United States Blood Collection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.94 Billion |

| Market Size (2026) | USD 3.06 Billion |

| Market Size (2031) | USD 3.83 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

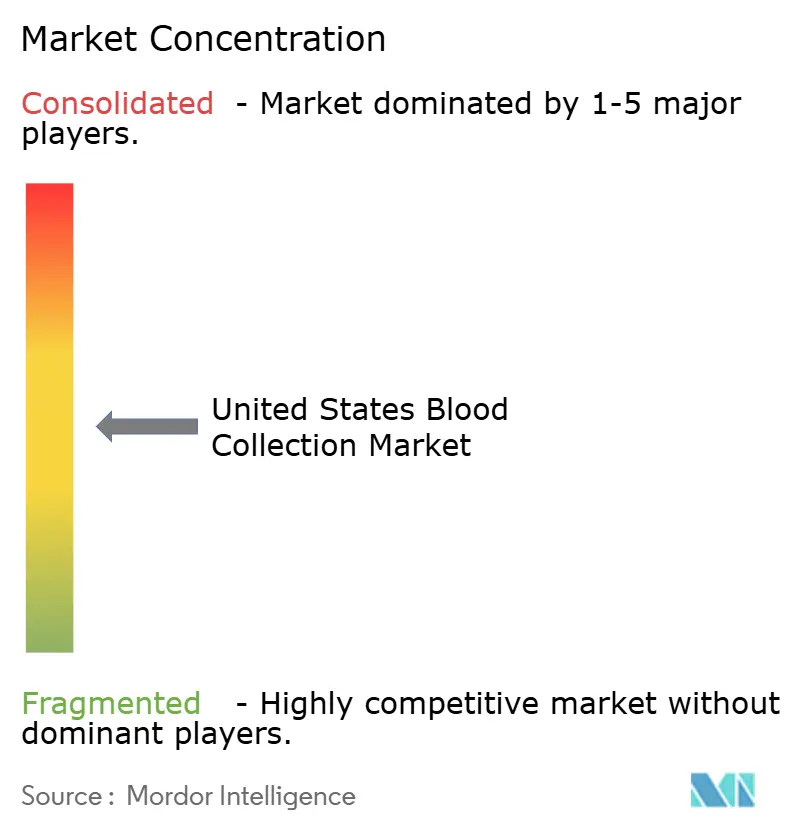

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Blood Collection Market Analysis by Mordor Intelligence

The United States Blood Collection Market size is expected to grow from USD 2.94 billion in 2025 to USD 3.06 billion in 2026 and is forecast to reach USD 3.83 billion by 2031 at 4.61% CAGR over 2026-2031.

The blood collection market is expanding on the back of a large patient base that needs repeated diagnostic monitoring, especially as chronic disease burden and age-linked care intensity remain high across the country. The blood collection market also benefits from the continued importance of blood-based diagnostics in hospitals, physician offices, laboratories, and ambulatory care, where routine specimen collection remains part of standard care delivery. Demand is further supported by sustained transfusion use and by a continued move toward component collection, which increases the value of recurring consumables and collection sets used by blood centers and hospital networks. New growth is emerging from capillary sampling, home-based collection, and decentralized care workflows that extend collection activity beyond the traditional hospital campus. Competition remains active because large suppliers are defending integrated portfolios across tubes, needles, holders, blood bags, and software, while smaller players are targeting convenience-led capillary formats, and the 2024 blood culture vial shortage showed how quickly supply concentration can disrupt essential clinical operations.

Key Report Takeaways

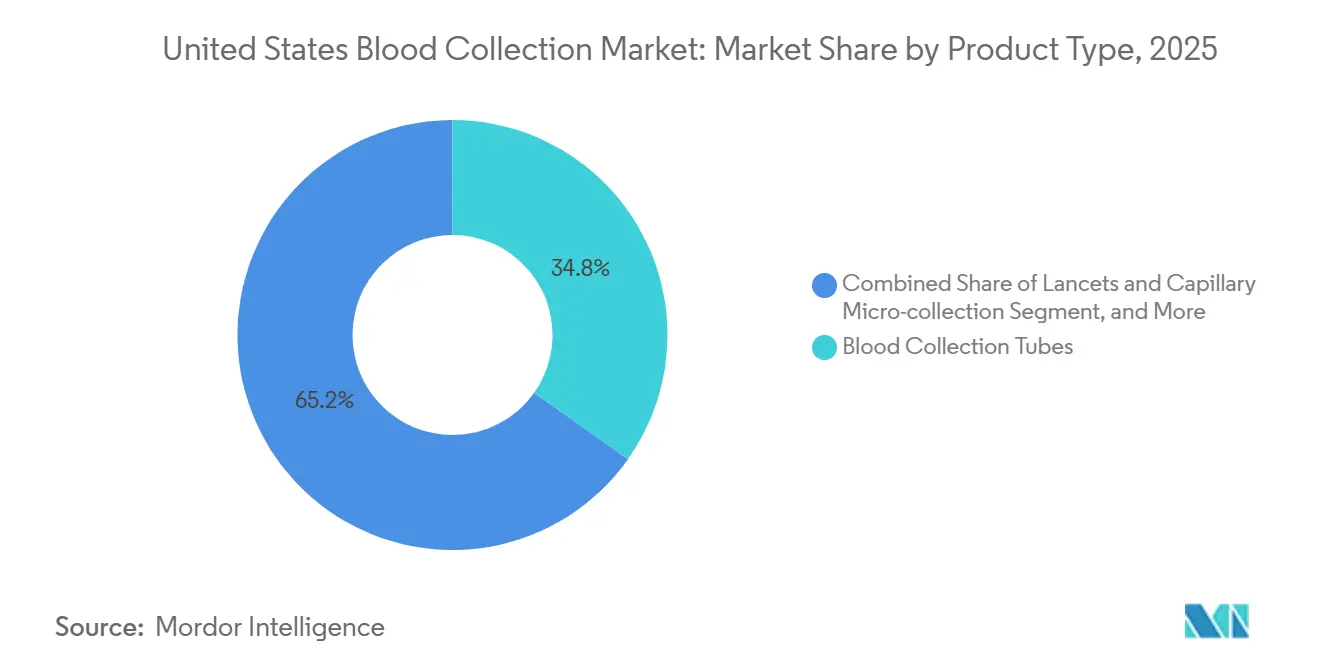

- By product type, blood collection tubes held 34.78% of the blood collection market share in 2025, while lancets and capillary micro-collection are forecast to expand at 5.47% CAGR through 2031.

- By site of collection, venous collection led with 40.57% revenue share in 2025, while capillary collection is projected to grow at 5.28% CAGR through 2031.

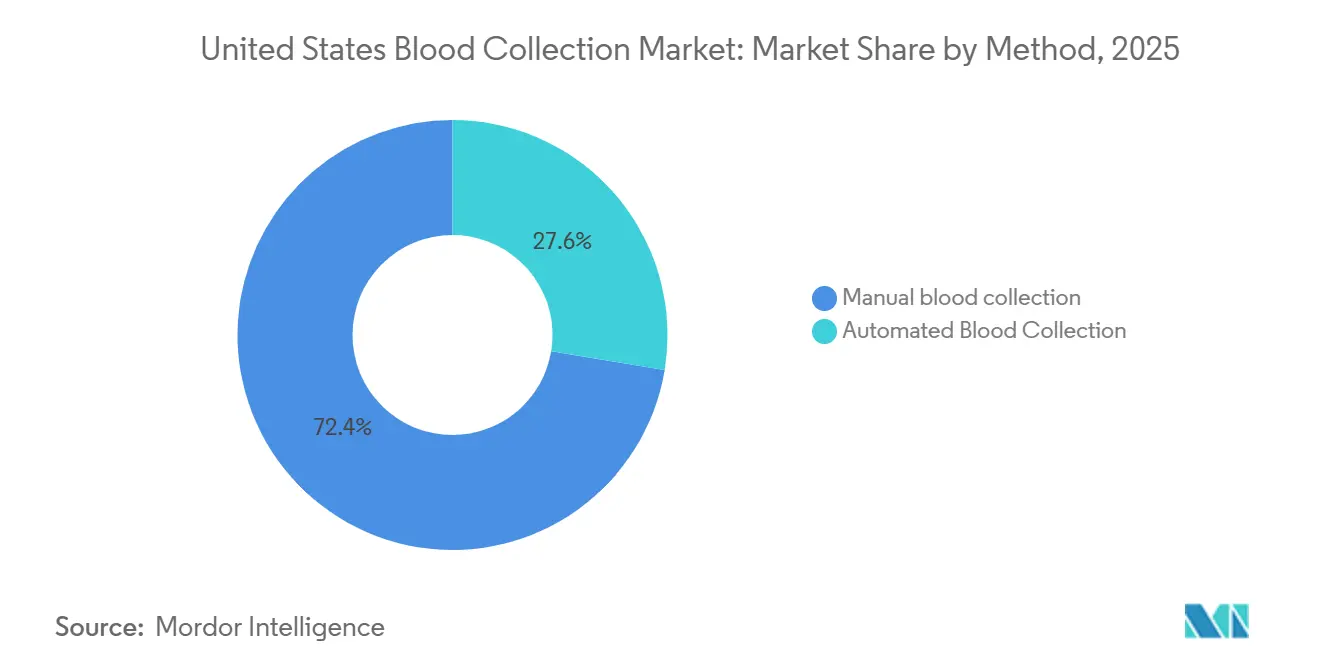

- By method, manual workflows held 27.36% of revenue in 2025, while automated blood collection is expected to post the fastest growth at 5.89% CAGR through 2031.

- By application, diagnostics accounted for 50.73% of the blood collection market size in 2025, while treatment and transfusion support are projected to expand at 6.66% CAGR through 2031.

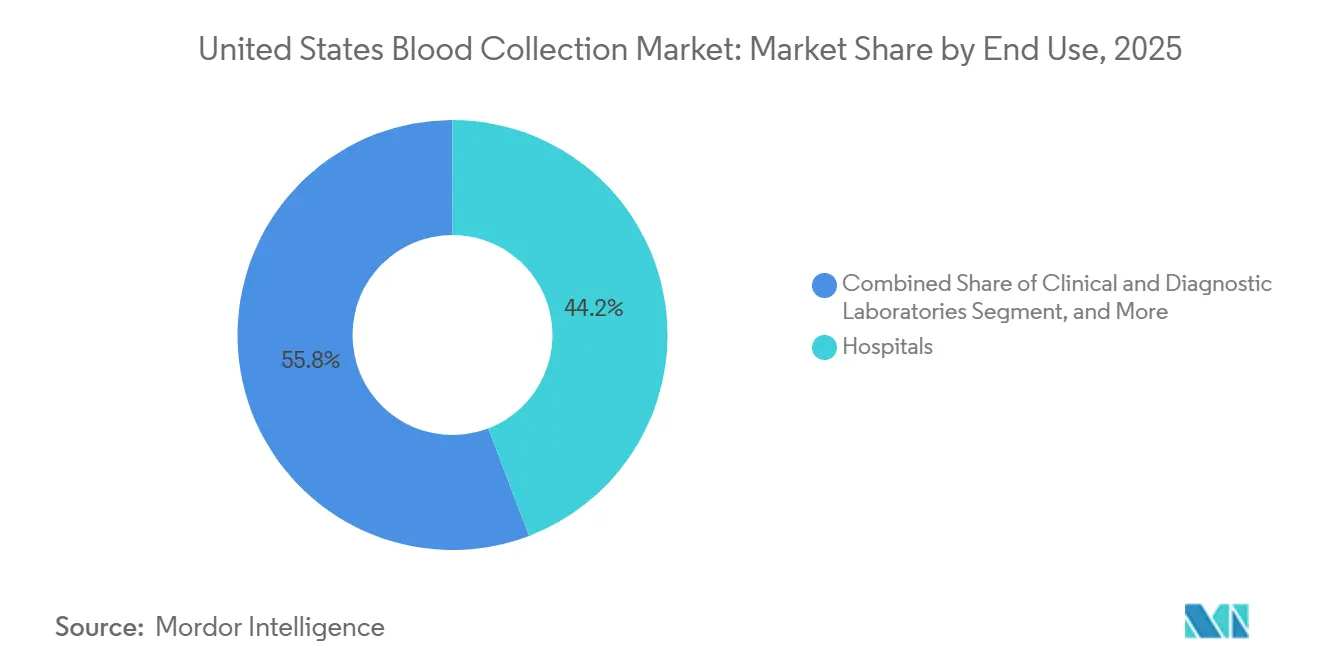

- By end use, hospitals represented 44.21% of revenue in 2025, while blood banks and blood centers are expected to grow at 6.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Blood Collection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Disease Diagnostic Volumes | +1.2% | National, concentrated in high-prevalence states across the Southeast, Midwest, and Appalachian regions | Long term (≥ 4 years) |

| High Blood Testing Intensity Across Hospitals and Labs | +0.9% | National, particularly high throughput in Northeast and urban hospital systems | Medium term (2-4 years) |

| Sustained Blood Donation and Transfusion Support Needs | +0.6% | National, strongest draw pressure in community blood center markets across the Southeast and Sun Belt | Long term (≥ 4 years) |

| Shift Toward Safety-Engineered Collection Devices | +0.5% | National, driven by OSHA Bloodborne Pathogens compliance mandates across all states | Medium term (2-4 years) |

| Adult Fingertip Collection Moving into Routine Testing | +0.4% | National, early gains in outpatient and primary care settings in suburban and rural corridors | Short term (≤ 2 years) |

| At-Home and Decentralized Microsampling Expansion | +0.7% | National, accelerated in geographically dispersed regions including the Mountain West, rural South, and Alaska | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Diagnostic Volumes

The strongest long-cycle demand support for the blood collection market comes from the continued burden of chronic disease across the adult population. CDC reporting showed that multiple chronic conditions remained widespread among U.S. adults and that the rise extended into younger age groups, which means diagnostic monitoring begins earlier and continues for longer periods across the care journey.[1]Centers for Disease Control and Prevention, “Trends in Multiple Chronic Conditions Among US Adults, By Life Stage, Behavioral Risk Factor Surveillance System, 2013–2023,” Preventing Chronic Disease, cdc.gov That shift matters because patients with diabetes, obesity, cardiovascular risk, and mental health conditions often move into recurring laboratory schedules that require specimen collection across primary care, specialist visits, and ambulatory settings. The blood collection market, therefore, benefits from volume durability rather than one-time spikes, since every additional monitored condition raises the likelihood of repeated blood draws during routine care. Cancer care adds another layer of recurring need because blood products are heavily used in oncology treatment pathways and supportive care. This demand pattern gives suppliers a stable base for tubes, needles, lancets, collection sets, and related consumables, even when broader healthcare spending conditions become less predictable.

Sustained Blood Donation and Transfusion Support Needs

The blood collection market also draws support from the ongoing need to maintain a functioning national blood supply. America’s Blood Centers reported that more than 15 million blood products were transfused in the United States and that transfusions continue at a very high daily rate, which keeps collection activity essential for hospitals and community blood networks.[2]America’s Blood Centers, “U.S. Blood Donation Statistics and Public Messaging Guide,” America’s Blood Centers, americasblood.org AABB findings also showed that collection mix is moving toward apheresis-based component collection, with platelet distribution now heavily dependent on apheresis formats and related disposable sets. That shift changes the economics of procurement because automated component collection uses specialized hardware, software, and high-value consumables rather than lower-value whole-blood supplies alone. Low donor participation continues to keep the system tight, which means blood centers need dependable collection infrastructure and strong donor throughput to meet hospital demand. As a result, the blood collection market gains support not only from diagnostic testing but also from the persistent operational need to secure enough donated blood and blood components for clinical use.

Shift Toward Safety-Engineered Collection Devices

Safety requirements are pushing the blood collection market toward higher-value device refresh cycles even when core collection workflows remain familiar. OSHA’s Bloodborne Pathogens standard and the Needlestick Safety and Prevention Act require healthcare employers to evaluate and implement safer sharps devices, which keep procurement focused on protected needles, winged sets, and collection systems with built-in safety features.[3]Occupational Safety and Health Administration, “Bloodborne Pathogens Standard 29 CFR 1910.1030,” U.S. Department of Labor, osha.gov In practical terms, that means hospitals and laboratory networks cannot rely indefinitely on older venipuncture hardware if safer alternatives are available and clinically validated. Suppliers with broad venous access portfolios benefit because compliance reviews often favor standardized platforms that can be deployed across large health systems with consistent training and supply contracts. The blood collection market, therefore, sees support from regulation-driven replacement demand rather than only from patient volume growth. This also helps integrated vendors defend their positions because safety features, training support, and compatibility across holders, sets, and tubes make switching less attractive for large institutional buyers.

At-Home and Decentralized Microsampling Expansion

Decentralized care is opening one of the clearest new demand lanes in the blood collection market. The FDA cleared Truvian Health’s TruVerus system in late 2025, creating a new option for chemistry, immunoassay, and hematology testing from a small capillary sample in decentralized care environments. A 2026 medRxiv study also showed that parent-administered pediatric capillary collection with overnight ambient shipping was feasible across urban, suburban, remote, and Alaskan settings, which supports the case for broader home-based testing logistics. Tasso and ARUP Laboratories further reinforced the clinical direction of this shift by validating a growing panel of assays for capillary microsamples in decentralized research settings. These developments matter because fingertip and other capillary formats are moving beyond pediatric or niche use and are starting to fit adult routine monitoring, research participation, and geographically dispersed care delivery. As that transition continues, demand spreads toward micro-containers, dried blood spot kits, safety lancets, and capillary collection devices that were once peripheral to mainstream clinical workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Donor Participation and Deferral Limitations | -0.3% | National, with acute pressure in underserved and rural markets across the South and Appalachia | Long term (≥ 4 years) |

| Specimen Contamination and Pre-Analytical Error Risk | -0.3% | National, concentrated in high-throughput hospital labs and blood culture-intensive ICU settings | Medium term (2-4 years) |

| Phlebotomy and Laboratory Staffing Shortages | -0.4% | National, most severe in rural hospitals, long-term care settings, and mobile collection services | Medium term (2-4 years) |

| Intermittent Collection-Container Supply Disruptions | -0.2% | National, historically acute in high-volume urban hospital systems with concentrated procurement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Phlebotomy and Laboratory Staffing Shortages

Workforce limitations remain a material constraint on how much collection capacity the blood collection market can convert into realized volume. The U.S. Bureau of Labor Statistics expects phlebotomist employment to grow 6% from 2024 to 2034, which signals that demand for draw capacity is rising faster than many providers can staff today. The Medical and Public Health Laboratory Workforce Coalition also reported a training pipeline that remains well below the level needed to fill projected annual openings across the laboratory workforce. When staffing stays tight, facilities face slower throughput, delayed specimen processing, and less flexibility to absorb peaks in diagnostic demand or donor center traffic. That pushes some institutions toward automation and workflow redesign, but it does not fully remove the near-term capacity pressure created by too few trained workers. The result is that the blood collection market has strong underlying demand, yet parts of that demand remain operationally constrained by labor availability in hospitals, laboratories, and mobile services.

Intermittent Collection-Container Supply Disruptions

Supply disruption remains another restraint because many essential consumables still depend on a narrow manufacturing base. The CDC classified the 2024 BD BACTEC blood culture bottle shortage as a critical shortage, and hospitals had to restrict blood culture use in order to preserve available inventory for the most urgent cases. A 2025 study available through PubMed Central showed that some institutions cut blood culture ordering sharply during the shortage period, which demonstrated how quickly collection behavior can change when a core consumable is unavailable. These events do not eliminate underlying diagnostic needs, but they do reduce short-term collection volume and force clinicians to conserve supplies. The same vulnerability can extend to additive chemistries, plastic inputs, and electronic components tied to specialized collection devices and accessories. For the blood collection market, this means supply resilience is not simply a procurement issue because it directly affects test access, workflow continuity, and confidence in single-source product categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tube Dominance Anchors Volume, Capillary Formats Build Momentum

Blood collection tubes held 34.78% of the blood collection market share in 2025, which reflected their central role in routine venipuncture across hospitals, clinics, and laboratories. Serum separation and plain serum tubes continued to support a large share of everyday chemistry and immunoassay workflows, while EDTA tubes remained important for hematology and selected molecular applications. Citrate tubes also stayed relevant in coagulation testing, especially in cardiovascular and thrombosis care pathways where repeat monitoring remains common. Heparin and plasma-oriented formats gained support in testing environments where plasma stability and turnaround efficiency matter for clinical decision making. This broad utility keeps tubes at the core of the blood collection market because they serve the largest installed base of collection and laboratory workflows.

Lancets and capillary micro-collection are projected to grow at 5.47% CAGR through 2031, making them the fastest-expanding product sub-segment in the United States blood collection market. Their growth is tied to safety lancets, micro-containers, and dried blood spot kits that fit self-collection, outpatient convenience, and decentralized programs. Truvian’s 2025 FDA clearance showed that small-volume capillary samples can support a wider menu of testing in compact settings, which strengthens the case for broader adult adoption of microsampling devices. Tasso’s 2025 collaboration with ARUP Laboratories also supported assay validation from capillary microsamples, which helps move capillary collection from limited-use cases toward more routine workflows. As this product mix broadens, tubes are likely to retain scale leadership, while capillary formats supply much of the incremental growth in the blood collection market.

By Site of Collection: Venous Throughput Leads, Capillary Improves Access and Convenience

Venous collection accounted for 40.57% of revenue in 2025, which kept it as the leading site of collection across the United States blood collection market. That position reflects the continued need for larger specimen volumes in inpatient diagnostics, outpatient testing, donor collection, and apheresis procedures. Venous workflows remain deeply embedded in clinical operations because they support broad analyte menus, high-throughput phlebotomy, and compatibility with established laboratory instruments. OSHA rules and the Needlestick Safety and Prevention Act also support recurring replacement of venous access hardware with safer designs, which sustains procurement activity around needles and winged sets. For large hospitals and diagnostic networks, venous collection remains the default route wherever volume, standardization, and menu breadth outweigh convenience considerations.

Capillary collection is expected to grow at 5.28% CAGR through 2031, making it the fastest-rising site sub-segment in the blood collection market size outlook. Its growth reflects stronger acceptance of fingerstick and pediatric home collection in settings where venipuncture is less practical or less desirable. The 2026 RedDrop ONE study showed that parent-administered capillary collection can work across varied geographies with overnight ambient shipping to a CLIA-certified lab, which gives the model real operational relevance beyond pilot settings. Tasso and ARUP Laboratories also demonstrated broader assay validation potential for decentralized microsampling, which improves confidence in capillary workflows for research and monitored care use cases. Capillary collection is unlikely to displace venous methods at scale in the near term, but it is reshaping how the United States blood collection market reaches patients outside traditional draw sites.

By Method: Manual Workflows Hold Scale, Automation Improves Yield and Efficiency

Manual blood collection represented 27.36% of revenue in 2025, which made it the largest method segment across the blood collection market. That dominance came from standard venipuncture in outpatient settings, physician offices, smaller hospitals, and community blood center workflows, where lower capital intensity still matters. Manual systems also remain attractive because training requirements are well understood, and facilities can adapt quickly without committing to large platform investments. For donor collection, manual whole-blood workflows continue to provide the operational base that supports much of the country’s collection infrastructure through community blood centers. This keeps manual collection highly relevant even as higher-value automation grows faster from a smaller base.

Automated blood collection is projected to expand at 5.89% CAGR through 2031, making it the fastest-growing method segment in the United States blood collection market. Growth is strongest in apheresis and plasma collection, where software, donor-specific optimization, and recurring disposable pull-through make automation financially attractive. Fresenius Kabi received FDA clearance in 2025 for its Adaptive Nomogram software on the Aurora Xi Plasmapheresis System, and the company stated that the technology was deployed nationally at BioLife Plasma Centers. Haemonetics also highlighted strong fiscal 2026 growth in plasma collection and linked Persona PLUS technology to higher per-donation yield on the NexSys PCS platform. As a result, automation is rebalancing the economics of the blood collection market even while manual collection continues to define the overall scale.

By Application: Diagnostics Holds Revenue Leadership, Transfusion Support Advances Faster

Diagnostics accounted for 50.73% of the blood collection market size in 2025, which made it the largest application segment by a wide margin. That leadership reflects the basic role of blood sampling in chemistry, hematology, immunoassay, infectious disease testing, and a broad range of physician-ordered panels used in everyday care. Diagnostic demand stays broad because blood tests are embedded in screening, treatment monitoring, chronic disease management, acute care triage, and preventive visits. The segment also benefits from the large installed base of phlebotomy and laboratory workflows that already rely on standardized tube formats, holders, and needles. This gives the blood collection market a steady revenue base even when faster-growing niches such as advanced molecular testing or home collection are still building scale.

Treatment and transfusion support is forecast to grow at 6.66% CAGR through 2031, which makes it the fastest-growing application segment in the United States blood collection market. The segment is benefiting from rising reliance on component collection, strong platelet demand, and the continued importance of blood products in oncology and chronic transfusion care. AABB reported that apheresis platelets now represent nearly all platelet distributions and that pathogen-reduced platelet transfusions have expanded rapidly, which increases demand for specialized collection sets and related consumables. Research and clinical trials remain smaller in value terms, but decentralized studies and remote specimen models are making this application more strategically important for capillary and microsampling suppliers. This mix means diagnostics still anchors scale, while transfusion support provides the faster growth path for the broader blood collection market.

By End Use: Hospitals Lead Procurement, Blood Centers Gain Momentum

Hospitals held 44.21% of revenue in 2025, which kept them as the largest end-use segment across the blood collection market. Their leading role comes from the combination of inpatient diagnostics, outpatient follow-up, emergency care, surgical support, and transfusion needs handled within hospital networks. America’s Blood Centers noted that blood transfusion is involved in a meaningful share of hospitalizations and remains especially common in older patient groups, which supports strong ongoing demand for blood bags, collection sets, and diagnostic blood draws. Hospitals also purchase at scale through standardized contracts, which favors suppliers that can support broad portfolios and dependable delivery. This makes the hospital channel central to pricing, product standardization, and vendor positioning in the United States blood collection market.

Blood banks and blood centers are projected to grow at 6.13% CAGR through 2031, which makes them the fastest-growing end-use tier in the blood collection market size outlook. The key driver is the shift from whole-blood collection toward apheresis-led component collection, which raises the value of each collection event through specialized disposables and automated systems. AABB data showed that apheresis platelets dominate platelet distribution, and that trend supports a stronger spending profile for advanced collection technologies within blood center operations. Laboratories remain another important end-use group because large-volume diagnostic processing relies on a stable supply of tubes, needles, and related accessories across centralized testing networks. Home programs, physician offices, ambulatory centers, and emergency departments are also growing in relevance as the blood collection market expands into lower-acuity and more distributed care settings.

Geography Analysis

The United States blood collection market operates within one federal regulatory structure, but regional healthcare density still shapes where procurement intensity is highest. The Northeast remains one of the most concentrated demand centers because it combines academic medical centers, oncology networks, large hospital systems, and dense outpatient referral patterns that support frequent diagnostic blood draws. Established laboratory and hospital supply relationships in this region also tend to favor large vendors with broad product portfolios, validated quality systems, and dependable logistics. These conditions keep the blood collection market especially stable in the Northeast, where volume discipline and supply continuity often matter as much as product innovation.

The South and Southeast present some of the strongest growth conditions in the United States blood collection market because chronic disease burden is high and access gaps are wider in many communities. CDC chronic disease indicators continue to show elevated disease burden across several Southern states, which supports long monitoring cycles and recurring specimen demand in both urban and rural settings. Rural service gaps also make decentralized models more relevant, since remote collection can ease distance barriers for follow-up testing and chronic care management. Blood center activity is also important in the region because transplant programs, oncology demand, and population growth support higher collection needs over time. The Midwest remains a steady procurement region because it includes large community blood center operations and hospital networks that support ongoing demand for whole-blood and apheresis collection infrastructure.

The West and Pacific regions are shaping the innovation side of the blood collection market through stronger adoption of microsampling, digital care models, and distributed testing workflows. Tasso’s 2025 collaboration with ARUP Laboratories and the multi-state 2026 pediatric home collection study both showed how Western-led innovation is helping remote blood collection move into more practical clinical use. The region also benefits from a strong concentration of medical device developers working on capillary sampling and convenience-led collection formats. FDA 510(k) clearances for new collection systems continue to set the commercial pace for these entrants, regardless of where they are based. This keeps the West important not only as a demand region, but also as a product development and early adoption center for the next phase of the United States blood collection market.

Competitive Landscape

The United States blood collection market is moderately concentrated at the top, with a small group of established suppliers holding strong positions across tubes, needles, safety devices, and automated component collection systems. BD remains the broadest platform player because it spans core venous consumables and continues to add new cleared products to its portfolio, including multiple 510(k) clearances in 2026 for blood collection sets, arterial syringes, and plasma-oriented tube formats. In February 2026, BD also completed the separation of its Biosciences and Diagnostic Solutions business into Waters, which narrowed its direct diagnostics exposure while leaving its core collection franchise strategically important to hospital procurement. Greiner Bio-One and SARSTEDT continue to compete effectively in venous collection, especially where safety features, tube chemistry quality, and institutional standardization remain central to vendor selection.

Automated apheresis is more concentrated because a smaller group of companies controls the relevant installed base and recurring disposable demand. Haemonetics strengthened its position in 2026 through Persona PLUS on NexSys PCS and through the Vivasure Medical acquisition, while also reporting strong plasma collection performance in its investor materials. Fresenius Kabi added competitive pressure after receiving FDA clearance for the Adaptive Nomogram on Aurora Xi and rolling the software into national plasma center operations. These moves matter because yield optimization, donor throughput, and disposable pull-through often determine switching decisions in automated collection. The blood collection market, therefore, rewards companies that can tie hardware, software, and service together in a way that improves donor economics for large collection networks. This integrated model gives incumbents a defensible advantage in the most specialized parts of the United States blood collection market.

The capillary and remote collection space remains more open than mainstream venous collection, which is why smaller innovators still have room to gain attention. Truvian’s FDA-cleared small-sample system and Tasso’s continued work with ARUP Laboratories show that convenience-led collection can move into more clinically credible territory when device performance is tied to validated testing use cases. Retractable Technologies also improved its position in 2025 through revenue growth and a Vizient Innovative Technology designation for its EasyPoint blood collection holder with needle, which can help expand group purchasing access in health systems. Competition in the United States blood collection market is therefore strongest where patient convenience, safety, and workflow compatibility intersect. That structure supports stable leadership at the top of the blood collection market, while still leaving room for selective disruption in capillary, decentralized, and patient-managed collection formats.

United States Blood Collection Industry Leaders

Becton, Dickinson and Company

Terumo Blood and Cell Technologies

Cardinal Health, Inc.

Nipro Medical Corporation

QIAGEN N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: BD received FDA 510(k) clearance (K252506) for the BD Vacutainer Safety-Lok Blood Collection Set with Pre-Attached Holder, reinforcing its safety-engineered venipuncture portfolio for OSHA-compliant hospital procurement cycles.

- April 2026: BD's BD Preset and BD A-Line Arterial Blood Collection Syringes received FDA 510(k) clearance (K260128), expanding its arterial blood gas collection range for critical care and ICU settings.

- March 2026: BD Vacutainer Plasma Separator Tubes and Sodium Heparin Blood Collection Tubes received 510(k) clearance (K252040), adding validated plasma chemistry formats to the Vacutainer line for routine clinical chemistry testing.

- February 2026: BD completed the separation of its Biosciences and Diagnostic Solutions business, including the BACTEC blood culture media platform, to Waters Corporation, fundamentally reshaping BD's collection portfolio and creating an independent specialty diagnostics entity within Waters' commercial infrastructure.

United States Blood Collection Market Report Scope

The United States Blood Collection Market comprises the medical devices, equipment, and services required to draw, process, and transport blood from patients or donors. It is primarily driven by the rising prevalence of chronic diseases, increasing surgical interventions, and the ongoing need for diagnostic screenings and transfusions.

The United States Blood Collection Market Report is segmented across several dimensions that define its scope and structure. By product type, it includes tubes, needles and sets, blood bags, lancets, and collection systems. By site of collection, the market is divided into venous and capillary methods. In terms of method, segmentation covers both manual and automated approaches. By application, the market encompasses diagnostics, transfusion support, and research. Segmentation by end use highlights adoption across hospitals, laboratories, blood banks, and physician offices. Finally, by geography, the scope is focused on the United States, with market forecasts provided in terms of value (USD), reflecting the financial scale and growth potential of these product categories.

| Blood collection tubes | Serum separation and plain serum tubes |

| Plasma and heparin tubes | |

| EDTA tubes | |

| Citrate and coagulation tubes | |

| ESR and specialty analyte-preservation tubes | |

| Blood collection needles and sets | Multi-sample needles |

| Winged blood collection sets | |

| Holders and luer adapters | |

| Blood bags and whole-blood collection disposables | Whole-blood bag systems |

| Leukoreduction and sampling accessories | |

| Lancets and capillary micro-collection | Safety lancets |

| Micro-containers and micro-hematocrit tubes | |

| Dried blood spot and microsampling kits | |

| Collection systems and accessories | Blood transfer devices |

| Specimen-diversion and blood-culture collection systems | |

| Manual collection monitors and mixers | |

| Automated apheresis and component-collection systems |

| Venous | Diagnostic venipuncture |

| Donor whole-blood and component collection | |

| Capillary | Fingerstick sampling |

| Heelstick and pediatric sampling |

| Manual blood collection | Standard venipuncture workflows |

| Manual donor whole-blood collection | |

| Automated blood collection | Apheresis and component collection |

| Assisted automated sample-preparation workflows |

| Diagnostics | Clinical chemistry and immunoassay testing |

| Hematology and coagulation testing | |

| Infectious disease testing | |

| Molecular, genomic, and liquid biopsy testing | |

| Treatment and transfusion support | Whole-blood donation |

| Component collection and transfusion support | |

| Research and clinical trials | Biobanking and translational research |

| Decentralized sample-collection studies |

| Hospitals |

| Clinical and diagnostic laboratories |

| Blood banks and blood centers |

| Physician offices and ambulatory care centers |

| Emergency departments and mobile services |

| Academic and research institutes |

| Home and decentralized collection programs |

| By Product Type | Blood collection tubes | Serum separation and plain serum tubes |

| Plasma and heparin tubes | ||

| EDTA tubes | ||

| Citrate and coagulation tubes | ||

| ESR and specialty analyte-preservation tubes | ||

| Blood collection needles and sets | Multi-sample needles | |

| Winged blood collection sets | ||

| Holders and luer adapters | ||

| Blood bags and whole-blood collection disposables | Whole-blood bag systems | |

| Leukoreduction and sampling accessories | ||

| Lancets and capillary micro-collection | Safety lancets | |

| Micro-containers and micro-hematocrit tubes | ||

| Dried blood spot and microsampling kits | ||

| Collection systems and accessories | Blood transfer devices | |

| Specimen-diversion and blood-culture collection systems | ||

| Manual collection monitors and mixers | ||

| Automated apheresis and component-collection systems | ||

| By Site of Collection | Venous | Diagnostic venipuncture |

| Donor whole-blood and component collection | ||

| Capillary | Fingerstick sampling | |

| Heelstick and pediatric sampling | ||

| By Method | Manual blood collection | Standard venipuncture workflows |

| Manual donor whole-blood collection | ||

| Automated blood collection | Apheresis and component collection | |

| Assisted automated sample-preparation workflows | ||

| By Application | Diagnostics | Clinical chemistry and immunoassay testing |

| Hematology and coagulation testing | ||

| Infectious disease testing | ||

| Molecular, genomic, and liquid biopsy testing | ||

| Treatment and transfusion support | Whole-blood donation | |

| Component collection and transfusion support | ||

| Research and clinical trials | Biobanking and translational research | |

| Decentralized sample-collection studies | ||

| By End Use | Hospitals | |

| Clinical and diagnostic laboratories | ||

| Blood banks and blood centers | ||

| Physician offices and ambulatory care centers | ||

| Emergency departments and mobile services | ||

| Academic and research institutes | ||

| Home and decentralized collection programs | ||

Key Questions Answered in the Report

What is the projected value of the United States blood collection market by 2031?

The United States blood collection market is projected to reach USD 3.83 billion by 2031, rising from USD 3.06 billion in 2026 at a 4.61% CAGR.

Which product category leads revenue in blood collection in the United States?

Blood collection tubes led product revenue with a 34.78% share in 2025 because they remain central to routine venipuncture and laboratory workflows.

Which segment is growing fastest in the United States blood collection products?

Lancets and capillary micro-collection are forecast to grow fastest at 5.47% CAGR through 2031, supported by self-sampling and decentralized testing use cases.

Why are hospitals still the leading end users for blood collection products?

Hospitals held 44.21% of revenue in 2025 because they combine inpatient diagnostics, emergency care, surgery, outpatient follow-up, and transfusion demand in one procurement channel.

How is home-based sampling changing blood collection in the United States?

Home and decentralized sampling are expanding demand for capillary devices, micro-containers, and dried blood spot formats as validated logistics and FDA-cleared systems improve adoption.

Page last updated on: