Blood Processing Devices And Consumables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 55.53 Billion |

| Market Size (2031) | USD 80.06 Billion |

| Growth Rate (2026 - 2031) | 7.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

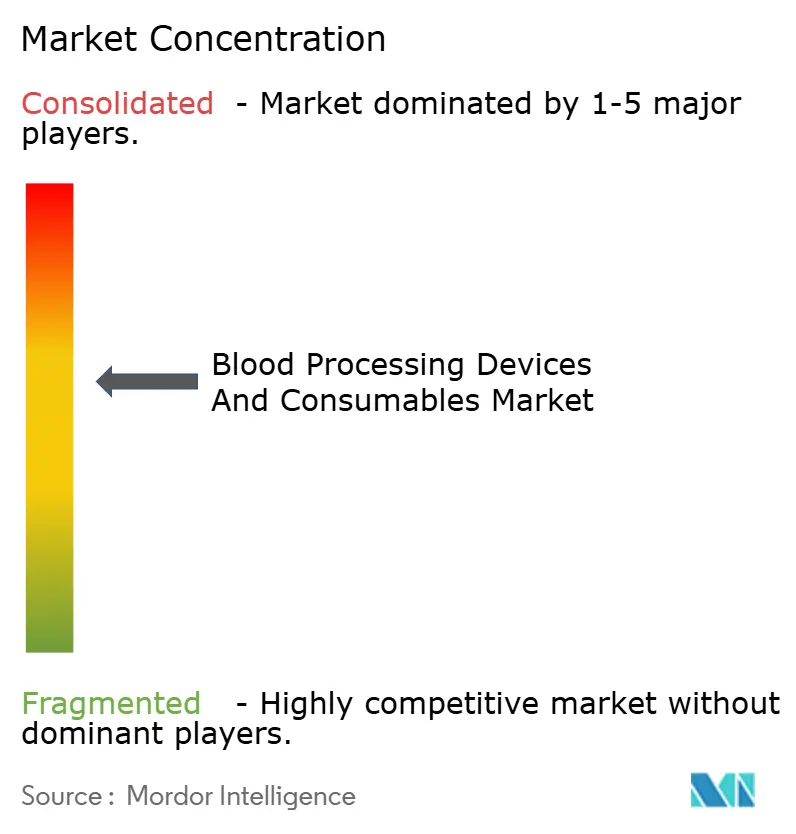

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Processing Devices And Consumables Market Analysis by Mordor Intelligence

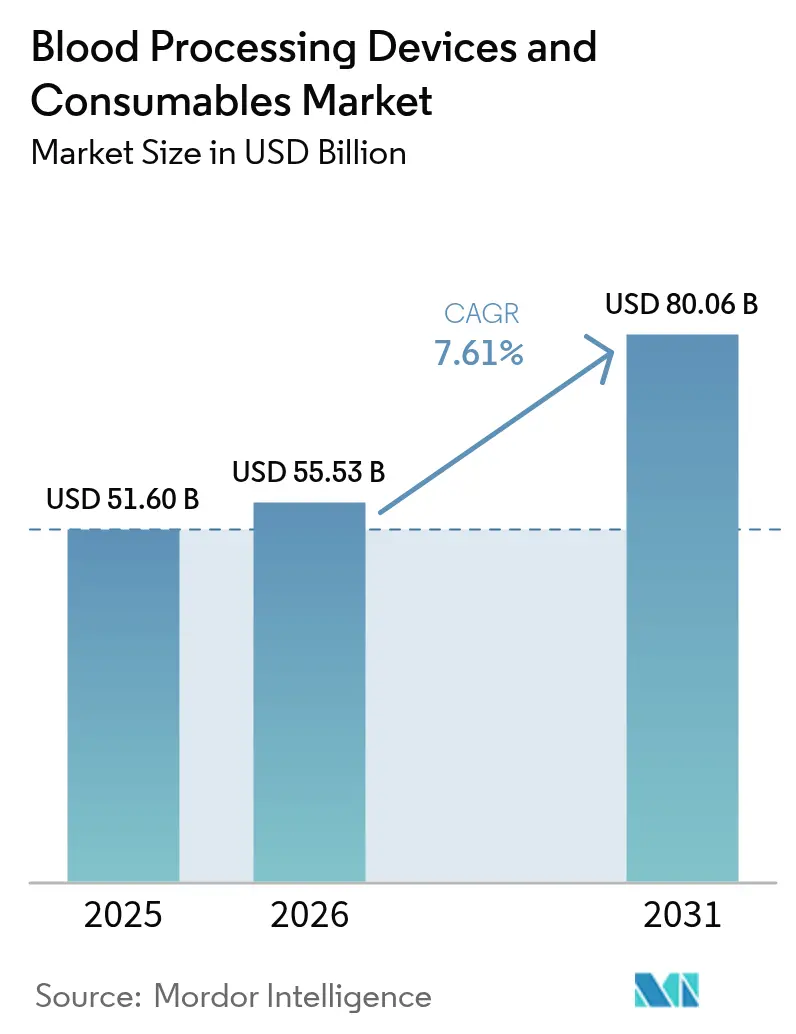

The blood processing devices and consumables market size is expected to grow from USD 51.60 billion in 2025 to USD 55.53 billion in 2026 and is forecast to reach USD 80.06 billion by 2031 at 7.61% CAGR over 2026-2031. Growing transfusion volumes, rapid uptake of automated apheresis systems, and heightened blood safety mandates are accelerating capital spending across blood centers and hospital laboratories. Hospitals are expanding mobile processing capabilities to serve remote locations, while AI-enabled cross-matching and inventory tools are beginning to optimize unit allocation and reduce wastage. Demand is reinforced by a rising geriatric base and by regenerative medicine procedures that rely on highly specialized components. Vendors are responding with modular device platforms, integrated software, and service models designed to boost throughput and lower per-unit processing costs.

Key Report Takeaways

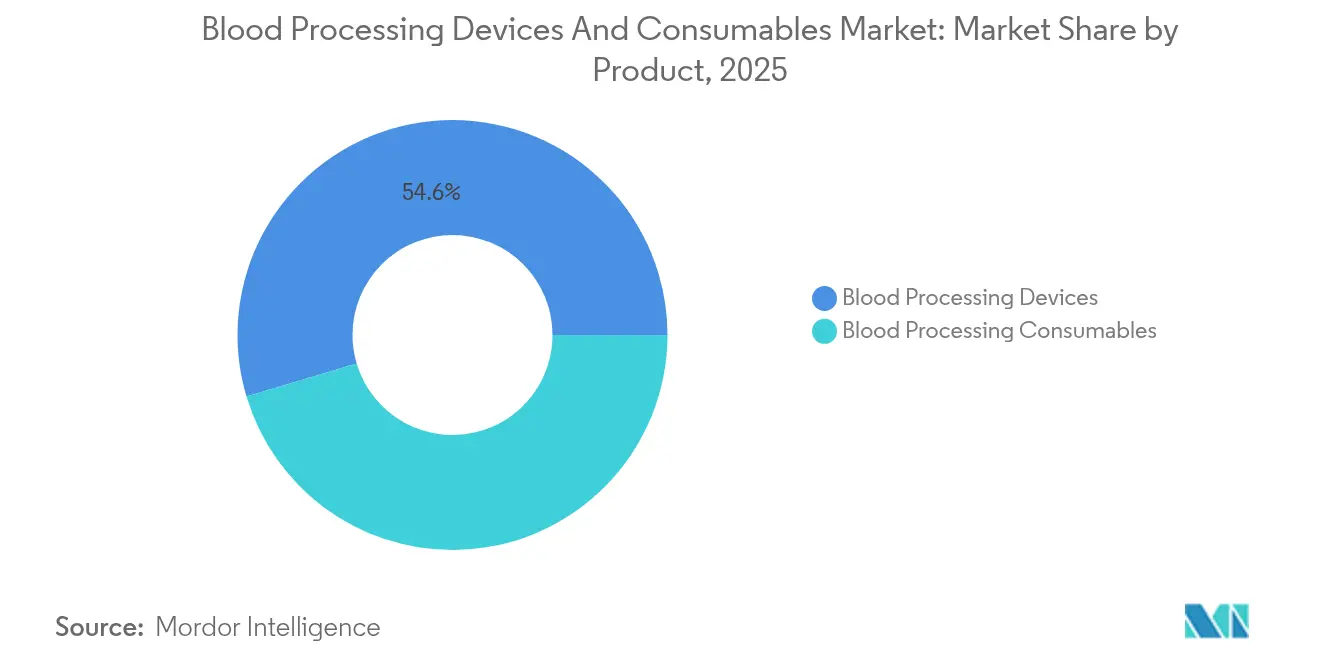

- By product, devices held 54.62% of blood processing devices and consumables market share in 2025, while consumables are expected to post the fastest 9.31% CAGR through 2031.

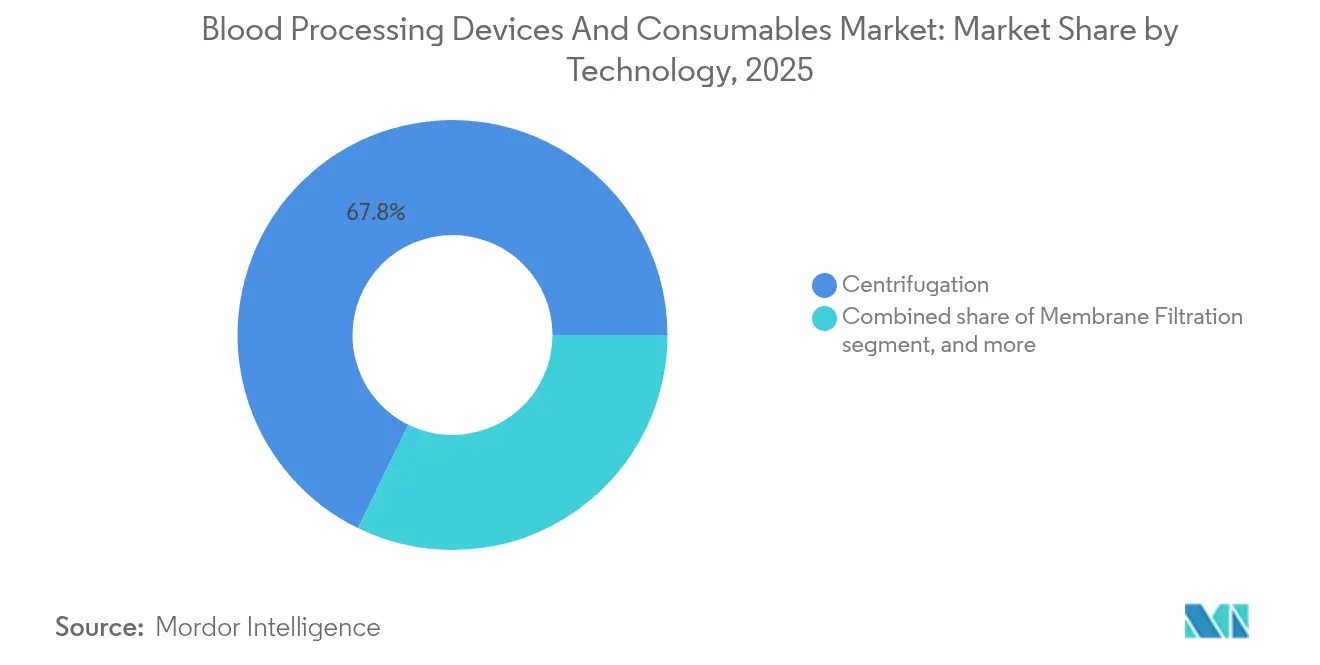

- By technology, centrifugation led with 67.75% revenue share in 2025; AI-enabled cross-matching platforms are expanding at the highest 8.70% CAGR to 2031.

- By end user, hospitals and clinics accounted for 65.60% of blood processing devices and consumables market size in 2025, whereas blood banks and transfusion centers are projected to grow at 9.96% CAGR by 2031.

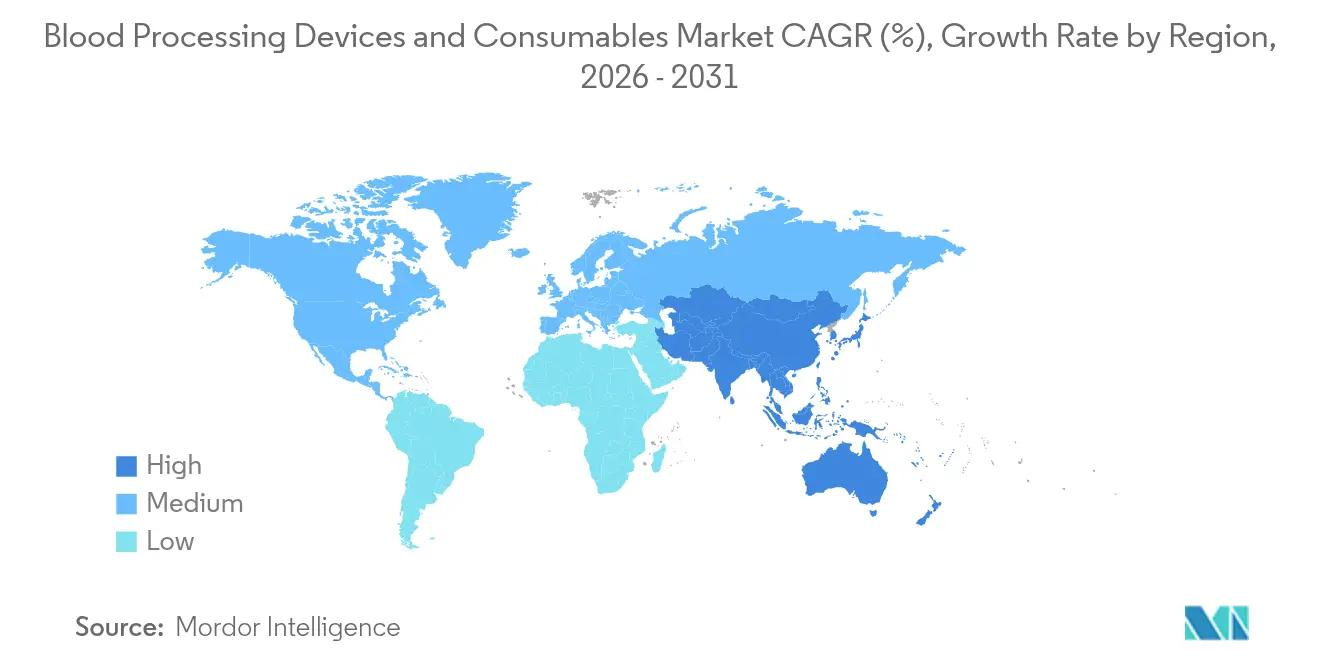

- By geography, North America dominated with 38.10% revenue share in 2025; Asia-Pacific is forecast to record the quickest 8.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Processing Devices And Consumables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Blood Transfusion Demand | +2.1% | Global, with acute needs in emerging markets | Medium term (2-4 years) |

| Growing Geriatric Population Base | +1.8% | North America & Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion Of Regenerative Medicine And Cell Therapies | +1.5% | North America & EU leading, Asia-Pacific adoption accelerating | Medium term (2-4 years) |

| Government Programs To Enhance Blood Safety Infrastructure | +1.2% | Global, priority focus in developing nations | Long term (≥ 4 years) |

| Technological Advancements In Apheresis And Automation | +0.7% | Developed markets initially, scaling to emerging regions | Short term (≤ 2 years) |

| Increasing Point-Of-Care And Mobile Blood Processing Adoption | +0.2% | Rural and remote areas globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Blood Transfusion Demand

Worldwide transfusion requirements continue to outstrip donations, with the American Red Cross citing a 25% decline in supply even as surgical and trauma cases rise. The World Health Organization confirms that voluntary unpaid donations still contribute less than half of needed units in many low-income regions, underscoring chronic shortfalls[1]U.S. Food & Drug Administration, “Human Cells, Tissues, and Cellular and Tissue-Based Products Guidance,” fda.gov. High-yield component separators and automated cold-chain logistics are therefore essential. Taiwan’s teaching hospitals demonstrate best-in-class inventory control, trimming wastage to 0.08% through real-time monitoring. University Hospitals processed 7% more samples in 2024 after automating triage workflows, activating 323 Massive Transfusion Protocols in the same year. These examples illustrate how capacity gains hinge on sophisticated devices and consumables that maximize usable components from every donation.

Growing Geriatric Population Base

United Nations projections show rapidly aging populations across developing economies, converting erstwhile donors into recipients. U.S. healthcare spending rose 7.5% to USD 4.9 trillion in 2023, mainly through Medicare outlays linked to older patients. Blood centers are piloting donor-management systems that safely extend eligibility for seniors to mitigate shrinking youth donor pools. The WHO’s patient blood-management guidelines urge adoption of resource-efficient component processing for anemia in the elderly, spurring uptake of compact cell processors that can run small volumes with minimal wastage. As geriatrics grow, facilities must scale processing while navigating stricter hemovigilance standards.

Expansion of Regenerative Medicine and Cell Therapies

The cell-therapy arena is set to reach USD 26.8 billion by 2033 at 16.9% CAGR, intensifying demand for closed-system apheresis and controlled-rate freezing. Terumo Blood and Cell Technologies created a Global Therapy Innovations unit that combines the Spectra Optia and Quantum Flex platforms, aligning with growth of autologous CAR-T manufacturing. Real-world data on cilta-cel therapy show 89% response in 236 relapsed myeloma cases, many outside pivotal trial criteria, highlighting the escalating volume of patient-specific processing cycles. Such therapies rely on ultra-clean consumables and precision devices, positioning integrated suppliers for premium growth.

Government Programs to Enhance Blood Safety

Regulators worldwide are heightening scrutiny. CMS implemented an 18% CLIA-fee increase from January 2024, while the FDA’s fiscal-year 2025 user-fee schedule adds cost layers for device makers and blood facilities[2]AABB, “CLIA Fee Increase and Outpatient Payment Updates,” aabb.org. WHO quality-system blueprints encourage full digital traceability and pathogen-reduced components, stimulating demand for bag sets with RFID tags and rapid pathogen-inactivation kits. Public-private funding programs in Africa and South-East Asia are underwriting regional mega-centers that buy automated centrifuges in bulk, favoring vendors with turnkey installation and training packages.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory and Quality Compliance Requirements | -1.4% | Global, with varying intensity by region | Long term (≥ 4 years) |

| High Capital and Maintenance Costs of Equipment | -0.9% | Emerging markets primarily; cost pressures in developed regions | Medium term (2-4 years) |

| Limited Reimbursement for Advanced Procedures | -0.6% | Developed markets and higher-income emerging economies | Medium term (2-4 years) |

| Shortage of Skilled Technicians in Low-Resource Settings | -0.4% | Sub-Saharan Africa, parts of South Asia and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Quality-Compliance Requirements

The FDA’s updated donor-eligibility draft guidance expands documentation demands, extending validation cycles and internal audit workloads[3]Federal Register, “FY 2025 Medical Device User Fee Rates,” federalregister.gov. WHO technical directives stipulate that every blood establishment must embed quality systems covering donor recruitment through transfusion, forcing smaller centers to invest in bar-coded bags, audit software, and staff certification. While necessary for safety, these rules elevate operating costs and create steep learning curves, discouraging new entrants.

High Capital and Maintenance Costs of Equipment

Laboratory operating budgets often exceed USD 1 million yearly, with service contracts alone costing USD 20,000-50,000. Medicare’s 2.9% outpatient rate increase for 2025 is below inflation, squeezing margins for transfusion services that must still cover consumable and equipment upgrades. Terumo allocated USD 250 million to new manufacturing lines, highlighting the scale of investment needed to remain competitive. Capital intensity thus favors cash-rich incumbents and slows refresh cycles for budget-constrained public hospitals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Devices Provide the Revenue Base, Consumables Propel Future Growth

Devices contributed 54.62% of blood processing devices and consumables market revenue in 2025, reflecting their indispensability in every transfusion service. FDA clearances for multi-bag automated separators and smart freezers confirm fast innovation. Hospitals prefer modular systems that integrate chilling, mixing, and barcode tracking to slash manual steps. Vendors are embedding predictive-maintenance algorithms that reduce downtime and extend asset life. Operating-lease models are emerging, shifting capex to opex and broadening access in mid-tier facilities.

Consumables, although smaller today, are the chief growth engine at 9.31% CAGR to 2031, making them critical to the long-term trajectory of the blood processing devices and consumables market. Single-use apheresis kits, pathogen-inactivation sleeves, and leukofilters are ordered with every procedure, producing recurring revenue streams. In Asia-Pacific, hospital upgrades and rural outreach programs are boosting baseline demand, while mature markets pivot to premium consumables with RFID and antimicrobial coatings. As a result, disposables producers with localized manufacturing footprints can shorten lead times and cushion currency risks.

By Technology: Centrifugation Dominates, AI Platforms Shift Testing Protocols

Centrifugation retained 67.75% of blood processing devices and consumables market share in 2025, underscoring its reliability and cost-effectiveness. Suppliers are refining rotor geometry and sensor arrays to achieve higher platelet yields per spin and reduce red-cell hemolysis. Compact tabletop centrifuges targeting satellite clinics are opening low-volume niches.

AI-enabled cross-matching platforms, expanding at an 8.70% CAGR, introduce algorithm-driven typing, automated image capture, and cloud-based analytics. Early adopters report fewer serology reruns and tighter inventory balance. Integration challenges persist-particularly data-privacy compliance and laboratory-information-system alignment-but pilot installations indicate double-digit time savings on compatibility tests. Over the forecast horizon, hybrid architectures that pair centrifugation for separation with AI for compatibility screening will dominate high-throughput labs, consolidating vendor ecosystems.

By End User: Hospitals Anchor Demand, Blood Banks Expand the Network

Hospitals and clinics accounted for 65.60% of blood processing devices and consumables market size in 2025, driven by trauma, oncology, and obstetric needs. Operating-room transfusion remains the largest volume generator, prompting hospital labs to invest in rapid-response component processors and near-patient platelet agitators. Integrated health networks are standardizing device fleets across campuses to negotiate bulk consumable pricing and streamline training.

Blood banks and transfusion centers, while capturing a smaller share today, will grow fastest at 9.96% CAGR to 2031, reflecting consolidation into regional mega-centers. Centralized facilities use high-volume separators, robotic bag sealers, and automated storage carousels that lower per-unit costs. Emerging national services in Africa and South-East Asia are adopting this model to comply with WHO mandates. Such growth indicates that the blood processing devices and consumables market will increasingly hinge on specialized centers optimized for scale and compliance.

Geography Analysis

North America commanded 38.10% of 2025 revenue, leveraging mature infrastructure, stringent but transparent regulation, and USD 4.9 trillion in healthcare spending. Large integrated delivery networks continuously refresh centrifuges, warmers, and compatibility analyzers to meet evolving AABB standards. Abbott’s USD 500 million manufacturing expansion in Illinois and Texas, scheduled to go live by end-2025, will amplify domestic supply of transfusion-diagnostic kits. FDA guidance pipelines foster predictable approval cycles that encourage vendors to pilot next-gen AI algorithms in regional reference labs.

Asia-Pacific is the fastest-growing territory at an 8.41% CAGR through 2031, fueled by hospital build-outs, medical tourism, and middle-class insurance uptake. China’s national quality re-certification program for 600 blood centers is accelerating centrifuge and apheresis upgrades. Terumo’s USD 15 million production plant in Hangzhou will assemble local versions of its Reveos system, aligning with provincial procurement preferences. In India and Thailand, public-private partnerships are co-financing regional plasma-fractionation hubs, mandating high-throughput separators and sterile-tube welders.

Europe shows steady replacement demand as hospitals tighten cost controls yet pursue pathogen-reduced components to meet new EN standards. Bulk-buying alliances in Germany and France favor suppliers offering multi-year service bundles with uptime guarantees. Eastern European modernization funds tied to EU cohesion budgets are financing first-time adoption of automated component extractors in mid-size cities, broadening the installed base.

Middle East & Africa and South America provide incremental upside though infrastructure gaps persist. Gulf states invest in cutting-edge robotics to support tertiary-care hubs, while Sub-Saharan Africa leans on donor-funded mega-centers outfitted with rugged centrifuges and solar-powered storage. Latin America’s private hospital chains are upgrading compatibility analyzers to win medical-tourism contracts. Across these regions, vendors that offer flexible financing and on-site training gain competitive traction.

Competitive Landscape

The blood processing devices and consumables market is moderately consolidated. Abbott Laboratories leads with 14.0% 2024 share, followed by Terumo Corporation at 12.0%, Grifols S.A. at 11.0%, Haemonetics Corporation at 10.0%, and F. Hoffmann-La Roche AG at 9.0%. These five control 56% of global revenue, yet niche innovators are eroding share through AI software and synthetic blood research.

Strategic investments underscore the race for scale. Grifols posted record EUR 6.592 billion revenue in 2023 and appointed a new CEO to sharpen operational efficiency amid a prospective EUR 7 billion takeover bid by Brookfield. Haemonetics divested its whole-blood product line to GVS for USD 67.8 million in January 2025 to redirect resources toward higher-margin apheresis systems. Terumo’s Reveos platform, capable of processing four units of whole blood simultaneously, lowers manual steps by 65% and is being adopted in a 10-year agreement with Sanquin in the Netherlands, illustrating how automation differentiates suppliers.

Partnerships and OEM deals extend reach. Siemens Healthineers renewed a global OEM pact with Sysmex for hemostasis instruments and reagents, leveraging 25 years of collaboration to address rising thrombotic-disease testing needs. In addition, Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s purification unit enhances its filtration portfolio, enabling bundled offerings for plasma-fractionation customers.

Emerging disruptors pursue artificial blood substitutes. Japanese university consortia report hemoglobin-based products with two-year shelf life and universal compatibility, while Israel’s RedC Biotech is scaling lab-grown red cells under pharma partnerships. Although pre-commercial, such breakthroughs could compress demand for donated units, prompting incumbents to hedge through R&D alliances.

Blood Processing Devices And Consumables Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche AG

Terumo Corporation (Terumo BCT)

Grifols S.A.

Haemonetics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Terumo Blood and Cell Technologies confirmed that Parachute Health adopted Rika Plasma Donation System, enabling 1,000 mL plasma collections in under 35 minutes with live donor-comfort analytics.

- April 2025: Abbott Laboratories posted USD 10.358 billion Q1 revenue, a 4% year-on-year rise, and announced USD 500 million U.S. manufacturing expansion due online by late 2025.

- May 2025: Becton, Dickinson and Company published data showing BD MiniDraw capillary device matches venous draw accuracy across 52 assays, easing decentralized diagnostics.

- February 2025: Thermo Fisher Scientific agreed to buy Solventum’s purification and filtration unit for USD 4.1 billion, extending its blood-purification portfolio.

- January 2025: FDA’s Center for Biologics Evaluation and Research released draft guidance on donor-eligibility criteria for human cellular products.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the blood processing devices and consumables market as all capital equipment and disposable items used to collect, separate, preserve, store, and warm whole blood or its components before transfusion or further therapeutic manipulation. Products span centrifugation-based cell processors, grouping analyzers, bank freezers, warmers, bags, sets, vials, and filters that operate within hospital transfusion services, blood banks, and diagnostic laboratories.

Scope Exclusions: Single-use diagnostic reagents that never enter the blood-processing workflow and direct-to-consumer finger-stick test kits remain outside our scope.

Segmentation Overview

- By Product

- Blood Processing Devices

- Blood Bank Freezers

- Blood Grouping Analyzers

- Blood Warmers

- Blood Cell Processors

- Other Blood Processing Devices

- Blood Processing Consumables

- Blood Bags

- Disposable Apheresis Kits

- Blood Lancets

- Vials & Collection Tubes

- Blood Administration Sets

- Other Consumables

- Blood Processing Devices

- By Technology

- Centrifugation

- Membrane Filtration

- Automated Robotic Processing

- AI-Enabled Cross-Matching Platforms

- By End User

- Hospitals and Clinics

- Diagnostic Laboratories

- Blood Banks & Transfusion Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

To bridge gaps, we interviewed transfusion medicine chiefs, biomedical engineers, and procurement managers across North America, Europe, and Asia-Pacific. Their inputs on device utilization rates, average shelf-life of consumables, and adoption barriers helped us validate secondary findings and fine-tune key coefficients.

Desk Research

We began with public domain datasets such as the WHO Global Blood Safety statistics, the United States FDA Blood Establishment Registration listings, the European Centre for Disease Prevention and Control transfusion surveillance, and the National Health Service Blood & Transplant annual report. Trade groups like AABB and the International Society of Blood Transfusion provided practice benchmarks, while 10-K filings of leading device firms offered pricing corridors. D&B Hoovers and Dow Jones Factiva fed company-level revenue clues. This menu of sources built our foundational demand picture; many other authoritative publications were also reviewed even if not named here.

Market-Sizing & Forecasting

A top-down model converts national whole-blood collection volumes into device and consumable demand pools, then applies penetration and replacement factors that we corroborate through sampled bottom-up roll-ups of supplier shipments. Variables such as average units processed per installed centrifuge, procedure growth tied to surgical volumes, capital replacement cycles, regulatory uptake of pathogen-reduction systems, and median unit pricing anchor the model. Forecasts to 2030 employ multivariate regression blended with scenario analysis to reflect shifts in donor demographics and elective-surgery recovery, with expert consensus guiding final adjustments.

Data Validation & Update Cycle

Outputs run through variance checks against external market ratios; anomalies trigger analyst reviews and, when needed, call-backs to experts. Reports refresh each year, and we reopen the model for any material events before delivery so clients always receive the latest view.

Why Mordor's Blood Processing Devices and Consumables Baseline Commands Trust

Published figures often diverge because firms adopt dissimilar product baskets, inflation bases, and refresh cadences. Our disciplined scope selection, annual re-benchmarking, and transparent variable mapping minimize that spread.

Key gap drivers include competitors rolling blood collection and storage devices into the same pool, applying static average selling prices, or using outdated 2023 donor data, whereas we align every assumption to 2025 customs, hospital-procedure, and pricing realities.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 51.60 B | Mordor Intelligence | - |

| USD 55.10 B | Global Consultancy A | Includes stand-alone blood collection and storage equipment and applies constant 2024 exchange rates |

| USD 52.03 B | Industry Research B | Relies on device maker shipment disclosures without adjusting for multi-use consumable lifecycles |

Taken together, the comparison shows that Mordor's balanced blend of procedure-linked demand, refreshed pricing, and granular scope filtering delivers a dependable baseline clients can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the blood processing devices and consumables market, and how large will it be by 2031?

The market stands at USD 55.53 billion in 2026 and is on course to hit USD 80.06 billion by 2031, reflecting a 7.61% CAGR over 2026-2031.

Which product segment is expanding the fastest?

Consumables-such as apheresis kits and blood bags-are projected to grow at a 9.31% CAGR through 2031, outpacing devices.

Which region offers the highest growth opportunity for suppliers?

Asia-Pacific delivers the quickest expansion, with an 8.41% CAGR driven by hospital build-outs, medical tourism, and quality-system upgrades.

What technology is most likely to disrupt conventional blood processing workflows?

AI-enabled cross-matching platforms, growing at 8.70% CAGR, automate compatibility testing and tighten inventory control.

Who are the market leaders, and how concentrated is the competitive landscape?

Abbott, Terumo, Grifols, Haemonetics, and Roche collectively hold 56.0% share, signaling moderate concentration and active competition.

What primary challenge could restrain near-term market growth?

Stringent regulatory compliance and rising equipment costs inflate operating budgets, especially for smaller or emerging-market facilities.

Page last updated on: