Time And Attendance Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

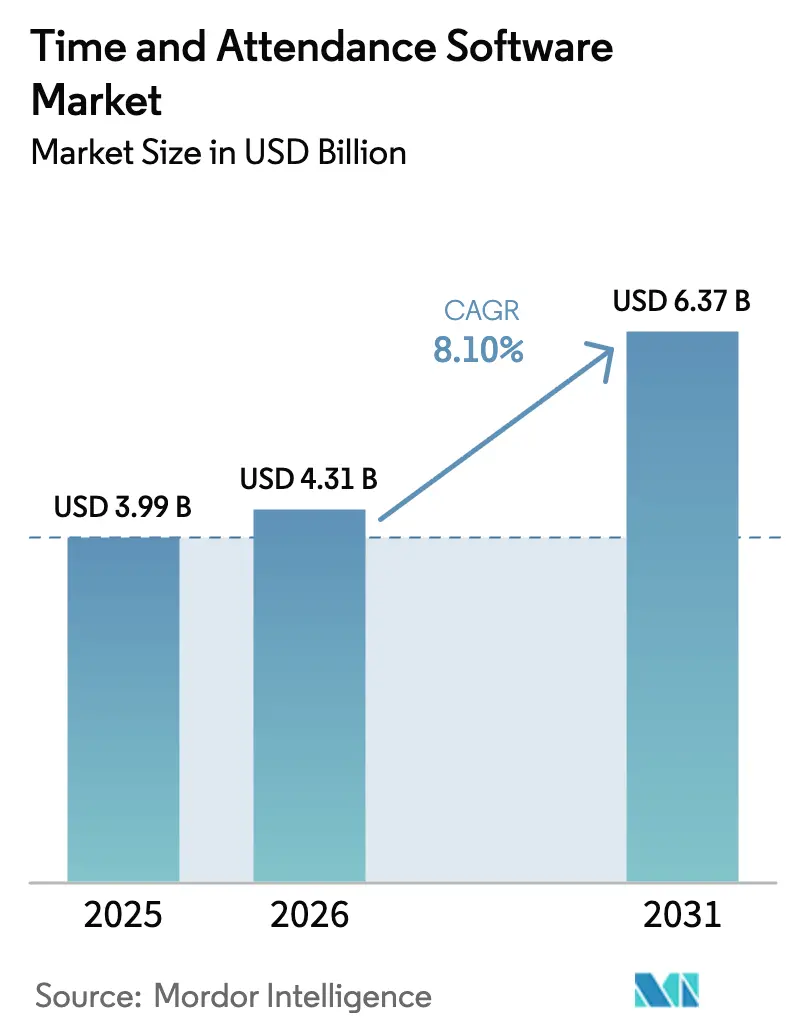

| Market Size (2026) | USD 4.31 Billion |

| Market Size (2031) | USD 6.37 Billion |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

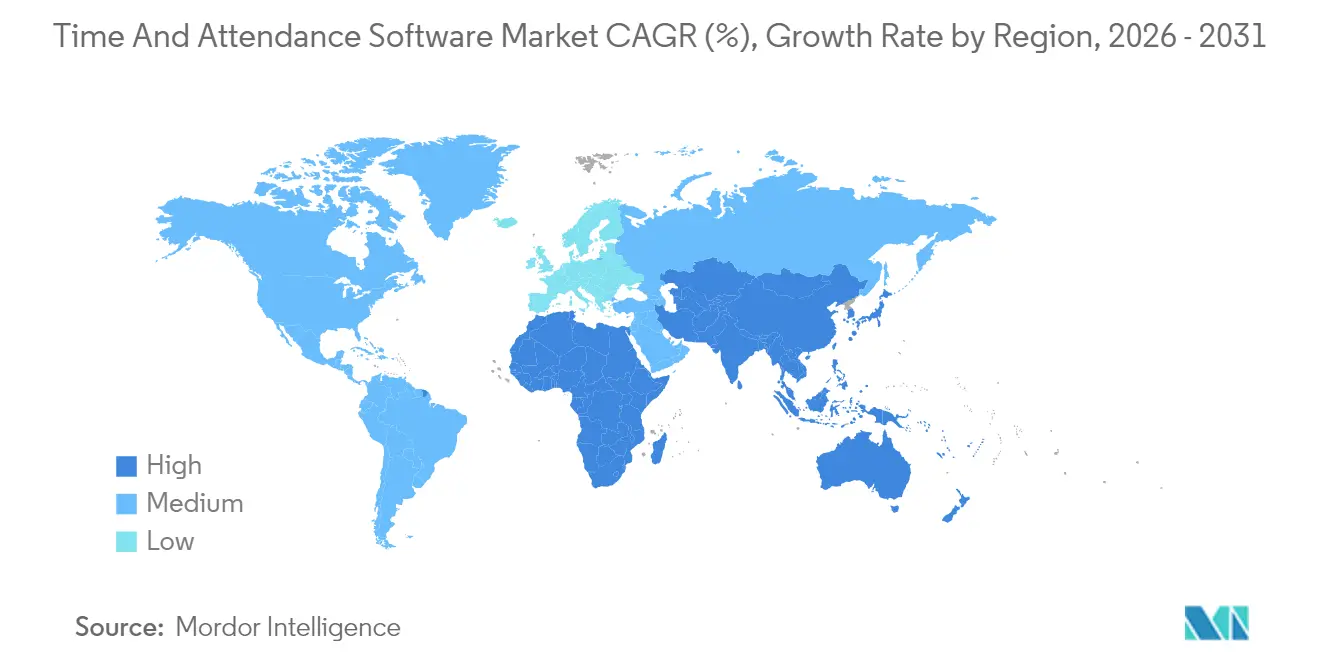

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

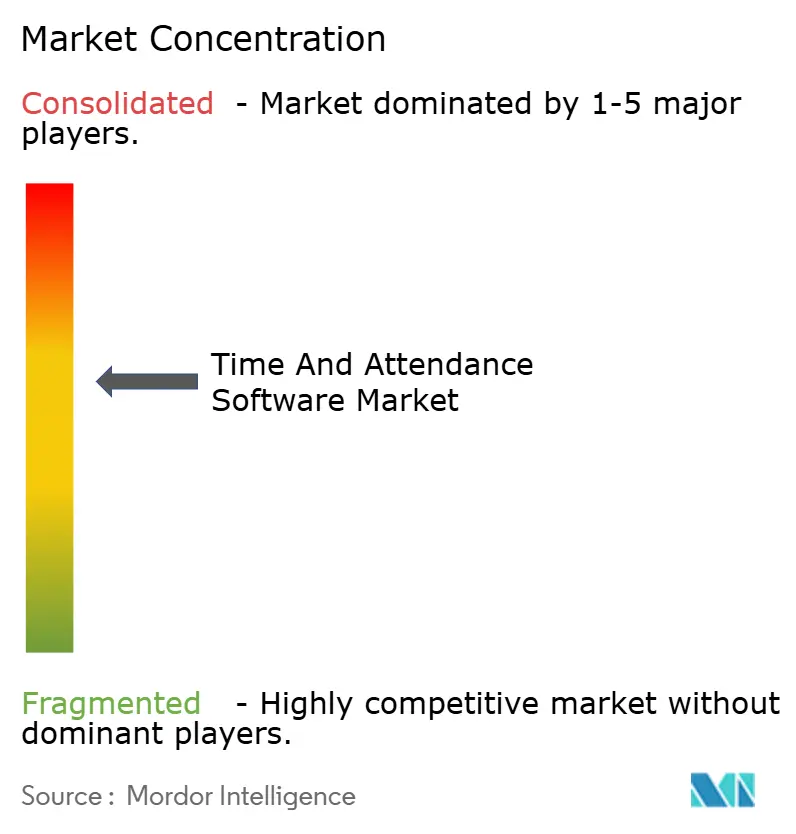

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Time And Attendance Software Market Analysis by Mordor Intelligence

Time and attendance software market size in 2026 is estimated at USD 4.31 billion, growing from 2025 value of USD 3.99 billion with 2031 projections showing USD 6.37 billion, growing at 8.1% CAGR over 2026-2031. Robust demand is anchored in hybrid work adoption, sharper enforcement of labor-compliance rules, and the shift to cloud-delivered workforce-management platforms. Vendors are expanding AI-driven analytics that predict staffing needs, while biometric authentication and IoT devices raise accuracy and security. North America retains early-mover advantage, yet Asia-Pacific delivers the fastest regional growth as manufacturing and services firms accelerate digitization. Competitive dynamics remain moderate: large HCM-suite providers leverage embedded ecosystems, whereas niche players specialize in vertical solutions and advanced biometrics.

Key Report Takeaways

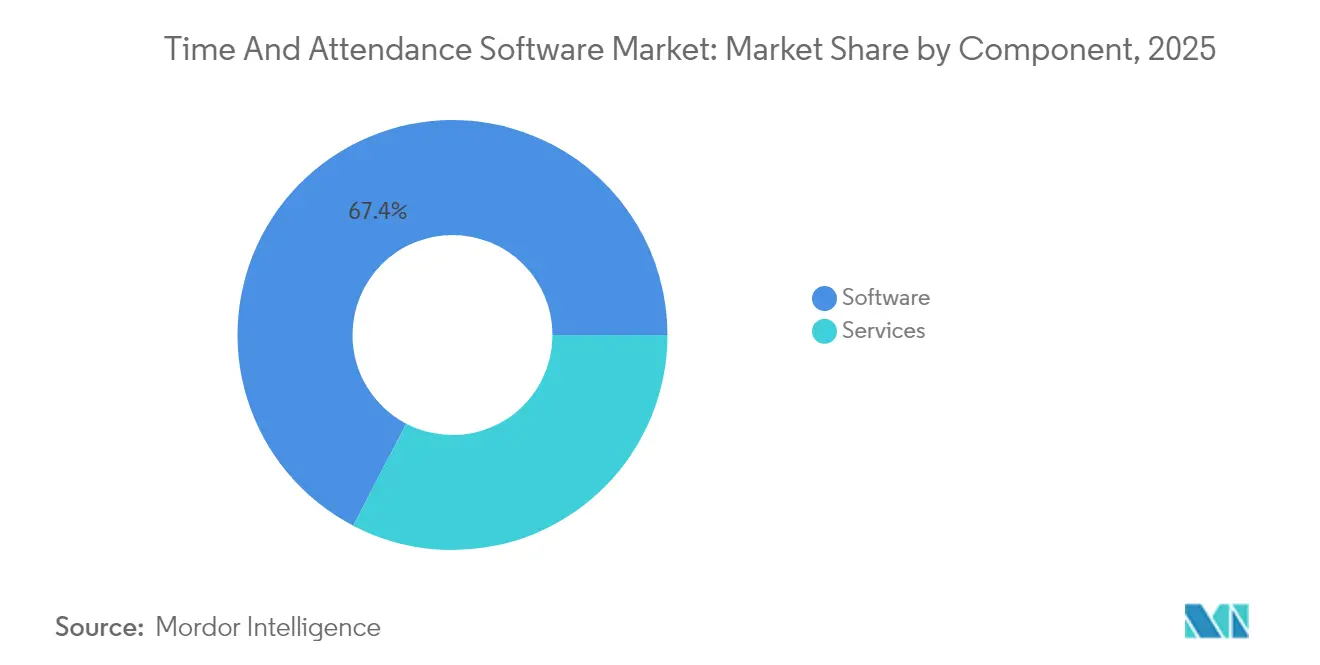

- By component, software retained a 67.35% revenue share in 2025; services represent the fastest component growth at a 11.8% CAGR to 2031.

- By deployment mode, cloud held 71.25% of the time and attendance software market share in 2025 and is projected to expand at an 11.35% CAGR through 2031.

- By organization size, large enterprises accounted for 44.35% of the 2025 market; the micro- and small-enterprise segment is accelerating but remains unquantified in the revised data set.

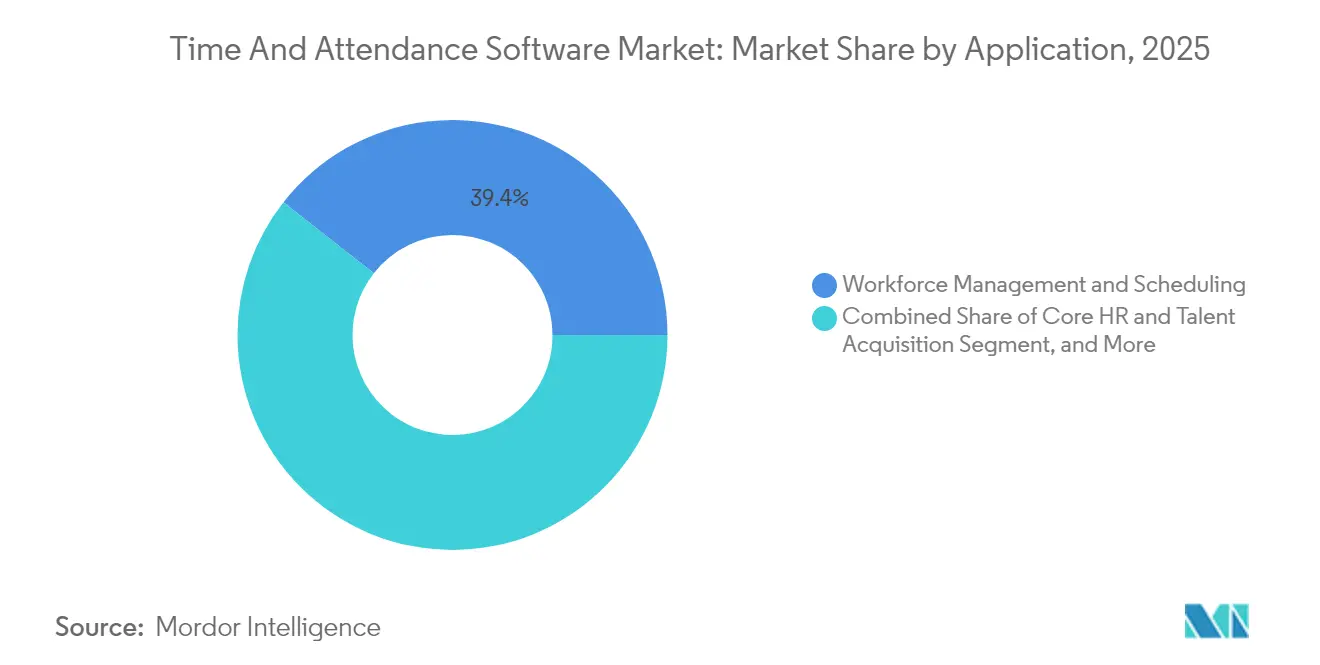

- By application, workforce management and scheduling contributed 39.40% of the time and attendance software market size in 2025, whereas payroll-integration and compliance applications are growing at a 12.8% CAGR to 2031.

- By end-user industry, IT and telecommunications led with an 17.65% share in 2025, while healthcare and life sciences post the highest industry CAGR at 12.29% through 2031.

- By geography, North America commanded 34.55% of 2025 revenue; Asia-Pacific is the fastest-growing region with an 11.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Time And Attendance Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Labor-Compliance Mandates (FLSA, EU Working Time Directive) | +2.1% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Hybrid and Remote Workforce Expansion Requiring Cloud/Mobile Time Capture | +1.8% | Global, led by North America and APAC urban centers | Short term (≤ 2 years) |

| AI-Driven Productivity Analytics for Labor-Cost Optimization | +1.4% | North America and EU core, expanding to APAC | Long term (≥ 4 years) |

| SMB Digitization of Payroll and Time-Tracking via SaaS Platforms | +1.2% | Global, with rapid adoption in APAC and Latin America | Medium term (2-4 years) |

| Consolidation of HCM Modules to Reduce HR-Tech Stack Cost | +0.9% | North America and EU primarily, selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Labor-Compliance Mandates Drive Adoption

Recent U.S. Department of Labor guidance on AI-based monitoring heightens record-keeping expectations, while the 2024 FLSA overtime threshold rules require more granular hour classification. European companies face parallel pressure under the Working Time Directive, spurring replacement of legacy systems that cannot automate multi-jurisdictional rules. AI monitoring amplifies legal complexity as firms balance productivity insights with worker privacy rights under GDPR and related statutes. [1]Ogletree Deakins, “Navigating AI-Based Workforce Monitoring,” ogletree.com

Hybrid and Remote Workforce Expansion Requires Cloud/Mobile Capture

With 80% of large organizations supporting mixed work patterns, demand has shifted to mobile-first systems that geofence location, authenticate biometrics, and sync data in real time. [2]FlowForma, “Hybrid Workforce Management Survey 2024,” flowforma.com Cloud deployment removes on-premise constraints and aligns payroll across time zones. Vendors embed palm-vein and facial recognition to curb fraud while preserving convenience.

AI-Driven Productivity Analytics Optimize Labor Costs

Machine-learning engines mine historical attendance to forecast staffing gaps, yielding up to 30% productivity gains and overtime savings, according to industry case studies. [3]ResearchGate, “IoT-Enabled Attendance Management: A Review,” researchgate.net Large retailers deploy dynamic scheduling that aligns labor with demand spikes, improving wage efficiency and employee satisfaction.

SMB Payroll Digitization via SaaS Platforms

Affordable subscription models—typically 200-400 JPY (USD 1.4-2.8) per user per month—allow small firms to access features once reserved for enterprises. [4]Aspic Japan, “SaaS Subscription Pricing Trends 2024,” aspicjapan.org Government e-record mandates across APAC accelerate uptake by making electronic attendance a prerequisite for compliance filings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Biometric Regulations (GDPR, BIPA) | -1.6% | Global, with highest impact in EU and select U.S. states | Medium term (2-4 years) |

| Integration Complexity with Legacy ERP and Payroll Systems | -1.1% | North America and EU primarily, emerging in mature APAC markets | Short term (≤ 2 years) |

| Price Sensitivity in Developing Economies Drives Manual/Freemium Use | -0.8% | APAC emerging markets, Latin America, MEA | Medium term (2-4 years) |

| Labor-Union Pushback on Perceived "Surveillance" Features | -0.5% | North America and EU, selective APAC manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Biometric Regulations

Illinois’ BIPA mandates explicit consent and imposes statutory damages, prompting firms to add consent workflows and local storage, thereby doubling some rollout budgets. GDPR further requires privacy-impact assessments and restricts cross-border data transfers, fragmenting system architectures.

Integration Complexity with Legacy Systems

Many large enterprises run payroll applications that lack open APIs, forcing costly middleware or manual reconciliation. Dual-running old and new systems during cutover inflates operating costs and can stall modernization until broader ERP refresh cycles justify the investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expand Amid Software Leadership

Software held 67.35% of 2025 revenue, underscoring the primacy of cloud-native platforms in the time and attendance software market. Professional-services revenue is growing at 11.8% CAGR as organizations seek integration skills, biometric expertise, and compliance consulting. The services surge illustrates how complex deployments elevate demand for managed offerings that handle updates, rule changes, and mobile device management.

Services also differentiate vendors in an environment where core timekeeping functionality is commoditized. Managed services for SMEs outsource maintenance at predictable fees, freeing scarce IT staff. For global enterprises, consultancies configure multi-jurisdictional rule engines that codify overtime, break periods, and union agreements.

By Deployment Mode: Cloud Ascendancy Reshapes Infrastructure

Cloud accounted for 71.25% of 2025 revenue and is expanding at an 11.35% CAGR, confirming that scalability and mobile accessibility outweigh legacy fears. Cloud platforms provide native smartphone apps with geofencing and biometric login, eliminating punch-clock hardware. Continuous software updates enable automatic compliance with evolving labor codes, an advantage on-premise systems cannot match.

Hybrid architectures persist where data sovereignty is critical, yet even those designs integrate public-cloud analytics for AI-driven insights. Vendors leverage cloud ecosystems to bundle payroll, onboarding, and analytics, deepening customer lock-in and extending average contract terms.

By Organization Size: SME Adoption Democratizes Capability

Large enterprises captured 44.35% of 2025 spending, but growth momentum has shifted toward micro- and small-business buyers empowered by low-cost SaaS. Flexible monthly fees and free trials remove cap-ex hurdles, while pre-built connectors slot into popular accounting suites. SMEs in retail, healthcare, and field services adopt mobile clocks that replace paper timesheets and streamline labor-law reporting.

Enterprises continue to favor integrated HCM suites that unify talent, learning, and scheduling. Their focus is shifting to predictive analytics and scenario planning, where attendance data feeds strategic workforce-planning algorithms.

By Application: Compliance-Centric Growth Outpaces Scheduling

Workforce management and scheduling represented 39.40% of 2025 revenue, reflecting core demand for shift optimization. The payroll-integration and compliance segment is advancing at a 12.8% CAGR as fines for mis-classification mount. Healthcare providers integrate attendance with payroll engines to handle shift differentials, while service industries embed regulatory rules to automate break compliance.

Elsewhere, project-time tracking gains traction in professional services, and attendance data increasingly feeds performance-management dashboards to correlate presence with outcomes.

By End-User Industry: Healthcare Accelerates on Safety Mandates

IT and telecommunications held 17.65% share in 2025, leveraging early cloud adoption to manage dispersed talent. Healthcare and life sciences grow fastest at 12.29% CAGR as staffing-ratio regulations and patient-safety protocols demand minute-level accuracy. Manufacturing leverages attendance data to align labor with Just-In-Time production, while public-sector modernization programs stipulate electronic time logs for audit transparency.

Banking institutions value audit trails for regulatory exams, and universities extend systems to monitor student attendance, illustrating the breadth of vertical use cases fueling sustained adoption.

Geography Analysis

North America commanded 34.55% of 2025 revenue, benefitting from strict overtime rules and advanced enterprise IT environments. Vendors such as UKG and Oracle iterate AI features rapidly, yet customer acquisition moderates as installed bases mature. Growth increasingly comes from upselling analytics, biometrics, and industry-specific modules rather than net-new logos.

Asia-Pacific is projected to grow at an 11.02% CAGR through 2031, propelled by government digitization drives and SME cloud readiness. Digital services trade in the region rose from USD 403.4 billion in 2005 to USD 1.4 trillion in 2019, underscoring a structural shift toward digital workflows. Local champions such as ZKTeco and Matrix pair competitive pricing with region-specific compliance features, while multinationals deepen channel partnerships.

Europe maintains steady expansion as GDPR enforces stringent biometric safeguards and the Working Time Directive continues to tighten record-keeping obligations. Public-sector digitization accelerates adoption, and manufacturing clusters in Germany and the Nordics deploy integrated attendance-and-shop-floor systems to lift productivity. Emerging markets in Latin America, the Middle East, and Africa remain earlier in the adoption curve, but cloud availability and mobile-first deployments lower entry barriers.

Competitive Landscape

The time and attendance software market shows moderate concentration. SAP, Oracle, and UKG leverage broad HCM suites, embedded analytics, and large installed bases to sustain competitive moats. Switching costs rise as attendance data feeds performance, payroll, and learning modules across the same platform.

Specialist vendors differentiate through vertical depth and biometric innovation. ZKTeco’s third-place finish in the 2025 Fingerprint Verification Competition affirms algorithmic prowess supported by a 900-plus patent portfolio, enabling OEM partnerships with global HCM providers. Matrix tailors multi-location compliance tools for banking and fintech, while ATOSS capitalizes on European labor-law expertise to expand managed services revenue.

New entrants attack the SME tier with freemium mobile apps and consumer-grade UX, shrinking implementation times from months to days. Larger incumbents counter by offering trimmed cloud packages and marketplace ecosystems that integrate niche extensions. Patent activity remains intense around multimodal biometrics and AI-driven scheduling, signalling technology as the prime battleground over pure feature parity.

Time And Attendance Software Industry Leaders

SAP SE

FingerCheck

NETtime Solutions

ADP, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Zalaris ASA reported NOK 1.346 billion (USD 125.6 million) in 2024 revenue, boosted by its PeopleHub SaaS platform spanning 150 countries; regional expansion underlines cross-border payroll complexity as a growth lever.

- April 2025: Oplus integrated its shift-management tool with Minajin’s attendance platform, offering free plans for up to 100 users; the alliance showcases API-driven ecosystems that lower SMB adoption friction.

- March 2025: ATOSS posted record EUR 170.6 million (USD 185.2 million) sales for 2024, the 19th consecutive growth year, underscoring sustained European demand for integrated workforce management.

- February 2025: Matrix unveiled new time-attendance modules at IBEX India 2025, targeting BFSI compliance with real-time field-officer tracking; the move deepens sector focus and positions the firm for managed-services contracts.

Global Time And Attendance Software Market Report Scope

The automatic time tracking of employee's working hours, the creation of digital timesheets to track payroll processes, and the provision of real-time attendance data to management are the tasks that time, and Attendance software performs. Additionally, it gives employees a centralized location to monitor schedules, submit requests, and receive updates on any changes to corporate policy.

Time and Attendance Software Market has been segmented based on Deployment (On-premise, Cloud), By Application (Core HR and Talent Acquisition, Workforce Management), By End-User Industry (BFSI, Retail& E-Commerce, IT & Telecommunication, Government, Healthcare, Manufacturing, Education), and By Geography (North America, Europe, Asia Pacific, Latin America and the Middle East & Africa)

| Software | Stand-alone Time and Attendance Software | |

| Integrated HCM Suite Modules | ||

| Services | Professional Services | Implementation and Integration |

| Consulting and Training | ||

| Managed Services | ||

| On-premise |

| Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| Workforce Management and Scheduling |

| Core HR and Talent Acquisition |

| Payroll Integration and Compliance |

| Other Applications |

| BFSI |

| Retail and E-commerce |

| IT and Telecommunications |

| Government and Public Sector |

| Healthcare and Life Sciences |

| Manufacturing |

| Education |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Software | Stand-alone Time and Attendance Software | |

| Integrated HCM Suite Modules | |||

| Services | Professional Services | Implementation and Integration | |

| Consulting and Training | |||

| Managed Services | |||

| By Deployment Mode | On-premise | ||

| Cloud | |||

| By Organization Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Application | Workforce Management and Scheduling | ||

| Core HR and Talent Acquisition | |||

| Payroll Integration and Compliance | |||

| Other Applications | |||

| By End-User Industry | BFSI | ||

| Retail and E-commerce | |||

| IT and Telecommunications | |||

| Government and Public Sector | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Education | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the time and attendance software market?

The time and attendance software market is valued at USD 4.31 billion in 2026.

How fast is the market expected to grow?

It is forecast to expand at an 8.1% CAGR, reaching USD 6.37 billion by 2031.

Which region is growing the fastest?

Asia-Pacific posts the highest regional CAGR at 11.02% through 2031 due to rapid digitization and SME cloud adoption.

Why is cloud deployment overtaking on-premise solutions?

Cloud platforms offer scalability, continuous compliance updates, and mobile access, capturing 71.25% of 2025 revenue and growing at an 11.35% CAGR.

How do labor-compliance rules influence buying decisions?

Updated overtime thresholds (FLSA) and EU Working Time Directive enforcement add +2.1% to forecast CAGR by pushing firms toward granular, automated time tracking.

What technologies are redefining attendance management?

AI-driven scheduling, geofenced mobile clocks, and multimodal biometrics (palm-vein, facial recognition) are now mainstream features enhancing accuracy and security.

Page last updated on: