Africa Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

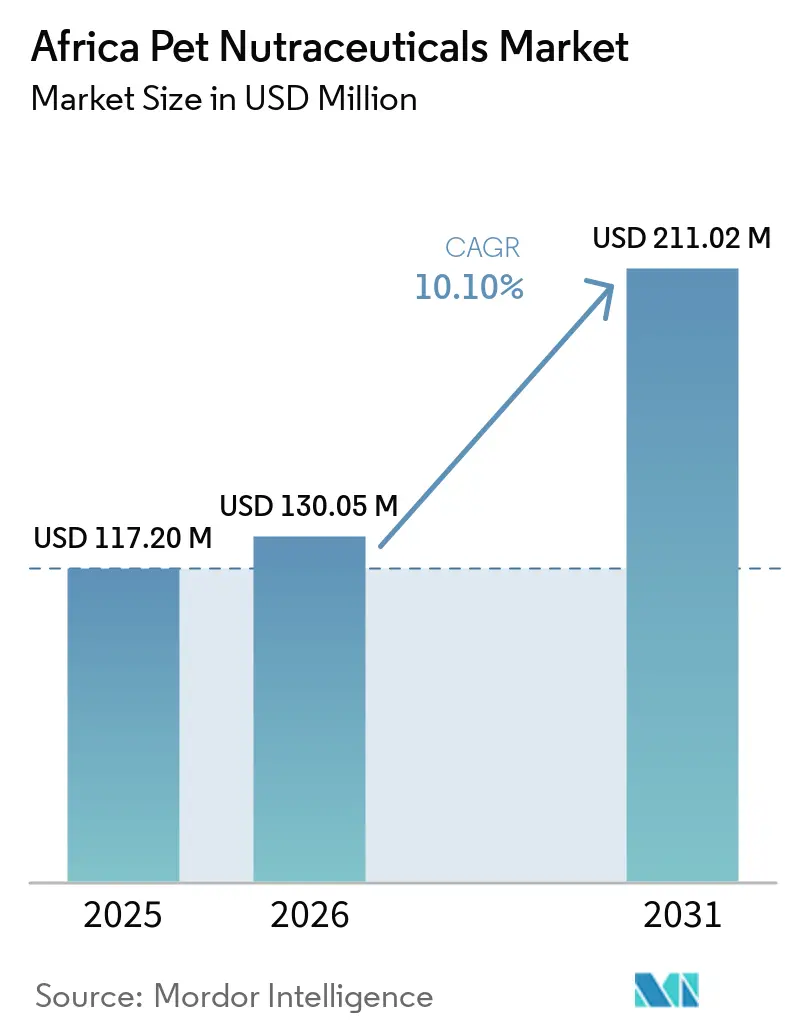

| Base Year Market Size (2025) | USD 117.20 Million |

| Market Size (2026) | USD 130.05 Million |

| Market Size (2031) | USD 211.02 Million |

| Growth Rate (2026 - 2031) | 10.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Pet Nutraceuticals Market Analysis by Mordor Intelligence

The Africa Pet Nutraceuticals Market size was valued at USD 117.20 million in 2025 and is estimated to grow from USD 130.05 million in 2026 to reach USD 211.02 million by 2031, at a CAGR of 10.10% during the forecast period (2026-2031). The category is moving beyond basic feeding, as more urban households now treat pet wellness as a planned part of daily care rather than a response to illness. Demand is being shaped by stronger interest in vitamins, omega-3 fatty acids, probiotics, and specialty proteins, especially in South Africa, Nigeria, Kenya, Egypt, and Morocco. Veterinary credibility is becoming a major route for category adoption, particularly in cities where pet owners want clearer health claims and practical product guidance. Regulatory progress in South Africa is also improving confidence in registered products and may influence quality expectations in nearby markets. As digital ordering expands and local co-manufacturing improves, the Africa pet nutraceuticals market is likely to become less dependent on imports and better positioned for steady category expansion.

Key Report Takeaways

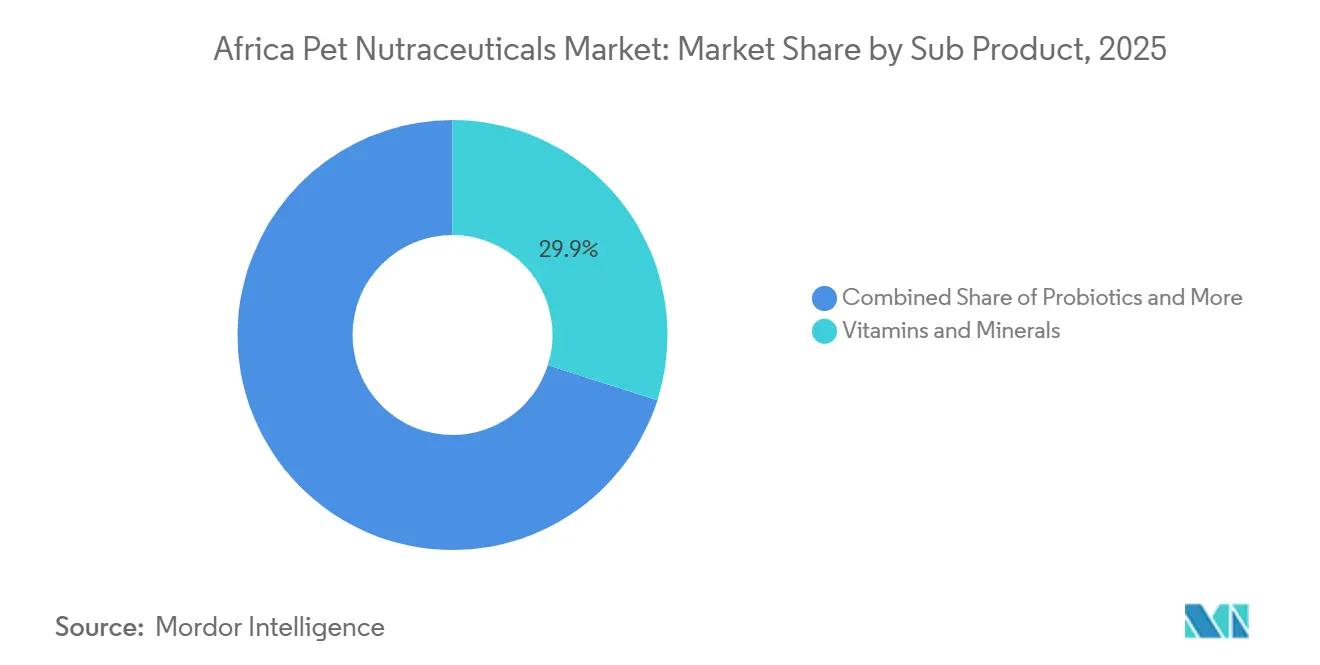

- By sub-product, vitamins and minerals were the largest segment, accounting for 29.9% of the Africa pet nutraceuticals market size in 2025, and are also the fastest-growing sub-product category, projected to grow at 10.5% through 2031.

- By pet type, dogs were the largest segment, accounting for 91.8% of the Africa pet nutraceuticals market share in 2025, and cats are the fastest-growing pet category, projected to grow at 13.4% through 2031.

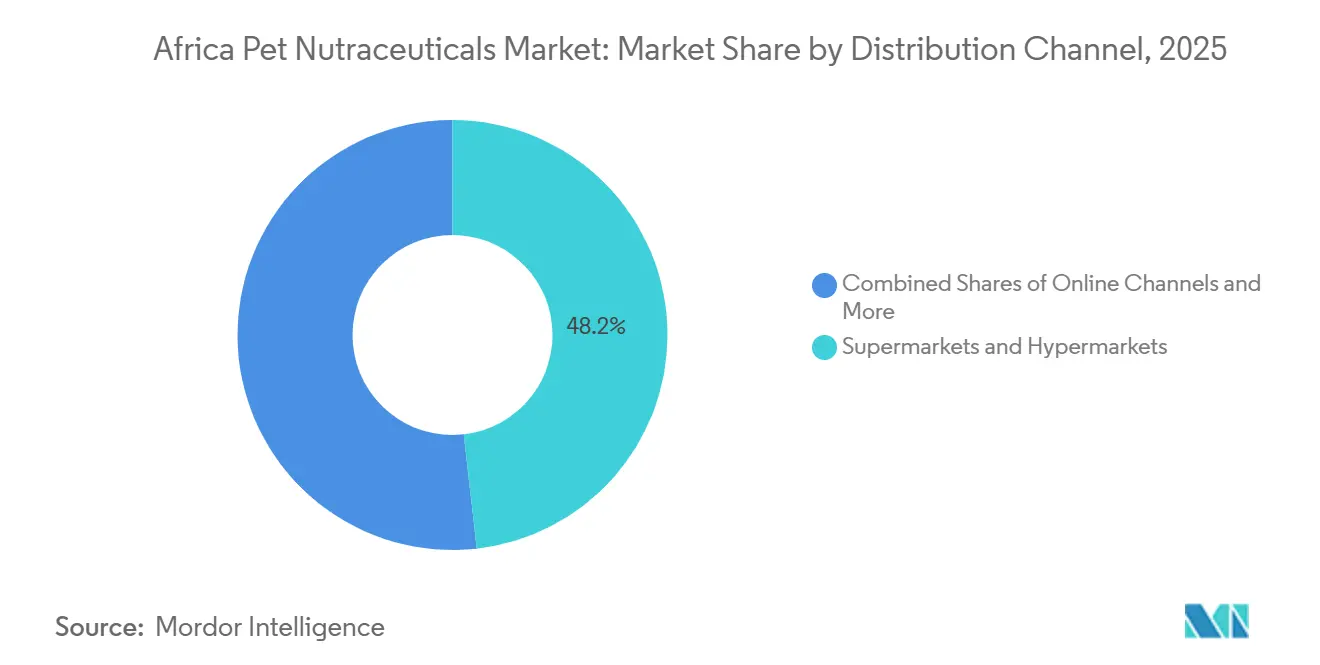

- By distribution channel, supermarkets and hypermarkets were the largest channel with 48.2% share in 2025, while the online channel is the fastest segment and is projected to grow at 11.1% through 2031 as part of the Africa pet nutraceuticals market size outlook.

- By geography, South Africa was the largest country market with a 19.2% share in 2025, while South Africa is also the fastest-growing region with a 10.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet humanization and wellness spending | +2.5% | Global, with concentration in South Africa, Nigeria, Kenya | Short term (≤ 2 years) |

| Expansion of veterinary-recommended preventive care | +1.8% | South Africa core, East Africa, Southern African Development Community spillover | Medium term (2-4 years) |

| Growth of premium functional formulations in urban centers | +1.5% | South Africa, Egypt, Nigeria, Morocco | Medium term (2-4 years) |

| Faster e-commerce access and digital ordering adoption | +1.2% | South Africa, Kenya, Nigeria, with spillover across urban Middle East and North Africa | Short term (≤ 2 years) |

| Improving cold-chain and last-mile distribution for sensitive ingredients | +1.0% | South Africa core, incremental gains across East and West Africa | Long term (≥ 4 years) |

| Formalization of feed and supplement regulation improving trust | +0.8% | South Africa primary, Southern African Development Community secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization and Wellness Spending

Pet humanization has made companion animal health spending more emotionally important for many urban households across Africa. This shift is helping the Africa pet nutraceuticals market shift from discretionary purchases to recurring wellness spending. South Africa remains the clearest example, where specialist retail has broadened consumer access to life-stage and condition-based pet nutrition. The Pet Food Industry Association of Southern Africa reported that ingredient transparency and clinically supported claims now rank high in buying decisions, especially for vitamins, minerals, and joint-care products. The same pattern is emerging in Nairobi, Lagos, and Accra, where branded supplements increasingly signal responsible ownership. That behavior supports repeat demand, as first-time buyers often start with basic wellness products before moving into more specialized formats.

Expansion of Veterinary-Recommended Preventive Care

Veterinarians are becoming a trusted demand channel for supplements that need stronger credibility, especially joint support, omega-3 products, and probiotics. This is helping the Africa pet nutraceuticals market build category awareness in places where consumer knowledge is still limited. The African Pet Health Symposium 2026 program placed clear emphasis on prevention-first care and nutritional interventions, showing stronger professional support for supplementation in companion animal health. That matters because veterinary advice can reduce hesitation about new formulations and increase repeat use. The effect is strongest in South Africa and selected East African cities, where pet owners already engage more regularly with formal veterinary care. The main near-term limit is low veterinary density across many rural and secondary markets, which restricts how quickly this channel can scale across the continent.

Growth of Premium Functional Formulations in Urban Centers

Urban middle-income households represent a key demand base for premium formulations in Africa. These households, concentrated in cities such as Johannesburg, Cairo, Lagos, Nairobi, Casablanca, and Accra, provide suppliers with a strategic entry point into the Africa pet nutraceuticals market. The growing pet ownership trend among these households, coupled with increasing awareness of pet health and wellness, drives demand for specialized products. Items such as chewable omega-3 supplements, probiotic toppers, and amino-acid-based recovery formulas cater to this demand and command higher price points compared to basic vitamin blends. Furthermore, urban density enhances unit economics by reducing costs associated with consumer education, retail support, and product replenishment. This makes major city clusters the most practical initial focus for market entry, allowing suppliers to establish a strong foothold before expanding distribution to smaller urban centers and rural areas.

Faster E-Commerce Access and Digital Ordering Adoption

E-commerce is reducing one of the main barriers to specialty supplement adoption, which has been limited physical shelf space. This channel is shortening the route to purchase for the Africa pet nutraceuticals market, especially in major cities. Platforms such as Takealot and Jumia allow imported and locally produced supplements to reach buyers who may never see these products in general retail. The Global Cold Chain Alliance linked quick-commerce and dark-store growth across African cities to rising cold-chain investment, which should gradually widen online availability for sensitive stock-keeping units. Digital commerce also gives brands direct customer data, which helps shape subscription models and repeat-order programs. That matters in a category where education, trial, and retention are more important than one-time impulse purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing limits mass adoption outside major cities | -1.5% | Pan-Africa, most acute in rural Sub-Saharan Africa | Short term (≤ 2 years) |

| Uneven regulatory clarity across african markets | -1.2% | Pan-Africa, most acute outside South Africa and Egypt | Medium term (2-4 years) |

| Limited veterinary density in secondary and rural markets | -0.8% | Rural Sub-Saharan Africa, West Africa, Central Africa | Long term (≥ 4 years) |

| Import dependence raises lead times and supply risk | -0.5% | Pan-Africa, highest severity in landlocked markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Limits Mass Adoption Outside Major Cities

Premium pricing remains one of the clearest barriers to wider adoption across the continent. In much of Africa, imported nutraceuticals still sit far above what many households can spend repeatedly on pet care. This limits the Africa pet nutraceuticals market to affluent buyers in major cities, even when awareness is rising. The challenge is stronger in peri-urban and rural areas where informal feeding practices remain common and basic functional supplementation still feels nonessential. Lower-cost delivery formats such as sachets, bulk powders, and tablet chewables could widen the addressable base if they maintain active ingredient quality. That is particularly relevant in Nigeria, Ghana, and Tanzania, where urban demand is growing but household budgets remain a major filter on repeat purchase behavior.

Uneven Regulatory Clarity Across African Markets

Regulatory inconsistency makes regional expansion harder than it appears from a demand perspective. South Africa has a more structured pathway, but many other African markets still lack dedicated rules for pet nutraceutical labeling and claims. This slows the Africa pet nutraceuticals market because suppliers must manage country-by-country interpretation instead of following a clear regional standard. The South African government continues to set out registration requirements under Act 36 of 1947, which gives local operators a more visible compliance base than many neighboring markets[1].Source: Animal Feed Manufacturers Association, “Feed And Pet Food Bill,” afma.co.za The absence of harmonized standards across several major markets also weakens consumer trust because enforcement quality is uneven. Until broader alignment develops, registered brands will still face delays, added cost, and inconsistent treatment next to informal imports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Vitamins and Minerals Anchor Baseline Supplementation

Vitamins and minerals accounted for the largest market share at 29.9% in 2025 and are also the fastest-growing sub-product category, with a projected growth rate of 10.5% through 2031. This trend highlights that basic micronutrient support remains the primary entry point for buyers exploring functional pet nutrition for the first time. These products address fundamental wellness needs that are straightforward to explain, price, and distribute compared to more specialized formulations. The simplicity and accessibility of these products make them appealing to a broad range of consumers, particularly those new to functional pet nutrition. Claims related to bone health and coat quality remain particularly significant for dog owners in South Africa and key cities in West Africa, where pet owners are increasingly prioritizing their pets' overall health and appearance. This growing awareness and demand for pet wellness products are expected to further drive the adoption of vitamins and minerals in these regions.

The Africa pet nutraceuticals market size for premium sub-products is being shaped more by value growth than by basic volume growth, as omega-3 fatty acids and probiotics move into a stronger premium position. These categories benefit from rising awareness around digestive health, immune support, and recovery-focused care in urban settings. They also fit well with specialist retail and online formats where product education is easier to deliver. Mars Incorporated said that in October 2025, its Next Generation Pet Food Program had selected startups specializing in biotech-based nutrients and fermentation-derived proteins, reflecting trends relevant to the Africa Pet Nutraceuticals Market and the direction of emerging functional differentiation[2]Source: Mars Incorporated, “Big Idea Ventures And Mars Petcare Select Three Startups For 2025 Pet Food Program,” mars.com. Within the Africa pet nutraceuticals industry, probiotics face a practical limit in markets with weak cold chains. That creates room for heat-stable strains and shelf-stable formats that can tolerate ambient transport better than standard refrigerated products.

By Pets: Dogs Dominate, Cats Represent a Structural Growth Opportunity

Dogs held the largest market share at 91.8% in 2025, reflecting the long-standing dominance of canine ownership across many African countries. This concentration also mirrors dosage economics, since dogs usually require larger volumes than cats and therefore represent a greater share of category value. The scale of dog demand means even modest adoption gains can add meaningful volume to the Africa pet nutraceuticals market. In many urban areas, dog ownership combines companionship, status, and security, creating demand for joint care, skin health, and digestive support. The shift from informal feeding toward formulated pet nutrition in Nigeria, Kenya, and Ghana is also creating a first-purchase pathway for vitamins and minerals. That early trial behavior can later support movement into higher-value functional categories.

Cats are the fastest-growing pet category, projected to grow at 13.4% through 2031. The Africa pet nutraceuticals market size for cats remains much smaller, but the segment has a credible long-term growth path as apartment living rises in South Africa, Egypt, Morocco, and Nairobi. Cat ownership fits smaller homes and urban lifestyles, making it more visible in dense city settings. In its March 2025 investor presentation, Colgate-Palmolive Company emphasized ongoing investment in science-based specialty nutrition through Hill's Pet Nutrition Inc., reinforcing the strategic importance of targeted feline nutrition in the Africa Pet Nutraceuticals Market[3]Source: Colgate-Palmolive Company, “Investor Presentation, March 2025,” investor.colgatepalmolive.com. That matters because renal support, urinary health, and weight management are more differentiated product needs than basic wellness support. Within the Africa pet nutraceuticals industry, cats still start from a low base, but the category offers suppliers a clearer premium niche than mass-market dog supplements. Other pets remain small and specialized, with limited scale compared with the two main companion animal groups.

By Distribution Channel: Online Channel Challenges Supermarket Primacy

Supermarkets and Hypermarkets held the largest market share at 48.2% in 2025, supported by their broad reach in South Africa and their expanding urban presence in Nigeria, Kenya, and Egypt. Their advantage comes from foot traffic, familiar shopping behavior, and the ability to place supplements beside regular pet food purchases. That structure helps with basket-building and reduces the effort required for the first-time trial. At the same time, the online channel is the fastest channel with an projected 11.1% CAGR through 2031. This combination shows that the Africa pet nutraceuticals market still relies on general retail for its current scale, while digital formats will lead the next phase of growth. Online retail also gives niche brands access to buyers without waiting for broad physical shelf placement.

The Africa pet nutraceuticals market size linked to digital channels is likely to grow as online assortments improve and replenishment programs become easier to manage. Specialty stores still matter because they give premium products a stronger educational environment and a better fit for veterinary referral. That model is best developed in South Africa and remains in its early stages in much of the rest of the continent. Convenience stores and other channels continue to serve lower-priced, proximity-led demand, while modern retail remains limited. Within the Africa pet nutraceuticals industry, many brands are likely to treat e-commerce as the testing ground before wider physical expansion.

Geography Analysis

South Africa is projected to hold the largest share of the Africa pet nutraceuticals market in 2025, accounting for 19.2%. This dominance is attributed to higher urbanization levels, a well-established veterinary infrastructure, broader retail distribution, and a longer history of registered pet nutrition products. The country's urbanization has driven an increase in pet ownership, boosting demand for advanced pet care solutions, including nutraceuticals. Furthermore, a well-developed veterinary network ensures better access to professional advice and recommendations on pet nutrition. Additionally, South Africa's retail sector offers extensive coverage, making pet nutraceutical products more accessible to consumers. The market also benefits from a robust compliance framework that enhances product trust, encourages participation through formal channels, and fosters industry growth and stability.

South Africa is also the fastest-growing region with a 10.3% CAGR through 2031. The rest of Africa represents the broader growth field, although market maturity differs sharply by subregion. Egypt and Morocco are among the more commercially developed markets because urban demand and formal veterinary engagement are relatively stronger there. Kenya and Tanzania are early-stage markets, but Nairobi and other urban centers are showing improving conditions for omega-3 and probiotic adoption. Nigeria and Ghana offer clear volume potential for basic vitamins and minerals, even though price sensitivity still limits premium penetration. Across these countries, the Africa pet nutraceuticals market is being shaped by the same urban pattern, concentrated demand, growing digital access, and stronger interest in proactive pet care.

West Africa and smaller Sub-Saharan African markets remain less formalized, with informal feeding still dominant in many areas. This keeps branded nutraceutical demand narrow outside the main cities and slows physical retail scale-up. A hub-and-spoke model centered on South Africa, Egypt, and Kenya remains the most practical route for regional expansion, balancing logistics and regulatory exposure. The Global Cold Chain Alliance said the African Continental Free Trade Area could raise intra-African trade by 2045, which supports the long-term case for broader cross-border distribution. As harmonization improves, the Africa pet nutraceuticals market should gain from easier movement of finished products and ingredients across regional trade corridors.

Competitive Landscape

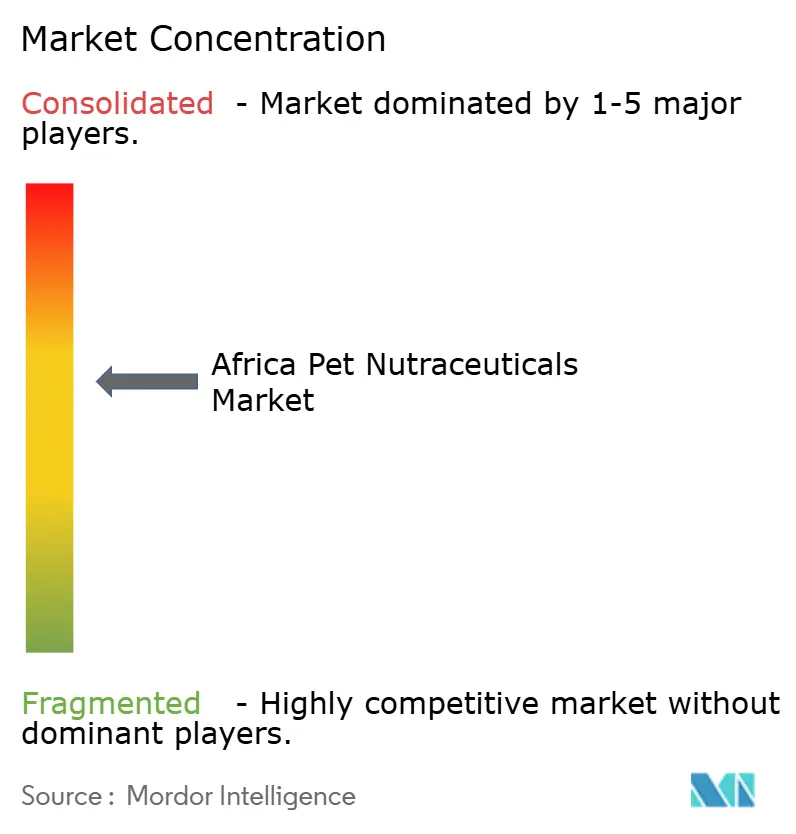

The Africa pet nutraceuticals market remains moderately fragmented, and no company holds a dominant pan-continental position across all categories and countries. Mars Incorporated, Nestle S.A. (Purina), Zoetis Inc., Virbac S.A., and Kemin Industries, Inc. are strongest in premium and therapeutic niches, usually with South Africa as the first point of entry. Regional and niche players still matter because they often move faster in cost-sensitive channels and informal distribution settings. Competition is therefore not defined by a single clear leader, but by distinct strengths in veterinary credibility, retail access, and product specialization.

Mars Incorporated has been actively pursuing upstream innovations that could shape future formulation strategies in the Africa pet nutraceuticals market. In October 2025, the company selected startups specializing in biotech-based essential nutrients and fermentation-derived proteins through its Next Generation Pet Food Program. In June 2026, Mars Incorporated, in collaboration with Big Idea Ventures, expanded this initiative by launching the 2026 Global Pet Food Innovation Program, focusing on ingredient and feed innovation. These efforts indicate that future competition in the Africa pet nutraceuticals market will hinge not only on brand strength and distribution channels but also on securing early access to differentiated ingredients.

Colgate-Palmolive Company has also implemented strategic initiatives aligned with premium functional nutrition in the Africa pet nutraceuticals market. In February 2025, the company announced its agreement to acquire Care TopCo Pty Ltd, the owner of the Prime100 brand, through Hill's Pet Nutrition Inc. Additionally, its March 2025 investor presentation emphasized a commitment to science-backed specialty nutrition through Hill's Pet Nutrition Inc. Within this context, opportunities remain in areas such as cat nutraceuticals, shelf-stable probiotics, and value-tier multivitamins, where agile competitors can establish a foothold in the Africa pet nutraceuticals market before it becomes more standardized.

Africa Pet Nutraceuticals Industry Leaders

Mars, Incorporated

Virbac SA

Zoetis Inc.

Nestle S.A. (Purina)

Kemin Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mars Incorporated and Big Idea Ventures have launched the 2026 Global Pet Food Innovation Program in collaboration with AAK, Bühler, and Givaudan. The program supports startups developing biotech-based ingredients and essential nutrients, with potential applications in the Africa pet nutraceuticals market. It emphasizes innovations like microalgae-based taurine and fermentation-derived proteins for future product pipelines.

- April 2025: The Pet Food Industry Association of Southern Africa issued updated guidelines on pet food labels, requiring accurate listing of vitamins, minerals, and nutraceutical additives at inclusion levels as of the best-before date. This supports transparency and consumer trust in Africa's pet nutraceuticals market.

- February 2025: Colgate-Palmolive Company announced an agreement to acquire Care TopCo Pty Ltd, the owner of the Prime100 fresh pet food brand, through its Hill's Pet Nutrition Inc. division. This acquisition supports Hill's expansion into the fresh and functional pet nutrition segment, with potential implications for the growing Africa pet nutraceuticals market.

Africa Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are non-drug, food-derived substances administered to animals to provide medicinal or health benefits. They are primarily used to support organ function, promote joint health, boost immunity, and help prevent or manage chronic conditions.

The Africa Pet Nutraceuticals Market Report is Segmented by Sub Product (Milk Bioactives, Omega-3 Fatty Acids, Probiotics, Proteins and Peptides, Vitamins and Minerals, and More), by Pets (Cats, Dogs, and Other Pets), by Distribution Channel (Convenience Stores, Online Channel, and More), and by Geography (South Africa and the Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Nutraceuticals |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| South Africa |

| Rest of the Africa |

| Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Nutraceuticals | |

| Pets | Cats |

| Dogs | |

| Other Pets | |

| Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels | |

| Geography | South Africa |

| Rest of the Africa |

Key Questions Answered in the Report

What is the outlook for Africa pet nutraceuticals through 2031?

The Africa pet nutraceuticals market is projected to rise from USD 130.05 million in 2026 to USD 211.02 million by 2031, at a 10.10% CAGR. Growth is being supported by rising pet humanization, stronger wellness spending, wider online access, and higher interest in preventive veterinary care, especially in major urban centers.

Which country leads sales across the continent?

South Africa was the largest country market in 2025 with a 19.2% share, supported by a stronger retail base, better veterinary access, and a clearer regulatory structure.

Which pet category contributes the most revenue?

Dogs accounted for 91.8% of category value in 2025, making canine-focused supplements the main source of current demand.

Which product type has the strongest current position?

Vitamins and Minerals was the largest sub product segment in 2025 with a 29.9% share, showing that basic supplementation remains the main entry point for many buyers.

Which sales channel is growing fastest?

Online Channel is the fastest channel and is projected to grow at 11.1% through 2031, helped by digital ordering and wider product discovery.

What are the main challenges for suppliers entering African markets?

The biggest constraints are premium pricing outside major cities, uneven regulation, low veterinary density in many areas, and heavy reliance on imported active ingredients.

Page last updated on: