Data Center Accelerator Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Market Size (2026) | USD 14.69 Billion |

| Market Size (2032) | USD 32.13 Billion |

| Growth Rate (2026 - 2032) | 13.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Center Accelerator Market Analysis by Mordor Intelligence

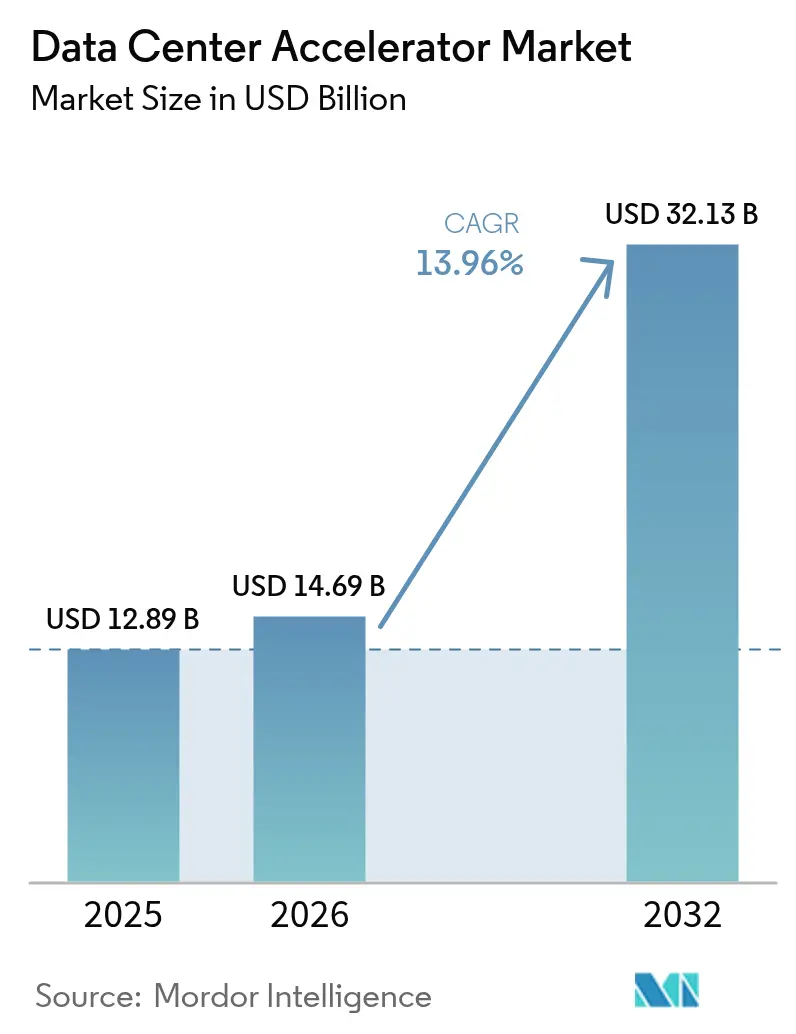

Data Center Accelerator market size in 2026 is estimated at USD 14.69 billion, growing from 2025 value of USD 12.89 billion with 2032 projections showing USD 32.13 billion, growing at 13.96% CAGR over 2026-2032. Escalating artificial-intelligence training cycles, the proliferation of hyperscale facilities, and the pivot toward GPU, ASIC, and other purpose-built chips are the primary engines behind this expansion. Sovereign-cloud programs, export-control regimes, and sustainability mandates are reshaping regional investment patterns, nudging buyers toward domestically sourced accelerators and greener infrastructure. Strained packaging-substrate capacity and high-bandwidth-memory shortages are tempering near-term hardware availability, prompting cloud providers to prioritize the highest-margin configurations. At the same time, liquid-cooling retrofits and renewable-power purchase agreements are emerging as critical selection criteria for capital projects, signaling that energy efficiency is now a competitive differentiator rather than a cost center.

Key Report Takeaways

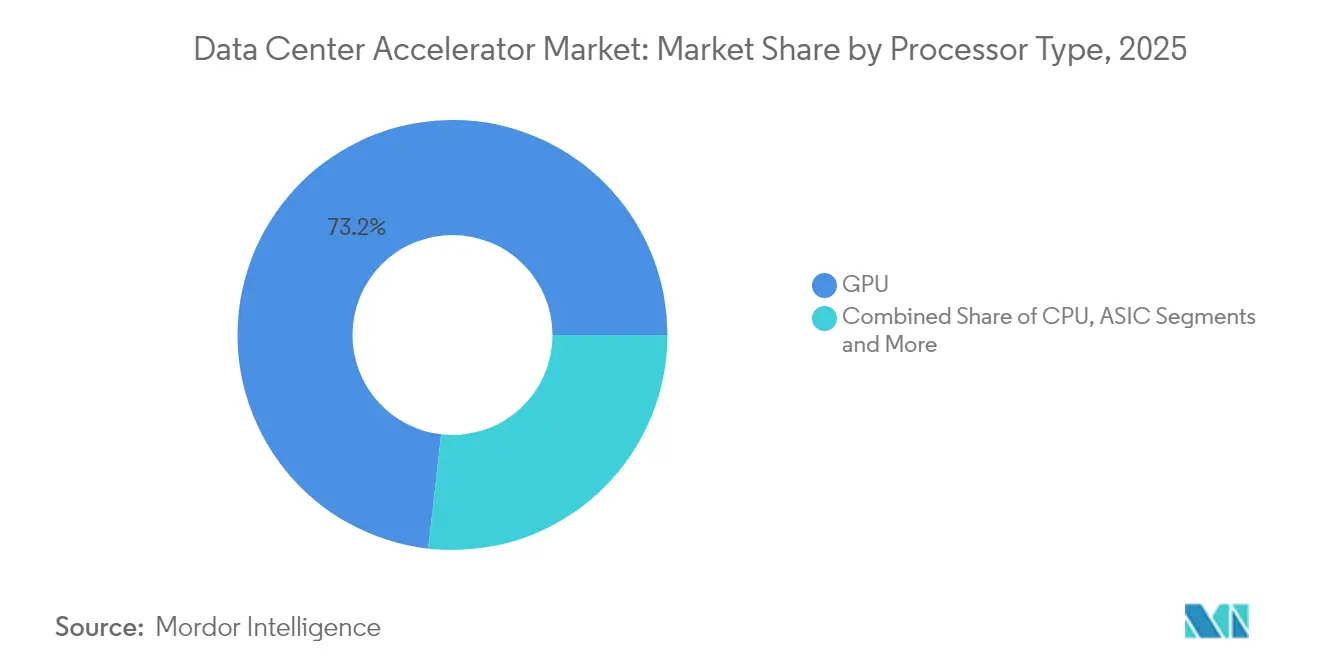

- By processor type, GPUs led with 73.20% revenue share in 2025; ASICs are projected to expand at a 15.42% CAGR through 2032.

- By application, AI training accounted for 49.30% of the Data Center Accelerator market share in 2025, while AI inference is advancing at a 15.55% CAGR through 2032.

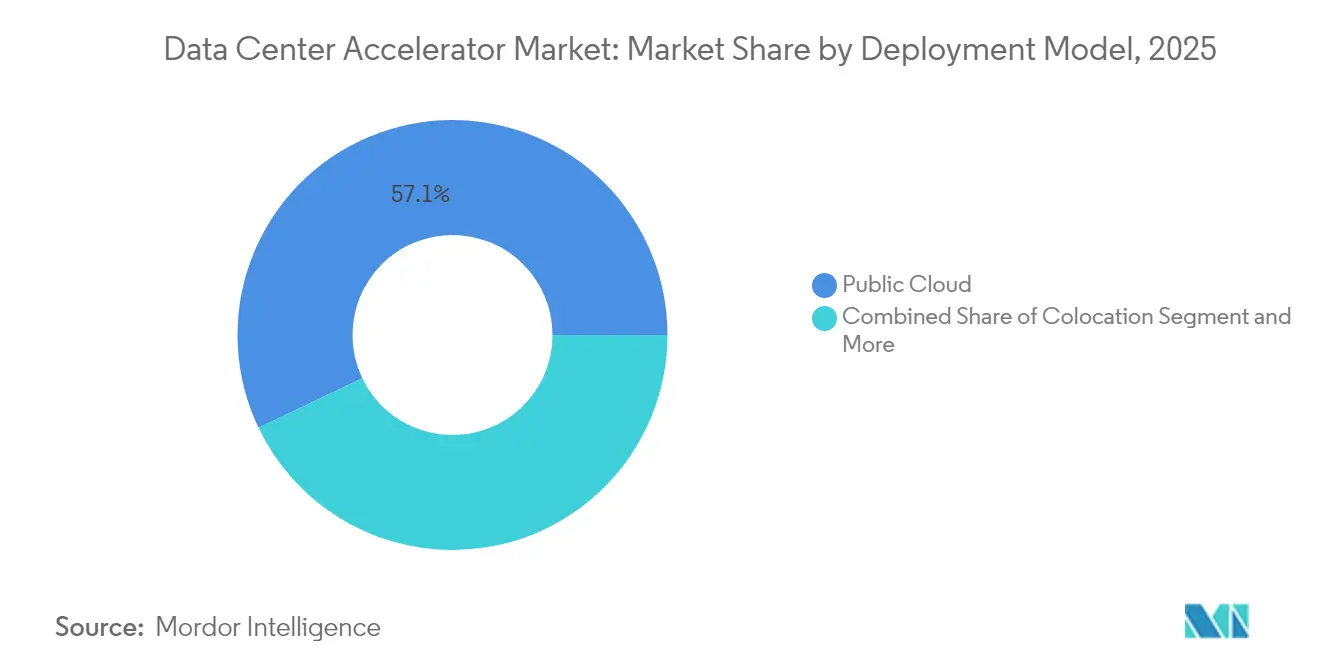

- By deployment model, public cloud captured 57.10% of the Data Center Accelerator market size in 2025; hybrid and edge configurations are expanding at a 15.72% CAGR to 2032.

- By end-user industry, IT and telecom held 39.40% revenue share in 2025, whereas healthcare and life sciences are forecast to grow at a 14.62% CAGR to 2032.

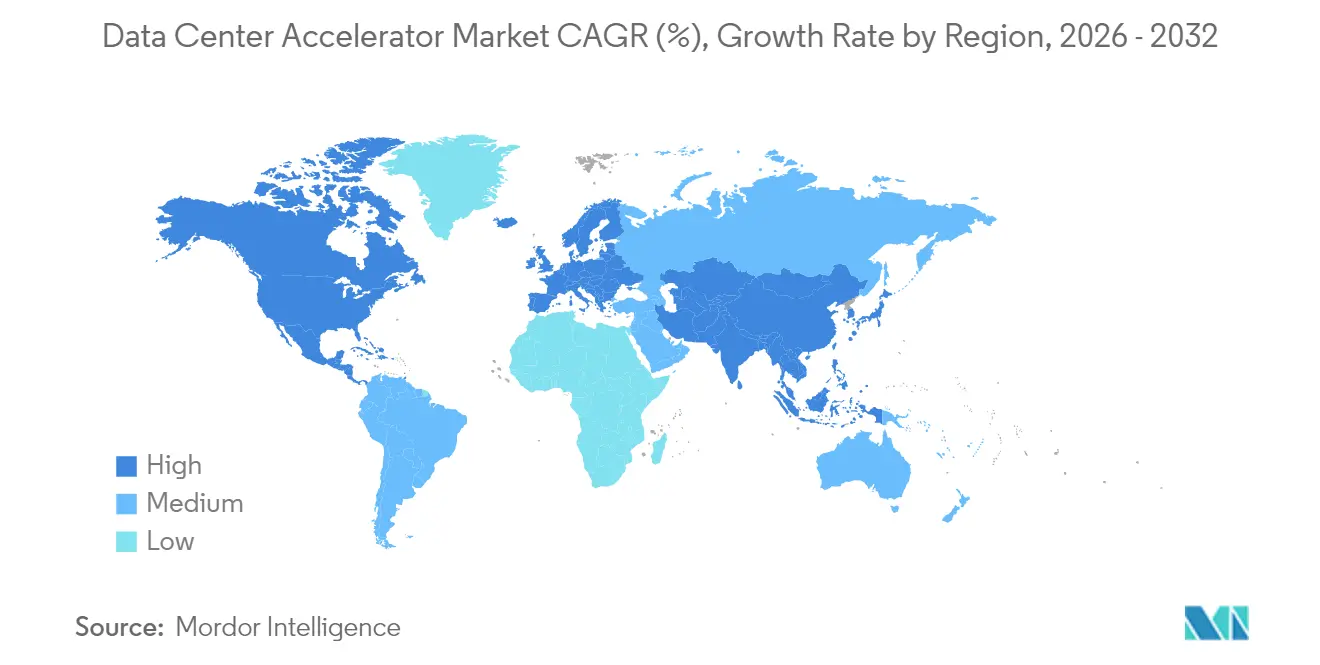

- By geography, North America retained the largest regional stake in 2025, while APAC is projected to record the fastest CAGR through 2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Center Accelerator Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging AI/ML training workloads in hyperscale data centers | +4.2% | North America, APAC | Medium term (2-4 years) |

| GPU scarcity driving cloud-based accelerator rentals | +2.8% | North America, Europe | Short term (≤ 2 years) |

| Rapid adoption of generative AI in SaaS platforms | +3.1% | North America, Europe | Medium term (2-4 years) |

| Quantum-inspired algorithms demanding heterogeneous accelerators | +1.5% | North America, Europe, APAC | Long term (≥ 4 years) |

| Edge-to-core workload orchestration | +2.3% | APAC, Europe | Medium term (2-4 years) |

| Sovereign-cloud programs subsidizing domestic accelerator fabs | +1.8% | APAC, MEA, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging AI/ML Training Workloads in Hyperscale Data Centers

Hyperscale operators now deploy data halls purpose-built for AI that demand 10–100 times more compute density than legacy enterprise workloads. Meta’s USD 800 million Indiana campus exemplifies the shift as it standardizes liquid-cooled racks to accommodate multi-petaflop GPU clusters. Microsoft earmarked more than USD 80 billion for U.S. AI facilities in fiscal-year 2025, underscoring the geographic clustering of training infrastructure. Amazon’s USD 100 billion multistate expansion further signals that cloud hyperscalers are pursuing scale economics, but every new megawatt must meet internal renewable-energy thresholds.[3]Datacenters.com Staff, “Amazon’s $100 Billion Data Center Expansion,” datacenters.com A balancing act is emerging as enterprises move from prototype models to inference pipelines, resulting in more heterogeneous rack designs that integrate GPU, CPU, and ASIC nodes. Financial institutions exemplify this dual-track buildout, allocating discrete GPU clusters for real-time fraud detection while maintaining CPU-heavy analytics farms for regulatory reporting.

GPU Scarcity Driving Cloud-Based Accelerator Rentals

Chronic shortages of premium GPUs have spawned GPU-as-a-Service platforms that decouple hardware ownership from usage. Oracle Cloud Infrastructure’s supercluster supports 16,384 AMD Instinct MI300X GPUs and offers consumption-based web portals, reducing procurement lead times from months to minutes.[1]Oracle Newsroom, “Oracle and AMD Collaborate to Help Customers Deliver Breakthrough Performance,” oracle.com Re-purposed cryptocurrency-mining sites in North America and Europe contribute power-dense real estate, allowing operators to monetize stranded electrical capacity. The rental model democratizes access for small and midsize organizations that could not previously justify the capital outlay for top-tier accelerators. Service providers also gain leverage when negotiating vendor allocations, enhancing resilience against single-supplier constraints.

Rapid Adoption of Generative AI in SaaS Platforms

Software-as-a-Service vendors are weaving generative AI directly into collaboration, customer-service, and analytics suites, a move that sharply increases inference transactions per active user. Together AI’s large-language-model cluster underscores hardware differences between inference and training; memory bandwidth and latency eclipse peak FLOPS as bottlenecks. Healthcare SaaS examples, such as diagnostic-imaging APIs, must process encrypted images in real time, thereby favoring ASICs tuned for small-batch inference. In financial services, real-time credit-risk models demand millisecond responses, driving adoption of in-memory computing fabrics. The result is a sustained market for accelerators optimized for power efficiency and deterministic latency rather than absolute throughput.

Quantum-Inspired Algorithms Demanding Heterogeneous Accelerators

Although practical quantum computers remain years away, quantum-inspired classical algorithms have entered pilot use in cryptography, portfolio optimization, and drug-discovery modeling. These workflows pair CPU pre-processing with GPU or FPGA emulation layers and call for hybrid system topologies unlike standard AI clusters. Government research programs and defense contracts are driving early funding, signaling a long-tail demand curve that begins in national laboratories and defense installations before filtering into commercial sectors.[2]Department of Defense, “AI-Enabled Detection System Set to Replace Aging Airspace Awareness System,” diu.mil Vendors able to blend quantum-simulation engines with mainstream accelerators will command a defensible niche as the market evolves.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Tight global supply of advanced packaging substrates | -2.1% | APAC manufacturing hubs | Short term (≤ 2 years) |

| Steep learning curve for heterogeneous programming models | -1.4% | Global | Medium term (2-4 years) |

| Rising Scope-3 emission targets constraining mega-GPU clusters | -1.8% | North America, Europe, APAC | Medium term (2-4 years) |

| Export-control regimes on high-end GPUs and ASICs | -1.2% | China, Russia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight Global Supply of Advanced Packaging Substrates

Accelerators that integrate HBM stacks and chiplets rely on Ajinomoto Build-Up Film and CoWoS packaging, materials now subject to year-long lead times. Suppliers prioritize high-margin SKUs, leaving smaller vendors scrambling for limited allocations. Organic-interposer experimentation is underway but will not meaningfully ease constraints for at least two production cycles. Taiwan and South Korea have announced aggressive substrate-capacity expansions, yet the ramp window extends beyond current demand inflection points.

Steep Learning Curve for Heterogeneous Programming Models

As chips diversify, developers must adopt multiple toolchains, from CUDA to ROCm to vendor-specific SDKs. Skill shortages increase integration costs and prolong proof-of-concept timelines. Open-standard efforts such as OneAPI attempt to bridge gaps, but mismatched release cadences across hardware generations complicate maintenance. Emerging markets face the steepest hurdles because local universities lag in specialized curriculum offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processor Type: ASICs Emerge as Inference Champions

GPU processors retained a 73.20% stake in 2025, reflecting their versatility across both model-training and inference tasks. ASIC shipments, however, are projected to rise at a 15.42% CAGR to 2032 as enterprises tune for lower power draw during steady-state inference workloads. Google’s internally developed TPU v6 exemplifies the in-house silicon trend that balances performance and cost. Meanwhile, AMD’s Instinct MI350 family expands HBM capacity to 288 GB, targeting memory-bound transformer models. CPU sockets still orchestrate I/O and housekeeping tasks, while FPGA cards maintain relevance in telecom edge nodes that call for deterministic latency.

ASIC growth illustrates shifting buyer priorities. Power budgets inside co-location cages rarely scale linearly with rack density, driving operators to favor TOPS-per-watt metrics. Inference-dense SaaS offerings, such as customer-support chatbots and real-time personalization engines, require predictable latency that ASIC designs now deliver. Training workloads will still concentrate on multi-GPU clusters, yet a portion of compute cycles migrates to specialized tensor engines integrated into next-gen GPUs, blurring categorical boundaries. Overall, processor diversity strengthens vendor competition, offering buyers leverage on pricing and supply continuity.

By Application: AI Inference Accelerates Past Training

AI training accounted for 49.30% of Data Center Accelerator market revenue in 2025, but inference workloads will record a faster 15.55% CAGR through 2032. Businesses once content with pilot projects are now releasing chatbots, recommendation models, and image-analysis services into production, where latency slippage translates directly into customer churn. High-performance computing remains a stable niche centered on weather modeling, genomics, and computational fluid dynamics, relying on GPUs with larger HBM stacks rather than pure ASICs.

Inference growth ripples across hardware selection. Batch-size variability and strict service-level agreements necessitate accelerators that optimize memory bandwidth over raw floating-point throughput. Healthcare providers employ inference-optimized boards to perform diagnostic imaging at the point of care, shortening time to diagnosis for conditions such as stroke. Financial institutions likewise leverage accelerators for real-time risk scoring, embedding compute nodes inside private-cloud environments for regulatory compliance. The expanding application mix will continue to diversify purchase criteria, with software ecosystem maturity increasingly tipping buying decisions.

By Deployment Model: Hybrid Edge Configurations Drive Growth

Public-cloud tenants consumed 57.10% of Data Center Accelerator market size in 2025. But hybrid-edge installations will expand at a 15.72% CAGR as organizations co-locate inference engines closer to data sources. Telcos upgrade central offices into micro-data centers to process traffic from autonomous vehicles and augmented-reality streams. Co-location providers respond with liquid-cooling retrofits and sovereign-cloud zones to court regulated industries.

On-premise options regain traction where data-sovereignty or cost-predictability outweigh hyperscale convenience. Retailers, for example, run video analytics on in-store edge servers to avoid backhaul latency. Development teams still burst training jobs into the public cloud but increasingly repatriate models for inference. The resulting architectural pluralism fuels demand for management platforms that orchestrate workloads across clouds, co-location sites, and customer campuses.

By End-User Industry: Healthcare Leads Growth Trajectory

IT and telecom operators represented 39.40% of 2025 revenue as carriers modernized networks for 5G core slicing and network-function virtualization. Healthcare and life sciences, however, will be the fastest-growing vertical at a 14.62% CAGR to 2032. Genomics pipelines depend on petabyte-scale throughput, while diagnostic-imaging instruments require AI inference at the edge to guide physicians in real time. Gretel’s synthetic-data services employ accelerators to generate privacy-preserving datasets, helping hospitals comply with stringent regulatory frameworks.

Financial-services workloads focus on nanosecond-level fraud detection and algorithmic trading simulations, necessitating dedicated accelerator pools inside private clouds. Government and defense users, bolstered by multihundred-million-dollar AI procurement programs, favor secure, air-gapped infrastructures. Media and entertainment studios adopt GPU render farms to accelerate content creation and real-time streaming. These diverse requirements sustain market momentum and foster specialization among chip vendors and system integrators.

Geography Analysis

North America remains the largest buyer, underpinned by hyperscale capital-expenditure plans from Amazon, Microsoft, and Google. Microsoft’s spending alone surpasses USD 80 billion for domestic facilities in 2025. Canada and Mexico emerge as near-shore options that balance power-cost and latency considerations while staying within North American regulatory frameworks.

APAC will post the highest CAGR, buoyed by sovereign-cloud mandates and the construction of enormous campuses such as South Korea’s USD 35 billion complex. China advances domestic accelerators like Huawei’s Ascend series to navigate export-control limitations. Japan’s Rapidus consortium and SoftBank’s chip initiatives, aided by public funding, aim to reclaim semiconductor manufacturing relevance.

Europe’s GAIA-X and IPCEI-CIS programs foster cross-border data-sovereignty clouds. Blackstone’s USD 13 billion UK data-center commitment underscores investor confidence in regional AI demand. Middle East and Africa growth hinges on sovereign wealth-fund backing, with energy-price advantages supporting power-hungry installations in the UAE and Saudi Arabia.

Competitive Landscape

The Data Center Accelerator market displays moderate concentration. NVIDIA dominates training clusters, yet AMD compresses its GPU road map, advancing MI350 launch to early 2025 to win hyperscale sockets. Intel positions Gaudi accelerators for price-performance niches, while Google and Amazon field proprietary TPUs and Inferentia chips to reduce merchant-silicon reliance.

Architectural diversity invites nimble entrants. Cerebras targets wafer-scale AI, Tenstorrent pushes RISC-V designs, and Alibaba’s Hanguang line serves domestic Chinese clouds. Software ecosystems become decisive; vendors bundle compilers, low-level APIs, and model-optimization utilities to lock in developers. Supply-chain risk reshapes sourcing strategies as customers dual-source GPU and ASIC boards to hedge against substrate shortages.

Strategic deals underscore the arms race. Oracle partners with AMD to deploy MI300X superclusters, offering customers an NVIDIA alternative. Microsoft collaborates with liquid-cooling specialists for on-premise clusters in high-density zones. Patent filings in chiplet interconnects surge as firms seek defensible IP positions, evidencing a pivot from monolithic dies to modular architectures.

Data Center Accelerator Industry Leaders

Intel Corporation

NVIDIA Corporation

Advanced Micro Devices Inc.

Achronix Semiconductor Corporation

Xilinx Inc. (Advanced Micro Devices Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Red Hat launched the llm-d community for scalable generative AI inference, supported by CoreWeave, Google Cloud, IBM Research, and NVIDIA, focusing on native Kubernetes architecture and vLLM-based distributed inference capabilities.

- February 2025: AMD announced Instinct MI325X accelerators with 256GB HBM3e memory and 6TB/s bandwidth, promising 1.4x higher inference performance compared to competitors and enabling businesses to achieve better results with fewer GPUs.

- October 2024: MITRE launched the Federal AI Sandbox in partnership with NVIDIA, featuring a USD 20 million supercomputer powered by NVIDIA DGX SuperPOD with 248 H100 GPUs for secure federal agency AI development and deployment.

- October 2024: AMD delivered leadership AI performance with MI325X accelerators featuring 1.3x greater peak theoretical compute performance, entering production shipments in Q4 2024 with widespread availability expected in Q1 2025

Global Data Center Accelerator Market Report Scope

Datacenter accelerators are hardware designed and used to process visual data. It is a hardware device or software program that improves the overall performance of computers. Datacenter accelerators help increase consumer-driven data demand and use AI-based services to drive the demand for AI-centric data centers.

The Global Data Center Accelerator Market is segmented by processor type (CPU, GPU, FPGA, ASIC), application (high-performance computing, artificial intelligence), and geography (North America, Europe, Asia Pacific, Latin America, Middle East & Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| CPU |

| GPU |

| FPGA |

| ASIC |

| High-Performance Computing |

| Artificial Intelligence Training |

| Artificial Intelligence Inference |

| Other Workloads |

| On-Premise/ Enteprise/Edge |

| Colocation |

| Public Cloud |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Government and Defense |

| Media and Entertainment |

| Others End Users |

| North America | United States | |

| Mexico | ||

| Canada | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Processor Type | CPU | ||

| GPU | |||

| FPGA | |||

| ASIC | |||

| By Application | High-Performance Computing | ||

| Artificial Intelligence Training | |||

| Artificial Intelligence Inference | |||

| Other Workloads | |||

| By Deployment Model | On-Premise/ Enteprise/Edge | ||

| Colocation | |||

| Public Cloud | |||

| By End-user Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| Media and Entertainment | |||

| Others End Users | |||

| By Geography | North America | United States | |

| Mexico | |||

| Canada | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is demand for accelerators expected to grow through 2032?

The Data Center Accelerator market is projected to rise at a 13.96% CAGR, more than doubling from USD 12.89 billion in 2025 to USD 32.13 billion by 2032.

Which processor segment will gain the most share by 2032?

ASIC-based accelerators are forecast to post a 15.42% CAGR, narrowing the gap with GPUs for inference-heavy workloads.

Why are enterprises adopting hybrid and edge deployments?

Latency-sensitive 5G, autonomous-vehicle, and industrial-IoT workloads require local inference, driving a 15.72% CAGR for hybrid-edge installations.

What is the biggest restraint facing accelerator suppliers today?

Shortages of advanced packaging substrates such as ABF and CoWoS limit near-term production capacity, dampening shipment growth by an estimated 2.1 percentage points.

Which industry vertical shows the fastest spending growth?

Healthcare and life sciences will lead with a 14.62% CAGR as genomics, drug-discovery, and diagnostic-imaging workflows demand specialized compute.

Page last updated on: