Africa Cat Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

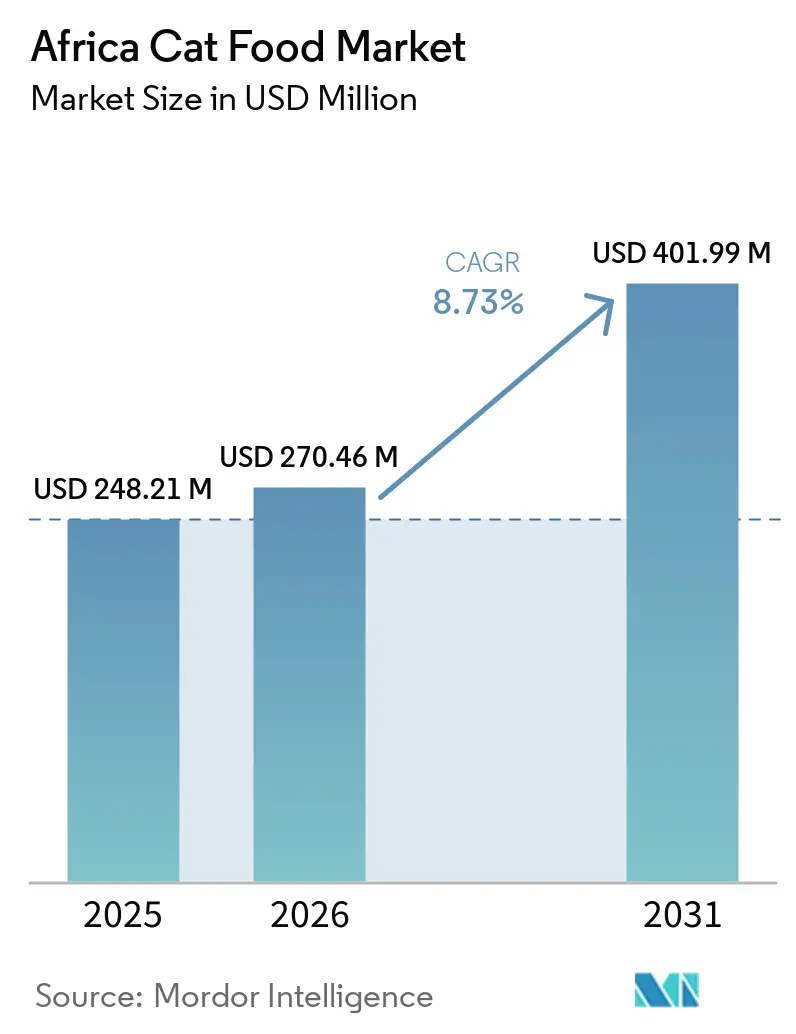

| Base Year Market Size (2025) | USD 248.21 Million |

| Market Size (2026) | USD 270.46 Million |

| Market Size (2031) | USD 401.99 Million |

| Growth Rate (2026 - 2031) | 8.73% CAGR |

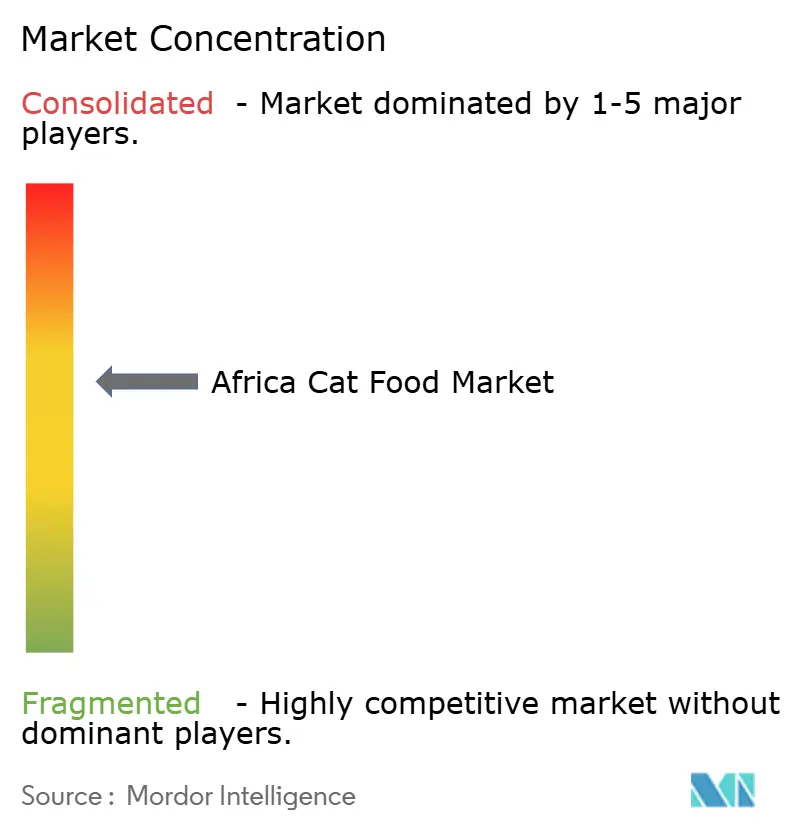

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Cat Food Market Analysis by Mordor Intelligence

The Africa cat food market size is projected to grow from USD 248.21 million in 2025 to USD 270.46 million in 2026 and is forecast to reach USD 401.99 million by 2031 at 8.73% CAGR over 2026-2031. The Africa cat food market is supported by a broader shift in household spending across urban Africa, where rising incomes and denser city living are making packaged pet nutrition more relevant to a wider base of cat owners. According to the Organization for Economic Co-operation and Development (OECD), Africa’s urban population stood at 700 million in 2025 and is projected to reach 1.4 billion by 2050, suggesting a longer runway for formal pet care demand across the region. The Africa cat food market is also being shaped by stronger influence from veterinarians, more visible premium product placement in organized retail, and a gradual shift toward functional and life-stage nutrition in the largest urban centers. Competitive conditions remain mixed across the region, with tighter rivalry in South Africa’s premium and therapeutic tiers and a more fragmented structure across much of sub-Saharan Africa and North Africa. Local manufacturing and shelf-stable product development are also reducing supply risk over time, which should help the Africa cat food market widen its reach beyond the most developed retail corridors.

Key Report Takeaways

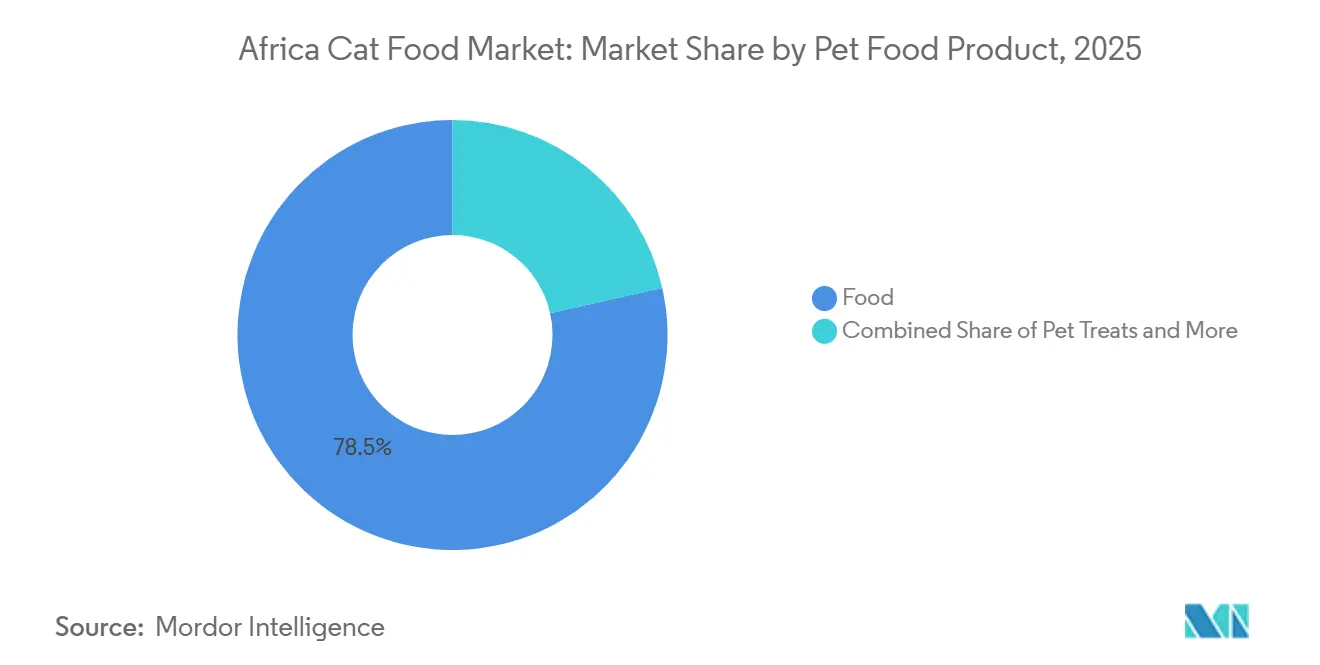

- By pet food product, food was the largest segment, with 78.5% of the Africa cat food market share in 2025, while pet nutraceuticals and supplements are the fastest-growing segment, with a forecasted 13.4% CAGR through 2031.

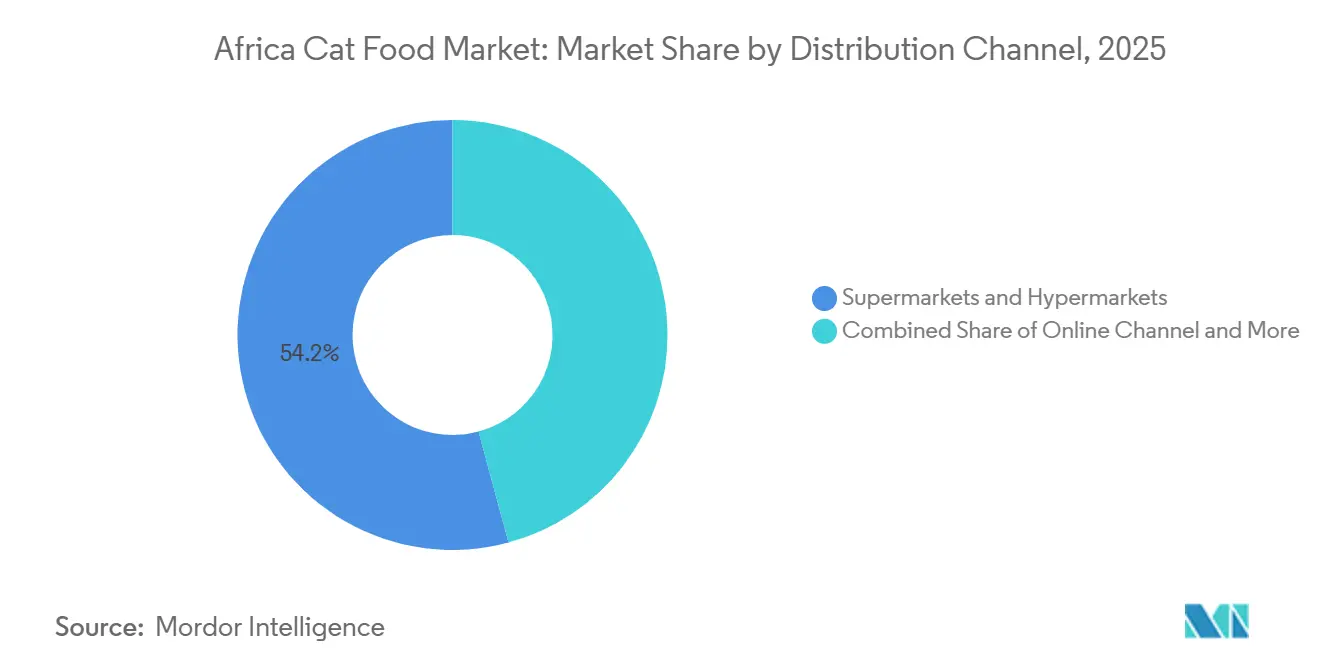

- By distribution channel, supermarkets and hypermarkets were the largest segment, accounting for 54.2% of the Africa cat food market size in 2025, while the online channel was the fastest-growing segment, with a projected 10.3% CAGR through 2031.

- By geography, South Africa was the largest segment with a 32.7% share in 2025 and also projected to be the fastest-growing segment, with a 10.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Cat Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet humanization and premiumization | +3.2% | Africa, strongest in South Africa, Nigeria, and Kenya | Medium term (2-4 years) |

| Expansion of organized pet retail and e-commerce | +2.1% | South Africa urban corridors, Egypt, and Morocco | Short term (≤ 2 years) |

| Growth in veterinary-recommended and functional nutrition | +1.5% | South Africa and Nigeria, with spillover into Egypt and Kenya | Medium term (2-4 years) |

| Rising indoor cat ownership and demand for life-stage nutrition | +1.0% | South Africa, Egypt, Morocco, and Kenya | Medium term (2-4 years) |

| Growth of local manufacturing and regional supply localization | +0.8% | Kenya, Nigeria, and South Africa | Long term (≥ 4 years) |

| Demand for shelf-stable, portion-controlled wet and dry formats | +0.6% | Sub-Saharan Africa and North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization and Premiumization

The trend of pet humanization is influencing cat food purchases in the Africa cat food market, shifting the focus from basic feeding to nutrition-driven decision-making. This change is not solely dependent on income levels, as urban living in cities like Nairobi and Lagos makes cats a practical pet choice for smaller households. With the rise of apartment living and smaller family units, cats are increasingly preferred for their adaptability to confined spaces and lower maintenance requirements compared to other pets. This trend supports increased spending per pet in urban areas, where owners are willing to invest in higher-quality ingredients, tailored nutrition, and reputable brands. Additionally, ingredient transparency and clean-label positioning are gaining traction in markets such as South Africa, Nigeria, and Kenya. Consumers are becoming more conscious of the nutritional content and sourcing of cat food, leading to a growing demand for products that align with these preferences. These factors are driving the market toward premium dry food, functional products, and specialized nutrition offerings, catering to pet owners' evolving needs.

Expansion of Organized Pet Retail and E-Commerce

Organized pet retail is improving visibility, assortment, and purchase confidence in the Africa cat food market, especially in South Africa. Retail chains such as Petshop Science and broader modern trade networks are shifting cat food sales away from informal outlets and into environments where premium placement, shelf navigation, and repeat purchasing are easier to sustain. The online route is also strengthening as major delivery and marketplace platforms make routine replenishment faster for urban households. Amazon entered South Africa in May 2024 with a pet supplies category, which raised expectations around assortment and fulfillment speed in one of the region’s most developed digital retail markets. In North Africa, specialized platforms in Egypt and Morocco show that organized pet commerce is developing beyond South Africa, providing the Africa cat food market with more formal touchpoints for premium, information-led sales.

Growth in Veterinary-Recommended and Functional Nutrition

Veterinary influence is becoming a stronger demand driver in the Africa cat food market, particularly in markets where owners rely heavily on clinic-based guidance. According to the World Organization for Animal Health's 2025 coverage, in Nigeria, veterinarians were identified as the top pet care information source by 72% of pet owners, giving medically positioned brands a clear advantage in trust and product recommendations[1]Source: World Organisation for Animal Health coverage, “WOAH Recognizes Dry, Extruded Pet Food as Safe for Trade,” petfoodindustry.com. Functional nutrition is gaining relevance as owners look for support for digestive health, skin sensitivity, obesity, and urinary concerns before problems become more serious. The September 2025 FEDIAF Nutritional Guidelines for Complete and Complementary Pet Food for Cats and Dogs also give producers and importers a recognized nutritional framework that can strengthen product credibility in emerging African markets. In practical terms, this means the Africa cat food market is seeing more value shift toward products that combine clinical messaging, veterinary endorsement, and clearly communicated functional benefits.

Rising Indoor Cat Ownership and Demand for Life-Stage Nutrition

Indoor cat ownership is expanding in major African cities, creating greater demand for category-specific feeding in the Africa cat food market. Statistics South Africa reported in June 2026 that 2 million cats were owned by 1.3 million households, representing 6.4% of all households, which gives a clearer baseline for one of the continent’s most advanced pet care markets. Indoor cats tend to generate more demand for hairball control, weight management, urinary support, and age-targeted formulas because owners can observe behavior and health changes more closely. The same pattern is emerging in urban Kenya, where cats are gaining relevance among apartment-dwelling households that value lower space requirements and easier daily care. As this buyer base grows, the Africa cat food market is likely to see deeper development in kitten, adult maintenance, and senior formulas, rather than relying on a single broad feeding option.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity in mass-market households | -2.5% | Africa, concentrated in sub-Saharan Africa outside South Africa | Long term (≥ 4 years) |

| Limited cold-chain tolerance for premium wet offerings | -1.5% | Sub-Saharan Africa outside South Africa major metro areas | Medium term (2-4 years) |

| Import dependence and currency volatility for premium inputs | -1.0% | Nigeria, Egypt, and Kenya | Medium term (2-4 years) |

| Uneven pet food penetration outside major urban corridors | -0.7% | Rest of Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity in Mass-Market Households

Price remains one of the clearest limits on the Africa cat food market outside the most formal retail systems. In the November 2025 Sagaci Research survey, 48% of African pet owners still relied on table scraps as their main feeding method, indicating that commercial cat food has not yet become a default purchase for many households. The gap is wider in markets where organized retail is thin, and consumers face a narrow choice between higher-priced imported brands and informal feeding. Compliance also affects affordability, as South Africa’s Fertilizers, Farm Feeds, Agricultural Remedies, and Stock Remedies Act 36 adds formulation and registration requirements that feed into retail pricing. Until lower-cost local production broadens supply at scale, the Africa cat food market will continue to face slower conversion from informal feeding in the mass segment.

Limited Cold-Chain Tolerance for Premium Wet Offerings

Cold handling remains a practical barrier for premium wet cat food across much of the Africa cat food market. Wet products offer higher moisture content and premium positioning, but their distribution is harder to scale where storage conditions, transport quality, and last-mile handling are inconsistent. Outside South Africa’s major metropolitan areas, these constraints narrow the viable footprint for wet-heavy portfolios and favor dry, semi-moist, or shelf-stable alternatives. This creates concentration risk because growth in wet food becomes tied closely to a limited set of urban retail corridors with stronger infrastructure. As a result, the Africa cat food market is likely to continue leaning on dry food volume for wider reach, while wet food remains more urban, premium, and selective in its expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Food Product: Food Category Commands Premium Shelf Position

Food held the largest market share in the Africa cat food market in 2025 at 78.5%, which confirms that everyday complete nutrition remains the commercial base of category demand. Food also reflects the fact that packaged dry and wet diets are still far more established than supplements, treats, or therapeutic products in routine feline feeding. Dry cat food, especially extruded kibble, remains the main volume driver because it aligns with affordability, shelf-life, and handling needs across many African markets. Wet cat food is smaller in volume, but it is building value in premium urban tiers where owners are more willing to pay for moisture-rich feeding and more specialized nutrition.

Pet nutraceuticals and supplements are the fastest-growing segment, with a 13.4% CAGR through 2031, driven by growing awareness of digestive support, skin health, and targeted functional ingredients. Extruded kibble works well in markets where refrigeration is limited, and households want portion control, easier storage, and lower spoilage risk. Pet nutraceuticals and pet treats are also gaining traction as cat ownership becomes more visible and emotionally driven in parts of South Africa and Kenya. Within the Africa cat food industry, this means value creation is gradually expanding beyond staple foods, even though complete nutrition remains the largest anchor of demand.

By Distribution Channel: Online Channel Outpaces Traditional Routes to Market

Supermarkets and Hypermarkets held the largest market share in the Africa cat food market in 2025 at 54.2%, reflecting their strong role in branded visibility, repeat purchases, and assortment depth. This channel is supported by stronger category management in South Africa, Egypt, and Morocco. Modern trade remains important because it combines price promotions, merchandising, and one-stop shopping, helping cat food stay in the regular household basket. Shoprite Holdings reinforced its position in Africa in 2025 by introducing a veterinarian-developed premium private label dry cat and dog food range, available across 144 stores and the Sixty60 platform[2]Source: Shoprite Holdings, “Petshop Science Launches Premium Private Label Pet Food,” shopriteholdings.co.za. That move shows how large retailers can use private label to build margins and increase category participation simultaneously.

The Africa cat food market size for the online channel is projected to expand at a 10.3% CAGR through 2031, making it the fastest route to market in the current outlook. This growth reflects stronger use of same-day delivery, app-based replenishment, and subscription-led convenience in dense metro areas such as Gauteng and the Western Cape. Online platforms also help formal sellers explain ingredients, nutritional purposes, and feeding guidance more clearly than informal trade channels. Specialty stores still matter because they carry deeper premium and veterinary product ranges, while convenience outlets support smaller, more urgent purchases. Across the Africa cat food industry, online distribution is gaining weight not because stores are weakening, but because digital ordering is becoming the easiest way to repeat purchase in the most developed city markets.

Geography Analysis

South Africa held the largest market share in the Africa cat food market at 32.7% in 2025, and it is also the fastest-growing geography with a projected 10.0% CAGR through 2031. South Africa reflects stronger retail formalization, higher pet care spending, and a more developed premium channel structure. Agrimark also reported 28% growth in pet food sales from 2021 to 2025, supporting the view that repeat purchasing in South Africa remains strong even as the category matures. Modern trade, specialty retail, and e-commerce operate together more effectively in South Africa than elsewhere on the continent, which is why the country remains the core commercial anchor of the Africa cat food market.

Nigeria and Kenya stand out as the highest-priority growth opportunities within the Rest of Africa grouping. Nigeria still has low commercial cat food penetration outside affluent urban households, but veterinary influence is unusually strong, with 69% of pet owners using veterinary care and 38% buying pet food through clinics. That matters because clinic-led purchasing supports premiumization and therapeutic feeding even before broad retail formalization is complete. Kenya is moving along a different path, with local production helping improve accessibility and supply continuity. Loop Pet Food launched its tilapia-based Samaki Crunch range in December 2025 and had already expanded output at its Nairobi site to 60 metric tons per month, creating a meaningful production base for East Africa.

North Africa is emerging as an important secondary growth zone in the Africa cat food market, led mainly by Egypt and Morocco. Egypt’s larger cities are seeing stronger cat ownership among apartment-dwelling households, which supports dry and premium wet food and targeted urban retail formats. Morocco has also improved the regulatory framework for inputs, issuing a formal code in 2024 for the import of animal meal used in pet food production. Algeria remains underpenetrated in commercial cat food despite high household pet ownership, suggesting trade and retail barriers rather than weak consumer demand. The African Continental Free Trade Area (AfCFTA) should support broader intra-African movement of finished cat food over time, which could help South Africa-based and other regional producers extend their reach across more markets.

Competitive Landscape

The Africa cat food market is moderately concentrated in premium and therapeutic products, where Mars, Incorporated, Nestlé S.A., The J.M. Smucker Company, General Mills, Inc., and Affinity Petcare, S.A. These companies rely heavily on veterinary relationships, premium shelf positioning, and formulation credibility rather than on broad, low-priced distribution. Their strongest advantage lies in South Africa, where organized retail and clinic networks can sustain brand recommendations and repeat purchases. This part of the Africa cat food market is harder for low-cost suppliers to disrupt because clinical messaging and trust matter more than price alone.

Mars, Incorporated has reinforced its premium supply position through a EUR 1 billion (USD 1.17 billion) investment across European facilities in France, Poland, and Spain for 2025 and 2026, supporting premium capacity and Royal Canin SAS formulations that feed global markets, including Africa-bound volumes. Shoprite Holdings is taking a different route by building private-label strength in the mass-premium space through Petshop Science, which gives it better control over pricing, placement, and customer capture. United Petfood Group B.V. and VAFO Group a.s. also remain relevant through distributor-led and private-label supply models that do not depend on strong direct retail branding in every African market. This keeps the middle tier of the Africa cat food market more competitive and less locked by a few global brand owners. It also means supply chain flexibility can be as important as consumer-facing brand equity.

Local and regional manufacturers are gaining relevance where global firms face higher logistics costs or weaker route-to-market depth. Montego Pet Nutrition in South Africa and Loop Pet Food in Kenya show that local sourcing and shorter lead times can create a meaningful edge in selected markets. The clearest white space remains in functional nutrition and life-stage feeding for cats, where consumer education is still developing outside South Africa. Brands that invest early in veterinary outreach, organized retail placement, and FEDIAF-aligned nutritional positioning should build a stronger long-term footing[3]Source: European Pet Food Industry Federation, “Nutritional Guidelines for Complete and Complementary Pet Food for Cats and Dogs,” FEDIAF, europeanpetfood.org. Overall, the Africa cat food market is not dominated by one or two firms across the full region, but leadership is clearer in higher-value pockets than in mass-market supply.

Africa Cat Food Industry Leaders

Mars, Incorporated

Nestlé S.A.

The J.M. Smucker Company

General Mills, Inc.

Affinity Petcare, S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: VAFO Group a.s. restructured into 3 independent entities, VAFO Praha (flagship brands Brit and Carnilove), VAFO Production (manufacturing plants in the Czech Republic, Estonia, Finland, and Poland), and VAFO Private Labels, to sharpen strategic focus and support targeted Africa, Western European, and international expansion.

- November 2025: Shoprite Holdings launched a veterinarian- and animal-nutritionist-developed premium private label dry cat and dog food range under the Petshop Science brand across 144 South African stores and the Sixty60 rapid delivery platform, covering life stages from kitten to senior.

- November 2025: Loop Pet Food launched the tilapia-based Samaki Crunch range for cats and dogs in Kenya, marking a significant product and geographic expansion as East Africa's first and only locally produced cat food manufacturer. The company already supplies Rwanda and signaled further East African expansion for 2026.

Africa Cat Food Market Report Scope

Cat food is specialized nutrition formulated to meet the exact dietary requirements of domestic cats, which are obligate carnivores. The Africa Cat Food Market Report is Segmented by Pet Food Product (Food, Pet Nutraceuticals/Supplements, Pet Treats, and Pet Veterinary Diets), Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and Other Channels), and Geography (South Africa and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft And Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | ||

| Diabetes | ||||

| Digestive Sensitivity | ||||

| Obesity Diets | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary tract disease | ||||

| Other Veterinary Diets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| South Africa |

| Rest of Africa |

| By Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft And Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | |||

| Diabetes | |||||

| Digestive Sensitivity | |||||

| Obesity Diets | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary tract disease | |||||

| Other Veterinary Diets | |||||

| By Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

| By Country | South Africa | ||||

| Rest of Africa | |||||

Key Questions Answered in the Report

What is the projected value of the Africa cat food market by 2031?

The Africa cat food market is forecast to reach USD 401.99 billion by 2031, rising from USD 270.46 billion in 2026 at an 8.73% CAGR over 2026 to 2031.

Which product category leads cat food demand across Africa?

Food is the largest category, with 78.5% share in 2025, because complete dry and wet diets remain the main commercial feeding option across the region.

Which sales channel is growing the fastest for cat food in Africa?

The Online Channel is the fastest-growing distribution route, with a projected 10.3% CAGR through 2031, driven by stronger app-based ordering and home delivery in major cities.

Why is South Africa so important to cat food suppliers?

South Africa held 32.7% share in 2025 and is also the fastest-growing geography at 10.0% CAGR, supported by better retail infrastructure, stronger premium demand, and more formal pet care channels.

What is limiting wider adoption of packaged cat food in Africa?

Price sensitivity, uneven retail access, cold-chain gaps for wet food, and exposure to imported premium inputs continue to slow conversion from table scraps and informal feeding.

How are veterinary channels shaping cat food purchases in Africa?

Veterinary influence is becoming more important, especially in Nigeria and South Africa, because therapeutic and functional diets depend on trust, diagnosis, and professional recommendation.

Page last updated on: