Africa Dog Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

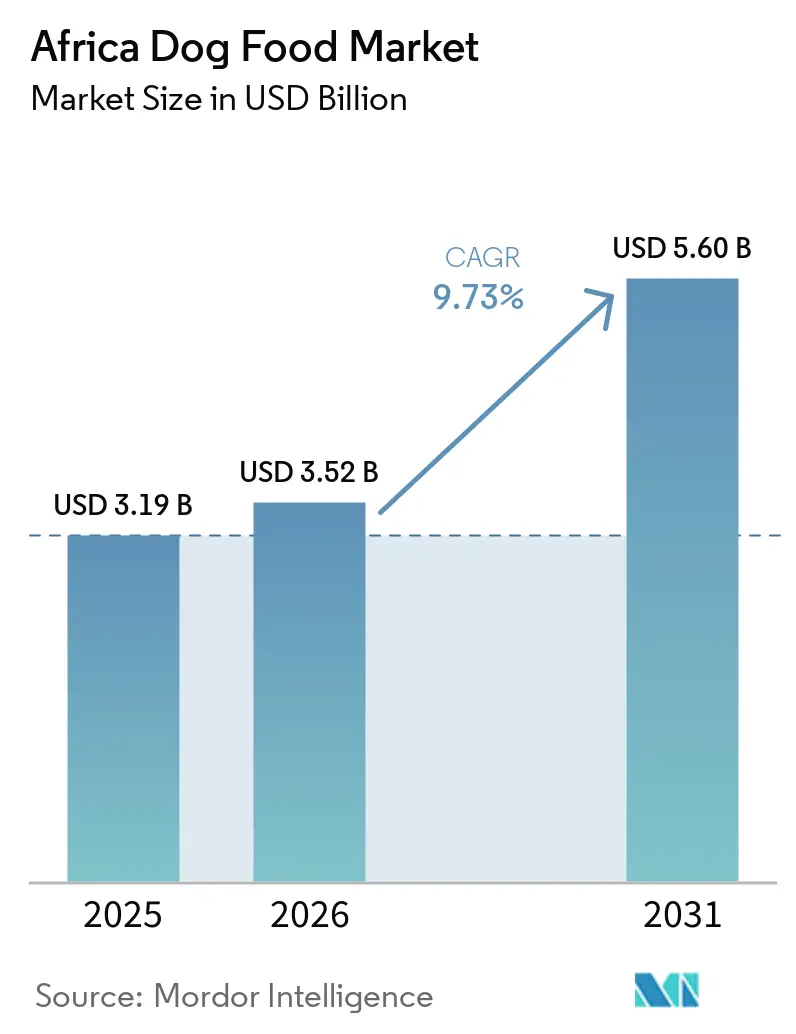

| Base Year Market Size (2025) | USD 3.19 Billion |

| Market Size (2026) | USD 3.52 Billion |

| Market Size (2031) | USD 5.60 Billion |

| Growth Rate (2026 - 2031) | 9.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Dog Food Market Analysis by Mordor Intelligence

The Africa dog food market size was USD 3.19 billion in 2025 and is projected to grow from USD 3.52 billion in 2026 to USD 5.60 billion by 2031 at 9.73% CAGR during the forecast period (2026-2031). Africa experienced the highest year-on-year growth in pet food production globally in 2025, with a significant increase in output. South Africa accounted for the largest share of this growth, indicating a stronger regional supply base for the Africa dog food market. Additionally, South Africa’s official household survey released by Statistics South Africa highlights a substantial and well-defined dog population across millions of households in 2025, providing a more reliable baseline for demand compared to earlier estimates of the Africa dog food market. The pet care market in South Africa continued to grow, driven by the increasing presence of organized retail formats. This has improved product availability and enhanced brand visibility within the Africa dog food market. Factors such as rising pet humanization, expanding retail formalization, and greater involvement from veterinary professionals are supporting consistent consumer spending. Despite household budget constraints, these trends contribute to a positive medium-term growth outlook. The market, however, remains relatively concentrated among leading players. Recent product recall incidents have influenced shelf space allocation, favoring more trusted brands. This underscores the growing importance of execution, product quality, and consumer trust, alongside scale, in shaping competition within the Africa dog food market.

Key Report Takeaways

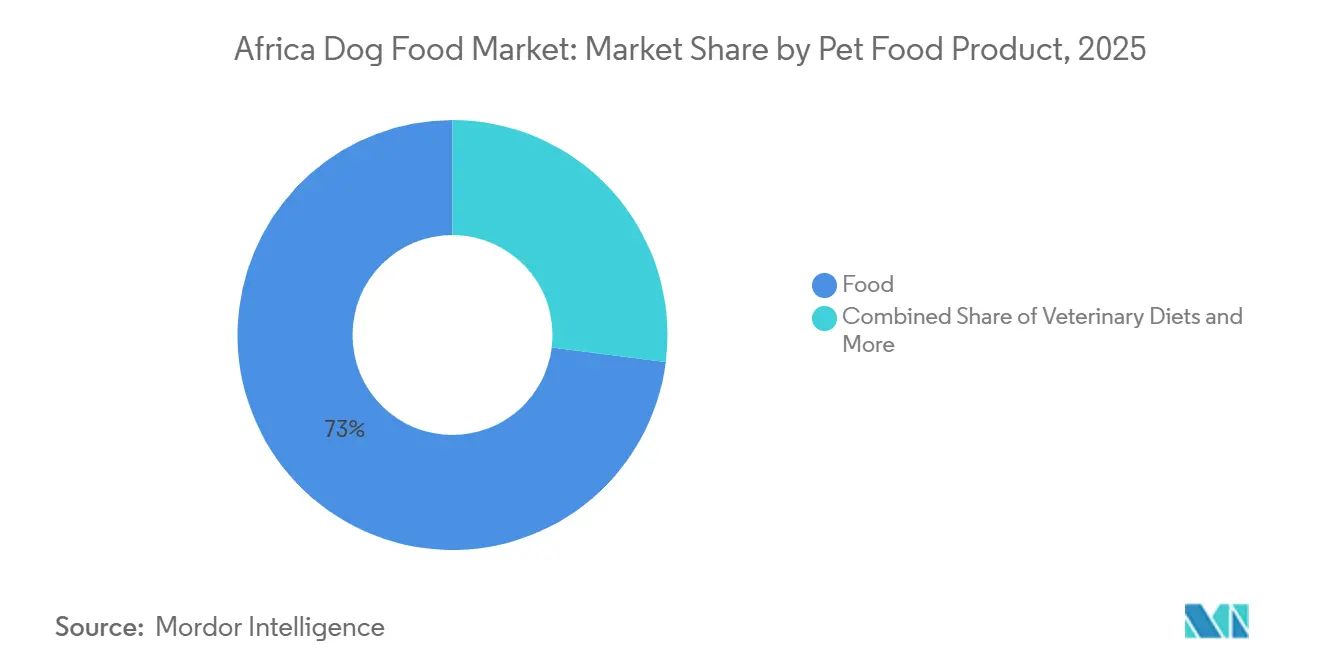

- By pet food product, food held 73.0% of the Africa dog food market share in 2025, while pet veterinary diets are projected to expand at an 11.5% CAGR through 2031.

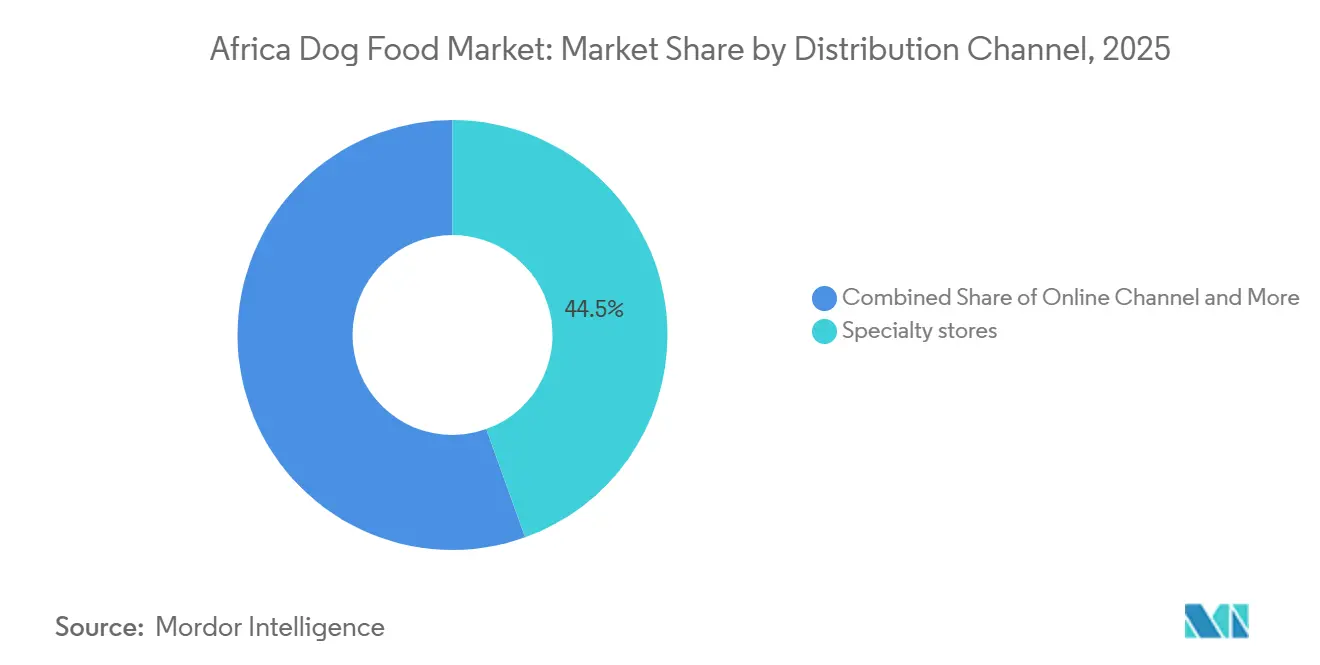

- By distribution channel, specialty stores accounted for 44.5% of the Africa dog food market size in 2025, while the online channel is forecast to grow at an 11.7% CAGR through 2031.

- By geography, South Africa held 18.0% share of the Africa dog food market in 2025 and is also projected to record the fastest growth at 11.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Dog Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising premiumization of dog food purchases | +2.2% | South Africa, Morocco, Egypt, Kenya, Nigeria | Short term (≤ 2 years) |

| Expansion of modern retail and specialty pet retail | +1.8% | South Africa, Morocco, Egypt, Kenya | Medium term (2-4 years) |

| Growth in urban dog ownership and smaller household pet spending | +1.5% | South Africa, Nigeria, Kenya, Egypt | Medium term (2-4 years) |

| Expansion of e-commerce and last-mile pet supply delivery | +1.3% | South Africa, Nigeria, Kenya | Short term (≤ 2 years) |

| Rising veterinary awareness of preventive nutrition | +1.0% | South Africa, Egypt, Morocco | Medium term (2-4 years) |

| Development of local manufacturing and private label offerings | +0.8% | South Africa, Kenya, Nigeria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Premiumization of Dog Food Purchases

Premiumization is emerging as a sustained spending trend in the Africa dog food market, extending beyond higher-income groups. Retail performance data indicates that spending on pet food has outpaced general consumer inflation, highlighting a stronger consumer focus on pet care. This shift is closely tied to changing owner perceptions, with many pet owners increasingly treating their pets as family members. This change is significant as it stabilizes food spending, even when households cut back on other discretionary expenses. Pet care spending has remained resilient under broader budget pressures, and the overall pet care market has shown steady growth. Products with better ingredients, health-focused attributes, and trusted brands are capturing a larger share of consumer spending. This trend is driving a higher-value product mix in the market, particularly in categories such as dry food, supplements, and therapeutic products, where brand trust is stronger. Additionally, it is creating opportunities for premium private-label offerings from organized retailers. These retailers are increasingly leveraging health-focused positioning rather than relying solely on price to encourage repeat purchases. This approach keeps value growth ahead of volume growth and enhances margin potential.

Expansion of Modern Retail and Specialty Pet Retail

Formal retail expansion is a significant driver of category growth in the Africa dog food market. In South Africa, corporate grocery groups have rapidly expanded specialty pet retail formats, with national networks such as Checkers Petshop Science, Absolute Pets (Woolworths), and SPAR Pet Storey projected to reach a combined total of approximately 350 outlets by 2026[1]Source: Business Explainer, “South Africa’s R10.4bn Pet Boom,” Business Explainer, businessexplainer.co.za.. Additionally, the introduction of premium, locally produced private-label dry dog food ranges across large store networks and online platforms has supported category growth by enabling better control over product assortment and pricing. Modern retail plays a crucial role not only by selling products but also by influencing consumer behavior through health claims, breed-specific product placement, and enhanced shelf comparisons. This educational impact is particularly important for first-time commercial feeders transitioning from table feeding to branded packaged food. A similar trend is emerging in North African cities, where grocery modernization and the rise of local brands are increasing category visibility in markets such as Morocco and Egypt. As these networks expand, the Africa dog food market benefits from improved access, stronger merchandising, and more stable distribution channels for premium and veterinary product segments.

Growth in Urban Dog Ownership and Smaller Household Pet Spending

Urban household formation is expanding the consumer base for the Africa dog food market. According to Statistics South Africa, there were 7.4 million dogs across 4.2 million households in 2025, with Gauteng and the Western Cape identified as key regions with high pet ownership[2]Source: Statistics South Africa, “General Household Survey 2025, Pet Ownership Module,” News24, news24.com. These areas support formal pet retail and regular product replenishment. The concentration of pets in larger urban centers enhances store profitability, as repeat demand sustains dedicated pet retail formats and faster delivery services. Additionally, urban areas continue to generate new pet-owning households, ensuring a steady influx of consumers into the market. A growing willingness to invest in higher-quality pet nutrition is evident beyond South Africa, signaling emerging demand for premium and organic products across various African markets. Furthermore, smaller household structures often lead to higher spending per pet, as pets increasingly become integral to household budgets rather than serving solely functional roles. This trend drives demand for branded products, treats, and improved feeding practices, gradually increasing the overall market value. As urban households prioritize convenience and packaged solutions, the Africa dog food market benefits from a larger base of repeat buyers, reducing reliance on occasional premium purchases.

Expansion of E-Commerce and Last-Mile Pet Supply Delivery

Digital retail is enhancing access and product variety in the African dog food market, particularly in major urban areas, where heavy pet food packs can be effectively delivered through organized delivery networks. The online channel is anticipated to experience the fastest growth in distribution, driven by a shift toward app-based repeat purchases and subscription models. The entry of prominent e-commerce platforms into South Africa, along with the growth of rapid-delivery services, has increased competition for convenience, visibility, and direct fulfillment. This development is significant because physical retail shelf space often cannot accommodate the full range of veterinary, breed-specific, or premium products that consumers increasingly seek. Suppliers are responding by offering larger pack sizes and formats tailored to online purchasing preferences. Furthermore, digital access is enabling peri-urban consumers to purchase branded products without relying on nearby specialty stores. Consequently, e-commerce is not only gaining market share from physical retail but also broadening the market's formal reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility and currency pressure on imported inputs | -1.5% | South Africa, Nigeria, Kenya, rest of sub-Saharan Africa | Medium term (2-4 years) |

| Limited cold chain and warehouse coverage in secondary cities | -0.8% | Secondary cities across sub-Saharan Africa | Medium term (2-4 years) |

| Price sensitivity in mass-market dog food segments | -1.2% | South Africa, Nigeria, Kenya, rest of Africa | Short term (≤ 2 years) |

| Informal channel competition and counterfeit product leakage | -0.9% | South Africa, Nigeria, Kenya | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Volatility and Currency Pressure on Imported Inputs

Input cost volatility remains a significant constraint on the growth of the African dog food market. Alltech’s 2026 Agri-Food Outlook identified grain prices and currency fluctuations as critical factors influencing feed performance across Africa and the Middle East, underscoring the persistent instability of raw materials. This challenge is further exacerbated by the limitations of local substitution, as weaker quality control measures can introduce additional risks. For instance, in November 2025, the National Consumer Commission reported the recall of multiple dry pet food brands by RCL FOODS Limited due to elevated levels of Deoxynivalenol in maize used in production, impacting 55,352 bags of pet food [3]Source: National Consumer Commission South Africa, “Product Recall, Various Dry Pet Foods Supplied by RCL Foods,” National Consumer Commission, thencc.org.za. This incident highlighted how reliance on cheaper local inputs, without robust testing standards, can harm brand reputation and erode channel confidence. Producers with stronger process controls are better equipped to manage such risks, emphasizing supply chain design to ensure ingredient quality and operational efficiency. However, volatility in grain prices, exchange rates, and imported additives continues to exert pressure on pricing strategies within the Africa dog food market. When costs escalate rapidly, suppliers face the dilemma of either absorbing reduced margins or passing price increases onto consumers, who are often highly price-sensitive. This dynamic slows the adoption of premium products and may drive households toward lower-cost feeding practices.

Limited Cold Chain and Warehouse Coverage in Secondary Cities

Infrastructure limitations in secondary cities continue to restrict the growth of the Africa dog food market beyond its reliance on dry food. Dry kibble remains the dominant product due to its ambient shelf stability, which facilitates storage and transportation in regions with limited refrigeration and specialized warehousing. These same constraints hinder the scalability of wet food and higher-value formats outside major urban centers, even when demand exists. Additionally, heavy-format SKUs have historically had limited e-commerce penetration, though improvements in delivery systems are beginning to address this, highlighting the significant role logistics play in shaping the product mix. While specialty stores and modern retail outlets support distribution in densely populated metropolitan areas, the market's broader expansion into smaller cities depends on enhanced warehousing and last-mile infrastructure. The lack of a robust cold chain also slows the distribution of fresh, therapeutic, or premium wet food formats, impacting their ability to reach new consumers in optimal condition. Consequently, market expansion typically begins with stable dry formulas, with more specialized products introduced later. This dynamic does not halt growth but delays product diversification, leading to uneven regional scaling and, as reflected in market performance, uneven market performance. Until storage and logistics infrastructure improve further, these factors will continue to influence product assortment and value realization in the Africa dog food market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Food Product: Veterinary Diets Outpace Mainstream Food Categories

The food segment accounted for 73.0% of the African dog food market share in 2025, establishing it as the largest product category. This dominance is attributed to the widespread use of dry kibble as the primary commercial feeding option across various income groups, owing to its affordability, flexible packaging options, and ambient stability. In comparison, wet pet food and pet treats represent smaller segments but are gaining popularity as urban pet owners incorporate toppers, snacks, and reward-based feeding into their dogs' dry food routines. Additionally, nutraceuticals and supplements are emerging as a premium segment, particularly in products containing probiotics, omega-3 fatty acids, vitamins, minerals, and milk bioactives, reflecting the growing emphasis on health-focused feeding in the African dog food market.

Pet veterinary diets are anticipated to grow at a CAGR of 11.5% from 2026 to 2031, making them the fastest-growing product segment in the African dog food market. The broader veterinary nutrition category is also gaining traction, driven by increasing clinical confidence and improved distribution networks. Currently, derma diets and digestive sensitivity products lead in volume, while formulations targeting renal health and obesity are expanding as the management of chronic conditions becomes more prevalent. The growth of therapeutic nutrition beyond South Africa indicates a broader regional adoption trend. This development is significant, as veterinary diets rely heavily on professional recommendations and consumer trust, resulting in stronger pricing power and higher customer retention rates compared to mainstream pet food products.

By Distribution Channel: Online Channel Disrupts Specialty Store Dominance

Specialty stores accounted for 44.5% of revenue in 2025, making them the largest distribution channel in the Africa dog food market. This dominance was driven by South Africa’s rapid expansion of dedicated pet retail outlets established by major grocery-linked groups. These developments provided branded suppliers with enhanced category presentation and a broader product assortment. Supermarkets and hypermarkets represented the second-largest distribution channel, continuing to support the widespread distribution of mainstream dry dog food at a national level. Convenience stores remained significant for frequent, small-pack purchases in township and peri-urban areas. Other channels included veterinary clinics and farm supply outlets, which focused on therapeutic and preventive product lines.

The online channel is projected to grow at a CAGR of 11.7% from 2026 to 2031, making it the fastest-growing distribution format in the Africa dog food market. The entry of major e-commerce platforms in South Africa, along with the expansion of rapid delivery services, has improved access to bulky dry food and premium stock-keeping units (SKUs) that were previously challenging to distribute through digital channels. Suppliers are also adapting pack formats to align with online purchasing behavior, signaling that digital retail is transitioning into a primary growth channel rather than a supplementary option. Online platforms are particularly critical in peri-urban areas where specialty retail networks are less developed. As logistics and last-mile delivery systems continue to advance, digital access is anticpated to bridge the gap in product availability between major urban centers and smaller markets, thereby broadening the overall reach of the Africa dog food market.

Geography Analysis

In 2025, South Africa accounted for 18.0% of the Africa dog food market share and is projected to grow at a CAGR of 11.2% through 2031, maintaining its position as the largest and fastest-growing national market in the region. The country produced two-thirds of Africa’s pet food volume in 2025, solidifying its role as the continent's central supply hub[4]Source: Alltech, “2026 Agri-Food Outlook, Global Pet Food Production,” Pet Food Processing, petfoodprocessing.net. South Africa’s competitive advantage stems from a combination of factors, including a large owned dog population, a robust specialty store network, and a more developed veterinary infrastructure. Even disruptions caused by product recalls highlight the market’s maturity, as branded share shifts occur through formal channels and visible shelf reallocation. This reflects a structured retail environment in which competition is driven by brand positioning, product quality, and consumer trust in the Africa dog food market.

The rest of Africa accounted for the majority share of total revenue, indicating that the combined opportunity outside South Africa represents a larger volume pool in the Africa dog food market. Nigeria stands out for its large urban consumer base, though commercial feeding continues to compete with traditional household feeding practices. Kenya is advancing more rapidly in formal supply chains, as recent expansion by local producers highlights the scalability of domestic production when demand aligns with regional export routes. Morocco has also shown steady progress in formalization, with increasing visibility for both local and imported brands supporting market development. These trends indicate that while South Africa remains the most developed market, the rest of Africa is gradually expanding through improved supply chains, urban demand growth, and rising product awareness, contributing to a broader, more diversified growth base.

Egypt is emerging as a key growth market in North Africa, particularly in the area of therapeutic nutrition. The launch of veterinary diet product lines demonstrates the growing commercial relevance of the veterinary channel beyond South Africa. This development underscores Egypt’s potential as an entry point for specialized pet food products in the region. The Africa dog food market is characterized by a mature anchor market in South Africa and a set of emerging markets that are scaling up through urbanization, local production, and formal retail expansion. However, growth across the region remains uneven due to variations in logistics, price sensitivity, and retail infrastructure. Despite these challenges, the market is no longer reliant on a single geography for momentum. South Africa continues to serve as the operational hub, while the broader region contributes to the next phase of demand growth.

Competitive Landscape

The Africa dog food market was moderately concentrated in 2025. Mars, Incorporated held the leading market share, driven by the widespread presence of Pedigree across both mainstream and premium price segments. Nestlé S.A. (Purina) followed, leveraging Purina’s science-based positioning and strong brand presence across various pet nutrition categories. Colgate-Palmolive Company, through Hill’s Pet Nutrition, Inc., maintained a significant presence in the higher-value clinical and premium segments. Meanwhile, Montego Pet Nutrition and RCL FOODS Limited remained key African-based players with robust local channel networks. This market structure indicates that while leadership is significant, it is not absolute, and operational missteps can quickly impact market share within the Africa dog food market.

Competitive dynamics changed significantly following RCL FOODS Limited's product recall events in November 2025 and March 2026, which created opportunities for competitors in formal grocery and pet specialty channels. Montego Pet Nutrition enhanced its market position when Monic Group completed the acquisition of Marltons Pet Care in March 2026, expanding its presence across both food and non-food pet care categories[5]Source: RCL FOODS, “RCL Foods Expands into Pet Care with USD 36M Acquisition of Martin and Martin,” Feed Business MEA, feedbusinessmea.com. Additionally, strategic acquisitions targeting wet pet food, treats, and biscuits suggest that companies are actively working to capture a larger share of the value chain. Simultaneously, global players have entered the fresh pet food segment through acquisitions, reflecting an increasing focus on higher-value and differentiated product offerings.

Global companies are combining strong brand presence with consistent investment, while local companies capitalize on their proximity, manufacturing control, and understanding of regional markets. International players are increasing production capacity and enhancing innovation capabilities, emphasizing long-term goals of efficiency and product development. Meanwhile, African-based companies are demonstrating competitiveness through quality and innovation rather than relying solely on price, supported by certified manufacturing processes and an expanding export footprint. Additionally, premium and therapeutic-focused companies are intensifying competition by forming veterinary partnerships and offering specialized products. With no single company dominating therapeutic distribution in the region, the Africa dog food market remains open to new entrants and ongoing shifts in market share.

Africa Dog Food Industry Leaders

Mars, Incorporated

Nestlé S.A. (Purina)

Colgate-Palmolive Company (Hill’s Pet Nutrition, Inc.)

Montego Pet Nutrition

RCL FOODS Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.) launched new Prescription Diet therapeutic formulations targeting kidney, skin, and gastrointestinal conditions. These launches reinforce growth in the veterinary nutrition segment, which is expanding in key African pet care markets.

- April 2026: RCL FOODS Limited announced the acquisition of Martin & Martin (Husky, Pamper, Beeno, Bob Martin brands) from Simrose Overseas S.A. for USD 36 million, subject to regulatory approval. The deal expands RCL FOODS Limited beyond dry food into wet pet food, treats, and biscuits, positioning it as a more diversified Africa pet food platform.

- March 2026: Montego Pet Nutrition acquired Marltons Pet Care, merging two of South Africa’s established pet care businesses and creating broader coverage across food, accessories, and grooming.

Africa Dog Food Market Report Scope

Pet foods are usually intended to provide complete and balanced nutrition to the pet, but are primarily used as functional products. The scope includes the food and supplements consumed by pets, including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

The Africa Dog Food Market Report is Segmented by Pet Food Product (Food, Pet Nutraceuticals/Supplements, Pet Treats, and Pet Veterinary Diets), by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and Other Channels), and by Geography (South Africa and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Food | Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||

| Wet Pet Food | ||

| Pet Nutraceuticals/Supplements | Milk Bioactives | |

| Omega-3 Fatty Acids | ||

| Probiotics | ||

| Proteins and Peptides | ||

| Vitamins and Minerals | ||

| Other Pet Nutraceuticals/Supplements | ||

| Pet Treats | Crunchy Treats | |

| Dental Treats | ||

| Freeze-Dried and Jerky Treats | ||

| Soft and Chewy Treats | ||

| Other Pet Treats | ||

| Pet Veterinary Diets | Derma Diets | |

| Diabetes | ||

| Digestive Sensitivity | ||

| Obesity Diets | ||

| Oral Care Diets | ||

| Renal | ||

| Urinary Tract Disease | ||

| Other Pet Veterinary Diets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Distribution Channels |

| South Africa |

| Rest of Africa |

| By Pet Food Product | Food | Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||

| Wet Pet Food | |||

| Pet Nutraceuticals/Supplements | Milk Bioactives | ||

| Omega-3 Fatty Acids | |||

| Probiotics | |||

| Proteins and Peptides | |||

| Vitamins and Minerals | |||

| Other Pet Nutraceuticals/Supplements | |||

| Pet Treats | Crunchy Treats | ||

| Dental Treats | |||

| Freeze-Dried and Jerky Treats | |||

| Soft and Chewy Treats | |||

| Other Pet Treats | |||

| Pet Veterinary Diets | Derma Diets | ||

| Diabetes | |||

| Digestive Sensitivity | |||

| Obesity Diets | |||

| Oral Care Diets | |||

| Renal | |||

| Urinary Tract Disease | |||

| Other Pet Veterinary Diets | |||

| By Distribution Channel | Convenience Stores | ||

| Online Channel | |||

| Specialty Stores | |||

| Supermarkets/Hypermarkets | |||

| Other Distribution Channels | |||

| By Geography | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Africa dog food sector?

The current size of the Africa dog food sector is USD 3.52 billion in 2026.

Which product category leads revenue in Africa?

Food is the largest category, with 73.0% revenue share in 2025, mainly because dry kibble remains the core commercial feeding format across income groups.

Which distribution channel is growing the fastest?

The online channel is the fastest-growing route to market, with an 11.7% CAGR through 2031, helped by stronger last-mile delivery and broader digital assortment.

Why does South Africa remain the key country in the region?

South Africa held 18.0% of revenue in 2025, is projected to grow at 11.2% CAGR, and produced two-thirds of Africa’s pet food volume in 2025.

What is driving demand for higher-value dog food in Africa?

Pet humanization, rising specialty retail reach, stronger veterinary involvement, and a shift toward preventive nutrition are raising demand for premium and therapeutic products.

What are the main risks affecting branded dog food suppliers in Africa?

The main risks are price volatility, currency pressure, infrastructure gaps, price sensitivity, and informal resale of unsafe or counterfeit products.

Page last updated on: