Expense Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

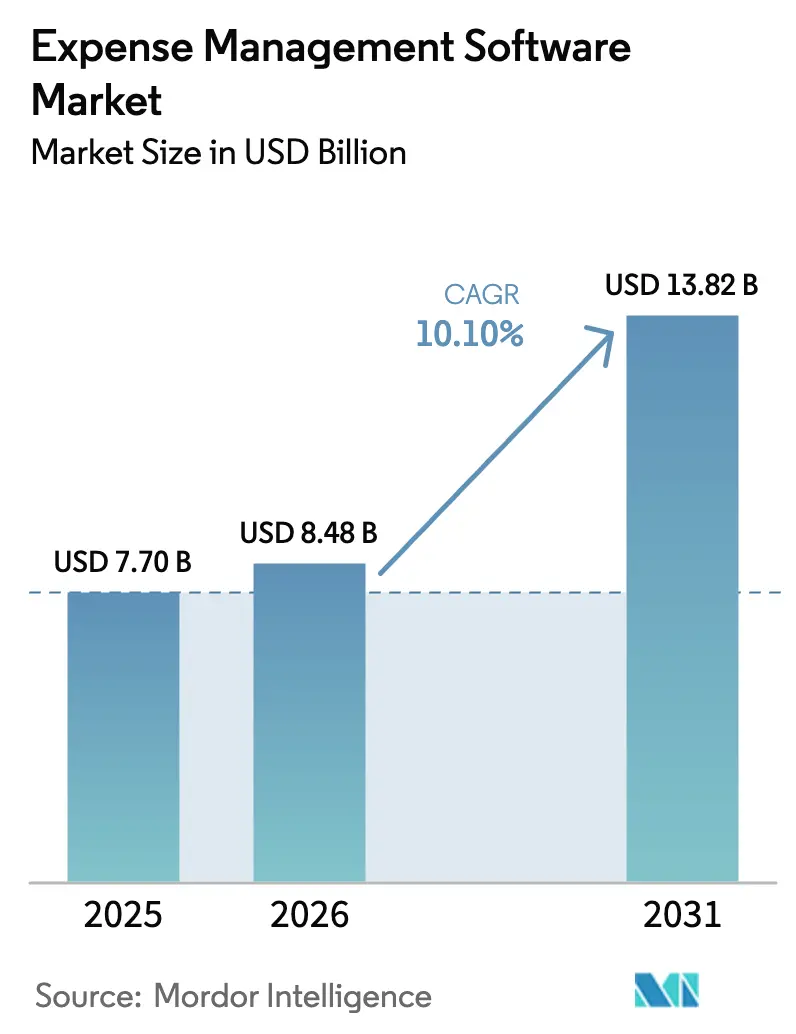

| Market Size (2026) | USD 8.48 Billion |

| Market Size (2031) | USD 13.82 Billion |

| Growth Rate (2026 - 2031) | 10.10% CAGR |

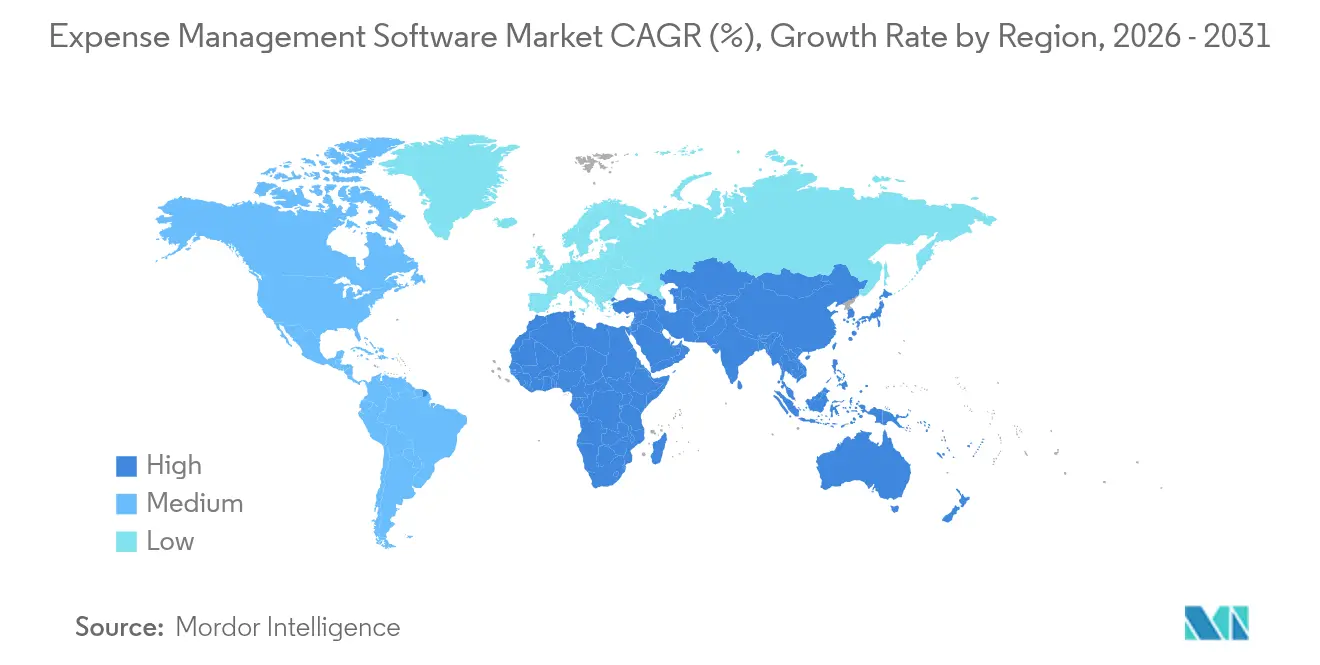

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Expense Management Software Market Analysis by Mordor Intelligence

Expense Management Software Market size in 2026 is estimated at USD 8.48 billion, growing from 2025 value of USD 7.70 billion with 2031 projections showing USD 13.82 billion, growing at 10.10% CAGR over 2026-2031.

Growth is propelled by mandatory e-invoicing rules, CFO pressure to automate finance workflows, and rapid migration from on-premises tools to cloud platforms that deliver real-time visibility over global spend. Large enterprises are scaling integrated suites that unite travel, telecom, and procurement expenses under one policy engine, while small and medium businesses (SMBs) spur innovation in intuitive user experiences and low-friction pricing. Artificial intelligence is moving beyond basic receipt capture to full-volume audit automation, enabling finance teams to review every submission rather than a small sample. Embedded-finance card programs add further momentum by streaming enriched transaction data directly into approval workflows, accelerating reimbursements and eliminating manual coding. As a result, the expense management software market continues to evolve from point solutions toward device-agnostic, compliance-ready platforms that reduce risk and administrative overhead.

Key Report Takeaways

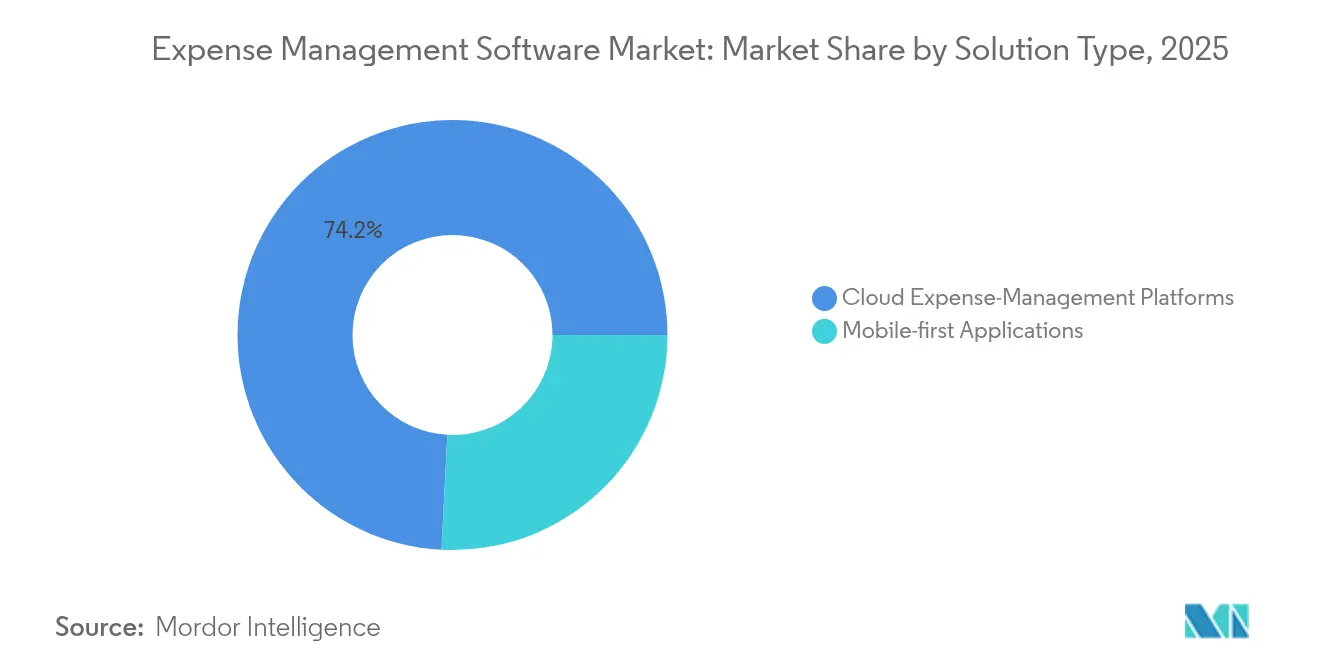

- By solution type, cloud platforms held 74.18% of the expense management software market share in 2025, while mobile-first tools are on track to register the fastest 14.8% CAGR through 2031.

- By enterprise size, the large-enterprise segment commanded 67.05% of the expense management software market size in 2025 and is expanding at a robust 13.8% CAGR to 2031.

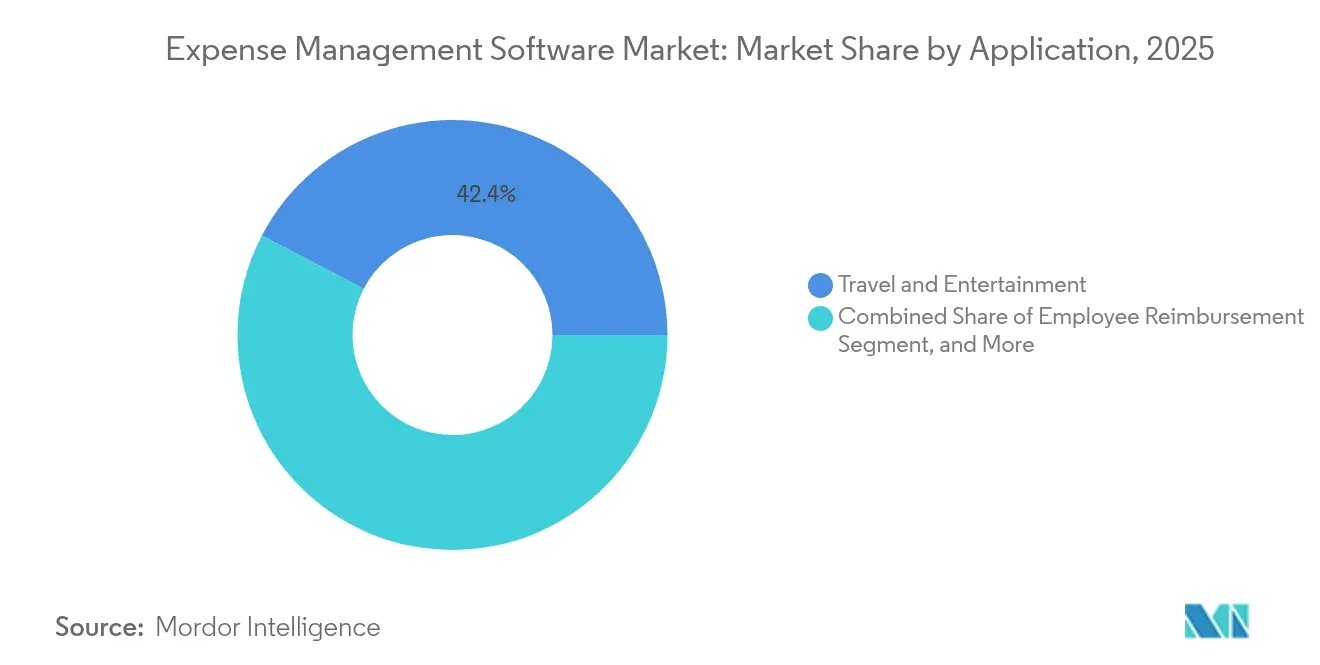

- By application, travel and entertainment solutions led with 42.35% revenue share in 2025; telecom expense management is projected to post the highest 15.4% CAGR through 2031.

- By end-use industry, banking, financial services, and insurance accounted for 29.20% adoption in 2025, whereas the IT and telecom sector is advancing at a 14.7% CAGR to 2031.

- By geography, North America retained 39.05% share in 2025; Asia-Pacific is forecast to grow the fastest at 17.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Expense Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cloud migration of finance stacks | +2.1% | Global, with early gains in North America and EU | Medium term (2-4 years) |

| Accelerating shift to mobile-first UX | +1.8% | Asia-Pacific core, spill-over to global markets | Short term (≤ 2 years) |

| Post-pandemic TandE rebound and real-time spend visibility needs | +1.5% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Mandatory e-invoicing/receipt tax rules in EU and LATAM | +1.3% | EU and LATAM, with compliance spillover globally | Long term (≥ 4 years) |

| AI-driven audit cost savings and fraud detection | +1.7% | Global, with enterprise adoption leading | Medium term (2-4 years) |

| Embedded-finance partnerships with card issuers and neobanks | +1.1% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Cloud Migration of Finance Stacks

Finance leaders are shifting from on-premises systems to multitenant cloud suites that deliver up-to-date features without disruptive upgrades. By eliminating local hardware and maintenance, enterprises cut IT operating costs by up to 40% while gaining global uptime guarantees and real-time analytics. Cloud platforms integrate natively with AI services for automatic category coding and fraud scoring, allowing finance teams to close the month 50% faster and reduce manual data entry by 43%.[1]SAP Concur, “Global Expense Insights 2024,” concur.com

Accelerating Shift to Mobile-First UX

Employees now expect to capture receipts, mileage, and approvals from the same smartphone they use outside work. Modern apps apply optical character recognition and machine-learning models to transcribe images instantly, shrinking report preparation time by 75% and triggering push alerts that keep policies front of mind.[2]Fyle, “Mobile Expense Management Benefits,” fylehq.com GPS automatically logs mileage, and offline caching supports field staff on weak connections. These consumer-grade experiences raise compliance and slash reimbursement cycles.

Post-Pandemic TandE Rebound and Real-Time Visibility

Corporate travel volumes climbed sharply in 2024 and 2025, and finance teams demand end-to-end insight from booking through reimbursement to keep budgets on track. Integrated travel and expense suites pull itinerary data into pre-trip approvals, enforce negotiated hotel rates, and surface exceptions instantly for manager review. Continuous monitoring helps companies balance duty-of-care obligations with cost containment as airfares and lodging rates fluctuate.

AI-Driven Audit Cost Savings and Fraud Detection

Machine-learning engines now screen 100% of submissions for duplicate claims, weekend anomalies, and out-of-policy vendors, replacing manual sampling that covered only 10-15%. Organizations deploying AI auditing report 3-5% direct savings on total spend and an 80% cut in review time.[3]AppZen, “AI Audit Benefits 2024,” appzen.com As algorithms learn from historical data, false positives fall and high-risk transactions surface swiftly for human follow-up.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating data-sovereignty/privacy compliance costs | -1.4% | EU and Asia-Pacific, with global regulatory spillover | Long term (≥ 4 years) |

| Persistent user-adoption fatigue in legacy ERPs | -1.2% | Global, with concentration in established enterprises | Medium term (2-4 years) |

| Saturation of SMB freemium tools driving price compression | -0.8% | North America and EU, expanding globally | Short term (≤ 2 years) |

| Integration complexity with multi-country payroll systems | -0.9% | Global, with acute challenges in Asia-Pacific and LATAM | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Data-Sovereignty and Privacy Compliance Costs

GDPR and similar laws require data to stay within regional borders or be pseudonymized, compelling vendors to spin up localized data centers and encryption regimes. Monthly outlays for privacy platforms add USD 827 to USD 2,275, and periodic audits inflate the total cost of ownership for smaller suppliers. Continuous rule changes across Germany, India, and Singapore force IT departments into costly upgrades and sophisticated access-control mapping.

Persistent User-Adoption Fatigue in Legacy ERPs

Employees resist systems that force multiple clicks, jargon-laden menus, and VPN access. Where integrations bolt modern tools onto legacy payroll engines, approval queues slow and data fields misalign, reducing completion rates and prolonging reimbursements. Firms report that when submission steps exceed three, compliance drops sharply, leaving finance teams with missing receipts and manual accrual work.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Cloud Platforms Dominate Yet Mobile Momentum Builds

Cloud suites captured 74.18% of 2025 revenue, underscoring enterprise trust in scalable, policy-rich environments that consolidate global workflows and offer advanced analytics. This segment anchors the expense management software market and sets the functional baseline for security certifications, multicurrency settlement, and role-based access controls. Vendors package connectors to ERP, HR, and tax engines so that data flows without rekeying. Cloud deployments also encourage rapid proof-of-concept rollouts that demonstrate value in weeks rather than quarters, supporting aggressive CFO automation roadmaps. Consequently, the expense management software market continues to steer IT budgets toward SaaS subscriptions rather than perpetuating license upgrades and local server refreshes.

Mobile-first products, while holding a smaller share, are expanding at a 14.8% CAGR. Their success stems from leveraging smartphone cameras and sensors to eliminate paper, reduce time between spend and submission, and deliver contextual prompts such as per-diem limits based on location. These apps appeal strongly to sales, field service, and gig economy workers who seldom open laptops. Leading providers are merging codebases so that mobile experiences mirror desktop dashboards, creating hybrid offerings that blur category lines. Over the forecast horizon, the expense management software market is expected to see cloud vendors embed progressive web applications and offline capabilities, ensuring device-agnostic access without sacrificing security or functionality.

By End-User Enterprise Size: Large Companies Extend Leadership While SMEs Influence Design

Large enterprises controlled 67.05% of global revenue in 2025 and are projected to grow at 13.8% CAGR. Their outsize impact on the expense management software market stems from complex approval hierarchies, multicountry tax exposure, and pressure to centralize data for external audit readiness. Investments focus on unifying disparate travel, procurement, and telecom modules under one policy framework to uncover duplicate spend and secure volume-based discounts. Portfolio rationalization also drives upgrades, as CFOs retire custom scripts and aging on-premises servers in favor of single sign-on cloud suites that promise consistent controls.

SMBs, while accounting for the rest of the expense management software market size, punch above their weight in shaping product roadmaps. Freemium tiers and USD 5 per user plans popularized by new-age vendors lower adoption barriers and teach the broader market that implementation should finish in days rather than months. Simpler onboarding, wizard-driven configurations, and chatbot guidance pioneered in the SME arena increasingly appear in enterprise editions. The dialogue between both segments ensures that future releases balance depth of controls with consumer-grade ease, reinforcing the inclusive direction of the expense management software market.

By Application: Travel and Entertainment Still Leads Yet Telecom Advances Fast

Travel and entertainment tools remained the largest application, accounting for 42.35% of spending in 2025, as companies resumed client meetings and conferences. Policy engines tie negotiated airline contracts and hotel caps to pre-trip approvals, contributing to disciplined budget recovery. Real-time feeds from global distribution systems allow finance departments to compare booked versus actual costs instantly, elevating governance across borderless itineraries.

Telecom expense management is the fastest-growing niche at a 15.4% CAGR, mirroring the surge in remote collaboration subscriptions, mobile data plans, and device stipends. TEM platforms ingest carrier invoices, detect billing errors, and recommend tariff optimizations, preserving working-capital in thin-margin industries. Over time, enterprises are likely to adopt unified spend dashboards that juxtapose TandE, TEM, and SaaS licensing so budget owners weigh trade-offs holistically. This convergence will further deepen platform stickiness within the expense management software market.

By End-Use Industry: BFSI Holds the Crown as IT and Telecom Accelerate

Banks, insurers, and capital-market firms represented 29.20% of 2025 deployments, reflecting strict audit trails and regulatory mandates. Features such as segregation-of-duties checks and automated retention schedules mitigate compliance risk. Fraud analytics also resonate in environments handling confidential customer funds.

The IT and telecom sector is posting the quickest 14.7% CAGR because distributed engineering teams rack up project expenses across cloud services, development licenses, and third-party gig talent. Automated tagging by cost center, sprint, or client contract delivers granular insight to program managers and enables timely cross-charges. Healthcare, retail, and government verticals likewise increase software uptake to satisfy sector-specific documentation requirements, signaling that the expense management software industry is diversifying its revenue base beyond white-collar travel.

Geography Analysis

North America retained 39.05% of 2025 turnover thanks to early cloud adoption, mature corporate card penetration, and Sarbanes-Oxley-driven audit rigor. Continuous innovation from established vendors headquartered in the United States sustains demand for AI modules and embedded-payment rails. Canadian enterprises follow similar trajectories as they modernize finance back-office stacks in response to digitized tax reporting mandates.

Asia-Pacific is the most dynamic region, advancing at 17.1% CAGR through 2031. Government-imposed e-invoicing frameworks in India, Indonesia, and China push even micro-enterprises to digitize receipts, creating a rising tide across the expense management software market. Smartphone ubiquity and the dominance of super-apps foster employee expectations for mobile expense functionality, accelerating adoption by first-time users.

Europe follows closely as Germany rolls out mandatory structured e-invoices in 2025 ahead of the EU-wide ViDA initiative scheduled for 2028. Latin America expands steadily on the back of electronic fiscal document rules first pioneered in Brazil and Mexico, while the Middle East and Africa open new greenfield opportunities tied to economic diversification programs.

Competitive Landscape

The market shows moderate consolidation. SAP Concur alone captured 49.6% of travel and expense revenue in 2024, leveraging decade-long integrations with enterprise resource planning systems and global tax engines. Coupa, Oracle NetSuite, and Workday position full spend-management suites that bundle procure-to-pay, supplier risk, and expense modules for unified insights. Meanwhile, challenger brands Brex, Ramp, and Navan differentiate through corporate cards that issue virtual numbers instantly, feeding enriched metadata back into automated reconciliation workflows.

Strategic partnerships shape competitive trajectories. American Express, Mastercard, and Visa embed APIs that let software vendors push authorization rules at the point of swipe, ensuring policy compliance before expenses hit general ledgers. Acquisitions accelerate feature breadth: AccountsIQ bought ExpenseIn in 2025 to deliver an end-to-end mid-market finance suite, while Visma added Rindegastos and Mobilexpense to deepen its European and Latin American footprint. Heavy RandD spending on machine learning, large-language-model chatbots, and continuous compliance updates remains a key differentiator as customers prioritize vendors that future-proof their finance architectures.

White-space opportunities persist in industry-specific packages. Healthcare entities seek HIPAA-aligned receipt storage, public-sector bodies require grant code allocation, and non-profits need donor reporting workflows. Vendors able to pre-configure such templates while maintaining horizontal scalability stand to capture incremental wallet share. As these dynamics unfold, the expense management software market is expected to witness ongoing consolidation tempered by specialized entrants targeting niche pain points.

Expense Management Software Industry Leaders

SAP Concur Technologies

Coupa Software Incorporated

Expensify, Inc.

Zoho Corporation

Oracle (NetSuite | ER-P Expense)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Visma acquired Rindegastos, bringing AI-enhanced expense tools to more than 4,500 businesses in Chile and surrounding markets.

- April 2025: Expensify introduced a simplified USD 5 per member monthly plan aimed at SMBs, bundling expense tracking, corporate cards, travel booking, and team chat.

- January 2025: AccountsIQ acquired ExpenseIn to broaden its finance platform and now supports 175,000 users across 40 countries.

- November 2024: Visma acquired Mobilexpense, adding over 2,000 European clients and strengthening its presence in unified spend management.

Global Expense Management Software Market Report Scope

Expense management software streamlines the process of tracking, reporting, and managing business expenses, offering automated tools for real-time visibility and control over spending. It is widely adopted across industries to reduce administrative burdens, enhance compliance, and provide analytics-driven insights for better financial decision-making. The market is evolving rapidly with cloud-based and mobile-first solutions enabling greater accessibility and integration with existing financial systems.

Expense Management Software Market is Segmented by Solution Type (Mobile-First Applications and Cloud Expense-Management Platforms), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Application (Travel and Entertainment Management, Employee Reimbursement, and More), End-Use Industry (IT and Telecom, BFSI, Healthcare, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Mobile-first Applications |

| Cloud Expense-Management Platforms |

| Large Enterprises |

| Small and Medium Enterprises (SME) |

| Travel and Entertainment Management |

| Employee Reimbursement |

| Procurement and Vendor Spend |

| Telecom Expense Management (TEM) |

| Project and Grant Management |

| IT and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Solution Type | Mobile-first Applications | ||

| Cloud Expense-Management Platforms | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SME) | |||

| By Application | Travel and Entertainment Management | ||

| Employee Reimbursement | |||

| Procurement and Vendor Spend | |||

| Telecom Expense Management (TEM) | |||

| Project and Grant Management | |||

| By End-use Industry | IT and Telecom | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Government and Public Sector | |||

| Other End-use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the expense management software market?

The expense management software market size is USD 8.48 billion in 2026.

How fast will the market grow over the next five years? I

T is projected to register a 10.10% CAGR, reaching USD 13.82 billion by 2031.

Which segment is expanding the quickest?

Telecom expense management is forecast to grow at 15.4% CAGR, the fastest among application categories.

Why are cloud platforms so dominant?

Enterprises prefer cloud suites because they lower IT operating costs, enable rapid feature releases, and integrate easily with AI services for real-time policy enforcement.

Which region offers the strongest growth opportunity?

Asia-Pacific has the highest projected CAGR of 17.1% through 2031, driven by e-invoicing regulations and widespread mobile adoption.

Page last updated on: