Small Breed Dog Food Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

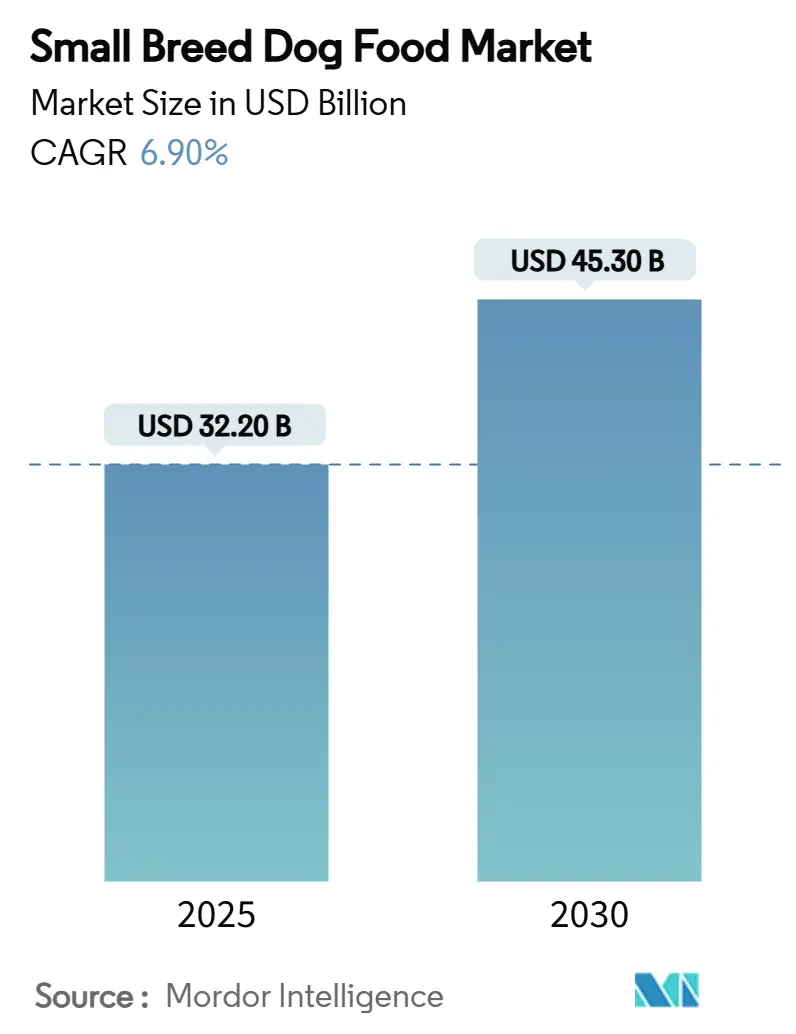

| Market Size (2025) | USD 32.20 Billion |

| Market Size (2030) | USD 45.30 Billion |

| Growth Rate (2025 - 2030) | 6.90% CAGR |

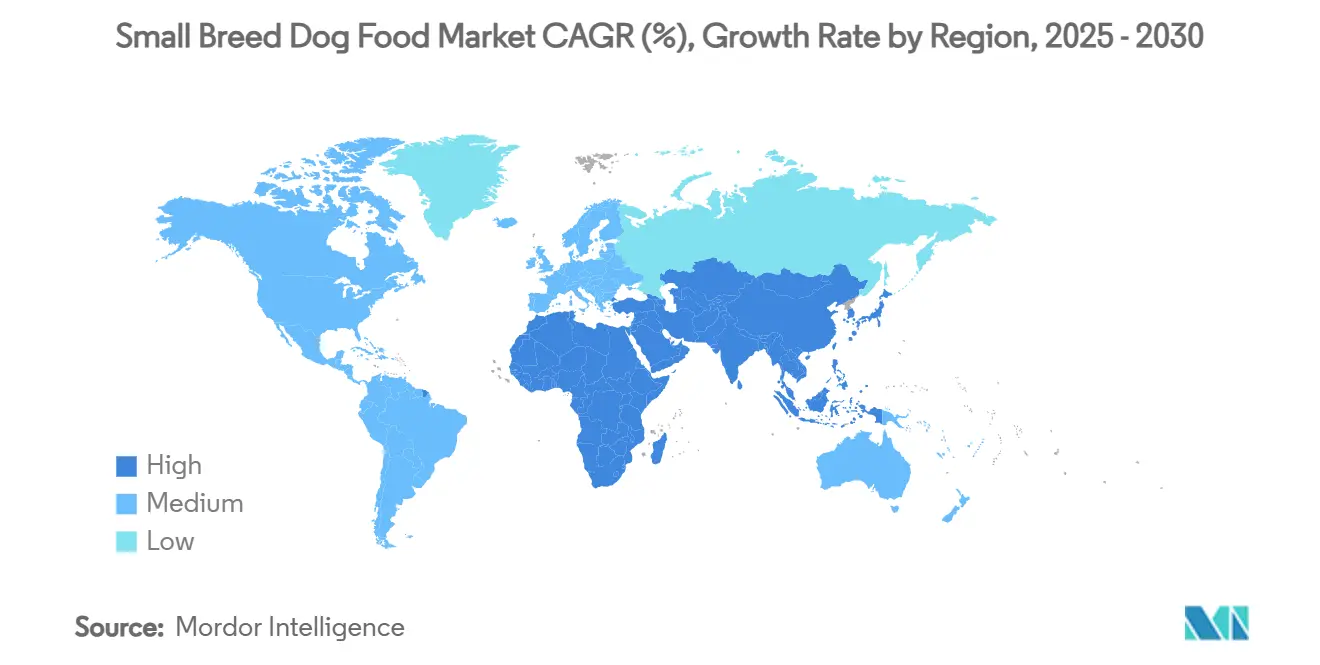

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Breed Dog Food Market Analysis by Mordor Intelligence

The small breed dog food market is valued at USD 32.2 billion in 2025 and is forecast to reach USD 45.3 billion by 2030, expanding at a 6.9% CAGR, with both the current market size and the projected CAGR illustrating a robust growth runway. Momentum is anchored in three concurrent forces, including sustained urbanization that favors compact companions, the premiumization of breed-specific nutrition, and digital retail models that use data to refine replenishment cycles. Treats and snacks are expanding fastest as owners blend functional supplements with reward routines, while dental mini-kibble continues to elevate premium dry recipes. North America remains the largest revenue hub, but Asia-Pacific delivers the highest incremental value, driven by rising disposable income and pet humanization across Shanghai, Tokyo, and Mumbai. Digital transformation quickens, with subscription deliveries reducing friction for time-pressed millennials and funneling granular consumption data back to formulators, these insights are already shaping AI-powered feeding recommendations that strengthen lifetime customer value.

Key Report Takeaways

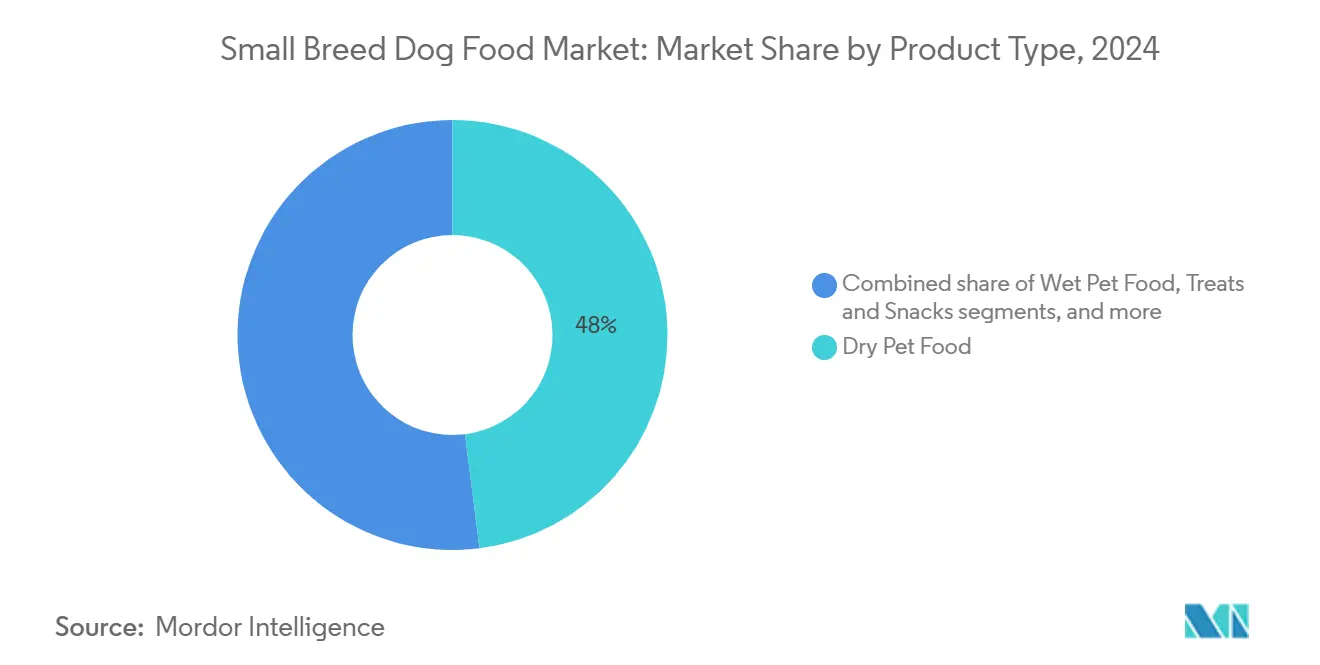

- By product type, dry pet food held 48% of the small breed dog food market share in 2024, whereas treats and snacks are set to post a 9% CAGR through 2030.

- By ingredient source, animal proteins commanded 68% share of the small breed dog food market size in 2024, with insect inputs projected to advance at an 8.2% CAGR to 2030.

- By life stage, adult formulas accounted for 41.5% of the small breed dog food market in 2024, while senior diets will log the fastest 7% CAGR.

- By health functionality, dental recipes captured 28% of the small breed dog food market size in 2024 and are advancing at an 8.2% CAGR.

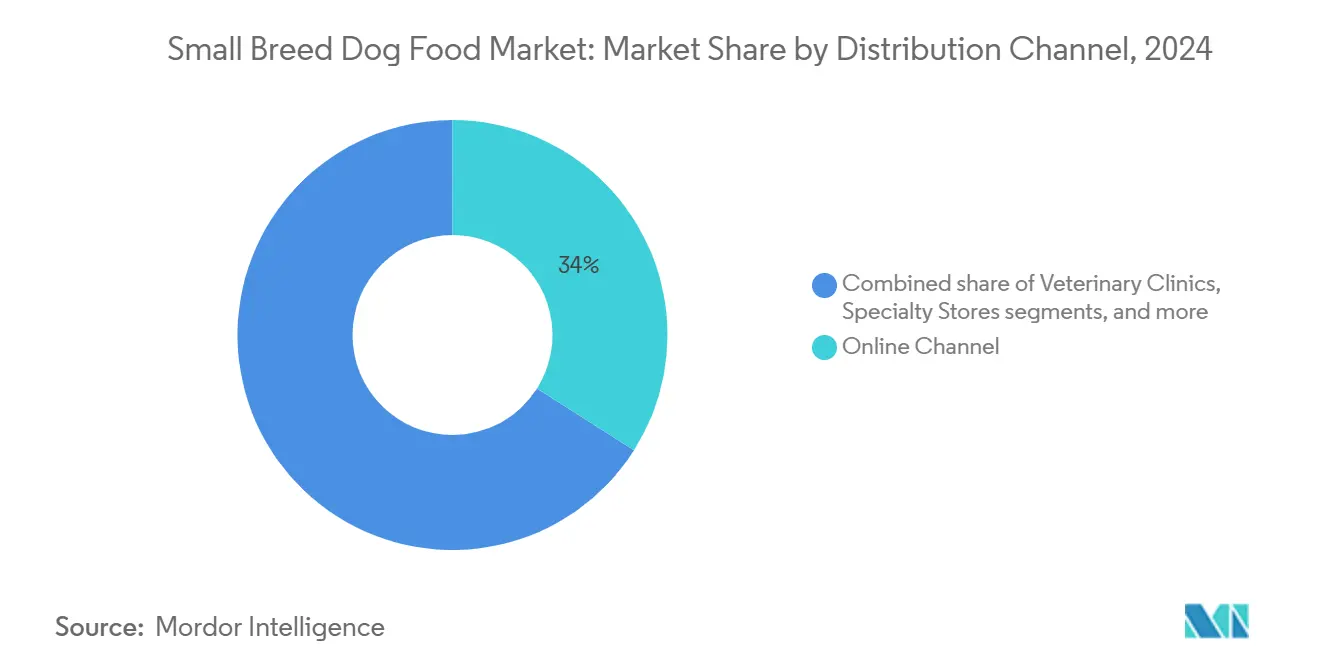

- By distribution channel, online sales represented 34% of the small breed dog food market in 2024 and will grow at an 11.4% CAGR.

- By geography, North America led with 36% revenue share in 2024, whereas Asia-Pacific will record an 8.4% CAGR.

Global Small Breed Dog Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of breed-specific formulas | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| E-commerce subscriptions and auto-delivery | +1.5% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Urban millennial preference for small dogs | +1.2% | Global urban centers, particularly Asia-Pacific | Long term (≥ 4 years) |

| Veterinary endorsement of dental mini-kibble | +0.9% | North America and Europe | Medium term (2-4 years) |

| Human-grade fresh and refrigerated options scaling | +0.8% | North America, expanding to Europe | Medium term (2-4 years) |

| AI-powered personalized feeding apps | +0.6% | North America and Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization of Breed-Specific Formulas

Premium dry and wet food tailored to small jaws, caloric density, and metabolic rates commands 30–50% price premiums over mass offerings. Mars’ Royal Canin Small Indoor Adult range and Hill’s Science Diet Small Paws deliver targeted nutrient profiles validated by clinical trials, cementing brand loyalty and supporting margin expansion[1]Source: Mars Incorporated, “Royal Canin Small Indoor Adult Product Sheet,” MARS.COM . Growing veterinary collaboration reinforces science-backed claims, prompting retailers to allocate extra shelf space to high-ticket SKUs. Market leaders are extending this strategy to supplements, with Royal Canin adding probiotics in 2025 to widen average order values. Accelerating label transparency mandates in the United States and the European Union amplifies consumer trust and further legitimizes premium tiers.

E-commerce Subscriptions and Auto-Delivery

Chewy, Amazon, and regional platforms capture subscribers seeking hassle-free replenishment and bulk discounts. The recurring customers spend 35% more per pet annually, justifying heavy investment in predictive logistics. AI-driven recommendation engines adjust portion sizes by weight, age, and activity, reducing food waste and enhancing wellness outcomes. COVID-19 era shopping behavior persisted into 2025, pushing online penetration of the small breed dog food market beyond 40% in developed economies. Brand owners leverage direct-to-consumer portals to test limited-edition flavors, shortening R&D cycles and nurturing feedback loops.

Urban Millennial Preference for Small Dogs

Rising apartment living and delayed parenthood in Seoul, São Paulo, and New York underpin a multiyear surge in toy and miniature breeds. It indicates that households earning above USD 75,000 allocate USD 1,630 per dog annually, 17% higher than the national average. Public transport pet-friendly rules in major Asian cities make compact breeds practical, reinforcing steady intake of specialized kibble and treats. Developers of pet-centric condominiums partner with premium brands to offer welcome boxes, creating embedded demand channels. This demographic shift supports durable volume and value gains for the small breed dog food market.

Veterinary Endorsement of Dental Mini-Kibble

The American Veterinary Medical Association links periodontal disease prevention to kibble diameter and texture, prompting clinics to recommend purpose-designed bites that scrub plaque mechanically. Hill’s patented interlocking fiber matrix and Nestlé Purina’s crunchy-soft dual cores recorded double-digit growth in clinic dispensaries. Oral-care-focused lines extend into treats, rinse-free chews, and water additives, broadening revenue streams. Insurers in Canada now reimburse dental diets, further spurring uptake. Manufacturer educational grants ensure continuous professional development, deepening the prescriber relationship and safeguarding premium shelf pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven down-trading to economy brands | -1.4% | Global, strongest impact in emerging markets | Short term (≤ 2 years) |

| Supply volatility of premium proteins | -1.1% | Global, particularly affecting premium segments | Medium term (2-4 years) |

| FDA scrutiny of grain-free diets | -0.8% | North America, expanding to other regions | Medium term (2-4 years) |

| Cold-chain emission cost pressure | -0.5% | Global, strongest in regions with strict environmental regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Down-Trading to Economy Brands

United States Pet food Consumer Price Index (CPI) sits 23% in 2025 above to past four years, despite recent easing, prompting 43% of owners to curtail spending. Price-sensitive owners switch to private-label formulations, temporarily slowing premium velocity. Retailers respond with better-for-less tiers that mimic leading SKUs at 15% lower price points. While trade-down risk is most pronounced in Brazil, India, and South Africa, loyalty programs and couponing partially offset volume leakage in mature markets. Manufacturers streamline packaging sizes and leverage contract co-packing to defend shelf presence without eroding brand equity.

Supply Volatility of Premium Proteins

Highly Pathogenic Avian Influenza outbreaks tightened egg supplies and pushed global spot prices up 40% in 2025[2]Source: The Cattle Site, “A 41.1% Increase in U.S. Egg Prices Expected in 2025,” THECATTLESITE.COM , lifting formulated diet costs. Drought-driven feed scarcity elevated beef and lamb raw material quotes, pressuring gross margins for wet pates rich in novel meats. Producers hedge through diversified sourcing, investing in insect meal and cultivated chicken pilot lines to stabilize inputs. Regulatory clearance of mealworm protein by AAFCO in 2024 provides risk mitigation, but palatability trials for miniature breeds lengthen commercialization timelines. Sustained volatility challenges price stability for the small-breed dog food market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dry Dominance Faces Fresh Innovation

Dry pet food anchored 48% of the small breed dog food market in 2024 because it balances cost, convenience, and dental benefits. Shape-optimized bites encourage chewing, improving oral hygiene without added steps. Wet food is appealing to picky eaters and older dogs with reduced bite force, yet margin pressure persists due to aluminum can price inflation.

Treats and snacks are emerging as the standout category, experiencing a 9% CAGR driven by functional chews aimed at anxiety relief and joint support. The subcategory’s premium sticks and refrigerated bites mirror human snacking trends, positioning it as a daily routine rather than an occasional indulgence. Fresh-frozen meals remain a niche but log the fastest dollar growth as cold-chain networks expand. Owners with limited storage still rely on shelf-stable tins and pouches, signaling a coexistence of formats rather than outright substitution within the small-breed dog food market.

By Ingredient Source: Alternative Proteins Enter the Mainstream

Animal protein recipes captured 68% of the small breed dog food market in 2024, leveraging high digestibility and amino acid completeness. Rising sustainability scrutiny, however, fuels double-digit gains for plant and insect inputs. The 2025 AAFCO nod for dried mealworm meal lets brands launch eco-labels boasting 80% lower land use than poultry. Plant-forward blends using pea or chickpea isolates face taurine supplementation challenges but meet vegan owner preferences in select urban clusters.

Insect-based protein development demonstrates the strongest growth trajectory at 8.2% CAGR through 2030, with companies like Protix partnering with Tyson for global expansion and multiple regulatory approvals pending across international markets. Synthetic nutraceutical boosters such as algal DHA, postbiotics, and yeast-derived beta-glucans are layered into core SKUs to add functional claims without altering taste. These micro-additions defend premium price points despite fluctuating meat costs. Hybrid formats, combining 70% chicken with 30% insect flour[3]Source: Association of American Feed Control Officials, “2025 Ingredient Definition Updates,” AAFCO.ORG , are piloted in Germany and Japan as a compromise between palatability and carbon reduction targets. Gradual consumer education remains vital, yet mainstream acceptance is accelerating inside the small-breed dog food market.

By Life Stage: Adult Formulas Lead, Senior Needs Surge

Adults comprise the largest group, accounting for 41.5% of the small breed dog food market in 2024, as the majority of small breeds maintain a stable metabolic state for extended periods. Formula updates in 2025 introduced L-carnitine and controlled fat to prevent mid-life weight creep. Puppies account for a significant share of consumption and deliver steady revenue through high-frequency feeding schedules. DHA-rich recipes support rapid neurodevelopment and command top-shelf pricing.

Senior SKUs accelerate at 7% CAGR as veterinary visits flag kidney and joint issues earlier. Companies add medium-chain triglycerides for cognitive support and green-lipped mussel for cartilage integrity. Pharmaceutical style packaging with age-indexed labeling simplifies consultation across retail outlets. Manufacturers bundle lab test vouchers with senior diet purchases, embedding a health monitoring loop and elevating stickiness in the small breed dog food market.

By Distribution Channel: Online Service Redefines Convenience

Online channel accounted for 34% of the small breed dog food market in 2024, growing at the highest CAGR of 11.4% driven by automatic reorder services that align with 4-kilogram monthly consumption cycles typical for small breeds. Repeat delivery discounts and curated gift boxes lift basket sizes by 27%. Specialty pet stores retain a good amount of share by offering custom measuring stations and nutrition consultations. Supermarkets are highly profitable but play an essential role in encouraging spontaneous treat purchases during weekly grocery trips.

Veterinary clinics capture a premium margin on prescription diets for urinary and dermatologic issues. Tele-vet platforms integrate in-app food recommendations linked to home delivery, blending professional advice with e-commerce fulfillment. Omnichannel loyalty programs let owners earn points across vet visits, mobile apps, and physical stores, cementing long-term engagement with the small-breed dog food market.

By Health Functionality: Dental and Digestive Lines Gain Momentum

Dental health diets delivered 28% of the small breed dog food market in 2024, and are advancing at an 8.2% CAGR buoyed by evidence that 80% of dogs under 20 lbs show periodontal symptoms by age 3. Clinical chew innovations using enzymatic coatings reduce tartar by up to 44% after 28 days. Digestive health posts the second-fastest growth as prebiotic fiber blends ease sensitive stomachs common to miniature breeds.

Weight management maintains steady demand amid owner concern over sedentary indoor lifestyles. Products fortified with L-carnitine and reduced energy density keep calorie intake in check without diminishing satiety. Skin and coat lines leverage salmon oil and biotin to address atopic dermatitis prevalence among Shih Tzus and Yorkies. Multifunctional recipes now merge dental, joint, and gut claims, compressing SKU counts while raising average selling prices within the small breed dog food market.

Geography Analysis

North America led with 36% revenue share in 2024, underpinned by 66% household pet ownership and mature premium segments. The United States alone has the highest share in small breed formulations, supported by 28,000 veterinary clinics endorsing science-based brands. Canada’s online penetration reached 48%, spurred by high broadband access and harsh winters that favor home delivery. Mexico’s rising middle class boosts volume, yet value uptake trails due to income disparity.

Asia-Pacific is the fastest mover, posting 8.4% CAGR through 2030. China’s small breed dog food market is growing, with imported labels enjoying tariff relief under the Phase 1 trade accord. Japan spends the most per pet at USD 2,056 annually, reflecting aging owner demographics that treat pets as family. India, still early in premium adoption, shows triple-digit online channel growth in smartphone commerce and fintech payment ease. Southeast Asian megacities such as Bangkok and Jakarta witness a surge in toy breed ownership, creating micro-warehouses to speed last-mile delivery.

Europe posts a steady growth. Germany and the United Kingdom anchor volume, while France leads sustainable packaging pilots demanded by eco-conscious shoppers. The European Union’s novel food regulation streamlines insect protein approvals, giving regional pioneers first-mover advantage. Private label share peaks at 34% as discounters in Spain and Poland scale own-brand mini-kibble. Nordic markets experiment with cultivated meat inclusions backed by public R&D grants, signaling future innovation pathways for the small-breed dog food market.

Competitive Landscape

The leading competitors have demonstrated a reasonable level of concentration, while still allowing space for niche players. Mars Incorporated operates through Royal Canin, Cesar, and Nutro ranges. Nestlé Purina, through Purina ONE and Pro Plan Small Breed, is leveraging global manufacturing and veterinary endorsements. Colgate-Palmolive’s Hill’s brand focuses on clinic-exclusive Science Diet and Prescription Diet SKUs. Spectrum exits fish-centric divisions to sharpen focus on dog nutrition, while J.M. Smucker divests select pet assets to realign on consumer staples.

Strategic activity centers on capacity expansion and technology acquisition. Mars inaugurated a new dry plant in Ohio, significantly increasing output while achieving LEED Silver certification. Nestlé Purina broke ground on a wet food factory in Georgia to meet rising pouch demand. General Mills purchased Whitebridge Pet Brands, adding functional toppers and freeze-dried snacks to its Blue Buffalo portfolio. Ongoing consolidation tightens ingredient procurement power but opens white spaces for agile start-ups.

Digital and fresh specialists challenge incumbents. Freshpet, The Farmer’s Dog, and Nom Nom scale subscription platforms that bypass retail markups and gather granular feeding data. Mars invested in AI to personalize nutrition and launched the Greenies Canine Dental Check app that analyzes extensive image datasets for plaque detection. Insect-protein supplier Ÿnsect obtained AAFCO clearance, partnering with multinational co-packers to embed sustainable inputs into legacy brands. These moves intensify innovation cycles inside the small breed dog food market.

Small Breed Dog Food Industry Leaders

Mars, Incorporated

Colgate-Palmolive Company (Hill’s Pet Nutrition, Inc.)

General Mills, Inc.

Spectrum Brands Holdings Inc.

Nestlé (Purina)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mars Incorporated, one of the major small breed dog food suppliers, opened a USD 450 million Royal Canin facility in Lewisburg, Ohio, marking its largest dry pet food factory globally and creating 270 jobs while earning Silver LEED certification for sustainability.

- April 2025: Just Food For Dogs expanded its fresh-frozen dog food line through a partnership with PetSmart, capitalizing on the 30% sales growth in fresh pet food compared to 2.4% in the overall dog food market including small breed dog food.

- November 2024: General Mills announced its acquisition of Whitebridge Pet Brands for USD 1.45 billion, including Tiki Pets and Cloud Star brands that supplies small breed dog food, marking its fifth pet-related acquisition in 6 years.

Global Small Breed Dog Food Market Report Scope

| Dry Pet Food |

| Wet Pet Food |

| Treats and Snacks |

| Other Food |

| Animal-based Protein |

| Plant-based Protein |

| Insect-based Protein |

| Synthetic Nutraceutical Additives |

| Puppy |

| Adult |

| Senior |

| Weight Management |

| Skin and Coat |

| Dental Health |

| Digestive Health |

| Joint Support |

| Others |

| Supermarkets and Hypermarkets |

| Online Channels |

| Specialty Stores |

| Veterinary Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Italy | |

| Netherlands | |

| Poland | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Dry Pet Food | |

| Wet Pet Food | ||

| Treats and Snacks | ||

| Other Food | ||

| By Ingredient Source | Animal-based Protein | |

| Plant-based Protein | ||

| Insect-based Protein | ||

| Synthetic Nutraceutical Additives | ||

| By Life Stage | Puppy | |

| Adult | ||

| Senior | ||

| By Health Functionality | Weight Management | |

| Skin and Coat | ||

| Dental Health | ||

| Digestive Health | ||

| Joint Support | ||

| Others | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Online Channels | ||

| Specialty Stores | ||

| Veterinary Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the small breed dog food market?

The small breed dog food market is worth USD 32.2 billion in 2025.

How fast will the market grow through 2030?

Revenue is projected to rise at a 6.9% CAGR, reaching USD 45.3 billion by 2030.

Which region shows the strongest growth potential?

Asia-Pacific leads with an anticipated 8.4% CAGR, fueled by urbanization and rising disposable income.

What segment expands quickest within the market?

Treats and snacks are forecast to grow at a 9% CAGR as owners pair functional benefits with training rewards.

Page last updated on: