Blood Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

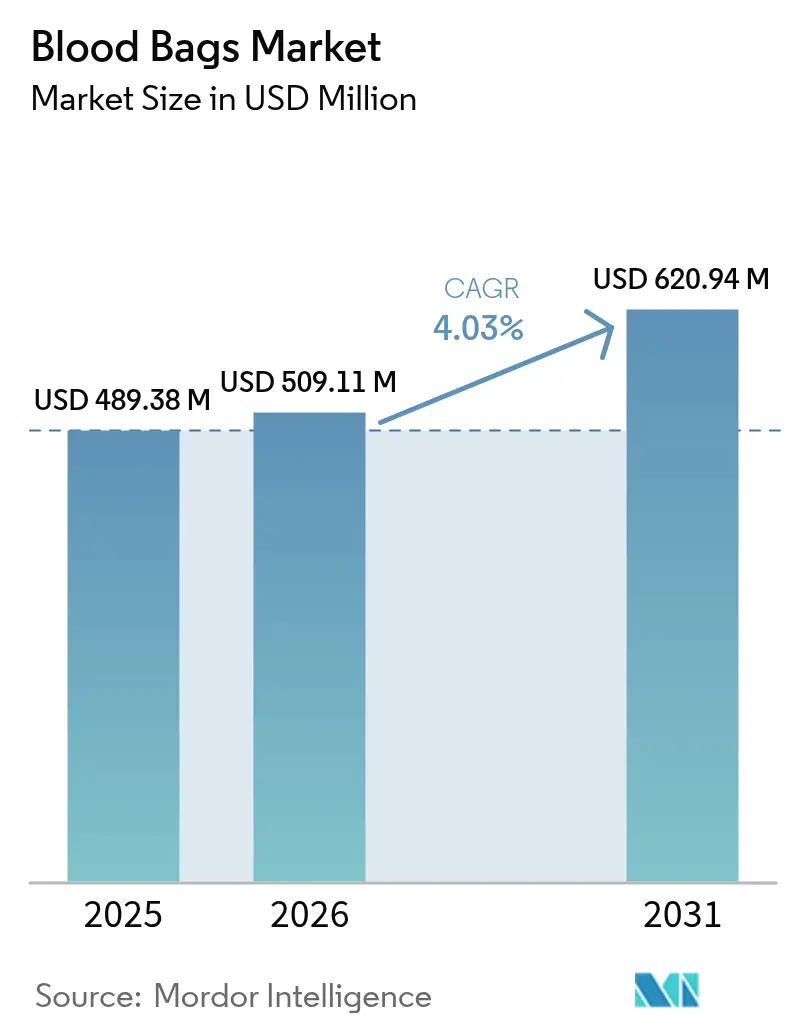

| Market Size (2026) | USD 509.11 Million |

| Market Size (2031) | USD 620.94 Million |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Bags Market Analysis by Mordor Intelligence

The Blood Bags Market size is projected to expand from USD 489.38 million in 2025 and USD 509.11 million in 2026 to USD 620.94 million by 2031, registering a CAGR of 4.03% between 2026 to 2031.

Steady expansion reflects rising surgical volumes, higher trauma incidence, and stricter blood-safety regulations that oblige health systems to modernize collection, processing, and storage infrastructure. Regulatory mandates such as the European Union’s REACH rule and California’s AB 2300 are accelerating the transition from DEHP-plasticized polyvinyl chloride (PVC) toward safer formulations, spurring material innovation and capital spending.[1]Source: AABB, “California Bans DEHP in Medical Devices, Excludes Blood Bags,” aabb.org Hospitals and blood centers are adopting pathogen-reduction platforms, automated component-separation systems, and RFID-enabled traceability, which collectively raise demand for multi-compartment bag configurations. North America leads in advanced trauma care networks, yet Asia-Pacific records the fastest growth as voluntary donation campaigns and local plasma-fractionation plants scale capacity.

Key Report Takeaways

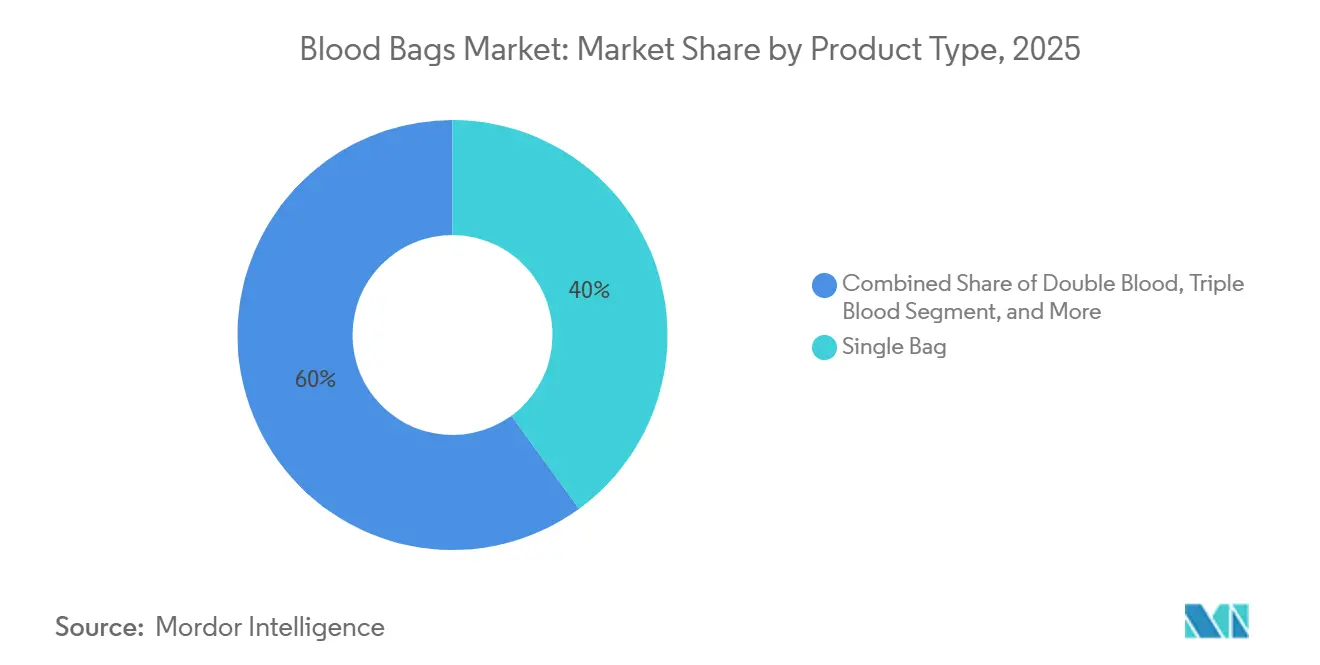

- By product type, single bags led with 39.97% revenue share in 2025; quadruple bags are projected to post the fastest 4.42% CAGR through 2031.

- By material, PVC (DEHP) accounted for 62.20% of the blood bags market share in 2025, whereas PVC (DEHP-free) is advancing at a 4.72% CAGR to 2031.

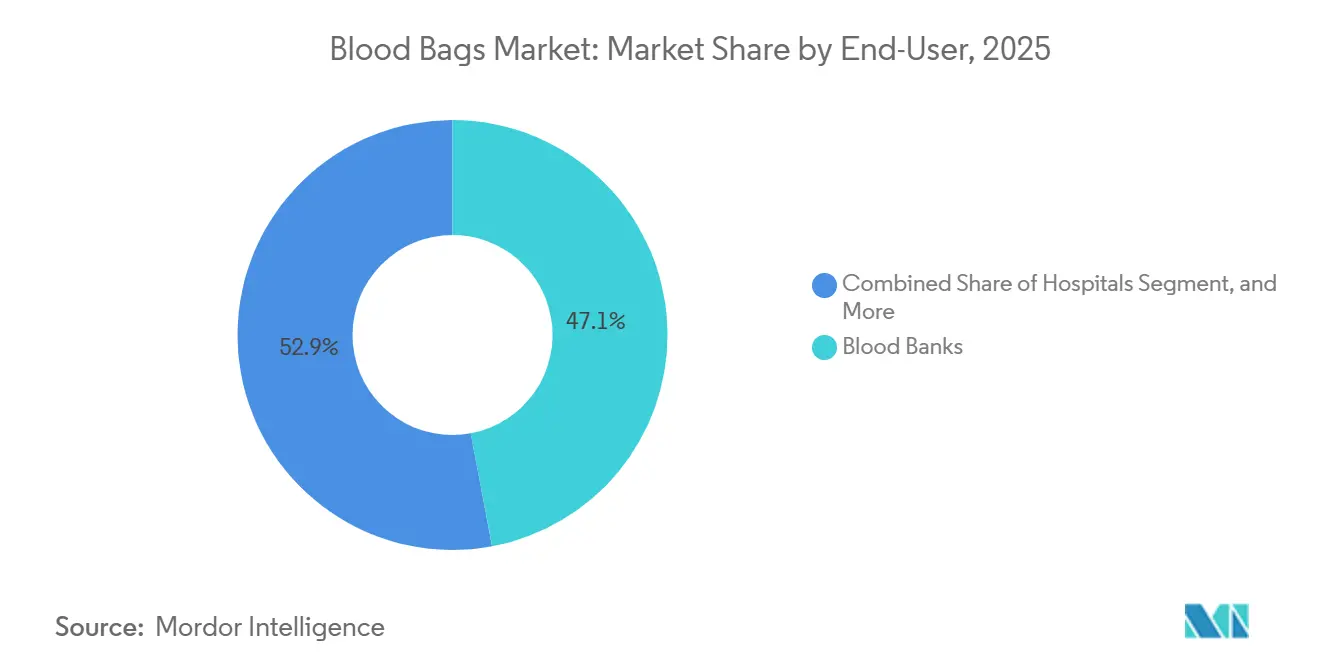

- By end user, blood banks captured 47.06% of the blood bags market in 2025, while hospitals are expected to register the highest CAGR of 4.66% between 2026 and 2031.

- By application, collection dominated the blood bags market with a 53.22% share in 2025; processing is forecast to expand at a 4.55% CAGR through 2031.

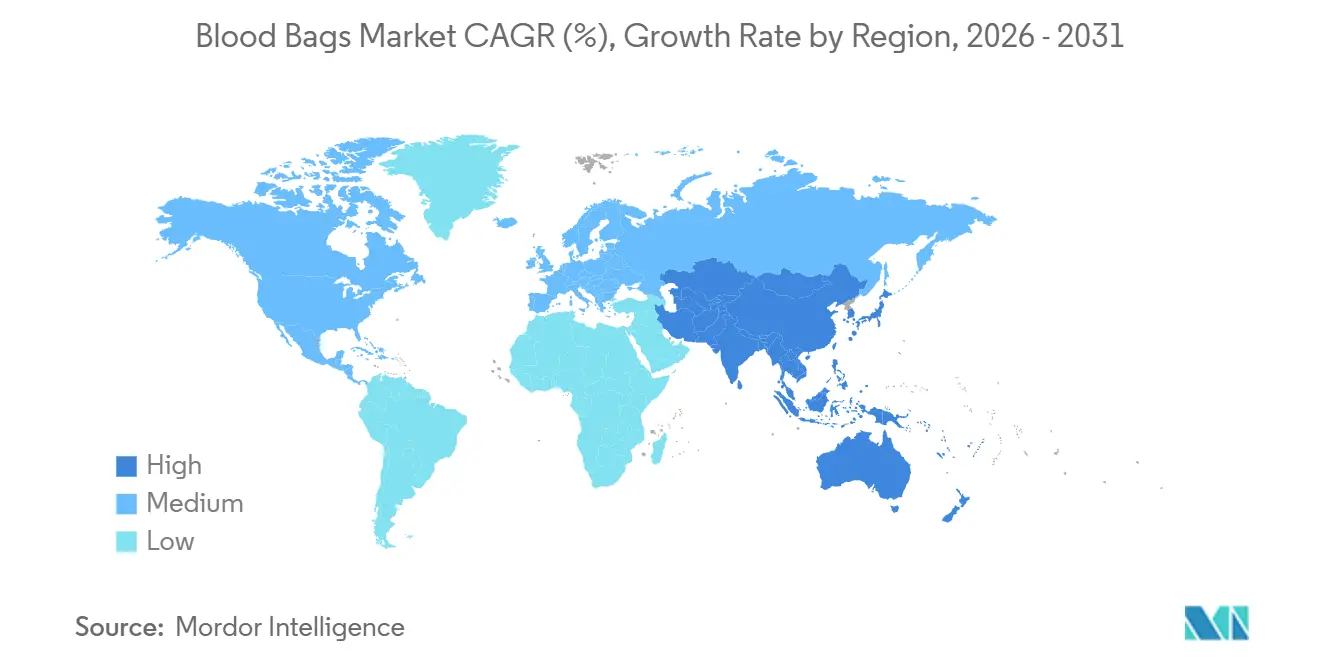

- By geography, North America held 37.88% of 2025 revenue, and Asia-Pacific is set to grow the quickest at a 4.86% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Blood Bags Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising surgical volumes & trauma incidence | +0.9% | Global, acute in APAC & MEA | Medium term (2–4 years) |

| Growth in voluntary, non-remunerated blood donations | +0.7% | Global, led by APAC, Africa, South America | Long term (≥ 4 years) |

| Regulatory mandates for pathogen-reduction adoption | +0.6% | North America, EU, Australia | Medium term (2–4 years) |

| RFID-enabled traceability cuts wastage | +0.4% | EU, North America, urban APAC hubs | Short term (≤ 2 years) |

| Emerging plasma-fractionation capacity in EMS | +0.5% | India, China, Brazil, Southeast Asia | Long term (≥ 4 years) |

| Production-linked incentives for local manufacturing | +0.3% | India, Vietnam, select African nations | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Volumes & Trauma Incidence

Level 1 trauma centers report transfusion triggers at hematocrits below 32.08 for red cells, and platelet counts under 130,000 µL, illustrating rising demand for packed components. Based on the medRxiv preprint by Turkulainen et al. published in November 2024, electronic health records from HUS Helsinki University Hospital reveal that 107,331 blood units were transfused to 19,637 patients during 2021-2022, with 61.5% driven by emergency department admissions and peak usage occurring during early evening hours.[2]Source: Esa Turkulainen et al., “Electronic Health Records Reveal Variations in the Use of Blood Units,” medrxiv.org Simulated mass-casualty drills in the United States reveal inadequate inventories of platelets and O-negative red cells, pushing hospitals to enlarge onsite storage and adopt whole-blood resuscitation that lowers 30-day mortality. These usage patterns boost procurement of single and triple bags for immediate transfusion and quadruple sets for component therapy. Manufacturers scaling production capacity address this volume surge by integrating in-line leukoreduction filters and high-flow tubing that meet updated AABB hemolysis limits.

Growth in Voluntary, Non-Remunerated Blood Donations

WHO-backed campaigns drove voluntary donations to 118 million units in 2025, up four percentage points from 2020, with the largest absolute gains in South Asia and sub-Saharan Africa. Gamified apps and employer-sponsored drives encourage first-time donors among urban millennials and Gen Z cohorts, expanding supply diversity by geography and demographics. Flexible SKU pallets that accommodate both high-throughput urban hubs and low-volume rural outreach are increasingly critical in tenders, placing a premium on suppliers with agile distribution networks. Softer deferral policies for certain donor groups incrementally expand the eligible donor pool, bolstering a robust upward trend in the blood bags market.

Regulatory Mandates for Pathogen-Reduction Adoption

In 2024, the FDA finalized guidance on platelet pathogen-reduction systems, prompting U.S. hospitals to procure compatible quadruple kits that eliminate bacterial culture testing and extend shelf life to 7 days. The revised EU Blood Directive mandates universal platelet inactivation by 2027, accelerating demand for multi-bag assemblies with built-in photochemical chambers. While consumable costs rise by USD 15-25 per unit, hospitals recover part of that expense through lower discard rates, improved inventory flexibility, and fewer transfusion reactions. Emerging economies are piloting similar programs after dengue and Zika outbreaks, laying the groundwork for longer-term adoption and expanding the global addressable base for the blood bags market.

RFID-Enabled Traceability Cuts Wastage

NHS Blood & Transplant trials logged 98% read rates in 2024, validating RFID’s ability to flag cold-chain breaches and near-expiry units in real time. Centralized procurement agencies increasingly require embedded RFID rather than aftermarket labels, rewarding manufacturers able to integrate tags without compromising sterility. Hospitals adopting RFID report 15-20% reductions in wastage, a saving that offsets incremental tag costs and supports broader digitization of transfusion workflows. As hospital information system modernization continues, RFID-ready bags are transitioning from optional to baseline requirements in new tenders, boosting penetration in the blood bags market.

Restraints Impact Analysis of Blood Bags Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| DEHP phase-out conversion costs | -0.6% | EU, North America, gradual uptake in APAC | Medium term (2–4 years) |

| Autologous transfusion & blood substitutes | -0.4% | North America, EU, Australia | Long term (≥ 4 years) |

| Contamination-driven procurement audits | -0.2% | Global, tightest in North America & EU | Short term (≤ 2 years) |

| PVC-resin supply volatility | -0.3% | Global, pronounced in APAC hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

DEHP Phase-Out Conversion Costs

EU REACH Annex XVII restrictions oblige a transition to alternative plasticizers once performance parity is demonstrated, but tooling and validation cost at least USD 2 million per line, nudging smaller firms toward exit or consolidation. The FDA confirmed adult exposures remain below toxicological limits, yet neonatal units increasingly specify DEHP-free bags, forcing hospitals to juggle dual inventories. Price premiums of 8-12% slow adoption in budget-constrained markets, softening near-term growth for DEHP-free variants within the blood bags market.

Autologous Transfusion & Blood Substitutes

Cell-salvage devices cut allogeneic demand by 22% in United States orthopedic surgeries in 2024. Experimental hemoglobin-based carriers in late-stage trials could displace up to 10% of red-cell usage in austere environments once approved. At the same time, pre-operative autologous donation complicates blood-bank logistics despite waning popularity. Substitution risk curtails volume growth in high-income regions, underlining the strategic importance of emerging-market expansion for the blood bags market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Blood Bags Market Segment Analysis

By Product Type:

Component Separation Drives ComplexitySingle blood bags delivered 39.97% of the blood bags market share in 2025 because of low cost and suitability for whole-blood transfusions in facilities without component infrastructure. Quadruple sets are rising at 4.42% annually through 2031 as hospital protocols align with WHO guidance favoring component therapy, which maximizes therapeutic yield per donation and minimizes donor-exposure risk. Double and triple variants serve mid-tier hospitals needing only red-cell and plasma separation, whereas penta bags, a niche today, are gaining traction in pediatric units and research centers that rely on multiple aliquots. FDA and EU rules require closed-system processing for contamination control, inherently advantaging multi-chamber designs. The resulting product-mix shift, coupled with higher average selling prices on multi-bag sets, underpins value growth for the blood bags market even where unit volumes plateau.

By Material:

DEHP-Free Formulations Accelerate Amid Regulatory PressurePVC with DEHP kept 62.20% of the blood bags market size in 2025, reflecting decades of clinical familiarity and low cost. DEHP-free PVC, growing at 4.72% through 2031, benefits from REACH timelines and FDA advisories on phthalate migration. PET bags eliminate plasticizers but remain niche due to cost and cold-temperature brittleness; polyolefin blends and thermoplastic elastomers seek environmental advantages yet still await broad regulatory acceptance. High validation and surveillance costs impede rapid material turnover, meaning PVC will remain dominant through 2031 even as DEHP-free variants capture incremental volume within the blood bags market.

By End-User:

Hospitals Internalize Collection to Cut CostsBlood banks represented 47.06% of demand in 2025, yet hospitals are growing faster at 4.66% per year as integrated systems build on-site suites, install automated processors, and link donor data directly to electronic health records. This internalization trims third-party fees, shortens cross-match turnaround, and aligns with patient-blood-management goals that elevate per-unit value. Military, humanitarian, and disaster-relief programs expand modestly, supporting strategic reserves. The shift forces suppliers to cater to both centralized blood services with long procurement cycles and agile hospital networks that require just-in-time deliveries, broadening complexity in the blood bags market.

By Application:

Processing Workflows Expand on Pathogen-Reduction MandatesCollection accounted for 53.22% of 2025 sales, but processing centrifugation, leukoreduction, pathogen inactivation, plasma freezing is climbing at 4.55% CAGR as regulations tighten bacterial-risk control. Investments in automated processors standardize quality and shrink labor variability; however, they bind hospitals to proprietary bag sets, reinforcing vendor lock-in. Cold-chain monitoring in transportation and storage segments benefits from IoT data loggers that ensure 2-6 °C compliance for red cells and 20-24 °C for platelets, adding a technology layer to the blood bags market.

Geography Analysis

North America and Europe Blood Bags Market

North America’s 37.88% share in 2025 reflects mature donation networks, strict FDA standards, and widespread component therapy adoption, allowing premium pricing on DEHP-free and RFID-embedded bags. Hospital consolidation squeezes unit prices, but higher-spec products cushion margins. Europe, facing REACH-driven material shifts, emphasizes sustainability and blockchain traceability, reducing PVC dependency while keeping demand stable thanks to aging demographics and oncology caseloads.

APAC, MEA and South America Blood Bags Market

Asia-Pacific leads growth at 4.86% CAGR through 2031 on India’s PLI incentives, China’s plasma goals, and Southeast Asia’s voluntary campaigns. Japan and South Korea offset workforce shortages with automation, while Australia harmonizes with FDA and EMA protocols, attracting device trials. The Middle East and Africa display a dual track: GCC states import advanced centers, whereas sub-Saharan nations rely on donor-funded programs addressing cold-chain gaps. South America centers on Brazil’s fractionation ramp-up and Argentina’s donor expansion, though macro volatility complicates procurement. Divergent approval and enforcement timelines let multinationals price-tier products, serving premium and value segments simultaneously in the blood bags market.

Competitive Landscape

The blood bags market is moderately consolidated, further consolidated after GVS acquired Haemonetics’ whole-blood business in December 2024, broadening GVS’s vertically integrated filtration-to-bag portfolio. Terumo and Fresenius Kabi differentiate via technology leadership in pathogen reduction and DEHP-free materials, respectively, while Macopharma and Grifols leverage regional distribution depth. RFID solution providers partner with bag manufacturers to embed passive tags at molding, creating end-to-end traceability ecosystems attractive to large hospital chains.

New entrants focus on autologous transfusion and point-of-care hemostasis systems, yet high 510(k) compliance costs and sterilization-validation hurdles protect incumbents. Patent filings for rapid collection-and-infusion containers indicate future competition from combined device-and-bag kits aimed at emergency medicine. Global suppliers invest in regional molding sites to reduce freight on high-cubic-volume products and to qualify for local-content tenders in Southeast Asia and Latin America.

Blood Bags Industry Leaders

Terumo Corporation

Maco Pharma International GmbH

Fresenius SE & Co. KGaA

Haemonetics Corporation

Kawasumi Laboratories Inc.

- *Disclaimer: Major Players sorted in no particular order

Blood Bags Market Companies Covered in this Report

- AdvaCare

- B. Braun

- Demotek Ltd.

- Fresenius

- Grifols

- Haemonetics

- HLL Lifecare

- JMS Co. Ltd.

- Kawasumi Laboratories

- Maco Pharma SA

- Mitra Industries Pvt. Ltd.

- Neomedic International

- Nigale Biomedical Co. Ltd.

- Nipro

- Poly Medicure Ltd.

- Shandong Weigao Group Medical Polymer Co. Ltd.

- Shandong Zhongbaokang Medical Devices Co. Ltd.

- Span Healthcare Private Ltd.

- Terumo

- Wego Blood Transfusion Products Co. Ltd.

Recent Industry Developments in Blood Bags Market

- January 2026: A United States Midwest health system began hospital-wide use of RFID-embedded blood bags supplied by Terumo, reporting a 19% reduction in expiries within six months.

- July 2025: PURIBLOOD Medical launched Taiwan’s first domestic blood-bag plant in Shulin with 8 million-bag capacity, aiming for self-sufficiency in leukocyte-reduction kits.

- March 2025: India’s National Blood Transfusion Council funded six new component-extraction laboratories equipped with Fresenius apheresis lines, each requiring proprietary quadruple-bag kits.

Global Blood Bags Market Report Scope

As per the scope of the report, blood bags are used for the reliable collection, separation, storage, and transport of blood and its components, such as RBCs, WBCs, and platelets. Additionally, they prevent blood from coagulating and contaminating.

The blood bags market is segmented by product, type, end-user, and geography. By product, the market is segmented into single, double, and triple blood bags, and other products. By type, the market is segmented into collection bags and transfer bags. By end user, the market is segmented into hospitals and clinics, blood banks, and other end users. By geography, the market is segmented into North America, Europe, Asia Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

Segmentation Overview

| Single Blood Bags |

| Double Blood Bags |

| Triple Blood Bags |

| Quadruple Blood Bags |

| Penta Blood Bags |

| PVC (DEHP) |

| PVC (DEHP-Free) |

| PET |

| Other Polymers |

| Blood Banks |

| Hospitals |

| Others |

| Collection |

| Transportation / Storage |

| Processing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Single Blood Bags | |

| Double Blood Bags | ||

| Triple Blood Bags | ||

| Quadruple Blood Bags | ||

| Penta Blood Bags | ||

| By Material | PVC (DEHP) | |

| PVC (DEHP-Free) | ||

| PET | ||

| Other Polymers | ||

| By End-User | Blood Banks | |

| Hospitals | ||

| Others | ||

| By Application | Collection | |

| Transportation / Storage | ||

| Processing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the blood bags market?

The blood bags market size is USD 509.11 million in 2026.

How fast will demand grow over the next five years?

Revenue is projected to rise at a 4.03% CAGR, reaching USD 620.94 million by 2031.

Which product configuration is gaining traction quickest?

Quadruple bags show the fastest 4.42% CAGR because they support advanced component separation.

Why are hospitals emerging as the fastest-growing end users?

Hospitals invest in on-site automation that lowers external procurement dependence and speeds emergency response.

How do regulations affect material choices for blood-bag production?

EU REACH and Californias AB 2300 drive a shift from DEHP-plasticized PVC toward DEHP-free polymers, spurring product redesign and validation.

Which region offers the highest growth potential?

Asia-Pacific leads with a 4.86% CAGR thanks to expanding surgical volumes and improving voluntary donation systems.

Page last updated on: