains moderately consolidated, with Semrush, BrightEdge, and Conductor holding strong enterprise mindshare, while specialist vendors compete with narrower sets of citation and analytics features. This structure keeps pricing power uneven because large platforms can spread development costs across broader product suites, while smaller vendors can move quickly within focused use cases. Competition centers on feature release speed, breadth of answer-engine coverage, and the ability to turn raw citation data into actionable operational decisions. The AI search optimization software market also shows a split between broad platforms that aim to become systems of record and specialists that aim to win through precision in a single problem area.

Semrush raised the feature threshold in 2026 through a series of releases that included Query Fan-Out Analysis in January, Crawler Profiles in March, Source and Sentiment Analysis automations in May, and an expansion of the 32-country AI Visibility Database in May. Conductor repositioned itself in April 2026 with its next-generation AI Search Performance launch, which tied measurement, recommendations, and execution into a single workflow. BrightEdge also moved aggressively in March 2026 with AI Hyper Cube and AI Agent Insights, expanding its role from standard reporting to prompt-level and technical monitoring. These moves show that vendors are competing on control, speed, and operational depth rather than on rank-tracking alone.

Specialist players are trying to build an advantage through proprietary data, infrastructure connectivity, and engine-specific visibility signals. Botify moved in that direction in June 2025, expanding its AI agents and MCP Server integration and aligning more closely with AWS through the ISV Accelerate Program. Ahrefs also pursued a data-led approach and stated in May 2026 that its benchmark report across 75,000 brands found YouTube mentions to be the strongest signal of AI visibility. The wider AI search optimization software market still has room in localization, attribution modeling, and agent-level monitoring, where buyer needs are clear but product maturity is still developing. That leaves the category competitive, but not concentrated around a small closed set of providers.

AI Search Optimization Software Industry Leaders

Semrush Holdings, Inc.

Ahrefs Pte. Ltd.

Moz, Inc.

Conductor, Inc.

BrightEdge Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Semrush released the expanded 2026 AI Visibility Index, analyzing 126 million U.S. AI search prompts. The study provides category-level citation benchmarks across major AI engines, establishing Semrush as a primary research authority in the AI search intelligence space and reinforcing enterprise platform stickiness.

- May 2026: Semrush expanded its AI Visibility Database to 32 countries, adding 17 new regional markets and growing the total prompt database to over 261 million LLM prompts. This global expansion directly targets enterprise clients managing multi-geography brand visibility in AI search environments.

- May 2026: Semrush Enterprise AI Optimization added Reddit Analysis and Negative Sentiment Analysis automations, enabling brands to monitor how Reddit-sourced content shapes their perception in AI-generated responses. The update reflects the outsized influence of community-generated content on LLM citation behavior.

- May 2026: Ahrefs released the Q1 2026 AI Search Benchmark Report, analyzing 75,000 brands and identifying YouTube mentions as the strongest predictor of AI visibility across major answer engines. The report establishes a proprietary citation-signal framework for content and distribution strategy.

Global AI Search Optimization Software Market Report Scope

The AI search optimization software market encompasses software solutions and associated services that leverage artificial intelligence, machine learning, and natural language processing to enhance a brand's visibility, ranking, and performance across traditional search engines and emerging AI-driven search modalities (such as generative AI search, conversational AI, and large language model responses). These solutions automate and optimize various aspects of digital search presence, including AI search visibility, content optimization, technical SEO, performance analytics, and brand reputation management. Deployed across cloud-based, on-premise, and hybrid environments, these platforms cater to organizations of all sizes across diverse industries, including retail, BFSI, healthcare, and media. By analyzing complex search algorithms and user intent, AI search optimization software helps businesses adapt to the evolving search landscape, drive highly targeted organic traffic, and maintain a competitive edge in an increasingly AI-dominated digital ecosystem.

The AI Search Optimization Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Optimization Type (AI Search Visibility Optimization, Content Optimization, Technical SEO Automation, AI Analytics and Performance Monitoring, and Reputation and Brand Presence Optimization), Enterprise Size (Large Enterprises, and Small And Medium Enterprises), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Government and Public Administration, Education and Research Institutions, Transportation and Logistics, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| AI Search Visibility Optimization |

| Content Optimization |

| Technical SEO Automation |

| AI Analytics and Performance Monitoring |

| Reputation and Brand Presence Optimization |

| Large Enterprises |

| Small And Medium Enterprises |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Government and Public Administration |

| Education and Research Institutions |

| Transportation and Logistics |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Optimization Type | AI Search Visibility Optimization | ||

| Content Optimization | |||

| Technical SEO Automation | |||

| AI Analytics and Performance Monitoring | |||

| Reputation and Brand Presence Optimization | |||

| By Enterprise Size | Large Enterprises | ||

| Small And Medium Enterprises | |||

| By End-User Industry | Retail and E-Commerce | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Media and Entertainment | |||

| Government and Public Administration | |||

| Education and Research Institutions | |||

| Transportation and Logistics | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and future value of the AI search optimization software space?

The AI search optimization software market size stands at USD 1.23 billion in 2026 and is forecast to reach USD 3.32 billion by 2031 at a 21.97% CAGR over 2026-2031.

What is driving demand for AI search optimization software?

Demand is rising because answer engines are changing how users discover brands, which makes citation tracking, answer visibility, and technical readiness more important for enterprise teams.

Which component is generating the most revenue?

Software led with 71.24% of revenue in 2025, showing that platform subscriptions still form the core spending base for this category.

Which deployment model is growing the fastest?

Hybrid deployment is projected to grow at 23.19% CAGR through 2031, mainly because regulated buyers want tighter control over sensitive data.

Which end-user group is expanding the fastest?

Healthcare and life sciences are projected to grow at 24.71% CAGR through 2031, driven by stronger needs for accuracy, governance, and monitored AI citations.

Which region offers the strongest growth outlook?

Asia-Pacific has the fastest outlook with a projected 27.84% CAGR through 2031, supported by a fragmented answer-engine environment that requires broader optimization coverage.

Page last updated on: