Vacuum Blood Collection Tubes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 2.26 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

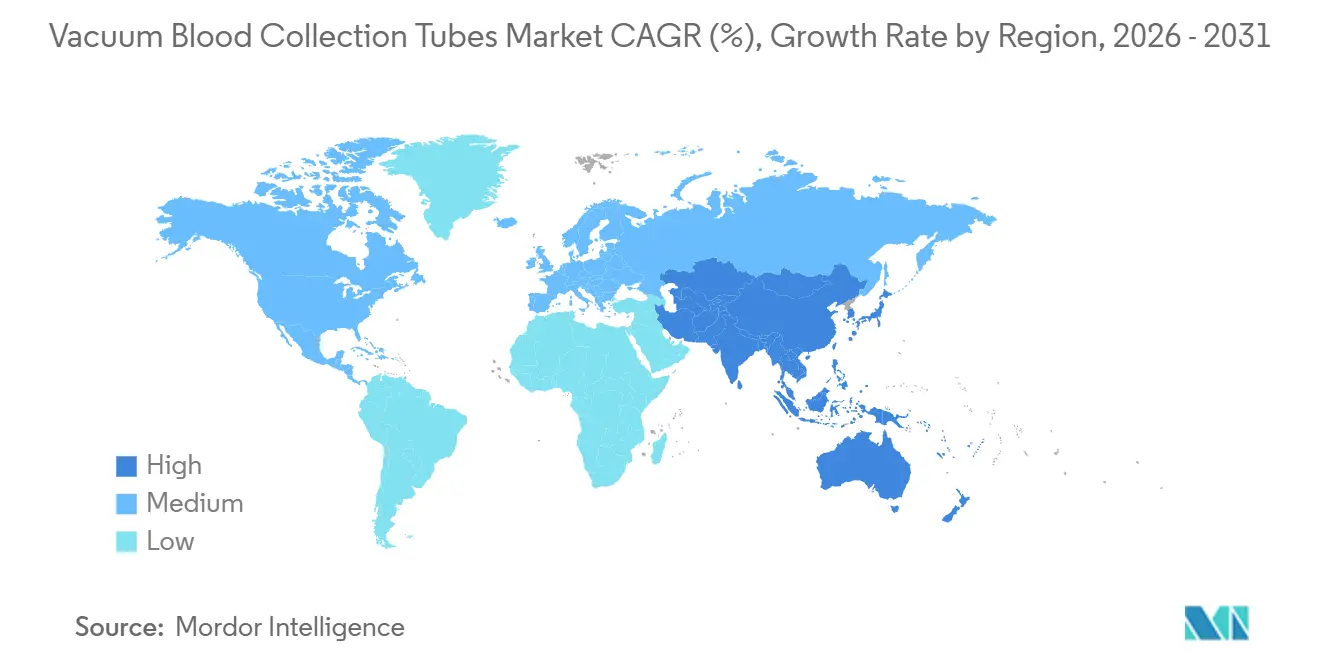

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

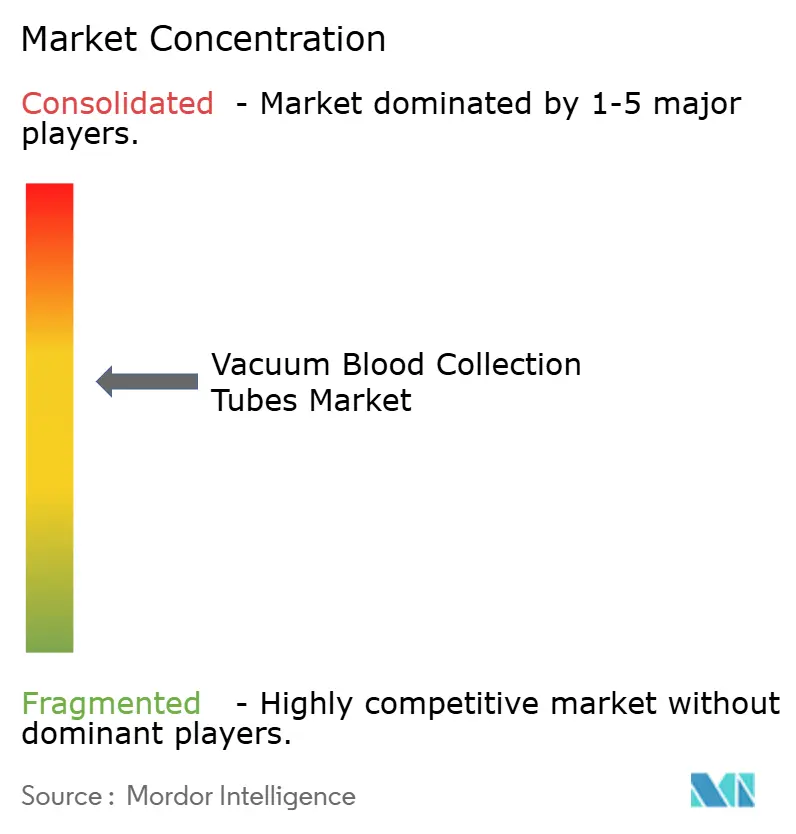

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vacuum Blood Collection Tubes Market Analysis by Mordor Intelligence

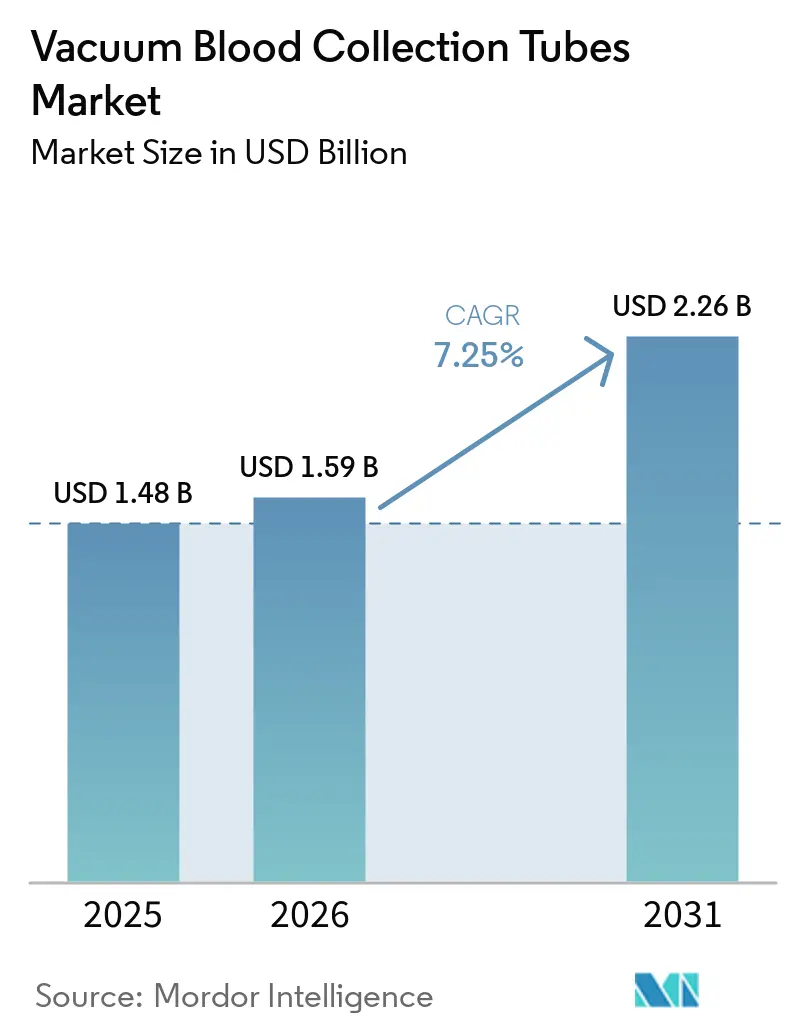

The Vacuum Blood Collection Tubes Market size was valued at USD 1.48 billion in 2025 and is estimated to grow from USD 1.59 billion in 2026 to reach USD 2.26 billion by 2031, at a CAGR of 7.25% during the forecast period (2026-2031).

The market is expanding because chronic disease monitoring keeps specimen volumes high across outpatient and inpatient care, and 589 million adults were living with diabetes in 2024. Large hospital and reference laboratory networks are routing more samples through centralized hubs, which raises demand for automation-ready tube formats that can move through standardized workflows. The shift toward liquid biopsy and precision medicine is also increasing use of preservative tubes that protect sample integrity when immediate processing is not available. Decentralized care models, including pharmacy collection and home-based sampling, are widening demand for capillary-compatible and low-volume tubes as trained phlebotomy capacity stays tight. Competition in the vacuum blood collection tubes market remains centered on global suppliers with broad portfolios, while lower-cost Asian producers are gaining ground in standard categories and keeping pricing pressure active in emerging markets.

Key Report Takeaways

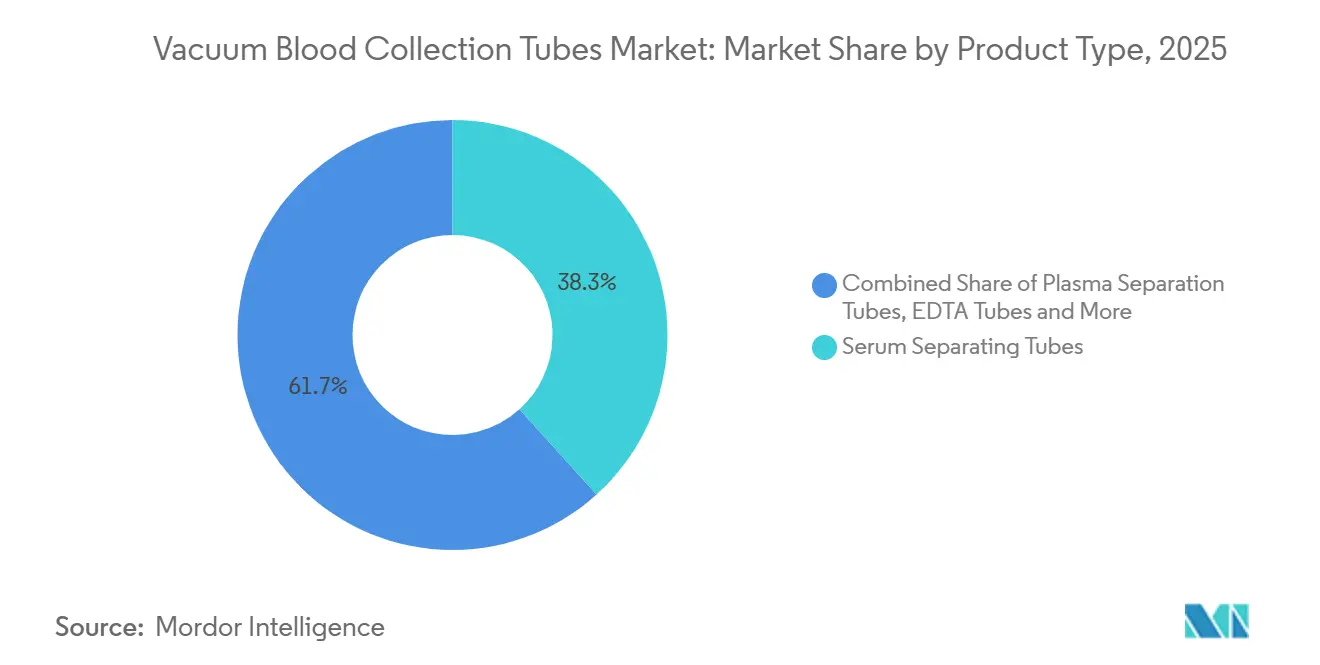

- By product type, serum separating tubes led with 38.31% share in 2025, and plasma separation tubes are forecast to expand at 8.38% CAGR from 2026 to 2031.

- By material, plastic tubes held 55.24% share in 2025, and glass tubes are expected to record the highest CAGR at 8.52% through 2031.

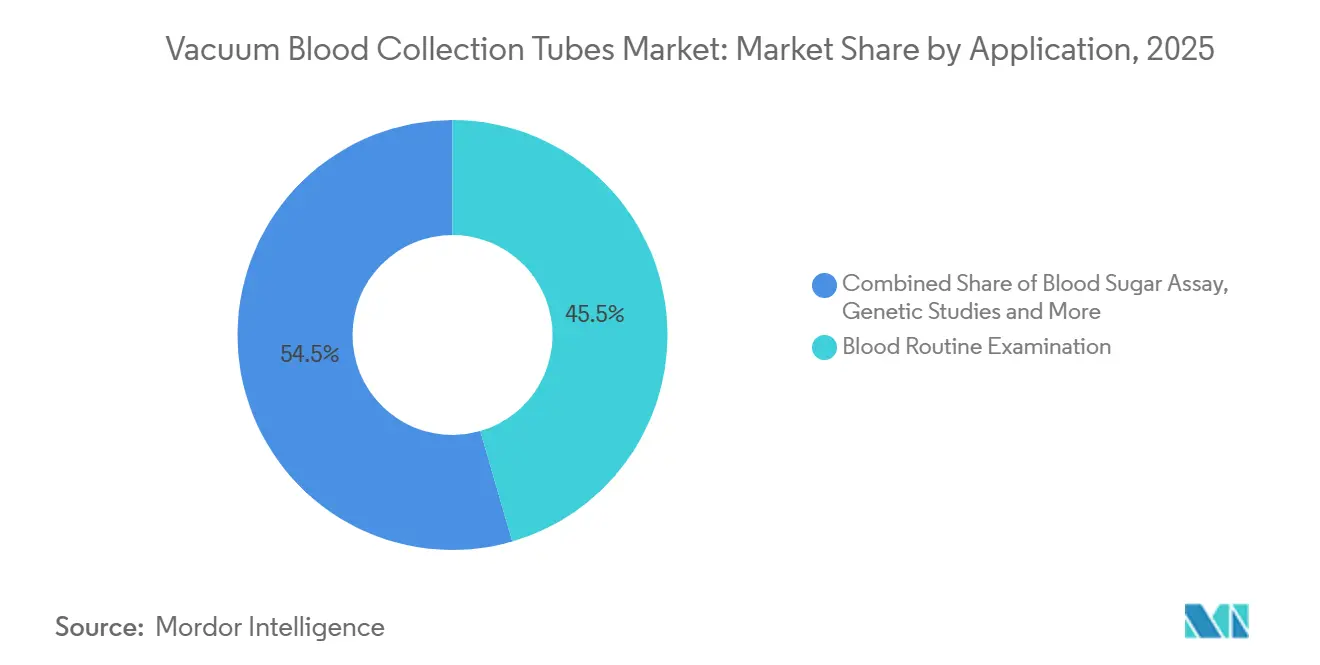

- By application, blood routine examination accounted for 45.52% share in 2025, and blood sugar assay is expected to advance at 9.25% CAGR through 2031.

- By end user, hospitals and clinics retained 48.22% share in 2025, and point-of-care and home-care settings are projected to grow at 9.65% CAGR through 2031.

- By geography, North America held 36.22% share in 2025, and Asia-Pacific is projected to expand at 8.65% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vacuum Blood Collection Tubes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Disease Monitoring Volumes | +2.1% | Global, with concentrated volume in North America, Western Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Expansion of High-Throughput Diagnostic Testing | +1.5% | North America and EU, spillover to large reference labs in India, Brazil, and South Korea | Medium term (2-4 years) |

| Safety-Engineered Closed Collection Protocols | +1.2% | Global, driven by regulatory adoption in North America, EU, and GCC, with early adoption in APAC | Medium term (2-4 years) |

| Decentralized and At-Home Sample Collection | +1.0% | North America, with expanding pilots in the UK, Germany, Australia, and Japan | Short term (≤ 2 years) |

| Liquid Biopsy and Precision Medicine Sample Stability Needs | +0.8% | North America and EU innovation corridors, with Japan and South Korea in APAC | Medium term (2-4 years) |

| Reusable Workflow Data Traceability Requirements in Labs | +0.5% | Global, concentrated in ISO 15189-accredited labs in North America, EU, and Oceania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Monitoring Volumes

Chronic non-communicable diseases remain the main engine of recurring demand in the vacuum blood collection tubes market. The World Health Organization stated in its 2025 monitor that noncommunicable diseases account for over 74% of all global deaths[1]World Health Organization, “Noncommunicable Diseases Progress Monitor 2025,” WHO Publications, who.int. Diabetes screening and follow-up are especially important because 589 million adults were living with diabetes in 2024, and 43% of people with diabetes remained undiagnosed. These testing patterns create repeat use across HbA1c, lipid, and complete blood count panels and keep demand steady even when provider budgets are under pressure. This demand base supports faster growth in blood sugar assay use across the vacuum blood collection tubes market.

Expansion Of High-Throughput Diagnostic Testing

High-throughput laboratories are reshaping product requirements in the vacuum blood collection tubes market. Centralized labs need precise fill volumes, consistent dimensions, and labels that work inside automated tracks. A 2025 analysis in Clinical Chemistry and Laboratory Medicine identified total lab automation and process consolidation as core drivers of workflow standardization in reference laboratories. That shift favors tubes that reduce manual intervention and support reliable analyzer loading. Plasma separation tubes are benefiting most because faster chemistry workflows often prefer plasma formats that shorten turnaround times.

Safety-Engineered Closed Collection Protocols

Safety-engineered closed collection protocols continue to support replacement demand in the vacuum blood collection tubes market. Hospitals and laboratories keep refreshing collection systems as needle safety, handling, and documentation requirements become more exact. The BD Vacutainer Eclipse Blood Collection Needle received FDA clearance in July 2025. The BD Vacutainer Safety-Lok Blood Collection Set also received FDA clearance in April 2026. These repeated approvals show why regulatory upkeep remains a real barrier for smaller suppliers that want hospital contracts.

Decentralized And At-Home Sample Collection

Decentralized and at-home sample collection is opening a new demand layer in the vacuum blood collection tubes market. The 2024 ASCP vacancy survey reported more than 24,000 laboratory positions open each year in the United States[2]American Association of Blood Banks, “ASCP Publishes Results of 2024 Vacancy Survey,” AABB News Resources, aabb.org. The same workforce strain is limiting collection capacity in ambulatory and rural settings. NAACLS reported in its 2024 annual survey that training capacity for clinical laboratory roles remains under pressure. In March 2025, BD and Babson Diagnostics reported peer-reviewed evidence that fingertip collection with the BD MiniDraw system matched conventional venipuncture performance for chronic disease management panels. That validation supports more use of low-volume and capillary formats as care shifts beyond traditional phlebotomy sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-Use Plastic Waste and Disposal Burden | -0.8% | EU, with a more restrictive compliance environment, and growing focus in California and other US states | Long term (≥ 4 years) |

| Skilled Phlebotomist Shortages and Pre-Analytical Error Risk | -0.7% | North America and EU, with growing strain in GCC and urban APAC | Medium term (2-4 years) |

| Raw Material Volatility for Polymer, Rubber, and Additives | -0.6% | Global, most acute for Asian PET and PP-dependent producers, with spillover to North America | Short term (≤ 2 years) |

| Tube Overdraw and Iatrogenic Blood Loss Concerns | -0.3% | Global, most acute in pediatric, ICU, and elderly patient populations across North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Single-Use Plastic Waste And Disposal Burden

Single-use plastic waste is becoming a tighter constraint on the vacuum blood collection tubes market. Germany's DIN Institute launched a 2025 committee focused on lifecycle assessment for medical devices and pharmaceutical products, which shows sustainability criteria are moving closer to procurement practice in Europe. Buyers are paying closer attention to packaging, recyclability, and disposal obligations for high-volume consumables. That pressure raises compliance work on materials, labeling, and end-of-life communication. The effect is strongest for PET and PP tube lines because routine collection depends on these formats.

Skilled Phlebotomist Shortages And Pre-Analytical Error Risk

Skilled phlebotomist shortages and pre-analytical error risk continue to restrain the vacuum blood collection tubes market. Collection quality can vary when staffing gaps force faster onboarding or shift sample handling to less experienced workers. The 2024 ASCP vacancy survey showed vacancies remained elevated and hiring timelines often stretched from 3 months to 1 year. In that setting, wrong tube type, underfill, poor mixing, and additive carry-over can trigger redraws and disrupt workflow. This encourages hospitals to favor color-coded, barcoded, and traceable tube systems that reduce dependence on operator experience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Serum Separating Tubes Drive Volume, Plasma Formats Gain Share

Serum separating tubes held 38.31% of vacuum blood collection tubes market share in 2025, and plasma separation tubes are projected to expand at 8.38% CAGR from 2026 to 2031. Serum separating tubes stay central to chemistry, immunology, and infectious disease testing because these panels move through high daily volumes in hospitals and pathology laboratories. Their gel barrier improves serum separation after centrifugation and reduces manual handling steps, which helps standardized laboratory throughput. Plasma separation tubes are gaining faster because automated chemistry workflows often prefer heparinized plasma when laboratories want shorter turnaround times.

EDTA tubes remain important across hematology and molecular workflows, including complete blood counts and PCR-based testing. Rapid serum tubes and coagulation tubes serve smaller but important use cases in emergency medicine and hemostasis monitoring. A February 2025 study in Scientific Reports found that K2EDTA tubes performed well for automated cell-free DNA extraction when samples were processed fresh, while specialized preservative tubes performed better when processing was delayed. That difference supports steady demand for both routine and specialized formats as the vacuum blood collection tubes market expands into oncology-adjacent workflows.

By Material: Plastic Tubes Dominate, Glass Retains Precision Roles

Plastic tubes held 55.24% of the material segment in 2025, while glass tubes are forecast to grow at 8.52% CAGR from 2026 to 2031. Plastic remains the main choice in the vacuum blood collection tubes market because PET and PP tubes reduce breakage risk and fit automated transport and decapping systems. Those benefits matter most in hospitals and large laboratories that process high specimen counts every day. Glass is growing faster in selected workflows where inertness and low contamination matter more than handling convenience.

Toxicology, trace element analysis, and some cytogenetic procedures still favor glass because polymer interaction or trace contamination can affect result quality. That keeps glass relevant even as plastic dominates routine testing volumes. Material selection also shapes margin stability because petroleum-derived polymers and rubber additives expose suppliers to input cost swings and procurement pressure. Producers with stronger sourcing discipline are better placed to protect continuity when the vacuum blood collection tubes market faces raw material volatility.

By Application: Routine Testing Leads, Glycemic Monitoring Rises Fast

Blood routine examination accounted for 45.52% of the vacuum blood collection tubes market size in 2025, and blood sugar assay is projected to expand at 9.25% CAGR from 2026 to 2031. Complete blood counts, erythrocyte sedimentation rate testing, and differential white cell counts create a stable demand floor because they are ordered across inpatient and outpatient care. This use pattern keeps EDTA and plasma-based formats moving through both acute care and follow-up testing pathways. The rise in blood sugar assay links directly to the wider diabetes testing pool in the vacuum blood collection tubes industry.

The International Diabetes Federation reported that 252 million people were living with undiagnosed diabetes in 2024, which supports long-run expansion in fasting glucose and glycated hemoglobin testing. Serology and immunology continue to add steady demand, especially where infectious disease surveillance and autoimmune screening are expanding. Genetic studies remain smaller in volume, but they are becoming more relevant as liquid biopsy workflows move into routine care. A 2025 study in EV and cfDNA Analysis found that Streck RNA tubes delivered the most stable combined cfDNA and extracellular vesicle performance after 7 days of room-temperature storage, which supports specialized tube use in precision oncology settings.

By End User: Hospitals Lead, Point-Of-Care Settings Expand Fastest

Hospitals and clinics retained 48.22% share in 2025, while the vacuum blood collection tubes market size for point-of-care and home-care settings is projected to rise at 9.65% CAGR from 2026 to 2031. Hospitals remain the largest buyers because complex diagnostic workups, surgical preparation, intensive care monitoring, and specialist consultations require the broadest product range. This setting also sustains demand for standardized formats that work across chemistry, hematology, coagulation, and molecular workflows. Pathology laboratories remain a key downstream customer because analyzer compatibility needs strongly influence tube selection across health systems.

Point-of-care and home-care settings are growing faster because decentralized clinical trials, pharmacy-based screening, and remote monitoring are shifting collection activity outside traditional phlebotomy suites. The March 2025 BD and Babson Diagnostics announcement added credibility to that shift by reporting clinically equivalent fingertip collection performance for chronic disease management panels. That trend favors capillary-compatible and low-volume formats that can be handled by trained healthcare workers beyond specialized draw centers. This change is opening fresh commercial space in the vacuum blood collection tubes industry for suppliers that can support transport stability and simple collection protocols.

Geography Analysis

North America held 36.22% of vacuum blood collection tubes market share in 2025, and Asia-Pacific is forecast to expand at 8.65% CAGR from 2026 to 2031. North America stayed ahead because it has the largest installed base of automated clinical laboratories and high per-capita testing volumes. Consolidation across hospital systems and reference laboratories is concentrating specimen flow into fewer large hubs, which supports demand for standardized and automation-compatible tubes[3]de Gruyter, “Laboratory Consolidation, Total Lab Automation and Process Design,” Clinical Chemistry and Laboratory Medicine, degruyterbrill.com. The United States remains the main regional demand center, while Canada and Mexico add stable volumes through public and private diagnostic networks. This makes North America the key market for suppliers that compete on documentation, quality consistency, and approved procurement status.

Asia-Pacific is growing faster because India, Southeast Asia, China, Japan, and South Korea are expanding testing access, private laboratory chains, and hospital infrastructure. The region is also adding new demand from populations that previously had limited access to formal diagnostic monitoring, especially in chronic disease care. Europe remains technically sophisticated and highly regulated, which favors established suppliers with deep documentation and quality systems. Germany's DIN Institute launched a 2025 committee on lifecycle assessment for medical devices and pharmaceutical products, which signals that sustainability criteria are becoming more relevant in procurement discussions.

South America and the Middle East and Africa remain smaller in absolute value, but they are becoming more structured through laboratory accreditation, health screening programs, and hospital capacity additions. Brazil leads South America by diagnostic volume, and South Africa continues to act as a distribution gateway for Sub-Saharan Africa. Price sensitivity stays high across these regions, which gives Chinese and Indian suppliers an opening in standard tube categories even as global incumbents retain an edge in premium and regulated channels. Regional demand therefore splits between mature markets that reward compliance depth and emerging markets that respond more quickly to price and local distribution reach.

Competitive Landscape

The vacuum blood collection tubes market is moderately concentrated, with Becton, Dickinson and Company holding the largest global position and Greiner Bio-One, Sarstedt, Terumo, and Sekisui Medical forming the next tier of scale suppliers. These companies set practical standards for analyzer compatibility, additive stability documentation, product breadth, and regulatory upkeep. Competition in the vacuum blood collection tubes market is driven less by simple price moves and more by system integration, supply reliability, and the ability to meet hospital and laboratory qualification requirements. Smaller Asian manufacturers are gaining ground in standard tubes, especially where buyers are highly price sensitive and compliance barriers are lower. That keeps the premium end of the market in the hands of firms that can support broad portfolios and long procurement cycles.

BD and Babson Diagnostics launched fingertip blood testing to health care organizations in December 2024, which strengthened BD's position in decentralized sample collection. In March 2025, BD reported peer-reviewed evidence that the BD MiniDraw system achieved equivalent testing accuracy to higher-volume venous draws for chronic disease management panels. In April 2026, BD also received FDA clearance for the MiniDraw SST capillary blood collection system, which extended its regulated capillary offering. These steps show how leading companies use product validation, channel partnerships, and regulatory filings to defend share in the vacuum blood collection tubes market.

Another active area is specialized sample preservation, where liquid biopsy workflows are creating demand for tubes that can maintain cell-free nucleic acids during delayed processing. Digital traceability is also becoming more important because large laboratories want barcode-ready and system-linked products that reduce pre-analytical error exposure. The vacuum blood collection tubes market still leaves room for regional challengers in standard categories, but moving into Europe and top hospital accounts remains difficult without strong documentation and quality systems. The overall structure therefore supports steady leadership by established firms, while leaving selective growth pockets open in capillary collection, specialized preservation, and cost-led supply.

Vacuum Blood Collection Tubes Industry Leaders

Becton, Dickinson and Company

Greiner Bio-One International GmbH

Terumo Corporation

Sarstedt AG and Co. KG

Sekisui Medical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Australia’s Q-Sera Pty Ltd launched its patented blood collection technology in Japan via Terumo Corporation's VenoJect II RAPClot platform, aiming to speed up clot formation and serum preparation.

- January 2026: Terumo Corporation introduced the Venosafe II Replot vacuum blood collection tube in Japan, designed to improve clotting speed and reduce lab turnaround while preserving specimen quality.

Global Vacuum Blood Collection Tubes Market Report Scope

As per the scope of the report, vacuum blood collection tubes are specialized containers used to collect and store blood samples for laboratory testing. They are pre-sterilized and contain a vacuum that creates a negative pressure, which automatically draws the blood from the vein into the tube when the needle is inserted. These tubes often contain additives or anticoagulants depending on the test requirements and are designed to ensure the sample's integrity during transportation and analysis.

The vacuum blood collection tubes market is segmented by product type, material, application, end user, and geography. By product type, the market includes serum separating tubes, plasma separation tubes, EDTA tubes, rapid serum tubes, coagulation tubes, and other product types. By material, the segmentation covers plastic tubes and glass tubes. By application, the market is categorized into serology and immunology, routine blood examination, coagulation tests, genetic studies, blood sugar assay, and other applications. By end user, the market is divided into hospitals and clinics, pathology laboratories, blood banks, point-of-care and home-care settings, and other end users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Serum Separating Tubes |

| Plasma Separation Tubes |

| EDTA Tubes |

| Rapid Serum Tubes |

| Coagulation Tubes |

| Other Product Types |

| Plastic Tubes |

| Glass Tubes |

| Serology and Immunology |

| Blood Routine Examination |

| Coagulation Tests |

| Genetic Studies |

| Blood Sugar Assay |

| Other Applications |

| Hospitals and Clinics |

| Pathology Laboratories |

| Blood Banks |

| Point-of-Care and Home-Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Serum Separating Tubes | |

| Plasma Separation Tubes | ||

| EDTA Tubes | ||

| Rapid Serum Tubes | ||

| Coagulation Tubes | ||

| Other Product Types | ||

| By Material | Plastic Tubes | |

| Glass Tubes | ||

| By Application | Serology and Immunology | |

| Blood Routine Examination | ||

| Coagulation Tests | ||

| Genetic Studies | ||

| Blood Sugar Assay | ||

| Other Applications | ||

| By End User | Hospitals and Clinics | |

| Pathology Laboratories | ||

| Blood Banks | ||

| Point-of-Care and Home-Care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the vacuum blood collection tubes market?

The vacuum blood collection tubes market stands at USD 1.59 billion in 2026 and is projected to reach USD 2.26 billion by 2031 at a 7.25% CAGR.

Which product type leads demand for vacuum blood collection tubes?

Serum separating tubes lead demand with 38.31% share in 2025 because they are widely used in chemistry, immunology, and infectious disease testing.

Which application is growing the fastest in blood collection tubes?

Blood sugar assay is the fastest-growing application with a 9.25% CAGR through 2031, supported by expanding diabetes screening and follow-up testing.

Which end-user group drives the highest growth in this space?

Point-of-care and home-care settings are growing the fastest at 9.65% CAGR through 2031, while hospitals and clinics remain the largest end-user group with 48.22% share in 2025.

Which region has the largest and fastest-growing opportunity?

North America held the largest share at 36.22% in 2025, while Asia-Pacific is the fastest-growing region with an 8.65% CAGR through 2031.

What are the main risks affecting suppliers of blood collection tubes?

The main risks are plastic waste and disposal pressure, phlebotomist shortages that raise pre-analytical error risk, and raw material volatility in polymers and rubber additives.

Page last updated on: