Patient Blood Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.67 Billion |

| Market Size (2031) | USD 24.60 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient Blood Management Market Analysis by Mordor Intelligence

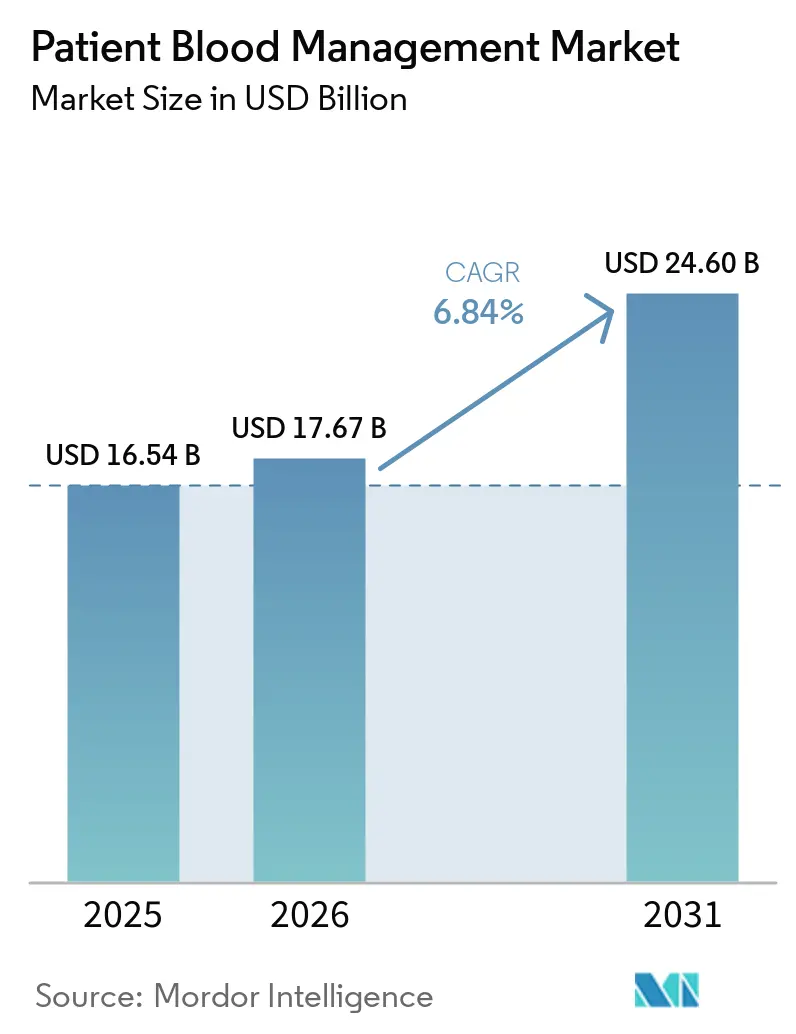

The Patient Blood Management Market size is projected to be USD 16.54 billion in 2025, USD 17.67 billion in 2026, and reach USD 24.60 billion by 2031, growing at a CAGR of 6.84% from 2026 to 2031.

The patient blood management market is growing due to increasing complex surgeries, the adoption of value-based reimbursement, and transfusion stewardship programs across developed and emerging health systems. Hospitals now view blood management as a cost and margin driver, with well-implemented programs delivering up to a 7:1 return on investment through reduced complications, shorter hospital stays, and lower episode costs. Procurement decisions are increasingly tied to measurable operational outcomes, particularly in systems tracking transfusion appropriateness and post-surgical efficiency. North America leads the market, driven by established stewardship programs, accreditation standards, and reimbursement frameworks. WHO guidance is also encouraging adoption in resource-constrained regions. However, adoption remains inconsistent. A January 2025 AABB survey found that only 46% of global institutions had formal programs, and just 42.6% of North American facilities assessed elective surgery patients for preoperative anemia.[1]Society for the Advancement of Patient Blood Management, “SABM Executive Guide, 3rd Edition,” SABM, sabm.org

Key Report Takeaways

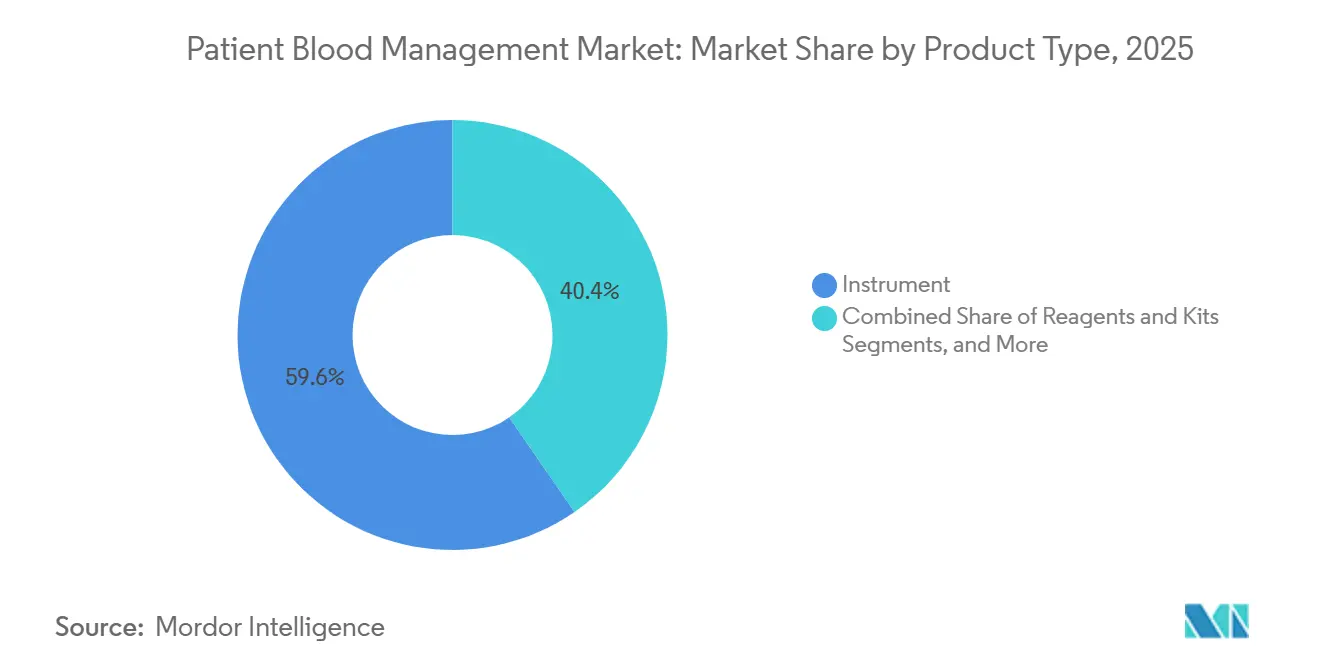

- By product type, instruments led with 59.6% revenue share in 2025, while reagent and kits are forecasted to expand at an 8.76% CAGR through 2031.

- By end user, blood banks held 56.77% of the patient blood management market share in 2025 and are projected to record the fastest CAGR at 8.45% through 2031.

- By geography, North America captured 39.4% of the patient blood management market share in 2025, while Asia-Pacific is projected to advance at a 7.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Patient Blood Management Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising elective surgical volumes and blood conservation priorities | +1.8% | Global, with highest intensity in North America, Germany, and urban Asia-Pacific centers | Short term (≤ 2 years) |

| Preoperative anemia screening and treatment expands PBM adoption | +1.5% | North America and EU, early-stage uptake in India and Southeast Asia | Medium term (2-4 years) |

| Value-based care and transfusion stewardship pressure hospitals to standardize | +1.2% | North America, spill-over to EU and Australia | Medium term (2-4 years) |

| Expansion of point-of-care testing for rapid blood management decisions | +0.9% | Global, strongest in surgical hubs across China, the United States, and Germany | Short term (≤ 2 years) |

| Ai-enabled transfusion decision support and analytics improve compliance | +0.7% | North America and APAC core, spill-over to MEA | Medium term (2-4 years) |

| Reimbursement and quality reporting incentives favor lower transfusion use | +0.6% | National in the United States and the United Kingdom, early gains in Germany and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Elective Surgical Volumes and Blood Conservation Priorities

Elective surgeries have surpassed pre-pandemic levels in many high-income healthcare systems, boosting demand in the patient blood management market. A 2025 study revealed that each unit of red blood cells used in elective non-cardiac surgeries added an average direct hospital cost of USD 491, representing 5.2% of the median total episode cost.[2]AABB, “AABB Survey Explores International PBM Practices,” AABB News, aabb.org Hospitals are increasingly leveraging blood management teams as cost-control units, influencing capital approvals for monitoring and salvage systems. The 2024 EACTS and EACTAIC guidelines elevated point-of-care viscoelastic testing algorithms to essential tools in cardiac centers, driving demand for thromboelastography and ROTEM platforms and enhancing instrument utilization and consumable demand.[3]V. Rao et al., “The Transfusion of a Single Unit of Red Blood Cells Significantly Increases Total Hospital Costs in Adult, Non-cardiac Surgical Patients,” Scientific Reports, nature.com

Preoperative Anemia Screening and Treatment Expands PBM Adoption

Preoperative anemia, affecting 25% to 35% of surgical patients, remains underdiagnosed and untreated, creating growth potential for the patient blood management market. Untreated anemia increases perioperative risks and reliance on transfusions. A 2025 study of 1,294 colorectal cancer patients showed intravenous iron protocols reduced postoperative transfusion rates to 10.7%, with compliance improving over time. Hospitals are shifting demand upstream to outpatient screening kits, iron therapy, and related accessories, boosting reagent and kit demand. AABB certification frameworks are helping integrate anemia screening into institutional workflows.

Value-Based Care and Transfusion Stewardship Pressure Hospitals to Standardize

Reimbursement systems rewarding fewer complications and shorter hospital stays are shaping the patient blood management market. The CMS Hospital Value-Based Purchasing Program redistributes 2% of base operating DRG payments based on quality performance, incentivizing practices that reduce transfusion-related complications and hospital stays.[4]Centers for Medicare and Medicaid Services, “FY 2026 Hospital Inpatient Prospective Payment System and Long-Term Care Hospital Prospective Payment System Proposed Rule Fact Sheet,” CMS, cms.gov Hospitals are investing in analytics and decision support tools to prepare for reporting periods. SABM research linked patient blood management programs to ROI as high as 7:1, driven by reduced transfusion use, shorter stays, and lower costs per case. As these models expand beyond the United States, hospitals increasingly view transfusion stewardship platforms as essential infrastructure.

Expansion of Point-of-Care Testing for Rapid Blood Management Decisions

Point-of-care viscoelastic testing, including thromboelastography and rotational thromboelastometry, is becoming standard in cardiac, trauma, and orthopedic surgeries, expanding the patient blood management market. A 2026 review highlighted that viscoelastic test-guided hemostatic therapy reduces transfusion exposure, offsetting implementation costs. These tools are now used beyond operating rooms in pre-admission units and general wards, supporting restrictive transfusion practices. A 2025 AABB survey found 80.2% of respondents promoted single-unit transfusion strategies, increasing demand for bedside hemoglobin and coagulation confirmation tools. This broader application enhances recurring revenue per instrument as testing extends beyond high-acuity surgery suites.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront cost of PBM devices, software, and training | -1.3% | Global, most severe in South Asia, Southeast Asia, Sub-Saharan Africa, and smaller community hospitals | Medium term (2-4 years) |

| Workflow resistance among clinicians and transfusion committees | -1.0% | Global, higher in markets with weak institutional PBM governance | Short term (≤ 2 years) |

| Uneven clinical evidence adoption across specialty and resource-constrained settings | -0.8% | APAC emerging economies, MEA, and parts of South America | Long term (≥ 4 years) |

| Fragmented procurement and lack of interoperability across hospital IT systems | -0.7% | Global, acute in multi-site health systems in the United States and the United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of PBM Devices, Software, and Training

Capital expenditures remain a key barrier to expanding patient blood management (PBM), particularly for district and smaller community hospitals with limited budgets. In Germany, only 70 out of 2,000 hospitals participated in the national PBM network, reflecting financial and administrative challenges. A 2024 Oxford University study found that just 14.2% of NHS England hospitals implemented advanced clinical decision support for transfusion management, with financial constraints and limited senior engagement as major obstacles. Multi-year contracts bundled with instrument placements often obscure long-term costs, leading to underestimated consumable expenses and delayed rollouts. WHO guidance from 2025 suggests cost-effective scale-up strategies, but adoption timelines remain lengthy for many facilities.

Workflow Resistance Among Clinicians and Transfusion Committees

Workflow challenges continue to impede PBM adoption, even in hospitals that invest in software and decision support. A 2025 study in Turkey found only 30.3% physician compliance with a new clinical decision support system, citing time pressures and heavy workloads as key barriers. Experienced physicians showed higher engagement than junior clinicians, indicating that training alone does not close the implementation gap. Underutilization reduces software value and consumable demand, while large academic centers face deployment delays of 12 to 24 months due to complex stakeholder involvement. Accreditation pathways like AABB certification are aligning expectations, but adoption rates vary widely based on hospital culture and governance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Instrument Dominance Masks Accelerating Reagent Pull-Through

In 2025, instruments accounted for 59.6% of the patient blood management market, driven by a decade of investments in automated blood analyzers, cell salvage systems, and viscoelastic testing platforms. Increased utilization of these systems is significantly enhancing reagent demand. Reagents and kits are projected to grow at an 8.76% CAGR through 2031, supported by rising anemia screenings, donor panels, and coagulation tests. Roche's 2026 launch of the cobas MPX-E assay highlights the market's shift toward workflow consolidation and higher reagent use per sample.

Software remains the smallest revenue segment in the patient blood management market, while accessories benefit from increased blood handling, separation, and apheresis activities in blood banks and hospitals. Accessories like blood bags, syringes, and vials see steady demand, particularly in Asia-Pacific and Latin America. Despite its smaller revenue base, software plays a strategic role in influencing instrument usage and adherence to transfusion protocols. Hospitals are adopting software for oversight, auditability, and aligning policies with daily transfusion practices.

By End User: Blood Banks Anchor Revenue While Hospitals Drive Protocol Complexity

Blood banks held a 56.77% share of the patient blood management market in 2025 and are expected to grow at an 8.45% CAGR through 2031. This growth is driven by simultaneous upgrades of aging systems and expanding donor screening requirements. WHO guidance in 2025 emphasized patient blood management's role in improving blood health and system control. Terumo Blood and Cell Technologies' launch of the Reveos Automated Blood Processing System in 2024 demonstrates the ongoing automation opportunities in blood center workflows.

Hospitals and clinics are the second-largest end users in the patient blood management market, with demand linked to expanding surgical services and PBM protocol integration. Diagnostic centers and labs follow, as anemia screenings and related tests shift to outpatient settings. The 'others' category is growing due to rising outpatient surgeries and broader adoption of blood management protocols. In the United States, the CMS Value-Based Purchasing framework incentivizes quality outcomes, reducing transfusion complications and hospital stays.

Geography Analysis

In 2025, North America accounted for 39.4% of the patient blood management market, driven by advanced healthcare infrastructure, high surgical volumes, and established stewardship governance. The United States leads regional demand due to a reimbursement framework linking hospital performance to transfusion safety and efficiency outcomes. PBM program adoption in North America reached 50.2% in 2025, up from 37.8% in 2013, with 80.2% of institutions promoting single-unit transfusion strategies. Canada supports market stability by aligning with U.S. clinical practices, while Mexico shows growing demand as PBM adoption expands. The region benefits from EHR-integrated decision support, increasing vendor retention in hospital workflows.

Europe remains a key player in the patient blood management market, with Germany, the United Kingdom, France, Italy, and Spain as major demand centers. Germany highlights significant potential, with only 70 of its 2,000 hospitals part of the national PBM network, leaving room for expansion. The 2024 cardiac surgery guidelines are formalizing viscoelastic testing across European cardiac centers, supporting structured replacement cycles for TEG and ROTEM platforms. Reimbursement structures vary, but markets like Germany show clear alignment between PBM outcomes, reduced complications, and improved hospital performance.

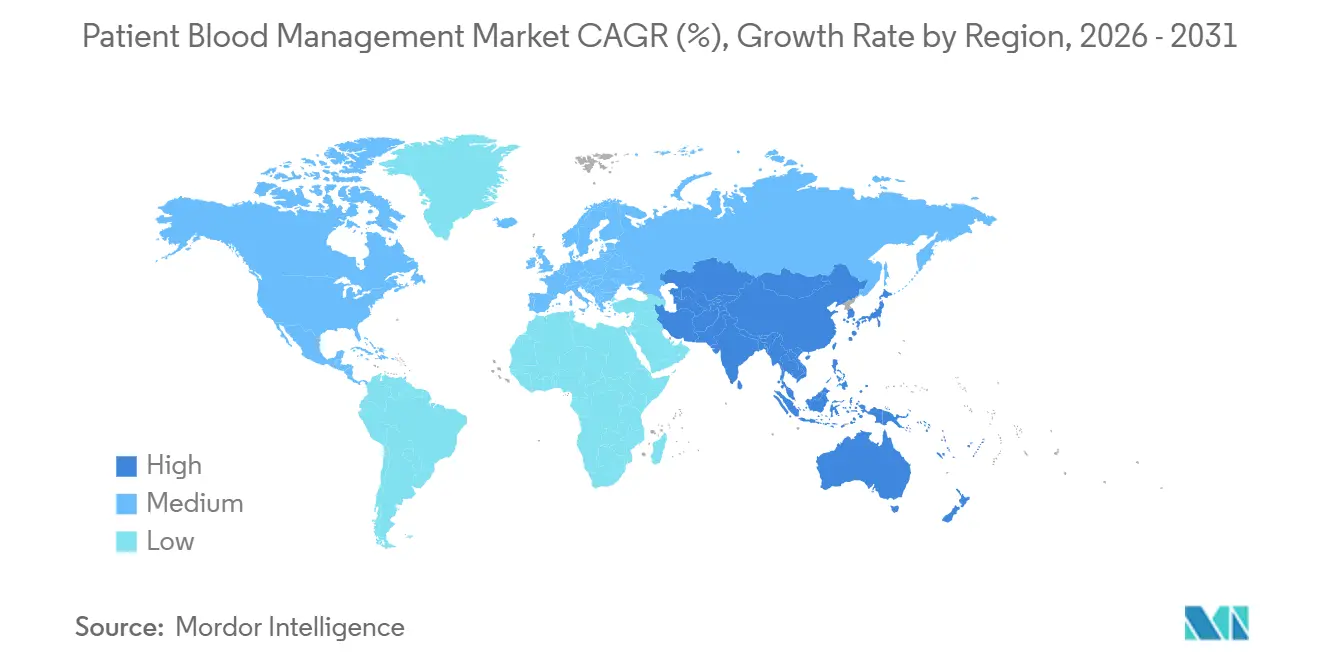

Asia-Pacific is projected to achieve the fastest growth in the patient blood management market, with a 7.23% CAGR through 2031. China drives this growth with revised regulations mandating patient-centered blood management protocols, preoperative anemia management, and autologous transfusion promotion. Its National Blood Management Information System is enhancing hospital demand for blood bank information systems and related software. India, Japan, Australia, and South Korea are scaling adoption due to aging populations and rising surgical volumes, while the GCC and parts of South America are gradually advancing blood bank automation.

Competitive Landscape

The patient blood management market is moderately consolidated in instruments and reagents, with Haemonetics Corporation, Roche Holding AG, Siemens Healthineers AG, Sysmex Corporation, and Grifols S.A. holding strong positions across core workflows. Vendors are increasingly focusing on integrated platforms combining hardware, consumables, and software, as recurring reagent revenue and integration efforts make account retention more valuable than one-time equipment sales. Roche’s March 2026 launch of the cobas MPX-E assay, which combines four donor screening targets into one workflow, enhances efficiency on automated cobas x800 systems. Additionally, Roche strengthened its position in modular laboratory automation with the United States FDA 510(k) clearance for the cobas c 703 and cobas ISE neo analytical units in March 2026.

Competition in the market is expanding beyond analyzer performance to include automation and decision support. Sysmex America’s May 2026 launch of the XR-Series hematology solution highlights the ongoing replacement cycle in high-volume laboratory platforms, emphasizing throughput and analytics. Terumo’s October 2024 United States launch of the Reveos Automated Blood Processing System demonstrated the potential of automation in blood centers, particularly where semi-manual processing limits scalability. University Hospitals’ April 2026 deployment of HemaLogiX within Epic reflects the growing demand for real-time order review and compliance support alongside physical instruments.

Opportunities remain strongest in AI-enabled decision support and modernizing blood bank information systems, as the market lacks a dominant standard. While this creates room for new software-focused entrants, established players retain an advantage due to their strong integration, clinical validation, and service continuity. Haemonetics’ January 2026 acquisition of Vivasure Medical for EUR 185 million (approximately USD 202 million) highlights how major companies are diversifying portfolios while maintaining financial strength in core procedural offerings. Overall, the market is expected to prioritize bundled platforms, clinical validation, and workflow compatibility over price-driven competition.

Patient Blood Management Industry Leaders

bioMérieux SA

Terumo Corporation

Haemonetics Corporation

B. Braun SE

Sysmex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Sysmex America introduced the XR-Series hematology solution, an upgraded version of its XN-Series platform, designed for high-volume labs with enhanced automation and analytics to strengthen its position in hematology diagnostics.

- April 2026: University Hospitals in Cleveland implemented HemaLogiX's real-time blood ordering alerts within the Epic EHR system to optimize blood component orders using patient-specific data and advisory alerts.

- March 2026: Roche launched the cobas MPX-E assay in CE-marked countries, offering a 4-in-1 nucleic acid test for HIV 1/2, HCV, HBV, and HEV, targeting the CHF 800 million NAT blood screening market.

- March 2026: Roche received U.S. FDA 510(k) clearance for cobas c 703 and cobas ISE neo analytical units, expanding its cobas pro integrated solutions platform to address automation and staffing challenges in hospital labs.

- February 2026: Haemonetics secured FDA 510(k) clearance for the NexSys PCS Plasma Collection System with Persona PLUS technology, delivering improved plasma volume per donation and cost efficiencies for plasma centers.

Global Patient Blood Management Market Report Scope

As per the scope of the report, Patient Blood Management (PBM) is an evidence-based, multidisciplinary approach that optimizes the care of patients by managing and preserving their own blood, reducing the need for donor blood transfusions. It is increasingly recognized globally as a standard of care that improves patient outcomes and reduces complications. The Patient Blood Management Market refers to the global healthcare industry sector encompassing the medical devices, diagnostics, and software used to execute these blood-conservation strategies.

The patient blood management market is segmented by product type, end-user, and geography. By product type, the market includes instruments, accessories, reagents and kits, and software solutions. By end-user, the market is segmented into hospitals & clinics, blood banks, diagnostic centers & laboratories, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Instrument |

| Accessories |

| Reagent and Kits |

| Softwares |

| Hospitals & Clinics |

| Blood Banks |

| Diagnostic Centers & Laboratories |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Instrument | |

| Accessories | ||

| Reagent and Kits | ||

| Softwares | ||

| By End User | Hospitals & Clinics | |

| Blood Banks | ||

| Diagnostic Centers & Laboratories | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the patient blood management market?

The patient blood management market is valued at USD 17.67 billion in 2026 and is forecast to reach USD 24.60 billion by 2031 at a 6.84% CAGR.

Which region leads patient blood management adoption?

North America led with 39.4% share in 2025 because reimbursement alignment, stewardship programs, and digital decision support are more established there.

Which geography is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing region with a 7.23% CAGR through 2031, supported by regulatory action in China and broader infrastructure expansion across major healthcare systems.

Which product category is growing the fastest?

Reagent and kits are projected to grow at an 8.76% CAGR through 2031 as testing intensity rises across anemia screening, donor screening, and coagulation monitoring workflows.

Which end user contributes the most revenue?

Blood banks accounted for 56.77% of revenue in 2025 and are also expected to post the highest CAGR, at 8.45%, because of automation upgrades and stronger screening requirements.

What is holding back wider adoption of PBM programs?

Upfront system cost, clinician workflow resistance, uneven protocol compliance, and integration issues across hospital IT environments remain the main barriers to faster rollout.

Page last updated on: