Specimen Retrieval Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

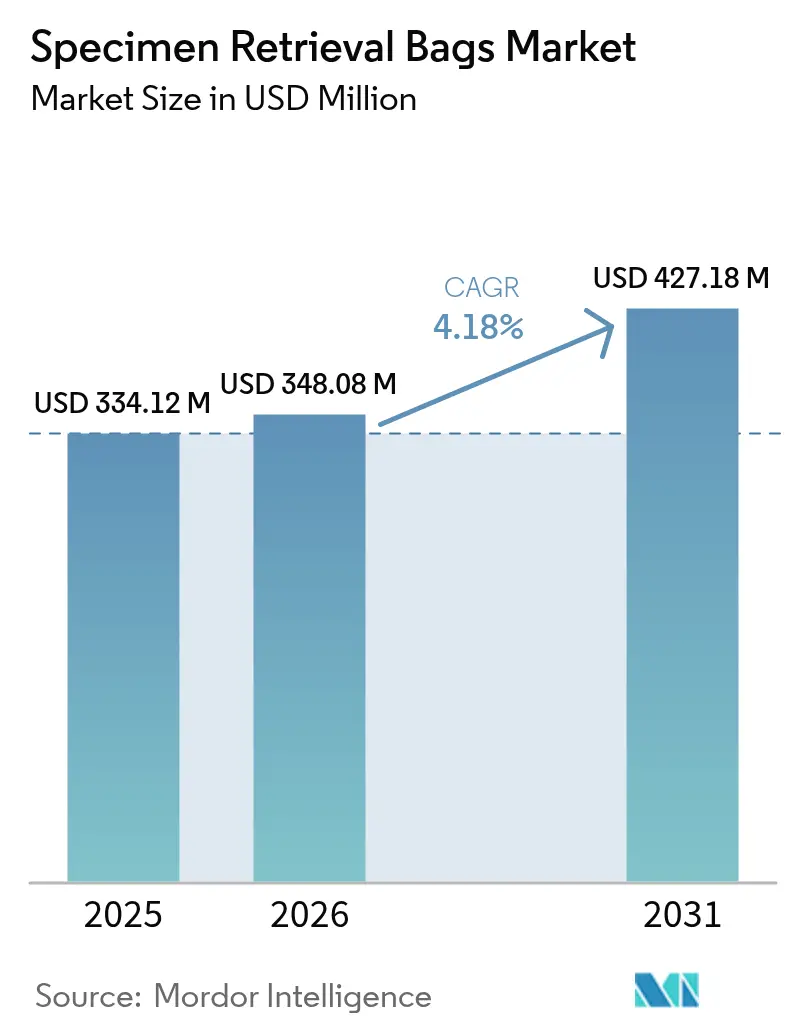

| Market Size (2026) | USD 348.08 Million |

| Market Size (2031) | USD 427.18 Million |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

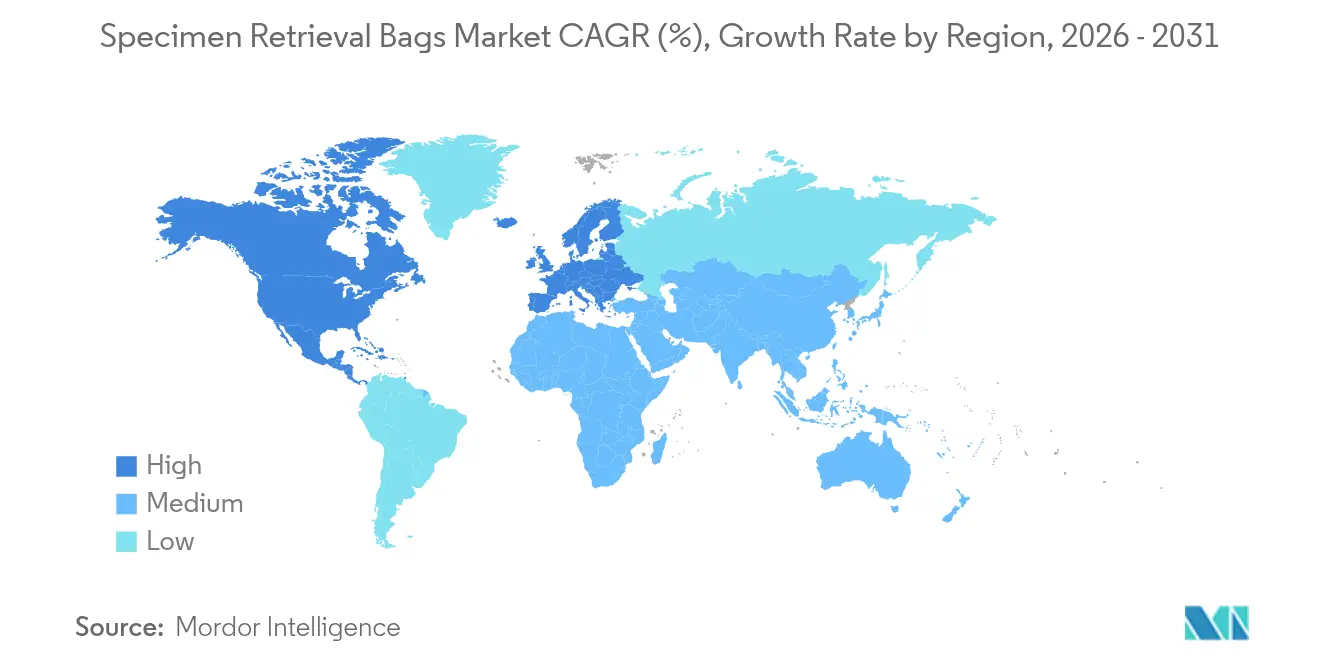

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

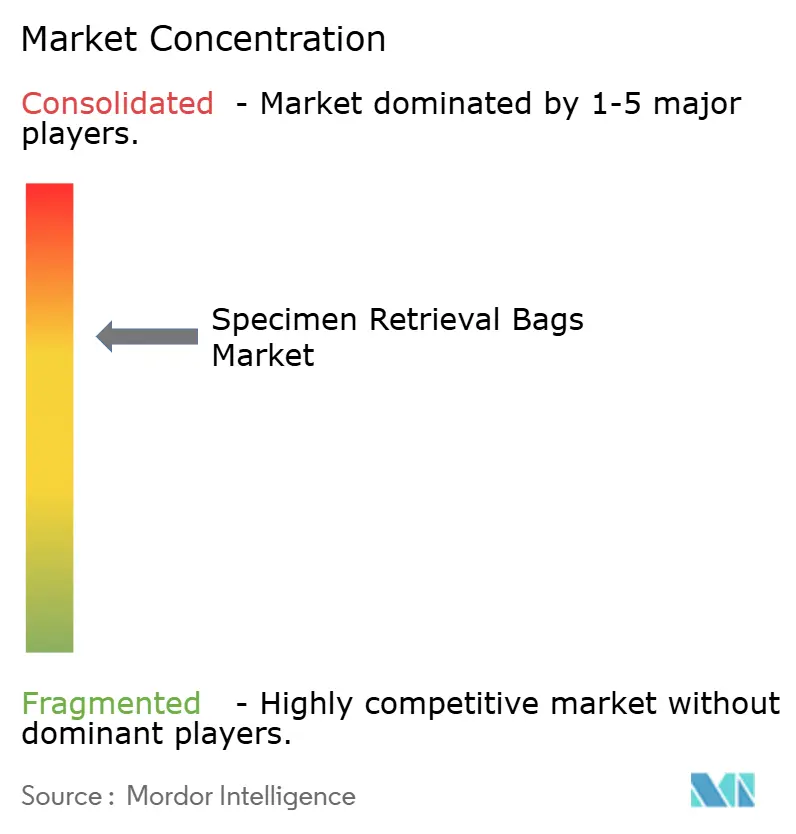

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specimen Retrieval Bags Market Analysis by Mordor Intelligence

Specimen retrieval bags market size in 2026 is estimated at USD 348.08 million, growing from 2025 value of USD 334.12 million with 2031 projections showing USD 427.18 million, growing at 4.18% CAGR over 2026-2031. Growth reflects a mature yet resilient arena where reimbursement policies, oncology-focused containment guidelines, and the outpatient surgery boom combine to expand the addressable base of minimally invasive procedures. Rising chronic-disease burdens, notable technology refresh cycles in laparoscopic instrumentation, and an accelerating shift toward ambulatory settings keep demand steady even as value-based care heightens scrutiny of premium device pricing. Asia-Pacific achieves the fastest regional pace at 6.13% CAGR, while North America captures 42.75% revenue share on the strength of entrenched reimbursement and early adoption of post-2024 morcellation standards. Non-detachable retrieval bags hold 65.35% share, underlining surgeon trust in proven simplicity even as detachable formats register 5.23% CAGR. Competitive intensity remains moderate: large incumbents defend positions with global distribution, robust regulatory dossiers, and incremental product upgrades.

Key Report Takeaways

- By product type, non-detachable systems led with 64.78% of the specimen retrieval bags market share in 2025, while detachable formats are projected to expand at a 5.01% CAGR through 2031.

- By application, gastrointestinal surgery accounted for 47.10% of the specimen retrieval bags market size in 2025 and gynecological procedures are advancing at a 5.55% CAGR through 2031.

- By end user, hospitals held 68.72% revenue share in 2025; ambulatory surgery centers log the highest projected CAGR at 5.18% for 2026-2031.

- By region, Asia-Pacific commands the fastest 5.89% CAGR, yet North America retains dominance with 42.30% of 2025 revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Specimen Retrieval Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally-invasive surgery | +1.2% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Increasing global surgical volumes from chronic diseases | +0.8% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Rapid upgrade cycle in laparoscopic instrumentation | +0.6% | North America & Europe primarily | Short term (≤ 2 years) |

| Adoption surge in emerging ambulatory surgery centers | +0.9% | North America, expanding to APAC | Medium term (2-4 years) |

| "In-bag" morcellation standards post-2024 oncology guidelines | +0.7% | Global, FDA-influenced markets first | Short term (≤ 2 years) |

| Circular-economy push for recyclable polymer retrieval bags | +0.3% | Europe leading, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally-Invasive Surgery

Ambulatory surgery centers (ASCs) expect 21% procedure growth by 2034, directly elevating demand for reliable retrieval bags that fit shortened case times [1]ASC Focus Editorial Board, “2024 Impact of Change Report,” ascfocus.org. Medicare raised ASC reimbursement 3.8% in 2025, widening the economic runway for laparoscopic cases despite rising supply-chain costs. Robotic workflows gain share but currently lengthen operating times in complex cases, highlighting the need for extraction devices that balance innovation with throughput. Manufacturers responding with pre-loaded, self-opening pouches emphasize ease of deployment to satisfy efficiency metrics that dominate ASC purchasing. Europe follows a similar arc, but heightened circular-economy mandates spur interest in polymer blends that enable recycling without compromising barrier integrity.

Increasing Global Surgical Volumes from Chronic Diseases

The World Bank identifies 4,433 procedures per 100,000 people in Brazil for 2024, reflecting higher case volumes tied to diabetes, cancer, and cardiovascular disease [2]Ulises G. Pacheco, “Surgical System Assessment in Brazil,” BMJ Global Health, bmj.com. Yet postoperative mortality in Sub-Saharan Africa remains twice the global average, underscoring infrastructure gaps that dampen high-value device uptake. Advanced economies now tailor retrieval features—including smoke evacuation-ready seals and reinforced seams—to support extensive oncologic resections, while low- and middle-income nations prioritize affordability and straightforward usability. These diverging clinical realities create tiered product strategies, prompting manufacturers to keep legacy nylon bags in portfolios alongside premium polyurethane designs offering improved puncture resistance.

Rapid Upgrade Cycle in Laparoscopic Instrumentation

Next-generation articulated instruments such as ArtiSential® trim operative time by 40 minutes in select complex cases, a benefit that encourages surgeons to refresh platforms earlier than standard depreciation cycles [3]Yong K. Song, “Articulated Instruments Shorten Complex Laparoscopic Procedures,” BMC Surgery, biomedcentral.com. Hospitals adopting such tools often bundle retrieval systems during capital refresh, giving integrated vendors a channel advantage. However, budget committees increasingly demand proof of net procedure savings; cost-utility studies show robotic prostatectomy achieves lower total episode cost after factoring shorter length of stay despite higher disposables. Consequently, retrieval bag suppliers highlight compatibility with both laparoscopic and robotic ports to remain on standardized preference lists.

Adoption Surge in Emerging Ambulatory Surgery Centers

More than 70% of US ASCs remain independent, preserving decentralized procurement that favors nimble device suppliers. Gastroenterology and ophthalmology dominate early ASC case mix, but recent additions of gynecological and bariatric programs enlarge the specimen retrieval bags market baseline. Independent centers require compact packaging and simplified deployment to minimize set-up times in lean staffing models. Meanwhile, payors integrate ASC site-neutral payments for certain procedures starting 2025, accelerating inpatient-to-outpatient migration. Manufacturers catering to these trends incorporate color-coded cinch cords and low-profile rings to streamline extraction through 12 mm ports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit cost of proprietary retrieval systems | -0.6% | Global, acute in price-sensitive markets | Medium term (2-4 years) |

| Evidence questioning clinical benefit versus glove/direct extraction | -0.4% | North America & Europe primarily | Short term (≤ 2 years) |

| Low penetration of advanced MIS in low-income countries | -0.3% | Sub-Saharan Africa, parts of Asia | Long term (≥ 4 years) |

| Skills gap for robotic-assisted specimen extraction | -0.2% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Unit Cost of Proprietary Retrieval Systems

A 2024 comparative study on laparoscopic sleeve gastrectomy found no statistical difference in complication rates between branded bags and direct extraction, intensifying price pressure on specialized devices. Latin American health ministries echo this concern, imposing reference-pricing caps that compress distributor margins. In response, global suppliers introduce value segments featuring thinner film gauges and simplified closure toggles while preserving sterile barrier performance. Asia-Pacific hospitals negotiate multiyear tenders that bundle retrieval pouches with trocars, exploiting economies of scale to trim per-unit cost. Such strategies partially offset the restraint but reinforce the need for demonstrable outcome advantages.

Evidence Questioning Clinical Benefit Versus Glove/Direct Extraction

Randomized trials on contained morcellation highlight intact bag integrity but fail to show significant reduction in specimen spillage compared with glove retrieval in low-risk myomectomy, challenging automatic bag use. Value-based purchasing committees therefore require granular data on infection reduction or wall injury prevention. Manufacturers now sponsor multicenter registries targeting 10,000-case enrollment to capture statistically solid endpoints, yet results remain pending. Until then, surgeons increasingly reserve premium systems for oncology or obese patients, trimming overall volume growth. Device makers counter with training modules underlining ergonomic benefits such as reduced fascial stress, seeking to reframe the discussion around workflow rather than pure safety.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Non-Detachable Systems Dominate Despite Innovation Push

Non-detachable bags controlled 64.78% 2025 revenue, anchoring the specimen retrieval bags market through reliability that resonates in high-throughput settings. The segment benefits from simple drawstring closure that minimizes failure modes, a feature especially valuable when adopting single-site laparoscopy where articulation space is scarce. Hospitals report fewer pouch-loading errors with pre-attached rigid rings, supporting faster turnovers. Detachable formats, despite only 35.22% share, post 5.01% CAGR as surgeons appreciate staged extraction that reduces intra-abdominal manipulations. The specimen retrieval bags market size for detachable systems is estimated at USD 123.42 million in 2026 and is projected to reach USD 157.68 million by 2031, reflecting targeted gains in bariatric and gynecologic procedures. Applied Medical’s Inzii® line integrates guide beads that reopen the mouth once outside the cavity, illustrating incremental advances addressing earlier usability concerns. Meanwhile, hybrid pouches featuring peripheral reinforcement and optional detachment emerge, catering to orthopedic sports-medicine arthroscopy. Manufacturers must balance inventory breadth with cost efficiency, often offering modular handle-bag combinations built on a shared introducer platform. The specimen retrieval industry continues to monitor polymer innovation, with cyclic-olefin co-polymer blends promising higher clarity for intra-operative visualization though currently at premium price points. Surgeons remain wary of latch failures on magnetic closure systems, suggesting non-detachable pouches will sustain majority share until robust field data confirm alternative reliability.

By Application: Gastrointestinal Procedures Lead, Gynecological Growth Accelerates

Gastrointestinal surgery captured 47.10% of 2025 revenue as cholecystectomy, appendectomy, and colon resections routinely demand safe removal of inflamed or malignant tissue. Hospitals standardize retrieval bag use in these cases to mitigate bile spillage and peritoneal contamination, sustaining base volume. The specimen retrieval bags market size for gastrointestinal procedures is forecast to grow from USD 163.95 million in 2026 to USD 195.72 million by 2031 at 3.61% CAGR as staple adoption is already high. Conversely, gynecology drives incremental momentum with 5.55% CAGR, spurred by FDA-driven contained morcellation mandates effective January 2024. This regulation pushes universal bag deployment in myomectomy and hysterectomy, enlarging the addressable pool by nearly 1.2 million annual US cases. Oncology centers likewise embrace thicker-gauge pouches for specimen isolation during transvaginal extraction, an area previously served by improvised glove techniques. Urology remains a steady contributor on the back of nephrectomy and prostatectomy, though adoption lags due to anatomical constraints that sometimes favor in-bag morcellation over whole-organ extraction. Other surgeries such as thoracic wedge resections and bariatric sleeve gastrectomies together provide ancillary demand, particularly in high-BMI populations where contaminated fluid must be contained to reduce port-site hernia risk. Industry product roadmaps now include extended-length sleeve designs catering to trans-anal extraction in colorectal surgery, evidence of application-specific tailoring.

By End User: Hospitals Maintain Dominance as ASCs Gain Momentum

Hospitals retained 68.72% of 2025 shipments owing to case complexity and established bulk-buying agreements that integrate retrieval pouches within laparoscopic kit packs. These facilities regularly handle oncologic resections where margin integrity is crucial, supporting sustained preference for multi-layer films with validated sterility over 180-day shelf lives. The specimen retrieval bags market share held by hospitals is projected to taper slightly to 65.30% by 2031 as ambulatory settings accelerate. ASCs, logging 5.18% CAGR, benefit from payer support for outpatient site-of-service shifts, including expanded reimbursement for hysterectomy and colectomy. Centers of excellence within orthopedics and bariatrics pilot single-use mini-bags featuring self-inflating collars, allowing extraction through 8 mm ports and reducing fascial dilation. Physician-owned specialty clinics, especially in endoscopy, represent an emerging micro-segment that values compact sterilizable introducers to minimize waste. As provider consolidation progresses, group purchasing organizations negotiate dual-source contracts that stipulate both premium and economy lines, forcing manufacturers to cultivate agile manufacturing capable of mixed-model production.

Geography Analysis

North America captured 42.30% of global revenue in 2025 as robust reimbursement and early compliance with oncology containment guidance ensure high device utilization. Widespread adoption of da Vinci platform upgrades in 2025 also boosts trocar-compatible pouch demand across urology and general surgery. Yet payers invoke bundled DRG reviews to curb disposable expenditure, encouraging value offerings and prompting suppliers to introduce tiered lines in mid-2025.

Asia-Pacific leads growth at 5.89% CAGR thanks to rising healthcare investment, aging demographics, and rapid diffusion of laparoscopic skills into secondary-tier cities. China’s NMPA approval of Boston Scientific’s FARAPULSE™ in 2025 signals regulatory openness to advanced systems, encouraging parallel acceptance of complementary retrieval solutions. Japan and Australia favor premium pouches with anti-slip perimeters, while India, Indonesia, and Vietnam lean on cost-efficient nylon bags that satisfy basic leakage requirements. Europe posts moderate expansion as procurement directives emphasize circular-economy goals; hospitals in Germany and the Nordics pilot take-back schemes where used pouches are converted into industrial feedstock. The Middle East invests in large robotic surgery centers in the Gulf, translating into demand for high-capacity bags capable of removing enlarged thyroid or kidney specimens through small fascial openings. Africa remains constrained by workforce shortages and postoperative mortality challenges, though teaching hospitals in South Africa and Nigeria adopt retrieval systems for donor-derived transplant programs. Latin America, led by Brazil and Mexico, shows mixed adoption as tax incentives on locally manufactured pouches coexist with foreign-branded premium offerings in private networks.

Regulatory Landscape

In the United States, specimen retrieval bags are commonly regulated as Class II devices under FDA product code GCJ and 21 CFR 876.1500, which typically requires a 510(k) premarket notification demonstrating substantial equivalence to a predicate. Recent clearances in this device category include Ximedica's ENDOCOLLECT Specimen Retrieval Bag (K240635, April 2024) and Dannik LLC's DANNIK Laparoscopic Single-Use Poly Specimen Retrieval System (K250411, February 2025), indicating continued regulatory activity and iterative design updates within the established pathway.

In Europe, market access is governed by the Medical Device Regulation (EU) 2017/745 (MDR), where classification and conformity assessment are determined by intended use and invasiveness using the Annex VIII ruleset, supported by European Commission and MDCG guidance documents on classification and borderline decisions. Under the MDR framework, technical documentation, clinical evaluation planning, and post-market obligations take on added weight, which can shape product lifecycle management and the timing of material or design changes for retrieval pouches sold across EU member states.

Value Chain Analysis

The value chain starts with raw material suppliers providing medical-grade polymer films (often TPU-based) and components for introducers and support rings (commonly ABS plastics and stainless steel). These inputs then move to OEMs and contract manufacturers for film conversion, assembly, packaging, and sterilization coordination, followed by quality release under regulated manufacturing systems and documentation. In FDA-influenced markets, the chain is shaped by Class II 510(k) requirements and quality-system expectations, with labeling, packaging integrity, and traceability (including UDI practices where applicable) embedded as products move downstream.

Distribution is led by direct sales to integrated delivery networks and hospital systems, alongside channel partners such as wholesalers and group purchasing organizations that standardize items into laparoscopic kits and procedure packs. Manufacturers with broader surgical portfolios (for example, Medtronic and Ethicon under Johnson and Johnson) use bundling with access instrumentation to support formulary placement, while mid-tier suppliers compete through differentiated deployment mechanics and material strength. Operationally, resilience depends on reliable sourcing of specialized biocompatible films and validated sterilization capacity, and supply-chain risk management has become a formal procurement consideration in many health systems.

Competitive Landscape

Competitive intensity is moderate. Johnson & Johnson’s Ethicon brand leverages proprietary polymer science delivering 9.8 lbs abdominal wall retention force while keeping leak rates at 0.2%, positioning it as a premium benchmark. Medtronic expands its Solutions Group portfolio around mini-laparoscopic access kits bundled with retrieval pouches, bundling incentives that lock in hospital-wide contracts. Teleflex capitalizes on broad distribution, adding quick-deploy spring-ring technology after acquiring a vascular intervention unit in 2024, illustrating adjacency-driven capability expansion. Mid-tier players such as CONMED and Applied Medical differentiate through niche innovations like self-righting mouth orientation and bead-guided detachability that streamline specimen clearance.

Patent filings in 2025 showcase inflatable retractors integrated with containment bags designed for single-incision cholecystectomy, underscoring incremental rather than radical innovation. Start-ups emerging from academic incubators explore smart polymers that shift color upon puncture to alert surgeons to micro-tears, though commercial viability depends on cost absorption within DRG payment ceilings.

Strategic collaborations prevail over standalone R&D; Stryker’s 2025 alliance with Intuitive Surgical to pilot data-enabled retrieval forceps exemplifies cross-platform interoperability moves. Competitive rhetoric increasingly emphasizes environmental metrics, with Olympus committing to 30% recycled content in its next pouch generation, a stance resonating with EU procurement guidelines that weight sustainability in tender scoring.

Specimen Retrieval Bags Industry Leaders

Medtronic PLC

Teleflex Incorporated

Applied Medical Resources Corporation

B. Braun SE

Johnson & Johnson Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An opportunity is emerging at the intersection of containment rigor and workflow efficiency in minimally invasive oncology and gynecology, where the post-2024 emphasis on contained tissue handling has raised expectations for puncture resistance, seal integrity, and visualization. FDA clearance activity for multiple single-use systems, including K240635 in April 2024 and K250411 in February 2025 under product code GCJ, shows product iteration remains feasible within the existing Class II pathway, supporting differentiated designs such as reinforced films, low-profile introducers, and port-size-optimized options.

Technology-led opportunity is also visible in research and IP focused on more controllable specimen handling in constrained incisions. In February 2026, researchers reported RoboRetrieve, a hand-held robotic concept validated in laparoscopic simulator trials for spillage-reduced retrieval, and a March 2026 patent publication described a retrieval apparatus with integrated lifting bands to manipulate tissue position inside the bag during extraction. With procedure migration to ambulatory settings, suppliers have room to develop robot-compatible, ergonomics-forward systems and standardized protocols for containment use cases that currently show variable practice patterns.

Recent Industry Developments

- February 2026: Researchers reported RoboRetrieve, a hand-held robotic system concept for specimen retrieval that was validated in laparoscopic simulator trials. The work highlights active R&D toward more controllable, spillage-reduced extraction tools that complement laparoscopic and robotic workflows. It also signals a pathway for suppliers to differentiate beyond film strength by integrating assistive mechanics and interface design.

- September 2025: Surgical Principals, Inc. received FDA 510(k) clearance (K251743) for the SPI LaproSac Laparoscopic Single-Use Rip-Stop Nylon Specimen Retrieval System under product code GCJ. The clearance adds another single-use, reinforced-material option to the competitive set, supporting procurement teams seeking durability-focused alternatives. It reinforces the role of 510(k) activity as a steady channel for new entrants and niche designs in this category.

- April 2024: Ximedica received FDA 510(k) clearance (K240635) for the ENDOCOLLECT Specimen Retrieval Bag in 8 mm, 12 mm, and 15 mm configurations under product code GCJ. Multi-size offerings expand fit across common port sizes, which is central to standardizing retrieval steps across service lines. The clearance illustrates continued product refinement oriented toward OR compatibility and streamlined deployment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from specimen retrieval bags used to contain and remove tissue or organs during minimally invasive procedures. The bags are typically passed through laparoscopic or robotic ports in sterile surgical settings.

Scope exclusions: The sizing excludes rigid morcellators, suction canisters, and pathology storage vials, even when they are sold to the same operating room buyers.

Segmentation Overview

- By Type

- Detachable Retrieval Bags

- Non-Detachable Retrieval Bags

- By Application

- Gastrointestinal Surgeries

- Urological Surgeries

- Gynecological Surgeries

- Other Surgeries (Thoracic, Bariatric, Oncology)

- By End User

- Hospitals

- Ambulatory Surgery Centers (ASCs)

- Specialty & Physician-Owned Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a practical demand map around minimally invasive surgery volumes and the typical use of retrieval bags per case, since most public data does not directly publish bag consumption. We reviewed public sources such as the US FDA device databases, CDC healthcare statistics, OECD health data, World Bank macro indicators, and customs trade statistics where they helped explain import and export movement for relevant medical device categories.

Next, we used company filings, investor presentations, and reputable medical society and hospital procurement information to understand product positioning (single use versus reusable), common pack formats, and pricing direction. A paid subscription for company financials and intelligence, and another for patent databases, were used selectively to validate which companies are active, and which product features are being commercialized. That cross-check supported adoption timing assumptions. These sources are not exhaustive, and many other public documents and datasets were also referenced during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with operating room procurement stakeholders, minimally invasive surgery clinicians, and regional distributors who see order patterns across hospitals and ambulatory surgical centers. Since this is a global market, inputs were validated across APAC, EMEA, and the Americas to confirm procedure mix, utilization per procedure, and realistic pricing ranges, then gaps from desk research were closed before finalizing assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | APAC: 42% |

| Mid tier: 51% | Functional/Unit leaders: 42% | EMEA: 34% |

| Smaller Players: 15% | Managers: 43% | Americas: 24% |

Market-Sizing & Forecasting

The model is built mainly through a top down approach, where procedure volumes and minimally invasive surgery penetration are used to reconstruct the addressable demand pool for retrieval bags, followed by an adjustment for usage patterns in hospitals versus ambulatory surgical centers. Results are then checked using selective bottom-up approximations, such as sampling typical bag usage per procedure, validating average selling price bands by region, and doing limited channel checks on how packs flow through distributors.

Key inputs that shape the numbers include laparoscopic and robotic surgery volumes, the share of cases where tissue extraction requires containment, typical bags used per case (including double bagging in certain procedures), the split between single use and reusable products, and regional price ladders tied to hospital purchasing behavior. When a country level input is missing, we use a proxy based on nearby procedure intensity and healthcare spend, and then stress test it through expert feedback so outliers are not carried into the total.

For forecasting, scenario analysis is applied around procedure growth and adoption behavior. A smoothing method is used for pricing so sudden jumps are avoided unless there is a clear signal. Forecast assumptions are confirmed through primary inputs on OR workflow preferences, regulatory and safety awareness, and expected changes in minimally invasive case mix over the next few years.

Data Validation & Update Cycle

Outputs are validated through triangulation across procedure indicators, trade and supply signals, and interview based pricing and utilization ranges. If a country or region shows a sharp variance from peers, the drivers are reviewed, assumptions are rechecked, and the relevant experts are recontacted so the change is properly explained.

Before sign-off, the model and narrative go through multi step analyst reviews, where calculations, unit consistency, and currency conversion timing are checked again. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or abrupt shifts in surgical volumes. Right before delivery, a final pass is done so clients receive the latest updated view available at that time.

Mordor Intelligence's Specimen Retrieval Bags Market Estimate Compared With Other Published Estimates

Published market sizes for specimen retrieval bags can look far apart because the counted product boundary and the year choices are not always aligned, and then pricing and procedure assumptions amplify the difference. We also see variation when one study mixes adjacent laparoscopic accessories into the total, or when the forecast horizon starts from a different recovery or utilization point.

By tracking procedure volume signals, price bands by region, and scope exclusions in one model, Mordor Intelligence keeps the estimate tied to retrieval bags used through laparoscopic or robotic ports rather than bundling in nearby device categories. In addition, currency timing and the refresh cadence can shift the reported value for the same year, especially when exchange rates move and ASPs are assumed to rise faster than what procurement teams confirm.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 348.08 M (2026) | |

| Global Market Publisher A | USD 320.00 M (2024) | Uses a different base year and growth window, and the scope detail is less explicit on excluding adjacent OR accessories, which can change what is counted and how pricing is projected. |

| Industry Publisher B | USD 316.00 M (2024) | Starts from an earlier year with a separate CAGR period and may apply broad average pricing, which can understate regional price ladders and the impact of procedure mix changes. |

The spread in the table is mostly explained by timing and scope discipline, since a 2024 starting point will not match a 2026 starting point even before method choices are considered. When the demand pool is anchored to minimally invasive procedure activity and then cross checked with realistic utilization and pricing ranges, the final number is easier to trace and repeat year after year.

Key Questions Answered in the Report

What is the current Specimen Retrieval Bags Market size?

The market is valued at USD 348.08 million in 2026, with a forecast value of USD 427.18 million by 2031.

Which region is growing fastest in the specimen retrieval bags market?

Asia-Pacific leads with a projected 5.89% CAGR through 2031, driven by rising surgical volumes and expanding healthcare infrastructure.

Which is the fastest growing region in Specimen Retrieval Bags Market?

Surgeons favor their proven simplicity and reliability, giving non-detachable bags 64.78% of 2025 revenue despite emerging detachable alternatives.

Which region has the biggest share in Specimen Retrieval Bags Market?

In 2025, the North America accounts for the largest market share in Specimen Retrieval Bags Market.

Page last updated on: