Africa Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

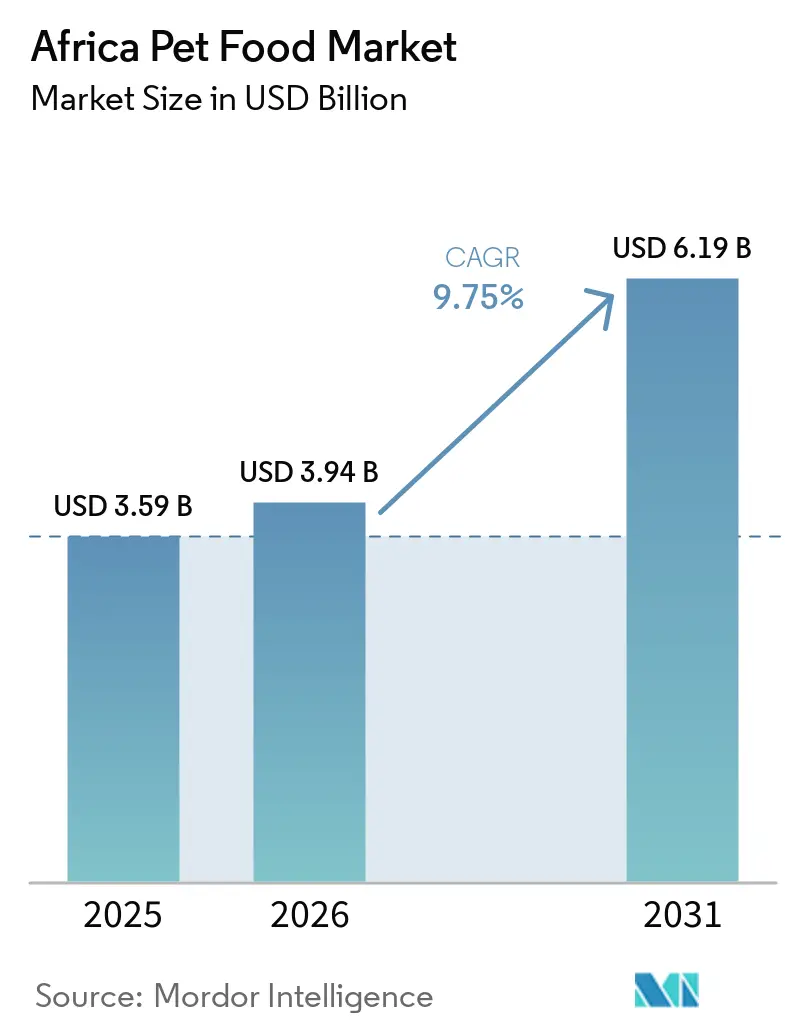

| Base Year Market Size (2025) | USD 3.59 Billion |

| Market Size (2026) | USD 3.94 Billion |

| Market Size (2031) | USD 6.19 Billion |

| Growth Rate (2026 - 2031) | 9.75% CAGR |

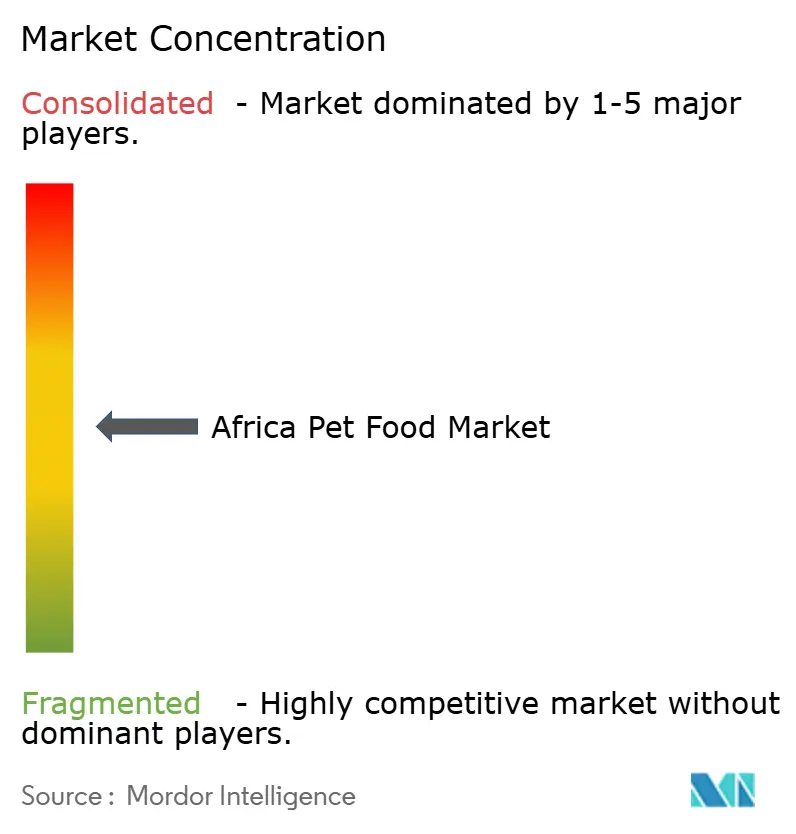

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Pet Food Market Analysis by Mordor Intelligence

The Africa pet food market size is projected to grow from USD 3.59 billion in 2025 to USD 3.94 billion in 2026 and is forecast to reach USD 6.19 billion by 2031 at 9.75% CAGR over 2026-2031. The Africa pet food market is expanding as more households shift from informal feeding to branded, packaged diets, while pets are also taking on a more central role in urban family life. Growth in the Africa pet food market is supported by rising urban incomes, wider access to supermarkets and specialty stores, and better veterinary access in the continent’s larger cities. Dry food remains the core volume format across the Africa pet food market because it is affordable, shelf-stable, and easier to distribute across varied retail environments, while premium, functional, and therapeutic products are gaining ground in organized channels. Local manufacturing is becoming more important in the Africa pet food market because it improves cost control and supply stability, especially in South Africa, Kenya, and Nigeria, where investment in feed and nutrition capacity is increasing. Competitive intensity in the Africa pet food market is rising as multinational brands face stronger local and regional challengers, even though price sensitivity, fragmented regulation, and weak cold-chain coverage still limit faster category development outside the most formal urban centers.

Key Report Takeaways

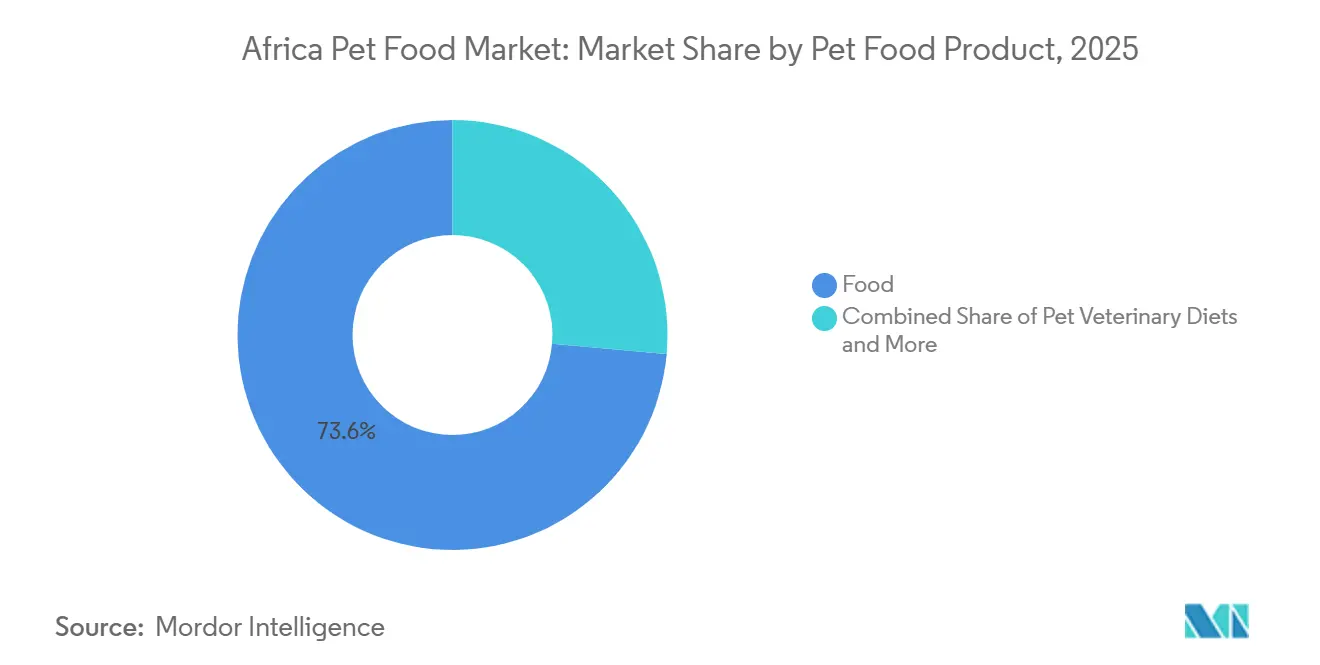

- By pet food product, food held 73.6% of the Africa pet food market share in 2025, while pet veterinary diets are projected to expand at 11.7% CAGR through 2031.

- By pets, dogs accounted for 88.9% of the market in 2025, and are also forecast to record the fastest growth at 10% CAGR through 2031.

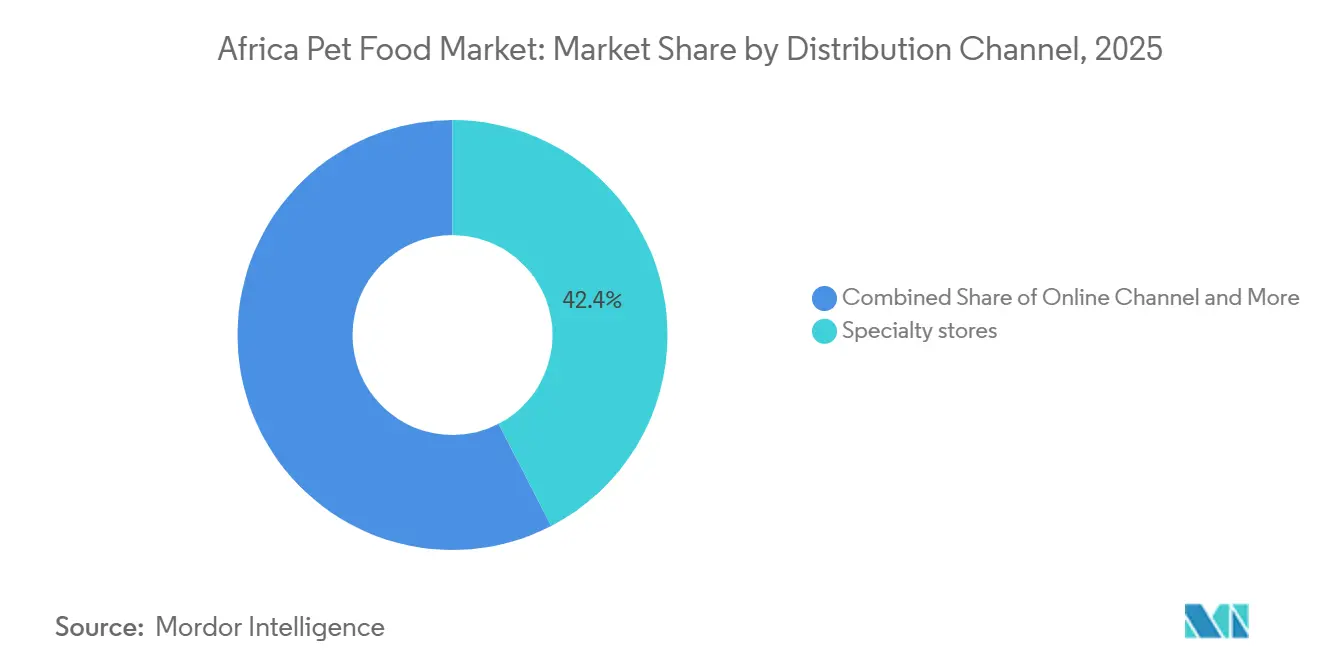

- By distribution channel, specialty stores captured 42.4% of the Africa pet food market size in 2025, while the online channel is forecast to grow at a 11.5% CAGR through 2031.

- By geography, South Africa led with 20.0% revenue share in 2025 and is projected to expand at a 10.9% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet humanization and premium nutrition demand | +3.2% | Continental, strongest in South Africa, Nigeria, and Kenya | Short term (≤ 2 years) |

| Expansion of modern retail and specialty pet channels | +1.8% | South Africa, East Africa, and North Africa | Medium term (2-4 years) |

| Local manufacturing and import substitution in key hubs | +1.5% | South Africa, Kenya, and Nigeria | Medium term (2-4 years) |

| Functional diets for health, weight, and skin support | +1.3% | South Africa and major urban centers across the continent | Medium term (2-4 years) |

| Informal feeding conversion into packaged pet food | +1.1% | Broadly across Sub-Saharan Africa | Long term (≥ 4 years) |

| E-commerce and direct-to-consumer brand reach | +0.8% | South Africa urban core, Nairobi, and Lagos | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization and Premium Nutrition Demand

The Africa pet food market is being reshaped by a steady shift in how urban households think about animal care and daily feeding. Pet ownership is moving closer to a family-care model in larger cities, which is boosting interest in branded diets, higher-quality ingredients, clearer labels, and products tailored to age, condition, and lifestyle. This change matters because it supports repeat purchasing behavior, not just occasional trade-up buying, and that gives the Africa pet food market a stronger base for sustained growth. The same pattern is also helping premium dry food, functional treats, and targeted formulas gain visibility even when overall household budgets remain tight, because pet nutrition is becoming a more deliberate spend rather than a casual add-on. In practice, companies that explain product benefits clearly and align them with digestive support, skin health, and life-stage needs are better placed to gain traction as the Africa pet food market matures. Formal labeling and ingredient disclosure remain important trust signals in this shift, especially in South Africa’s organized retail system.

Expansion of Modern Retail and Specialty Pet Channels

The Africa pet food market is also benefiting from a broader shift in how products are sold, displayed, and replenished across formal trade. Supermarkets are treating pet food as a more defined destination category, which improves visibility, range depth, and pack-size choice for shoppers who want both entry-level and premium options. Specialty retail is adding another layer to the Africa pet food market because it can carry therapeutic diets, supplements, and niche products that general trade often cannot support at scale. This matters for category development because better shelf presentation and stronger in-store advice tend to reduce consumer hesitation and encourage migration from informal feeding to packaged diets. In South Africa, the scale of specialist retail has already created a stronger premium ecosystem, with Absolute Pets operating more than 200 stores and helping extend access to higher-value categories across multiple urban locations. That retail depth gives the Africa pet food market a clearer path to premiumization than would be possible through fragmented neighborhood trade alone.

Local Manufacturing and Import Substitution in Key Hubs

Local production is becoming a structural advantage in the Africa pet food market because it lowers exposure to imported input costs and shortens supply chains. In Kenya, Loop Pet Food scaled its processing line in Nairobi from 2 to 3 metric tons per month to 60 metric tons per month in March 2025, showing that East Africa is moving beyond very small-batch production into a more commercial manufacturing phase. In February 2026, De Heus Kenya opened a KSH 3 billion (USD 23 million) animal feed facility in Athi River, which strengthens the upstream ingredient and feed base that supports more competitive local nutrition products. These investments matter because the Africa pet food market still faces significant affordability gaps, and local sourcing of grains, fish, and protein ingredients can help brands create products that better align with local purchasing power. Local manufacturing also gives producers more room to adapt recipes, pack sizes, and pricing to country-specific demand, which is critical in the Africa pet food market because consumer preferences and distribution realities vary sharply across the continent. As trade links deepen, South African and Kenyan producers are likely to use this base to reach neighboring markets more efficiently.

Functional Diets for Health, Weight, and Skin Support

Functional nutrition is moving from a niche offering to a more established premium segment within the Africa pet food market. Urban pet owners are showing greater interest in products linked to digestive support, coat condition, healthy weight, and age-related needs, which is pushing brands to connect nutrition claims with visible pet wellness outcomes. The veterinary channel is central to this part of the Africa pet food market because consumers often trust product recommendations from clinics more than claims on standard shelf packs. That has helped companies with stronger therapeutic and clinical nutrition positions hold an advantage in prescription and specialist segments. The same direction is visible in South Africa’s specialist retail channel, where vet-endorsed formulations with digestive and probiotic support are being introduced to bridge the gap between everyday feeding and more advanced nutrition positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity outside premium urban clusters | -1.8% | Continental, most acute in rural Sub-Saharan and secondary urban markets | Long term (≥ 4 years) |

| Weak online penetration in most African markets | -0.8% | Continental except South Africa urban core | Medium term (2-4 years) |

| Fragmented regulation and labeling compliance across countries | -0.7% | Continental across cross-border trade systems | Long term (≥ 4 years) |

| Limited cold chain and logistics coverage for moist and fresh formats | -1.0% | Broadly across Sub-Saharan Africa, especially inland and secondary markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity Outside Premium Urban Clusters

Price remains the biggest barrier to wider adoption of packaged food across the Africa pet food market. Commercial diets are well established in the main urban centers, but the Africa pet food market still depends on converting a much larger base of owners who continue to feed pets with household food or low-cost informal alternatives. This challenge is sharper outside the main metropolitan clusters, where consumers have less room for trade-up spending and often buy in small quantities, constrained by strict daily budget limits. In Nigeria, the reported rise in the price of a 15 kg bag of dog food from NGN 40,000 to NGN 70,000, or from USD 25 to USD 44, shows how quickly affordability can narrow when local currencies weaken, or input costs rise[1]Source: THE-STAR.CO.KE, "More Africans get cats, dogs as disposable income grows", www.the-star.co.ke. The practical result is that brands that rely too heavily on imported premium formulas face a narrower addressable base in the Africa pet food market than topline pet ownership would suggest. Companies that build economy dry food lines with local inputs and relevant pack sizes are more likely to unlock broader adoption.

Limited Cold Chain and Logistics Coverage for Moist and Fresh Formats

Cold-chain weaknesses are a major physical barrier to product diversification in the Africa pet food market. Wet, moist, and fresh formats require more reliable refrigerated storage and transport than dry kibble, making them much harder to scale beyond the continent’s most developed urban corridors. The Global Cold Chain Alliance reported that Africa loses 30% to 50% of perishable food due to weak cold storage and refrigerated transport, and that the broader infrastructure gap directly affects the reach of wet pet food formats[2]Source: Global Cold Chain Alliance, “Urgent Action Needed to Mitigate Energy Blackout Threat to Food Supply Chain Resilience in Africa,” Global Cold Chain Alliance, gcca.org. Even in South Africa, where the Africa pet food market is most formalized, repeated power outages have raised storage and handling costs for temperature-sensitive products and reduced the appeal of broader wet-format investment. This keeps dry food in a stronger position across much of the Africa pet food market because it is easier to move, store, and stock consistently. Until power reliability and refrigerated logistics improve, premium wet nutrition will remain concentrated in a limited set of cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Food Product: Dry Kibble Anchors Volume as Therapeutic Diets Lead Premium Growth

Food held 73.6% market share in the Africa pet food market in 2025, and that leadership reflects the basic commercial feeding pattern seen across most countries on the continent. Dry food, especially kibble, remains the largest format because it is affordable, easy to transport, and suitable for retail systems that range from formal supermarkets to smaller neighborhood outlets. Wet food is present in premium urban channels, especially in South Africa, but its reach is still much narrower because storage and logistics requirements are more demanding. Treats are growing as owners look for products tied to training, bonding, and occasional indulgence, and that is widening shelf variety in organized trade. Nutraceuticals and supplements are also gaining space in the Africa pet food industry as vet guidance and health-led positioning make owners more comfortable with functional add-ons, while local product innovation, such as game meat treats, gives South African brands a distinct point of difference.

The Africa pet food market size for pet veterinary diets is set to grow fastest at a 11.7% CAGR through 2031, underscoring how quickly health-led feeding is becoming a serious premium category rather than a narrow clinic-only niche. Demand is strongest in formulas linked to skin issues, digestion, weight control, renal care, and urinary health, because these are conditions owners can understand and monitor with veterinary support. Colgate-Palmolive Company, through Hill's Pet Nutrition Inc., and Nestlé S.A., through Purina, retain strong positions here because clinic distribution and professional trust are harder for newer entrants to replicate quickly. South Africa’s regulatory environment also shapes the segment, as products sold through formal channels must meet labeling and feed compliance requirements, which raise the entry bar for companies without strong regulatory resources. That makes veterinary diets one of the clearest examples of how the Africa pet food market is moving up the value ladder, even while mass-market affordability remains important.

By Pets: Cat Households Lead Volume as Dog Ownership Accelerates Across Urban Africa

Dogs held 88.9% market share by pet type in the Africa pet food market in 2025, reflecting their strong presence in North African households and their fit with apartment living in major urban areas. Cat food demand is still centered on dry products, which align with everyday feeding routines and work well in markets where shoppers prefer formats with long shelf life and low storage risk. Imported and multinational brands remain visible in formal cat food retail, but local and regional producers have room to grow if they can offer credible quality at mid-tier price points. Wet cat food is expanding in the premium channel, especially where urinary and hydration concerns are shaping consumer choice after veterinary consultation. Other pets remain a small and underserved category in the Africa pet food market, leaving room for specialist brands to enter segments that still see limited assortment in mainstream retail.

The Africa pet food market for dogs is projected to grow at a 10% CAGR through 2031, making dogs the fastest-expanding pet type in commercial feeding terms. Growth is supported by two parallel patterns, one tied to security and working-dog ownership in peri-urban settings, and another tied to companion-animal adoption among younger urban households. That mix gives dog food broader depth across price tiers, from economy dry food to premium life-stage and therapeutic formulas. In Kenya, the growing spread of pet shops, grooming outlets, and veterinary services around Nairobi shows that dog ownership is creating a broader service economy focused on food, health, and daily care. Senior dog nutrition is also becoming more relevant because the Africa pet food market is beginning to support longer pet lifespans and more condition-specific feeding through the companion animal lifecycle.

By Distribution Channel: Supermarkets Anchor Share as Digital Commerce Reshapes Premium Access

Specialty stores captured 42.4% market share in the Africa pet food market in 2025 and remain the largest organized distribution points for packaged pet food. Their importance stems from a dependable assortment, visible shelf placement, and the ability to carry both entry-level and premium products in a single shopping trip. In South Africa and the more modern retail pockets of Kenya, Nigeria, Egypt, and Morocco, supermarket pet aisles are becoming more clearly defined categories rather than low-visibility shelf extensions. Specialty stores are also strengthening the category by carrying therapeutic diets, supplements, premium wet formats, and advisory-led ranges that need more explanation than general trade can offer. At the same time, convenience stores, kiosks, and other informal outlets still matter across the Africa pet food industry because they keep basic dry food available where organized retail has not reached full scale.

The Africa pet food market size for the online channel is forecast to grow at 11.5% CAGR through 2031, even though digital sales are still building from a small base. Online demand is strongest where consumers are already comfortable ordering heavy repeat-purchase products and where delivery networks can support predictable replenishment. In the Africa pet food market, Absolute Pets reported a 33% year-on-year increase in online sales in 2024, noting that online basket values were significantly higher than in-store basket values. This indicates that digital buyers tend to favor premium and planned purchases. Platform expansion is widening product discovery and supporting subscription-style replenishment for dry food, but the Africa pet food market will still depend heavily on physical retail because many consumers prefer to inspect products in person, and secondary-city logistics remain uneven. Digital commerce is therefore likely to grow fastest at the upper end of the category while brick-and-mortar channels keep overall volume leadership.

Geography Analysis

South Africa accounted for a 20.0% revenue share in 2025 and is anticipated to grow at a CAGR of 10.9% from 2026 to 2031. Pet food accounts for the majority of pet care spending in the country, providing South Africa with a stronger volume base than other African sub-markets. The country benefits from an organized retail infrastructure, clear labeling standards, and an established code of practice, which enhance consumer confidence in formal shelf products. Additionally, the growing urbanization and rising disposable incomes in South Africa have contributed to increased pet ownership, further driving demand for pet food and related products. These factors position South Africa as a key player in the African pet food market, serving both as a significant consumer market and an export hub for neighboring countries. The country's strategic location and well-developed logistics network also facilitate efficient distribution to other African nations, strengthening its role as a regional leader in the pet food industry.

Kenya is emerging as one of the most dynamic growth points in the Africa pet food market because manufacturing investment and urban retail development are moving forward at the same time. Loop Pet Food’s locally produced Samaki Crunch range, launched in December 2025, shows how Kenyan players are building products around local protein sources and more practical cost structures. Nigeria remains an important volume opportunity in the Africa pet food market, but wider packaged-food adoption is still constrained by affordability and weaker logistics, even as feed and milling investment gradually improves the supply base.

North Africa is entering a different phase of development in the Africa pet food market, with a clearer shift from an import-heavy supply toward wider local brand participation in organized retail. Morocco is an important example because domestic brands are entering mass-market channels that were previously dominated by imported products. Egypt and Algeria also offer meaningful scale, as large urban populations and established retail networks can support broader packaged food distribution once product range and pricing better align with local demand. The rest of the continent remains a longer-term opportunity for the Africa pet food market, with progress likely to depend on income growth, retail formalization, better cold-chain coverage, and easier cross-border product movement.

Competitive Landscape

The Africa pet food market remains moderately fragmented, with competitive strength split between global multinationals and strong local players better aligned with country-level pricing and distribution realities. Mars Incorporated, Nestlé S.A. (Purina), The J.M. Smucker Company, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), and General Mills Inc., through Hill's Pet Nutrition Inc., enjoy strong brand visibility across premium retail and veterinary channels, particularly in markets with more developed formal trade. Farmina Pet Foods and Virbac S.A. occupy a more specialized position in the Africa pet food market through functional and therapeutic nutrition, where product credibility and clinic access matter more than pure shelf breadth. Local South African suppliers remain important because they combine a manufacturing presence with stronger value positioning, making them more resilient in a market where consumers often need quality at a lower price point. That balance keeps the Africa pet food market competitive without allowing a single company to dominate at the continental level.

Strategic consolidation is increasingly evident in the Africa pet food market as local companies aim to enhance their scale to compete with the spending power and supply capabilities of multinational firms. In March 2026, Monic Group finalized the acquisition of Marltons Pet Care, bolstering its distribution network and product offerings in South Africa. This move enabled Monic Group to strengthen its presence in the region and better meet growing consumer demand. Similarly, in April 2026, RCL Foods announced its agreement to acquire Martin and Martin for R695 million (USD 36 million). This acquisition broadened RCL Foods' portfolio in the Africa pet food market to include wet food, treats, and biscuits, complementing its existing dry food products and enabling the company to cater to a wider range of customer preferences[3]Source: Global Cold Chain Alliance, “Urgent Action Needed to Mitigate Energy Blackout Threat to Food Supply Chain Resilience in Africa,” Global Cold Chain Alliance, gcca.org.

The clearest openings in the Africa pet food market are still in functional mid-tier nutrition, wet products where infrastructure allows, and affordable packaged dry food that can convert informal feeders. Companies that combine local sourcing with cleaner labels and clearer health claims are likely to gain more traction than those that simply import premium products and hope demand will catch up. Digital tools are also becoming more important in the Africa pet food market because they help brands improve product discovery, reorder behavior, and consumer retention without relying only on physical shelf expansion. Even so, success will continue to depend on practical execution, which means pricing discipline, reliable supply, strong retail relationships, and product formats that match how African consumers actually shop.

Africa Pet Food Industry Leaders

-

The J.M. Smucker Company

-

General Mills Inc.

-

Nestle S.A. (Purina)

-

Mars Incorporated

-

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Wellness Pet Company launched limited-edition P'Nutty B-Day Party treats under its Old Mother Hubbard brand. Developed in collaboration with Milk Bar, these treats include peanut butter and dog-safe vanilla yogurt icing. Such innovative product offerings influence the Africa Pet Food Market by driving demand for premium and specialized pet treats, catering to the growing trend of pet humanization in the region.

- April 2026: RCL Foods acquired Martin and Martin, a local pet food manufacturer, from Simrose Overseas S.A. for R695 million (USD 36 million). The deal includes brands like Husky, Pamper, Beeno, and Bob Martin, expanding RCL Foods' portfolio into wet pet food, treats, and biscuits, and strengthening its position in South Africa's pet care market.

- March 2026: Monic Group, the parent company of Montego Pet Nutrition, has acquired Marltons Pet Care, uniting two of South Africa's leading pet care businesses. Building on a relationship since 2018, the merger strengthens distribution, product development, and competitiveness in domestic and Sub-Saharan export markets.

Africa Pet Food Market Report Scope

Pet food is any commercial sustenance specially formulated to meet the nutritional needs of domesticated animals. It typically consists of processed meats, grains, vitamins, and minerals, available in dry kibble, wet canned food, or raw meals.

The Africa Pet Food Market Report is Segmented by Pet Food Product (Food, Pet Nutraceuticals/Supplements, and More), by Pets (Cats, Dogs, and Other Pets), by Distribution Channel (Convenience Stores, Online Channel, and More), and Geography (South Africa and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft And Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | ||

| Diabetes | ||||

| Digestive Sensitivity | ||||

| Obesity Diets | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary tract disease | ||||

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| South Africa |

| Rest of Africa |

| Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft And Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | |||

| Diabetes | |||||

| Digestive Sensitivity | |||||

| Obesity Diets | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary tract disease | |||||

| Other Veterinary Diets | |||||

| Pets | Cats | ||||

| Dogs | |||||

| Other Pets | |||||

| Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

| Geography | South Africa | ||||

| Rest of Africa | |||||

Key Questions Answered in the Report

What is the current value of the Africa pet food market?

The Africa pet food market stands at USD 3.94 billion in 2026 and is forecast to reach USD 6.19 billion by 2031, growing at 9.75% CAGR over 2026-2031.

Which product category leads pet food sales across Africa?

Food is the largest category, holding 73.6% share in 2025, driven mainly by dry kibble because it is affordable, shelf stable, and widely available.

Which pet type is growing fastest in commercial feeding demand?

Dogs are the fastest-growing pet type with a 10% forecast CAGR through 2031, supported by both security-related ownership and companion-animal adoption in urban areas.

Which sales channel is expanding the fastest?

The Online Channel is projected to grow at 11.5% CAGR through 2031, although specialty stores remained the largest organized channel in 2025 with 42.4% share.

Why does South Africa lead regional demand?

South Africa has the strongest formal retail structure, a more established manufacturing base, and clearer labeling and quality systems, which support both premium sales and export supply.

What is holding back faster growth in wet pet food?

Weak cold-chain infrastructure and high logistics costs are limiting wet and moist format expansion, which keeps dry food in a stronger position across most African markets.

Page last updated on: