Absence Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

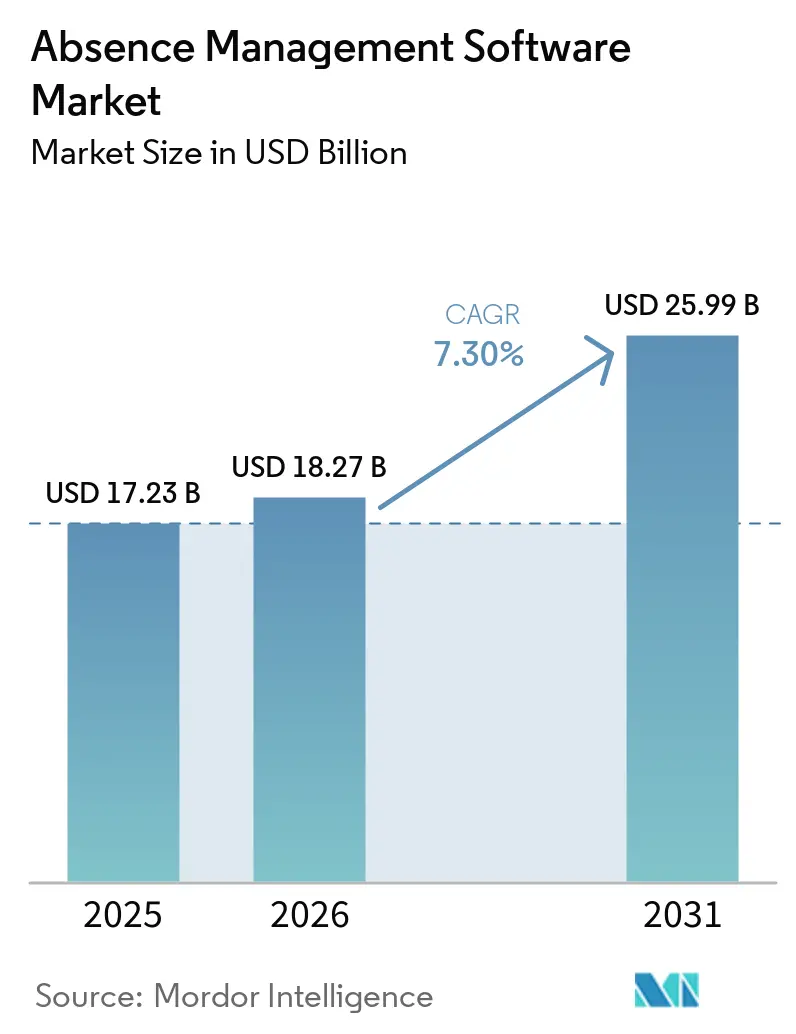

| Market Size (2026) | USD 18.27 Billion |

| Market Size (2031) | USD 25.99 Billion |

| Growth Rate (2026 - 2031) | 7.30% CAGR |

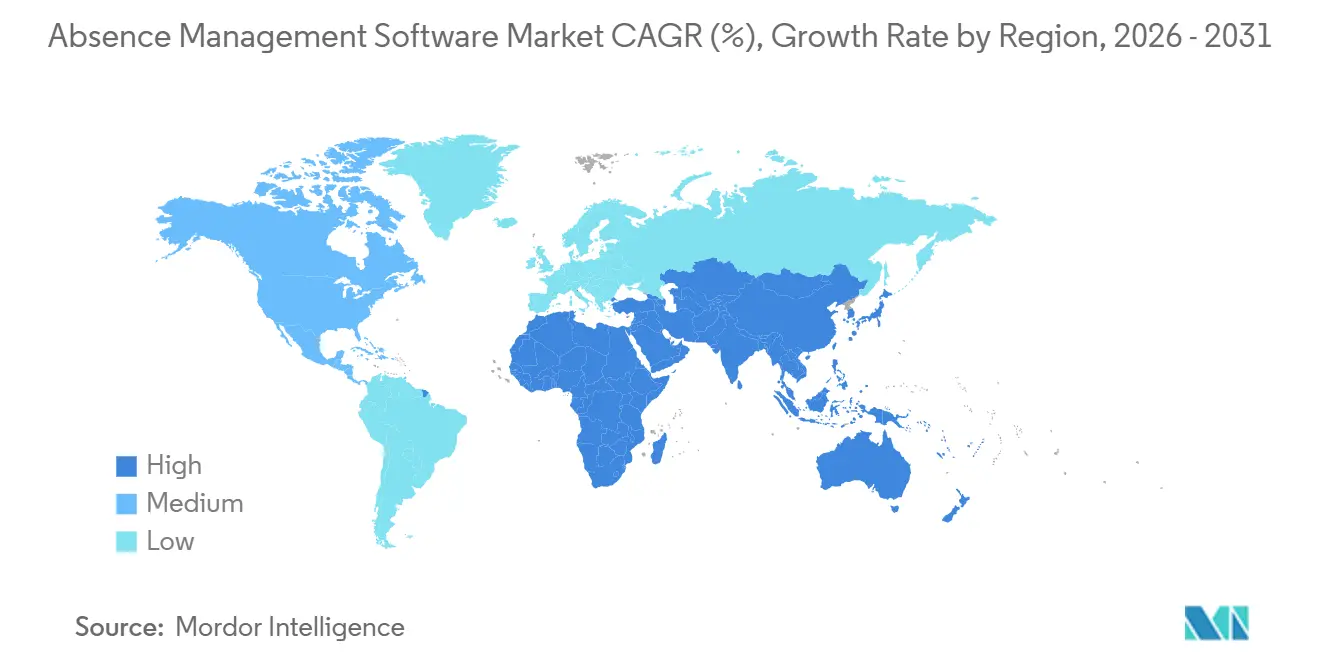

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

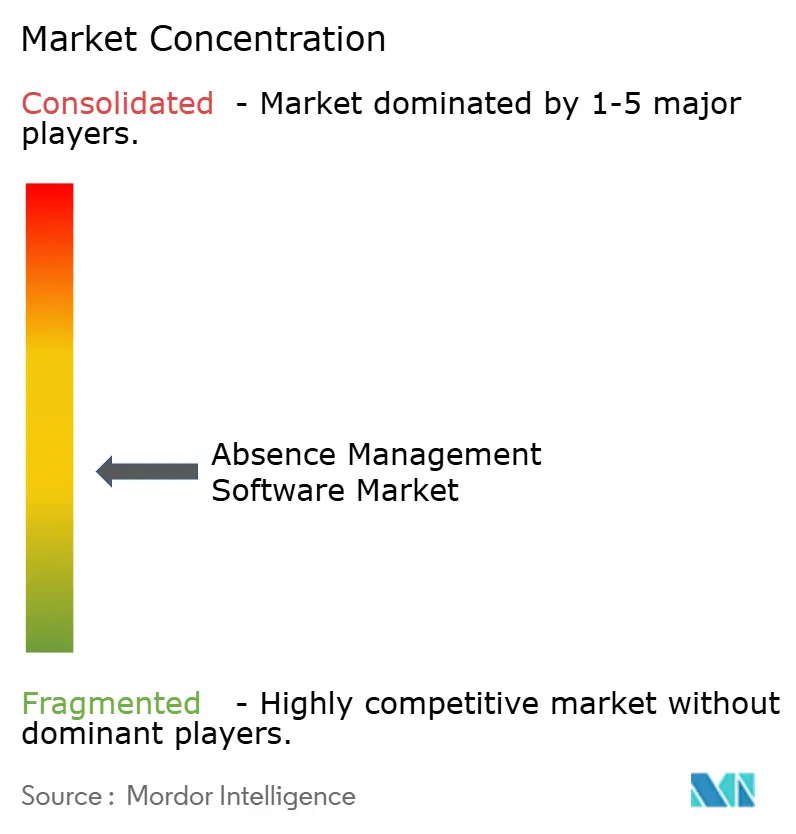

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Absence Management Software Market Analysis by Mordor Intelligence

The absence management software market was valued at USD 17.23 billion in 2025, grew to USD 18.27 billion in 2026, and is forecast to reach USD 25.99 billion by 2031, expanding at a CAGR of 7.30% during 2026-2031. Growth is being shaped by the faster spread of state-paid family and medical leave rules in the United States and by the shift of human capital management workloads toward cloud-native systems. Employers with workers across several states now face overlapping leave, accommodation, documentation, and notice requirements that manual tools do not handle well, pushing absence platforms into core HR operations. The same pressure is rising around remote work accommodations and return-to-office policies, as larger employers are seeing higher case volume and greater process risk. AI is also becoming more relevant, but new rules around employee-facing AI use are raising the cost of compliance engineering and favoring vendors with broader legal, product, and governance capacity. The result is a market where demand keeps rising, competitive pressure remains high, and mid-market consolidation becomes more likely as smaller vendors struggle to keep pace with both regulatory requirements and platform expectations.

Key Report Takeaways

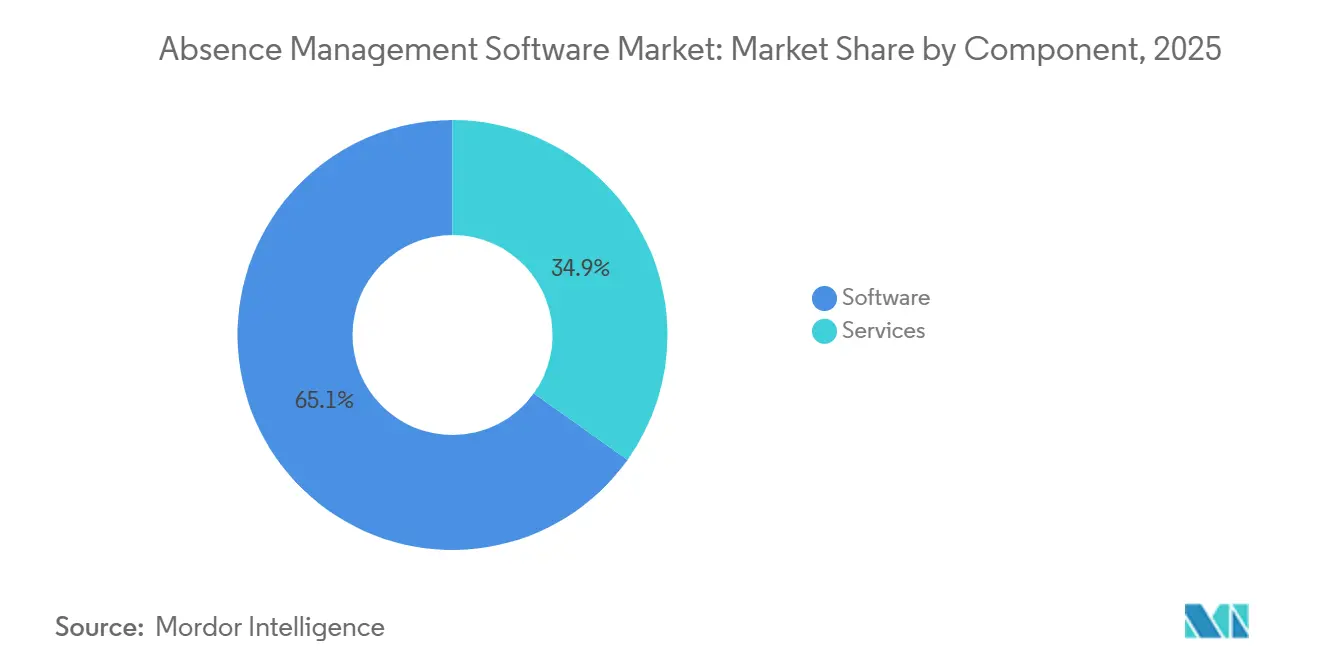

- By component, software accounted for 65.12% of the absence management software market revenue in 2025, while services are forecast to expand at a 10.11% CAGR through 2031.

- By deployment mode, cloud-based deployment held 55.24% of revenue in 2025 and is also the fastest-growing segment, advancing at a 9.53% CAGR through 2031.

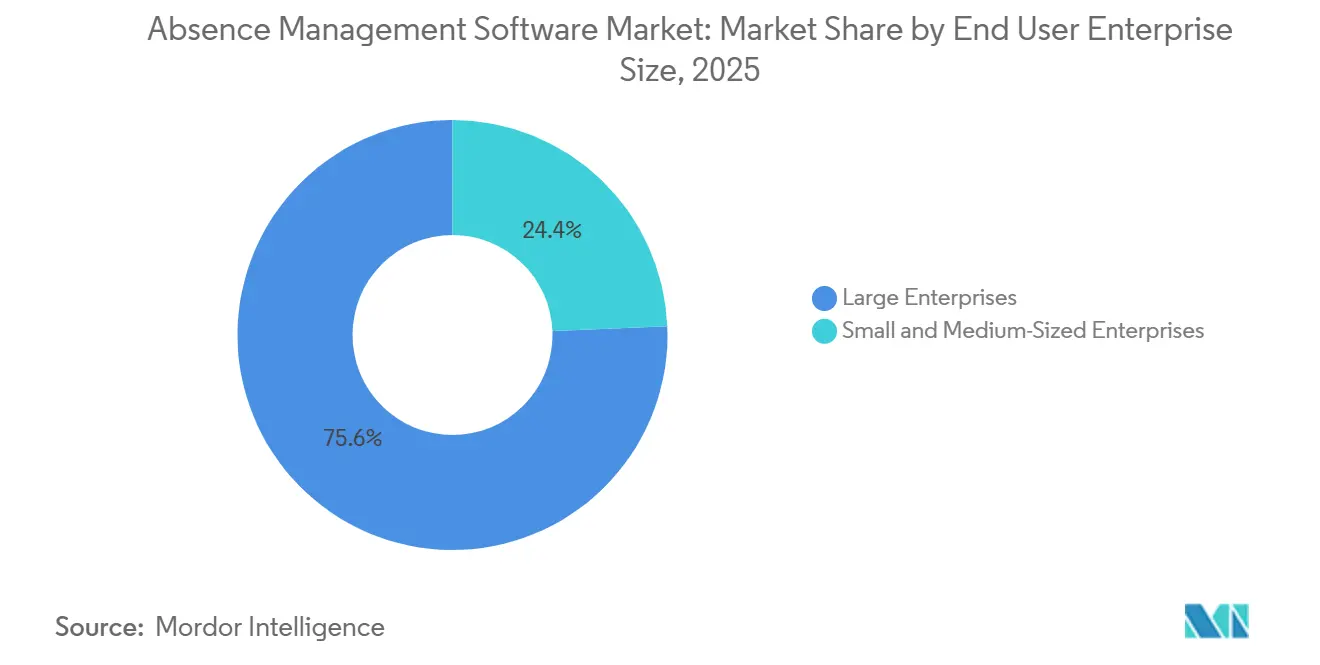

- By enterprise size, large enterprises accounted for 75.64% of revenue in 2025, while SMEs are projected to record the highest CAGR of 8.75% through 2031.

- By application, leave management accounted for 40.23% of segment revenue in 2025, while analytics and reporting are forecast to grow at a 9.81% CAGR through 2031.

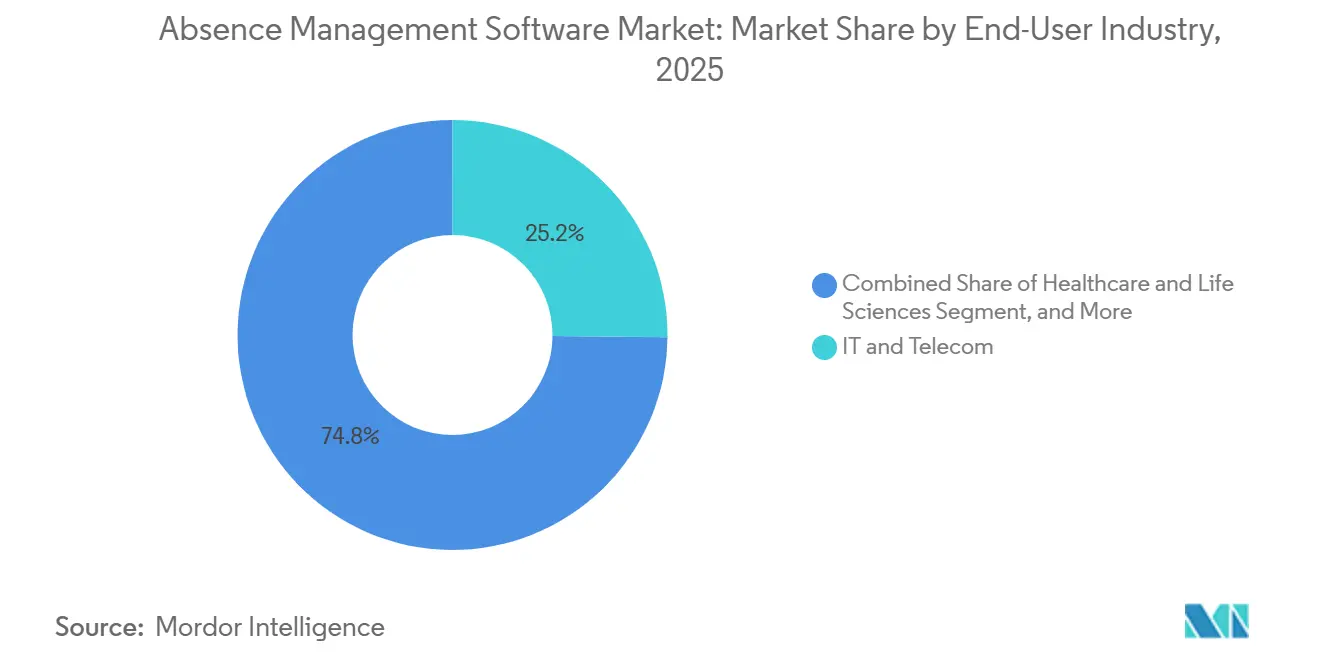

- By end-user industry, IT and telecom held 25.17% of revenue in 2025, while healthcare and life sciences are expected to expand at a 9.21% CAGR through 2031.

- By geography, North America accounted for 35.12% of global revenue in 2025, while Asia-Pacific is projected to post the fastest CAGR at 11.11% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Absence Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Multi-Jurisdiction Leave And Labor Compliance Requirements | +1.8% | North America, Europe, APAC | Short term (= 2 years) |

| Cloud-Based Human Resources Software Adoption | +1.5% | Global | Medium term (2-4 years) |

| Remote And Hybrid Workforce Policy Administration Needs | +1.2% | North America, Europe, APAC core | Medium term (2-4 years) |

| Demand For Automation, Analytics, And Employee Self-Service | +1.0% | Global | Long term (= 4 years) |

| Return-To-Office Accommodation Request Growth | +0.7% | North America, United Kingdom | Short term (= 2 years) |

| Five-Generation Workforce Complexity | +0.5% | Global | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Stricter Multi-Jurisdiction Leave And Labor Compliance Requirements

Multi-jurisdiction leave rules have shifted from an HR inconvenience to a core operating issue for employers in the absence of management software. In 2026, Delaware, Maine, Minnesota, Colorado, and New York City either launched major paid leave programs or expanded existing entitlements, bringing the total to 15 states and Washington, D.C. that already had mandatory PFML frameworks in place. The applicable rule set usually follows the employee’s physical work location, not the employer’s state of incorporation, which means each remote hire in a new state can create a new compliance requirement.[1]Nancy Gunzenhauser Popper et al., “2026 Family and Medical Leave Law Updates - What Employers in Seven States Need to Know,” The National Law Review, natlawreview.com Employers also need to administer ADA, PWFA, and state PFML obligations in parallel, and that combination creates documentation, certification, and notice steps that spreadsheet workflows do not handle consistently. In the absence of a management software market, vendors that can automatically update leave rules by location gain a clear product advantage because buyers increasingly value accuracy and speed over generic workflow coverage.

Cloud-Based Human Resources Software Adoption

Cloud adoption has evolved into a capability decision rather than a narrow cost decision, and that shift is expanding the absence management software market. ISG’s 2025 HR technology survey found that 69% of organizations already operated SaaS or hybrid cloud HR models, and 83% expected to do so by the end of 2027. The same survey showed average HR AI budgets rising to USD 1.6 million in 2026, indicating that cloud platforms are now the default base for analytics, automation, and AI-enabled workflow tools. Large HCM vendors are also embedding native absence functionality into broader suites, raising enterprise expectations for integration, reporting, and workflow continuity. That is pushing standalone vendors in the absence management software market to deepen partnerships, improve interoperability, and show clearer business value than they needed to prove in earlier buying cycles.

Remote And Hybrid Workforce Policy Administration Needs

Hybrid work has turned leave administration into a distributed compliance function, and that change continues to support the absence management software market. By 2025, 58% of firms had adopted permanent hybrid work policies, and employees were working an average of 2.6 days each week from remote locations.[2]State Paid Leave Laws Affecting Multi-State Employers,” Multi-State Employer, multistateemployer.com Because leave rules follow the employee’s work location, a workforce spread across several states can trigger multiple PFML frameworks simultaneously. NFP reported in 2025 that 70% of managers had no formal training in leading hybrid teams, leaving an execution gap that self-service tools and automated manager workflows can help close. As productivity-tracking and workforce-analytics tools spread more widely, absence data is becoming a shared operating dataset rather than a stand-alone HR record, thereby increasing the strategic role of the absence management software market.

Demand For Automation, Analytics, And Employee Self-Service

The next stage of growth in the absence management software market is tied to automation, reporting depth, and employee self-service. McKinsey found that GenAI was already in operational use across 35% of core HR processes in the United States by 2025, while time tracking and absence management represented 23% of European operational GenAI deployments. At the same time, NFP reported that only 1% of companies were using AI specifically for leave management, which shows how early this automation cycle still is. McKinsey also found that 47% of European employees were already using self-service tools for vacation requests, and high-performing organizations had reduced staffing ratios from 1 HR professional per 70 employees to 1 per 200 after automating core workflows. That combination supports vendors that can tie automation to faster case handling, better compliance records, and visible labor savings within short implementation windows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Payroll And Human Resources System Integration Complexity | -0.6% | North America, Europe | Medium term (2-4 years) |

| Sensitive Workforce Health Data Privacy Risks | -0.5% | Europe, North America | Long term (= 4 years) |

| Uncontrolled Generative Artificial Intelligence Use In Leave Decisions | -0.3% | Global | Short term (= 2 years) |

| Standalone Vendor Pricing Pressure From Bundled Human Capital Management Suites | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy Payroll And Human Resources System Integration Complexity

Integration with legacy payroll and HR systems remains one of the clearest brakes on wider adoption in the absence management software market. ISG ranked core-platform integration as the second-most-important adoption factor in its 2025 HR survey, just behind data security. NFP found that only 31% of organizations that implemented new HR technology during the previous two years reported significant efficiency gains after deployment, and integration problems were a major reason many others saw limited returns. Many large employers still run payroll on systems with proprietary data structures, so absence balances, pay calculations, and leave events do not move cleanly between old and new environments. This slows the absence management software market because buyers often need middleware, IT support, and long testing cycles before they can trust the system in live compliance workflows.[3]NFP, “2025 NFP US Leave Management and HR Trend Report,” NFP, nfp.com

Sensitive Workforce Health Data Privacy Risks

Privacy risk is a structural constraint because the absence management software market routinely handles some of the most sensitive employee records in the HR stack. These systems process diagnosis details, disability categories, behavioral health claims, and pregnancy-related documentation, which are protected under the GDPR and protected health information rules in the United States. The UK Information Commissioner’s Office updated its guidance on worker health data in March 2024, reinforcing the care required when employers and vendors process health-related information. At the same time, the EU AI Act has elevated employment-related AI use to a higher control category, raising oversight, documentation, and governance expectations for vendors serving Europe. As buyers respond, privacy-by-design architecture, clear data flow mapping, and strong audit readiness have moved from product differentiators to basic buying requirements across the absence management software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Momentum Signals A Shift Beyond Licensing

Software accounted for 65.12% of revenue in 2025, making it the largest component of the absence management software market. That position reflects enterprise demand for configurable platforms that can be adapted to complex federal, state, local, and employer-specific leave rules. Large employers have often preferred licensed systems because each compliance exception can require its own workflow logic, approval path, and documentation set. In the absence of management software, this still favors products that allow deep configuration within existing HCM and payroll environments. The result is a component mix in which software remains the core spending category, as many buyers still want direct control over policy setup and process execution.[4]Oracle Fusion Cloud Absence Management 26A What’s New,” Oracle Help Center, oracle.com

Services are forecast to expand at a 10.11% CAGR from 2026 to 2031, showing that implementation and operational support are becoming more important across the absence management software market. Buyers increasingly recognize that owning a platform does not remove the need for configuration updates, legal monitoring, employee communications, and case administration support. Each new state PFML rule creates additional setup work, making managed services and advisory support more relevant for mid-market employers with smaller HR teams. Oracle’s February 2026 Absence Management 26A update added AI agents that reference uploaded policy documents during employee leave interactions, demonstrating how product design is beginning to absorb work that once sat outside the software layer. Even so, the absence management software market still offers room for continued growth, as employers seek faster deployment, fewer compliance errors, and more support for translating policy into repeatable daily workflows.

By Deployment Mode: Cloud Consolidates Its Lead While Hybrid Gains Traction

Cloud-based deployment accounted for 55.24% of revenue in 2025, giving it the largest share of the absence management software market by deployment mode. Its lead comes from the fact that SaaS vendors can quickly push statutory rule updates when a state or city change affects eligibility, benefit design, or documentation requirements. That update speed matters more in the absence of administration than in many other HR tasks because errors can affect pay, eligibility, and legal compliance simultaneously. On-premises systems still retain a real installed base in government, defense, and parts of financial services where data residency and internal hosting rules remain strict. This keeps deployment demand mixed, but it also reinforces why buyers increasingly ask vendors to support both control and speed.

Cloud-based deployment is also the fastest-growing option, with the absence management software market size for this segment projected to expand at a 9.53% CAGR through 2031. ISG reported that 83% of organizations expected to operate cloud- or hybrid-HR models by the end of 2027, supporting continued migration toward hosted absence platforms. Hybrid models are gaining ground among mid-market and European employers that want employee portals and cloud-based analytics while keeping some sensitive health-related data under tighter internal control. That structure aligns with procurement needs in countries where buyers place strong emphasis on audit readiness, security certifications, and transparency in data handling. Across the absence management software market, vendors with mature hybrid roadmaps are therefore better placed to win enterprise contracts that require both statutory agility and more conservative data governance.

By End User Enterprise Size: Large Enterprises Anchor Revenue While SMEs Drive Growth

Large enterprises accounted for 75.64% of revenue in 2025, making them the largest segment of the absence management software market by end-user enterprise Size. Their lead reflects very large employee populations, broader geographic footprints, and heavier volumes of leave, disability, and accommodation cases. Unum found in late 2025 that large employers were 65% more likely to face a surge in remote work accommodation requests after tighter in-office requirements, which helps explain why they need more structured case management and documentation tools. Littler’s 2025 employer survey also showed stronger litigation expectations among large employers, adding another reason to standardize leave and accommodation workflows. In the absence of management software, scale does not just increase volume; it also increases legal exposure and the cost of inconsistent process handling.

SMEs are projected to grow at an 8.75% CAGR through 2031, making them the fastest-expanding enterprise-size segment in the absence management software market. Subscription pricing and lighter cloud deployments are lowering the entry barrier for employers that once relied on manual spreadsheets, email chains, or payroll add-ons. This shift matters because state PFML obligations can apply at very low employee thresholds, meaning smaller employers are now facing compliance tasks that used to be seen as an enterprise issue. Vendors are responding with simpler implementations, more guided workflows, and narrower product bundles that still handle the most common leave scenarios. That is gradually broadening the buyer base for absence management software beyond large organizations and turning smaller employers into a more meaningful growth engine.

By Application: Analytics Accelerates As Leave Management Holds The Core

Leave management accounted for 40.23% of revenue in 2025, making it the largest application in the absence management software market. That lead reflects the basic fact that employers first buy these systems to administer leave correctly, especially where FMLA, state PFML, ADA, and employer-specific policies overlap. Accurate tracking of eligibility, certification, approval timing, and return dates remains the primary operational need driving software selection. Because those workflows are mandatory, leave management continues to anchor the platform relationship even when buyers later expand into reporting or return-to-work tools. This keeps the application mix stable at the center, even while adjacent functions grow faster.

Analytics and reporting are projected to expand at a 9.81% CAGR through 2031, making it the fastest-growing application across the absence management software market. Employers are asking for more than case administration, as legal, finance, and operations teams now want absence data that shows patterns, risk indicators, and staffing impacts. Unum reported that US behavioral health absences averaged 72.6 days in 2025, underscoring the need for better visibility into duration, recurrence, and return-to-work outcomes. Littler also noted a stronger employer focus on accommodation and return-to-office issues in 2025, making reporting more relevant as a legal documentation tool rather than solely an HR dashboard. As a result, the absence management software market is moving toward a model in which analytics is part of the core product value, rather than a secondary feature added after compliance needs are met.

By End-User Industry: Healthcare Escalates While IT And Telecom Anchors Demand

IT and telecom held 25.17% of revenue in 2025, giving it the largest position in the absence management software market by end-user industry. This reflects the sector’s earlier adoption of cloud HR systems, its large and distributed workforces, and its higher tolerance for software-led process redesign. Many technology employers operate across multiple US states and international jurisdictions, so they need systems that can handle layered leave entitlements and frequent policy variation. That operating model fits well with configurable compliance engines and integrated employee self-service. It also keeps IT and telecom at the center of demand for vendors that sell complex, high-volume absence administration platforms.

Healthcare and life sciences are forecast to grow at a 9.21% CAGR through 2031, making it the fastest-rising vertical in the absence management software market. Growth here is tied to both workforce scale and the heavier operational impact of long or recurring absences, especially where shift coverage and regulated staffing levels matter. Time tracking and absence management accounted for 23% of European operational GenAI deployments in 2025, with healthcare organizations among the most active adopters of AI in workforce processes. FINEOS also stated in 2024 that its platform handled leave and disability records for 7 of the 10 largest US employee benefits insurers, underscoring how closely absence administration aligns with insurance-linked workflows across this broader customer base. The absence management software industry is also seeing support from manufacturing and frontline settings, where TeamSense reported an average absentee rate of 2.4% among platform users in 2025, below the 2.8% Bureau of Labor Statistics average cited in its benchmarking analysis.

Geography Analysis

North America held 35.12% of the absence management software market share in 2025, making it the largest regional revenue pool. The United States remains the main driver because employers often have to administer federal FMLA, state PFML rules, local paid sick leave ordinances, and ADA accommodation requirements simultaneously. In 2026, several states and localities launched or expanded paid leave programs, further complicating an already dense operating environment. The work-situs rule also matters because leave obligations usually follow the employee’s physical work location, making distributed hiring a direct compliance trigger. Canada and Mexico add regional demand through differing provincial rules and formalization trends, but the North American absence management software market still draws most of its weight from the United States.

Asia-Pacific is projected to record the fastest growth in the absence management software market size, at an 11.11% CAGR from 2026 to 2031. The regional story differs from North America because many employers in India and Southeast Asia are building digital HR systems for the first time rather than replacing older leave platforms. That creates more greenfield demand and reduces some of the integration drag seen in mature markets. Australia, Japan, South Korea, and China are also supporting the absence management software market through tighter labor compliance expectations, broader digital HR adoption, and more formal monitoring of leave and work-hour obligations.

Europe remained the third major regional cluster in 2025, led by Germany, the United Kingdom, and France. European employees missed 15% of assigned working time in 2025, equal to 37 working days per year, and France and Italy posted especially high health-related absence shares. GDPR remains a major selection factor because employee health records require stronger legal justification, tighter governance, and clearer processing controls. The region is also influenced by new reporting obligations and policy shifts that raise the value of configurable systems over rigid point tools. South America, the Middle East, and Africa remain smaller in scale, but demand is rising where labor regulation is formalizing, and employers are improving data governance standards for workforce systems.

Competitive Landscape

The absence management software market remains moderately fragmented, with specialized vendors competing alongside broader HCM suites. Pure-play providers such as AbsenceSoft, WorkForce Software, Stiira Corporation, and Qcera Inc. focus on depth of compliance, case management, and workflow flexibility. Large suite vendors compete on another front by embedding absence features within broader HR, finance, and workforce planning systems, which creates pricing pressure at the lower end of the market. This split means competition is no longer only about product features; it is also about integration reach, update speed, and the ability to support adjacent insurance and disability workflows. In the absence of a management software market, the vendors that stand out are usually those that combine strong legal rule coverage with easier deployment in larger operating ecosystems.

A clear competitive pattern is the carrier-and-platform partnership model. EIS launched AbsenceLink in April 2025 using AbsenceSoft’s compliance engine, which more directly connected leave and disability management with insurance claims workflows. FINEOS and Sutherland announced a strategic alliance in April 2025 to combine the FINEOS Absence platform with automation-led BPaaS capabilities for US employee benefit carriers. Guardian then completed its integration with FINEOS AdminSuite in March 2026 to support Guardian Absence Solutions through a single cloud-based system with automated compliance updates. These moves show that vendors are not only selling to HR teams, they are also entering carrier-led distribution channels that can lock in higher-volume demand.

The absence management software market is also being shaped by AI-enabled workflow upgrades and by financial sponsorship. Oracle introduced a Time-off Assistant AI Agent in its February 2026 Fusion Cloud update, while Paychex released a Time-Off Request Agent in the same month across its Paycor and Paychex Flex platforms. AbsenceSoft had already shown strong commercial momentum before its 2024 acquisition by Luminate Capital Partners, including revenue growth of more than 400% over the prior three years and net revenue retention above 110%. That combination of product expansion, channel partnerships, and capital backing suggests the management software market will continue consolidating around vendors that can bear both compliance engineering costs and broader platform expectations.

Absence Management Software Industry Leaders

UKG Inc.

ADP, LLC

Workday, Inc.

SAP SE

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- 2026: Guardian Life integrated FINEOS AdminSuite into Guardian Absence Solutions™, offering unified cloud-based absence and disability benefits with automated compliance updates.

- February 2026: Paychex added AI-powered time-off tools in Paycor and Flex, including an agent that checks staffing, holidays, and conflicts before recommending leave approvals.

- February 2026: Oracle’s Fusion Cloud Absence Management 26A introduced an AI Time-off Assistant for conversational leave logging and policy-based compliance referencing.

- June 2025: TeamSense released its Absenteeism Benchmarking Report, showing a 2.4% absentee rate versus 2.8% BLS average, with nearly one million weather-related missed shifts.

Global Absence Management Software Market Report Scope

The absence management software market refers to the segment of HR technology focused on automating, tracking, and managing employee leave, disability, and accommodation processes across complex regulatory frameworks. These platforms help employers comply with federal, state, and local paid leave laws and internal policies, while streamlining documentation, certifications, and case workflows. By integrating with payroll and HCM systems, absence management software reduces compliance risks, improves reporting accuracy, and enhances employee self-service. The market is driven by hybrid work, expanding PFML programs, and growing demand for automation and analytics.

The Absence Management Software Market is segmented by Component (Software and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), End User Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Application (Leave Management, Compliance Management, Disability and Return-to-Work Management, and Analytics and Reporting), End-User Industry (Information Technology and Telecom, Banking Financial Services and Insurance, Healthcare and Life Sciences, Industrial Manufacturing, Retail and E-commerce, Government and Public Sector, and Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Leave Management |

| Compliance Management |

| Disability and Return-to-Work Management |

| Analytics and Reporting |

| Information Technology (IT) and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Industrial Manufacturing |

| Retail and eCommerce |

| Government and Public Sector |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Application | Leave Management | |

| Compliance Management | ||

| Disability and Return-to-Work Management | ||

| Analytics and Reporting | ||

| By End-User Industry | Information Technology (IT) and Telecom | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Industrial Manufacturing | ||

| Retail and eCommerce | ||

| Government and Public Sector | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and future value of the absence management software market?

The absence management software market was valued at USD 17.23 billion in 2025 and is forecast to reach USD 25.99 billion by 2031, growing at a 7.30% CAGR during 2026-2031.

What is driving demand for absence management software?

The main drivers are multi-jurisdiction leave compliance, cloud HR adoption, hybrid workforce administration, and rising demand for automation, analytics, and employee self-service.

Which deployment model is growing fastest in absence management software?

Cloud-based deployment led with 55.24% of revenue in 2025 and is also the fastest-growing deployment model, with a 9.53% CAGR through 2031.

Which end user enterprise segment is creating the most growth opportunities?

Large enterprises still dominate revenue with 75.64% share in 2025, but SMEs are expanding faster at an 8.75% CAGR as subscription pricing lowers adoption barriers.

Which application area is expanding fastest?

Leave management remains the core use case with 40.23% of revenue in 2025, while analytics and reporting is growing fastest at a 9.81% CAGR through 2031.

Which region offers the strongest growth outlook?

North America remained the largest regional market in 2025 with 35.12% share, while Asia-Pacific is expected to post the fastest growth at an 11.11% CAGR through 2031.

Page last updated on: