Blood Collection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

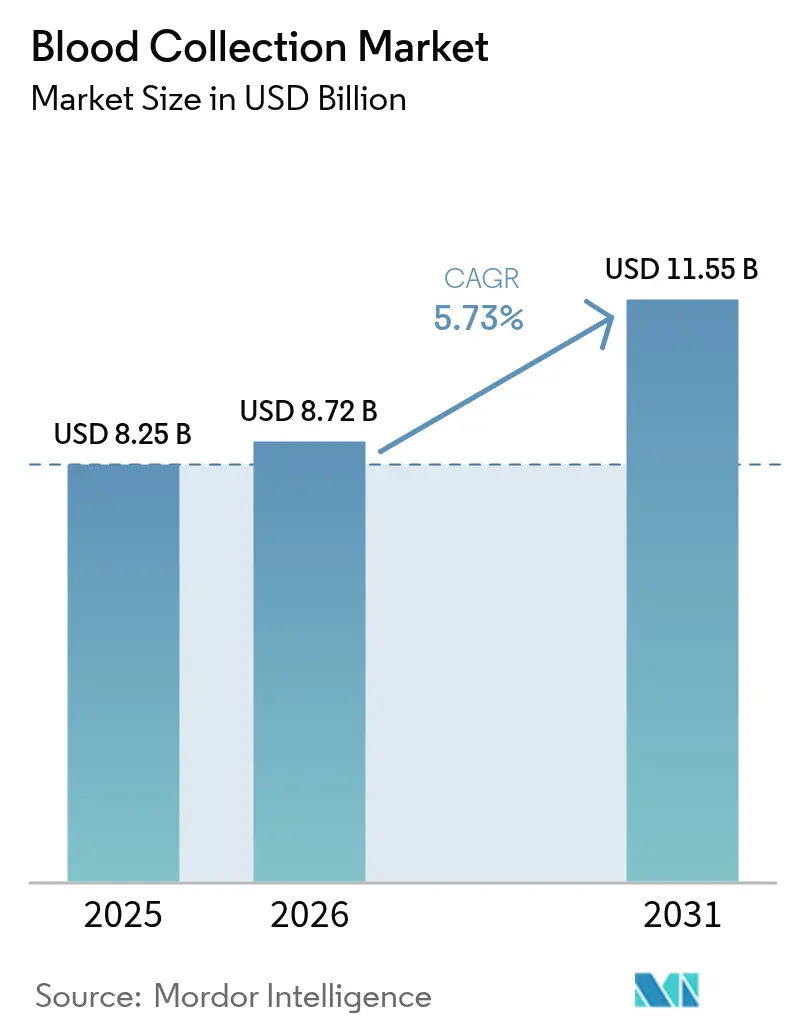

| Market Size (2026) | USD 8.72 Billion |

| Market Size (2031) | USD 11.55 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Collection Market Analysis by Mordor Intelligence

The blood collection market size was valued at USD 8.25 billion in 2025 and estimated to grow from USD 8.72 billion in 2026 to reach USD 11.55 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031). Growth is anchored in the mounting prevalence of chronic diseases, the surge in surgical procedures, and the widening of diagnostic capacity. Regulatory pressure to reduce needlestick injuries is accelerating the shift to safety-engineered products, while labor shortages are driving laboratories toward automation that ensures sampling precision. Mature economies are investing in robotic phlebotomy and needle-free platforms, whereas emerging regions focus on scaling basic collection infrastructure. Competitive intensity is heightening as incumbents defend their share through product refreshes and alliances with technology start-ups.

Key Report Takeaways

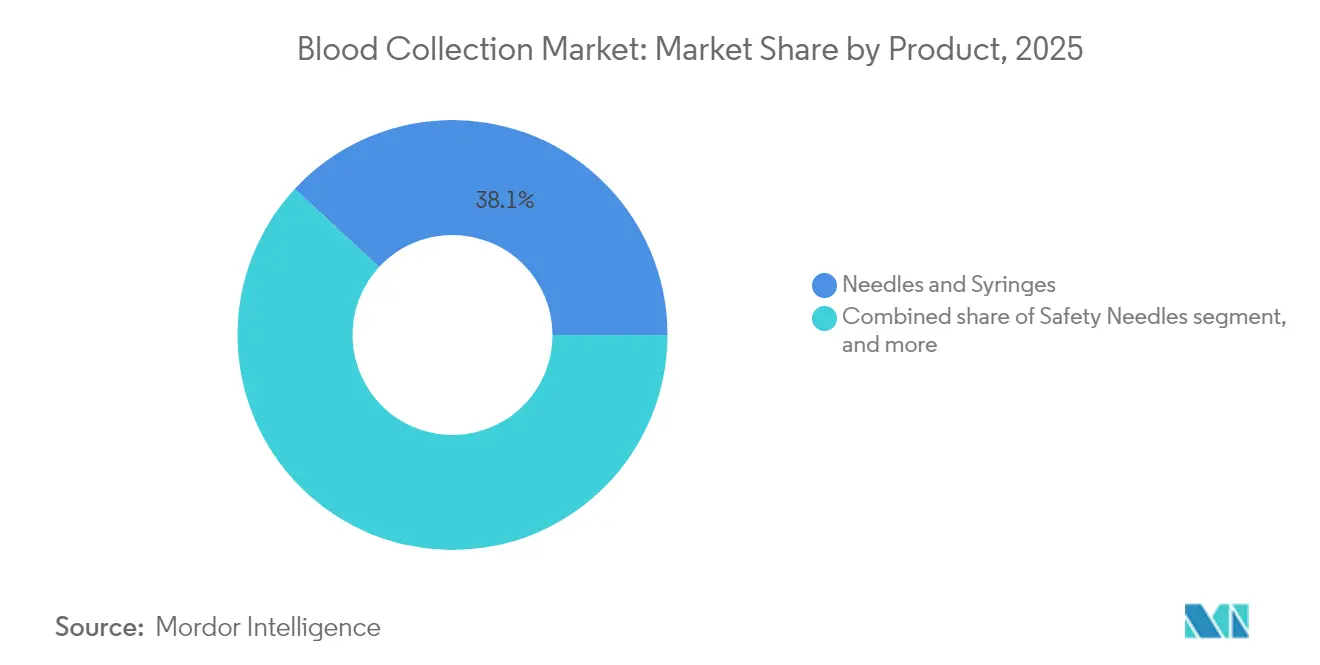

- By product, needles and syringes led with a 38.12% revenue share in 2025; tubes are anticipated to register the fastest growth of 7.29% CAGR through 2031.

- By collection method, manual collection held a 55.05% share of the blood collection market size in 2025, while automated systems are projected to advance at an 8.43% CAGR between 2026 and 2031.

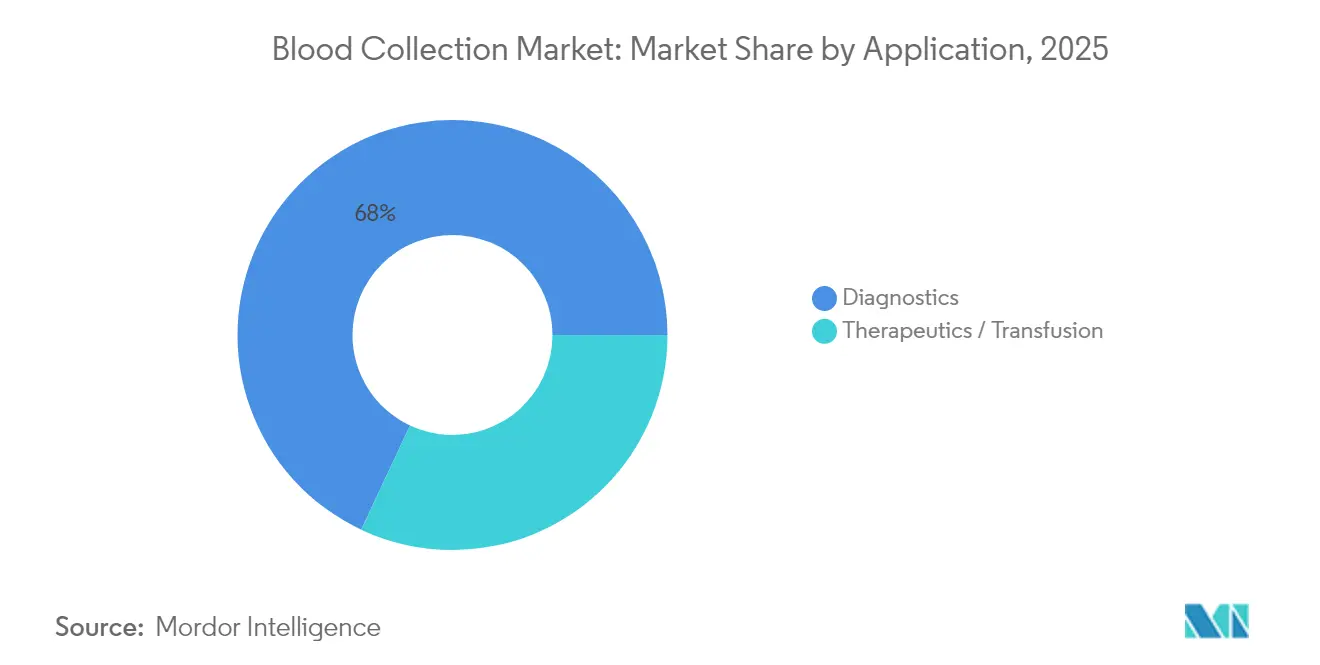

- By application, diagnostics accounted for a 68.02% share of the blood collection market size in 2025, and therapeutic/transfusion uses are forecast to grow at a 7.08% CAGR through 2031.

- By end user, hospitals and diagnostic centers captured 53.78% of the blood collection market share in 2025; point-of-care and home-care settings are set to expand at an 8.21% CAGR to 2031.

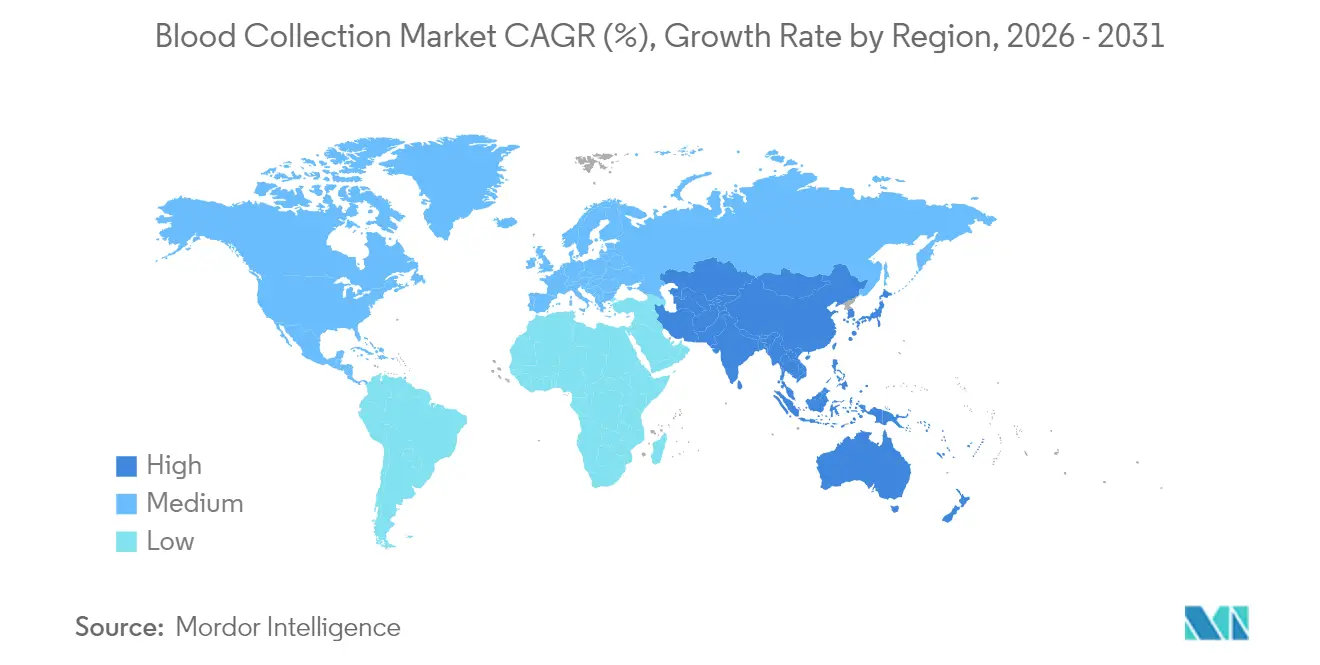

- By geography, North America accounted for 42.10% of 2025 revenue, whereas the Asia-Pacific region is poised for the highest 6.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Collection Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic diseases | +1.2% | North America, Europe, expanding globally | Long term (≥ 4 years) |

| Rising incidence of trauma and accidents | +0.8% | Higher impact in emerging markets | Medium term (2-4 years) |

| Increasing volume of surgical procedures | +1.1% | North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of diagnostic and POC infrastructure | +1.3% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Technological advances in collection devices | +0.9% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Government initiatives for blood safety | +0.7% | US and EU leadership | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic Diseases

Chronic disorders now affect 76.4% of US adults, and incidence among younger cohorts is climbing, pushing routine venous and capillary testing demand upward. Healthcare providers are scaling automated analyzers and decentralized sampling kits to manage rising specimen volumes without proportionally increasing headcount. Value-based care contracts tie reimbursement to timely monitoring, prompting hospitals to embed point-of-care (POC) coagulation and HbA1c panels inside primary-care clinics. Device makers respond by miniaturizing tubes pre-filled with optimized anticoagulants that preserve biomarkers for extended transport windows. These shifts collectively reinforce sustained revenue visibility for the blood collection market.

Rising Incidence of Trauma and Accidents

Urbanization correlates with higher trauma presentations that require immediate type-and-screen and coagulation work-ups. Level-I trauma centers are outfitting emergency bays with cartridge-based POC analyzers fed by 2 mL arterial draws, delivering results inside 3 minutes. The strategy reduces door-to-intervention time and improves survival metrics, nudging regional hospitals to replicate the model. Suppliers have introduced vacuum-assisted winged infusion sets with integrated flash-visibility to shorten first-stick time and minimize redraws under chaotic conditions. Emerging-market facilities are leapfrogging to these safety-optimized kits as donor agencies underwrite procurement.

Increasing Volume of Surgical Procedures

Elective and cancer-related surgeries rebounded in 2024, driving a 7% rise in blood sample throughput at leading academic medical centers. Higher median BMI among surgical candidates raises the probability of complex draws, fostering adoption of ultrasound-guided collection carts that locate deep veins swiftly. Minimally invasive techniques demand tighter peri-operative hemoglobin tracking, so operating suites now integrate inline sampling lines that funnel micro-volumes directly to blood gas analyzers. Collectively, these practices lift per-patient draw frequency, bolstering the blood collection market.

Expansion of Diagnostic and Point-of-Care Testing Infrastructure

Seventy-seven percent of hospitals ran POC blood-gas panels in 2024, reflecting a pivotal shift toward near-patient analytics. Pharmacy chains follow suit, piloting capillary-based lipid and COVID-19 antibody screens that need just six drops of blood using BD MiniDraw devices. Remote communities exploit mobile vans outfitted with battery-powered centrifuges, closing diagnostic gaps without building full labs. This democratization of testing scales demand for lightweight collection kits compatible with rugged environments, fuelling the blood collection market over the forecast horizon.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of blood-borne infections | −0.6% | Higher impact where safety infrastructure is weak | Medium term (2-4 years) |

| Needlestick injuries and liability | −0.8% | North America & Europe | Short term (≤ 2 years) |

| Alternative non-invasive diagnostics | −0.4% | North America & EU, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Shortage of skilled phlebotomists | −0.7% | Acute in rural and developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Risk of Blood-Borne Infections and Contamination

In 2025 the FDA issued updated hepatitis-B screening guidance that tightens performance criteria for donor testing platforms, raising compliance costs for collection centers. Facilities adopt double-sterility barriers and prefabricated closed-loop collection systems to mitigate contamination, but these safeguards elevate per-unit expense. Laboratories in infrastructure-poor regions struggle to fund such upgrades, deferring purchases and dampening near-term demand. Continuous surveillance for emerging pathogens maintains the pressure to upgrade devices, yet reimbursement schemes seldom offset added overhead, tempering the blood collection market’s expansion rate.

Needlestick Injuries and Associated Liability Costs

Hospital staff still sustain an estimated 385,000 needlestick incidents annually despite widespread safety devices, with 27.3% occurring even when protective features exist. Legal settlements and post-exposure prophylaxis inflate total cost per incident, steering procurement toward premium retractable or shielded needles. Asia-Pacific hospitals face unique challenges as insulin pen needles account for 20% of syringe injuries, prompting bulk conversion to safety-engineered pen sets. Although these transitions spur unit revenue growth, resistance from budget-constrained facilities can slow overall market uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Tubes Drive Specialized Testing Growth

Needles and syringes accounted for 38.12% of 2025 revenue, underscoring their widespread use for venous access across various care settings. Tubes, however, constitute the fastest-advancing niche, set to log a 7.29% CAGR through 2031 as clinicians demand additive-coded vacutainers tailored for genetics, proteomics, and oncology panels. This trajectory highlights how assay sophistication reconfigures consumable mix within the blood collection market.

Demand for safety needles rises steadily thanks to OSHA standards, yet premium pricing moderates adoption speed in low-margin outpatient labs. Capillary lancets are gaining favor in retail clinics, where fingertip sampling is sufficient for metabolic and infectious disease screens. BD MiniDraw exemplifies capillary innovation, matching venous-draw accuracy with six-drop volumes, broadening consumer access. Blood bags maintain stable hospital demand for transfusion services, although synthetic substitutes and optimized inventory systems are curbing volume growth. Emerging robotic and needle-free products, currently a small slice, could capture an outsized share post-2030 as clinical validation accumulates.

By Collection Method: Automation Gains Despite Manual Dominance

Manual draws retained a 55.05% share in 2025, reflecting the entrenched nature of these skills and their minimal capital requirements, especially in community hospitals and mobile drives. Yet the automated cohort will expand at an 8.43% CAGR, propelled by phlebotomist shortages projected at 19,600 US openings per year. Institutions trial autonomous robots like Vitestro’s system, achieving 95% first-stick success and standardizing specimen quality.

High-volume outpatient labs justify robotics through throughput and reduced redraw costs, whereas critical-access hospitals still rely on manual versatility for challenging anatomies. AI-guided ultrasound probes integrate seamlessly into carts, reducing the average collection time to 90 seconds and minimizing patient discomfort. Capital expenditure remains a barrier; nonetheless, leasing models and productivity incentives are narrowing the affordability gap, sustaining the blood collection market’s automation pivot.

By Application: Diagnostics Dominate While Therapeutics Accelerate

Diagnostics captured 68.02% of 2025 turnover as chronic disease monitoring and preventive screens became routine in primary care. The inclusion of molecular assays in standard check-ups increases the per-test yield, reinforcing the centrality of diagnostics to the blood collection market size.

Therapeutic and transfusion-oriented draws are expected to increase at a faster 7.08% CAGR through 2031, driven by cell-therapy manufacturing and clinical trials for laboratory-grown red blood cells. Specialized apheresis kits and leukoreduction filters support this vertical, with RESTORE-trial milestones expected to stimulate additional demand. Laboratories expand specimen banking for personalized oncology, driving uptake of cryo-preservation tubes and RNA-stabilizing media. While regenerative medicine remains nascent, each incremental trial inflates the value of high-integrity collection products.

By End User: Point-of-Care Settings Surge Ahead

Hospitals and reference labs owned 53.78% of sales in 2025, leveraging integrated workflows and group purchasing power. Their centralized models facilitate the rapid adoption of next-generation safety consumables and automation, keeping them at the forefront of customers within the blood collection devices industry.

Point-of-care and home-care venues, however, will post an 8.21% CAGR, energized by consumer demand for convenience and telemedicine adoption. Pharmacy chains embed MiniDraw bays staffed by general nurses, enabling after-work lipid-panel checks with no venipuncture training. Mobile nursing fleets carry capillary kits to rural homes, closing equity gaps and expanding the total addressable market for blood collection. Blood banks maintain their strategic relevance for transfusion support, but optimization software now curbs wastage, tempering the volume growth. Research institutes and pharmaceutical sponsors contribute to a niche demand for protocol-specific kits that preserve novel biomarkers.

Geography Analysis

North America preserved 42.10% of 2025 revenue, buoyed by stringent OSHA compliance and high per-capita test utilization. Hospitals invest in robotic phlebotomy pilots and transition to fully closed systems to meet tightening donor-screening guidelines that favor high-throughput, error-proof devices. Growth remains moderate given the region’s installed base, yet replacement cycles and tech refreshes underpin predictable recurring sales.

Europe follows closely, guided by the 2024 EU Regulation on substances of human origin, which harmonizes safety standards across member states and encourages cross-border sharing of blood products. National health systems allocate modernization funds to vacuum-assisted safety tubes and barcode traceability, underpinning steady expansion. Pilot deployments of AI-enabled vein-finders in Germany and the Netherlands illustrate how clinical performance benchmarks catalyze procurement decisions, supporting revenue uplift across Western Europe.

Asia-Pacific is set to deliver the fastest 6.19% CAGR to 2031, drawing on healthcare infrastructure upgrades and policy initiatives like Australia’s Plasma Pathway that add 95,000 donations annually. China’s hospital expansion plans integrate fully automated sample-processing lines, magnifying demand for compatible closed-system consumables. India’s telehealth surge spurs rural adoption of capillary-based lipid and glucose testing, stretching distribution networks and providing fresh volume streams for the blood collection market. Though Middle East & Africa and South America trail in spending power, targeted investments in tertiary centers and trauma facilities signal rising opportunities, especially for safety-engineered needles that satisfy WHO injury-prevention guidelines.

Competitive Landscape

The marketplace exhibits moderate fragmentation. Becton Dickinson, Terumo, and Cardinal Health each leverage global manufacturing scale and end-to-end portfolios spanning syringes, tubes, and safety accessories, enabling bundled contracting with large hospital networks. Continuous product refresh—such as BD’s pre-analytical micro-collection tubes tailored for mass spectrometry—safeguards share.

Disruptive entrants concentrate on patient-centric solutions. Vitestro’s CE-marked robot reduces procedure variability and targets outpatient draw stations where phlebotomist availability is tight. Tasso and Drawbridge Health market painless upper-arm microneedle kits that integrate with mail-in molecular test panels, unlocking a direct-to-consumer revenue lane. Partnerships are proliferating: BD infused capital into Babson Diagnostics to commercialize fingertip MiniDraw services within retail chains, accelerating omnichannel reach.

Intellectual-property filings climb as competitors explore nanocoated needles that reduce insertion force and terahertz spectroscopy for real-time hemoglobin quantification. Incumbents hedge disruption risk by co-developing platforms with start-ups or acquiring specialized IP. Regulatory know-how and distribution strength remain decisive, but the line between collection device and diagnostic interface continues to blur, compelling firms to broaden competencies well beyond legacy consumables.

Blood Collection Industry Leaders

Cardinal Health

Becton Dickinson and Company

Haemonetics Corporation

Medline Industries LP

Greiner Bio-One International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BD and Babson Diagnostics published data confirming MiniDraw capillary accuracy matched venous draws across comprehensive panels.

- March 2025: Tasso partnered with SNBL to offer at-home blood collection services across Japan, extending its Asia-Pacific footprint.

- December 2024: BD and Babson began commercial rollout of the combined MiniDraw-BetterWay fingertip testing platform to US health providers.

- October 2024: Babson secured a strategic equity injection from BD to accelerate retail deployment of fingertip testing booths.

- August 2024: Vitestro obtained CE mark for its robotic blood-drawing system, enabling commercial sales across Europe.

Global Blood Collection Market Report Scope

As per the scope of the report, blood specimen collection is a routine procedure performed to obtain blood for various laboratory tests. Blood can be collected from venous access devices and occasionally by fingerstick. However, it is most frequently obtained via a peripheral vein puncture called venipuncture.

The blood collection market is segmented by product, application, end user, and geography. By product, the market is segmented as needles and syringes, tubes, lancets, blood bags, and other products. By application, the market is segmented as diagnostics and treatment. By end user, the market is segmented as hospitals and diagnostic centers, blood banks, and other end users. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the market size and forecasts in value (USD) for the above segments.

| Needles & Syringes |

| Safety Needles |

| Tubes (Vacutainer, EDTA, Serum, Gel, Etc.) |

| Lancets & Capillary Devices |

| Blood Bags (Collection & Transfer) |

| Other Products |

| Manual |

| Automated |

| Diagnostics |

| Therapeutics / Transfusion |

| Hospitals & Diagnostic Centers |

| Blood Banks |

| Point-Of-Care & Home-Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Needles & Syringes | |

| Safety Needles | ||

| Tubes (Vacutainer, EDTA, Serum, Gel, Etc.) | ||

| Lancets & Capillary Devices | ||

| Blood Bags (Collection & Transfer) | ||

| Other Products | ||

| By Collection Method | Manual | |

| Automated | ||

| By Application | Diagnostics | |

| Therapeutics / Transfusion | ||

| By End User | Hospitals & Diagnostic Centers | |

| Blood Banks | ||

| Point-Of-Care & Home-Care Settings | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the blood collection market?

The sector generated USD 8.72 billion in 2026 and is set to reach USD 11.55 billion by 2031.

Which product segment is growing the quickest?

Tubes are advancing at a 7.29% CAGR thanks to specialized diagnostic protocols that require additive-specific vacutainers.

Why are automated blood collection systems gaining traction?

Labor shortages and the need for standardized, high-throughput sampling drive an 8.43% CAGR for automated platforms through 2031.

Which region is forecast to expand the fastest?

Asia-Pacific will grow at a 6.19% CAGR, propelled by healthcare infrastructure upgrades and chronic disease management programs.

How are safety regulations influencing device adoption?

OSHA-aligned mandates and updated FDA donor guidelines are accelerating replacement of conventional needles with safety-engineered and closed-loop devices.

Page last updated on: