U.S. Non-PVC IV Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

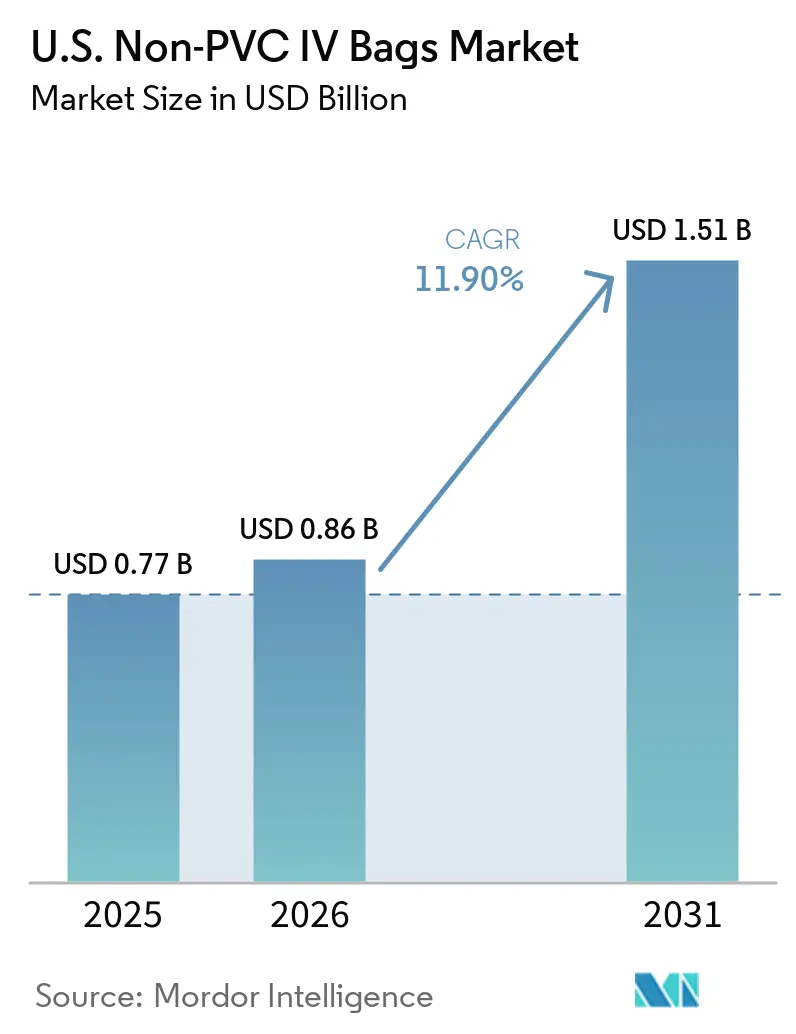

| Base Year Market Size (2025) | USD 0.77 Billion |

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.51 Billion |

| Growth Rate (2026 - 2031) | 11.90% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

U.S. Non-PVC IV Bags Market Analysis by Mordor Intelligence

The U.S. Non-PVC IV Bags Market size is projected to be USD 0.77 billion in 2025, USD 0.86 billion in 2026, and reach USD 1.51 billion by 2031, growing at a CAGR of 11.90% from 2026 to 2031.

The United States non-PVC IV bags market is growing faster than the broader infusion-bag sector. This growth is driven by the shift away from DEHP, influenced by legal mandates, hospital policies, and product selection standards. California's AB 2300 has established a clear compliance framework, while legislative actions in North Carolina and Pennsylvania have transitioned hospital procurement teams from optional plans to fixed schedules. Supply disruptions caused by Hurricane Helene prompted providers to reassess purchasing strategies. They now prioritize domestic supply resilience and dual sourcing to mitigate risks associated with a limited manufacturing base. The adoption of non-PVC materials is further supported by the increasing use of ready-to-administer premix formats, frozen mixtures, and multi-chamber systems, which enhance drug stability and workflow safety.

Key Report Takeaways

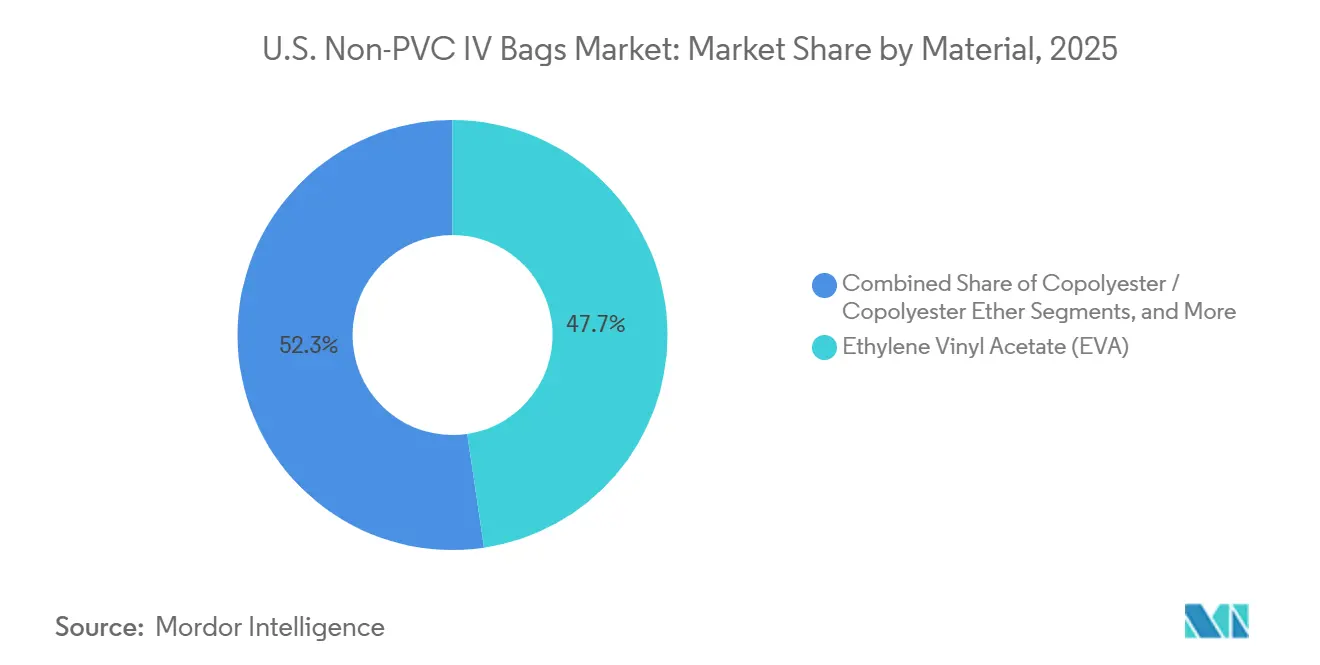

- By material, EVA held 47.65% of revenue in 2025, while polypropylene recorded the fastest projected growth at a 13.20% CAGR through 2031.

- By chamber configuration, single-chamber bags accounted for 65.55% of revenue in 2025, while multi-chamber bags are projected to expand at a 12.10% CAGR through 2031.

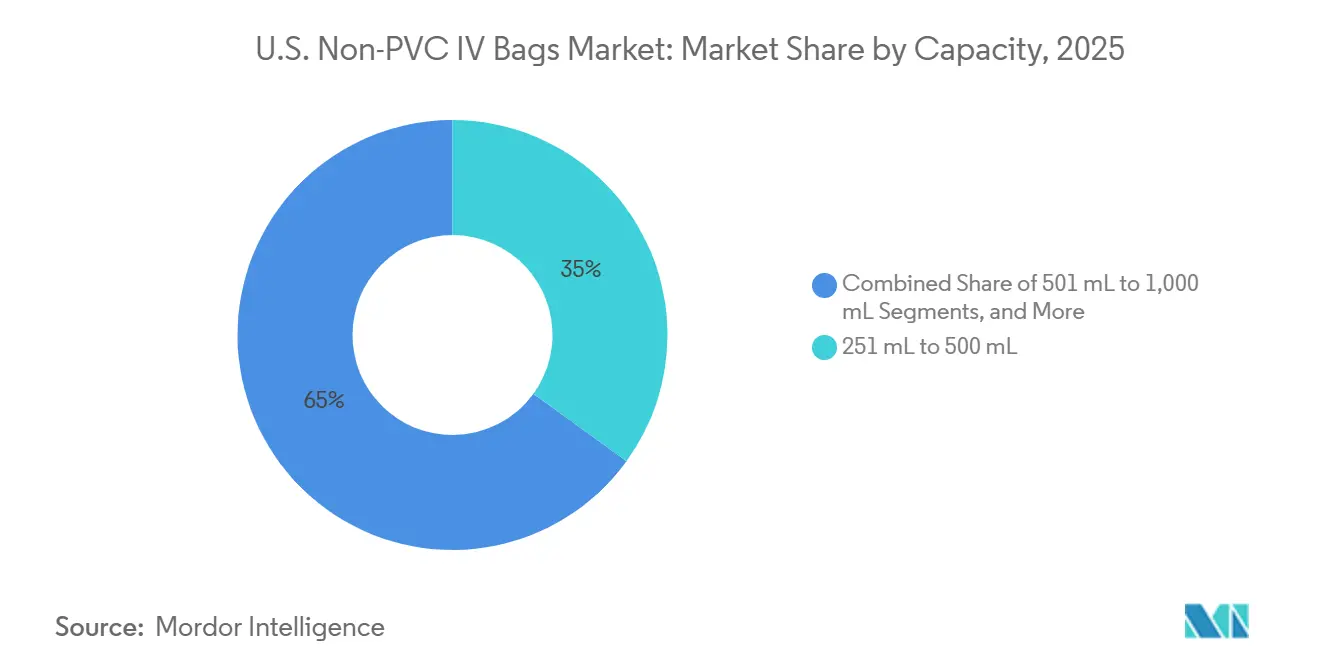

- By capacity, 251 mL to 500 mL bags captured 34.99% of revenue in 2025, while the 100 mL to 250 mL range is projected to grow at a 12.75% CAGR through 2031.

- By content type, liquid mixtures led with a 69.60% revenue share in 2025, while frozen mixtures are projected to advance at a 13.55% CAGR through 2031.

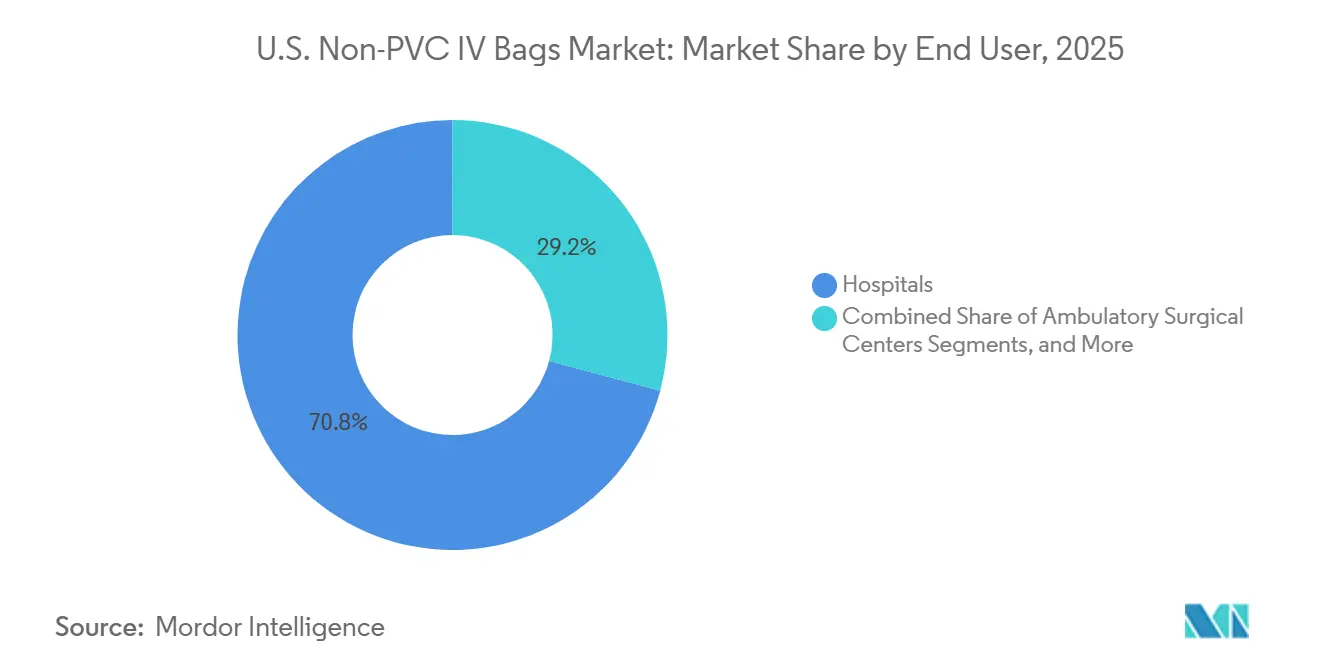

- By end user, hospitals held 70.85% of revenue in 2025, while ambulatory surgical centers are expected to post the highest CAGR at 12.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Non-PVC IV Bags Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| DEHP and PVC phase-out in high-risk patient cohorts | +3.2% | National, with early enforcement in California, North Carolina, Pennsylvania, and Washington | Short term (≤ 2 years) |

| Oncology and hazardous-drug compatibility needs | +2.5% | National, concentrated in NCI-designated cancer centers and infusion clinics in the Northeast, Southeast, and West Coast | Medium term (2-4 years) |

| Ready-to-administer and premix infusion adoption | +2.1% | National, with accelerated uptake in high-volume urban hospital systems | Medium term (2-4 years) |

| Domestic supply-resilience sourcing after IV fluid disruption | +1.8% | National, with capacity build-out in the Southeast and South-Central corridors | Short term (≤ 2 years) |

| USP <797>-driven container validation in sterile compounding | +1.5% | National, affecting 503A and 503B pharmacies, hospital compounding units, and infusion centers | Medium term (2-4 years) |

| State-level non-DEHP compliance and sustainability-led procurement | +1.3% | California, North Carolina, Pennsylvania, and Washington, with expected spillover to other states by 2028 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

DEHP/PVC Phase-Out in High-Risk Patient Cohorts Drives Specification Rewrites

State laws are driving the United States non-PVC IV bags market by setting clear standards for hospitals and suppliers. California's AB 2300, enacted in September 2024, bans DEHP in IV solution containers from 2030 and prohibits substitution with other ortho-phthalates.[1]California Legislature, “AB-2300 Medical Devices Di-(2-Ethylhexyl) Phthalate (DEHP),” California Legislative Information, leginfo.legislature.ca.gov Pennsylvania's Senate Bill 804, passed in March 2026, follows a similar approach. These regulations are critical in neonatal care, oncology infusion, and long-term parenteral nutrition, where plasticizer migration risks are significant. Pharmaceutical Compounding Sterile Preparations,” USP, usp.org"> Pharmaceutical Compounding Sterile Preparations,” USP, usp.org"> Pharmaceutical Compounding Sterile Preparations,” USP, usp.org">[2]United States Pharmacopeia, “General Chapter <797> Pharmaceutical Compounding Sterile Preparations,” USP, usp.org Hospitals revising specifications for these patient groups often extend changes across broader formularies for easier standardization, accelerating the market's shift to system-wide adoption.

Oncology and Hazardous-Drug Compatibility Needs Redefine Container Selection Standards

In oncology, stricter container selection criteria emphasize compatibility with hazardous drugs, increasing the demand for non-PVC materials. Updated USP standards have shifted focus from cost to container interaction with formulations. Non-PVC options like polypropylene multilayer systems are preferred for their chemical stability and safety. Suppliers such as ICU Medical and Fresenius Kabi are positioning non-PVC formats for critical applications, embedding these specifications into routine practices and stabilizing market demand.

Ready-to-Administer and Premix Infusion Adoption Reshapes Compounding Economics

The United States non-PVC IV bags market benefits from the growing adoption of premix products, which reduce in-house compounding and streamline workflows. Ready-to-use premix medications offer 9- to 24-month shelf lives, enhancing storage and standardization. Non-PVC systems like Baxter's GALAXY containers and Fresenius Kabi's freeflex bags support frozen and room-stable formats, ensuring drug integrity and reducing compounding errors. This trend aligns with hospitals' efforts to lower labor intensity in sterile preparations, driving faster market adoption.

Domestic Supply-Resilience Sourcing Accelerates Nearshoring Investment

The 2024 disruption at Baxter's North Cove facility highlighted the risks of supply concentration, prompting investments in domestic manufacturing. Fresenius Kabi's Wilson, North Carolina facility and ICU Medical's partnership with Otsuka Pharmaceutical Factory, operational since May 2025, have expanded production capacity to approximately 1.4 billion annual IV solution units. Hospitals increasingly favor suppliers meeting non-PVC specifications with reliable redundancy, securing long-term agreements that stabilize market dynamics.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Higher non-PVC resin and conversion economics | -1.8% | National, disproportionately impacting rural hospitals, critical-access facilities, and independent ASCs | Medium term (2-4 years) |

| Drug-container compatibility and validation burden | -1.2% | National, concentrated in academic medical centers and specialty pharmacies running large oncology and parenteral nutrition programs | Long term (≥ 4 years) |

| Installed-base PVC workflow lock-in | -0.9% | National, particularly in mid-size community hospitals with existing smart-pump libraries configured for PVC bag geometries | Medium term (2-4 years) |

| Non-DEHP versus non-PVC labeling ambiguity | -0.5% | National, creating procurement confusion especially in multi-facility hospital systems without standardized formulary management protocols | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Non-PVC Resin and Conversion Economics Constrain Adoption Rate

The primary barrier to faster adoption is cost, as advanced non-PVC films are priced higher than standard PVC materials. Bag manufacturers face increased expenses due to costly inputs like polypropylene and advanced EVA structures, along with additional investments in equipment. Hospitals and Ambulatory Surgical Centers (ASCs), particularly smaller facilities with fixed-price contracts, struggle to absorb these higher costs. The broader economic benefits of premix use, such as reduced labor and handling, are often overlooked in budget evaluations, slowing the transition despite strong clinical and compliance arguments. Growth in the United States non-PVC IV bags market remains steady, but the pace depends on balancing material safety with cost pressures.

Drug-Container Compatibility and Validation Burden Slows Formulary Transitions

Extensive validation for each drug and bag combination is another key restraint. Non-PVC materials like EVA and polypropylene vary in extractables, leachables, and storage performance, requiring thorough documentation. The emphasis on sterile preparation controls has increased the focus on compatibility during purchasing and formulary transitions. Academic medical centers and oncology programs face greater challenges due to broader formularies and complex products like lipid-based and biologic drugs. This slows the shift from PVC formats, as each formulation change demands detailed reviews. However, once validation is complete, hospitals rarely revert, reducing the long-term impact on the United States non-PVC IV bags market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: EVA Anchors Market, Polypropylene Commands Premium Growth Trajectory

In 2025, EVA accounted for 47.65% of revenue, making it the leading material in the United States non-PVC IV bags market. Its dominance stems from broad drug compatibility, clear visibility for inspections, and stable freeze-thaw performance, making it ideal for frozen antibiotics, electrolyte solutions, and blood-compatible formulations. EVA's versatility supports standardized bag formats, reinforcing its position as the market's foundation.

Polypropylene, growing at a 13.20% CAGR through 2031, is gaining traction in specialized applications like oncology and multi-chamber parenteral nutrition systems. Its advantages include hazardous-drug compatibility and suitability for advanced multi-layer construction. Innovations like Fresenius Kabi's patent for multilayer infusion bags highlight the material's expanding role in premium clinical applications.

By Chamber Configuration: Single-Chamber Dominance Persists as Multi-Chamber Bags Accelerate

Single-chamber bags held 65.55% of revenue in 2025, maintaining their lead in the United States non-PVC IV bags market. Their straightforward use in fluid replacement and routine infusions, coupled with ease of manufacturing and alignment with nursing workflows, ensures their continued dominance.

Multi-chamber bags, projected to grow at a 12.10% CAGR through 2031, address the demand for ready-to-mix products in parenteral nutrition and antibiotic combinations. These bags simplify sterile preparation, reduce compounding errors, and align with standardized workflows, driving their growth in the market.

By Capacity: Mid-Range Volumes Lead While Small-Dose Formats Accelerate With Targeted Therapy Growth

The 251 mL to 500 mL segment led with 34.99% of revenue in 2025, reflecting its alignment with common adult dosing practices for antibiotics, hydration, and antiviral treatments. Its balance of flexibility and standardization makes it a cornerstone of hospital inventories.

The 100 mL to 250 mL segment, growing at a 12.75% CAGR through 2031, is driven by the rise of targeted oncology therapies and biologics. These smaller volumes require non-PVC, non-DEHP-compliant bags to ensure drug integrity, making this segment a key growth driver.

By Content Type: Liquid Mixtures Lead on Volume, Frozen Mixtures Accelerate on Safety Economics

Liquid Mixtures dominated with 69.60% of revenue in 2025, driven by their use in routine therapies like saline maintenance and antibiotic administration. Their compatibility with automated systems and established supply chains ensures their continued market leadership.

Frozen Mixtures, growing at a 13.55% CAGR through 2031, offer extended shelf-life and reduced on-site compounding needs. Their suitability for temperature-sensitive medications and high-sensitivity therapies positions them as a critical growth area in the market.

By End User: Hospitals Anchor Demand, ASCs Represent the Sharpest Growth Inflection

Hospitals accounted for 70.85% of revenue in 2025, leading the United States non-PVC IV bags market due to high surgical and inpatient IV volumes. Their scale and compliance with state regulations position them as key drivers of market demand.

Ambulatory Surgical Centers, growing at a 12.66% CAGR through 2031, are expanding due to the shift toward outpatient procedures. Their preference for compact, lighter non-PVC bags aligns with portable smart-pump systems, making them a significant growth segment in the market.

Geography Analysis

In 2026, the United States non-PVC IV bags market, valued at USD 0.863 billion, sees its strongest regulatory momentum on the West Coast. California's AB 2300 mandates a 2030 ban on DEHP in IV solution containers, prompting early procurement planning by major delivery networks. With over 400 acute-care hospitals and a large patient base, California's decisions significantly influence national supplier strategies. Hospitals are acting early to manage formulary changes, contract cycles, and inventory transitions, positioning the West Coast as a leader in the market.

The Southeast has become a key production hub for the United States non-PVC IV bags market, driven by regulatory changes and manufacturing investments. North Carolina's policy alignment with California and the opening of Fresenius Kabi's Wilson freeflex facility in 2024 have strengthened domestic supply. ICU Medical's Austin operations, supported by its Otsuka partnership, further enhance the region's role. Concentrated production reduces lead times for nearby hospitals and highlights the competitive advantage of regional manufacturing.

The Northeast and Midwest remain major consumption centers due to dense hospital networks and academic institutions, though their transition to non-PVC IV bags has been slower. Pennsylvania's 2026 Senate action is expected to accelerate conversions in the Northeast, particularly in Philadelphia and Pittsburgh. In the Midwest, Baxter's non-PVC premix platforms and recycling initiatives maintain engagement despite limited state-led policy pressure. States without DEHP legislation represent near-term opportunities, where GPO decisions and contract renewals can drive faster adoption. The market reflects a pattern where policy-driven states lead demand, while non-legislated states offer the next growth wave.

Competitive Landscape

The United States non-PVC IV bags market is moderately consolidated, with Baxter International, Fresenius Kabi USA, and ICU Medical holding key strategic positions. Baxter, the world's largest flexible IV bag supplier, has committed to transitioning its portfolio to fully non-DEHP IV fluid bags by 2030 and IV tubing by 2035. This move signals a shift away from legacy materials. Baxter also utilizes its GALAXY platform to enhance premix and frozen product categories, emphasizing workflow and shelf-life benefits. Fresenius Kabi has strengthened its position through domestic capacity, particularly at its Wilson, North Carolina freeflex facility, and offers a diverse portfolio of PVC- and DEHP-free bags across various sizes and formulations. Competition now focuses on scale, compliance, and supply continuity.

ICU Medical has adopted a partnership-driven approach, securing a significant role in the United States non-PVC IV bags market, especially in advanced formats. Its collaboration with Otsuka Pharmaceutical Factory has created a platform with an annual capacity of 1.4 billion IV solution units, aimed at introducing PVC-free technologies like admixtures, multi-chamber parenteral nutrition bags, and premix IV antibiotics to North America. Additionally, ICU Medical's distribution of the Fleboflex polypropylene container highlights its strategy to combine external film expertise with its commercial reach. Fresenius Kabi's 2025 patent activity on multilayer bag construction underscores the growing importance of material science and bag performance as competitive differentiators. Strategic decisions now revolve around platform depth, clinical fit, and proprietary manufacturing expertise.

U.S. Non-PVC IV Bags Industry Leaders

-

B. Braun Medical Inc.

-

Baxter International Inc.

-

Fresenius Kabi AG

-

ICU Medical, Inc.

-

RENOLIT SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GVS launched Non-PVC multilayer IV bags designed to meet stringent medical regulations and high-quality standards for infusion and drug delivery solutions.

- March 2026: Pennsylvania's Senate passed Senate Bill 804 with a 48-1 vote, proposing a ban on DEHP in IV solution containers by 2035. The bill also prohibits replacing DEHP with other ortho-phthalates, ensuring compliance without chemical substitution.

- February 2026: axter International expanded its US IV solutions manufacturing capacity by upgrading sterile fluid production lines. The initiative focuses on increasing premixed IV bag output to meet rising hospital demand and address drug shortages following the 2024 North Cove disruption.

- May 2025: ICU Medical, Inc. and Otsuka Pharmaceutical Factory, Inc. formed Otsuka ICU Medical LLC, a joint venture with an upfront payment of approximately USD 200 million from Otsuka. The partnership combines ICU Medical's Austin, Texas production with Otsuka's 16-site Asian manufacturing network, creating an annual capacity of 1.4 billion IV solution units and focusing on introducing PVC-free technologies to the North American market.

U.S. Non-PVC IV Bags Market Report Scope

As per the scope of the report, non-PVC IV bags are specialized medical containers used to deliver fluids, medications, and nutrients into a patient's bloodstream. Unlike traditional polyvinyl chloride (PVC) bags, they are manufactured using advanced polymers like polypropylene, polyethylene, or ethylene-vinyl acetate (EVA).

The U.S. Non-PVC IV Bags Market is segmented by material, chamber configuration, capacity, content type, and end-user. By material, the market includes polypropylene, polyolefin blends, ethylene vinyl acetate (EVA), copolyester/copolyester ether, and ethylene-propylene copolymer and other multilayer films. By chamber configuration, the market is segmented into single-chamber bags and multi-chamber bags. By capacity, the market is categorized into below 100 mL, 100 mL to 250 mL, 251 mL to 500 mL, 501 mL to 1,000 mL, and above 1,000 mL. By content type, the market includes liquid mixtures and frozen mixtures. By end-user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Polypropylene |

| Polyolefin blends |

| Ethylene Vinyl Acetate (EVA) |

| Copolyester / Copolyester Ether |

| Ethylene-Propylene Copolymer and Other Multilayer Films |

| Single-chamber bags |

| Multi-chamber bags |

| Below 100 mL |

| 100 mL to 250 mL |

| 251 mL to 500 mL |

| 501 mL to 1,000 mL |

| Above 1,000 mL |

| Liquid Mixtures |

| Frozen Mixtures |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Others |

| By Material | Polypropylene |

| Polyolefin blends | |

| Ethylene Vinyl Acetate (EVA) | |

| Copolyester / Copolyester Ether | |

| Ethylene-Propylene Copolymer and Other Multilayer Films | |

| By Chamber Configuration | Single-chamber bags |

| Multi-chamber bags | |

| By Capacity | Below 100 mL |

| 100 mL to 250 mL | |

| 251 mL to 500 mL | |

| 501 mL to 1,000 mL | |

| Above 1,000 mL | |

| By Content Type | Liquid Mixtures |

| Frozen Mixtures | |

| By End User | Hospitals |

| Specialty Clinics | |

| Ambulatory Surgical Centers | |

| Others |

Key Questions Answered in the Report

What is the expected value of the US non-PVC IV bags market by 2031?

The US non-PVC IV bags market is forecast to reach USD 1.51 billion by 2031 from USD 0.863 billion in 2026, with an 11.90% CAGR over the period covered in this draft.

Why are hospitals moving away from PVC-based IV bags in the United States?

The shift is being driven by state DEHP restrictions, stricter attention to compatibility and documentation, and growing use of premix and frozen formats that are better suited to non-PVC materials.

Which material leads current revenue and which one is growing fastest?

EVA led with 47.65% of revenue in 2025 because of broad compatibility and strong freeze-thaw performance, while polypropylene is forecast to grow fastest at a 13.20% CAGR through 2031.

Which content type is expanding most quickly?

Frozen Mixtures are the fastest-growing content type at a 13.55% CAGR through 2031 because they combine longer shelf life, lower compounding burden, and stronger fit for stability-sensitive therapies.

Why are multi-chamber bags gaining traction?

Multi-chamber bags are projected to grow at a 12.10% CAGR because they support ready-to-mix nutrition and antibiotic formats that reduce preparation steps and help limit compounding errors.

Which end-user group offers the strongest growth opportunity outside hospitals?

Ambulatory Surgical Centers are the fastest-growing end-user segment with a 12.66% CAGR through 2031, supported by the continued shift of eligible procedures toward outpatient settings.

Page last updated on: