Employee Attrition Prediction Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 11.28% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Employee Attrition Prediction Software Market Analysis by Mordor Intelligence

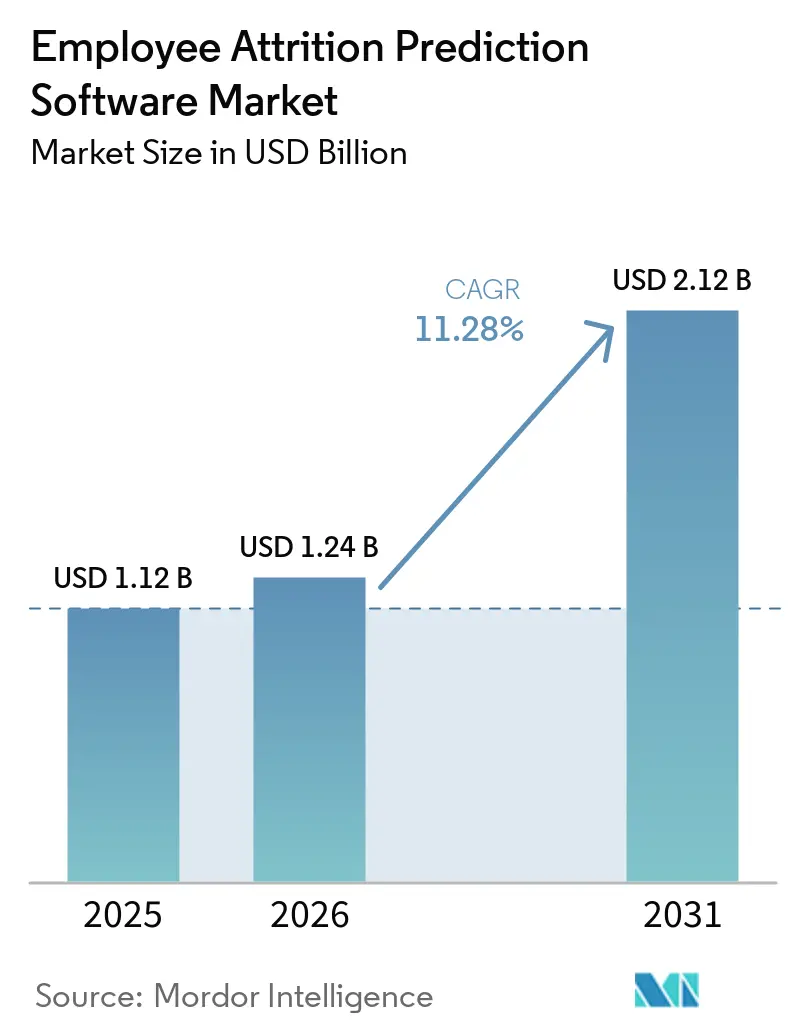

The Employee attrition prediction software market size is projected to be USD 1.12 billion in 2025, USD 1.24 billion in 2026, and reach USD 2.12 billion by 2031, growing at a CAGR of 11.28% from 2026 to 2031. The current market size shows a clear shift from backward-looking headcount reviews to continuous retention monitoring built on live employee signals. Boards and finance teams now expect attrition risk to be expressed in business terms, which is pushing predictive retention tools into standard enterprise planning and review cycles. Cloud-based human capital management environments, broader adoption of machine learning, and stronger demand for measurable workforce stability are driving the employee attrition prediction software market on a firm expansion path. Competitive activity is also rising because specialist analytics providers, HCM suite vendors, and employee experience platforms are now targeting the same buyer groups with different products and pricing models. Growth opportunities remain strongest where vendors can reduce deployment friction, explain model outputs clearly, and connect risk detection with manager action inside everyday enterprise workflows.

Key Report Takeaways

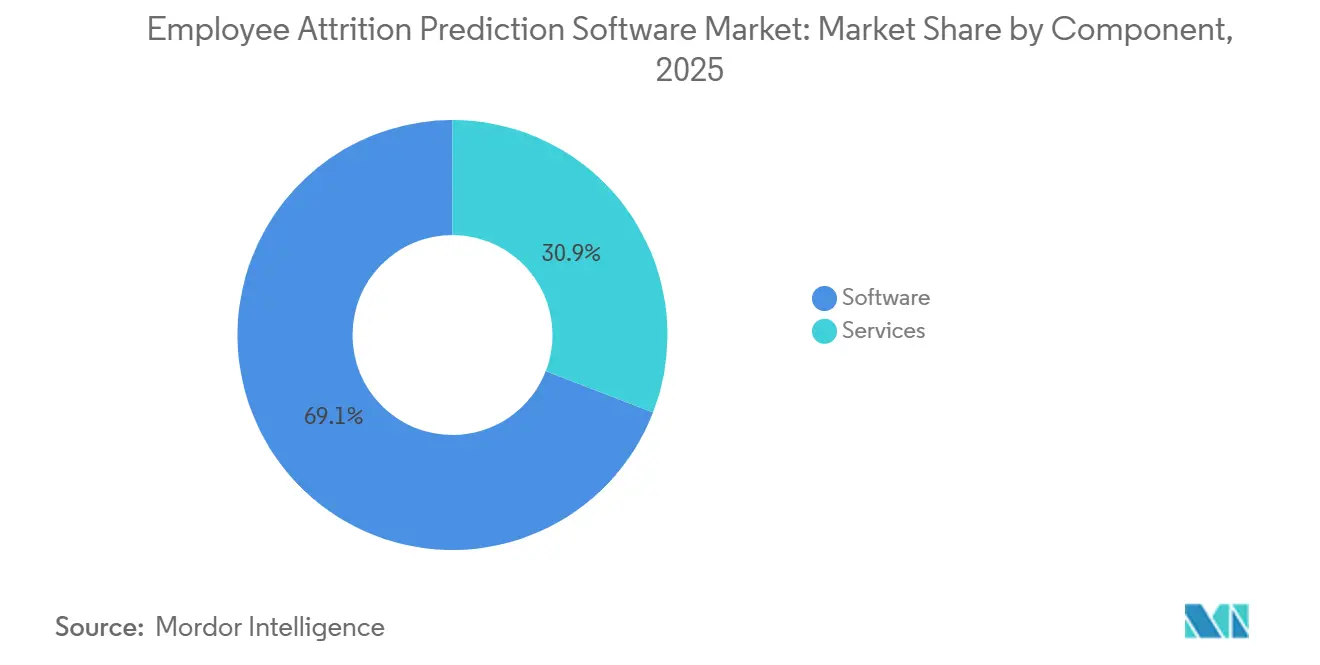

- By component, software held 69.14% share of the employee attrition prediction software market in 2025, while services are projected to expand at a 12.91% CAGR through 2031 as enterprises seek deeper onboarding, integration, and change support.

- By application, turnover prediction and flight-risk scoring accounted for 36.71% of revenue in 2025, while retention intervention and prescriptive action planning are projected to grow at an 11.92% CAGR through 2031.

- By deployment mode, on-premises held 68.41% share of the employee attrition prediction software market in 2025, while cloud-based deployment is expected to expand at a 13.41% CAGR through 2031.

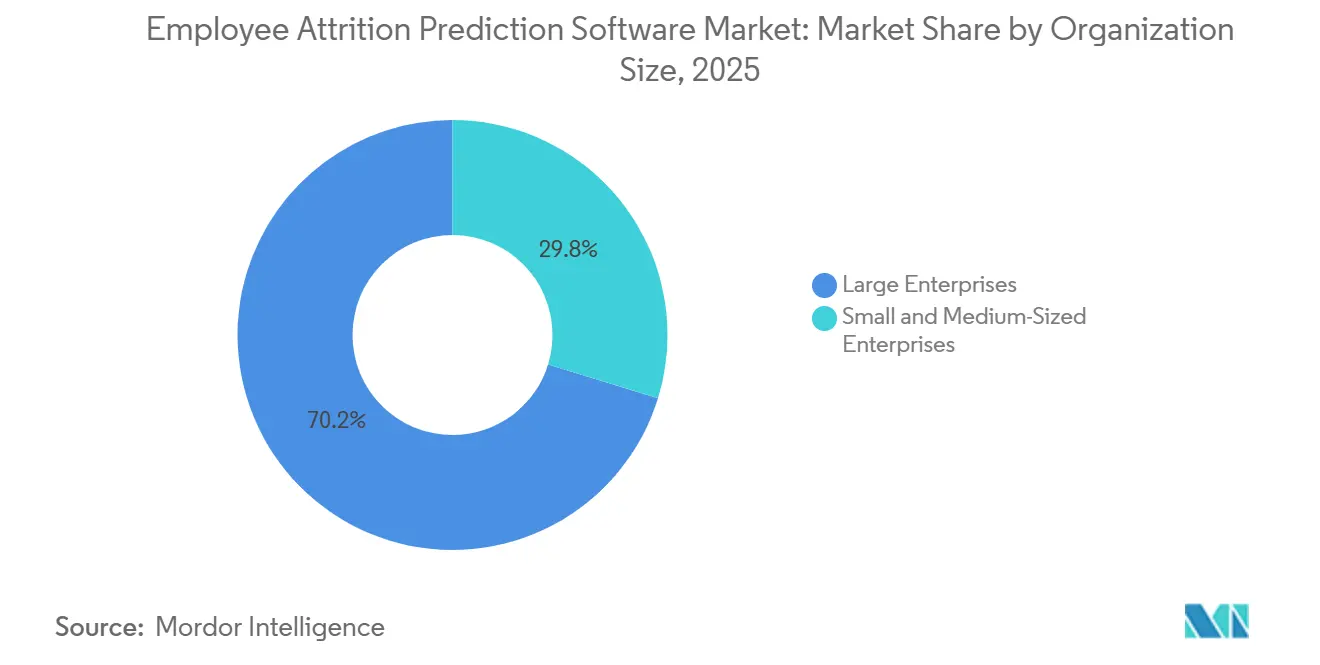

- By organization size, large enterprises accounted for 70.24% of revenue in 2025, while small and medium-sized enterprises are projected to grow at a 12.67% CAGR through 2031.

- By end-user industry, information technology and telecommunications led with 29.12% revenue share in 2025, while healthcare and life sciences are expected to record the fastest growth at an 11.56% CAGR through 2031.

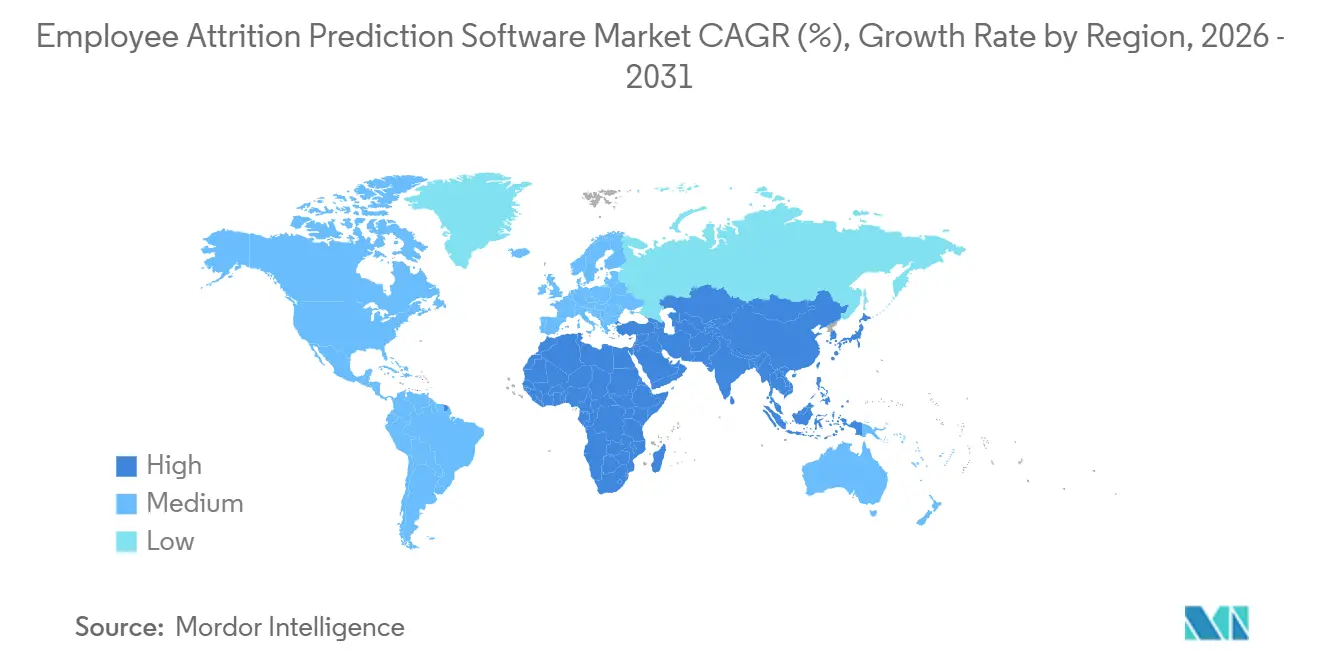

- By geography, North America held 37.22% share in 2025, while Asia-Pacific is projected to grow at a 12.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Employee Attrition Prediction Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cost of Regrettable Attrition and Backfill Delays | +3.2% | Global, with concentrated intensity in North America and Western Europe | Short term (≤ 2 years) |

| Growing Use of AI and Machine Learning for Flight-Risk Scoring | +2.8% | Global, early adoption in North America, rapid uptake in APAC and India | Medium term (2-4 years) |

| Expansion of Cloud-Native HR Analytics and HCM Ecosystems | +2.1% | Global, strongest in North America and APAC, emerging in Middle East and Africa | Medium term (2-4 years) |

| CFO-Led Demand to Quantify Attrition Risk in Dollar Terms | +1.5% | North America and EU, with spillover to Australia and Singapore | Short term (≤ 2 years) |

| Need for Hybrid Workforce Visibility and Continuous Listening | +1.0% | North America, core EU markets, and APAC technology hubs | Medium term (2-4 years) |

| Skills-Based Internal Mobility Programs Requiring Predictive Retention Signals | +0.8% | North America and EU, with early adoption in APAC technology enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cost of Regrettable Attrition and Backfill Delays

Rising replacement costs have made the employee attrition prediction software market easier to justify at the business-unit level, as retention technology is now tied directly to avoidable labor expense. Turnover cost per worker reached USD 45,236 in 2026, up from USD 36,723 in 2025, and 50% of US companies expected voluntary separations to rise further in 2026. That shift matters because buyers are no longer treating attrition as a soft human resources issue; they are treating it as a cost-control problem with immediate budget consequences. Gloat reported that identifying high-flight-risk employees 6 weeks earlier than managers could do on their own helped retain 68% of flagged employees, while the intervention cost was USD 28,000 against USD 340,000 in replacement outlay, and total savings reached USD 4.8 million in one business unit.[1]Gloat, “Talent Retention Agent Use Case,” Gloat, gloat.com As more return cases enter procurement discussions, the employee attrition prediction software market is moving from optional pilot spending to mainstream workforce investment. The practical buying question is now less about whether a company needs predictive retention software and more about which platform best aligns with internal hiring costs, manager workflows, and intervention capacity.

Growing Use of AI and Machine Learning for Flight-Risk Scoring

The employee attrition prediction software market is also benefiting from the wider acceptance of machine learning as a credible way to identify departure risk before managers see visible warning signs. A clinical deployment by Lotis Blue showed that an ML model predicted healthcare worker turnover with 90% accuracy, and 45% of employees who later quit had received no proactive retention conversation. That result supports the view that predictive systems are gaining traction because they can expose silent risk pockets that manual review often misses. It also explains why buyers now expect more than dashboards, because basic reporting alone does not change outcomes unless it triggers action at the manager level. As adoption expands, the employee attrition prediction software market is likely to reward vendors that can keep models current when performance reviews, engagement inputs, and other people's data become noisier. This creates a secondary demand layer for recalibration, explainability, and data-quality controls, especially in enterprises that already use generative AI in HR processes.

Expansion of Cloud-Native HR Analytics and HCM Ecosystems

The spread of cloud-native people systems is changing how the employee attrition prediction software market is bought, deployed, and compared across vendors. SAP introduced People Intelligence within SAP Business Data Cloud in May 2025, linking attrition-related signals more directly with SAP SuccessFactors talent records. Workday expanded its data ecosystem in late 2025 through zero-copy integration with Google BigQuery, enabling HR analytics to run against live operational data without replication lag. These moves lower the cost of activation for customers already in major HCM environments, reducing the advantage once held by stand-alone point tools. The employee attrition prediction software market is therefore shifting toward platforms that integrate smoothly into broader enterprise architecture rather than requiring buyers to build a separate analytics stack. Independent vendors still have room to grow, but they increasingly need to pair risk scoring with workflow automation, decision support, and faster implementation to avoid being treated as interchangeable add-ons.

CFO-Led Demand to Quantify Attrition Risk in Dollar Terms

The employee attrition prediction software market is being shaped more directly by finance leadership because workforce instability is now reviewed as a measurable exposure with cash implications. German companies were estimated to face annual attrition costs of EUR 118 billion (USD 127.4 billion), a figure that is moving attrition discussion from HR dashboards into CFO reporting and board review. This shift changes who signs off on software budgets and also changes the tests vendors must pass during evaluation. User experience still matters, but financial scenario modeling, intervention economics, and replacement-cost visibility now carry more weight in enterprise buying committees. Vendors that arrive with total-cost-of-turnover calculators and budget-ready return logic are better positioned as the employee attrition prediction software market becomes more finance-led. This also shortens the path from problem recognition to software purchase when attrition costs are already visible in labor planning, overtime, and delayed hiring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Employee Data Privacy and AI Governance Compliance | -1.8% | EU is primary, with spillover to Canada, Japan, and Southeast Asia | Short term (≤ 2 years) |

| Data Silos and Legacy HRIS Integration Complexity | -1.4% | Global, most acute in large enterprises across North America and Europe | Medium term (2-4 years) |

| Works Council and Employee Pushback on Digital Exhaust Monitoring | -0.9% | Core EU markets, with spillover to the Nordics and Japan | Medium term (2-4 years) |

| GenAI-Generated Feedback Noise Weakening Model Precision | -0.7% | Global, concentrated in organizations using GenAI-enabled performance platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Employee Data Privacy and AI Governance Compliance

Compliance pressure remains a major brake on the employee attrition prediction software market, as many employers must now treat it as a high-risk AI use case. Legal analysis of the EU AI Act noted that Annex III obligations on transparency, human oversight, and bias testing apply to workforce tools that assess or influence employee behavior, and that planning requirements are already in effect, even after the compliance timeline was extended. This means product deployment is no longer a pure technology exercise, as legal review, documentation, governance design, and audit readiness are now part of the same project. GDPR enforcement also kept pressure high, with reporting in 2025 showing that cumulative penalties moved past EUR 5 billion (USD 5.4 billion) for the first time. The effect on the employee attrition prediction software market is evident in longer sales cycles and a higher first-year deployment burden, especially in Europe and in jurisdictions with similar accountability rules. Vendors that cannot show clear consent logic, human review pathways, and bias controls face slower conversion even when the product itself is technically strong.

Data Silos and Legacy HRIS Integration Complexity

Data fragmentation slows the employee attrition prediction software market because model performance depends on clean links across systems that were rarely built to work together. Technical review of enterprise use cases has shown that underperforming attrition models often stem from broken data architecture rather than weak algorithms. Attrition tools need consistent feeds from HRIS, learning systems, performance tools, communication signals, and compensation records, yet these datasets usually reside in separate environments with different rules and update cycles. That makes deployment difficult for large organizations where HR, legal, and IT still work through separate approval tracks and data ownership models. Vendors with validated connectors for Workday, SAP SuccessFactors, Oracle HCM, and ADP are reducing friction and gaining a structural edge in the employee attrition prediction software market. The problem becomes even harder in multi-country rollouts, because data that is permissible for scoring in one jurisdiction may need redesign or exclusion in another.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue While Professional Services Scale Faster

Services are projected to grow at a 12.91% CAGR through 2031, making them the fastest-growing segment of the employee attrition prediction software market,, even though software remained the core revenue base in 2025. Software still anchors most commercial value because it houses the prediction engine, data model, workflow logic, and reporting interface that buyers license first. That base position keeps software central to every major deal, especially in large organizations that want broad retention visibility across regions and business units. At the same time, the employee attrition prediction software industry is moving toward more complex deployments that depend on configuration, onboarding, and cross-functional rollout support. This is why services are expanding faster, because many buyers now need help translating model output into manager actions, policy changes, and ongoing governance routines.

Implementation and integration work have become more important as the employee attrition prediction software market moves beyond simple dashboard deployment into embedded operational use. Vendors are spending more time on connector setup, intervention design, alert calibration, and manager adoption because those steps now affect realized value as much as model accuracy does. Service teams also help reduce customer churn, since accounts that rely on a vendor for process redesign and change support are less likely to treat the platform as replaceable. This gives vendors a stronger long-term relationship and makes services a practical retention tool for both the supplier and the buyer. The same trend is raising the importance of certified partner networks, because buyers want implementation resources that already understand major HCM stacks and enterprise governance requirements.

By Application: Flight-Risk Scoring Leads as Prescriptive Capabilities Attract Investment

Turnover prediction and flight-risk scoring accounted for 36.71% of revenue in 2025, keeping this use case at the center of the employee attrition prediction software market. Most enterprises still start here because flight-risk scoring is the clearest way to show immediate value from people data. It provides HR teams and line managers with a clear entry point and lays the data foundation for later use cases, such as intervention planning or internal mobility targeting. In that sense, flight-risk scoring remains the operational gateway to the broader employee attrition prediction software market rather than a single use case among many. Retention intervention and prescriptive action planning are expected to grow at a 11.92% CAGR through 2031, indicating that buyers increasingly want recommendations tied to action, not just flags tied to observation.

This shift matters because the category is moving from prediction toward guided response. Gloat integrated retention recommendations into Microsoft 365 Copilot and Microsoft Teams in April 2026, which let managers respond to risk signals inside familiar work tools instead of opening a separate application. Employee engagement and sentiment analytics still play an important role because they provide early context that helps explain why flight risk is rising before an employee signals intent directly. Compensation and pay equity analytics are also becoming more relevant where employers face audit pressure and need a defensible view of pay-linked retention issues. Workforce planning and internal mobility analytics remain important for large enterprises that want to connect retention, redeployment, and skills strategy within a single planning framework.

By Deployment Mode: On-Premises Entrenched as Cloud Deployment Expands Rapidly

On-premises accounted for 68.41% of the employee attrition prediction software market share in 2025, while cloud-based deployment is projected to record the fastest employee attrition prediction software market size growth at 13.41% CAGR through 2031. This mix looks uneven at first, but it reflects the fact that the largest early adopters often work in regulated settings with strict data residency and control requirements. Financial services, healthcare, and public sector buyers have tended to extend analytics within existing controlled environments rather than moving quickly to public cloud models. That kept on-premises strong even as new buyers entered the employee attrition prediction software market through lighter and faster cloud options. The split now resembles a two-track market, with legacy enterprise accounts retaining on-premises deployments while mid-market and newer adopters favor cloud delivery from the start.

Cloud growth is accelerating because platform providers are reducing the compliance tradeoff that once pushed buyers toward local deployment. SAP tied People Intelligence more closely to its cloud data environment in 2025, and Workday expanded live analytics access through its BigQuery integration in late 2025.[2]SAP SE, “Future of Intelligent Applications with SAP Business Data Cloud,” SAP News, news.sap.comThese changes matter for the employee attrition prediction software industry because they make it easier to run predictive workflows without duplicating full data sets or incurring long custom engineering costs. Sovereign-cloud features are also helping vendors address country-specific residency concerns without losing the scale benefits of cloud operations. As more certifications arrive in regulated markets, the balance inside the employee attrition prediction software market is likely to tilt gradually toward cloud deployment, even if on-premises remains important for the largest legacy buyers.

By Organization Size: Enterprise Dominance Masks a Faster SME Ramp

Large enterprises accounted for 70.24% of revenue in 2025, making them the dominant customer segment in the employee attrition prediction software market. Their lead reflects scale advantages in data volume, analytics maturity, and dedicated HR technology budgets, all of which support longer, deeper deployments. Many of these organizations already operate on major HCM platforms, so adding predictive retention tools becomes part of a larger workforce technology program rather than a stand-alone decision. That is why large enterprises still form the commercial core of the employee attrition prediction software market even as buyer diversity expands. Small and medium-sized enterprises are forecast to grow at a 12.67% CAGR through 2031, driven by simpler products that lower setup effort and entry cost.

The SME opportunity is becoming more tangible as vendors design tools around speed and ease rather than deep systems integration. freee K.K. launched freee Survey in December 2025 as an AI attrition prediction product for businesses with fewer than 100 employees, using short surveys to make risk monitoring practical for smaller teams. This matters because smaller firms usually lack the data engineering capacity that large enterprises take for granted. They respond better to lightweight tools that can fit inside an existing HR stack, subscription, or manager routine with limited configuration. Vendors that package attrition prediction inside a broader HRIS offer are therefore likely to win more share in this part of the employee attrition prediction software market than vendors that insist on separate licenses and longer implementation paths.

By End-User Industry: Technology Leads While Healthcare Moves Faster

Information technology and telecommunications accounted for 29.12% of revenue in 2025, giving this sector the largest position in the employee attrition prediction software market. This lead reflects a long-standing combination of higher attrition pressure, stronger internal analytics capability, and faster willingness to test new workforce tools. Technology employers often have internal data teams that can shorten implementation work and help managers trust model output sooner. Those strengths have made the sector a natural early buyer group for the employee attrition prediction software market and a proving ground for many vendor features. The healthcare and life sciences industry is expected to grow at a 11.56% CAGR through 2031, indicating how quickly demand is broadening into industries where labor shortages carry direct service and cost consequences.

The healthcare case is compelling because workforce exits can simultaneously disrupt care quality, scheduling stability, and labor budgets. An analysis published in 2025 estimated that nurse attrition costs the US healthcare system USD 60 billion each year, with attrition rates ranging from 15% to 25% among registered nurses and above 60% for home health aides. Banking, financial services, and insurance are also becoming a stronger user segment as firms connect flight-risk scoring with compensation and pay equity review. Retail and e-commerce, manufacturing, and government adoption are developing more gradually, but each sector has practical reasons to use predictive retention tools when turnover is costly, seasonal, or operationally disruptive. The result is a broader demand base for the employee attrition prediction software market, even though technology remains the most established customer vertical today.

Geography Analysis

North America held 37.22% of the employee attrition prediction software market share in 2025, maintaining its lead. The region benefits from high per-worker turnover costs, a dense vendor base, and enterprise buyers accustomed to adopting analytics tools through formal software procurement channels. The United States remains the center of demand because employers there face high replacement costs and generally operate under more permissive employee data-use practices than many of their European peers. Canada is also progressing, though privacy reform and algorithmic accountability expectations are adding a layer of compliance work that can delay deployment. South America remained at an earlier stage, with Brazil and Chile representing the clearest demand pockets, mostly within multinational organizations extending centrally selected platforms into regional operations.

Europe develops through a different pattern because regulation, labor consultation, and deployment design shape outcomes as much as technology readiness. Germany, the United Kingdom, and France remain the main revenue anchors, but each follows a different adoption path inside the employee attrition prediction software market. Germany stands out because co-determination rules can stretch deployment timelines when works councils are engaged late, and some employers have responded by building models at an aggregated grade level rather than at the individual level. The United Kingdom keeps a modest timing advantage in domestic adoption because its post-Brexit accountability framework does not mirror every EU requirement in the same way.

Asia-Pacific is projected to grow at a 12.34% CAGR through 2031, making it the fastest-growing region in the employee attrition prediction software market. India is benefiting from wider HR technology formalization and from employer demand to turn workforce stability into a sustained operating advantage, especially in global capability center environments. Japan is taking a distinct path, with domestic vendors and technology firms launching products that address labor scarcity and retention pressures. Canon Electronics launched its Retirement Risk Diagnosis Service in March 2026 using PC operation logs as behavioral indicators, and Jinjer announced an attrition alert function scheduled for launch in June 2026.[3]Canon Electronics Inc., “Canon Electronics Retirement Risk Diagnosis Service Launch,” Canon Electronics, canon-elec.co.jp China and South Korea offer scale but remain more challenging for foreign vendors because localization and data control rules shape product architecture and market access. The Middle East is becoming more relevant, led by the UAE and Saudi Arabia, as workforce nationalization and private-sector transformation programs raise interest in retention analytics. Africa is still nascent, but South Africa, Nigeria, and Egypt are showing early signs of adoption as HR digitalization deepens across multinational and larger domestic employers.

Competitive Landscape

The employee attrition prediction software market remains moderately fragmented, with no single vendor dominating the field and several product groups competing simultaneously. Specialist people analytics platforms such as Visier, Eightfold AI, Gloat, and One Model compete against predictive modules inside larger HCM suites from SAP, Workday, and Dayforce. They also face pressure from employee experience platforms such as Culture Amp, Perceptyx, and Leapsome, which are adding predictive scoring features to broader engagement products. This mix means that the employee attrition prediction software market is not decided by feature breadth alone, because buyers also compare deployment speed, model explainability, workflow fit, and evidence of measurable business outcomes. Vendors that can connect a risk score to a manager action inside an existing system often stand out more clearly than vendors that offer a stronger model but keep action separate from day-to-day work.

Strategic moves during 2025 and 2026 show where competition is heading. Visier launched its next-generation Workforce AI platform with Glean MCP integration in April 2026, signaling a push toward an open ecosystem of intelligence in which workforce signals can move across enterprise knowledge environments in real time. Gloat integrated its agentic HR capabilities with Microsoft 365 Copilot and Microsoft Teams in April 2026, which moved retention recommendations closer to the manager workflow and away from stand-alone dashboard use. Eightfold AI also extended its platform through direct integration with Oracle HCM Cloud in May 2026, reinforcing the value of native presence inside established enterprise talent systems.

Investment and partnership activity also points to where future competition may intensify. Darwinbox raised USD 140 million in March 2025 and later secured an additional USD 40 million in August 2025, which strengthened its ability to expand across Asia-Pacific and the Middle East. Workday signed its agreement to acquire Sana in September 2025, extending its position into learning and internal mobility, both of which directly support retention strategy.[4]Workday, “Workday Signs Definitive Agreement to Acquire Sana,” Workday Newsroom, newsroom.workday.com White space remains strongest in sub-100-employee deployments and in compliance-ready configurations for healthcare and financial services, where generic products often fall short on audit needs. Smaller vendors can still disrupt the employee attrition prediction software market if they keep implementation simple, price clearly, and solve narrow customer problems faster than larger suite providers.

Employee Attrition Prediction Software Industry Leaders

Visier, Inc.

Eightfold AI Inc.

Gloat Ltd.

UKG Inc.

Paylocity Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI launched TalentForge, an AI-powered talent intelligence suite expanding its flight-risk and skills-gap capabilities at enterprise scale, signalling continued R&D investment in deep workforce modelling.

- May 2026: Eightfold AI extended its agentic retention and hiring platform through direct integration with Oracle HCM Cloud, enabling attrition prediction signals to surface natively within Oracle talent management workflows.

- April 2026: Visier unveiled its next-generation Workforce AI platform with Glean MCP integration, enabling attrition signals and workforce insights to flow across enterprise knowledge graphs in real time, marking a move toward an open-ecosystem architecture.

- April 2026: Gloat integrated its agentic HR capabilities with Microsoft 365 Copilot and Microsoft Teams, allowing retention recommendations to surface directly in manager workflows without requiring a separate platform login.

Global Employee Attrition Prediction Software Market Report Scope

The Employee Attrition Prediction Software Market encompasses AI-driven tools that are at the forefront of predicting employee turnover. These platforms analyze workforce data, employing predictive modeling and behavioral analysis to pinpoint at-risk employees. By identifying these individuals, organizations can deploy targeted retention strategies, ultimately curbing turnover-related costs. The primary focus of this market is on bolstering workforce stability and enhancing decision-making through advanced predictive intelligence.

The Employee Attrition Prediction Software Market Report is Segmented by Component (Software, and Services [Implementation and Integration Services, Consulting and Advisory Services, and Support and Maintenance Services]), Application (Turnover Prediction and Flight-Risk Scoring, Retention Intervention and Prescriptive Action Planning, Employee Engagement and Sentiment Analytics, Workforce Planning and Internal Mobility Analytics, Compensation, Pay Equity, and Fairness Analytics, and Other Applications), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Information Technology and Telecommunications, Banking, Financial Services, and Insurance, Healthcare and Life Sciences, Retail and E-Commerce, Manufacturing, Government and Public Sector, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Implementation and Integration Services |

| Consulting and Advisory Services | |

| Support and Maintenance Services |

| Turnover Prediction and Flight-Risk Scoring |

| Retention Intervention and Prescriptive Action Planning |

| Employee Engagement and Sentiment Analytics |

| Workforce Planning and Internal Mobility Analytics |

| Compensation, Pay Equity, and Fairness Analytics |

| Other Applications |

| Cloud-Based |

| On-Premises |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Information Technology and Telecommunications |

| Banking, Financial Services, and Insurance |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Manufacturing |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | Implementation and Integration Services | |

| Consulting and Advisory Services | ||

| Support and Maintenance Services | ||

| By Application | Turnover Prediction and Flight-Risk Scoring | |

| Retention Intervention and Prescriptive Action Planning | ||

| Employee Engagement and Sentiment Analytics | ||

| Workforce Planning and Internal Mobility Analytics | ||

| Compensation, Pay Equity, and Fairness Analytics | ||

| Other Applications | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | Information Technology and Telecommunications | |

| Banking, Financial Services, and Insurance | ||

| Healthcare and Life Sciences | ||

| Retail and E-Commerce | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the employee attrition prediction software market?

The employee attrition prediction software market was valued at USD 1.12 billion in 2025, reached USD 1.24 billion in 2026, and is forecast to reach USD 2.12 billion by 2031 at an 11.28% CAGR.

Which application leads revenue in employee attrition prediction software?

Turnover prediction and flight-risk scoring led the application mix with 36.71% revenue share in 2025 because it is the most proven and widely adopted starting point for predictive retention programs.

Why are companies investing more in attrition prediction tools in 2026?

Buyers are reacting to rising turnover costs, stronger finance oversight, and the need to move from passive reporting to continuous retention management tied to manager action and measurable labor savings.

Which deployment model is growing fastest?

Cloud-based deployment is growing fastest at a 13.41% CAGR through 2031, even though on-premises still held 68.41% share in 2025 due to data control and compliance needs among large regulated employers.

Which customer group is expanding fastest by organization size?

Small and medium-sized enterprises are the fastest-growing buyer group, with a 12.67% CAGR through 2031, helped by lighter tools that reduce integration needs and entry cost.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to grow at a 12.34% CAGR through 2031, supported by HR technology formalization in India, domestic product development in Japan, and rising demand across expanding enterprise workforces.

Page last updated on: