Blood Collection Tubes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 3.54 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Collection Tubes Market Analysis by Mordor Intelligence

The blood collection tubes market size in 2026 is estimated at USD 2.55 billion, growing from 2025 value of USD 2.39 billion with 2031 projections showing USD 3.54 billion, growing at 6.75% CAGR over 2026-2031. Growth rests on the rebound in global diagnostic volumes, rapid technology upgrades in vacuum systems, and greater emphasis on patient-centric testing that collectively lift demand across hospitals, laboratories, and decentralized sites. Manufacturers are responding with hybrid materials that balance safety and sustainability, while automation—from capillary mini-draw devices to fully robotic phlebotomy—elevates both throughput and specimen integrity. At the same time, regulatory harmonization, exemplified by the FDA’s adoption of ISO 13485:2016, reduces compliance friction and supports cross-border production. Competitive focus is turning toward integrated solutions that merge smart tubes, digital tracking, and analytics, setting the stage for differentiated value propositions in an otherwise mature product category.

Key Report Takeaways

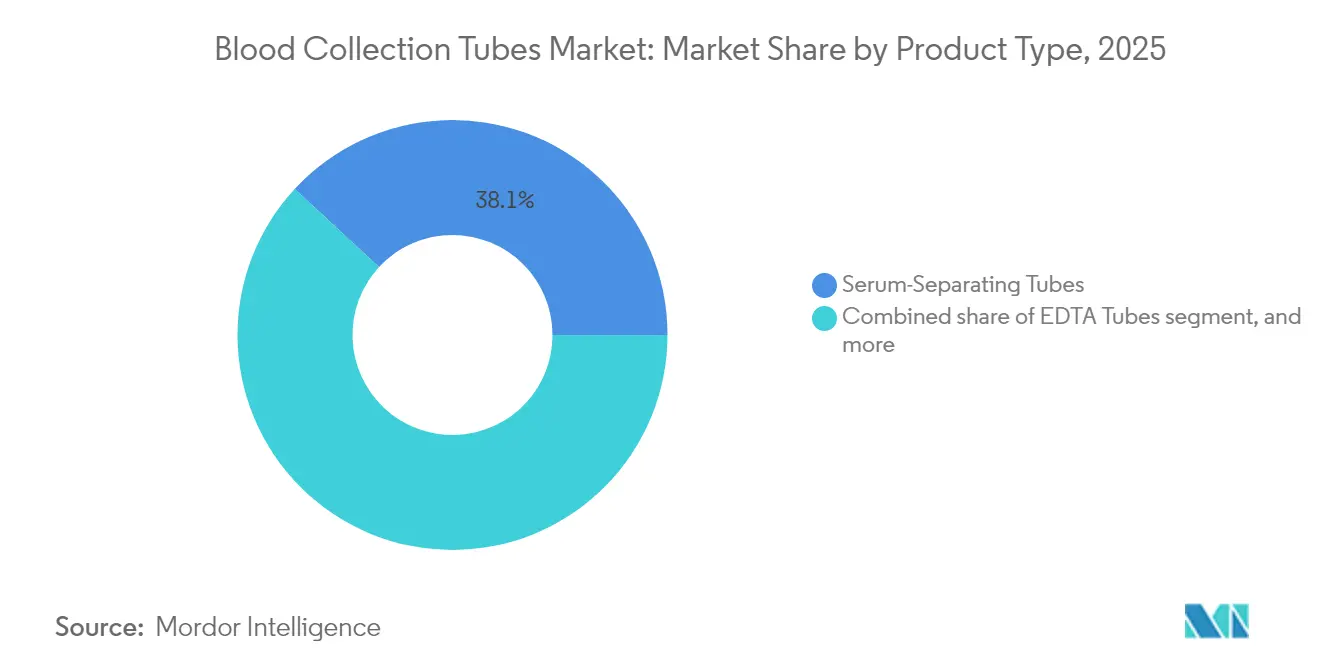

- By product type, serum-separating tubes led with 38.12% revenue share in 2025, whereas plasma-separating tubes are projected to compound at 8.53% CAGR to 2031.

- By material, plastic dominated with 54.92% of the blood collection tubes market share in 2025, while glass is forecast to expand at 8.63% CAGR through 2031.

- By method, vacuum tubes accounted for 46.21% of the blood collection tubes market size in 2025; non-vacuum formats are expected to grow at 8.41% CAGR between 2026 and 2031.

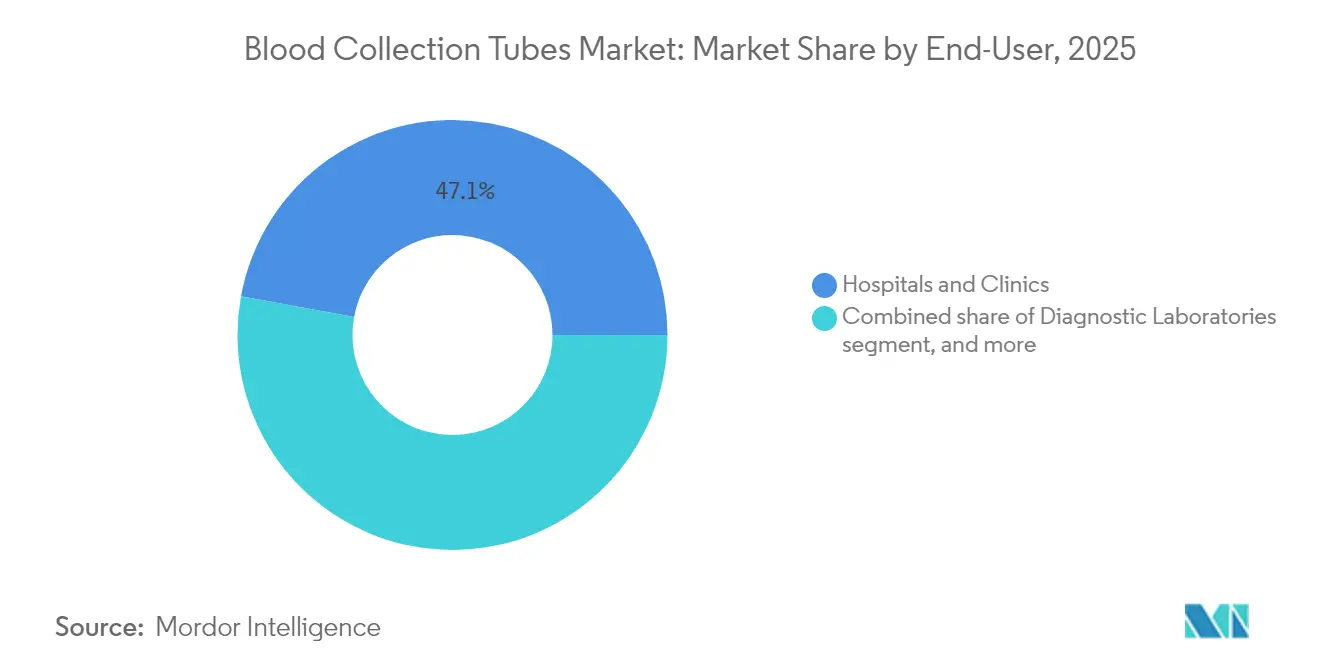

- By end-user, hospitals and clinics commanded 47.12% share in 2025, yet point-of-care and home-care settings will post the fastest 9.55% CAGR to 2031.

- By Application, diagnostics secured 58.09% share in 2025, yet therapeutic segment is projected to grow at 9.33% CAGR.

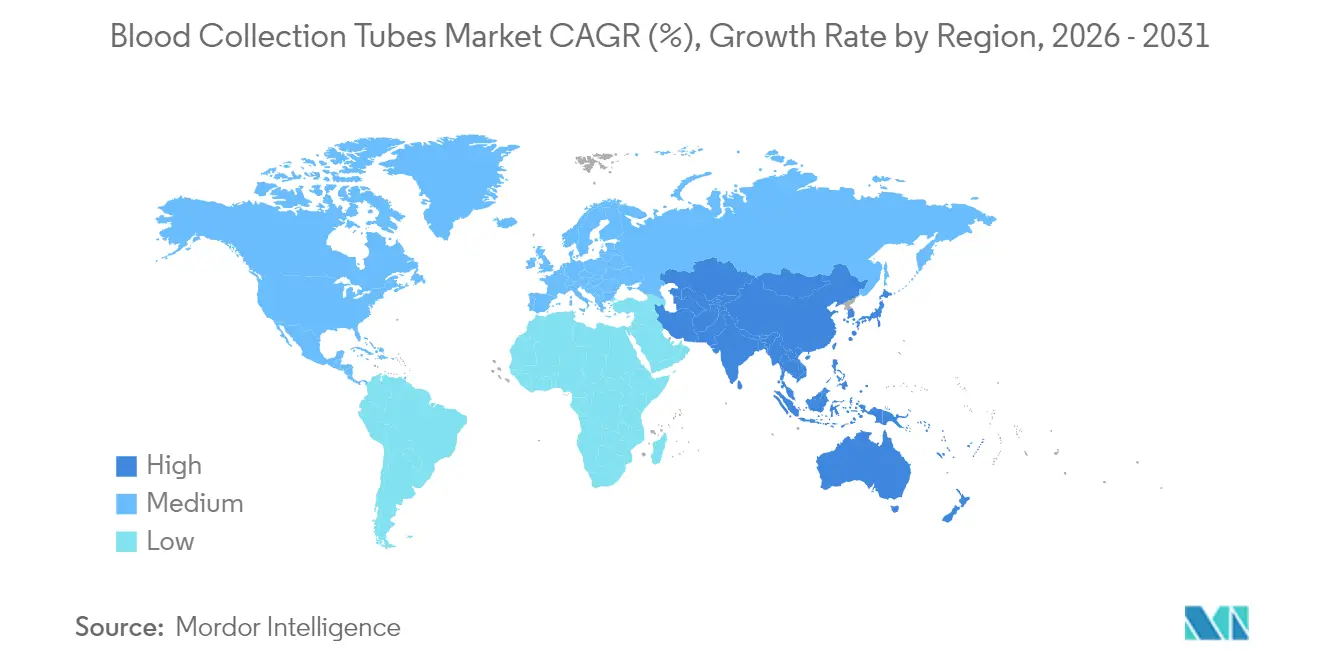

- By geography, North America retained 35.02% share in 2025, while Asia-Pacific is set to climb at a 7.28% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Collection Tubes Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic diseases | +1.2% | Global; strongest in North America and Europe | Long term (≥ 4 years) |

| Expansion of diagnostic testing volume | +1.8% | Global; fastest in Asia-Pacific | Medium term (2-4 years) |

| Rising surgical and trauma procedure rates | +0.9% | North America and Europe; emerging influence in Asia-Pacific | Medium term (2-4 years) |

| Increasing government blood donation drives | +0.7% | Emerging markets in particular | Long term (≥ 4 years) |

| Technological advances in vacuum systems | +1.1% | North America and Europe; extending to Asia-Pacific | Short term (≤ 2 years) |

| Rapid growth of point-of-care testing | +1.3% | Global; pronounced in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic Diseases

Rising incidences of diabetes, cardiovascular ailments, and cancer elevate routine monitoring needs, causing sustained uplift in tube volumes across hospital and outpatient sites. Aging populations in Europe and North America extend baseline demand, whereas emerging economies adopt guideline-based diagnostics that were previously scarce. WHO’s patient-blood-management framework underscores reliable specimen quality as essential for anemia reduction and maternal-health programs[1]World Health Organization, “Guidance on Patient Blood Management,” who.int. Novel tube chemistries that stabilize fragile biomarkers widen the testing menu for chronic-care pathways. As AI-driven platforms gain traction, early-stage detection expands, and high-quality tubes that guard analyte integrity become indispensable, thereby reinforcing the upward trajectory of the blood collection tubes market.

Expansion of Diagnostic Testing Volume

Post-pandemic reforms have permanently enlarged laboratory and point-of-care test menus. High-throughput panels now accompany annual wellness checks, chronic-disease reviews, and targeted screening, each requiring multiple tube types per encounter. Portable analyzers such as Truvian Health’s benchtop unit deliver 98% agreement against core labs, pushing diagnostic reach into pharmacies and community clinics. Precision-medicine initiatives further intensify specimen complexity, as clinicians request biomarker suites that depend on tubes engineered for RNA, cfDNA, or trace elements. This escalating test intensity directly multiplies unit consumption, reinforcing the growth of the blood collection tubes market worldwide.

Technological Advancements in Vacuum Collection Systems

Seventy-five years after the first Vacutainer, next-generation systems marry digital identifiers, closed-loop safety, and material science. BD’s MiniDraw enables finger-stick collection with venous-grade accuracy, serving retail care and home sampling. Hybrid chemo-PET tubes deliver glass-like vapor barriers while retaining shatter resistance, extending shelf life to two years[2]SLAS Technology Editorial Board, “Hybrid Chemo-PET Blood Collection Tubes,” slastech.org. Robotic phlebotomy, spearheaded by Vitestro’s Aletta, achieves 95% first-attempt success and integrates ultrasound guidance for vein mapping. Collectively, these advances elevate efficiency, reduce hemolysis, and unlock new service models that accelerate adoption across the blood collection tubes market.

Rapid Growth of Point-of-Care Testing Market

Decentralized care shifts blood collection from central labs to pharmacies, mobile units, and homes. BD’s collaboration with Babson Diagnostics delivers comprehensive panels using six capillary drops, cutting procedural time and needle anxiety. AI-enabled handheld devices maintain lab-grade precision, empowering non-phlebotomist staff to secure viable specimens. Needle-free systems like PIVO trim preanalytical errors by 56%, improving workflow and patient comfort. These attributes resonate in Asia-Pacific’s community clinics and Europe’s retail care hubs, driving the fastest CAGR segment within the blood collection tubes market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of infection from improper handling | –0.8% | Global; higher in low-resource settings | Medium term (2-4 years) |

| Price sensitivity and reimbursement limits | –1.1% | Global; most acute in emerging markets | Short term (≤ 2 years) |

| Regulatory pressure on single-use plastics | –0.6% | Europe and North America; spreading globally | Long term (≥ 4 years) |

| Volatility in raw-material supply chains | –0.9% | Global; region-specific vulnerabilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Risk of Infection from Improper Blood Handling

Occupational-safety agencies mandate sharps controls, yet uneven training raises exposure to needlestick injuries in resource-constrained hospitals. OSHA calls for puncture-proof containers and immediate disposal, adding operational cost[3]U.S. Department of Labor, “Needlestick Safety and Prevention,” osha.gov. Extreme weather disrupted over 19,000 U.S. donations in 2024, revealing fragility in collection logistics that can escalate contamination risk. Meanwhile, the FDA increased surveillance on substandard plastic syringes, signaling tougher oversight that can delay product releases. Together, these factors temper market expansion where infrastructure and compliance budgets remain thin.

Price Sensitivity and Reimbursement Constraints

Raw-material expenses absorb up to 20% of revenue for device makers, and supply-chain shocks from geopolitical conflicts push costs higher. Emerging-market hospitals face tighter reimbursement caps, compelling tender-driven purchases that favor lower-priced alternatives, even if performance lags. Smaller manufacturers coping with thin margins may delay innovation investments, curbing competitive diversity in the blood collection tubes industry. Policymakers advocating value-based care add further price pressure, squeezing profitability and slowing uptake of premium tube technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plasma Tubes Drive Therapeutic Innovation

Serum-separating formats retained 38.12% share in 2025, anchored in routine chemistry panels across global labs. However, plasma-separating tubes will expand at 8.53% CAGR through 2031 on the back of regenerative-medicine protocols and cell-therapy workflows. Therapeutic applications claim 9.33% CAGR as platelet-rich plasma gains clinical favor for orthopedics and dermatology. Emerging ultrafiltration methods that enrich growth factors sharpen this demand curve and elevate the profile of specialized tubes within the blood collection tubes market.

Capillary micro-collection products are carving a niche in pediatric and point-of-care settings, buoyed by devices such as MiniDraw that reduce draw volumes without compromising analytical scope. EDTA tubes remain indispensable for hematology; rapid-serum variants fill emergency needs where turnaround time dictates clinical action. Collectively, these dynamics foster a balanced but growth-tilted portfolio, ensuring the segment contributes materially to overall blood collection tubes market growth.

By Material: Glass Resurgence Challenges Plastic Dominance

Plastic retained 54.92% of the blood collection tubes market share in 2025 due to breakage resistance and lower cost. Yet glass tubes are slated for the fastest 8.63% CAGR, propelled by sustainability mandates and superior analyte stability in trace-element studies. The EU’s Packaging and Packaging Waste Regulation compels recyclability by 2030, prompting R&D in hybrid tubes that fuse plastic robustness with glass-like vapor barriers.

Advanced chemo-PET variants now rival glass for chemical inertness while staying within biosafety guidelines, positioning them as a mid-transition solution. Recycling pilots in Denmark show promise for circular programs that may blunt regulatory penalties linked to single-use plastics. As these material shifts gain momentum, they reshape procurement criteria and reinforce the competitive stakes in the blood collection tubes market.

By Method: Automation Transforms Collection Paradigms

Vacuum devices made up 46.21% of the segment revenue in 2025, reflecting hospital standardization. Non-vacuum systems-chiefly syringe and capillary formats-will rise at 8.41% CAGR owing to rising decentralized care. Robotic phlebotomy, typified by Vitestro’s Aletta, illustrates a step-change: 95% first-stick success slashes redraws and eases staffing shortages.

Needle-free PIVO adapters integrate with existing IV lines and have demonstrated 56% lower preanalytical errors, underscoring efficiencies from technology cross-pollination. Paired with AI-driven vein visualization, these tools elevate patient experience and data reliability, ultimately reinforcing demand across the blood collection tubes market.

By End-User: Point-of-Care Settings Accelerate Decentralization

Hospitals and clinics generated 47.12% of 2025 revenue, leveraging established laboratories and high acuity caseloads. Yet point-of-care and home-based services will show the strongest 9.55% CAGR, driven by convenience, chronic-care management, and expanding telehealth programs. Diagnostic laboratories remain critical, processing high-volume submissions and mandating standardized tube performance to sustain throughput.

Blood banks and transfusion centers sustain niche but stable growth, boosted by therapeutic apheresis and immunoglobulin self-sufficiency targets set by public health agencies. Collectively, shifting sample-flow patterns intensify product diversification and help lift overall blood collection tubes market growth prospects.

By Application: Therapeutics Reshape Collection Requirements

Diagnostics secured 58.09% share in 2025 and will remain foundational, yet therapeutic uses—including transfusion and cell therapy—are set for 9.33% CAGR on the back of regenerative-medicine breakthroughs. Standardized platelet-lysate protocols across European establishments provide reproducible inputs for cell expansion, anchoring demand for plasma-optimized tubes.

National programs, such as the NHS’s push to supply home-grown plasma therapies to 17,000 patients annually, further amplify specialized-tube consumption. Integration of diagnostic-therapeutic workflows in precision medicine aligns with tubes that preserve both cellular and molecular cargo, reinforcing convergence trends within the blood collection tubes market.

Geography Analysis

North America commanded 35.02% revenue share in 2025, a position underpinned by mature diagnostics infrastructure and early adoption of automation. The FDA’s Quality Management System Regulation, effective 2026, harmonizes requirements with ISO 13485:2016 and simplifies device clearances, encouraging domestic production and exports. BD’s pledge to invest USD 2.5 billion in U.S. capacity underscores confidence in steady regional demand. Weather-related donation shortfalls during 2024 spotlight resiliency gaps that may shape future infrastructure spending.

Asia-Pacific is projected to clock a 7.28% CAGR to 2031, powered by healthcare expansions under China’s “Healthy China 2030” and India’s widening lab networks. Terumo’s USD 15 million localization spend demonstrates the pull of regional scale and regulatory incentives. Rising per-capita outlays and government focus on AI enable leapfrog adoption of advanced collection and testing systems, positioning the region as the dynamo of blood collection tubes market growth.

Europe holds a robust share, strengthened by policy leadership in sustainability. The Packaging and Packaging Waste Regulation catalyzes material innovation, and collaborative platelet-lysate standardization across EU centers ensures high-quality therapeutic inputs. The NHS target of 25% plasma self-sufficiency by 2025 signals dependable domestic uptake, whereas smaller Eastern European markets offer incremental gains as infrastructure modernizes. Collectively, these geographies forge a balanced demand mix that underpins the global blood collection tubes market’s resilient outlook.

Competitive Landscape

Market leadership remains moderately consolidated, with BD, Greiner Bio-One, and Terumo anchoring roughly half of global revenue. BD’s strategic spin-off of Biosciences and Diagnostic Solutions aims to create a pure-play MedTech entity focused on integrated collection-to-analysis offerings. Greiner Bio-One intensifies U.S. expansion through its Preanalytics business, leveraging a broad tube portfolio and proprietary additives. Terumo’s localization in China strengthens regional responsiveness while extending the reach of its Reveos™ automated processing platform.

Innovation rivalry orbits around three axes: autonomous phlebotomy, sustainable materials, and smart traceability. Vitestro’s CE-marked Aletta robot exemplifies disruptive potential, pairing AI with robotics to reduce dependency on skilled phlebotomists and speed large-volume draws. Material hybrids such as chemo-PET and multi-layer glass-plastic composites promise heightened analyte stability without sacrificing safety, differentiating newer entrants against incumbents.

Strategic alliances supplement organic R&D. BD’s capillary-testing pact with Babson Diagnostics broadens point-of-care reach, while Terumo’s collaboration with Sanquin automates Dutch blood-processing pipelines. As regulatory scrutiny escalates and sustainability directives tighten, competitive advantage will hinge on agility in compliance and eco-design, setting the stage for continued evolution within the blood collection tubes industry.

Blood Collection Tubes Industry Leaders

Becton, Dickinson & Company

Greiner Bio-One International GmbH

Terumo Corporation

Sarstedt AG & Co. KG

Qiagen N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BD and Babson Diagnostics confirmed that BD MiniDraw™ capillary technology matches venous-draw accuracy, enabling finger-prick panels without specialized phlebotomy staff.

- March 2025: Vitestro introduced Aletta, the first autonomous robotic phlebotomy device, after CE marking and validation in more than 4,000 patients.

- February 2025: BD announced plans to separate its Biosciences and Diagnostic Solutions unit to sharpen MedTech focus and target USD 17.8 billion in FY 2024 revenue.

- February 2025: Sanquin partnered with Terumo BCT to deploy Reveos automated blood processing across the Netherlands, shrinking steps from 26 to 9.

- November 2024: Terumo Blood and Cell Technologies invested USD 15 million to localize Trima Accel and Spectra Optia production in China.

- August 2024: Vitestro secured CE marking for its autonomous blood-drawing robot, paving the way for European deployments.

Global Blood Collection Tubes Market Report Scope

As per the scope of the report, blood collection tubes are sterile glass or plastic test tubes with a colored rubber stopper creating a vacuum seal inside the tube, facilitating the drawing of a predetermined volume of liquid. The Blood Collection Tubes Market is Segmented by Product Type (Serum Separating Tubes, EDTA Tubes, Plasma Separation Tubes, Rapid Serum Tubes, and Others) And Geography (North America, Europe, Asia-pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

| Serum-Separating Tubes |

| EDTA Tubes |

| Plasma-Separating Tubes |

| Rapid Serum Tubes |

| Capillary Micro-Collection Tubes |

| Other Product Types |

| Plastic Tubes |

| Glass Tubes |

| Vacuum Blood Collection Tubes |

| Non-Vacuum / Syringe-Based Tubes |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Blood Banks & Transfusion Centers |

| Point-of-Care / Home-Care Settings |

| Diagnostics |

| Therapeutics (Transfusion / Cell-therapy) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Serum-Separating Tubes | |

| EDTA Tubes | ||

| Plasma-Separating Tubes | ||

| Rapid Serum Tubes | ||

| Capillary Micro-Collection Tubes | ||

| Other Product Types | ||

| By Material | Plastic Tubes | |

| Glass Tubes | ||

| By Method | Vacuum Blood Collection Tubes | |

| Non-Vacuum / Syringe-Based Tubes | ||

| By End-User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Blood Banks & Transfusion Centers | ||

| Point-of-Care / Home-Care Settings | ||

| By Application | Diagnostics | |

| Therapeutics (Transfusion / Cell-therapy) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the blood collection tubes market?

The blood collection tubes market size is valued at USD 2.55 billion in 2026.

Which region is growing fastest in the blood collection tubes market?

Asia-Pacific is expected to expand at a 7.28% CAGR through 2031, the highest among all regions.

Why are glass blood collection tubes regaining popularity?

Sustainability mandates and superior sample-stability qualities are pushing glass tubes to an 8.63% CAGR, outpacing plastics.

How is automation influencing blood collection practices?

Robotic and AI-guided systems, such as Vitestro’s Aletta, deliver 95% first-stick success and lower preanalytical errors, driving uptake in laboratories and clinics.

What impact will the FDA’s Quality Management System Regulation have?

The rule aligns U.S. requirements with ISO 13485:2016, streamlining global compliance for manufacturers and potentially accelerating product launches.

Which product segment is forecast to grow quickest?

Plasma-separating tubes are projected to grow at 8.53% CAGR due to expanding regenerative-medicine applications.

Page last updated on: