Dog Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

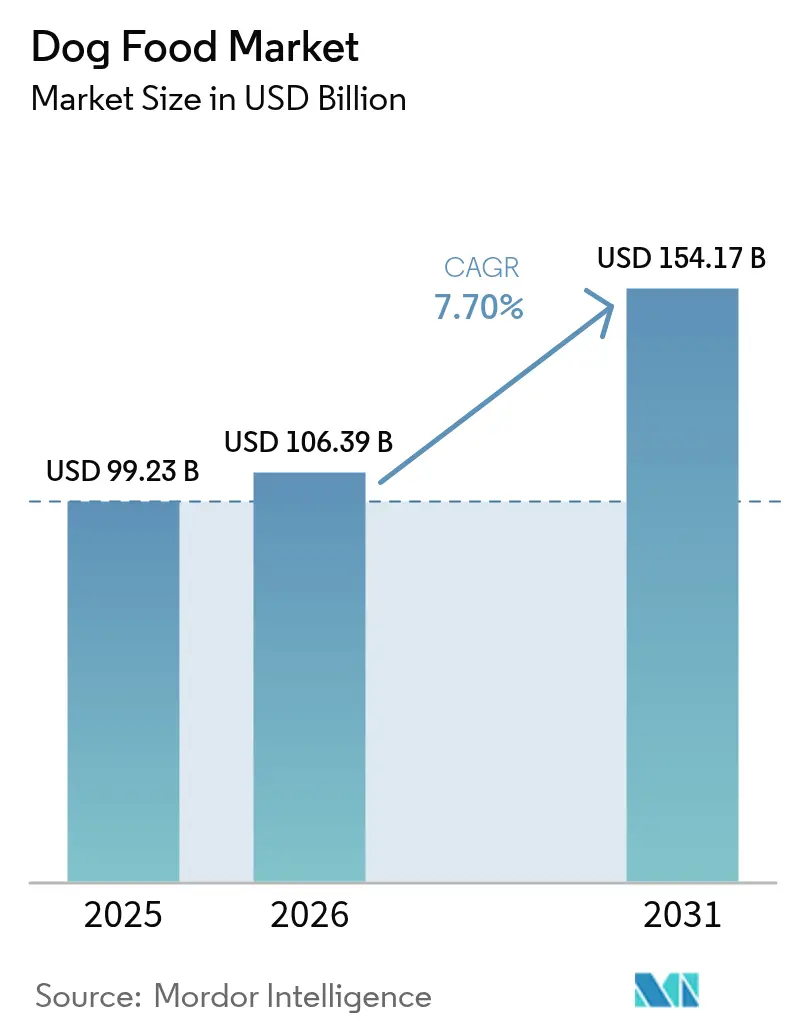

| Market Size (2026) | USD 106.39 Billion |

| Market Size (2031) | USD 154.17 Billion |

| Growth Rate (2026 - 2031) | 7.70% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dog Food Market Analysis by Mordor Intelligence

The dog food market size was valued at USD 99.23 billion in 2025 and is projected to grow from USD 106.39 billion in 2026 to reach USD 154.17 billion by 2031, at a CAGR of 7.70% during the forecast period (2026–2031). Underlying growth stems from the continued premiumization of canine diets, digital disruption via online subscription models, and rising interest in sustainable proteins that help temper exposure to volatile meat costs. Brands respond by widening human-grade portfolios, embedding functional additives that promise measurable health outcomes, and piloting insect and cultured-meat inputs that align with corporate climate goals. Competitive dynamics intensify as e-commerce private labels and fresh-food startups undercut mid-tier incumbents, forcing scale players to accelerate capacity builds in Asia and Africa, acquire niche innovators, and deploy data tools that personalize nutrition and lock in recurring revenue. Input-price swings, stricter green-marketing rules, and surging reports of grain sensitivities shape a risk backdrop that rewards firms with diversified protein sources, transparent labeling, and agile reformulation capabilities.

Key Report Takeaways

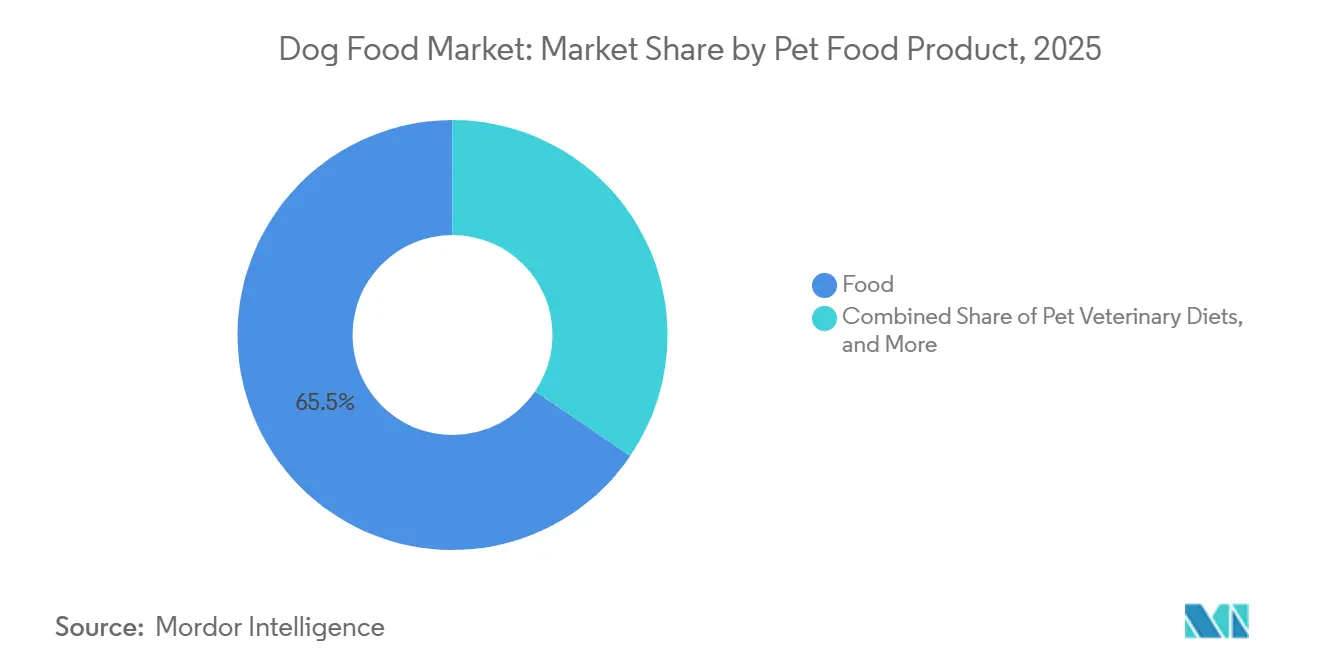

- By product type, food products led with 65.5% of dog food market share in 2025, and pet veterinary diets are forecast to expand at an 8.8% CAGR through 2031.

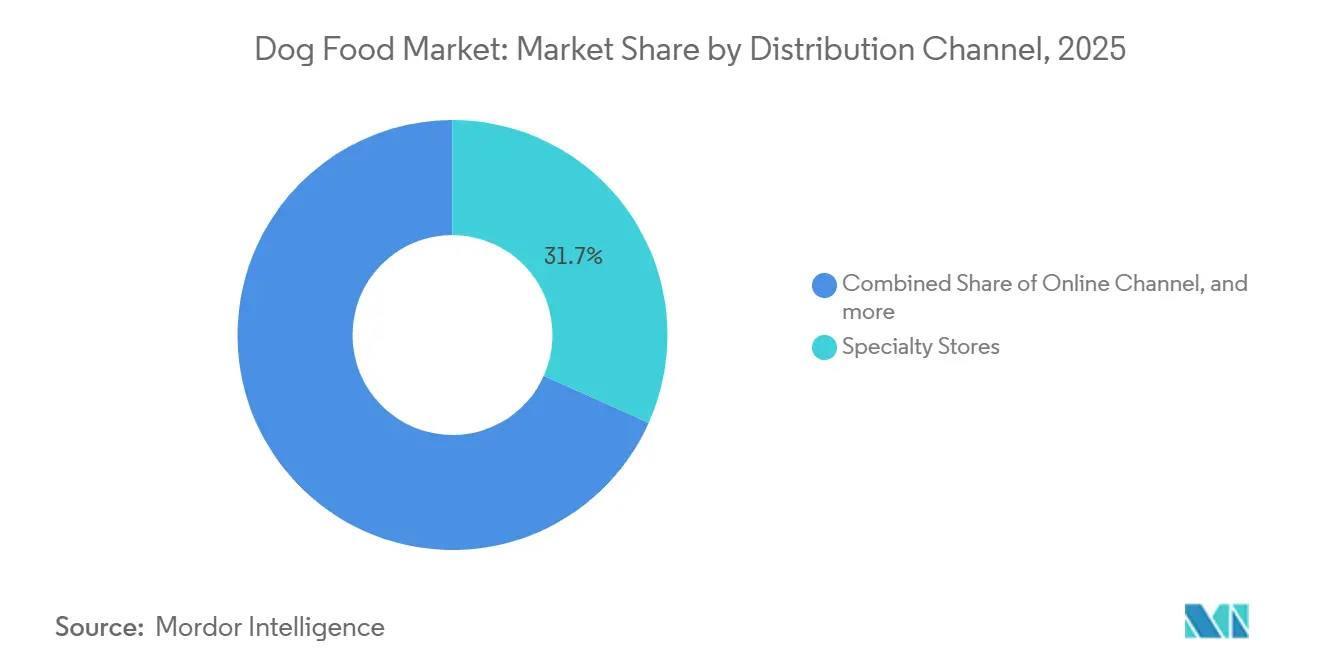

- By distribution channel, specialty stores held 31.7% share of the dog food market size in 2025, the online channel is projected to grow at a 10.0% CAGR between 2026 and 2031.

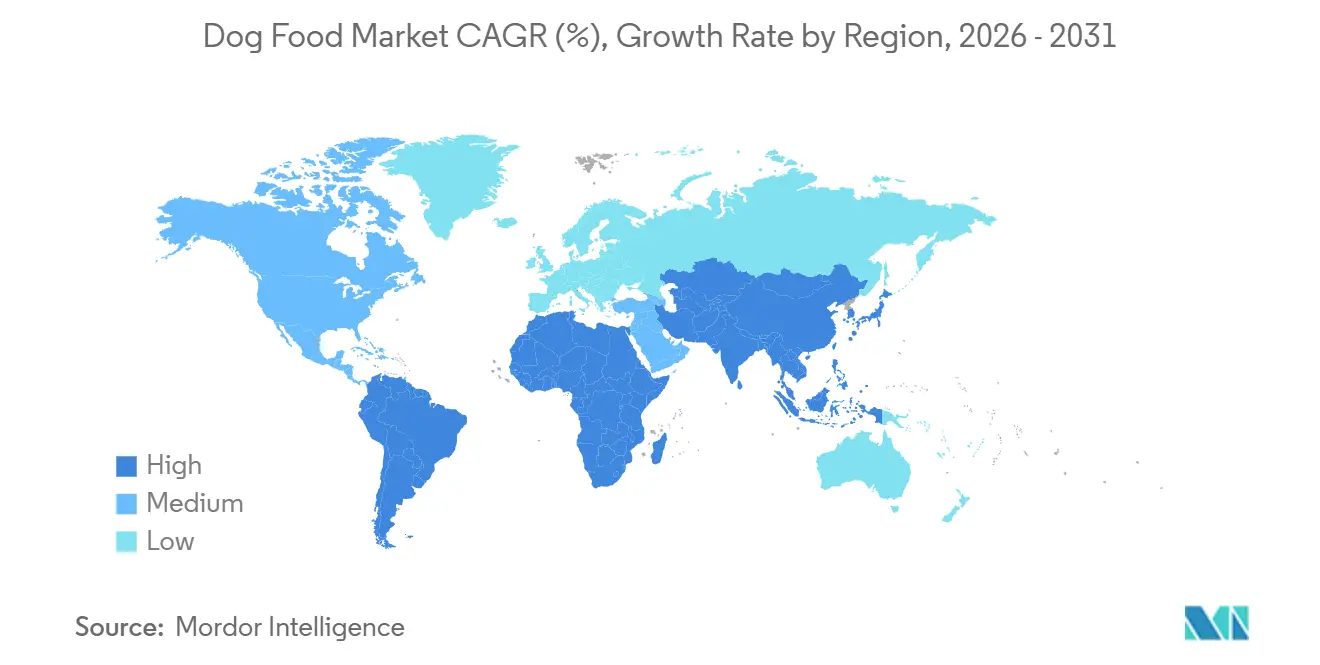

- By geography, North America accounted for 44.9% revenue share in 2025, while Africa is poised to record the fastest 9.4% CAGR through 2031.

- The dog food market is moderately concentrated, dominated by global giants including Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., The J. M. Smucker Company, Mars, Incorporated, and Nestle S.A. (Purina).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dog Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of dog diets | +1.2% | North America, Europe, and the Asia-Pacific core markets | Medium term (2-4 years) |

| Human-grade ingredient adoption | +1.0% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| E-commerce private-label expansion | +1.3% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Functional and fortified recipes | +0.9% | Global, with higher penetration in North America and the Asia-Pacific | Medium term (2-4 years) |

| AI-based personalization of feeding plans | +0.8% | North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Sustainable insect-protein formulations | +0.6% | Europe, Asia-Pacific, and spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization of Dog Diets

The premiumization of dog diets is influencing purchasing behavior as increasing disposable incomes in regions such as North America, Europe, and urban Asia-Pacific enable pet owners to upgrade from economy kibble to super-premium and ultra-premium options. These premium tiers focus on attributes like whole-meat proteins, limited ingredients, and grain-free formulations. In 2025, Mars Incorporated expanded its Royal Canin breed-specific portfolio, targeting consumers willing to pay a 30% to 50% premium for tailored nutrition addressing factors such as size, age, and genetic predispositions[1]Source: Mars Incorporated, “Mars Petcare Annual Review 2025,” mars.com. Similarly, Nestlé Purina introduced its Pro Plan LiveClear line, which reduces allergens in cat food, and is exploring comparable canine applications that offer functional benefits and justify premium pricing. This trend is gaining momentum in markets where pet ownership is shifting from utilitarian roles, such as guard dogs, to companion animals. This shift is particularly evident in countries like China and India, where middle-class growth is driving demand for branded, quality-assured pet products.

Human-Grade Ingredient Adoption

The adoption of human-grade ingredients in pet food highlights an increasing trend of anthropomorphism, as pet owners prioritize transparency, traceability, and ingredients that align with their own dietary standards. For instance, The Farmer's Dog, a direct-to-consumer startup, reported a 40% year-over-year revenue growth in 2025 by offering fresh, refrigerated meals made from United States Department of Agriculture (USDA)-inspected meats and vegetables. This positions its products as a premium alternative to traditional shelf-stable kibble. Similarly, companies such as Nom Nom and Ollie focus on human-grade standards and leverage subscription models to generate recurring revenue. These models also enable the collection of first-party data on factors like breed, age, and health conditions, which helps optimize product formulations. This market segment primarily attracts millennial and Gen Z pet owners, who place high value on ingredient provenance and are willing to pay a significant premium compared to conventional dry pet food. The human-grade claim requires brands to maintain detailed documentation and undergo third-party audits to ensure compliance and avoid potential enforcement actions.

Functional and Fortified Recipes

Functional and fortified recipes integrate nutrients that support joint health, skin and coat condition, digestive health, and cognitive function into daily feeding routines. This approach elevates dog food from basic nutrition to a preventive health tool. In 2025, Hill's Pet Nutrition expanded its Prescription Diet line with formulations designed to address canine cognitive dysfunction. These products include omega-3 fatty acids, antioxidants, and medium-chain triglycerides, which clinical trials suggest may help slow age-related cognitive decline. Similarly, Purina's Pro Plan Bright Mind emphasizes cognitive benefits for senior dogs, addressing pet owners' concerns about maintaining quality of life as advancements in veterinary care extend canine lifespans. Nutraceutical ingredients such as glucosamine, chondroitin, probiotics, and prebiotics are increasingly incorporated into mainstream kibble. This trend blurs the distinction between food and supplements, allowing brands to offer premium-priced products without requiring veterinary prescriptions.

AI-Based Personalization of Feeding Plans

AI-driven personalization of feeding plans is an emerging trend that utilizes algorithmic diet design, microbiome testing, and predictive analytics to customize nutrition for individual dogs. Companies like Kabo and Pet Plate gather data on factors such as breed, weight, activity level, and health conditions through onboarding questionnaires. This information is used to create tailored recipes and portion sizes, which are adjusted over time based on owner feedback and veterinary guidance. Some platforms also incorporate wearable devices to monitor activity and caloric expenditure, enabling real-time optimization of feeding recommendations through closed-loop systems. Additionally, this technology generates proprietary datasets that support product development, allowing brands to identify unmet needs and introduce targeted formulations more efficiently than traditional market research methods. Regulatory frameworks have not yet fully addressed this innovation, raising concerns about data privacy, veterinary oversight, and accountability for potential adverse health outcomes linked to algorithmic recommendations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of meat-based input prices | -0.7% | Global, with an acute impact in North America and Europe | Short term (≤ 2 years) |

| Regulatory scrutiny on sustainability claims | -0.5% | North America, Europe, and emerging in Asia-Pacific | Medium term (2-4 years) |

| Rising prevalence of canine grain allergies | -0.4% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Cultured-meat cost parity delays | -0.3% | Global, with R&D concentrated in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility of Meat-Based Input Prices

Volatility of meat-based input prices compresses producer margins when beef, chicken, and lamb costs spike due to disease outbreaks, drought, or geopolitical disruptions. Avian influenza outbreaks in the United States and Europe in 2024 and 2025 reduced poultry supply and elevated chicken-meal prices by 18% to 25%, forcing manufacturers to either absorb the cost, pass it through to retailers and consumers, or reformulate with lower-cost proteins such as pork or fish. Beef prices similarly fluctuated as drought in Australia and Brazil constrained cattle herds, while African swine fever in Asia disrupted pork supply chains. These dynamics disproportionately affect mid-tier brands that lack the purchasing scale to lock in long-term contracts or the pricing power to maintain margins through retail price increases. Premium brands with loyal customer bases and direct-to-consumer models exhibit greater resilience, as their buyers tolerate modest price adjustments in exchange for perceived quality and ingredient transparency.

Regulatory Scrutiny on Sustainability Claims

Regulatory oversight of sustainability claims intensified in 2025, with the Federal Trade Commission in the United States and the European Commission revising green-marketing guidelines. These updates aim to address vague or unverified environmental claims on pet food packaging. Brands that use terms such as carbon-neutral, eco-friendly, or sustainable without third-party verification or lifecycle assessments are subject to enforcement actions, fines, and reputational risks that can undermine consumer trust. The European Union's Green Claims Directive, introduced in 2024, mandates companies to substantiate environmental claims, including those related to carbon footprint, water usage, and biodiversity impact [2]Source: European Commission, “Green Claims Directive: New Rules on Environmental Marketing,” europa.eu. This has increased compliance costs, particularly for smaller companies, while benefiting larger players with established sustainability reporting systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Food Product: Veterinary Diets Outpace Food Dominance

Food is the largest segment, accounting for 65.5% of the dog food market size in 2025, driven by the convenience and shelf stability of extruded kibble, which dominates mass-market channels. Within the food category, dry kibble remains the primary choice, while wet food is gaining popularity among owners of senior dogs and breeds prone to dental issues. Additionally, freeze-dried and raw-frozen formats are attracting consumers seeking premium, minimally processed options. Hill's Pet Nutrition and Royal Canin lead the veterinary diet segment with prescription formulations targeting conditions such as obesity, renal disease, dermatological issues, and urinary tract health. These products are primarily distributed through veterinary clinics, which also offer diagnostic and monitoring services. Regulatory frameworks significantly impact product innovation, with the Association of American Feed Control Officials in the United States and the European Pet Food Industry Federation setting nutrient profiles, labeling standards, and manufacturing practices that regulate formulation and marketing claims.

Pet veterinary diets are the fastest-growing segment, forecast to expand at an 8.8% CAGR through 2031. Pet veterinary diets command price points two to three times higher than mainstream kibble due to significant investments in research and clinical trials. Pet nutraceuticals and supplements, such as probiotics, omega-3 fatty acids, and joint-care ingredients, drive additional spending as pet owners increasingly seek preventive health solutions to complement standard diets. Pet treats, available in formats such as crunchy, dental, freeze-dried jerky, and soft chewy options, serve dual purposes as training rewards and indulgent treats. Among these, dental treats are experiencing notable growth as pet owners prioritize oral hygiene to reduce the risk of expensive veterinary procedures. This segmentation highlights a divide between cost-conscious buyers focused on price per serving and health-oriented owners who consider nutrition a long-term investment in their pets' longevity and quality of life.

By Distribution Channel: Online Disruption Challenges Specialty Dominance

Specialty stores are the largest distribution channel with a 31.7% of the dog food market share in 2025, supported by subscription models, private-label growth, and the convenience of home delivery, which appeals to busy urban pet owners. Retailers such as Petco and PetSmart offer curated premium product assortments, employ trained staff for breed-specific guidance, and provide in-store veterinary clinics and grooming services, creating a comprehensive shopping experience. Supermarkets and hypermarkets remain essential for mass-market distribution, particularly in developing regions where online adoption is slower. Convenience stores serve immediate replenishment needs in urban areas, though their market share remains limited due to restricted shelf space and lower price competitiveness.

The online channel is fastest-growing channel projected to grow at a 10.0% CAGR between 2026 and 2031. The success of e-commerce in the dog food market relies on robust last-mile delivery infrastructure, AI-driven recommendation systems, and flexible fulfillment options, including buy online, pick up in store. Social commerce platforms like TikTok Shop and Instagram enhance product discovery, driving impulse purchases through short-form video content. Amazon's introduction of the Wag brand, combined with its Prime membership benefits, intensifies competition for traditional channels by leveraging its logistics network to provide same-day or next-day delivery in major metropolitan areas. Omnichannel retailers integrate inventory across physical and digital platforms to reduce stock-outs and maintain consistent pricing.

Geography Analysis

North America holds the largest share, accounting for 44.9% of revenue in 2025, reflecting high per-dog spending, widespread adoption of premium brands, and a cultural norm of treating dogs as family members deserving of quality nutrition and healthcare. The United States dominates the region, with an estimated 65-70 million dog-owning households spending an average of USD 500-700 annually on food, treats, and supplements, according to the American Pet Products Association [3]Source: American Pet Products Association, “Pet Industry Market Size, Trends and Ownership Statistics,” americanpetproducts.org. Canada and Mexico contribute smaller shares, both markets exhibit premiumization trends, driven by rising disposable incomes and urbanization, as specialty retail and e-commerce channels grow.

Africa is fastest-growing region and is poised to record a 9.4% CAGR through 2031, the fastest among all regions. This growth is fueled by urbanization in countries such as Nigeria, South Africa, Kenya, and Ghana, which is normalizing dog ownership beyond traditional guard-dog roles and increasing demand for commercial feeding solutions. South Africa leads the continent with its established retail infrastructure and a growing middle class adopting Western pet-care practices. Meanwhile, Nigeria's population growth and rising incomes position it as a long-term growth driver, despite current infrastructure challenges.

The Asia-Pacific region is projected to grow significantly, supported by rapid income growth in countries such as China, India, Indonesia, and Vietnam. In these markets, dog ownership is transitioning from a rural utility to an urban companion. China's pet food market, the largest in Asia, experienced accelerated premiumization in 2025, with local brands like Yantai China Pet Foods and international players competing for market share among millennial and Gen Z pet owners willing to invest in imported or super-premium products. Japan and Australia represent mature markets characterized by high per-dog spending and strong regulatory frameworks ensuring product safety and nutritional adequacy. India, while currently underpenetrated, holds double-digit growth potential as rising incomes and the shift to nuclear-family structures drive increased pet ownership.

Competitive Landscape

The dog food market is moderately competitive, with both global multinational corporations and regional players. Prominent global companies such as Mars, Incorporated, Nestlé S.A., The J. M. Smucker Company, Colgate-Palmolive Company, and General Mills Inc. hold significant market share. These companies benefit from economies of scale in procurement, research and development, and marketing activities. General Mills Inc. has strengthened its position in the pet food segment through acquisitions, including the purchase of Whitebridge Pet Brands for USD 1.45 billion in November 2024, which added Tiki Pets and Cloud Star to its portfolio alongside Blue Buffalo. Additionally, in April 2024, General Mills acquired Belgium-based Edgard and Cooper for EUR 100 million (USD 108 million), reflecting its confidence in the premium European market.

Private equity firms play a significant role in driving market activity. For instance, The Nutriment Company completed four acquisitions in 2024, including Germany-based PETMAN and United Kingdom-based Pet Treats Wholesale, to establish a comprehensive pan-European raw pet food portfolio. Meanwhile, technology-driven entrants are challenging established players by leveraging direct-to-consumer supply chains. Ollie’s acquisition of DIG Labs’ AI platform in December 2024 enables real-time algorithmic adjustments to formulations based on bio-markers collected through stool analysis. Additionally, the plant-based pet food segment is gaining traction, as evidenced by HOWND's October 2024 acquisition of Pets Choice Limited, underscoring growing interest in alternative protein solutions.

Incumbent companies are responding to market shifts by enhancing omnichannel engagement, increasing R&D investments in novel protein sources, and forming strategic co-manufacturing partnerships to ensure production capacity. Proprietary kibble extrusion technologies are being used to achieve higher nutrient density while meeting clean-label requirements. Marketing strategies now include influencer campaigns and veterinarian education initiatives to build consumer trust. Furthermore, large players leverage their expertise in regulatory compliance to navigate evolving standards related to packaging, ingredients, and product claims across various jurisdictions.

Dog Food Industry Leaders

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

General Mills Inc.

The J. M. Smucker Company

Mars, Incorporated

Nestle S.A. (Purina)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Mars, Incorporated is investing USD 200 million to expand its Royal Canin facility in South Korea, boosting capacity by 40%. The project adds automated packaging to meet surging demand for premium and veterinary diets across China, Japan, and Southeast Asia.

- December 2024: In March 2025, ADM opened its first USD 33 million wet pet food plant in Guadalajara, Mexico, producing high-quality dog and cat food. This facility shifts ADM from imports to local manufacturing, directly addressing Mexico's surging demand for functional, domestic pet nutrition.

- March 2023: Mars, Incorporated, launched its first pet food research and development center in the Asia-Pacific region, the Asia-Pacific Pet Center. The facility focuses on advancing product innovation for dog food and treats, supporting formulation, palatability, and nutritional research to strengthen Mars’ offerings in the growing regional dog food market.

Global Dog Food Market Report Scope

Dog food is commercially produced animal feed specifically formulated to meet dogs' nutritional requirements. It typically contains a combination of ingredients such as meat, poultry, fish, grains, and added vitamins and minerals. Dog food is designed to provide complete and balanced daily nutrition or to be used as treats.

The dog food market report is segmented by pet food product (food, pet nutraceuticals/supplements, pet treats, pet veterinary diets), by distribution channel (convenience stores, online channel, specialty stores, supermarkets/hypermarkets, and other channels), and by geography (Africa, Asia-Pacific, Europe, North America, and South America). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft and Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | ||

| Diabetes | ||||

| Digestive Sensitivity | ||||

| Obesity Diets | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary tract disease | ||||

| Other Veterinary Diets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Africa | Country | South Africa |

| Rest of Africa | ||

| Asia-Pacific | Country | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| Philippines | ||

| Taiwan | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | Country | France |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| North America | Country | Canada |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | Country | Argentina |

| Brazil | ||

| Rest of South America |

| By Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft and Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | |||

| Diabetes | |||||

| Digestive Sensitivity | |||||

| Obesity Diets | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary tract disease | |||||

| Other Veterinary Diets | |||||

| By Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

| By Geography | Africa | Country | South Africa | ||

| Rest of Africa | |||||

| Asia-Pacific | Country | Australia | |||

| China | |||||

| India | |||||

| Indonesia | |||||

| Japan | |||||

| Malaysia | |||||

| Philippines | |||||

| Taiwan | |||||

| Thailand | |||||

| Vietnam | |||||

| Rest of Asia-Pacific | |||||

| Europe | Country | France | |||

| Germany | |||||

| Italy | |||||

| Netherlands | |||||

| Poland | |||||

| Russia | |||||

| Spain | |||||

| United Kingdom | |||||

| Rest of Europe | |||||

| North America | Country | Canada | |||

| Mexico | |||||

| United States | |||||

| Rest of North America | |||||

| South America | Country | Argentina | |||

| Brazil | |||||

| Rest of South America | |||||

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms