Blood Purification Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

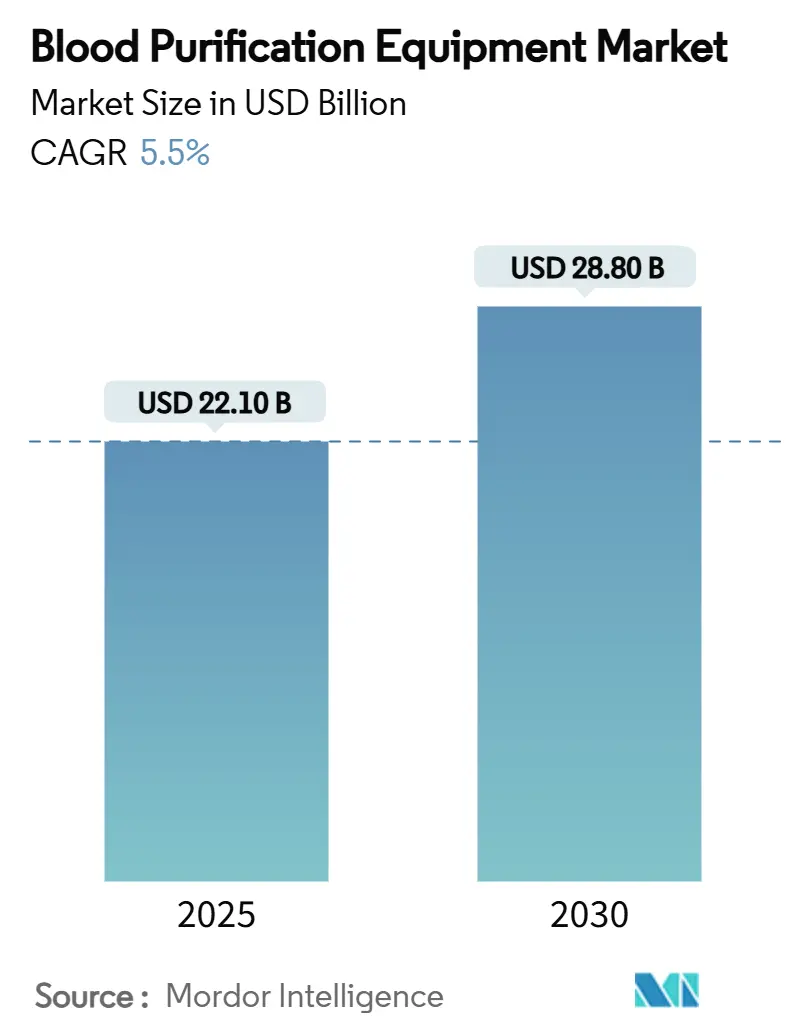

| Market Size (2025) | USD 22.10 Billion |

| Market Size (2030) | USD 28.80 Billion |

| Growth Rate (2025 - 2030) | 5.50% CAGR |

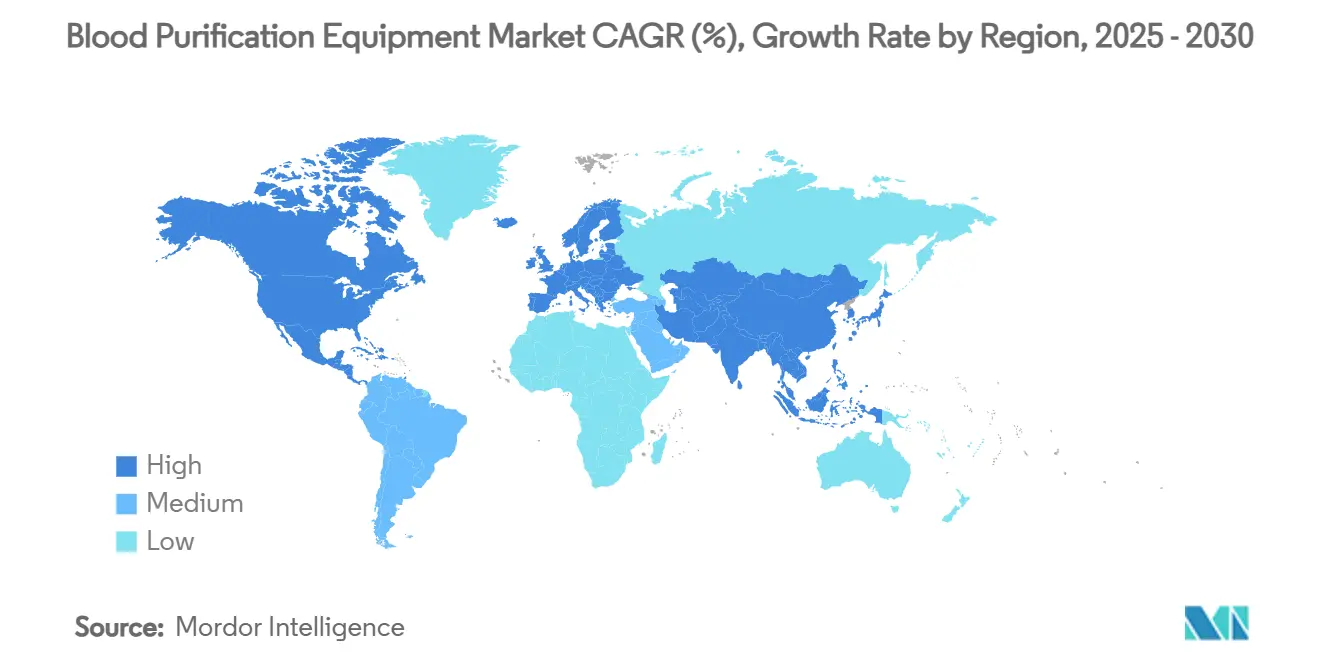

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Purification Equipment Market Analysis by Mordor Intelligence

The blood purification equipment market size reached USD 22.1 billion in 2025 and is forecast to climb to USD 28.8 billion by 2030, reflecting a 5.5% CAGR over the period. Accelerated demand stems from the global rise in chronic kidney disease, which now affects more than 850 million people, and from steady device breakthroughs that improve middle-molecule clearance and reduce anticoagulant use. Rapid uptake of home-based dialysis, the FDA’s breakthrough device pathway, and AI-driven dosing platforms together reinforce resilience across both acute and chronic care settings. North America and Europe preserve lead positions thanks to mature reimbursement systems, while Asia Pacific registers the highest growth as public-sector modernization widens patient access. Competitive activity remains moderate, but supply-chain volatility—illustrated by the 2025 shortage of hemodialysis tubing—underscores the strategic importance of vertically integrated manufacturing networks.

Key Report Takeaways

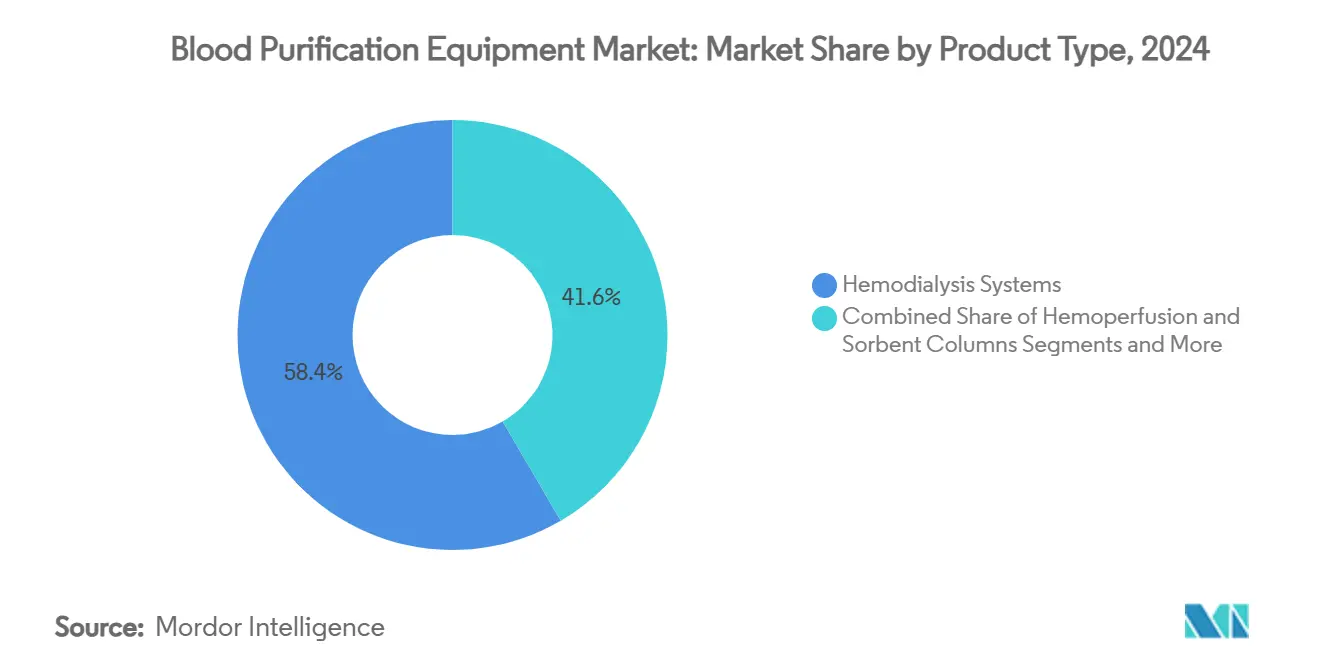

- By product type, hemodialysis systems held 59.8% of the blood purification equipment market share in 2024, while hemoperfusion and sorbent columns are advancing at a 13.4% CAGR through 2030.

- By modality, intermittent hemodialysis accounted for 52.1% of the blood purification equipment market size in 2024, and continuous blood purification is projected to expand at a 12.1% CAGR between 2025 and 2030.

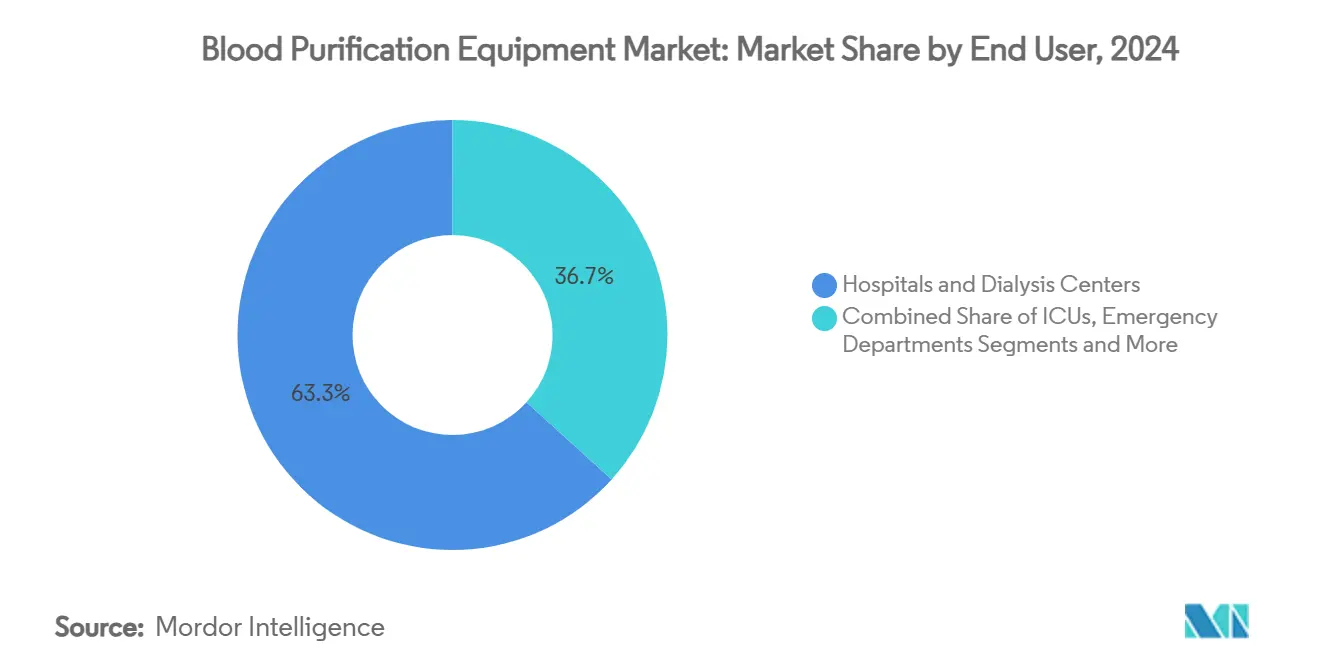

- By end user, hospitals and dialysis centers represented 73.4% of the blood purification equipment market size in 2024, whereas home care settings are forecast to grow at a 15.8% CAGR through 2030.

- By application, end-stage renal disease captured 61.2% of the blood purification equipment market share in 2024; sepsis and septic shock treatments are poised to increase at a 14.2% CAGR through 2030.

- By geography, North America led overall revenues in 2024, while Asia Pacific is expected to post the highest regional growth with an 11.2% CAGR to 2030.

Global Blood Purification Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global prevalence of chronic kidney disease | +1.80% | Asia Pacific, North America | Long term (≥ 4 years) |

| Rapid adoption of home-based hemodialysis systems | +1.20% | North America, EU, expanding APAC | Medium term (2-4 years) |

| Breakthroughs in high-flux and medium-cut-off membranes | +0.90% | Global, led by developed markets | Medium term (2-4 years) |

| Expanding reimbursement for extracorporeal therapies | +0.80% | North America, EU | Short term (≤ 2 years) |

| Non-renal indications driving adsorber demand | +0.60% | Global ICU markets | Short term (≤ 2 years) |

| AI-driven, closed-loop CRRT dosing platforms | +0.40% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of Chronic Kidney Disease (CKD)

Global CKD prevalence stands at 13.4% and affects more than 850 million people, making it the single biggest demand catalyst for the blood purification equipment market.[1]Richard A. Ward, “Regulatory Considerations for Hemodiafiltration,” Clinical Journal of the American Society of Nephrology, journals.lww.comEmerging economies shoulder a disproportionate burden as diabetes and hypertension accelerate with urbanization. In Saudi Arabia, CKD prevalence reached 4.76%, with male incidence at 5.83%—evidence of gender disparities that intensify treatment demand. Aging demographics compound the strain because CKD prevalence exceeds 50% in those aged 90 years and above. In response, health systems are expanding dialysis capacity and prioritizing equipment that maximizes middle-molecule clearance while maintaining workflow efficiency. Vendors capable of delivering cost-efficient, high-performance systems remain best positioned to monetize the rising CKD caseload.

Rapid Adoption of Home-Based Hemodialysis Systems

Patient demand for lifestyle flexibility and payer interest in lowering facility costs propel home-based platforms. Fresenius Medical Care’s FDA-cleared 5008X Hemodialysis System, able to replace up to 160,000 legacy devices, reduces mortality by 23% compared with conventional therapy. Portable concepts are proliferating; Seoul National University’s nanoelectrokinetic device achieved a 30% waste-removal rate in animal tests, signaling next-generation point-of-care potential.[2]José A. Moura-Neto, “Change in Peritoneal Dialysis in Brazil,” Healthcare, healthcare.mdpi.com Home modality acceleration boosts consumable pull-through, expands recurring revenue, and widens access for rural populations. Successful market entrants offer compact footprints, intuitive user interfaces, and remote monitoring features that assure clinical oversight.

Breakthroughs in High-Flux and Medium-Cut-Off Membranes

Membrane R&D now centers on improving selective toxin extraction without removing essential proteins, and recent clinical programs confirm mortality benefits from advanced hemodiafiltration. Incorporation of biocompatible polymers and enlarged surface areas elevates middle-molecule clearance—critical to mitigating cardiovascular events. Combined with AI-based dosing, these membranes underpin sharp gains in uremic toxin reduction. Regulatory bodies have rewarded such innovation through expedited approvals, translating into broader reimbursement and accelerated market diffusion. Suppliers emphasizing next-generation membranes thus carve out defensible differentiation in a maturing product landscape.

Expanding Reimbursement for Extracorporeal Therapies

Enhanced payer coverage in the United States and leading EU markets makes advanced modalities financially viable for providers. Medicare payment bundles now recognize high-volume hemodiafiltration and hemoperfusion cartridges, encouraging step-up therapy adoption. Similar trends appear in Germany, where public insurers reimburse medium-cut-off filters to improve patient-reported outcomes. Short-term reimbursement gains lift upfront capital budgets and underscore the importance of demonstrating economic value through reduced hospitalization days.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and treatment costs | -1.40% | Global, most acute in low-income regions | Long term (≥ 4 years) |

| Infrastructure gaps in low-income regions | -0.80% | Sub-Saharan Africa, parts of APAC & South America | Long term (≥ 4 years) |

| Competition from wearable/artificial kidney R&D | -0.60% | North America & EU, expanding globally | Medium term (2-4 years) |

| Environmental scrutiny over dialysate & plastics | -0.40% | EU lead, North America follow | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Treatment Costs for Providers and Payers

Advanced hemodialysis consoles can exceed USD 50,000 per unit, while annual per-patient treatment costs top USD 90,000 in mature markets, creating steep entry barriers in constrained health systems. South African cost-utility studies show peritoneal dialysis offers superior value but suffers from infrastructure gaps, illustrating the delicate balance between economic evidence and feasibility. As value-based care gains traction, manufacturers must prove lifetime savings through reduced hospitalizations to secure funding approvals.

Infrastructure Gaps in Low-Income Regions

Insufficient electricity, poor water quality, and limited specialist training restrict therapy rollout across rural zones. In Brazil, peritoneal dialysis utilization dropped to 4.3% by 2023 because logistical challenges outpaced clinical advantage.[3]Seoul National University, “Portable Artificial Kidney Device,” phys.org Supply chain fragility further heightens risk, with tube shortages illustrating cascading treatment interruptions. Durable, low-maintenance platforms tied to training partnerships offer a pathway to unlock latent demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hemodialysis Systems Sustain Leadership amid Sorbent Column Momentum

Hemodialysis systems accounted for 59.8% of the blood purification equipment market size in 2024, confirming their entrenched status in routine ESRD care. This dominance reflects decades of clinical familiarity, global reimbursement alignment, and robust supply ecosystems. Continuous design refinements, such as touch-screen interfaces and auto-priming circuits, strengthen provider loyalty and safeguard consumable pull-through. Simultaneously, hemoperfusion and sorbent columns post a 13.4% CAGR through 2030, buoyed by expanding indications in cytokine-storm mitigation and antiviral therapies. Cartridges like the Seraph 100, designated for expedited FDA review, highlight demand for targeted pathogen removal.

The competitive narrative increasingly revolves around platform convergence as manufacturers embed adsorber slots within hemodialysis consoles to broaden clinical reach. Plasmapheresis devices carve specialized niches for autoimmune disorders, while recurring revenue from disposables anchors profitability. As hospitals lean toward flexible systems capable of multi-modal therapy, suppliers delivering modular architectures stand to capture incremental wallet share within the blood purification equipment market.

By Modality: Intermittent Dominance Confronts Accelerating Continuous Therapy Adoption

Intermittent hemodialysis represented 52.1% of the blood purification equipment market share in 2024, reflecting established scheduling protocols and efficient clinic workflows. Its sustainability, however, faces pressure from a 12.1% CAGR in continuous blood purification that better suits hemodynamically unstable ICU patients. Hospitals invest in continuous renal replacement pumps that integrate regional citrate anticoagulation and AI-guided flow algorithms, widening use beyond nephrology units.

Hybrid options, including hemodiafiltration, exploit combined diffusive-convective transport to surpass uremic toxin thresholds unmet by legacy modalities. Precision-medicine trends accelerate the shift as dosing software tailors treatment intensity to biomarker feedback loops, embedding continuous platforms deeper into critical-care pathways.

By End User: Hospital Hegemony Meets Home-Care Acceleration

Hospitals and dialysis centers captured 73.4% of the blood purification equipment market size in 2024, leveraging centralized staffing and economies of scale. Yet 15.8% CAGR in home-care settings through 2030 signals a structural pivot toward patient-centric delivery models.

Miniaturized consoles, simplified cartridge changes, and tele-monitoring capabilities empower self-dialysis under remote nephrologist oversight. Specialty clinics capitalize on technology leaps to offer niche treatments such as double-filtration plasmapheresis, while critical care units broaden extracorporeal therapy use for non-renal indications. Manufacturers that bundle on-demand technical support and cloud-based analytics position themselves as enablers of distributed therapy networks within the expanding blood purification equipment market.

By Application: ESRD Retains Command as Sepsis Therapies Surge

End-stage renal disease occupied 61.2% of the blood purification equipment market share in 2024, driven by the chronic, recurring nature of dialysis treatments and comprehensive insurance coverage. Sepsis and septic shock, though smaller, grow at 14.2% CAGR as ICUs adopt hemoadsorption columns to remove inflammatory mediators. Acute kidney injury applications expand as early intervention protocols favor continuous modalities to forestall CKD progression.

Autoimmune and metabolic disorder indications rely on antibody-depleting and lipid-exchange cartridges, diversifying demand drivers. As clinical trials validate blood purification’s adjunctive role in treating multi-organ failure, equipment capable of rapid modality switching gains strategic importance to providers seeking versatile treatment arsenals.

Geography Analysis

North America retains the largest regional share thanks to comprehensive Medicare reimbursement, an extensive dialysis-center network, and willingness to trial breakthrough devices that reduce heparin exposure. The United States alone hosts more than 7,500 outpatient dialysis clinics, underpinning predictable consumable demand and enabling quick rollouts of AI-driven CRRT platforms. Canada enhances regional growth through universal insurance that funds high-flux filter adoption, while Mexico’s Seguro Popular reforms expand public access to end-stage renal treatments.

Europe ranks second, combining world-class manufacturing clusters with stringent health-technology assessments that reward clinically superior devices. Germany leads uptake of medium-cut-off membranes, and Italian procurement agencies include environmental performance in tender scores, encouraging recyclable cartridge use. The EU Medical Device Regulation, despite adding compliance overhead, provides a single approval pathway that reduces multi-country launch frictions. Sustainability initiatives—such as the United Kingdom’s NHS Net-Zero program—drive interest in water-saving dialysate systems, shaping future product roadmaps.

Asia Pacific is the fastest-growing territory within the blood purification equipment market, propelled by dual forces of epidemiological shift and economic expansion. China’s ESRD population crosses 1.2 million, prompting the government to subsidize domestic console production to mitigate import reliance. Japan continues to champion high-volume online hemodiafiltration, while India’s Pradhan Mantri National Dialysis Programme adds procurement scale. South Korea incubates start-ups integrating nanofiber membranes, and Australia invests in tele-dialysis to reach remote communities. Middle East & Africa and South America remain nascent but hold untapped potential as infrastructure projects and public–private partnerships inch forward.

Competitive Landscape

The blood purification equipment market exhibits moderate concentration as the top five players control near-60% of global revenue. Fresenius Medical Care, Baxter International, and B. Braun Melsungen leverage vertical integration to lock in consumable demand and maintain price discipline. Platform strategies bundle equipment, cartridges, and software, reinforcing long-term service contracts and stabilizing cash flows. Supply-chain resilience is now a differentiator; tube shortages in 2025 prompted accelerated dual-sourcing and on-shoring among leading vendors.

Adjacent life-science conglomerates are buying their way into the sector. Thermo Fisher Scientific’s USD 4.1 billion purchase of Solventum’s filtration business demonstrates converging interests between diagnostics, bioprocessing, and therapeutic apheresis. Investment flows toward high-growth niches: ExThera Medical raised USD 15.3 million to commercialize pathogen-binding filters, whereas Circulate Health attracted USD 12 million for longevity-focused plasma exchange services.

Technology differentiation centers on AI integration, biocompatible polymers, and portable design. Outset Medical’s TabloCart and Diality’s compact console illustrate escalating competition around mobility and usability. Established players counter by embedding predictive maintenance analytics and launching eco-friendly cartridge lines. The strategic narrative now balances product innovation, supply-security assurance, and sustainability credentials to win multi-year procurement tenders across a diversifying global customer base.

Blood Purification Equipment Industry Leaders

Fresenius Medical Care

Baxter International

B. Braun Melsungen

Nikkiso

Asahi Kasei Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Circulate Health secured USD 12 million in funding to advance longevity-oriented plasma exchange services.

- May 2025: Seoul National University revealed a portable nanoelectrokinetic peritoneal dialysis prototype with 30% waste-removal efficacy.

- March 2025: The FDA listed hemodialysis tubes as in short supply following B. Braun production halts, with constraints expected until fall 2025.

- January 2025: Haemonetics sold its whole-blood assets to GVS for USD 67.8 million to refocus on automated collection systems.

Global Blood Purification Equipment Market Report Scope

| Hemodialysis Systems |

| Continuous Renal Replacement Therapy (CRRT) Devices |

| Hemoperfusion & Sorbent Columns |

| Plasmapheresis Devices |

| Other Blood Purification Accessories & Consumables |

| Intermittent Hemodialysis |

| Continuous Blood Purification |

| Hemofiltration |

| Hemodiafiltration |

| Double-Filtration Plasmapheresis |

| Hospitals & Dialysis Centers |

| Home Care Settings |

| Specialty Clinics |

| Intensive Care Units (ICUs) |

| Emergency Departments |

| End-Stage Renal Disease (ESRD) |

| Acute Kidney Injury (AKI) |

| Sepsis & Septic Shock |

| Autoimmune & Metabolic Disorders |

| Others (e.g., Poisoning, Liver Failure) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hemodialysis Systems | |

| Continuous Renal Replacement Therapy (CRRT) Devices | ||

| Hemoperfusion & Sorbent Columns | ||

| Plasmapheresis Devices | ||

| Other Blood Purification Accessories & Consumables | ||

| By Modality | Intermittent Hemodialysis | |

| Continuous Blood Purification | ||

| Hemofiltration | ||

| Hemodiafiltration | ||

| Double-Filtration Plasmapheresis | ||

| By End User | Hospitals & Dialysis Centers | |

| Home Care Settings | ||

| Specialty Clinics | ||

| Intensive Care Units (ICUs) | ||

| Emergency Departments | ||

| By Application | End-Stage Renal Disease (ESRD) | |

| Acute Kidney Injury (AKI) | ||

| Sepsis & Septic Shock | ||

| Autoimmune & Metabolic Disorders | ||

| Others (e.g., Poisoning, Liver Failure) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the blood purification equipment market in 2025?

The blood purification equipment market size stands at USD 22.1 billion in 2025 and is expected to reach USD 28.8 billion by 2030.

What is the expected CAGR for blood purification devices through 2030?

Industry revenue is projected to increase at a 5.5% CAGR between 2025 and 2030.

Which product type holds the largest share of total revenues?

Hemodialysis systems dominate with 59.8% of 2024 revenue.

Which segment is expanding the fastest?

Hemoperfusion and sorbent columns are forecast to grow at 13.4% CAGR during 2025-2030.

Which region offers the highest growth potential?

Asia Pacific is the fastest-growing region due to rising CKD prevalence and rapid healthcare modernization.

How are AI platforms changing renal replacement therapy?

AI-driven continuous renal replacement systems automate dose adjustments in real time, improving consistency and reducing circuit clotting events.

Page last updated on: