Medical Vacuum Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

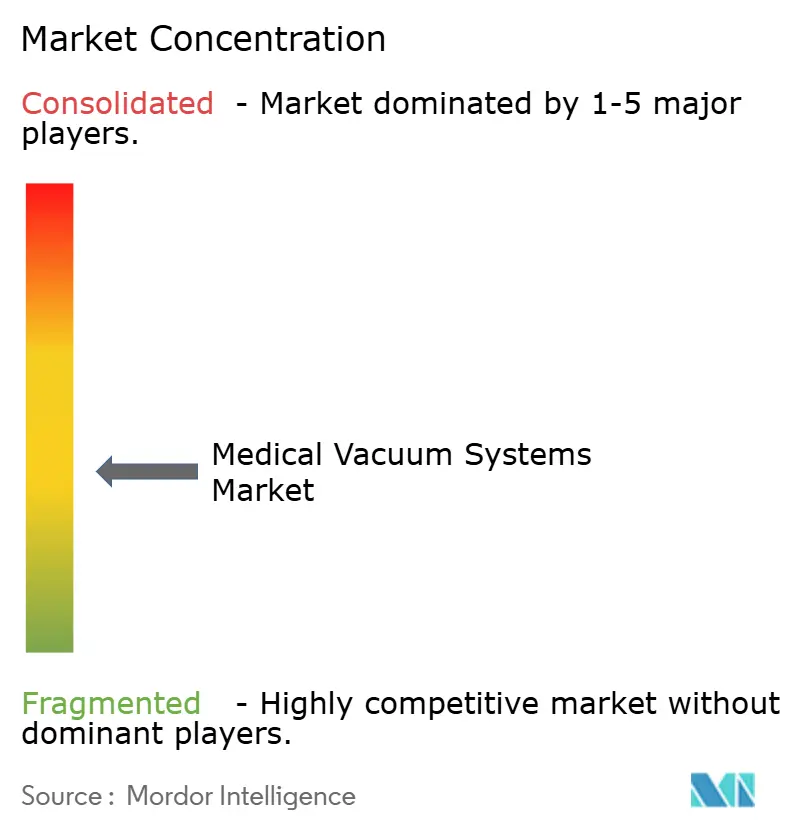

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Vacuum Systems Market Analysis by Mordor Intelligence

The Medical Vacuum Systems market size is expected to grow from USD 1.74 billion in 2025 to USD 1.85 billion in 2026 and is forecast to reach USD 2.51 billion by 2031 at 6.28% CAGR over 2026-2031.

Rising surgical volumes, the widening prevalence of chronic wounds, and hospitals’ shift to oil-free, energy-efficient pumps together form the backbone of this expansion. Healthcare providers are replacing water-ring and lubricated units with dry, NFPA-compliant platforms that deliver deeper vacuum levels, longer service life, and 30% lower energy use. Outpatient clinics and home-based wound-care programs also fuel demand for portable devices, while hospital decarbonization goals accelerate upgrades across centralized plants. Intensifying acquisition activity among leading manufacturers is consolidating know-how, broadening aftermarket networks, and keeping technological leadership firmly in view.

Key Report Takeaways

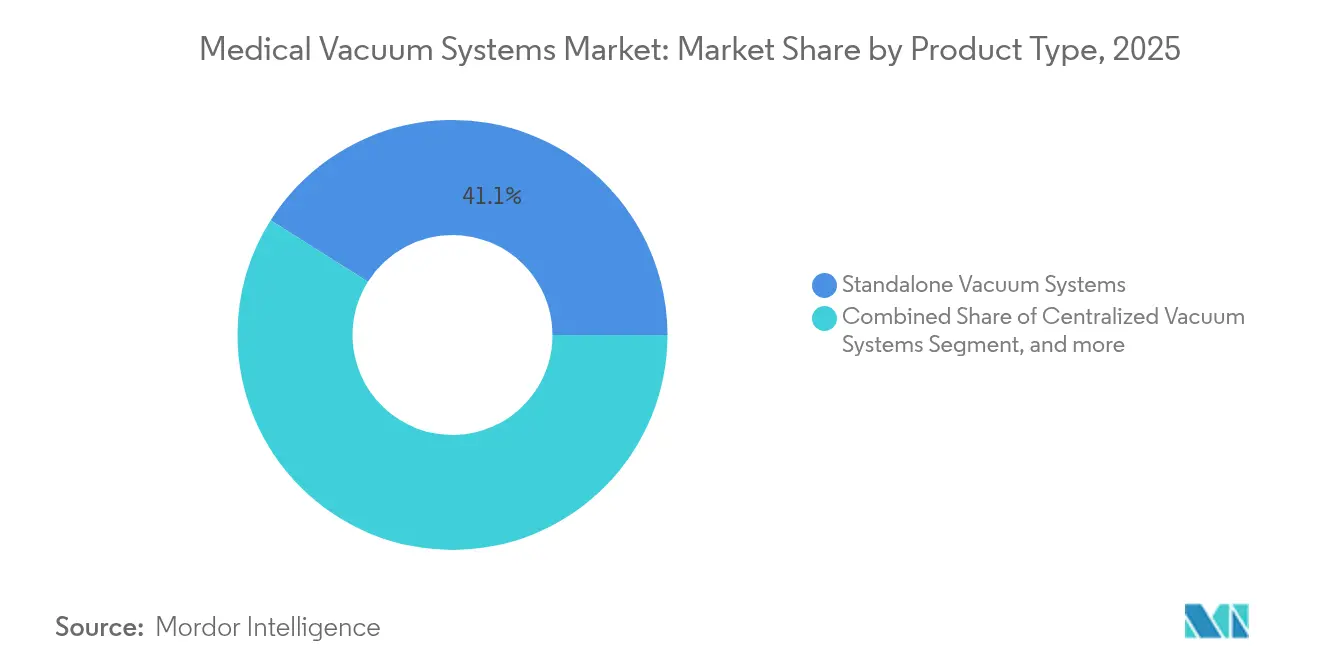

- By product type, standalone systems led with 41.05% of the medical vacuum systems market share in 2025; portable and compact systems are projected to expand at a 8.72% CAGR to 2031.

- By application, wound care and negative pressure wound therapy accounted for 31.66% of the medical vacuum systems market size in 2025, while dental applications are advancing at an 8.08% CAGR through 2031.

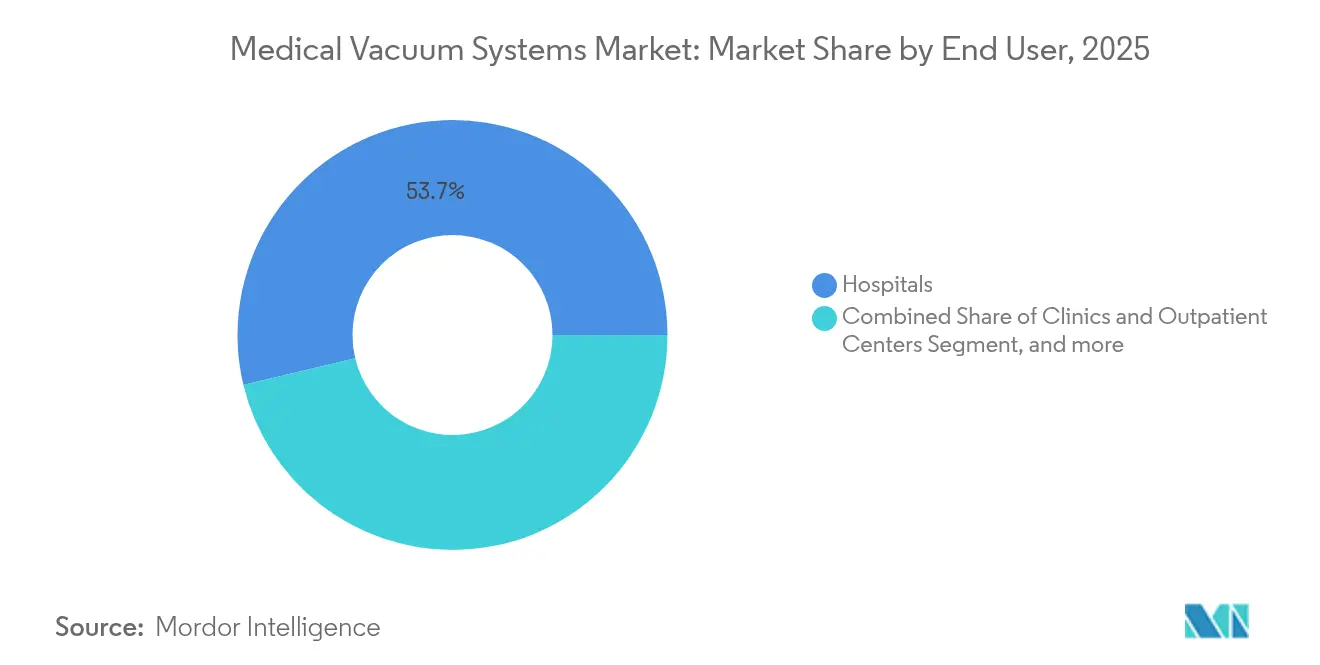

- By end user, hospitals held 53.74% of the medical vacuum systems market size in 2025, whereas home-care settings register the fastest growth at a 8.63% CAGR to 2031.

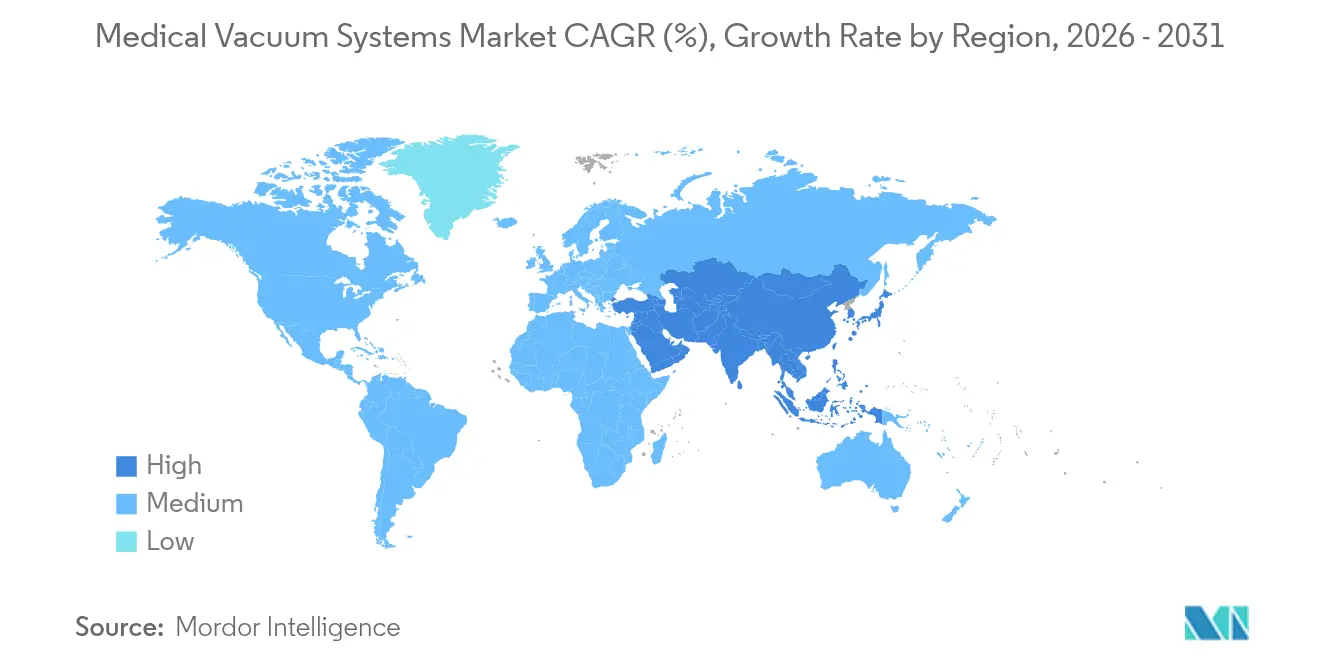

- By geography, North America captured 37.20% revenue in 2025; Asia-Pacific is forecast to post the fastest 7.59% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Vacuum Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic & infectious diseases | +1.8% | Global, higher in North America & Europe | Long term (≥ 4 years) |

| Growing surgical volumes & adoption of suction equipment | +1.5% | Global, led by Asia-Pacific emerging markets | Medium term (2-4 years) |

| Shift toward oil-free, NFPA-compliant dry vacuum pumps | +1.2% | North America & EU regulatory markets | Medium term (2-4 years) |

| Modular construction spurring demand for integrated vacuum booms | +0.9% | Mainly APAC, spill-over to MEA | Short term (≤ 2 years) |

| Hospital decarbonization targets favoring energy-efficient systems | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Expansion of outpatient wound clinics in emerging markets | +0.6% | Asia-Pacific, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic & Infectious Diseases

Chronic wounds affect up to 2% of the population in developed nations, and treatment for Medicare beneficiaries. These mounting costs are steering providers toward negative pressure wound therapy (NPWT) platforms that shorten healing times and reduce infection recurrence. COVID-19 heightened the need for reliable suction during respiratory management, while antibiotic resistance raised filtration standards across centralized plants. Larger facilities now deploy higher-capacity pumps with multi-stage filtration to protect immunocompromised patients. Value-based care incentives reward providers for lowering readmissions, keeping demand for portable and centralized NPWT solutions on a sustained upward path.

Growing Surgical Volumes & Adoption of Suction Equipment

An aging demographic and broader access to minimally invasive techniques are lifting global procedure counts, compelling operating rooms to integrate smarter fluid-control systems. Vacuum technology now reaches beyond basic suction into liposuction, endotracheal cleaning, and microsurgery fluid removal. Devices such as the Thopaz+ digital chest-drainage platform shorten intensive-care stays, which lowers costs and frees up capacity.[1]BeaconMedaes, “Thopaz+ Digital Chest Drainage System,” beaconmedaes.com In emerging Asia-Pacific markets, new operating theaters favor modular vacuum booms that install quickly without disruptive construction, helping hospitals bring critical services online faster.

Shift Toward Oil-Free, NFPA-Compliant Dry Vacuum Pumps

Regulators are tightening contamination and reliability rules, pushing hospitals toward dry technology. Oil-free pumps cut energy use by 30% compared with liquid-ring systems, eliminate water consumption, and extend service life from around 7 years to as long as 20 years.[2] Los Angeles Department of Water & Power, “Energy Efficiency Project Profiles,” ladwp.com Variable-speed drives save a further 50% in electricity, directly supporting hospital carbon-reduction programs. Dental operators, facing amalgam-separator mandates, are early adopters of contact-free claw and molecular-drag designs that meet NFPA 99 standards.[3]JH Foster, “Oil-Free Claw Pumps for Medical Applications,” jhfoster.com

Modular Construction Spurring Demand for Integrated Vacuum Booms

Hospitals in fast-growing regions are embracing off-site fabrication to open sooner and keep budgets predictable. Vacuum booms delivered as pre-tested modules shorten commissioning, improve spatial efficiency, and simplify future expansion. Builders specify units with built-in flow monitoring and remote diagnostics that tie into digital-hospital dashboards. The approach matches the speed of public–private build-operate-transfer projects in Asia-Pacific and especially fits resource-constrained markets needing standardized, replicable solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront & maintenance costs | -1.1% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Stringent installation-code compliance | -0.8% | North America & EU regulatory markets | Medium term (2-4 years) |

| Helium-supply volatility inflating pump manufacturing costs | -0.6% | Global manufacturing hubs | Short term (≤ 2 years) |

| Cyber-security risks in IoT-enabled centralized plants | -0.4% | Developed markets with advanced IT infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront & Maintenance Costs

Installing a medium-sized centralized plant often exceeds USD 100,000, and annual service contracts can reach 20% of that outlay. Budget-stretched hospitals in emerging economies must weigh these sums against beds, lab analyzers, and imaging equipment. Yet cost-of-care studies show portable NPWT can save USD 24,808 per complex-wound patient relative to surgery. Managed-equipment service agreements, such as the 98-facility Kenyan program, spread capital costs and guarantee uptime, gradually eroding this barrier.

Stringent Installation-Code Compliance

NFPA 99 stipulates strict testing, redundancy, and documentation, which lengthens timelines and pushes many facilities to hire certified contractors. Retrofits inside crowded plant rooms further complicate layout design. Multilayer regulation from device clearance to environmental permits varies by state, province, and municipality, increasing engineering hours. Manufacturers are now offering turnkey, pre-certified skids complete with templated inspection documents, shortening approval cycles and easing administrative load.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Standalone Systems Retain Capital Priority

Standalone pumps claimed 41.05% of the medical vacuum systems market in 2025, reflecting hospitals’ need for dedicated, high-capacity units in critical departments. These installations allow phased modernization because individual machines can be upgraded without disrupting wider service. Operating theaters and ICUs value quick service access and built-in redundancy that independent skids deliver. Energy-efficient dry-claw and scroll designs increasingly replace legacy lubricated models, dovetailing with capital programs aimed at cutting utility bills and maintenance labor.

Portable devices are growing fastest at a 8.72% CAGR. Home-health nurses routinely deploy two-pound, battery-powered NPWT dressings that stay in place for up to seven days, which keeps patients out of hospital and aligns with payer incentives. Advanced models now feature Bluetooth-enabled pressure logs that clinicians review remotely, supporting evidence-based therapy titration. The momentum behind decentralized care following the pandemic indicates sustained double-digit unit growth even after price erosion.

Accessories and consumables—filters, canisters, and tubing—form a resilient aftermarket stream that cushions revenue during capital-budget pauses. High-efficiency particulate filters must be replaced on a strict schedule, and antimicrobial canisters address rising infection-prevention standards. Manufacturers bundle these supplies into multiyear service packs that lock in customer loyalty and stabilize margins.

By Application: Wound Care Dominance Meets Dental Momentum

Wound care and NPWT captured 31.66% of the medical vacuum systems market size in 2025, underpinned by escalating diabetes prevalence and longer life expectancy. Studies attribute lower limb-amputation risk reduction and faster granulation to continuous-pressure dressings, while payers see shorter hospitalization episodes. Premium systems that incorporate intermittent instillation fetch higher prices, broadening revenue despite moderate unit sales. Hospitals also use centralized plants to feed multiple bedside NPWT stations simultaneously, further embedding vacuum infrastructure into wound-management pathways.

Dental suction exhibits the highest 8.08% CAGR as infection-control guidelines tighten. Small-footprint, oil-free pumps equipped with antimicrobe-lined piping help practitioners comply with amalgam-separator directives and reduce aerosol risks. A surge in cosmetic dentistry and orthodontics expands chair-time per patient, heightening demand for continuously reliable suction. Manufacturers market modular, under-cabinet packages that integrate air, vacuum, and water lines for simplified installation in new clinics.

Surgical and OR fluid management continues to evolve with minimally invasive techniques that require precise smoke evacuation and low-noise operation. Respiratory and airway management receives attention as ICUs expand capacity post-pandemic, leading to upgrades in vacuum regulators and pipeline outlets designed for high-flow suction during intubation. Laboratory and diagnostic applications maintain steady demand for vacuum ovens, filtration apparatus, and blood-gas analyzers, sustaining a diversified end-use mix.

By End User: Hospitals Dominate While Home Care Accelerates

Hospitals held 53.74% of the medical vacuum systems market size in 2025 owing to continual investment in operating theaters, intensive care expansion, and building-management integration. Multi-hospital networks standardize pump models and digital control panels to streamline spare-parts inventories and cross-facility maintenance. Predictive-maintenance algorithms tied into central supervisory control and data acquisition platforms forecast seal wear and trigger just-in-time service visits, minimizing downtime. Sustainability officers prioritize oil-free systems that pair with facility energy-management metrics, aligning capital buys with public net-zero pledges.

Home-care providers register a 8.63% CAGR through 2031, reflecting payers’ preference for lower-cost care sites and patients’ comfort with telehealth. Lightweight NPWT dressings average only USD 3,192 for a full healing episode compared with USD 28,000 for inpatient treatment. Device makers respond with intuitive interfaces, single-button pressure presets, and secure cellular connectivity that transfers compliance data to wound-care teams. Clinics and ambulatory surgical centers are also enlarging their vacuum footprints as same-day joint replacements and endoscopic procedures rise. Laboratories, diagnostic centers, and specialty outpatient hubs round out end-user demand with specialized vacuum requirements that call for oil-free, vibration-free systems to protect sensitive instruments.

Geography Analysis

North America accounted for 37.20% of the medical vacuum systems market in 2025, leveraging widespread NFPA 99 compliance and deep capital reserves for plant modernization. Health-system consolidation steers toward standardized technical specifications, enabling multisite frame agreements that lower unit costs and secure parts availability. Providers report 30% energy savings after upgrading to variable-speed, oil-free pumps, freeing operational budgets for further decarbonization. Major academic medical centers work closely with manufacturers during R&D, accelerating the rollout of digital diagnostics and remote-monitoring modules. Reimbursement certainty for NPWT under Medicare and private payers ensures ready uptake of premium portable devices across inpatient and outpatient settings.

Asia-Pacific is set to expand at an 7.59% CAGR, driven by large-scale hospital buildouts and growing domestic medical-device factories that shorten supply chains. Public healthcare investment programs in China, India, and Southeast Asia fund new tertiary centers equipped with NFPA-aligned medical-gas plants. Wound-healing clinics have multiplied rapidly, increasing specialized vacuum demand. Private hospitals targeting medical tourism install oil-free pumps and real-time vacuum alarms to meet international accreditation standards. While regulatory frameworks vary widely, regional harmonization efforts are underway, prompting vendors to develop adaptable compliance kits packaged for quick field-configuration.

Europe, the Middle East & Africa, and South America present meaningful growth potential as infrastructure expansions intersect with managed-equipment service models that mitigate upfront cost. The International Finance Corporation’s USD 56 billion commitment to private-sector healthcare in fiscal 2024 underscores lasting investment momentum ifc.org. European hospitals pursue ambitious climate targets under Green Deal policies, adopting dry-pump technology and intelligent controls to trim carbon footprints. Middle-East mega-hospital projects specify modular, pre-tested vacuum skids compatible with heat-recovery loops to cope with desert energy loads. South American providers partner with manufacturers for staff-training programs that counter limited engineering workforces and keep plant uptime high.

Competitive Landscape

The medical vacuum systems market remains moderately fragmented yet steadily converging as key suppliers strengthen vertical integration. Atlas Copco’s BeaconMedaes division, Busch Vacuum Solutions, and Gardner Denver (within Ingersoll Rand) command sizable installed bases. Each firm emphasizes proprietary oil-free pump designs, IoT-ready controllers, and multi-year service bundles that secure post-sale revenue. Product road maps lean heavily toward energy-efficiency improvements, remote diagnostics, and enhanced filtration performance that meets tightening infection-control norms.

Strategic acquisitions sharpen technological breadth. Ingersoll Rand’s purchase of Toshniwal Industries extended its footprint in precision pumps for Asia, while Busch Group’s acquisition of AVT GmbH deepened its service reach into heat-treatment vacuum furnaces. Supply-chain control from casting to rebuild kits shortens lead times and shields margins from raw-material inflation. Smaller regional players differentiate on rapid on-site service and custom engineering, though rising cybersecurity requirements may favor global actors equipped with robust IT-security resources.

Innovation revolves around predictive analytics platforms that integrate with hospital information technology. While such connectivity offers operational gains, health-system cybersecurity teams evaluate pump-controller firewalls and encrypted data paths before deployment, tempering immediate adoption. Manufacturers respond with isolated operational-technology networks, secure firmware-update protocols, and standards-based logging to alleviate concerns. Oil-free vacuum systems remain the definitive battleground as regulators and sustainability officers apply stronger purchasing weight to energy ratings and water conservation.

Medical Vacuum Systems Industry Leaders

Olympus Corporation

Atlas Copco AB (BeaconMedaes)

Busch Vacuum Solutions

Integra Biosciences AG

Ingersoll Rand (Gardner Denver)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Atlas Copco Group acquired Medi-teknique, a UK-based company specializing in maintenance contracts and servicing of medical gas pipeline systems, with revenues of approximately GBP 3.2 million (USD 4.1 million) in 2023, expanding regional coverage and aftermarket services.

- December 2024: Busch Group was recognized as world market leader in vacuum systems for 2025 by WirtschaftsWoche in collaboration with the University of St. Gallen, highlighting the company's innovation leadership in vacuum technology applications.

- November 2024: Busch Group completed the acquisition of AVT GmbH, a specialist in spare parts and services for industrial furnaces including vacuum furnaces used in medical technology applications, expanding service capabilities in heat treatment equipment markets.

- October 2024: Pfeiffer Vacuum rebranded as Pfeiffer Vacuum+Fab Solutions, reflecting its evolution into a comprehensive supplier for vacuum and semiconductor fab solutions as part of the Busch Group's strategic positioning in high-tech applications.

Global Medical Vacuum Systems Market Report Scope

As per the scope of the report, medical vacuum systems refer to the systems used to offer suction to unwanted fluids, and gases from laboratory and medical environments. These systems also offer a controlled framework through which medical specialists protect themselves from coming to contact with medically unhealthy substances. The medical vacuum systems are used in draining wounds, preparing assisted wound closures, lung and chest drainages, and others. medical vacuum systems market is segmented by product type, application, end-use and geography.

| Standalone Vacuum Systems |

| Centralized Vacuum Systems |

| Portable/Compact Vacuum Systems |

| Accessories & Consumables |

| Wound Care / NPWT |

| Anesthesiology |

| Gynecology & Obstetrics |

| Dental |

| Respiratory & Airway Management |

| Surgical Suction & OR Fluid Management |

| Diagnostic & Research |

| Pharma-Biotech Manufacturing |

| Hospitals |

| Clinics & Outpatient Centers |

| Laboratories & Diagnostic Centers |

| Pharmaceutical & Biotech Companies |

| Home Care Settings |

| Ambulance & Emergency Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Standalone Vacuum Systems | |

| Centralized Vacuum Systems | ||

| Portable/Compact Vacuum Systems | ||

| Accessories & Consumables | ||

| By Application | Wound Care / NPWT | |

| Anesthesiology | ||

| Gynecology & Obstetrics | ||

| Dental | ||

| Respiratory & Airway Management | ||

| Surgical Suction & OR Fluid Management | ||

| Diagnostic & Research | ||

| Pharma-Biotech Manufacturing | ||

| By End User | Hospitals | |

| Clinics & Outpatient Centers | ||

| Laboratories & Diagnostic Centers | ||

| Pharmaceutical & Biotech Companies | ||

| Home Care Settings | ||

| Ambulance & Emergency Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the medical vacuum systems market?

The market is valued at USD 1.85 billion in 2026 and is projected to reach USD 2.51 billion by 2031.

Which region is growing the fastest for medical vacuum systems?

Asia-Pacific is forecast to post the highest CAGR at 7.59% through 2031 due to large hospital buildouts and expanding device manufacturing.

Why are oil-free vacuum pumps gaining popularity in hospitals?

Oil-free technology lowers energy use by 30%, eliminates water consumption, extends service life up to 20 years, and meets stringent NFPA 99 contamination standards.

What application dominates the medical vacuum systems market?

Wound care and negative pressure wound therapy lead with 31.66% market share in 2025 thanks to their proven healing benefits and supportive reimbursement.

How are hospitals addressing budget constraints for vacuum system upgrades?

Many engage in managed-equipment service contracts that bundle equipment, maintenance, and training, allowing upgrades without large up-front capital expenditure.

Page last updated on: