Succession Planning Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

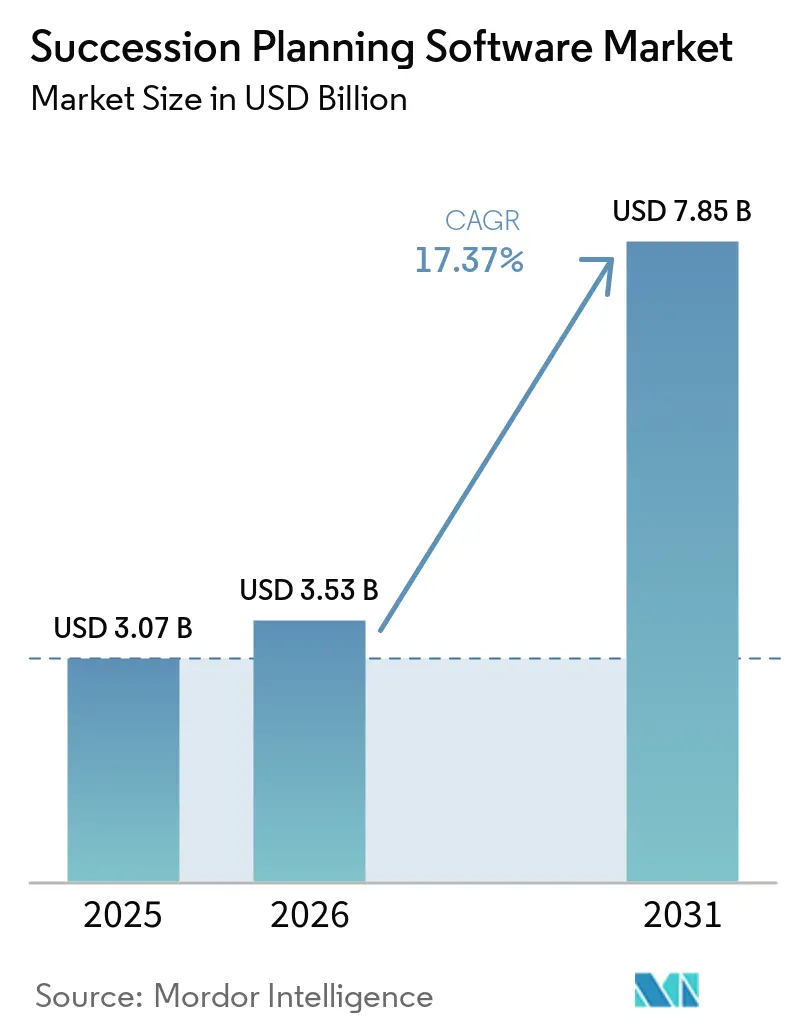

| Market Size (2026) | USD 3.53 Billion |

| Market Size (2031) | USD 7.85 Billion |

| Growth Rate (2026 - 2031) | 17.37% CAGR |

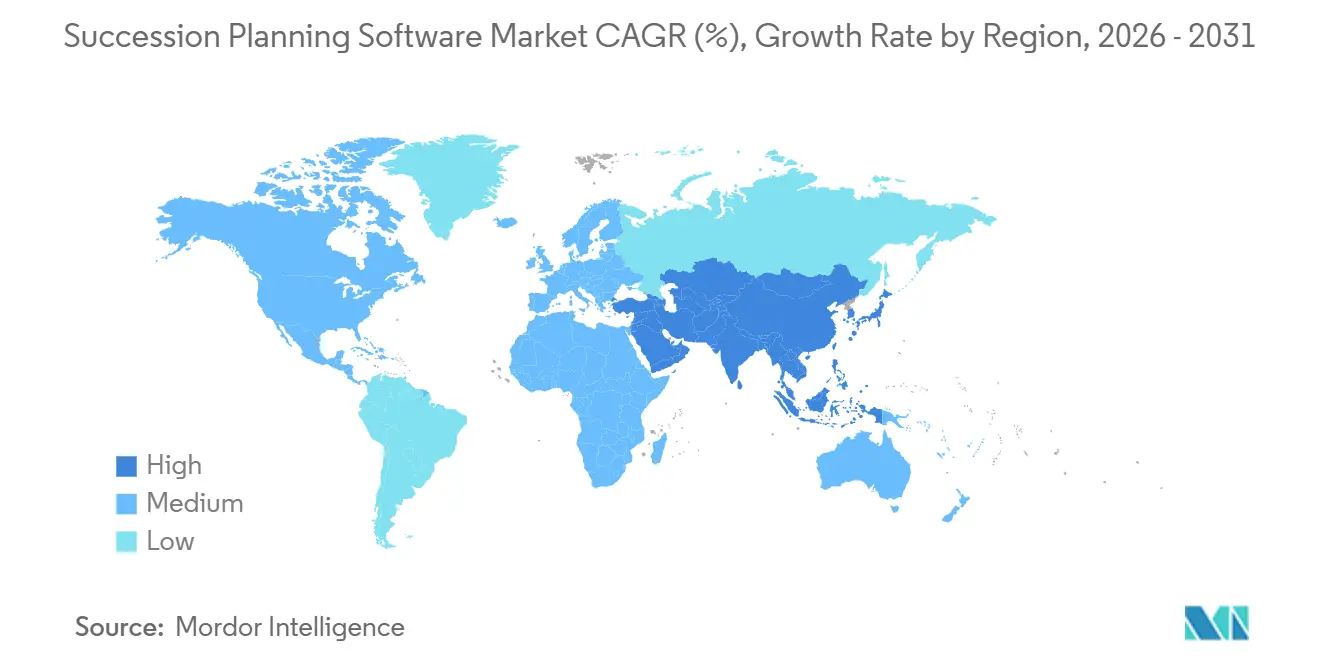

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Succession Planning Software Market Analysis by Mordor Intelligence

The succession planning software market size was valued at USD 3.07 billion in 2025 and estimated to grow from USD 3.53 billion in 2026 to reach USD 7.85 billion by 2031, at a CAGR of 17.37% during the forecast period (2026-2031). Cloud-native delivery, AI-driven talent analytics, and skills-based workforce models are expanding procurement budgets, while regulatory mandates in banking, healthcare, and government accelerate platform adoption. Large enterprises continue to dominate spending, yet small and medium-sized companies are closing the gap as vendors launch affordable subscription bundles. Competitive intensity is moderate because the top five vendors bundle succession with broader human capital suites, although AI-first challengers are winning mid-market deals through faster innovation cycles. Data privacy enforcement and macroeconomic volatility remain the chief headwinds to sustained growth.

Key Report Takeaways

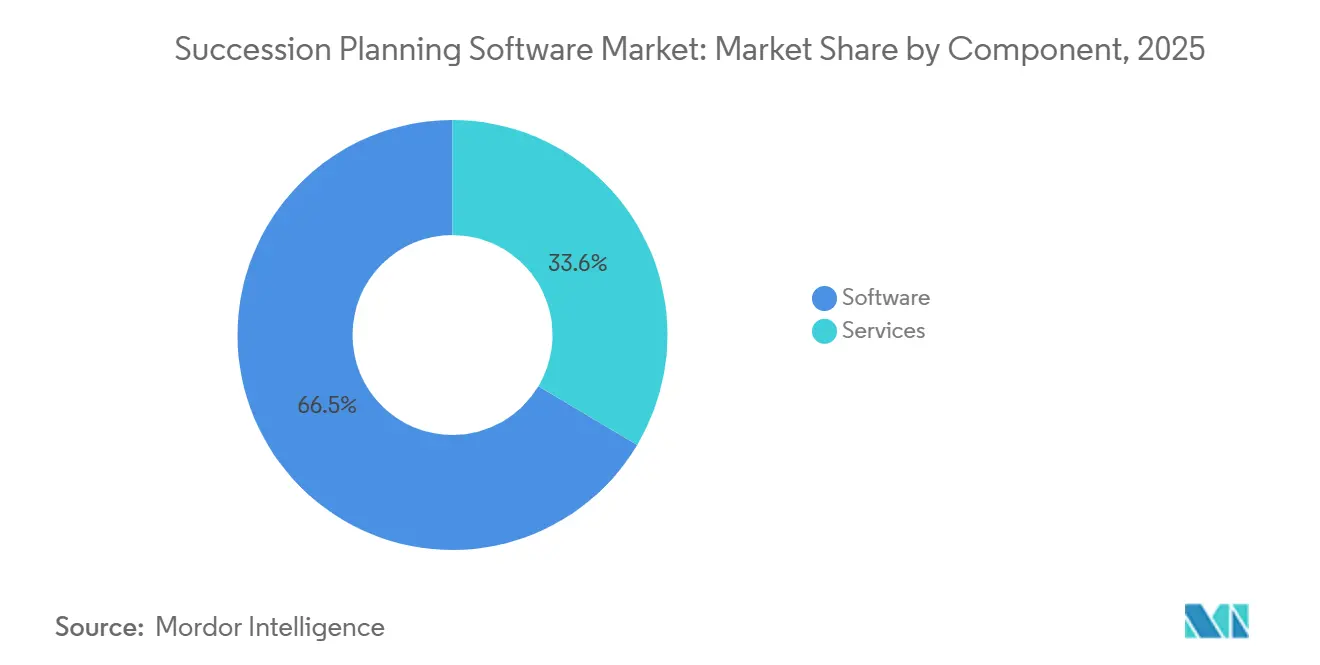

- By component, software commanded 66.45% revenue share of the succession planning software market in 2025, whereas services are advancing at a 19.23% CAGR through 2031.

- By deployment model, on-premises installations held 60.21% of the succession planning software market share in 2025, but cloud platforms are expanding at a 20.01% CAGR to 2031.

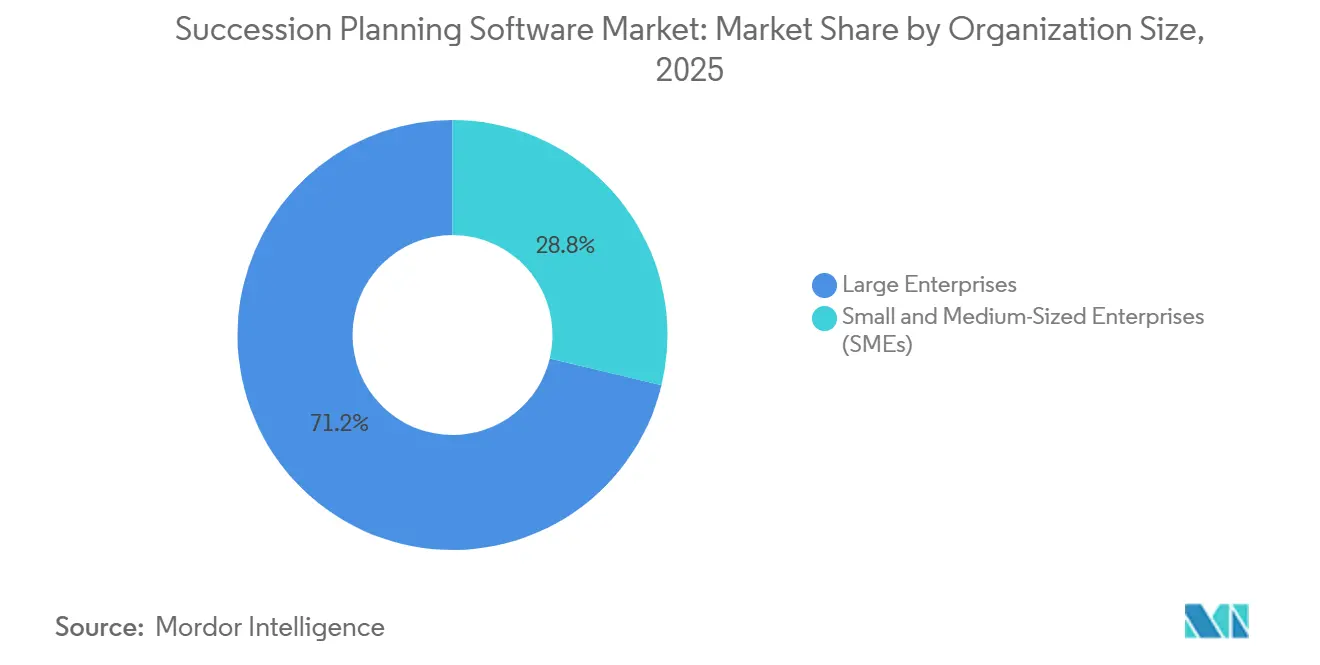

- By organization size, large enterprises accounted for 71.24% of succession planning software market size in 2025, while the small and medium-sized segment is projected to rise at a 19.62% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance led with 28.44% share in 2025, and healthcare is pacing the field with an 18.45% CAGR to 2031.

- By geography, North America represented 37.89% of 2025 revenue, whereas Asia-Pacific is set to grow at an 18.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Succession Planning Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of AI-Driven Talent Analytics | +4.2% | Global, early concentration in North America and Western Europe | Medium term (2-4 years) |

| Rising Demand for Internal Mobility Amid Skills Shortages | +3.8% | Global, particularly acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| Increasing Compliance Pressures for Leadership Continuity Planning | +2.9% | North America and EU, expanding to BFSI and government sectors globally | Long term (≥ 4 years) |

| Growing Shift Toward Cloud-Native HR Tech Stacks | +3.5% | Global, led by North America, Asia-Pacific, and South America | Medium term (2-4 years) |

| Expansion of Remote and Hybrid Work Models Requiring Digital Succession Processes | +2.1% | Global, strongest in technology and professional services sectors | Short term (≤ 2 years) |

| Integration of Succession Planning With Broader Talent Management Suites | +1.8% | North America and Europe, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of AI-Driven Talent Analytics

Artificial intelligence is transforming succession programs by converting episodic reviews into continuous talent intelligence. Modern platforms combine performance data, skills assessments, and peer feedback to create real-time succession heat maps that uncover flight risks months in advance, cutting time-to-fill for critical roles by 30% and boosting internal promotions by 18%. SAP embedded the Joule AI copilot in 2025 so managers can query succession scenarios in plain language, illustrating how conversational analytics hasten decision cycles. These capabilities carry particular weight in healthcare and manufacturing, where external hiring often struggles to match niche skill requirements.

Rising Demand for Internal Mobility Amid Skills Shortages

Tight labor markets have elevated internal mobility from a retention tactic to an enterprise strategy. The Australian Public Service Commission reported that 88% of agencies faced critical skills gaps in 2025, prompting urgent investment in tools that surface internal candidates before vacancies hit job boards. Fuel50’s Skills Growth Predictive Model, launched in March 2026, forecasts future competency needs and recommends individual learning paths that prepare employees for leadership years in advance. Organizations emphasizing internal mobility record 41% longer tenure and 25% higher engagement scores, figures that strengthen the business case for succession platforms that automate career pathing.

Increasing Compliance Pressures for Leadership Continuity Planning

Governance lapses in financial services have spurred auditors to treat documented succession plans as part of internal-control audits under the Sarbanes-Oxley Act, while European regulators now fold workforce planning metrics into sustainability disclosures. U.S. federal agencies must maintain succession frameworks for Senior Executive Service roles, a rule that is fueling platform deployments across government departments. A Spencer Stuart study showed that only one-third of companies kept formal CFO succession plans even though 22% of CFOs moved into the CEO seat, highlighting a compliance gap that software is designed to close.

Growing Shift Toward Cloud-Native HR Tech Stacks

Cloud deployments are growing at a 20.01% CAGR because they remove capital expense, accelerate updates, and allow mobile access, advantages magnified by hybrid workforces. ADP’s USD 1 billion acquisition of WorkForce Software in 2024 underscored vendor urgency to own cloud-native stacks that merge scheduling, payroll, and succession workflows.[1]ADP, “WorkForce Software Acquisition and Lyric HCM Platform Launch,” adp.com Retailers such as Coles Group reported faster onboarding and improved data integrity after integrating OpenText’s cloud solution with SAP SuccessFactors in 2025. Security certifications-SOC 2 Type II and ISO 27001-have quelled data-protection concerns, pulling even highly regulated sectors toward software-as-a-service.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Security Concerns in Talent Profiles | -2.4% | EU and North America, expanding to Asia-Pacific with new regulations | Medium term (2-4 years) |

| Resistance to Change From Traditional HR Practices | -1.9% | Global, strongest in manufacturing and government sectors | Long term (≥ 4 years) |

| Limited Skilled Administrators to Manage Advanced Platforms | -1.3% | Global, particularly acute in SMEs and emerging markets | Medium term (2-4 years) |

| Economic Uncertainty Causing HR Tech Spending Delays | -1.6% | Global, cyclical impact tied to macroeconomic conditions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Security Concerns in Talent Profiles

Succession tools store sensitive employment data that triggers strict consent and retention rules under the GDPR and the California Consumer Privacy Act. Regulators issued EUR 2.1 billion (USD 2.3 billion) in GDPR fines during 2024, causing 34% of HR leaders to pause platform deployments until governance models mature. Vendors now embed privacy-by-design features such as role-based access controls and pseudonymization, yet many small enterprises lack the legal resources to navigate multi-country compliance regimes.

Resistance to Change From Traditional HR Practices

Organizational inertia remains pronounced in industries with hierarchical cultures, where annual spreadsheet reviews still substitute for data-driven pipelines. The International City/County Management Association found that many local governments confront mass retirements without formal succession frameworks, a gap that software alone cannot bridge without executive sponsorship. Fear of transparency also slows uptake because real-time dashboards expose talent gaps to boards and investors, increasing accountability for leadership decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Implementation Complexity Rises

Software retained 66.45% of the succession planning software market in 2025, confirming that platform licenses still form the revenue core. Implementation challenges, however, are steering more contracts toward advisory partners that configure AI models and integrate legacy data, a shift that explains the 19.23% CAGR forecast for services. Enterprises facing multivendor human capital ecosystems often route deployments through global systems integrators, which now bundle change-management workshops alongside technical tasks. These value-added packages help vendors defend account stickiness as customers modernize talent workflows.

Managed services appeal to mid-market firms that lack in-house analytics staff, allowing providers to monitor data hygiene and deliver quarterly leadership pipeline reports. The succession planning software market size for managed offerings is projected to rise at double-digit rates through 2031, reflecting demand for subscription economics aligned with operating budgets. Niche consultancies have responded with fixed-price playbooks that compress launch timelines from months to weeks, thereby reducing disruption to ongoing performance reviews. This service-led momentum should continue as boards request more frequent bench-strength updates.

By Deployment Model: Cloud Overtakes Legacy On-Premises Installs

On-premises deployment accounted for 60.21% succession planning software market share in 2025 because many large enterprises still run talent modules inside older human capital suites. Yet cloud subscriptions are scaling at a 20.01% CAGR thanks to automatic updates, lower capital expense, and mobile access, benefits that resonate with hybrid workforces. Vendors that achieve SOC 2 Type II and ISO 27001 certifications now ease security objections that once anchored workloads on local servers. As a result, new buyers rarely request perpetual licenses.

The succession planning software market size for cloud platforms is expected to surpass on-premises revenue before 2031, a crossover driven by small and medium-sized enterprises prioritizing rapid implementation. API-enabled integration lets HR leaders stitch succession dashboards into recruiting, learning, and compensation systems in days rather than months. Hybrid architectures remain a transitional model in heavily regulated industries, keeping sensitive personal data on-site while pushing analytics workloads to the cloud. However, analysts agree that cloud-first procurement language is now standard in most RFPs.

By Organization Size: SMEs Embrace Affordable Cloud Modules

Large enterprises generated 71.24% of 2025 revenue because complex governance mandates require feature-rich platforms tightly woven into finance and compliance workflows. Still, the small and medium-sized cohort is expanding at a 19.62% CAGR, making it the fastest-growing slice of the succession planning software market. Lower per-employee pricing tiers, templated workflows, and no-code configuration tools remove historical cost and skill barriers. Family-owned firms eyeing generational transfers find these lightweight options especially useful.

Vendors target the segment with starter bundles that combine career pathing, succession mapping, and learning playlists for less than USD 10 per employee per month. The succession planning software industry has responded by adding in-product guidance, reducing reliance on certified administrators. As a result, many SMEs can publish their first succession heat map within two weeks of contract signature, accelerating time-to-value. This democratization expands the addressable user base beyond Fortune 1000 organizations.

By End-User Industry: Healthcare Surges as Physician Shortages Intensify

Banking, financial services, and insurance captured 28.44% of 2025 revenue because regulators expect documented leadership pipelines for risk-critical roles. Yet healthcare shows the highest trajectory, advancing at an 18.45% CAGR as hospitals confront looming physician gaps and elevated clinical turnover. Automated succession mapping identifies high-performing nurses and mid-level practitioners for leadership tracks, curbing reliance on costly locum tenens staffing. Skill-centric analytics also pinpoint where continuing education investments yield the greatest bench-strength gains.

Technology companies remain heavy adopters, given the pace at which cloud, cybersecurity, and data-science roles evolve. Manufacturing firms face knowledge loss as veteran engineers exit, pushing them toward platforms that codify tacit process know-how before retirement. Government departments respond to civil-service mandates by standardizing pipeline metrics across agencies, a practice that feeds comparative analytics. Collectively, these vertical dynamics diversify the succession planning software market, reducing overreliance on any single sector.

Geography Analysis

North America led the succession planning software market with a 37.89% share in 2025, supported by Sarbanes-Oxley governance rules and a dense vendor ecosystem. Public corporations routinely disclose board-level pipeline metrics, which normalizes platform spending across industries. Canada mirrors the trend as federal policies demand continuity plans for critical functions, and Mexico’s outsourcing hubs adopt standardized HR frameworks to serve multinational clients. This foundation gives regional suppliers strong renewal rates.

Asia-Pacific is projected to post an 18.96% CAGR, making it the fastest-growing territory within the succession planning software market. Digital HR transformation across India and China is accelerating because cloud infrastructure costs keep falling, while Australia’s public agencies actively seek tools that address nationwide skill shortages.[2]Australian Public Service Commission, “State of the Service Report 2024-25: Critical Skills Shortages Across Federal Agencies,” apsc.gov.au Japan’s aging workforce intensifies knowledge-transfer needs, prompting large conglomerates to replace manual mentorship schemes with analytics-driven succession dashboards. Local payroll and labor-law integrations remain table stakes for market entry. Vendors that secure data-residency assurances win faster procurement cycles.

Europe maintains steady uptake anchored in Germany, the United Kingdom, and France, where the Corporate Sustainability Reporting Directive elevates workforce planning to ESG disclosures. South America shows mixed momentum: Brazil’s banks invest steadily, but currency swings can slow project approvals elsewhere. The Middle East and Africa contribute niche demand driven by government diversification agendas, particularly in the United Arab Emirates and Saudi Arabia. Hybrid hosting models offer a bridge until regional data-protection frameworks mature.

Competitive Landscape

The succession planning software market shows moderate concentration, with SAP, Oracle, Workday, UKG, and Cornerstone securing roughly half of 2025 revenue. These incumbents retain clients by bundling succession modules inside end-to-end human capital suites that already anchor payroll, performance, and learning workflows, thereby inflating switching costs. They also extend multiyear enterprise agreements that lock pricing and guarantee roadmap influence. Nonetheless, AI-first specialists such as Gloat, Eightfold, Fuel50, and Degreed court mid-market enterprises with rapid feature releases focused on skills intelligence.

Platform mergers continue as vendors race to unify talent acquisition, development, and succession analytics. Phenom’s January 2026 takeover of Included for people analytics augments predictive attrition scores and diversity metrics that resonate with chief human resources officers. UKG’s planned integration of Inova Payroll widens payroll reach into the small and medium-sized segment, helping its suite compete on breadth. Such deals validate the thesis that embedded analytics drive renewal decisions more than core feature parity.

Vendors that preconfigure workflows for healthcare credentialing or manufacturing apprenticeships compress deployment timelines, letting clients avoid costly custom development. Platforms that embed generative AI to draft development plans and recommend learning content are winning evaluations against legacy systems. The shift toward skills-based workforce architectures is creating demand for platforms that integrate with learning management systems, as demonstrated by Fuel50's March 2026 Skills Growth Predictive Model.[3]Fuel50, “Skills Growth Predictive Model Launch Announcement,” fuel50.com Compliance modules that automate GDPR and CCPA controls are now baseline functionality because data-protection fines can dwarf annual subscription fees.

Succession Planning Software Industry Leaders

SAP SE

Oracle Corporation

Workday Inc.

UKG Inc.

ADP Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: HiBob launched “In Good Company Chapters,” a global HR community for peer learning on succession planning and analytics.

- March 2026: Fuel50 introduced its Skills Growth Predictive Model, integrating future skill forecasts into existing succession modules.

- January 2026: Fuel50 enhanced career pathing with role recommendations drawn from skills adjacency maps.

- January 2026: Phenom acquired Included to add AI-powered people analytics across the talent lifecycle.

Global Succession Planning Software Market Report Scope

The Succession Planning Software Market focuses on identifying, evaluating, and grooming employees for future leadership and pivotal roles within organizations. Centralizing competency frameworks, talent pools, and leadership assessments, these systems aid organizations in mitigating leadership pipeline risks, bolstering continuity planning, and aligning developmental investments with strategic goals. The market's growth is bolstered by demographic shifts in the workforce, a surge in executive turnover, and a heightened emphasis on internal mobility.

The Succession Planning Software Market Report is Segmented by Component (Software, and Services), Deployment Model (On-Premises, and Cloud-Based), Organization Size (Small and Medium-Sized Enterprises [SMEs], and Large Enterprises), End-User Industry (Banking, Financial Services, and Insurance [BFSI], Healthcare, Information Technology and Telecom, Manufacturing, Education, Government, and Other End-User Industry), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Talent Identification and Assessment Software |

| Succession Planning and Role Mapping Software | |

| Career Pathing and Development Planning Software | |

| Leadership Development and Readiness Software | |

| Workforce Analytics and Talent Intelligence Software | |

| Other Software | |

| Services |

| On-Premises |

| Cloud-Based |

| Small and Medium-Sized Enterprises (SMEs) |

| Large Enterprises |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare |

| Information Technology and Telecom |

| Manufacturing |

| Education |

| Government |

| Other End-User Industry |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Talent Identification and Assessment Software |

| Succession Planning and Role Mapping Software | ||

| Career Pathing and Development Planning Software | ||

| Leadership Development and Readiness Software | ||

| Workforce Analytics and Talent Intelligence Software | ||

| Other Software | ||

| Services | ||

| By Deployment Model | On-Premises | |

| Cloud-Based | ||

| By Organization Size | Small and Medium-Sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-User Industry | Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare | ||

| Information Technology and Telecom | ||

| Manufacturing | ||

| Education | ||

| Government | ||

| Other End-User Industry | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current succession planning software market size and projected growth?

The succession planning software market size is USD 3.53 billion in 2026 and is forecast to reach USD 7.85 billion by 2031, expanding at a 17.37% CAGR (Mordor Intelligence).

Which deployment model is growing fastest?

Cloud-native deployment leads growth, rising at a 20.01% CAGR through 2031 as enterprises shift from perpetual licenses to subscription models.

Which industry shows the highest adoption momentum after BFSI?

Healthcare posts the fastest growth at an 18.45% CAGR because physician shortages and regulatory pressures elevate leadership pipeline planning.

Why are small and medium-sized enterprises accelerating adoption?

Affordable subscription bundles under USD 10 per employee per month and no-code configuration shorten implementation to weeks, making advanced succession tools accessible to SMEs.

How do AI features improve succession outcomes?

AI-driven talent analytics cut time-to-fill for critical roles by 30% and raise internal promotion rates by 18% by spotting flight risks and recommending skills-based development paths.

Page last updated on: