Mortuary Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

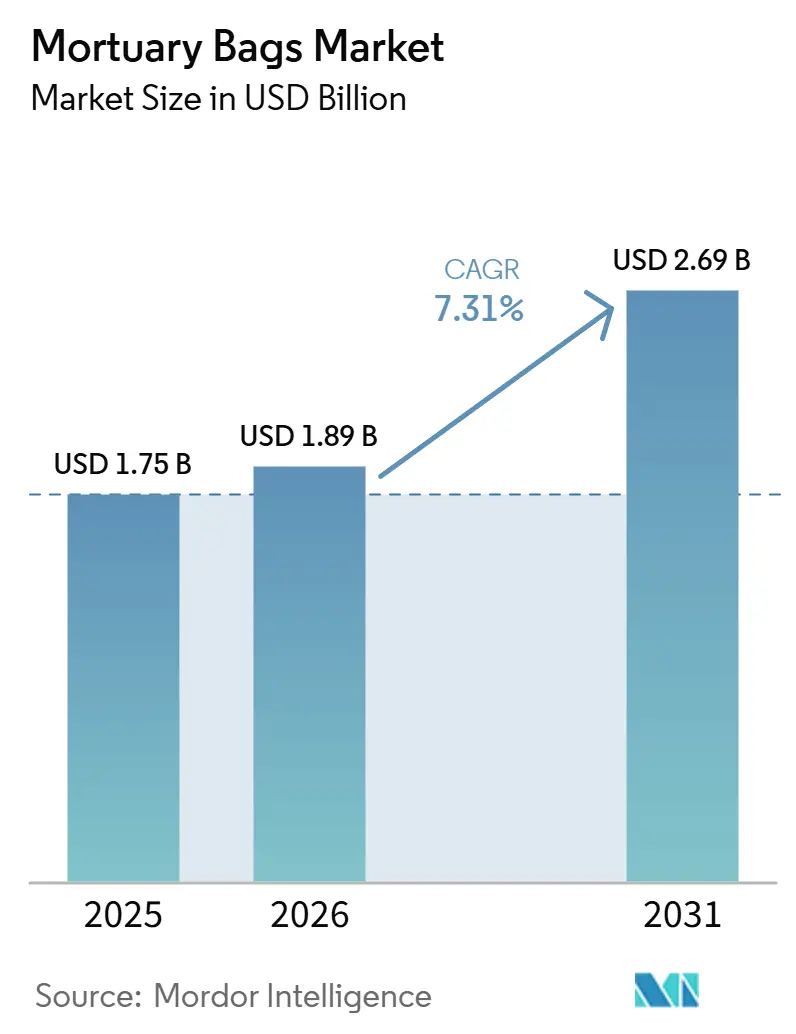

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mortuary Bags Market Analysis by Mordor Intelligence

The Mortuary Bags Market size is projected to expand from USD 1.75 billion in 2025 and USD 1.89 billion in 2026 to USD 2.69 billion by 2031, registering a CAGR of 7.31% between 2026 to 2031.

Surging demand stems from a combination of global aging, intermittent infectious disease outbreaks, and tighter biohazard regulations that require hospitals, mortuaries, and emergency response agencies to refresh containment inventories[1]Occupational Safety and Health Administration, “Bloodborne Pathogens Standard,” osha.gov. Ongoing materials innovation, exemplified by biodegradable and PFAS-free polymers, is widening replacement cycles, while RFID-enabled traceability and predictive stockpiling tools improve operational visibility for high-throughput facilities. Disaster-preparedness programs such as FEMA’s portable morgue units are spurring interest in heavy-duty, liquid-resistant pouches that remain stable under prolonged refrigeration[2]United Nations Department of Economic and Social Affairs, “World Population Prospects 2024 Revision,” un.org. Meanwhile, price swings in polyethylene and PVC resins heighten cost-management risk, prompting leading manufacturers to pursue long-term supply contracts and hedging strategies. The intersection of demographic pressure, sustainability mandates, and technology adoption positions the mortuary bags market for steady mid-single-digit expansion through 2031.

Key Report Takeaways

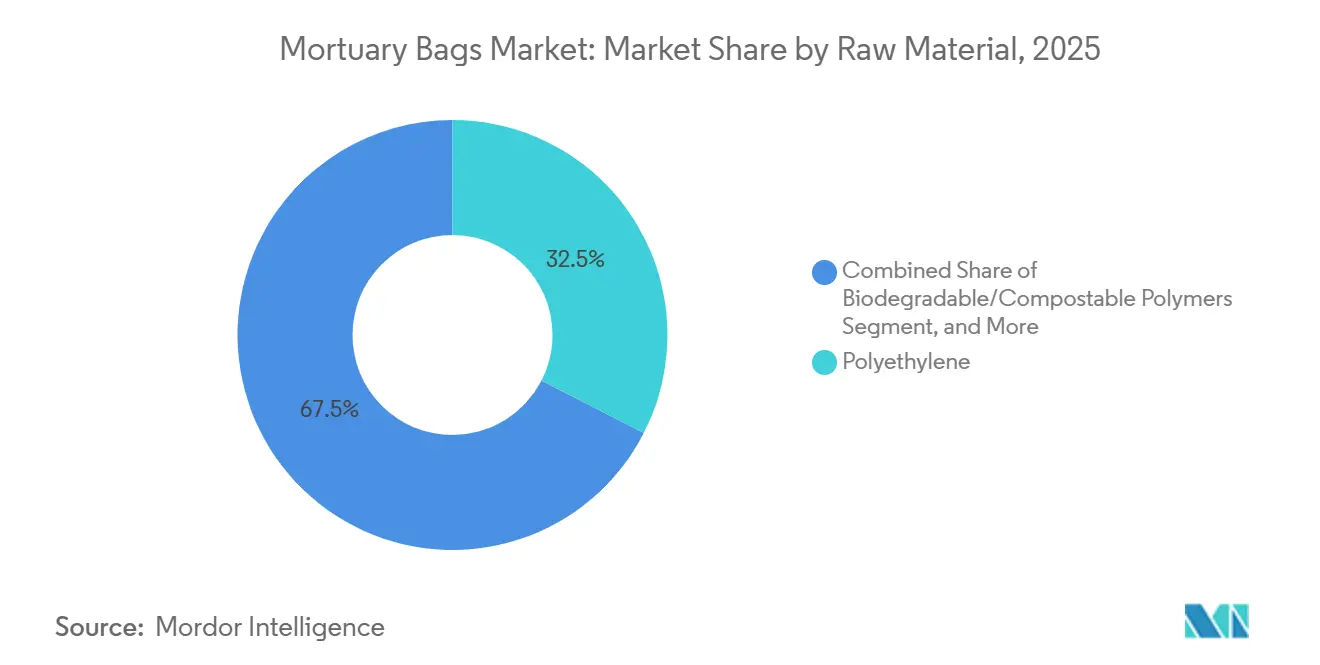

- By raw material, polyethylene led with 32.55% of the mortuary bags market share in 2025; biodegradable and compostable polymers are on track to grow at a 9.25% CAGR through 2031.

- By size, the adult segment captured 46.53% share of the mortuary bags market in 2025, while bariatric variants are forecast to expand at an 8.85% CAGR between 2026 and 2031.

- By weight duty, standard-duty designs held 39.23% of the mortuary bags market in 2025; heavy-duty offerings are advancing at an 8.55% CAGR to 2031 on the back of disaster-response procurement.

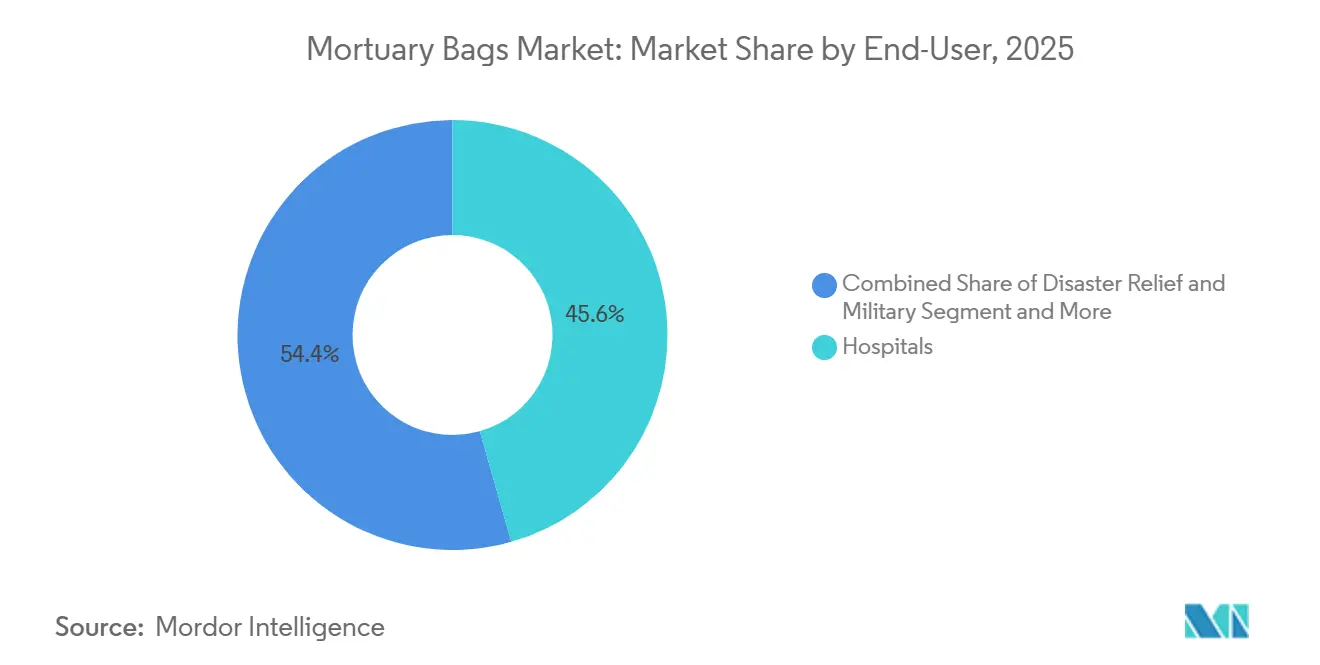

- By end-user, hospitals commanded 45.63% of the mortuary bags market in 2025, whereas the disaster-relief and military channels registered the highest growth at a 7.85% CAGR to 2031.

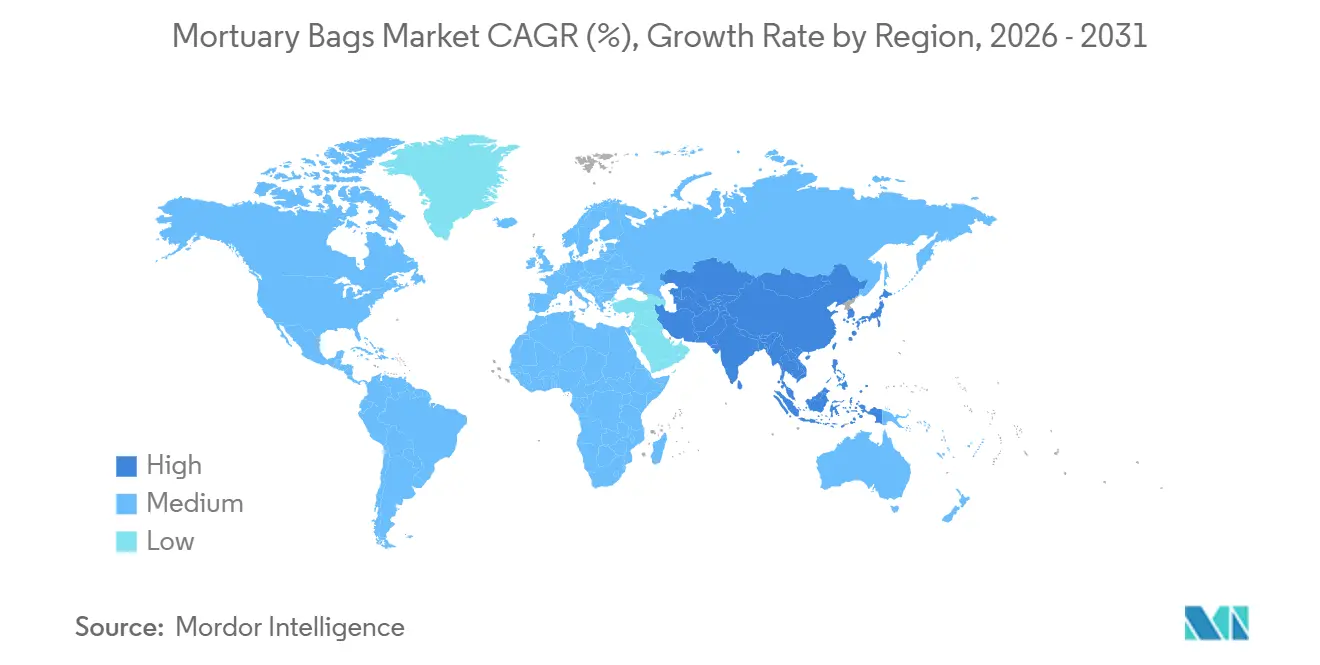

- By geography, North America retained 32.13% revenue share in 2025, yet Asia-Pacific is set to post the fastest 8.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mortuary Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Infectious-Disease Outbreaks | +1.8% | Sub-Saharan Africa, South Asia, global spill-over | Short term (≤ 2 years) |

| Global Aging Population and Higher Mortality | +2.1% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Stricter Biohazard Regulations on Corpse Handling | +1.5% | North America, Europe, Australia | Medium term (2-4 years) |

| Adoption of RFID-Enabled Traceability Solutions | +0.6% | North America, Europe, select Asia-Pacific hubs | Medium term (2-4 years) |

| Demand for Eco-Friendly Biodegradable Body Bags | +1.0% | Europe, North America, Australia | Long term (≥ 4 years) |

| Hospital Supply-Chain Digitization and Predictive Stockpiling | +0.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Infectious-Disease Outbreaks

Regional Ebola and Marburg flare-ups reinforce the need for leak-proof, double-bag solutions that meet ISO 16604's blood-penetration resistance[3]World Health Organization, “Disease Commodity Packages,” who.int. The Centers for Disease Control and Prevention’s 2024 guidance mandates dual containment layers and explicit biohazard labeling, instantly lifting per-case bag consumption. Procurement teams in Sub-Saharan Africa now pre-stage bags near outbreak hotspots, causing sharp, short-term volume spikes that ripple through global supply chains. Manufacturers able to certify rapid lead times and compliant seals are first in line for emergency contracts, underpinning a noticeable upswing in the mortuary bags market. The premium placed on compliant materials cements near-term pricing power for suppliers with scale.

Global Aging Population and Higher Mortality

United Nations projections put worldwide deaths at 61 million in 2025 and 82 million in 2050, a surge driven by greying demographics and higher chronic-disease prevalence. North America and Europe expect one in four citizens to be 65 years or older by 2030, which will inflate baseline demand for body-handling disposables. Funeral homes and hospitals have responded by signing multi-year framework agreements with price-escalation clauses, locking in guaranteed volumes that stabilize the mortuary bags market. Increased obesity among seniors feeds directly into bariatric sizes, merging demographic and product-mix shifts. Over the forecast horizon, steady mortality escalation provides a durable underpinning for manufacturers’ capacity-expansion decisions.

Stricter Biohazard Regulations on Corpse Handling

The European Union’s 2024 amendment to Directive 2000/54/EC requires leak-proof, color-coded bags for any suspected infectious case, complete with traceability documentation. OSHA’s Bloodborne Pathogens Standard drives similar compliance across U.S. acute-care facilities, fostering rapid adoption of multilayer polyethylene options in place of legacy PVC designs. Australian authorities now stipulate reinforced handles for bariatric remains above 250 kg, expanding the addressable value per unit. Although local adoption schedules vary, procurement teams worldwide have begun rewriting technical specifications to align with those of early-mover jurisdictions. The mortuary bags market benefits from this harmonization, as broadening conformity demands nudge buyers toward premium, certified models.

Adoption of RFID-Enabled Traceability Solutions

Barcode and RFID seals embedded in bag linings provide chain-of-custody visibility, a feature prized by high-throughput morgues and disaster teams. Integration with electronic health records in North America enables automated reconciliation of body inventory, shrinking administrative workloads, and reducing loss incidents. Unit-level tags, priced USD 0.50-2.00, increase per-piece cost but deliver clear value where litigation risk over misidentification is high. Makers offering end-to-end software connectivity gain an edge in multiyear tenders, especially those bundled with vendor-managed inventory. Progressive digitization continues to push the mortuary bags market toward data-rich consumables rather than commodity plastic sleeves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polymer Raw-Material Price Volatility | -0.9% | Import-dependent markets worldwide | Short term (≤ 2 years) |

| Environmental Regulations on Plastic Disposal | -0.6% | Europe, North America, Australia | Medium term (2-4 years) |

| Rising Popularity of Direct Cremation Services | -0.7% | North America, Europe, parts of Asia-Pacific | Long term (≥ 4 years) |

| Specialty-Zipper Supply-Chain Congestion | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Polymer Raw-Material Price Volatility

Spot polyethylene prices correlate closely with crude benchmarks, whipsawing input costs for manufacturers without hedging coverage. Currency depreciation compounds pain in Latin America and South Asia, where resin imports dominate supply. Buyers tied to annual contracts resist mid-term price pass-throughs, squeezing smaller fabricators and encouraging mergers. End-users begin specifying price-adjustment clauses pegged to resin indices, adding administrative complexity but preserving budget predictability. The uncertainty dampens near-term margin expectations across the mortuary bags market.

Environmental Regulations on Plastic Disposal

Extended producer-responsibility rules oblige manufacturers to fund collection and recycling networks, inflating compliance overhead in Europe and California. Export restrictions on non-recyclable waste curb offshoring of disposal liability, making landfill fees an unavoidable line item for plastic-heavy SKUs. Suppliers pivoting to compostable or mechanically recyclable blends shoulder R&D expense and third-party certification costs. Healthcare buyers scrutinize total ownership cost, favoring vendors that offer take-back schemes or certified degradable options. These factors temper growth for conventional polyethylene in favor of greener but pricier alternatives within the mortuary bags market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Biodegradable Polymers Challenge Polyethylene Dominance

Polyethylene accounted for 32.55% of the mortuary bags market in 2025 due to its balance of cost, tear resistance, and compatibility with heat seals. The mortuary bags market for biodegradable and compostable polymers, however, is projected to expand at a 9.25% CAGR to 2031 as extended producer responsibility fees and PFAS bans reset purchasing criteria. European and Australian health agencies already include EN 13432 compliance in tender documents, a stipulation that favors starch-based and PLA blends that degrade within 6 months. Suppliers tout reinforced multilayer films and vacuum-lock designs to match polyethylene’s fluid retention while reducing landfill waste. PVC maintains a foothold in price-sensitive African and South Asian contracts, yet tightening incineration rules in OECD economies erode its outlook. Early adopters of biodegradable lines exploit premium pricing and lower disposal tariffs, bolstering margin mix across the mortuary bags industry.

Polyester and nylon niche applications persist in military and forensic labs where abrasion resistance and infrared signature masking matter. For these users, procurement specifications prioritize tensile strength above environmental attributes, keeping high-performance synthetics in play despite elevated unit costs. Market leaders invest in blending lines that can toggle between conventional and bio-based resins, mitigating demand swings. The shift away from legacy plastic does not eliminate polyethylene overnight; instead, a dual-track trajectory is unfolding, with sustainable materials cannibalizing growth on new contracts while commodity grades service legacy agreements. Flexibility in resin sourcing, therefore, emerges as a strategic differentiator in the mortuary bags market.

By Size: Bariatric Segment Grows Amid Obesity Trends

The mortuary bags market size for adult variants accounted for 46.53% of revenue share in 2025, while the bariatric segment is forecast to post an 8.85% CAGR through 2031. Rising obesity among seniors, particularly in the United States and Germany, necessitates pouches rated for static loads above 300 lb. Updated Australian guidelines mandate six-handle configurations and reinforced seams, lifting average selling prices. Manufacturers respond with high-density polyethylene films and double-stitched web handles that evenly distribute weight. Pediatric and infant ranges occupy a smaller volume but sustain demand through standardized hospital protocols that now call for softer, tinted materials to reduce visual trauma for grieving families.

Bariatric adoption aligns with broader investments in mechanical lifting aids and larger refrigeration racks, creating complementary pull for heavy-duty bags. Catalogs such as Fisher Scientific added 40+ SKUs in 2025 tailored to patients weighing over 136 kg, indicating commercial momentum. Latin American health systems, where obesity rates are climbing quickly, begin issuing central tenders for bariatric supplies, echoing earlier moves in the United States. Suppliers that can demonstrate compliance with both load-bearing and leak-proof standards gain premium positioning. Consequently, the bariatric niche, though numerically smaller, generates outsized revenue growth within the mortuary bags market.

By Weight Duty: Heavy-Duty Variants Gain Traction in Disaster Response

Standard-duty products formed 39.23% of the mortuary bags market in 2025, well-suited for routine hospital transfers lasting under 48 hours. The mortuary bags market share for heavy-duty designs is expanding swiftly at an 8.55% CAGR, driven by disaster planners who demand 6-mil to 10-mil films that withstand refrigeration trailers and rough-terrain transport. FEMA’s portable morgue program specifies pouches capable of enduring direct-contact liquid cooling and stacked storage without seam failure, a requirement now mirrored by Japan’s Cabinet Office. Heavy-duty bags often feature RF-sealed closures and laminate reinforcements, raising unit costs but securing multi-year framework contracts.

Medium-duty options remain attractive for trauma centers that need more puncture resistance than standard variants but cannot absorb heavy-duty pricing. However, once facilities experience major casualty events, procurement usually shifts to top-tier specifications, permanently elevating their baseline. Suppliers with agile production lines that can scale thickness and reinforcement on demand are best placed to capture share. The expanding spectrum of duty ratings underscores the mortuary bags market’s maturation from one-size-fits-all commoditization to differentiated, application-specific portfolios.

By End-User: Disaster Relief and Military Applications Accelerate

Hospitals accounted for 45.63% of the mortuary bags market revenue in 2025, benefiting from predictable day-to-day turnover and centralized purchasing. Yet the military and disaster-relief channel is the fastest riser, clocking a 7.85% CAGR on the back of climate-driven catastrophes and geopolitical instability. U.S. Army regulations now require dual, RFID-tagged heavy-duty pouches for every battlefield fatality, embedding technology differentiation into procurement. FEMA’s Disaster Mortuary Operational Response Teams specify shelf-stable kits with 24-month service lives, incentivizing inventory rotation and recurring orders.

Funeral homes remain a robust secondary buyer group, albeit with margin pressure from direct cremation. Many offset volume declines by upgrading to aesthetic opaque colors and discrete labeling, features that fetch higher prices. Research and academic anatomy labs pursue biodegradable alternatives to align with campus sustainability pledges, carving out a green micro-segment. Across these end-user categories, tailored specifications steadily replace commoditized purchasing, undergirding value growth in the mortuary bags market.

Geography Analysis

North America accounted for 32.13% of the mortuary bags market in 2025, driven by OSHA and FDA guidelines that codify leak-proof, labeled containment. U.S. annual deaths are expected to rise, reinforcing dependable domestic demand. Canada’s cremation preference reduces embalming time yet still necessitates secure transport bags across vast geographic distances. Mexico’s public hospitals adopt pan-American biohazard benchmarks, upgrading morgue infrastructure and catalyzing new tenders.

Asia-Pacific is the fastest-growing region, with an 8.51% CAGR through 2031, driven by aging populations in China, Japan, and South Korea, and by healthcare capacity expansion in India and Southeast Asia. Provincial health bureaus in China receive earmarked funds for county-level funeral upgrades, prompting trials of biodegradable bags to curb incineration pollution. India’s life-expectancy gains translate into a larger elderly cohort, prompting private hospital chains to integrate mortuary planning into new-build projects. Australian states remain early adopters of bariatric guidelines and compostable materials, serving as test beds for premium specifications.

Europe maintains stable mid-single-digit growth as PFAS bans and waste-shipment rules reward suppliers with compliant, recyclable products. Scandinavian nations, where green procurement dominates, issue centralized biodegradable bag frameworks, whereas Southern Europe still relies on conventional polyethylene due to budget limits. The Middle East migrates toward heavy-duty pouches for mass-gathering events such as the Hajj, while Gulf Cooperation Council countries import refrigerated trailers with matching bag kits. South America’s demand concentrates in Brazil and Argentina, where urban hospital consolidation enhances purchasing power and standardization.

Competitive Landscape

The mortuary bags market remains moderately fragmented, with regional distributors dominating last-mile delivery. Yet, a cadre of specialized manufacturers, such as Mopec, HYGECO, Classic Plastics Corporation, controls advanced product lines. Mopec leverages scientific-supply portals to offer body-handling SKUs, underscoring breadth as a defensive moat. Competitors differentiate along three axes: sustainable materials, RFID traceability, and breadth of duty ratings. Adventpac channels first-mover advantage in compostable designs, capturing municipal contracts in Germany and Western Australia. HYGECO pairs pouches with turnkey morgue cabinetry in bundled deals, raising switching costs for new entrants.

RFID integration differentiates premium lines; proprietary seal tags interfacing with hospital ERPs create data lock-in and higher renewal rates. Heavy-duty innovations, such as Mopec’s MERC cooling system, require compatible, fluid-resistant pouches, thereby driving cross-selling opportunities. Raw-material hedging and multi-plant footprints help larger players weather resin volatility that threatens smaller firms. Nevertheless, niche opportunities persist: pediatric-specific designs, camouflage coatings for military use, and bariatric load ratings above 250 kg allow agile newcomers to claim premium niches without confronting scale head-on. Overall, innovation cadence and compliance agility outweigh price competition, supporting healthy margins across the mortuary bags market.

Mortuary Bags Industry Leaders

HYGECO

Mopec Inc.

Classic Plastics Corporation

Peerless Plastics

CEABIS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Crescent Capital Group provided specialty credit financing to refinance Protect Medical Holding GmbH, whose 4,500-item portfolio includes mortuary equipment and transport systems.

- June 2024: New South Wales Health issued updated bariatric-handling guidelines mandating body bags rated at 250 kg or more, with six reinforced handles, to mitigate tear risk.

Global Mortuary Bags Market Report Scope

As per the report's scope, mortuary bags, also known as body bags, are specialized containment bags used for the safe handling, storage, and transportation of deceased bodies. They are designed to prevent leakage, contain biohazards, and maintain dignity during post-mortem handling. Mortuary bags are commonly used in hospitals, mortuaries, forensic departments, disaster response, and funeral services.

Mortuary bag market segmentation includes raw material, size, weight duty, end-user, and geography. By raw material, the market is segmented into polyethylene, polyvinyl chloride (PVC), nylon, polyester, biodegradable/compostable polymers, and others. By size, the market is segmented into adult, bariatric, and child & infant. By weight duty, the market is segmented into standard duty, medium duty, and heavy duty. By end-user, the market is segmented into hospitals, mortuaries & funeral homes, disaster relief & military, research & anatomy labs, and others. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Polyethylene |

| Polyvinyl Chloride (PVC) |

| Nylon |

| Polyester |

| Biodegradable/Compostable Polymers |

| Others |

| Adult |

| Bariatric |

| Child & Infant |

| Standard Duty |

| Medium Duty |

| Heavy Duty |

| Hospitals |

| Mortuaries & Funeral Homes |

| Disaster Relief & Military |

| Research & Anatomy Labs |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Raw Material | Polyethylene | |

| Polyvinyl Chloride (PVC) | ||

| Nylon | ||

| Polyester | ||

| Biodegradable/Compostable Polymers | ||

| Others | ||

| By Size | Adult | |

| Bariatric | ||

| Child & Infant | ||

| By Weight Duty | Standard Duty | |

| Medium Duty | ||

| Heavy Duty | ||

| By End-User | Hospitals | |

| Mortuaries & Funeral Homes | ||

| Disaster Relief & Military | ||

| Research & Anatomy Labs | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the mortuary bags market expected to grow between 2026 and 2031?

The sector is projected to expand at a 7.31% CAGR, climbing from USD 1.89 billion in 2026 to USD 2.69 billion by 2031.

Which material currently dominates demand for mortuary bags?

Polyethylene remains the leading raw material with 32.55% share in 2025, although biodegradable polymers are the fastest-growing alternative.

Why are heavy-duty mortuary bags gaining popularity?

Disaster-preparedness programs and military field requirements call for reinforced 6-mil to 10-mil pouches that resist leaks during refrigerated storage and rough handling.

Which region offers the strongest growth opportunity for suppliers?

Asia-Pacific is forecast to record the highest 8.51% CAGR through 2031, driven by rapid population aging and expanding hospital infrastructure.

What technological features are hospitals requesting in new-generation body bags?

RFID or barcode traceability, leak-proof multilayer films, and formats compatible with automated inventory systems rank highest on procurement wish lists.

How are environmental regulations influencing purchasing decisions?

EU PFAS bans and extended producer-responsibility fees are steering buyers toward EN 13432-certified biodegradable bags despite higher unit costs.

Page last updated on: