Contract Lifecycle Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

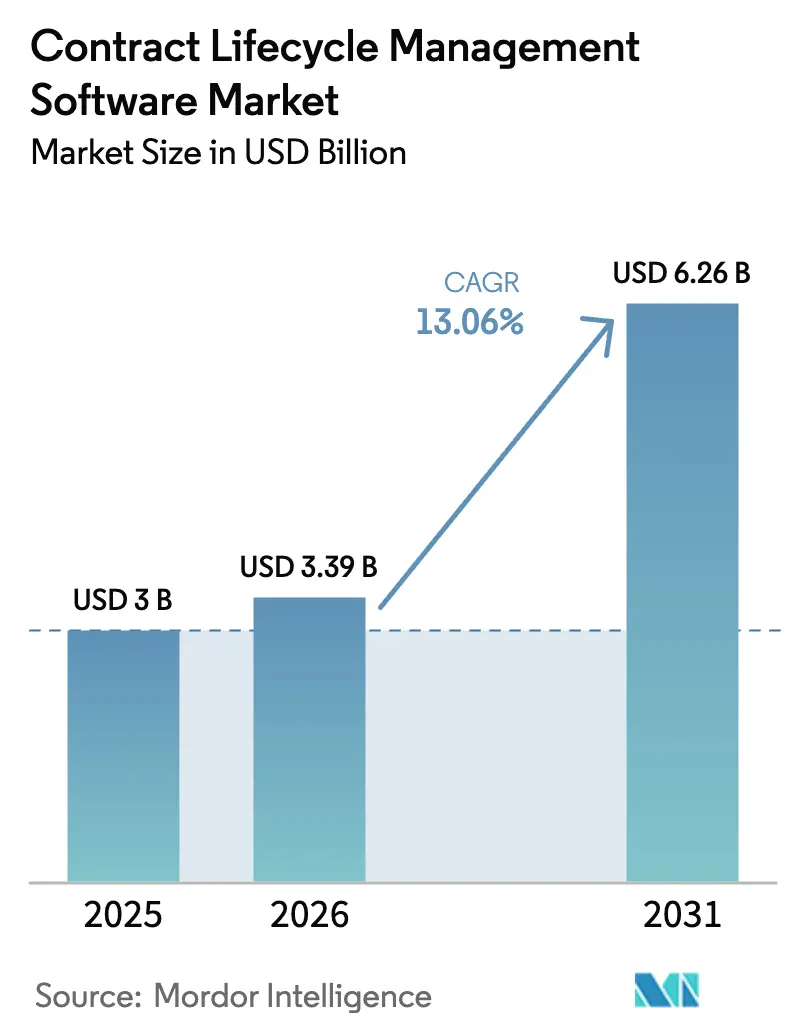

| Market Size (2026) | USD 3.39 Billion |

| Market Size (2031) | USD 6.26 Billion |

| Growth Rate (2026 - 2031) | 13.06% CAGR |

| Fastest Growing Market | North America |

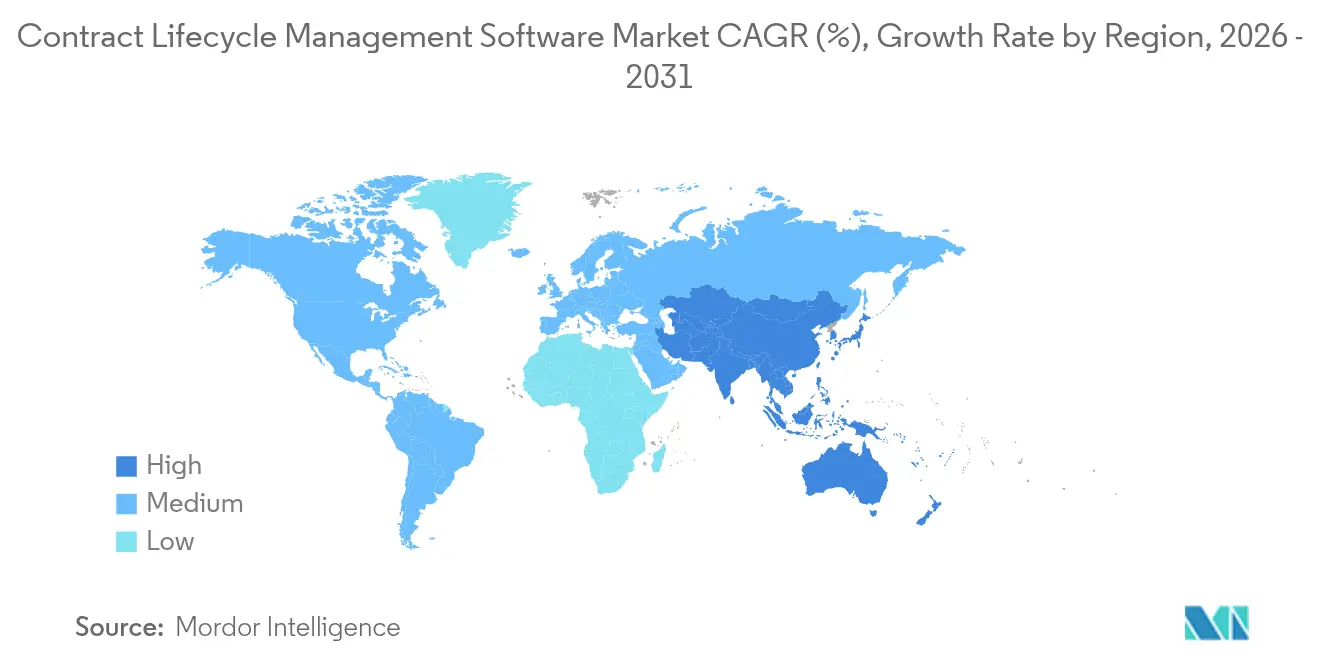

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Contract Lifecycle Management Software Market Analysis by Mordor Intelligence

Contract lifecycle management market size in 2026 is estimated at USD 3.39 billion, growing from 2025 value of USD 3.0 billion with 2031 projections showing USD 6.26 billion, growing at 13.06% CAGR over 2026-2031. Strong demand stems from the switch to AI-driven automation that extracts business intelligence buried in legal documents, stricter ESG-linked disclosure rules, and a widespread need to eliminate manual contract bottlenecks.[1]Federal Register, “Agency Information Collection Activities; Electronic Records: Electronic Signatures,” federalregister.gov North America leads current revenue, yet accelerating government digital programs in the Asia-Pacific region and rapid hybrid-cloud adoption globally keep growth broad-based. Intensifying compliance duties push enterprises to deploy systems that guarantee audit-ready trails while real-time analytics modules convert contracts into decision-support assets. Market momentum is also buoyed by rising remote-work requirements that prioritize mobile approvals and encrypted cloud collaboration. Consolidation is underway, illustrated by DocuSign’s USD 165 million purchase of Lexion in 2024 to deepen generative-AI capabilities.

Key Report Takeaways

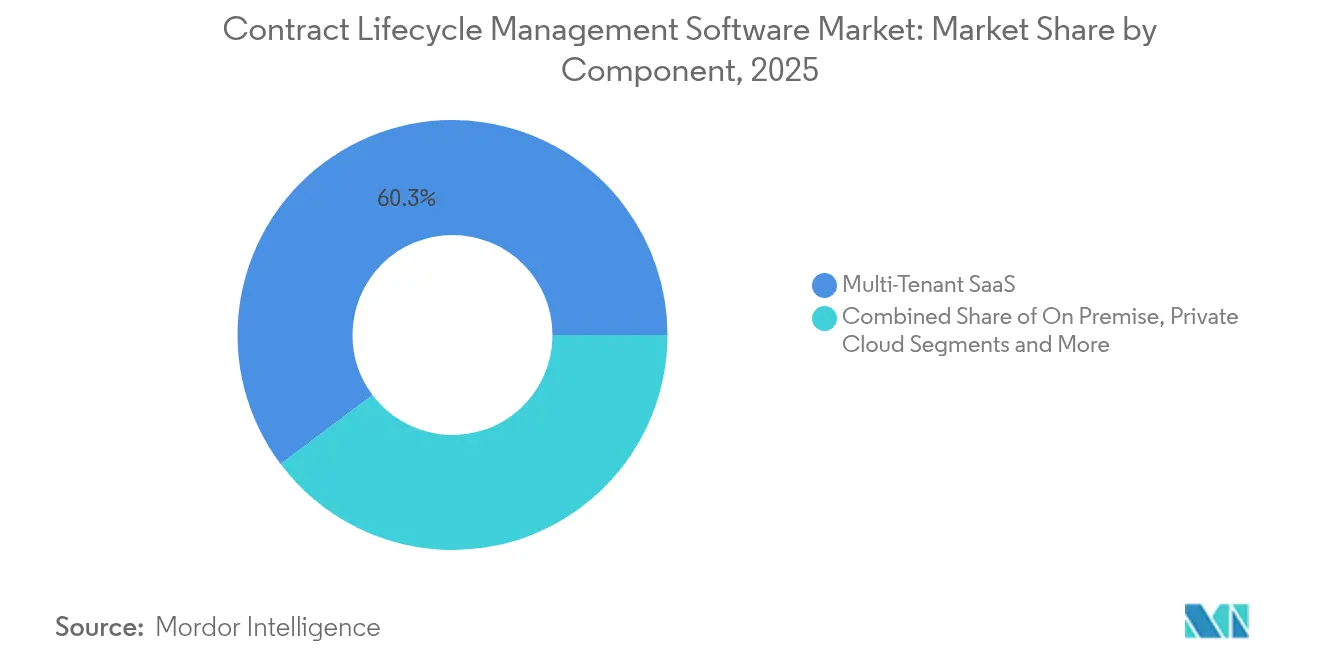

- By deployment type, multi-tenant SaaS held 60.25% of the contract lifecycle management market share in 2025, while hybrid models are projected to expand at a 17.15% CAGR through 2031.

- By organization size, large enterprises led with 58.30% revenue share in 2025; small and medium enterprises are on track for a 15.1% CAGR to 2031.

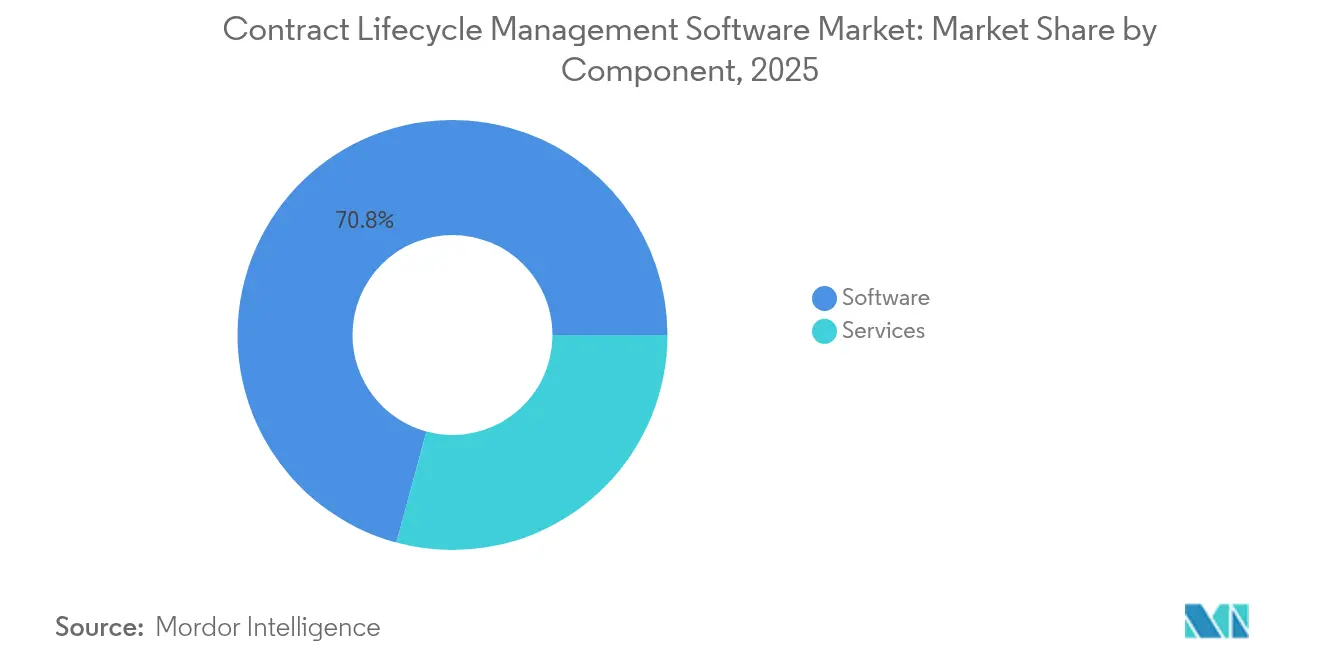

- By component, software accounted for 70.80% of the contract lifecycle management market size in 2025 and services are growing at 18.2% CAGR.

- By end-user industry, BFSI commanded 22.45% share of the contract lifecycle management market size in 2025; energy and utilities is advancing at a 18.6% CAGR to 2031.

- By geography, North America captured 41.40% of the contract lifecycle management market share in 2025, while Asia-Pacific records the fastest growth at 16.7% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Contract Lifecycle Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened regulatory scrutiny & audit readiness | +2.8% | North America, EU | Medium term (2–4 years) |

| Enterprise digital-transformation mandates | +3.2% | APAC, North America | Long term (≥ 4 years) |

| Accelerating remote & hybrid work models | +1.9% | Developed markets | Short term (≤ 2 years) |

| AI-powered clause extraction efficiency | +2.6% | North America, EU | Medium term (2–4 years) |

| ESG-linked contract-obligation tracking | +1.8% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Regulatory Scrutiny & Audit Readiness

Mandatory net-zero procurement rules and electronic-records legislation are reshaping contract governance. The Federal Sustainability Plan compels federal contractors exceeding USD 50 million in awards to disclose greenhouse-gas metrics within agreements, triggering demand for audit-ready CLM platforms. FDA acceptance of electronic signatures further validates digital records, and adopters report up to 50% shorter audit-prep cycles after centralizing contracts.[2]Cyient. "Cyient Success Story." As overlapping frameworks multiply, manual tracking proves unsustainable, cementing systematic CLM uptake.

Enterprise Digital-Transformation Mandates

Large-scale modernization programs insist that contract data travel seamlessly into ERP, procurement, and analytics suites. The UK government’s GBP 144.3 million Matrix Programme exemplifies how back-office SaaS drives integrated agreement workflows find.[3]Department for Science, Innovation & Technology. "Matrix Programme - Technology (including ERP) & Systems Integration Services." DocuSign’s FY 2024 revenue of USD 2.8 billion highlights enterprise appetite for platforms converting agreements into live performance dashboards. As outcome-based contracting rises, organizations prioritize CLM systems that surface obligations to finance, supply-chain, and operations teams in real-time.

Accelerating Remote & Hybrid Work Models

Distributed workflows expose paper-based weaknesses, pushing firms toward browser-based authoring, mobile approvals, and e-signature modules. Legal teams dispersed across time zones cite difficulties in spreadsheet tracking, whereas centralized CLM tools deliver automated alerts and encrypted repositories that safeguard sensitive terms. Heightened security requirements favor platforms with FedRAMP or StateRAMP credentials, ensuring compliance when staff collaborate outside corporate networks.

AI-Powered Clause Extraction Boosting Cycle-Time Efficiency

Generative AI is shortening review cycles by auto-identifying risk clauses and suggesting standardized language. USPTO guidance released in April 2024 gives legal teams confidence to deploy AI in document workflows.[4]United States Patent and Trademark Office, “Guidance on Use of Artificial Intelligence-Based Tools,” uspto.gov DocuSign leveraged its Lexion purchase to embed natural-language models that slash turnaround on repeatable contracts by up to 60%, freeing counsel for higher-value negotiations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation & Change-Management Costs | -1.4% | Worldwide, hitting smaller firms hardest | Short term (≤ 2 years) |

| Data-Security & Privacy Concerns in Multi-Tenant SaaS | -0.9% | Worldwide, especially in EU and heavily regulated sectors | Medium term (2–4 years) |

| Inconsistent contracting rules across borders | -0.7% | Worldwide, but most acute in cross-border deals | Long term (≥ 4 years) |

| Unclear regulations for AI-driven legal tech | -0.6% | Worldwide, starting to bite in North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Implementation & Change-Management Costs

Up-front migration, user training, and integration expenses weigh especially on smaller companies. Projects stall when underestimated resource needs collide with tight IT budgets, delaying the broader roll-out of contract lifecycle management market solutions. Continuous updates further strain finances until platforms mature and best-practice blueprints reduce custom work.

Data-Security & Privacy Concerns in Multi-Tenant SaaS

Sensitive pricing terms and IP heighten caution toward shared-cloud architectures. EU data-residency mandates and sector-specific rules in healthcare and finance compel some buyers to favor hybrid or private-cloud deployments until providers attain sector certifications and granular tenant-level encryption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Models Bridge Security and Scalability

Multi-tenant SaaS still dominated 60.25% of 2025 revenue, proving that affordability and rapid onboarding remain compelling. Yet the hybrid subset now posts a 17.15% CAGR, reflecting a preference to keep regulated data on-premises while tapping cloud analytics. Federal-level StateRAMP credentials awarded to leading vendors reassure agencies about security, enabling gradual migration. Enterprises thus tailor storage locations according to contract sensitivity, a flexibility that strengthens the contract lifecycle management market’s overall growth path.

The trend follows early lessons from all-cloud initiatives that ran into latency and sovereignty issues. Modern hybrid stacks use containerized micro-services and API gateways so that workflow engines operate in the cloud even as PDFs reside behind firewalls. Vendors that offer customers this mix are widening their installed base and bolstering renewal rates.

By Organization Size: SMEs Drive Democratization Through Simplified Platforms

Large enterprises captured 58.30% of 2025 revenue thanks to complex global portfolios and integration-heavy rollouts, anchoring the contract lifecycle management market. SMEs, however, register a 15.1% CAGR to 2031, indicating that intuitive UI, subscription pricing, and no-code configuration are lowering entry barriers. Small firms capitalize on ready-made templates and rule-based alerts that slash administrative overhead.

While Fortune 500 deployments still require multiyear projects that sync with ERP, CRM, and procurement suites, mid-market customers prioritize immediate visibility into renewal dates and obligations. Vendors now offer packaged connectors to popular accounting tools, aligning with CFO priorities and broadening the addressable contract lifecycle management industry user base.

By Component: Analytics Transform Contracts into Business Intelligence

In 2025, software still represented the bulk of contract-lifecycle-management spending at 70.80% of total market value. The spotlight, however, has shifted to services, which are expanding at a 18.2% CAGR through 2031 as organizations look for faster cycle-time visibility, stronger risk controls, and clearer insights into supplier performance.

Much of this momentum comes from implementation, integration, and AI-tuning projects. Generative-AI layers that forecast renewals and trigger automatic risk alerts are usually delivered through service-led engagements rather than as off-the-shelf add-ons. Providers that back their platforms with specialists who can weave contract data into enterprise systems, expose it through REST APIs, and tailor analytics to each client’s needs are pulling ahead of vendors that concentrate only on license sales.

By End-User Industry: Energy Sector Leads Growth Through Complex Agreement Management

BFSI retained a 22.45% slice of 2025 spending due to stringent audit needs and sunshine-act reporting. Yet the energy and utilities vertical is accelerating at 18.6% CAGR as renewable PPAs, carbon credit ledgers, and grid interconnection clauses require granular governance. Healthcare, manufacturing, and public sector projects also intensify, each driven by its own compliance lattice.

Leading vendors now bundle clause libraries fine-tuned for power-purchase agreements and tariffs, ensuring quick time-to-value. This specialization cements cross-sell opportunities inside the contract lifecycle management market when utilities expand into new geographies or procurement models.

Geography Analysis

North America contributed 41.40% of 2025 revenue, anchored by mature SaaS acceptance and strict disclosure mandates. Federal sustainability rules necessitate carbon-tracking clauses, helping agencies justify platform investments that feed data into procurement dashboards. High merger activity among vendors accelerates functional breadth, reinforcing the region’s leadership position.

Asia-Pacific is the fastest-growing region at 16.7% CAGR through 2031. The Asian Development Bank reports that 47% of funded digital projects now embed AI components, a trend that underpins record CLM adoption across infrastructure and public-service initiatives. Government stimulus, combined with data-privacy regulations in India and Indonesia, encourages hybrid deployments tailored to local residency rules, driving spend without compromising compliance.

Europe sustains sizable demand as GDPR and the forthcoming Corporate Sustainability Due Diligence Directive compel multinationals to implement supply-chain clause tracking. SAP’s EUR 13.66 billion 2023 cloud revenue illustrates enterprises funding integrated platforms that house CLM alongside analytics sap.com. Brexit adds further complexity, prompting UK public-sector bodies to commission digital-strategy partners for procurement modernization.

Competitive Landscape

Fragmentation persists with roughly 150–200 providers, yet mergers signal rising concentration. DocuSign’s Lexion buy is the latest in a string of AI-centric deals intended to fuse NLP, risk scoring, and workflow orchestration under one roof. Only 55% of corporate legal teams run CLM today, implying vast green-field momentum that favors platforms offering turnkey integrations and robust security.

Vendors differentiate through verticalized content—energy clause packs, healthcare value-based templates, or public-sector regulatory mappings. Patent data indicates a surge in blockchain-anchored contract verification filings as developers explore tamper-evident audit logs. Leaders with open-API ecosystems and AI-governance controls are widening their moat, whereas single-purpose point tools risk marginalization.

Investment in partner marketplaces also rises. Providers certify SI firms to accelerate rollouts, expanding addressable opportunities especially among mid-market buyers seeking rapid time-to-value. As price competition tightens for base e-signature modules, vendors bundle analytics dashboards at no extra cost to preserve recurring ARPU.

Contract Lifecycle Management Software Industry Leaders

-

ContractWorks, Inc.

-

Zycus Inc.

-

Concord, Inc.

-

Contract Logix, LLC

-

GEP, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Asian Development Bank launched Digital Development Facility Phase 2 with USD 1 million funding to mainstream AI and big data, benefiting public-sector contract modernization

- May 2024: DocuSign finalized its USD 165 million acquisition of Lexion, adding advanced NLP and automated risk assessment to its cloud suite

- April 2024: DocuSign introduced the Intelligent Agreement Management platform, positioning the product as a new SaaS category centered on AI-orchestrated contracts

- April 2024: USPTO released guidance on using AI in legal document practice, providing frameworks that extend to CLM software

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the contract lifecycle management (CLM) software market as packaged or SaaS platforms that digitize, automate, and track the authoring, negotiation, storage, renewal, and analytics of buy-side and sell-side contracts. We count vendor revenue from licenses or subscriptions together with implementation, integration, and training services that accompany the platform.

Scope Exclusions: Stand-alone e-signature utilities, generic document repositories, and one-off custom-coded projects are excluded.

Segmentation Overview

-

By Type of Deployment

- On-premise

- Cloud

-

By Oranization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

-

By End-user Industry

- BFSI

- Government

- Healthcare

- Retail

- Manufacturing

- IT and Telecom

- Other End-user Industries

-

By Geography***

- North America

- Europe

- Asia

- Australia and New Zealand

- Latin America

- Middle East and Africa

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed product managers, procurement heads, in-house counsels, and system integrators in North America, Europe, Asia-Pacific, and the Middle East. These conversations confirmed adoption triggers, tuned average selling prices, and flagged regional deployment lags that documents rarely reveal.

Desk Research

We began by pairing public indicators, U.S. Bureau of Labor Statistics corporate-legal staffing, Eurostat ICT-adoption surveys, and UN Comtrade exports of packaged software with the potential demand pool. Inputs from the International Association for Contract & Commercial Management and the Cloud Security Alliance refined average contract volumes and security spend. Company 10-Ks, investor decks, Questel patent counts, plus revenue breadcrumbs from D&B Hoovers and Dow Jones Factiva helped Mordor analysts benchmark price bands and innovation pace. The cited sources are illustrative; many other references guided validation.

Market-Sizing & Forecasting

We employ a top-down build that starts with global enterprise-application spend, filters it through contract-intensive sectors, SaaS penetration, and CLM spend ratios, then cross-checks totals with selective bottom-up vendor roll-ups. Core variables include contracts per employee, cloud share, median subscription fee, AI attach rates, and compliance-intensity scores. A multivariate regression projects these drivers to 2030, while scenario analysis bends them under macro shocks. Expert ranges plug unavoidable data gaps.

Data Validation & Update Cycle

Outputs pass two analyst reviews, and any variance above five percent triggers re-work. We refresh estimates each year and release interim updates after material M&A, regulation, or technology shifts so clients receive the latest view.

Why Mordor's Contract Lifecycle Management Software Baseline Commands Greater Trust

Published figures often diverge because firms pick different module mixes, service add-ons, currencies, and refresh cadences.

Our transparent scope and annual update keep the baseline aligned with how buyers budget for CLM, whereas software-only counts or aggressive seat-growth multipliers used elsewhere distort totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.0 Billion (2025) | Mordor Intelligence | - |

| USD 1.62 Billion (2024) | Global Consultancy A | Counts software only; nine advanced economies |

| USD 2.89 Billion (2025) | Research Firm B | Bundles e-signature suites; optimistic SME cloud uptake |

These contrasts show that Mordor Intelligence provides a balanced, transparent baseline anchored to clearly disclosed scope choices and repeatable steps that decision-makers can audit with ease.

Key Questions Answered in the Report

What is the current size of the contract lifecycle management market?

Mordor Intelligence values the sector at USD 3.39 billion in 2026, with a projected rise to USD 6.26 billion by 2031 at a 13.06% CAGR.

Which deployment model grows fastest through 2031?

Hybrid architectures lead, expanding at a 17.15% CAGR as firms keep sensitive data on-premises while leveraging cloud analytics.

Why is Asia-Pacific the most dynamic region?

Government-funded digital programs and emerging data-privacy laws drive a 16.7% CAGR, outpacing mature regions.

How are AI tools changing contract management?

Generative AI now automates clause extraction, risk scoring, and drafting, cutting standard-agreement turnaround times by up to 60%.

What industries invest most heavily today?

BFSI remains the largest spender with 22.45% revenue share, while energy and utilities post the highest growth due to complex renewable-energy agreements.

Page last updated on: