Recruitment Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

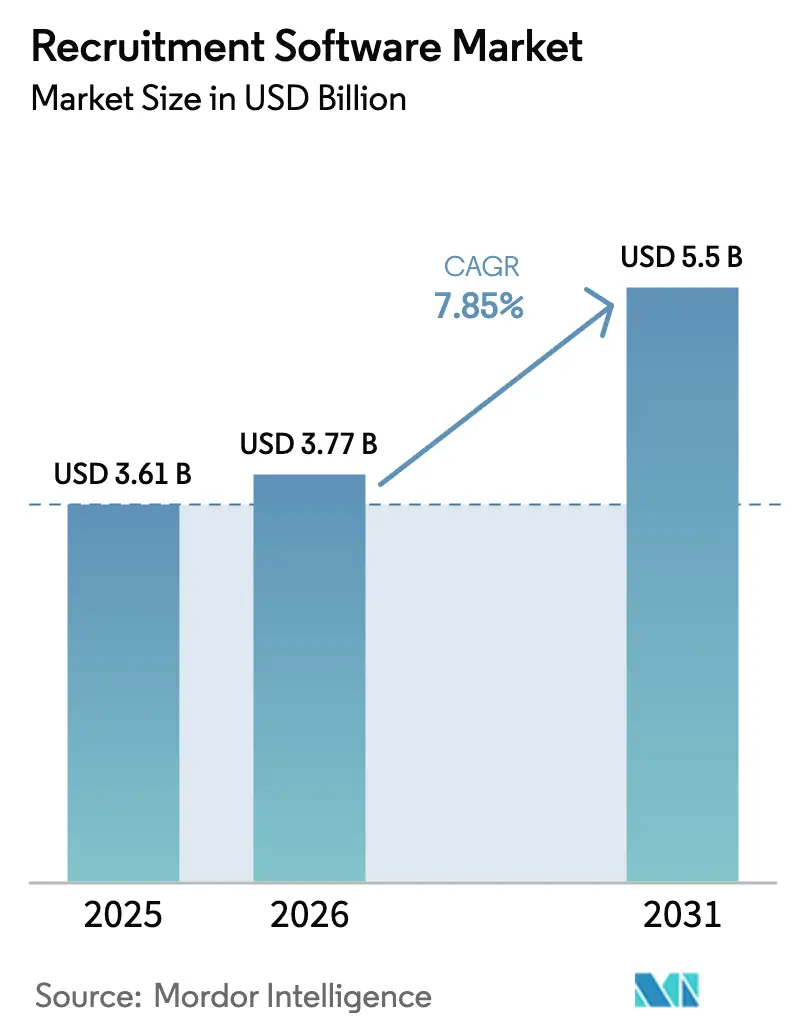

| Market Size (2026) | USD 3.77 Billion |

| Market Size (2031) | USD 5.5 Billion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

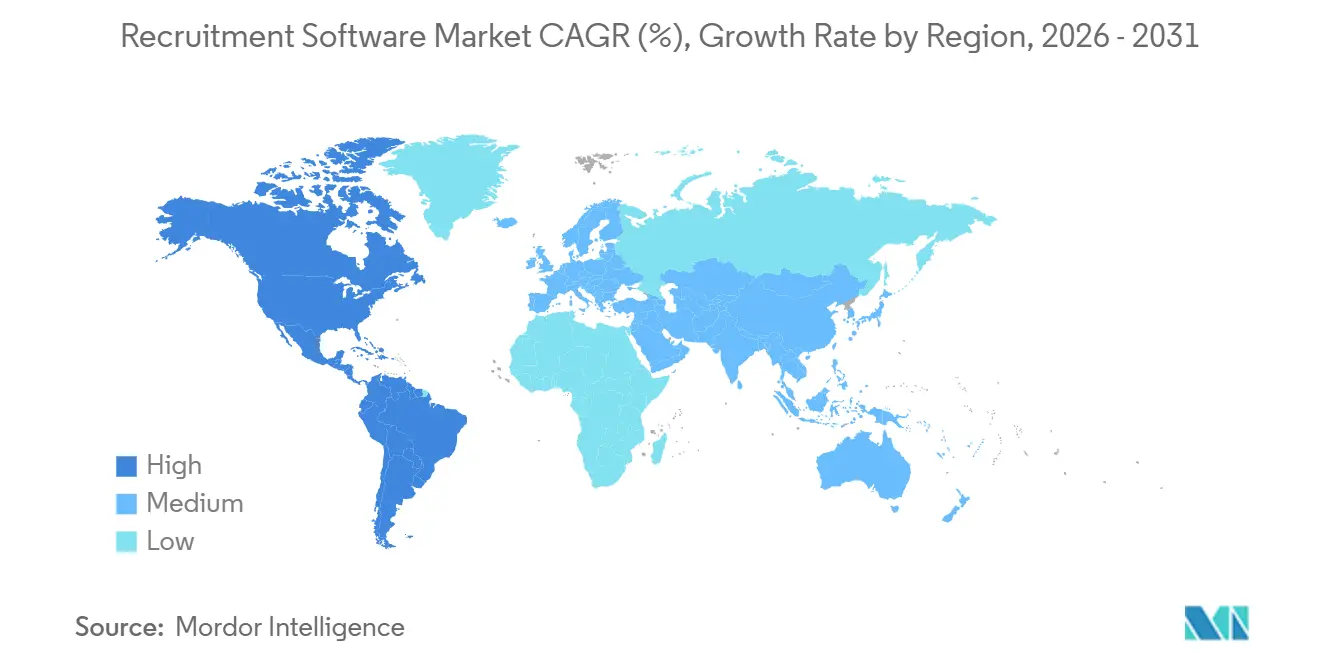

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

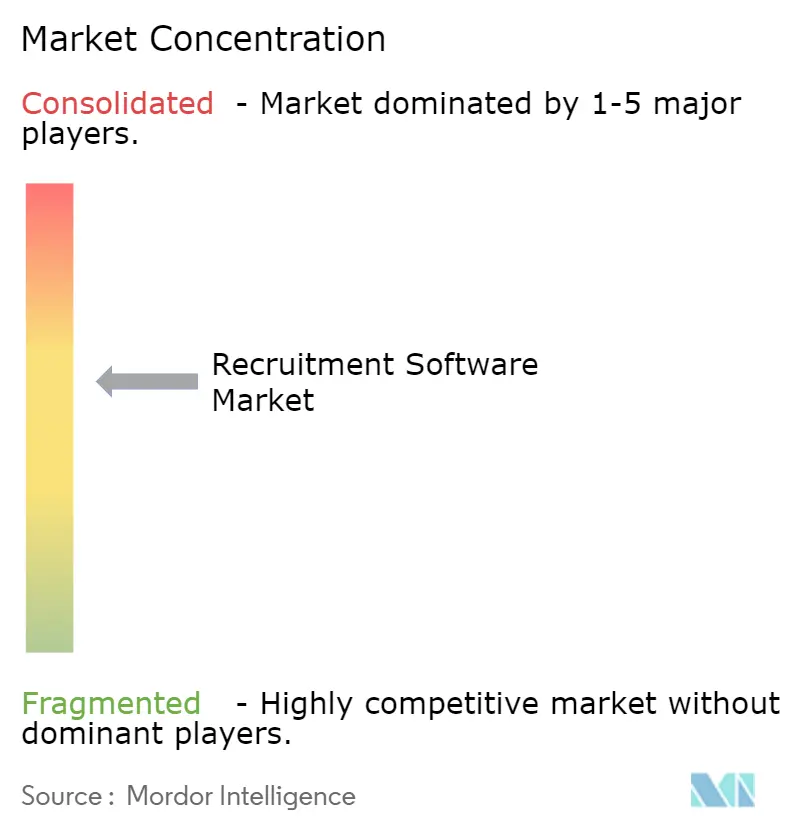

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recruitment Software Market Analysis by Mordor Intelligence

The Recruitment Software Market size is projected to expand from USD 3.61 billion in 2025 and USD 3.77 billion in 2026 to USD 5.5 billion by 2031, registering a CAGR of 7.85% between 2026 to 2031. Cloud deployment already anchors nearly seven-tenths of spending, and its elastic compute supports generative-AI copilots that shorten hiring cycles. Buyers also prioritize integrated suites that connect sourcing, engagement, assessment, and onboarding, replacing legacy point tools. Healthcare providers are modernizing fastest because clinician shortages demand accelerated credential checks, while Asia-Pacific enterprises widen addressable demand as they formalize talent pipelines. Vendors that embed explainable AI, bias mitigation, and pre-built connectors for major HRIS platforms command premium pricing.

Key Report Takeaways

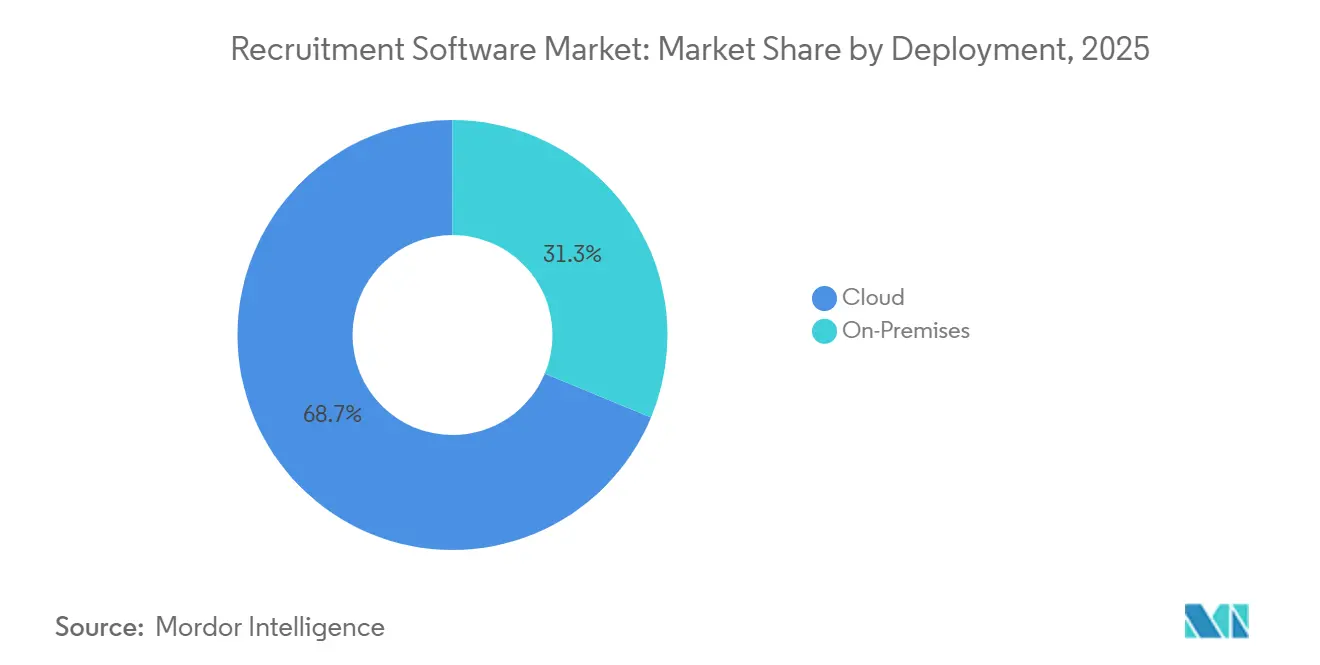

- By deployment, the cloud segment captured 68.73% of recruitment software market share in 2025 and is on track to grow at a 9.21% CAGR through 2031.

- By organization size, large enterprises held 60.95% of spending in 2025, whereas SMEs are forecast to rise at a 10.23% CAGR through 2031.

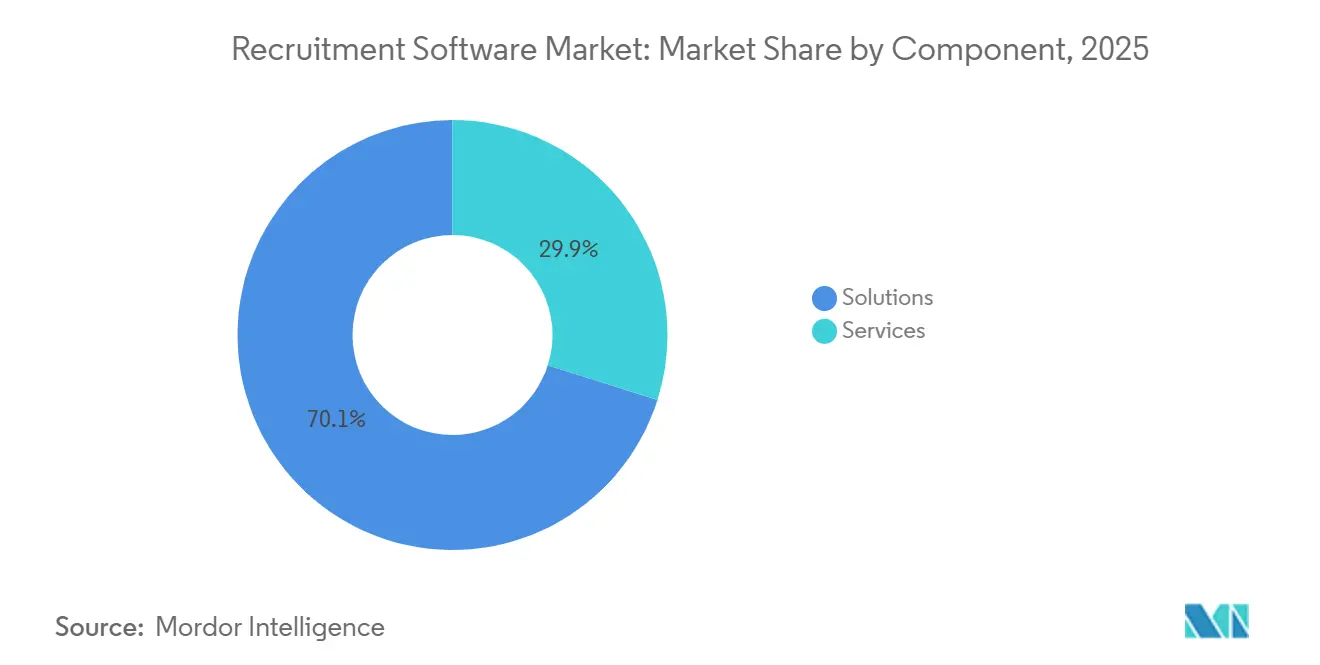

- By component, solutions represented 70.11% of 2025 revenue, yet services are expanding at an 8.74% CAGR on the back of bias-audit and integration projects.

- By functionality, applicant-tracking systems retained 53.87% share in 2025, while talent-analytics tools are climbing at a 9.82% CAGR.

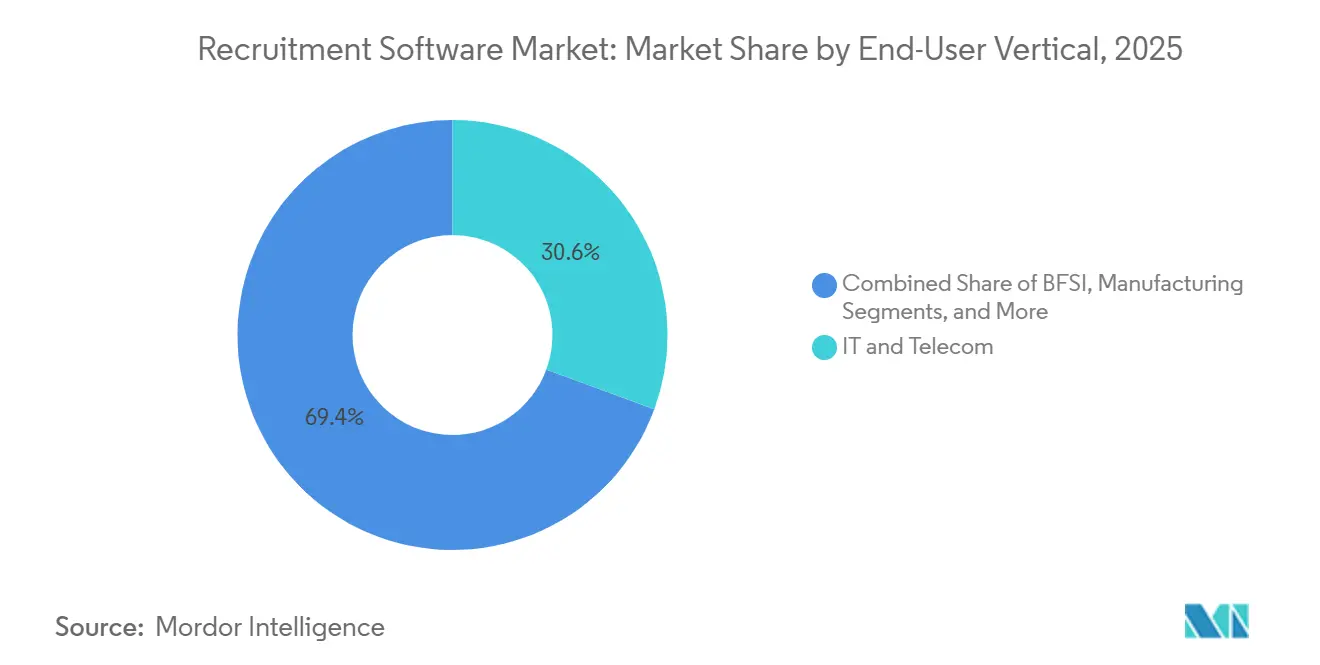

- By end-user vertical, IT and Telecom led with 30.62% revenue share in 2025; healthcare and life sciences are advancing at an 8.05% CAGR to 2031.

- By geography, North America commanded 34.62% of 2025 revenue, but Asia-Pacific is projected to expand at a 10.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recruitment Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first adoption across HR tech stacks | +1.8% | Global, with North America and Europe leading enterprise migrations | Medium term (2-4 years) |

| Explosion of AI/ML use-cases in talent acquisition workflows | +2.1% | Global, concentrated in North America, Europe, and Asia Pacific IT hubs | Short term (≤ 2 years) |

| Surge in remote and hybrid hiring models post COVID-19 | +1.2% | Global, with Asia Pacific and Latin America seeing accelerated adoption | Medium term (2-4 years) |

| Growth of social-media recruiting and employer-branding platforms | +0.9% | North America and Europe mature markets; Asia Pacific and Middle East emerging | Long term (≥ 4 years) |

| Emergence of autonomous agentic ATS with generative-AI copilots | +1.6% | North America and Europe early adopters; Asia Pacific following | Short term (≤ 2 years) |

| VC funding shift toward skills-graph and bias-mitigation analytics | +0.7% | North America venture capital concentration; spillover to Europe and Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Adoption Across HR Tech Stacks

Enterprises are decommissioning on-premises Applicant Tracking Systems in favor of unified SaaS suites that cut ownership costs and remove data silos. Oracle’s 2025 release of autonomous recruiting agents inside Fusion Cloud HCM shows how multi-tenant platforms now automate screening, interview scheduling and offer letters from one interface. Vendors pool anonymized hiring data to train matching algorithms, boosting fill-rate accuracy. Although broadband gaps slow adoption in parts of Latin America and Africa, sovereign-cloud offers and edge compute are narrowing residency barriers. The trend raises integration demand from the recruitment software market vendors, as firms connect cloud recruiting to payroll and performance modules for a single worker record.

Explosion of AI and ML Use-Cases

AI has shifted from pilot scope to enterprise staple. LinkedIn’s live listings feed 134 million vacancies into models that optimize ad spend and predict candidate success. Generative copilots from iCIMS and Workday draft outreach, create interview questions and summarize feedback in seconds, trimming cycle time by up to half. Regulators, however, now treat automated hiring as high risk. The EU AI Act obliges explainability dashboards and conformity assessments, steering buyers to vendors with built-in bias detection.[1]European Union, “Artificial Intelligence Act,” artificialintelligenceact.eu Platforms that deliver transparent scoring alongside predictive insights gain a compliance edge in the recruitment software market.

Surge in Remote and Hybrid Hiring Models Post COVID-19

Global employers rely on asynchronous video interviews and digital onboarding to source talent beyond headquarters. ManpowerGroup’s fourth-quarter 2025 survey recorded a +40% net employment outlook in India and +34% in China, with remote hiring prominent across IT roles. Tools such as HireVue cut hiring time from six weeks to six days for healthcare systems by automating screening and scheduling.[2]HireVue, “AI-Driven Video Interview Platform,” hirevue.com Yet dispersed workforces add identity-verification and tax-compliance complexity. Vendors now embed geo-fencing, blockchain credential checks and multi-jurisdiction alerting to ensure lawful onboarding.

Emergence of Autonomous Agentic ATS with Generative-AI Copilots

Agentic AI executes multi-step recruiting workflows without human prompts. Workday’s USD 1 billion purchase of Paradox in August 2025 underscores C-suite appetite for conversational agents that answer candidate questions and arrange interviews. Fountain applies similar logic to hourly roles, slashing recruiter workload by 60% in retail and logistics. Regulators still insist on human oversight when an algorithm declines an applicant, so vendors engineer tiered autonomy that automates routine gestures while reserving final approval for people managers.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and algorithmic-bias compliance costs | -1.3% | Europe (GDPR, EU AI Act), North America (CCPA, NYC Local Law 144), global spillover | Short term (≤ 2 years) |

| Integration complexity with ageing HRIS/ERP landscapes | -0.9% | Global, concentrated in large enterprises with legacy SAP, Oracle, and Workday deployments | Medium term (2-4 years) |

| SME price-sensitivity and low ATS awareness in emerging markets | -0.6% | Asia Pacific (India, Southeast Asia), Latin America, Africa | Long term (≥ 4 years) |

| Growing buyer fatigue from overlapping point solutions | -0.4% | North America and Europe mature markets with high vendor density | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Algorithmic-Bias Compliance Costs

The EU AI Act, GDPR Article 22 and New York City Local Law 144 demand bias audits, risk logs and human review, adding USD 0.5–2 million per enterprise rollout. Penalties climb to 7% of global turnover for non-compliance, a threat that redirects budgets from innovation to legal overhead. Large vendors can amortize these costs, while mid-tier suppliers face margin pressure or forced consolidation. Clients therefore gravitate toward providers that certify models and publish continual audit summaries.

Integration Complexity with Ageing HRIS/ERP Landscapes

Many employers still run payroll and core HR on 15-year-old on-premises systems that lack APIs. Recruitment platforms must build brittle custom connectors, delaying deployments and inflating service fees. Middleware from MuleSoft or Dell Boomi eases some friction but introduces new licenses and latency. As a result, mid-market firms delay upgrades, and large enterprises limit feature adoption to avoid data-sync errors. Vendors in the recruitment software market that ship pre-built adapters for SAP SuccessFactors, Oracle HCM and ADP gain significant competitive leverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Accelerates with Agentic AI

Cloud deployments accounted for 68.73% of 2025 revenue, and that slice is growing faster than the overall recruitment software market at a 9.21% CAGR to 2031. This leadership stems from instant scalability and continuous feature drops, including GPU-intensive large language model inference that on-premises servers cannot afford. Oracle’s October 2025 cloud agents illustrate the edge, drawing lessons from anonymized cross-client data to recommend shortlists automatically. On-premises systems remain in sectors such as defense and banking that impose data-sovereignty mandates, but hybrid architectures now let sourcing and engagement modules reside in cloud while candidate records stay behind the firewall. As sovereign-cloud programs mature, even regulated buyers are expected to migrate analytics workloads, narrowing the deployment divide.

The recruitment software market size for cloud deployments is forecast to add USD 1.3 billion by 2031, while on-premises revenue stays nearly flat. Vendors embed cost calculators that prove total ownership savings within 18 months, convincing finance teams to shift budgets from capital expenditure to operating expenditure. This transition unlocks recurring revenue streams and positions providers to cross-sell analytics and learning modules once the core ATS is live. Buyers that embrace full-cloud stacks also gain faster regulatory updates, an advantage as bias-audit mandates evolve yearly.

By Organization Size: SMEs Drive Volume Growth Despite Budget Constraints

Large enterprises still bring 60.95% of 2025 revenue in the recruitment software market, thanks to global head-counts that justify premium contracts. Yet, SME demand represents the fastest-growing cohort; the segment is forecast to post a 10.23% CAGR by 2031, as modular, seat-based pricing lowers the entry barrier. Freemium packages from BambooHR and Recruitee start at around USD 50 per user per month, allowing 10-person startups to access AI ranking and automated outreach typically reserved for Fortune 500 HR teams.

Awareness remains low in emerging economies where spreadsheets still track applicants, so vendors localize mobile-first interfaces and partner with regional payroll companies to bundle recruitment features. The recruitment software market share among SMEs is expected to tick up from 39% in 2025 to 45% by 2031. To capture that lift, suppliers streamline onboarding with click-and-connect job-board integrations, minimizing IT dependence for resource-constrained businesses.

By Component: Services Surge as Compliance and Integration Complexity Escalate

Solutions commanded 70.11% of 2025 spending, but professional and managed services revenue is growing at an 8.74% CAGR because buyers need external support for bias audits and legacy integrations. The recruitment software market size tied to services exceeded USD 1 billion in 2026 and is projected to nearly double by 2031. Providers package fixed-fee conformity-assessment bundles that document data lineage, risk logs and human-override workflows required under the EU AI Act.

Managed-services contracts also rise as mid-market clients outsource talent-pipeline execution entirely. Outcome-based pricing promises set reductions in time-to-fill, shifting risk to vendors but elevating switching costs. Software-only challengers must either form alliances with large integrators or build in-house consulting arms, a strategic fork that favors capital-rich incumbents.

By Functionality: Talent Analytics Overtakes Traditional ATS as Strategic Priority

Applicant-tracking systems held 53.87% share in 2025, yet demand is tilting rapidly toward predictive insights. Talent-analytics tools are forecast to outpace every other segment with a 9.82% CAGR, fueled by skills graphs that map more than one billion career paths and surface internal and external candidates. Eightfold AI’s platform demonstrates how analytics now drive requisition decisions, rather than just reporting hires.

Suites bundle CRM, onboarding and assessment to knit continuous journeys, converting recruitment software industry talk from transaction processing to talent intelligence. As scrutiny of bias rises, assessment vendors are embedding AI proctoring and fairness metrics. Greenhouse’s Real Talent engine, launched in September 2025, integrates those analytics straight into the core workflow to defend ATS incumbency.[3]Greenhouse, “Real Talent Candidate Discovery,” greenhouse.com The recruitment software market size attributable to analytics, therefore, carries the highest margin profile, encouraging intense investment.

By End-User Vertical: Healthcare Leads Growth Amid Structural Labor Shortages

IT and Telecom captured 30.62% of 2025 revenue, but healthcare and life sciences post the fastest trajectory at an 8.05% CAGR. U.S. nurse vacancies topping 200,000 in 2025 forced hospital chains to adopt automated license verification and shift-preference matching. Vivian Health’s AI assistant launched in October 2025 cut average nurse hire times from 66 days to 45 days.

Specialist platforms now bundle credential tracking and Joint Commission compliance to address sector-specific pain points, giving them defensible advantages over horizontal suites. Manufacturing and retail embrace mobile-first, high-volume hiring engines such as Fountain, which automates SMS-based workflows that scale to thousands of hourly applicants. As industry regulations tighten, vertical expertise becomes a key differentiator in vendor selection.

Geography Analysis

North America generated 34.62% of 2025 revenue, reflecting deep HR-tech penetration, high IT budgets and strict equal-opportunity enforcement. Major incumbents like Workday, Oracle and SAP maintain headquarters or significant operations in the region, shortening feedback loops for product iterations. Consolidation is high, as Paychex acquired Paycor in January 2025 to bolster distribution among mid-size employers.[4]Paychex, “Paychex to Acquire Paycor,” paychex.com Growth, however, decelerates relative to emerging regions because most large enterprises already run modern ATS suites.

Asia-Pacific is the fastest-growing region at a 10.66% CAGR through 2031. India’s IT-services giants hire hundreds of thousands of graduates each year, demanding platforms that screen millions of résumés. China’s state-owned enterprises favor domestic vendors for data sovereignty, but foreign multinationals standardize on global suites with localized Mandarin interfaces. Japan and South Korea retain referral-centric norms, yet aging demographics compel digital hiring to widen talent pools. Southeast Asian markets, notably Indonesia and Vietnam, represent white space; smartphone penetration exceeds desktop usage, so lightweight, app-centric recruiting tools gain traction.

Europe sits between these dynamics. GDPR and the EU AI Act raise compliance complexity, but free movement within the European Union expands candidate pools, prompting employers to implement bias-monitored sourcing. Germany’s mid-sized manufacturers face skilled-trade shortages, and the United Kingdom’s post-Brexit labor squeeze fuels adoption. The Middle East and Africa remain nascent; Saudi Arabia’s Vision 2030 infrastructure projects elevate formal hiring systems, while South Africa and Nigeria show early mobile-first uptake. Latin America’s cloud demand clusters in Brazil and Argentina but is tempered by currency volatility that shrinks import budgets for subscription software.

Competitive Landscape

Roughly 45-50% of global revenue of the recruitment software market is concentrated among the top 10 vendors, making the sector moderately fragmented. Acquisitions accelerated in 2025 as incumbents bought AI assets rather than building them. SAP’s September 2025 purchase of SmartRecruiters modernized SuccessFactors recruiting workflows. Workday also made consecutive acquisitions of Paradox and Sana to fold conversational AI and learning graphs into its HCM suite. ADP similarly launched WorkForce Suite in November 2025, integrating time and talent on a joint data model.

Technology differentiation centers on three vectors. First, the depth of autonomous agents: Paradox automates candidate scheduling via SMS and WhatsApp, reducing recruiter workload up to 60%. Second, live bias mitigation: platforms post public model audits to reassure regulators. Third, integration breadth: pre-built connectors for Oracle, SAP, Workday and ADP decide enterprise access. Vertical specialists defend against suite vendors by embedding compliance workflows, for example, Vivian Health’s license verification for nurses. Over the next five years, rising audit costs and buyer preference for unified suites are expected to reduce the long-tail vendor count, yet niches such as hourly hiring and gig marketplaces will still support independent innovators.

Recruitment Software Industry Leaders

SAP SE

Workday, Inc.

Oracle Corporation

Automatic Data Processing, Inc.

International Business Machines Corporation (IBM)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Workday confirmed regulatory clearance for its planned acquisition of Pipedream, a workflow-automation provider that will extend native integrations across HCM modules.

- November 2025: Workday closed the USD 1.1 billion purchase of Sana, adding AI-powered learning that links career growth with recruiting pipelines.

- November 2025: ADP debuted WorkForce Suite, a unified HCM platform for mid-market clients that merges payroll, scheduling and recruiting in one interface.

- November 2025: Workday announced intent to acquire Pipedream to simplify custom connectors between its HCM stack and third-party apps.

- October 2025: Oracle launched autonomous recruiting agents inside Fusion Cloud HCM, targeting a 40% reduction in time-to-hire.

Global Recruitment Software Market Report Scope

Recruitment software is a tool that enables recruiters to recruit employees more efficiently. The software is used to post job openings on a corporate website or job feed, screen resumes, and generate interview requests to shortlist candidates via various channels such as email or SMS.

The Recruitment Software Market Report is Segmented by Deployment (On-Premises, and Cloud), by Organization Size (Small and Medium Enterprises, and Large Enterprises), Component (Solutions, Services), by Functionality (Applicant Tracking System, Recruitment CRM/Marketing, Onboarding Software, Talent Analytics and AI Tools, and Background-check/Assessment Modules), by End-User Vertical (IT and Telecom, BFSI, Retail and E-commerce, Manufacturing, Healthcare and Life Sciences, and Other End-User Verticals), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premises |

| Cloud |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Solutions |

| Services |

| Applicant Tracking System (ATS) |

| Recruitment CRM/Marketing |

| Onboarding Software |

| Talent Analytics and AI Tools |

| Background-check/Assessment Modules |

| IT and Telecom |

| BFSI |

| Retail and E-commerce |

| Manufacturing |

| Healthcare and Life Sciences |

| Other End-User Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment | On-Premises | |

| Cloud | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Component | Solutions | |

| Services | ||

| By Functionality | Applicant Tracking System (ATS) | |

| Recruitment CRM/Marketing | ||

| Onboarding Software | ||

| Talent Analytics and AI Tools | ||

| Background-check/Assessment Modules | ||

| By End-User Vertical | IT and Telecom | |

| BFSI | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Healthcare and Life Sciences | ||

| Other End-User Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the recruitment software market in 2026?

The recruitment software market size is USD 3.77 billion in 2026.

What is the expected CAGR for recruitment platforms through 2031?

Market value is forecast to grow at a 7.85% CAGR from 2026 to 2031.

Which deployment model is growing fastest?

Cloud deployment is expanding at a 9.21% CAGR, driven by AI workloads and elastic compute.

Why is healthcare adoption accelerating?

Nurse and clinician shortages require faster credential checks, and AI assistants cut time-to-fill from 66 days to 45 days.

Which region will contribute the most incremental revenue?

Asia Pacific is projected to add the largest share of new revenue, advancing at a 10.66% CAGR.

How concentrated is vendor competition?

The top 10 suppliers hold roughly 45–50% of global revenue, indicating moderate concentration.

Page last updated on: