Capillary Blood Collection Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

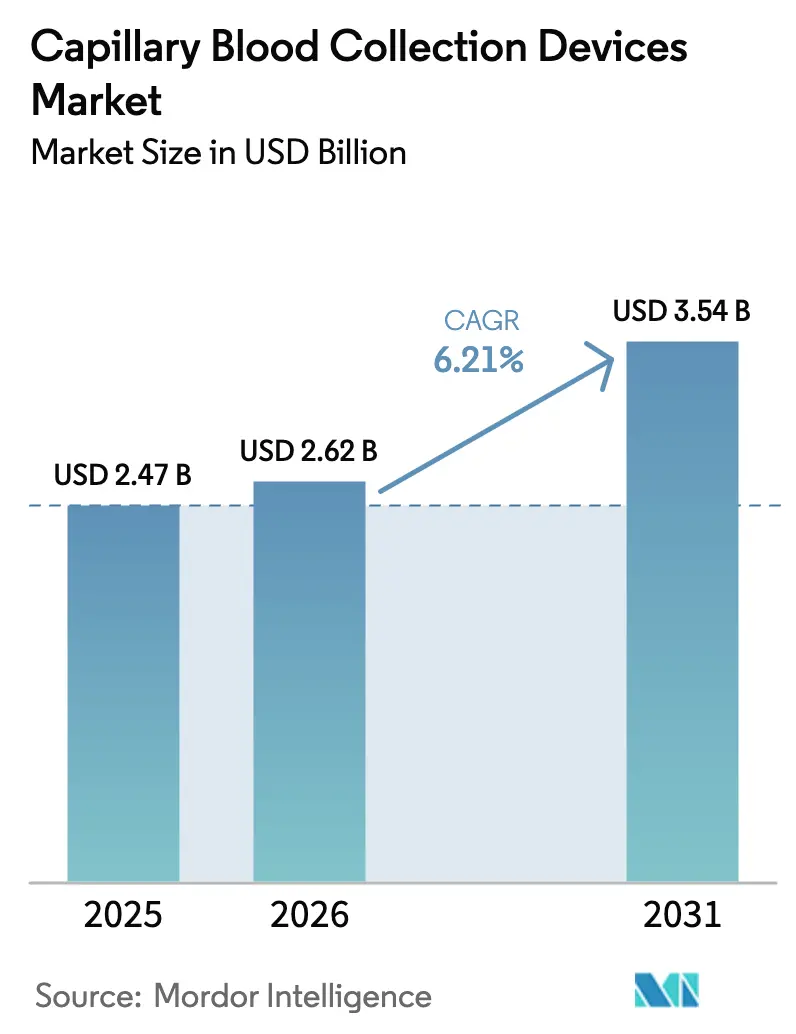

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.54 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Capillary Blood Collection Devices Market Analysis by Mordor Intelligence

The capillary blood collection devices market size is expected to grow from USD 2.47 billion in 2025 to USD 2.62 billion in 2026 and is forecast to reach USD 3.54 billion by 2031 at 6.21% CAGR over 2026-2031. Growth is underpinned by the rapid move toward minimally invasive diagnostics, wider deployment of point-of-care testing networks, and steady technological improvements in volumetric microsampling and dried blood spot (DBS) formats. Healthcare providers are prioritizing devices that reduce patient discomfort, support remote monitoring, and lower logistics costs, allowing decentralized testing models to flourish. Vendors able to integrate automated sampling with digital reporting workflows are capturing early-mover advantages, especially where chronic disease monitoring requires high testing frequency. At the same time, competition from emerging non-invasive technologies is sharpening the need for continual product differentiation and robust regulatory strategies.

Key Report Takeaways

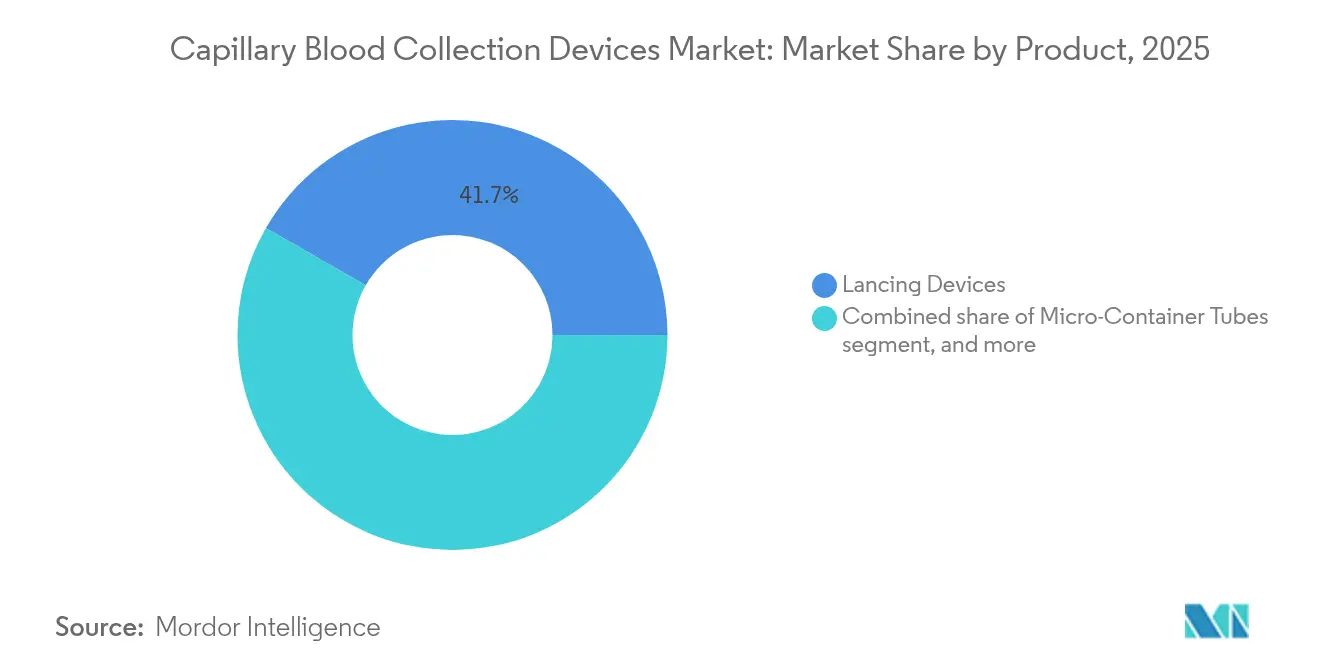

- By product category, lancing devices held 41.72% of the capillary blood collection devices market share in 2025; DBS cards are forecast to advance at an 8.47% CAGR through 2031.

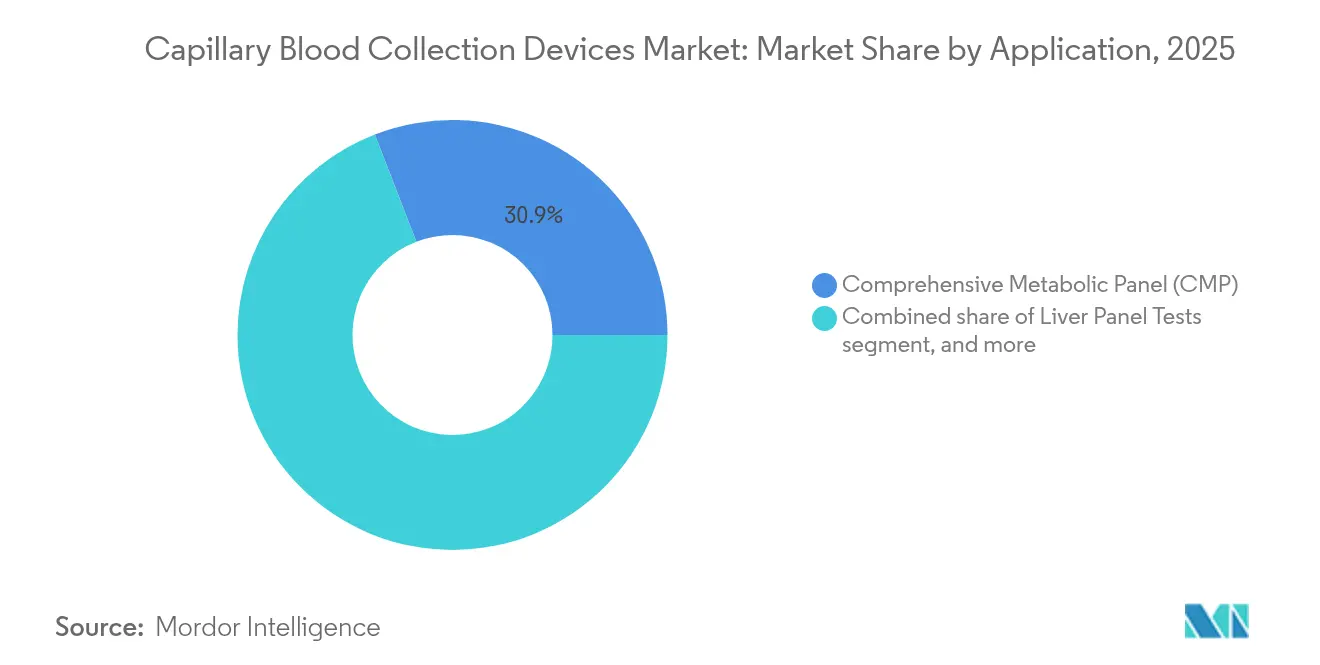

- By application, comprehensive metabolic panel testing accounted for 30.88% share of the capillary blood collection devices market size in 2025, while genetic and neonatal screening is projected to expand at an 8.61% CAGR to 2031.

- By end user, hospitals and clinics commanded 46.95% share of the capillary blood collection devices market size in 2025; home care settings are poised to grow at 9.37% CAGR between 2026-2031.

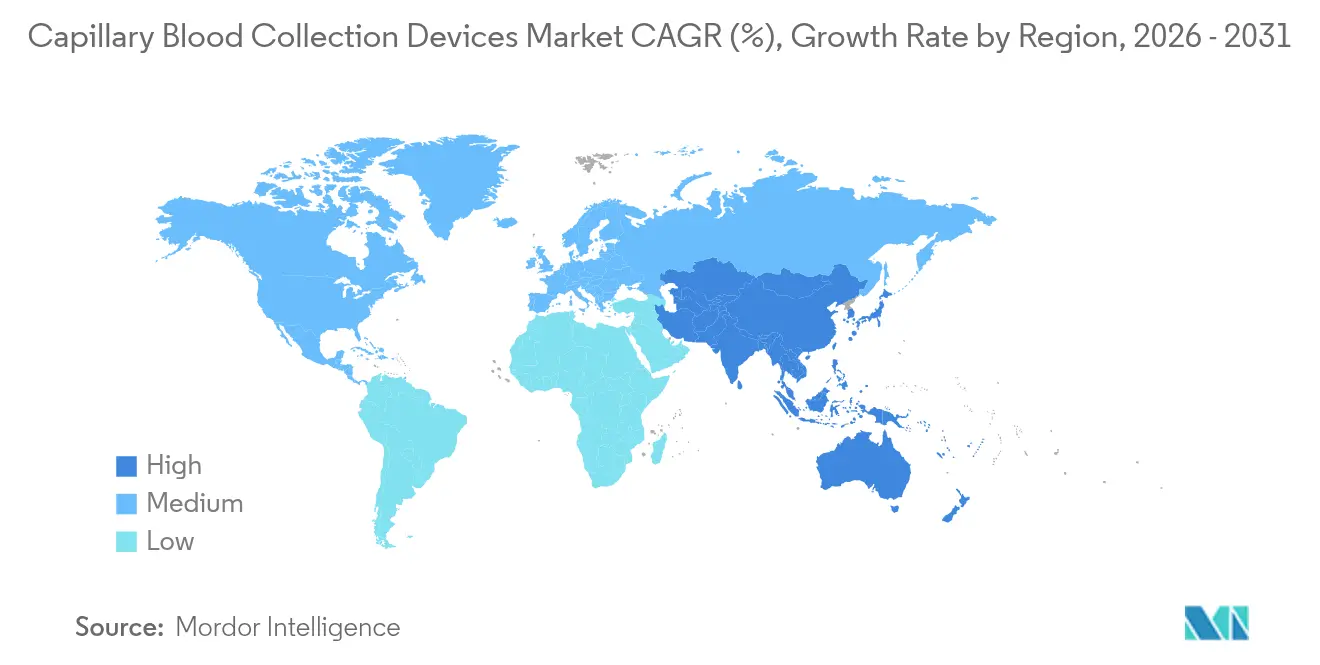

- By geography, North America led with 39.41% of the capillary blood collection devices market share in 2025, whereas Asia-Pacific is set to register a 7.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Capillary Blood Collection Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing burden of chronic and infectious diseases | +1.8% | Global, highest in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Expansion of point-of-care diagnostic infrastructure | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Growing adoption of at-home testing services | +1.2% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Technological advancements in microsampling devices | +1.0% | Global, innovation centers in North America and Europe | Medium term (2-4 years) |

| Favorable reimbursement policies for capillary testing | +0.7% | Primarily North America and Europe | Long term (≥ 4 years) |

| Rising healthcare expenditure in emerging economies | +0.9% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Burden of Chronic and Infectious Diseases

Rising prevalence of diabetes, cardiovascular disorders, and emerging infectious threats is pushing healthcare systems to adopt testing protocols that enable frequent sampling with minimal invasiveness. Diabetes management alone often demands several glucose checks each day, making capillary collection more practical than venous draws for routine self-monitoring. During the COVID-19 crisis, decentralized sampling models proved valuable for rapid triage and remote surveillance, highlighting the versatility of DBS and microsampling formats. Cardiovascular care is likewise adopting capillary-based assays for biomarkers such as HbA1c and high-sensitivity C-reactive protein, broadening the clinical scope of these devices[1]American Heart Association, “Capillary Sampling and Cardiovascular Biomarkers,” heart.org. As chronic disease programs pivot toward patient-centric models, high-throughput yet low-volume sampling tools will remain integral to care pathways across both developed and emerging economies.

Expansion of Point-of-Care Diagnostic Infrastructure

Retail pharmacies, emergency departments, and community clinics are investing in compact analyzers that depend on capillary specimens for rapid turnaround. Global point-of-care testing revenues are projected to exceed USD 55 billion by 2030, creating a direct pull for compatible sampling hardware. The BD MiniDraw platform, now deployed within pharmacy pilots, allows staff without phlebotomy certification to collect high-quality microsamples in under two minutes, reducing workflow bottlenecks. Such infrastructure boosts device penetration by embedding capillary sampling capabilities at numerous touchpoints within the continuum of care. As interoperability standards mature, lab networks benefit from streamlined logistics and shorter result cycles, further reinforcing demand.

Growing Adoption of At-Home Testing Services

Consumer demand for convenient, needle-sparing solutions is fueling brisk uptake of direct-to-patient kits that pair mail-back DBS cards with app-based result delivery. At-home diagnostics are on track to surpass USD 45 billion by 2031, and many operators specify capillary formats to avoid cold-chain costs that can be 90% higher for liquid specimens. Partnerships such as Thriva-Tasso target individuals who avoid facility-based draws due to needle anxiety, unlocking a sizeable latent user base. Telehealth pipelines amplify this trend by embedding sampling instructions, courier tracking, and electronic reporting into a single digital interface, encouraging adherence to monitoring regimens for chronic and preventive care alike.

Technological Advancements in Microsampling Devices

Next-generation devices leverage volumetric absorptive microsampling to neutralize hematocrit bias and produce fixed 10-20 µL aliquots with high analytical precision. Automated spring-loaded systems now demonstrate 95% first-stick success and sub-two-minute collection times, meeting stringent hospital workflow demands. Concurrently, biotech researchers are experimenting with bio-inspired lancet geometries that harvest 195 µL with lower pain perception scores, broadening acceptance in pediatrics and geriatrics. Artificial-intelligence-enabled readers further cut interpretation times to under two minutes, aligning capillary workflows with rapid-response clinical settings.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory compliance requirements | −0.8% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Sample volume limitations for advanced assays | −0.6% | Global, notably research applications | Long term (≥ 4 years) |

| Price sensitivity in low-income regions | −0.5% | APAC emerging markets, MEA, Latin America | Long term (≥ 4 years) |

| Competition from non-invasive monitoring technologies | −0.4% | Global, led by developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance Requirements

Capillary devices traverse a complex regulatory landscape with classifications ranging from Class I to Class III depending on intended use. Class II products must file 510(k) premarket notifications, delaying U.S. launches by six to twelve months on average. Quality system rules mandate rigorous design documentation and post-market surveillance, adding annual compliance outlays that can exceed USD 1 million for smaller firms. Recent warning letters, such as the 2025 FDA citation to Q'Apel Medical for design-verification gaps, underscore the reputational and financial hazards of non-compliance[2]U.S. Food & Drug Administration, “Medical Device Warning Letters 2025,” fda.gov. These pressures often push start-ups toward strategic alliances or acquisitions as a means of navigating approval pathways.

Competition From Non-Invasive Monitoring Technologies

Wearable optical sensors and continuous glucose monitors are making inroads by eliminating the need for finger-stick sampling in certain indications. Photoplethysmography-based glucose readings, once considered speculative, now demonstrate clinical-grade accuracy in pilot trials, threatening traditional lancet and strip demand. Hamamatsu Photonics, among others, is refining metabolic-index algorithms to support cuff-less hemodynamic assessments, signaling broader diagnostic ambitions. As reliability improves and reimbursement pathways solidify, the substitution risk for capillary products is likely to rise, compelling manufacturers to diversify into hybrid or adjunct technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Dried Blood Spot Innovation Drives Growth

The capillary blood collection devices market continues to rely on traditional lancets, which captured 41.72% share in 2025 thanks to entrenched use in glucose monitoring and routine hospital testing. Yet DBS cards are now the fastest-advancing format with an 8.47% CAGR, propelled by cold-chain independence and simple self-collection protocols. Integrated kits that bundle lancets, absorbent cards, and prepaid mailers have simplified logistics for home-based programs, supporting broader adoption in telehealth and decentralized clinical trials. Micro-container tubes and micro-hematocrit capillaries remain vital in laboratory workflows that demand precise volume control and centrifugation compatibility. Warming aids and single-use heaters address capillary flow issues in neonatal and geriatric cohorts, reducing re-stick rates and improving sample adequacy.

Technological convergence is redefining the value proposition of DBS platforms. Volumetric absorptive microsampling eliminates hematocrit-linked concentration errors, unlocking therapeutic drug monitoring applications once confined to venous draws. Analytical sensitivity gains now permit multi-analyte panels from a single 10 µL spot, cutting consumable redundancy and patient burden simultaneously. Automated punch-and-elute workstations accelerate downstream processing, making DBS competitive with liquid samples for turnaround-time-sensitive assays. Furthermore, bio-coated sampling cards preserve labile biomarkers, extending stability windows in hot-climate logistics. These advances position DBS solutions as credible alternatives in both high-volume reference labs and low-resource field settings, sustaining expansive tailwinds for the capillary blood collection devices market.

By Application: Genetic Screening Accelerates Market Expansion

Comprehensive metabolic panels commanded 30.88% of the capillary blood collection devices market size in 2025, reflecting their status as the workhorse of routine diagnostics in primary and acute care. Nevertheless, genetic and neonatal screening is charting an 8.61% CAGR as national newborn programs and precision-medicine initiatives converge on early-life genomic testing. DBS-based next-generation sequencing workflows have proven effective for dozens of inherited metabolic disorders from a single heel-prick specimen, reducing the need for repeat sampling. Infectious-disease screens, notably for HIV, hepatitis, and emerging viral pathogens, are also adopting rapid capillary assays to shorten diagnosis-to-care intervals.

Liver function panels and plasma-protein tests remain niche yet indispensable in monitoring hepatotoxic therapies and malnutrition, especially in regions lacking ready access to venous phlebotomy. Whole-blood coagulation and hematology profiles are finding renewed relevance as point-of-care analyzers downsize sample requirements to under 100 µL. Portable molecular platforms such as the Dragonfly unit demonstrate bacteremia detection in under 20 minutes from finger-stick samples, supporting emergency triage workflows. Application diversity is therefore broadening revenue streams and insulating the capillary blood collection devices market from over-reliance on single disease areas.

By End User: Home Care Settings Transform Market Dynamics

Hospitals and clinics retained a dominant 46.95% share of the capillary blood collection devices market size in 2025, buoyed by entrenched procurement contracts and high-volume testing throughput. Yet home care settings are forecast to post a 9.37% CAGR through 2031, spurred by payer incentives for remote monitoring and an aging population seeking in-home chronic-disease management. Direct-to-consumer brands now ship bundled sampling kits with mobile apps that guide users through lancet deployment, sample collection, and courier pickup scheduling.

Diagnostic centers leverage capillary formats to increase patient turnover and reduce overhead linked to venous phlebotomy training, while research laboratories employ microsampling to minimize participant discomfort and improve study retention. Artificial-intelligence-enhanced readers embedded in home-care devices relay result dashboards to clinicians in real time, closing the feedback loop for dose adjustments in transplant medicine or anticoagulation management. The cumulative effect is a sizeable shift toward decentralized networks that collectively expand addressable volumes for the capillary blood collection devices market.

Geography Analysis

North America dominated the capillary blood collection devices market share at 39.41% in 2025 on the back of robust reimbursement policies and early-stage technology adoption. Government funding channels and value-based-care models continue to reward suppliers capable of demonstrating cost offsets through reduced hospital admissions and streamlined laboratory logistics.

Asia-Pacific is forecast to register a 7.5% CAGR, the fastest worldwide, as chronic disease burdens escalate alongside rising middle-class healthcare spending. Public-private partnerships are financing community-level point-of-care labs, while telemedicine laws in markets such as India and China increasingly permit mail-in DBS testing under national guidelines. Regional healthcare expenditure, which climbed 42% between 2019 and 2024, provides fertile ground for vendors tailoring low-cost, ambient-temperature kits that bypass cold-chain constraints.

Europe mirrors a mature uptake curve, gaining incremental growth from aging demographics and pan-regional efforts to harmonize newborn screening programs. Latin America and the Middle East & Africa trail in value terms but deliver upside through pilot installations in urban centers where laboratory infrastructure remains underdeveloped. Financial-inclusion drives and mobile-health campaigns are expected to pull capillary solutions into peripheral regions over the coming decade, ensuring a broadening geographic footprint for the capillary blood collection devices market.

Competitive Landscape

The competitive arena is moderately fragmented, allowing product differentiation rather than price to shape share dynamics. Becton Dickinson leverages its MiniDraw system and global distribution channels to retain cross-segment exposure, while smaller players double down on niche innovation such as needle-free vacuum collection or automated DBS punchers.

M&A activity underscores the premium placed on rapid-diagnostic intellectual property: bioMérieux’s EUR 138 million acquisition of SpinChip Diagnostics brings a 10-minute immunoassay platform under its umbrella, signaling the value incumbents assign to speed and portability. Venture investment has likewise flowed to self-sampling specialists; Capitainer’s USD 2.8 million raise aims to ramp production capacity for volumetric DBS cards suitable for clinical biomarkers and drug monitoring.

Regulatory agility differentiates leaders from laggards. Firms with in-house quality-systems expertise expedite 510(k) clearances and CE marks, while newcomers often partner with contract development organizations to bridge compliance gaps. Patent portfolios around microfluidic channel design, lancet geometry, and anti-hemolysis coatings serve both as deal currency and as defensive moats against commoditization. Collectively, these strategies keep competitive intensity at a balanced level while leaving room for breakthroughs that could reorder the capillary blood collection devices market hierarchy.

Capillary Blood Collection Devices Industry Leaders

Abbott

Bayer AG

Becton, Dickinson and Company

Cardinal Health

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Becton Dickinson and Babson Diagnostics expanded fingertip blood testing across U.S. health systems using the FDA-cleared MiniDraw system to improve access in underserved areas.

- February 2025: Capitainer secured SEK 30 million (USD 2.8 million) from We Venture Capital to scale production of self-sampling blood and plasma collection solutions.

- November 2024: bioMérieux finalized its EUR 138 million acquisition of SpinChip Diagnostics, adding a 10-minute immunoassay platform suited for acute care settings.

- October 2024: Babson Diagnostics welcomed a strategic investment from BD to widen its BetterWay initiative, allowing pharmacies to collect capillary samples without phlebotomists.

- April 2024: Drawbridge Health obtained FDA 510(k) clearance for NanoDrop, the first OTC upper-arm blood-lancing device for at-home use.

- May 2024: Nova Biomedical received FDA clearance for the Stat Profile Prime Plus analyzer’s micro-capillary mode, enabling an 11-test panel from 90 µL of blood.

Global Capillary Blood Collection Devices Market Report Scope

As per the scope of the report, capillary blood collection devices are designed for obtaining small blood samples from capillary punctures, typically in the finger or heel. These devices include lancets for making shallow punctures and micro-collection tubes for holding the blood sample. They are minimally invasive, making them ideal for pediatric, geriatric, and point-of-care testing. Additionally, they are commonly used for glucose monitoring, hemoglobin tests, and neonatal screening.

The capillary blood collection devices market is segmented by product, application, end user, and geography. By product, the market is segmented into lancing devices, micro-container tubes, micro-hematocrit tubes, warming devices, and others. By application, the market is segmented into comprehensive metabolic panel (CMP) tests, liver panel tests, plasma/serum protein tests, whole blood tests and others. By end user, the market is segmented into diagnostic centers, hospitals and clinics, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Lancing Devices |

| Micro-Container Tubes |

| Micro-Hematocrit Tubes |

| Warming Devices |

| Integrated Capillary Collection Kits |

| Dried Blood Spot Cards |

| Comprehensive Metabolic Panel (CMP) |

| Liver Panel Tests |

| Plasma/Serum Protein Tests |

| Whole Blood Tests |

| Infectious Disease Screening |

| Genetic & Neonatal Screening |

| Diagnostic Centers |

| Hospitals & Clinics |

| Home Care Settings |

| Research Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Lancing Devices | |

| Micro-Container Tubes | ||

| Micro-Hematocrit Tubes | ||

| Warming Devices | ||

| Integrated Capillary Collection Kits | ||

| Dried Blood Spot Cards | ||

| By Application | Comprehensive Metabolic Panel (CMP) | |

| Liver Panel Tests | ||

| Plasma/Serum Protein Tests | ||

| Whole Blood Tests | ||

| Infectious Disease Screening | ||

| Genetic & Neonatal Screening | ||

| By End User | Diagnostic Centers | |

| Hospitals & Clinics | ||

| Home Care Settings | ||

| Research Laboratories | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the capillary blood collection devices market?

The market stands at USD 2.62 billion in 2026 and is projected to reach USD 3.54 billion by 2031 at a 6.21% CAGR.

Which application segment is expanding the fastest?

Genetic and neonatal screening is advancing at an 8.61% CAGR through 2031, driven by nationwide newborn programs and precision-medicine initiatives.

Why are dried blood spot cards gaining traction?

They cut cold-chain logistics costs by up to 94%, enable easy self-collection, and now offer hematocrit-neutral volumetric sampling that meets therapeutic drug monitoring accuracy standards.

How does regulatory compliance affect market entrants?

Class II devices require 510(k) submissions that can delay launches by up to 12 months, while annual quality-system compliance can exceed USD 1 million for smaller firms.

Which end-user segment is expected to grow the most?

Home care settings are set to expand at a 9.37% CAGR as payers incentivize remote monitoring and consumers seek convenient, needle-sparing options.

What regional market shows the strongest growth outlook?

Asia-Pacific is on course for a 7.5% CAGR due to rising chronic disease prevalence, telehealth adoption, and expanding healthcare infrastructure funding across major economies.

Page last updated on: